FCPA 2020 Year-End Update - January 26, 2021 Panelists

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FCPA 2020 Year-End Update

January 26, 2021

Panelists:

Patrick Stokes

John W.F. Chesley

Christopher W.H. Sullivan

Ella Alves Capone

Moderator: F. Joseph Warin

MCLE Certificate Information

• Most participants should anticipate receiving their certificate of

attendance within four weeks following the webcast.

• Virginia Bar Association members should anticipate receiving their

certificate of attendance within six weeks following the webcast.

• All questions regarding MCLE Information should be directed to

Victoria Chan (Attorney Training Administrator) at 650-849-5378 or

vchan@gibsondunn.com.

2

Today’s Panelists

F. Joseph Warin Patrick Stokes John Chesley

FWarin@gibsondunn.com PStokes@gibsondunn.com JChesley@gibsondunn.com

TEL:+1 202.887.3609 TEL:+1 202.955.8504 TEL:+1 202.887.3788

Christopher Sullivan Ella Alves Capone

CSullivan@gibsondunn.com ECapone@gibsondunn.com

TEL:+1 202.887.3625 TEL:+1 202.887.3511

3

Gibson Dunn Programs & Resources

Upcoming Programs

• February 23, 2021 webcast - 17th Annual Challenges in Compliance and Corporate Governance

• Securities Docket February 2, 2021 Webcast – Navigating the Minefield of Dodd-Frank’s

Whistleblower Provisions (2020 Update)

Recent Programs Gibson Dunn Webcasts (CLE Credit Available)

• December 10, 2021 webcast – International Anti-Money Laundering and Sanctions Enforcement

• January 12, 2021 webcast- FCPA Trends in the Emerging Markets of Asia, Russia, Latin America,

India and Africa

• January 7, 2021 webcast – Privacy and Consumer Protection in the Biden Administration

Resources

• 2020 FCPA Year-End Update

• 2020 FCPA Mid-Year Update

• Gibson Dunn FCPA Practice Group

• COVID-19 Resource Center

4

Agenda

1. FCPA Overview

2. Anti-Corruption Policy and Enforcement

Updates

3. DOJ FCPA Enforcement Framework

4. FCPA Trends and Enforcement Actions

5

FCPA Overview

FCPA – Overview

The FCPA was enacted in 1977 in the wake of reports that numerous U.S.

businesses were making large payments to foreign officials to secure business.

• Anti-Bribery Provisions. The FCPA prohibits corruptly giving, promising, or

offering anything of value to a foreign government official, political party, or party

official with the intent to influence that official in his or her official capacity or to

secure an improper advantage in order to obtain or retain business.

• Accounting Provisions. The FCPA also requires issuers to maintain accurate “books

and records” and reasonably effective internal controls.

U.S. Enforcement Agencies

Department of Justice Securities and Exchange Commission

• Criminal enforcement of anti-bribery provisions • Civil enforcement of the anti-bribery provision

• Criminal enforcement of the accounting provisions (issuers)

(books and records and internal controls) • Civil enforcement of the accounting provisions

(books and records and internal controls)

• Increasing utilization of non-FCPA statutes

• ~ 38 enforcement attorneys in Home Office, plus

• ~ 35 prosecutors in the Criminal Division FCPA Unit attorneys in several Regional Offices

7FCPA – Anti-Bribery Provisions

• The FCPA prohibits not only actual payments, but also any offer, promise, or

authorization of the provision of anything of value.

➢ An offer to make a prohibited payment or gift, even if rejected, may violate the FCPA.

• The FCPA also prohibits indirect corrupt payments.

➢ The FCPA imposes liability if a U.S. company authorizes a payment to a third party

while “knowing” that the third party will make a corrupt payment.

➢ Third parties include local agents, attorneys, brokers, consultants, distributors, joint-

venture partners, liaisons, and subsidiaries.

• There is no “de minimis” exception, and a “thing of value” can include:

Charitable / Political Contributions Consulting Fees Entertainment / Sporting Events

Education / Internships / Training Free Goods Gifts

Grants / Research Support Meals Travel

8FCPA – Accounting Provisions

• Connection to Bribery Allegations. Unlike the FCPA’s anti-bribery provisions, the books

and records and internal controls provisions do not require a nexus between:

➢ An inaccurate book or record or a weak control, and

➢ An allegedly improper payment.

