Fighting Fraud & Corruption in Uganda - Steven Powell 25 August 2021 - ENSafrica

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Fighting Fraud & Corruption in Uganda Steven Powell 25 August 2021

objectives? • fraud facts and theory including the profile of the fraudster • an explanation of corrupt practices, & procurement risks • corruption overview - tender abuse & other corrupt schemes • cyberfraud • EFT Fraud – (diverted payments) • fraud prevention and internal controls • fraud risk indicators • the tools to identify corruption • case studies

the profile of the typical fraudster

• White collar crime statistics reveal that more

than 80% of fraud involves internal employees,

most of whom have more than 5 years of service

• Many companies who fall victim to fraud rely

on trust rather than controls

• The fraudster could be your most capable, most

reliable & most trusted employee

Telegraph UK

Generally the profile of the typical fraudster is:

Older than 30, stable family situation, above average education, first

offender and has been with the company for more than 5 years

The fraudster is often the last person that anyone would suspect and

the “red flags” (symptoms) that become known are often ignored due

to high levels of trust

the fraud triangle - Psychology behind it

fraud takes place when the 3 factors described below converge

the fraud recipe

The employee will justify

fraud takes place committing acts of

when employees dishonesty by

under pressure rationalizing his or her

identify the behaviour

opportunity to Rationalization takes

commit fraud - the form of finding

coupled to a justification for the

perceived low risk behaviour by re-labeling

of detection to remove moral stigma

fraud

rationalization

fraud pressures

• Often, formally honest employees commit

fraud as a result of pressure which presents

itself in a variety of ways:

• living beyond means

• insecurity regarding tenure of position,

retrenchments

• trigger events

divorce

extra marital affairs

medical emergency

• peer pressure

• gambling alcohol or drug problems

opportunity

• When employees experience the pressure, they often start looking for gaps or

weaknesses in the control environment

• Opportunity to commit fraud presents itself in a variety of forms:

• Weak control environment

• Shared passwords

• Limited segregation of duties

• Limited independent review

• Poor management oversight

• Remote location

• High trust

examples of “rationalizations” Rationalization takes place when employees try to justify or re-label their illicit activity in order to make it seem less morally reprehensible Examples of rationalisations that have been verbalized: “it was just a loan I am going to pay it back” “it was a spotters fee” “it was just a commission” “the company makes huge profits but does not pay us enough” “the company has retrenched a lot of staff” “I should have been promoted long ago”

the detection of fraud

most frauds are discovered by accident when fraudsters become careless or greedy

60%

50%

40% management

auditors

30% tip-offs

accident

20%

10%

0%

Many frauds are discovered as a result of tip-offs (Colour green because many

tip-offs come from disgruntled mistresses or ex wives)

Michael J Comer

Procurement Fraud & Tender abuses in SA

• Collusion with government officials in tender irregularities:

• creation of artificial / inflated need

• tender fixing & drafting tender specifications

• avoiding tender by irregular expansion or extension of contract after award

• avoiding tender by misuse of single-source procurement exception

• government insiders sharing confidential tender information and assisting

bidders in tenders

• Systemic use of middle-men to influence tenders and facilitate suspect payments

• Enterprise development needs exploited - subcontractors as conduits to channel

funds

• Using vague agreements to contractually facilitate suspect payments – bland

descriptions

• Characterized by inappropriate gifting, sponsorships or donations

examples of fraudulent schemes ghost suppliers this is a letterhead and a bank account the corrupt employee signs off or requisitions payments for a company which does not exist payments are made to this entity and usually find the way to the employee or his spouses accounts no services or supplies are rendered key controls Someone other than the employee who ordered the goods should sign off confirmation of delivery/proof of service Close the gates – new vendors must be properly checked and verified when they are added to the vendor database (company and credits checks should be routine)

Procurement fraud case study

German motor manufacturer

• Head of procurement took

kickbacks for appointment as a

contractor

• home renovations

• Harley Davidson

• several cars including expensive

4x4

• regular o/seas trips

Result

• prejudice R7 million

• 4 service providers terminated

• 6 year jail sentence for head of

procurementMaintenance depot procurement fraud case study

• Officials place orders for parts to repair the vehicle

• Part is not delivered but officials complete paper trail

• Requisition

• Purchase OrderR5m-a-year corruption scam uncovered

• Delivery note

• Job cards

• When parts are actually delivered - Part is re-routed back to

supplier

• Illicit profit by supplier is shared with the syndicate

• Whistle blower reveals corruption running for more than a

decade

“R5million a year corruption scam uncovered”

