Financial stability implications of COVID-19 support measures

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ECB-Public

Financial stability implications

of COVID-19 support measures

SUERF E-workshop in

cooperation with KfW:

COVID-19 and government firm

rescue measures: best practices,

current challenges, and the way

forward post-corona

3 March 2021 Tuomas Peltonen

European Systemic Risk Board - Deputy Head of Secretariat

www.ecb.europa.eu ©

Key findings

1. To support the real economy during the COVID-19 pandemic, governments have

provided swift and unprecedented support packages.

− This has provided crucial relief to households and non-financial corporations.

− The financial system has continued to provide funding to the real economy, and loan

losses have remained limited.

− At the current juncture, credit markets are strongly supported by fiscal policy.

2. The longer the crisis lasts and the weaker the economic recovery will be, losses to

the non-financial sector could spill over to financial sector balance sheets.

− Deleveraging of banks might lead to adverse feedback loops.

− Cross-border banking activities might be particularly affected by deleveraging.

− There are trade-offs between supporting the economy and maintaining support for too

long.

2 www.ecb.europa.eu ©

The COVID-19 crisis has brought about a significant economic shock

• In comparison to previous crises, the expected cumulative output loss caused by the COVID-

19 pandemic is significant (loss of around 10% of EU GDP).

• Faster recovery than during GFC and Asian crisis expected. The Q4 2019 level is expected to

be reached by Spring 2022. Estimation of GDP losses for the COVID-19

Quarterly output loss of the COVID-19 pandemic and comparison with and other past crises (%)

other major crises (index, last period before recession = 100) GDP loss

Fiscal costs, net (Laeven and Valencia, 2018)

COVID-19 Russia (2008)

Global financial crisis (2008-2010) UK (1974) 25%

Asian crisis (1997) Mexico (1994)

Pre COVID

20%

130

125

15%

120 Area between dark blue and

115 grey lines (100) = 1.3 tn EUR

10%

110

105 5%

100

95 0%

COVID- Global Mexico UK (oil Asian Russia

90 19 financial (1994) crisis) crisis (2008)

85

crisis (1997)

(2008)

80 Source: Eurostat, European Commission, Haver Analytics, ESRB, Laeven and Valencia (2018) and

t t+1 t+2 t+3 t+4 t+5 t+6 t+7 t+8 t+9 t+10 t+11 t+12 ESRB Secretariat calculations.

Source: Eurostat, European Commission, Haver Analytics and ESRB Secretariat calculations. Note: GDP loss computed as the accumulated sum of the differences between quarterly GDP in the

Notes: the blue line represents q-o-q real GDP growth in the EU until Q4-2020 (t+4) and then the Winter Economic Forecast by the European 12 quarters of a crisis and GDP of the quarter immediately before the crisis, as a percentage of four-

Commission. Pre-COVID represents the estimated real GDP growth path in December 2019, according o the projections by the European Commission periods accumulated GDP at the onset of the crisis. Net fiscal costs, as reported by Laeven and

(growth for the last four quarters is forecasted to be constant at 0.3%). Global financial crisis refers to the EU real GDP growth path. The Asian crisis is Valencia (2018) are expected to be an approximation to the support received by the economy. The

computed as the average of Indonesia, Japan, South Korea, Malaysia, Philippines and Thailand. Real GDP growth for other crisis and countries is Asian crisis is computed as the average of Indonesia, Japan, South Korea, Malaysia, Philippines and

calculated in national currencies to avoid distortions by exchange rates. Thailand. No data on fiscal costs is available for the UK economy during the oil crisis and the EU

during the global financial crisis is the average of the net fiscal costs incurred by EU countries

(excluding UK).

. 3 www.ecb.europa.eu ©Recovery prospects vary significantly across EU Member States

• Italy and Spain are forecast to reach the pre-crisis real GDP level only in 2023.

• The heterogeneity of growth prospects is also reflected in the expected growth in the number of

insolvencies, albeit the relationship is weaker or even non-existent in some countries.

GDP forecasts for a selection of global economies Insolvency forecasts for 2020 and 2021

(Index: 2019 Q4 = 0) (Percentage change over same period in previous year)

2020 forecast

2021 forecast

Cumulative change 2020-2021

120

100

80

60

40

20

0

-20

CZ

NL

RO

HU

DE

FI

FR

EU*

IE

GR

IT

EE

PT

SK

ES

BE

PL

BG

AT

SE

LT

LV

LU

Source: Euler Hermes and Allianz Research. Notes: Forecast for DE, FR, ES, IT

and NL based on a revised version of the Euler Hermes and Allianz Research

report dated 24 September, other countries based on previous report dated 16

Source: EC Winter 2021 forecast and ESRB Secretariat calculations.

