Hidden Data Economy in Financial Services - Oracle

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Hidden Data Economy in Financial Services February 2021

Introduction

Data has often been described as the “new oil” or the “new gold”. emergence and adoption of platform technologies for harvesting

As world economies digitise, it has indeed become an exchange data, and the shift to an open banking data world are key factors

of value that lies at the foundation of their transformation. Senior underpinning the importance of data.

data strategist for Oracle, Paul Sonderegger describes that data

has now evolved into its own form of capital and therefore goes Banks are challenged because their IT data infrastructure and

beyond those simple metaphors. applications are generally wired deterministically to address

well understood questions and specific use cases such as core

“Data fulfills the literal, economic textbook definition of capital,” banking, payments, risk & compliance, market trades, and

he says. “This is because capital is a produced good, not a natural mortgage banking. To bring this data together, and continue to

resource. You have to invest to create it, it is not like oil or gold create the capability that can generate new, competitive insights,

where it is simply extracted from the ground. banks have established large data lakes but in the majority of

cases they struggle to derive value from these and make them

Banks realise the crucial role that data plays in their businesses. productive. To a large degree the reason is because it is hard

When you consider that well over 80% of the world’s money is to establish relationships between various data sets. This

already digital, and that banks generate vast amounts of data requires either a new data model that maps these connections or

every day, it’s no wonder that the role of data has become crucial technology that helps identify and extract them automatically.

for the industry. The need to better compete for customers, the

Page 2 - Hidden Data Economy in Financial Services

To effectively use data as a capital, banks need to approach transparency and upholding data property rights declared in a

the data plan holistically, with the vision of an enterprise data patchwork of overlapping regulations worldwide.

platform that has the following characteristics:

In July 2020 ADAPT, an independent Australian research and

Data Liquidity, advisory firm conducted a targeted research on behalf of

Oracle, focusing on the state of data discovery, governance,

Data Productivity, and management, productivity and analytics within 25 leading ANZ

Data Security. organisations. Research revealed that while all aspects of ‘data

economy’ were a challenge, the highest focus was on data

Data liquidity is the ability to get data from its point of origin to productivity as well as data governance and security.

its many points of use efficiently. The essence of data liquidity is

reducing the time, cost and effort to repurpose data for This paper is looking at how these concepts apply to the

new uses. financial services industry, especially through the prism of

banks’ today’s challenges.

Data productivity is dollar output per data input. That is, when

you apply a given dataset in a particular action or decision point, According to the PwC report From shock absorber to

what is the incremental revenue generated or incremental cost springboard?1, which assessed the 2020 full year results of

avoided? the major banks, the three big priories for the sector include:

rebuilding trust, improving on cost and productivity, and driving

Data security must provide protection for both the observer and growth.

the observed over observations about them. The “datafication”

of nearly every activity in personal, commercial, and civic life Including considerations for data liquidity, data productivity,

rewrites the social contract between people, companies, and and data security into a data management plan will help banks

governments. As a result, keeping data secure means not address these three key priorities and manage data as the new,

just authorisation, access, encryption, and auditing, but also strategic asset that it has clearly become.

1

From shock absorber to springboard? - Banking Matters | Major Banks Analysis Full Year; November 2020, PwC

Page 3 - Hidden Data Economy in Financial Services

1

Chapter 1

One: Rebuilding Trust

3 Bank Priorities The health pandemic provided a valuable opportunity for banks to

rebuild trust with their customers. Banks were a key player in Team

Australia – a group made up of banks, the government and regulators

– to help customers better manage the challenges during COVID.

In fact, when the banks announced COVID support measures that

included loans deferred on 500,000 mortgages, and more than

200,000 in small business loans, {source: ABA}, Commonwealth Bank

CEO Matt Comyn recognised that the approach could help restore

trust in the community, particularly following the royal commission.

“We have to be judged by our actions and our words, and this is an

incredibly important time for the country,” he said at the time.