Cape Argusconflict of interest

• large portions of procurement spend is allocated to companies

that employees and senior officials have undisclosed interests in

• undeclared interests and secret profits inflate the cost of doing

business exponentially -the solution is

• a robust declaration of interest policy which obliges

declaration of all interests

• coupled to vendor screening – (know who owns your service

providers)tools to ID fraud and tender abuse

lifestyle audit – also known as the means test

• By accessing various public databases – gather intelligence on buyers

managers and decision makers to ensure assets are commensurate to

known income stream:

• properties

• motor vehicles

• credit

• company links

• identify adverse information or negative data by using internet or

company searches and screen employees for negative histories

• credit and

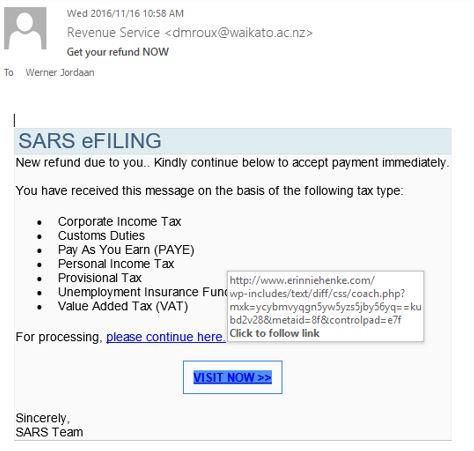

• criminaldigital fraud • Identity theft: where criminals obtain information about you to convince a bank or a customer service representative that they're you. • Phishing: where criminals attempt to trick unsuspecting individuals into clicking on a malicious URL or e-mail attachment to steal their login details which they can then use to gain unauthorized access to the victims' financial accounts. • Pharming refers to redirecting website traffic through hacking, whereby the hacker implements tools that redirect a search to a fake website. Pharming may cause users to find themselves on an illegitimate website without realizing they have been redirected to an impostor site, which may look exactly like the real site. • Ransomware: where a hacker encrypts files on your computer. The only way to get the files back is to pay the hijacker in crypto currency, like Bitcoin. • Online deposit scams (puppy scams etc). Recently, cyber security firm, Norton, said globally, 978 million consumers were affected by cyber crime in 2017 stealing a total of $172 billion.

phishing & pharming

how to minimise the risk

• Be very selective with the type of information

that you share on social media sites18

how to minimize the risks cont’d

• Use strong passwords, with a variety of upper case and lower case

letters, symbols, and numbers. Never write them down where

other people can see them. You should also try to change them up

every now and then.

• Only use reputable online shopping sites. One thing you can do is

look at the URL of the website. If it begins with “https” instead of

“http” it means the site is secure. Also check with friends if they’ve

heard of it or used it before.

• Be extra cautious when using Wi-Fi hotspots. Some scammers

falsify popular hotspots.

• Don’t click on random links.are you sharing too much?

The use of social media

• Names of children, places of employment, places you frequent

(your Facebook “check-ins”, birthdate – all can be accessed via

social media and can be used to perpetrate identify theft.

• Don’t post pics of your holiday in the Seychelles

• CFO case study

• Make sure your privacy settings are updated!!EFT fraud risk EFT fraud is essentially the diversion of funds from the organisation’s bank accounts to third parties, to whom those funds are not due, usually involving manipulation of the vendor payment system