July. EU* refers to GDP-weighted sample of countries shown in the chart.

Notes: No GDP quarterly forecasts are reported for CY, EL, MT and

LU.

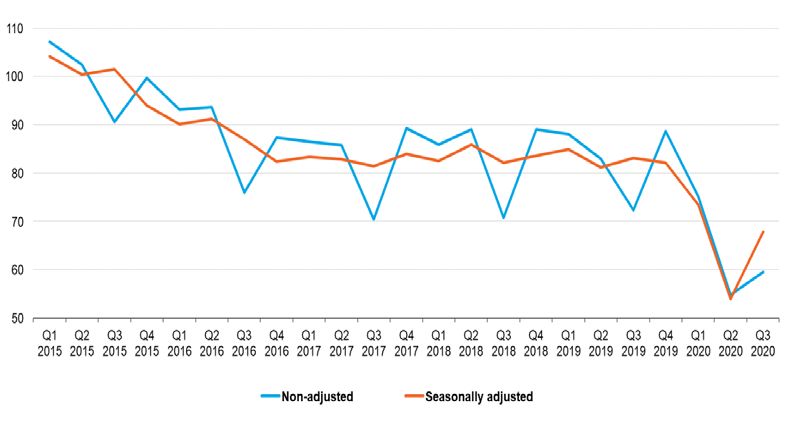

4 www.ecb.europa.eu ©Policy support has so far prevented mass corporate insolvencies

• Bankruptcies in the EU have so far decreased compared to the seasonally adjusted level.

• Banks’ provisions for IFRS stage 2 loans are highly heterogeneous across countries and –

contrary to expectations – not strongly driven by the country-specific size of the COVID-19

shock.

Declarations of bankruptcies in the EU, 2015-2020 Forecast GDP growth 2020-21 (x-axis, %) and change of

provisions for stage 2 loans (y-axis, percentage points)

0.7 p.p.

HU IE 0.6 p.p.

BG

0.5 p.p.

RO

0.4 p.p.

EBA 2018 R² = 0.0573

HR

BE 0.3 p.p.

PT CZ SK

AT

PL 0.2 p.p.

NL DK

CY SI EE 0.1 p.p.

FI LT

GR FR LU 0.0 p.p.

ES IT MT SE

LV

DE

-0.1 p.p.

-8% -6% -4% -2% 0% 2% 4% 6% 8%

Source: EBA Risk Dashboard, EC Winter Forecast and ESRB Secretariat calculations.

Source: Eurostat (2021)

Notes: Dots represent the change in provisions for stage 2 loans (share of stage 2 loans multiplied by

coverage) as reported in the EBA Risk Dashboard, between Q4 2019 and Q3 2020. EBA 2018 refers to

the adverse stress test scenario. Cumulative GDP growth in 2020 and 2021 in the 2021 EC Winter

Forecast.

5 www.ecb.europa.eu ©Fiscal support has been broad and swift, with differences in types of programs

and uptake across country

• Liquidity measures such as moratoria and public guarantees

until September 2020 were more important than solvency measures.

• Despite significant heterogeneity, countries hit harder have bigger programs and larger

uptake Total Total size

Total

uptake

Total size

announced

Uptake all measures

uptake announced Size all measures

(bn EUR) (bn EUR)

(% GDP (% GDP 2019) (y-axis: size or uptake in percentage of GDP; x-axis: QoQ GDP growth rate)

2019) 35%

Moratoria 838 5.0%

30%

Public

435 1,580 2.6% 9.5%

guarantees

Public loans 66 57 0.4% 0.3% 25%

Direct grants 112 327 0.7% 2.0%

20%

Tax

77 170 0.5% 1.0%

deferrals

15%

Tax reliefs 13 75 0.1% 0.4%

Public

support for 10%

n.a. 227 n.a. 1.4%

credit

insurance

5%

Total 1,541 9.2%

Total w/o 0%

704 2,436 4.2% 14.6%

moratoria -20% -15% -10% -5% 0% 5% 10%

Source: Recommendation ESRB/2020/08 (refer. date 30 Sep 2020), ECB (MNA, BSI, CBD). Source: Recommendation ESRB/2020/08 by 31 October 2020 (reference date 30 Sep 2020), ECB (MNA)

Note: Total size announced refers to field 1.1.01, and Total Uptake to field 2.2.10 for all Note: Announced size (field 1.1.01) and uptake (field 2.2.10) for all measures combined as a share of 2019 GDP on the y-axis.

measure apart from tax reliefs and tax deferrals, where field 2.2.12 was used. Reporting data Quarter-on-quarter GDP growth from Q1 2020 to Q2 2020 on the x-axis. Based on 28 countries (IS, LI and NO are excluded).

gaps exist – results should be interpreted with caution.