Page 4 - Hidden Data Economy in Financial Services

At the same time, remediation and compliance costs remain on the balance sheet despite the focus on conduct abating in light of the health pandemic. To date, banks have booked $3.71 billion in remediation costs, up 10 per cent compared to the previous year. The PwC report also identified that ‘notable charges’ are at best a useful metric that is providing a proxy to the degree of which banks are tackling historic conduct and compliance issues, especially the share related to remediation of customer harm and other improper conduct. Ensuring banks stay vigilant and focus on monitoring their processes and systems may help ease scrutiny on their conduct. Although the sector is now addressing its conduct issues, the PwC report notes that it will only take “just another incident such as anti-money laundering lapses to reignite the trust issue”. This will only mean high remediation costs for the banks. Therefore, it is crucial that banks keep their focus on monitoring processes and systems. Page - 5 - Hidden Data Economy in Financial Services

Two: Cost and Productivity

Despite the significant investment by the banks in cloud

and automation, total costs are still high, with cost growth

outpacing any productivity gains.

The 2020 full year results from the major banks highlighted

that costs remain a concern for the banks. Crunching the

numbers, PwC found that operating expenses (ex notables)

for the year were up 4 percent to $36.5 billion. Furthermore,

expense-to-income (excluding large notable items) stood at

45.1 per cent up 94 basis points compared to the previous

period.

For branches, banks’ need to reduce costs was compounded

by the accelerated adoption of digital banking during the

pandemic, therefore leading to more closures.

RFi Group data shows that the bulk of the market do not

require branches. However, the data shows that customers

still want the option of using a branch for products such as

home loans and banks are reticent to remove an important

brand presence that can help them to reinforce trust in the

communities they serve.

Therefore the decline in the usage of this channel only puts

pressure on customer engagement and acquisition. Ultimately

banks need to assess how they can balance cutting costs while

also investing for growth.

Page

Page 6 - Hidden Data Economy in Financial Services

Three: Restoring Growth from the Core The decision by the big banks to sell off their insurance and wealth businesses was underpinned by their strategy to be more customer focused. National Australia Bank has already finalised the sale of insurance and wealth manager MLC while the Commonwealth Bank also sold its 55 per cent stake in the wealth management business Colonial First State to a private equity firm only last year. The PwC report notes: “Today’s banks are in a position to be more focused on their core customers and mission than at any time since the 1990s. Given the track record of the past 15 years, that’s obviously an attractive proposition”. However, according to the PwC report this shift to focus on their core customers and mission will mean that “growth will be dependent on an increasingly narrow base”, that is “interest income, primarily from mortgage lending. The PwC report highlights that banks will therefore “have to rethink how they can extract better value for their customers from their core businesses: lending, deposit-taking and transaction support”. Page - 7 - Hidden Data Economy in Financial Services

2

Chapter 2

Banks already understand that data is an asset and understand that

it can now truly derive a competitive advantage for their customers,

How an enterprise-wide says Maximo Diez Blanco, Oracle’s global head of strategy for financial

services. “No bank needs to be convinced about that.”

data mangement Effective data management strategies will also be crucial to address the

approach helps banks priorities on trust, cost and productivity to achieve growth.

There are a number of practical solutions that Oracle has rolled out to

banks that has enabled them to apply data liquidity, data productivity

and data security to support them in these strategies.

Page 8 - Hidden Data Economy in Financial ServicesTrusting the Data

Trust is the foundation upon which the banking business is Reputation is also crucial in ensuring banks maintain trust.

built. According to the RFi Group research2, what goes to the There is no doubt that data breaches, lapses in AML compliance,

heart of a trusted institution is whether a bank is doing the and financial crime impact business reputation.

right thing by its customers. That is banks need to consistently

demonstrate that they have their customers’ interests at heart. However, banks are constantly challenged by a seemingly

never-ending flow of changes to regulations and reporting

Adopting the approach of doing what is right for the customer requirements. Compliance is critical as data breaches also have

would also increase share-of-wallet. The data shows that trust implications for consumer trust and confidence.