electronic funds transfer fraud

• two methods

• creation of alternative

vendor profile which is then

selected to perform illicit

transactions

• substitution of employee

account and deletion

• in the 1st scenario the risk

of being caught is higher as

the employee info remains

on the vendor profile and

should be detected through

proper checkswhose problem is EFT fraud

• it is invariably an account holder problem,

• and usually not a bank problem

• it is usually facilitated by password abuse within

the finance team

• spyware and collusion with bank officials must be

excludedcase study eft payment clerk

• shaken not stirred – 007 steals R740k from a large retailer

• position - eft payment clerk – earnings R10k

divorce weak controls

fraud

rationalizationcase study : EFT payment clerk

• A junior employee in a finance team, whose role involved

processing batches of vendor payments electronically, got

divorced

• He was already battling to manage financially and now needed

to pay for a messy divorce, alternative accommodation &

maintenance

• Realised that he can authorise and release transactions with his

supervisors password

• Made small talk with his supervisor as he was logging in, -

noted his password, and voila…. he could create, capture and

release payments

• He tested thresholds with small payments to himself then

waited…

• Suspect became very bold and loaded a duplicate vendor with

his personal bank account on the vendor master database

• Nobody noticed, and the volume and scale of his fraud

escalated, within a year he had stolen just under a millioncase study contd : the black hole

• lost payment – software programmers

showed our suspect how to manually

override the system to ensure that payments

reach the intended destination

• every time our suspect made a legitimate

payment he knew he could steal by changing

a text file on his c drive:

• “I could not resist the temptation; I had

the devil on my shoulder tempting me to

try process a fraudulent transaction, it

was just too easy!”case study – chief accountant

• R2 million in one year

• modus operandi – amendment of vendor banking

account detail on vendor master file

• substituted account not own account (DRC)

• once illicit transaction concluded – amended vendor

profile deleted and vendor banking info restored to

original

• when routine audits are performed – all appears as it

should

• where did the money go?

• the local casino received R1,95 million out of the R2

million stolencase study - FD at packaging company

• R4.2 million misappropriated

Bedside reading material

• R1.7 million in one morning

substitution and deletion

• vehicles, houses, timeshare (house

search), gambling, overseas travel,

holidays, private schooling, heart

operation,

• Property & vehicles for family,

• vehicle for close friend

• safety deposit boxes?

• R3 million recovery via full co-operation

which translated into mitigation for an

effective 5 year jail termCase

case studystudy 4 manager

– Financial

• Stole R4,2 million in Western Cape over 8 years

• Committed traditional EFT fraud via diverted payments

• suspect placed personal stop orders (DSTV, Telkom cars and

insurance on organisation account)

• suspect paid for her house R1.3 million with EFT to lawyers

• suspect overpaid suppliers and diverted reimbursement to

her accountwhat should the company have picked up?

• eft clerk

• the payments to a particular supplier whose profile was

exploited was far over budget

• routine audits testing payroll against the vendor master

files would have identified the illicit profile

• chief accountant

• password control was abused

• cfo signed off batches of eft’s – if he just counted the

transactions he would have noticed that there were more

payments in the batch than the paperwork reflected

• supplier payments were duplicate- a proper recon of each

supplier against approved budget would have identified

the overspend

• There were multiple changes to vendor banking details

which is abnormalkey controls to prevent EFT abuse

• vet vendors properly (address, history, bank

account, expertise & infrastructure)

• enforce tight control over changes to suppliers

bank accounts – add management authorisation

• audit changes to supplier banking info over the

past year

• interrogate the changes

• verify with suppliers and banking institutionthe symptoms of fraudulent behavior

the red flags or warning signals in respect of the corrupt

employee are always present - make sure that staff report

suspicious activityfraud red flags excessive lifestyle gambling alcohol or drug problems staff who constantly claim underpaid close relationships with suppliers sole suppliers - not shopping around poor credit rating poor communication and reports indulging in affairs not taking leave refusal of promotion excessive & unexplained overtime criminal record

divisional red flags

• too much trust placed in key employees

• limited segregation of duty

• no independent checks on reconciliation and payments

• no clear lines of authority or responsibility

• proper authorization procedures not enforced

• inadequate documentation & records

• infrequent independent reviews

• inadequate disclosure of interests & investments management

override of the controls

• operating on a crisis basis

• inadequate attention to detailconclusion

fraud and corruption are significant risks

prevention is better than cure

people will try to tempt your staff

promote a strong ethics culture

review your anti-fraud controls annually

perform control review regarding eft payments

do not rely only on controls - only as effective as the people

enforcing the controls

train people to recognize the symptoms

do not work in a vacuum - use the tools and technology &

experts

©2009 S Powellquestions

Steven Powell spowell@ENSafrica.com +27 21 410 2553 or +27 82 820 1036

You can also read