6 www.ecb.europa.eu ©While moratoria serve both NFCs and households, public guarantees are

mostly extended to NFCs.

• The share of loans under moratoria to total loans for most countries is higher for NFCs than

for HHs and strong for SMEs.

• Public guarantees had an uneven impact across European countries and banks. Most of the

support is extended to NFCs.

(% of total loans and advances to the household and NFC sector, respectively) (% of total loans and advances to the household and NFC sector, respectively)

Source: EBA, ESRB calculations (reference date June 2020). Source: EBA, ESRB calculations (reference date June 2020).

Note: Countries are sorted according to the share of loans under moratoria in total loans and advances Note: Countries are sorted according to the share of loans under moratoria in total loans and advances

to households and NFCs. The values correspond to the mean value for banks in the given country. to households and NFCs. The values correspond to the mean value for banks in the given country. CY

Values for CY – 45% for HHs, 53% for SMEs and 17% for Other NFCs are not shown for presentational – 45% for HHs, 53% for SMEs and 17% for Other NFCs – left out for presentational reasons.

reasons.

7 www.ecb.europa.eu ©More vulnerable sectors and countries have benefitted from the support

measures, but face a higher risk of an early withdrawal of support

• Countries with high employment in vulnerable sectors rely more on direct grants.

• The uptake of moratoria is positively correlated with pre-crisis debt levels.

(Direct grants) (Direct grants)

(Moratoria) (Moratoria)

Size direct grants (y-axis) and employement in 8% 8%

Less vulnerable vulnerable sectors (x-axis)

More vulnerable 4.0%

7% 7%

3.5%

3.5%

6% 6%

3.0%

3.0%

5% 5%

2.5% 2.5%

4% 4%

2.0% 2.0%

3% 3%

1.5% 1.5%

2% 2%

1.0%

1.0%

1% 1%

0.5%

0.5% 0% 0%

Low household debt High household Low NFC debt High NFC debt

0.0%

20% 25% 30% 35% debt

0.0%

Source: Recommendation ESRB/2020/08 by 31 October 2020 (reference date 30 Sep 2020), ECB (MNA) Source: Recommendation ESRB/2020/08 by 31 October 2020 (reference date 30 Sep 2020), ECB (MNA)

Note: Announced size (field 1.1.01) as a share of 2019 GDP on the y-axis for the three graphs. Vulnerability is defined as the Note: Uptake (field 2.2.20) of moratoria, public guarantees and loans as a share of 2019 GDP on the y-axis. Median over

share of employment in the NACE sectors G, H, I R, T, U in Q4 2019. The bar plots depict the median over the lowest (highest) countries in the lowest (highest) quartile of household ("HH") or NFC debt over GDP in Q4 2019 as "low debt" ("high debt") on

quartile of the vulnerability metric as "less vulnerable" ("more vulnerable"). The scatterplot compares the announced size of the x-axis. All graphs based on 28 countries (IS, LI and NO are excluded).

direct grants (as a share of 2019 GDP; y-axis) to the vulnerability metric (a higher share means higher vulnerability; x-axis). All

graphs based on 28 countries (IS, LI and NO are excluded).

8 www.ecb.europa.eu ©Following the surge in Q2, lending to the private sector decelerated in H2 2020

• The outstanding stock of NFC loans has been broadly stable in H2.

• Mortgage lending to HH continued to gradually accelerate in the course of 2020, while consumer

lending collapsed – in line with the propensity to increase precautionary savings.

Outstanding loans to NFCs Outstanding loans households

(growth rate and stock) (growth rate and stock)

NFC loans (outstanding stock, lhs)

NFC loans (y-o-y growth, rhs) 5.5 7%

Consumer loans

5.0 6% (outstanding stock, lhs)

4.4 7%

House purchases

4.5 5% (outstanding stock, lhs)

4.3 6% Other (outstanding stock,

4.0 4% lhs)

Consumer loans (y-o-y

Trillions of euros

4.2 5% 3.5 3% growth, rhs)

Trillions of euros

House purchases (y-o-y

3.0 2% growth, rhs)

4.1 4%

Other (y-o-y growth, rhs)

2.5 1%

4.0 3% 2.0 0%

1.5 -1%

3.9 2%

1.0 -2%

3.8 1%

0.5 -3%

3.7 0% 0.0 -4%

Mar-18

Mar-19

Mar-20

Jan-18

Jan-19

Jan-20

May-18

May-19

May-20

Jul-18

Sep-18

Nov-18

Jul-19

Sep-19

Nov-19

Jul-20

Sep-20

Nov-20

Mar-18

Mar-19

Mar-20

Jan-18

Jan-19

Jan-20

May-18

May-19

May-20

Jul-18

Sep-18

Nov-18

Jul-19

Sep-19

Nov-19

Jul-20

Sep-20

Nov-20

Source: ECB Balance Sheet Items and ESRB Secretariat calculations. Source: ECB Balance Sheet Items and ESRB Secretariat calculations.