is the top driver of choice for primary transaction accounts,

followed by recommendations from friends, family members or Adopting an integrated enterprise-wide approach to data

colleagues. This has increased as a driver of choice compared management to tackle this massive challenge will be the key.

to accounts opened in prior years. According to Diez Blanco, by bringing together an integrated

view of financial, risk, and compliance data, and being able

RFi Group data also shows that when consumers are asked to model and project multiple business scenarios, banks can

about what trust means to them, it encapsulates transparency, anticipate and adapt to change, making them more resilient.

honesty, acting ethically, and providing a positive customer This will give banks the confidence to ensure no breaches in

experience. regulatory requirements such as AML and financial crime as well

as providing them with a holistic view of their customers.

Importantly, trust is also underpinned by consumers believing

that banks are keeping their data safe. A number of Oracle customers recognise the importance of a

disciplined strategy as crucial to an enterprise data platform to

respond to new regulations.

2

RFi Group’s Trust in Banking Insights 2020 Report - September 2020

Page

- 9 - Hidden Data Economy in Financial ServicesOne of them, ICICI Bank in India, has adopted Oracle Financial

Services Analytical Applications (OFSSA) to create an enterprise

wide view of risk. It was key to the bank addressing increased

burden of regulatory requirements and bringing together

the finance and risk departments, to achieve a risk-adjusted

performance view that investors were demanding.

The single biggest learning that we had from Mr. Ganesh said they had a granular look at data sourcing up front,

to look beyond immediate needs, into the future data requirements

this data transformation is to take your data so that “if they can cover 90% of the extended stakeholders

really seriously and take this opportunity to reporting needs, they would think their job is well done.”

make your data sourcing as easy as possible.”

– A R Ganesh, then General Manager responsible for the project, The AML compliance failures can shake up even the most stable

now CSO at the ICICI Bank banks. An independent and external report acknowledged that,

“the business of banks is no longer just about collecting deposits

and lending to home buyers and commercial entities at a margin

which provides a fair return. But also to accumulate, store and

monitor information on every transaction and, when required by

law, pass onto regulators and police for their scrutiny in search for

evidence of any criminality.”

Page 10 - Hidden Data Economy in Financial ServicesToday’s modern technologies, such as Oracle’s specialised

financial services applications, employ the new capabilities of

If we reduce 99% false positives by just 1%, it graph, AI and ML that help detect and derive patterns and make

means we’ll half our workload; by 10% - it will the insights actionable. But the first step to be taken in the

be even better and we absolutely expect new journey to AML program modernisation is to consolidate the

technology to help us with it.” backend, and move from disparate systems to a unified platform

for KYC/Customer Due Diligence (CDD), monitoring, detection,

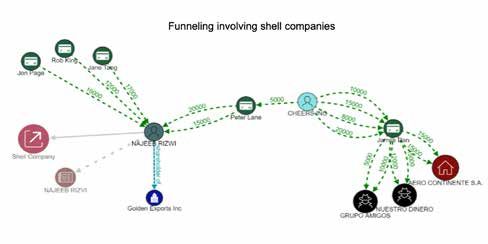

– François Cavayé, Global Head of Financial Security, investigation, and reporting.

Crédit Agricole Corporate Investment Bank

Another customer, Crédit Agricole, the world’s 10th largest bank

by total assets, is in the middle of transforming its systems as

part of its plan to overhaul its legacy technology. In particular,

the strategy focused on improving the anti-money laundering

function.

François Cavayé, Crédit Agricole Corporate & Investment Bank

Global Head of Financial Security, said that people have no

tolerance for such failures. The ‘balancing act’ is that customers

today expect new products, such as instant international

payments, which open banks to the increased risk. Cavaye’s

phased approach expects to gradually introduce new data sets Efficient investigation of highly organized financial crime requires technologies such as

graph analytics to succinctly express intricate money movement patterns, detect multi-hop

to the system, enable AI and big data to increase productivity, relationships, and identify hubs and spokes of activity.”

and eventually decrease “the unacceptable 99% false positive

alerts to drive productivity.”