Notes: Euro area aggregates. Notes: Euro area aggregates.

9 www.ecb.europa.eu ©Bank lending in 2020 characterised by large cross-country heterogeneity

• In few countries (CY, CZ, GR, IE, LT, PL, SI) lending to NFCs and households decelerated in the

course of 2020, while others reported large increases in lending to NFCs (ES, FR, PT, SE) or to

households (BE, BG, LU, SE).

Outstanding amounts of loans (blue bars) and of debt

securities issued (green bars) in the domestic economy, Outstanding amounts of loans to households in the

non-financial corporations, Jan 2020- Dec 2020 domestic economy, Jan 2020 - Dec 2020

(Index: Loans January 2020 = 100) (Index: January 2020 = 100)

115 115

110 110

105

105

100

100

95

95

90

90

85

80 85

AT BE BG CY CZ DE DK EE ES FI FR GR HR HU IE IT LT LU LV MT NL PL PT RO SE SI SK AT BE BG CY CZ DE DK EE ES FI FR GR HR HU IE IT LT LU LV MT NL PL PT RO SE SI SK

120

100

Source: ECB Balance Sheet Items, ECB Securities Statistics and ESRB Secretariat calculations.

80 Notes: the blue bars show the outstanding amount, at the end of each month in 2020, of loans to non-financial

60 corporations and to households, indexed to January 2020 = 100. The green bars show the outstanding

40 amounts of debt securities issued by non-financial corporations, between January and December 2020,

20

indexed to loans to non-financial corporations in January 2020 = 100. For debt securities, data is available on a

monthly basis only for euro area countries.

0

AT BE BG CY CZ DE DK EE ES FI FR GR HR HU IE IT LT LU LV MT NL PL PT RO SE SI SK

10 www.ecb.europa.eu ©Economic agents increased their holdings of liquid assets

• Deposits of NFCs and households significantly increased since the onset of the pandemic

(despite the low level of interest rates).

• Euro area banks increased their cash holdings by more than EUR 1tn to build a buffer in the

face of heightened uncertainty.

Changes in cash and other assets

Outstanding amounts of deposits by non-financial corporations (left-hand

(EUR trn)

side) and by households (right-hand side) on domestic banks (EUR trn) Cash

Other assets

3.6 Total assets

9.2

2.0

3.4 9

3.2 8.8 1.5

8.6

3 1.0

8.4

2.8

0.5

8.2

2.6

8 0.0

2.4

7.8

-0.5

2.2 7.6

2 7.4 -1.0

-1.5

2019Q1 2019Q2 2019Q3 2019Q4 2020Q1 2020Q2 2020Q3

Source: ECB Balance Sheet Items and ESRB Secretariat calculations. Source: SSM supervisory data and ESRB Secretariat calculations.

Notes: outstanding amount of deposits of households and non-financial corporations, for the EU 27 Notes: based on supervisory information published by the SSM on

for the period January 2018 to December 2020. the banks under its direct supervision.

11 www.ecb.europa.eu ©Policy priorities for addressing risks in the NFC sectors

• Continue public support measures until the economic recovery is firmly

entrenched on the back of the rollout of vaccinations.

• Gradually move to more targeted support measures to avoid supporting (i)

companies that can operate without public support; and (ii) unviable companies.

• Increasingly complement liquidity support with equity support for viable, but

already highly indebted companies (potentially in the form of quasi-equity

injections, subsidies and the restructuring of debt to banks and other creditors).

• Address deficiencies in bankruptcy frameworks; implement preventive

restructuring; strengthen capacity/efficiency of the judiciary to be able to handle

a surge in bankruptcies.

12 www.ecb.europa.eu ©Thank you for your attention

For more information at the ESRB website:

https://www.esrb.europa.eu/home/search/coronavirus/html/index.en.html

Database of public support measures

A new publication

tuomas.peltonen@ecb.europa.eu

13 www.ecb.europa.eu ©You can also read