Page 11 - Hidden Data Economy in Financial ServicesCosts and Productivity

In a bid to cut costs and increase productivity, the industry has They have not only improved data productivity but also ensured

invested in technology to streamline processes, tools and digital data liquidity by marrying data from its commercial, retail, research

platforms. Often though, these investments are yet to yield real and internal sources.

reduction in operational costs.

Adopting this approach, the standard banking process of risk

One area that is now coming into focus for optimizing operational analysis for loan grants was transformed. The bank used advanced

cost, is back office simplification and standardisation. It can also technologies such as ML to achieve a 7 per cent improvement in

drive the adoption of a common data model, common processes, the accuracy of its loan assessment which translated to a 12 per

so data is able to flow front-to-back and across business cent increase in profits on loans.

functions.

In another area, CaixaBank developed and deployed an algorithm

Spain’s CaixaBank is an example of success in this area. With trained from thousands of historical decisions on direct debits

more than 5,000 branches and 9,000 ATMs, CaixaBank has one of utility payments, and the result was a 99% accurate match to

of the largest networks in the country. It worked with Oracle to human decision-making. Once that level of accuracy was achieved,

undergo the most comprehensive transformation project that the algorithm took over the task. CaixaBank projected that 60,000

today underpins a holistic approach to managing a data platform, hours of human effort were saved across all branches, allowing

equipped to cater for future growth, quickly respond to current employees to spend more time on value-added tasks such as

and new regulations and offer its employees a unified and financial advisory, selling products, and services.

consolidated access to data from multiple sources.

Page 12 - Hidden Data Economy in Financial ServicesRebuilding Growth

With a greater focus on their core mission, the priority now

for banks is increasing that all important share of wallet. The

challenge is that the new customers entering the market may

never step foot in a bank branch, or call a contact center. Yet,

in a digital world, where customers are mostly “off-the bank”,

there are a myriad of opportunities.

One area of opportunity is in mobile banking. RFi Group

data shows that regular mobile banking usage (daily and

weekly) has increased over the last 12 months, and RFi Group

has forecasted that mobile banking usage will continue to

rise while branch banking will decline, albeit slowly.3 “Banks

also need to build loyalty and get better at servicing existing

customers to become more integral to their lives. For

example, this can be achieved by rolling out solutions that

help customers with budgeting and reaching their financial

goals,” Diez Blanco said.

Indeed, RFi Group data shows that features that help

customers save, such as incentivized savings goals, goal

trackers, and round up features have a lot of appeal including

for younger Australians – the customers of tomorrow.

3

RFi Group’s Australian Digital Banking Report 2020 - November 2020

Page

- 13 - Hidden Data Economy in Financial ServicesThe data also shows that tools such as identifying different barriers Striving to continuously improve customer service the bank

to savings can highlight how different features can appeal to employed Oracle Banking Platform to rationalise 23 systems and

certain segments. For example, the data shows that customers create a single Customer Service Hub, which provides staff with a

who struggle to cut back on their spending are more drawn to single view of customers across all Westpac brands and products,

round up features, safe to spend limits and smart tools that can starting with its core banking service - secured mortgage lending.

identify areas where they can save money.

In 2020 this project won the trade publication IT news’ Finance

This proposition puts the bank at the centre of their customers’ Project of the Year award and just recently clocked up a milestone

lives. Again, bringing together an extended customer view of 10,000th customer mortgage written on its platform.

that not only integrates internal transactions, but also external

customer activity and journeys will be important in achieving that By giving the bank’s lenders a single view of the customers, its

aggregated view. staff were able to engage with its customers both online and in

the branch. The end outcome of the Customer Service Hub has

Australia’s oldest bank, Westpac, has a rich history of over 200 been the creation of a smoother and faster home loan experience

years. Over the years, the bank has amassed a broad collection of for both Westpac bankers and customers that guides them and

technology platforms, and hence information about customers can supports them through the key elements of getting into the

be housed in multiple systems. property market, regardless of what channel they choose.

Page 14 - Hidden Data Economy in Financial ServicesHolistic Approach to Enterprise-Wide Data

3

Platform

Chapter 3 It is widely acknowledged that companies like Amazon or Facebook

have proven exceptionally adept at exploiting their data capital. What

are the defining elements in their operating models and architectures?

These companies first and foremost are platform businesses where the

Maximise data capital underlying data platform supports the channel to customers and drives

both innovation and the operating model.

value and grow your They have made significant investments in data infrastructure that

data economy

allows them to process massive quantities of data and make data liquid

and productive. Data platform components such as connectors,

data warehouses, data lakes, data science and APIs come pre-integrated

and packaged to support evolutionary deployments that match the

business’ roadmap and vision for maximising data capital value.

Banks like CaixaBank are starting to follow suit by designing

architectures that allow to make connections between data and create

data models that respond to new, more profitable ways to engage

customers, innovate with new products and scale up.

This puts them in a winning position in the face of growing competition

from new entrants, tighter regulatory regime and more sophisticated

financial crime.

Page 15 - Hidden Data Economy in Financial ServicesExample of an Enterprise Data Platform

ANALYSE, LEARN

DISCOVER INGEST TRANSFORM CURATE MEASURE & ACT

& PREDICT

Data Sources

Data Data Persistence Access & Data

Enterprise Data

Refinery Platform Interpretation Consumers

(can and will be

Batch Ingest Transaction Analytics Cloud anything)

Applications

Data Integration Serving Data Science People & Partners

Devices

Change Data Capture Object Storage Streaming Analytics

Applications

End Users Bulk Transfer Batch Processing Open Banking APIs

Streaming Ingest Streaming Processing Things

Events

Machines

Sensors

Security, Identity & Access Management Data Catalogue, Governance

Social Voice

Any Digital Asset

Discovery Lab & Sandbox

All services depicted above are part of the Oracle Cloud Infrastructure (OCI) portfolio

Page

- 16 - Hidden Data Economy in Financial ServicesThe ‘Example of an Enterprise Data Platform’ diagram (page 16) is showing the platform tools used to deliver departmental reporting from data that is coming from multiples sources and systems. In this example a data integrator is used to pull data from enterprise and departmental sources on a scheduled basis. Although the diagram displays data coming from enterprise applications, most often this data will be made available in the enterprise curated information area. After data is processed as needed it is then loaded into the Autonomous Data Warehouse (ADW) and data models are built, with enforced security to ensure continuity and compliance as reports are generated. Dashboards, information discovery (ML included), visualizations are created as needed. The Data Catalog is a no cost option that provides a means to begin collecting metadata, building glossaries, hierarchies to help establish a sound information framework as your information needs continue to grow. This is an example of architecture addressing the issues of data quality, accuracy, security and speed of reporting when leveraging a multitude of information sources for both actionable and deep insights. Page - 17 - Hidden Data Economy in Financial Services

Prioritisation and Faster Time to Value

A time-value reference for data is quite useful in prioritizing

investments to maximise the data capital that is being stored to

be re-purposed. How much time and effort would it take for a data

project to deliver a return - and what would be the value of this

return? McKinsey & Company argues that to keep the momentum

Being strategic about achieving quick wins early on going and win over skeptics, the project needs to start delivering

value within six months.4

and capturing benefits at each stage of platform

building gives companies the staying power to For Oracle customers, often the starting point is the modernisation

see long projects to completion, when exponential of finance and risk management and introduction of a common

value can be realised.” data platform across finance, risk, treasury and compliance. The

– McKinsey & Company’s Building a great data plaform financial services data foundation stages data directly from source

systems and allows to add new data sources over time, to cater for

the needs of other stakeholders.

4

Building a great data platform”, McKinsey & Company, August 2018

Page 18 - Hidden Data Economy in Financial ServicesBringing It All Together

For Oracle’s Sonderegger, banks tend to think of data in terms “However, even this is not the biggest prize. Increasing a firm’s

of what it takes to store, process and control it. However, a more data liquidity, data productivity, and data security puts it in a

robust approach to data management is crucial if banks are to position to take the next step—increasing data trade with built-in

grow their data economy. protections for all data stakeholders.”

He argues that because companies tend not to see data this way, According to Sonderegger as companies get their own internal

their internal data economies are hiding in plain sight. “As a data economies in order, they will find a new ability to license,

result of being hidden, most internal data economies are probably contract, and trade datasets with new and existing business

under-performing. Because companies don’t measure their data partners. “This will open the door for new digital goods and

creation and usage also suggests that companies get less value services these firms could not create on their own, enabling new

from their data than they should.” forms of value-creation for themselves and their customers.”

A firm’s reward for increasing its data liquidity, data productivity, Indeed, driving a unified focus on skills, back-end-processes,

and data security is both an increased return on data capital and core IT infrastructure and enterprise data architecture will be key

reduced legal and reputational risk costs that come from data if banks are to achieve a data-driven business that meets their

collection and usage. priorities in trust, cost and growth while also ensuring governance

and security. Building such a business will position banks to better

“Growing a company’s internal data economy by focusing on compete in the data economy while also meeting their customer

the data assets it creates and uses itself, emphasizes on using needs of today and the future.

proprietary data assets to create unique value in a unique way.

As a result, this is a potential source for sustainable competitive

advantage,” Sonderegger said.

Page 19 - Hidden Data Economy in Financial ServicesContributors

Christine St Ann Maximo Diez Blanco Paul Sonderegger

Editor, RFi Group VP, Industry Strategy Senior Data Strategist,

Group, Financial Oracle

Services, Oracle

Christine St Anne is a business journalist Maximo joined Oracle in 2006 from Paul leads the company’s work on data

with over 10 years experience. Accenture, where he was a Managing capital. Paul helps executives understand

Director at Accenture Financial Services the effects of data capital on competitive

She has written and edited for a wide range EMEA. strategy. He also works with Oracle’s data

of publications in the institutional and retail management product teams in setting

sectors and currently writes extensively on At Oracle, Maximo is responsible for Oracle’s future product direction. Paul speaks

banking and technology. Christine has also financial services industry strategy, including frequently on the rise of data capital, and is

written A Super History, a comprehensive the definition of new industry solutions, a contributing author at Forbes.com.

book about Australia’s compulsory GTM initiatives, and establishing strategic

superannuation system. partnerships with leading SIs, financial

services ISVs, and the fintech ecosystem.

Page 20 - Hidden Data Economy in Financial ServicesORACLE CORPORATION

Australian Headquarters

4 Julius Avenue, North Ryde NSW 2113

TEL 61 2 9492 1000

SALES 1300 366 386

oracle.com/au

Connect with us

Copyright © 2021, Oracle and/or it’s affiliates. All rights reserved. This document is provided for information

purposes only, and the contents hereof are subject to change without notice. This document is not warranted

to be error-free, nor subject to any other warranties or conditions, whether expressed orally or implied in

law, including implied warranties and conditions of merchantability or fitness for a particular purpose. We

specifically disclaim any liability with respect to this document, and no contractual obligations are formed either

directly or indirectly by this document. This document may not be reproduced or transmitted in any form or by

any means, electronic or mechanical, for any purpose, without our prior written permission.

Oracle and Java are registered trademarks of Oracle and/or its affilites. Other names may be trademarks of

their respective owners.

Intel and Intel Xeon are trademarks or registered trademarks of Intel Corporation. All SPARC trademarks are

used under license and are trademarks or registered trademarks of SPARC International, Inc. AMD, Opteron,

the AMD logo, and the AMD Opteron logo are trademarks or registered trademarks of Advanced Micro Devices.

UNIX is a registered trademark of The Open Group.

Oracle is committed to developing practices and products that help protect the environment.

Page

- 21 - Hidden Data Economy in Financial ServicesYou can also read