• DOJ / SEC Approach. The government often invokes the accounting provisions where it

lacks jurisdiction to bring a bribery charge or when it is seeking to compromise in the context

of settlement negotiations.

➢ The SEC has shown a greater willingness to bring charges based on the accounting

provisions even where it lacks sufficient evidence to conclude that bribery occurred.

➢ The SEC brings accounting provision charges against issuers, whereas DOJ may

bring parent or subsidiary accounting provision charges.

• Compliance Controls. The SEC frequently asserts that an expansive scope of conduct

implicates the internal controls provision, including accounting-related deficiencies and issues

traditionally associated with weak corporate compliance programs.

9DOJ Under the Biden Administration

Attorney General

Merrick Garland

(Nominated, Pending Confirmation)

Current Acting – Monty Wilkinson

Deputy Attorney General

Lisa Monaco

(Nominated, Pending Confirmation)

Current Acting - John Carlin

Criminal Division

Acting Assistant Attorney General

Nicholas McQuaid

Fraud Section

Acting Chief Daniel Kahn

FCPA Unit

Chief – Christopher Cestaro

10SEC Under the Biden Administration

Chairman

Commissioner Gary Gensler

Commissioner (Nominated, Pending Commissioner Commissioner

Allison Herren Lee

Caroline Crenshaw Confirmation) Hester M. Peirce Elad Roisman

(Term expires 2022)

(Term expires 2024) (Term expires 2025) (Term expires 2023)

Currently acting Chair

Enforcement

Acting Director - Melissa Hodgman

FCPA Unit

Chief – Charles Cain

11FCPA Enforcement Actions (2011-2021*)

35

35 DOJ Actions

32 SEC Actions

30 29

25

25

23

22

21 21

20 19 19

17 17

15

12

11 11

10 10 10

10 9

8

5

1 1

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 12

*As of January 25, 2021FCPA + FCPA-Related Enforcement Actions (2011-2021*)

FCPA-Related DOJ

SEC Actions

60

DOJ Actions

50

19

40

26

7

30 19

1 2 6

6

20

35

32

29

23 25 1 2 21 22 21

10 19 19

17 17

11 12 10 10 10 11

8 9

0 1 0

1

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

*As of January 25, 2021

13U.S. Corporate FCPA Top 10 List

No. Company Total Resolution DOJ Component SEC Component Date

1 Goldman Sachs $1,663,088,000 $1,263,088,000 $400,000,000 10/22/2020

2 Ericsson $1,060,570,432 $520,650,432 $539,920,000 12/06/2019

3 Mobile TeleSystems $850,000,000 $750,000,000 $100,000,000 03/06/2019

4 Siemens AG $800,000,000 $450,000,000 $350,000,000 12/15/2008

5 Alstom S.A. $772,290,000 $772,290,000 -- 12/22/2014

6 KBR/Halliburton $579,000,000 $402,000,000 $177,000,000 02/11/2009

7 Teva $519,000,000 $283,000,000 $236,000,000 12/22/2016

8 Telia $483,103,972 $274,603,972 $208,500,000 09/21/2017

9 Och-Ziff $412,000,000 $213,000,000 $199,000,000 09/29/2016

10 BAE Systems $400,000,000 $400,000,000 -- 02/04/2010

14Global Dimension of Anti-Corruption Enforcement Actions

In addition to substantial monetary penalties in the U.S., in recent years

companies are increasingly paying significant fines to non-U.S. enforcers.

Company Global Resolutions

Goldman Sachs agreed to pay over USD 2.9 billion to U.S. government bodies and foreign

Goldman Sachs (2020)

authorities in countries including the United Kingdom, Singapore, Hong Kong and Malaysia.

Odebrecht agreed to pay USD 2.6 billion (down from $4,503,600,000 due to inability to pay) in a

Odebrecht (2016)

coordinated resolution with U.S., Brazil, and Swiss authorities.

The total combined amount of United States, Dutch, and Swedish penalties was USD 965.8

Telia Company AB (2017)

million.

Airbus’s total sanctions, paid to United States, United Kingdom, and French authorities, totaled

Airbus SE (2020)

around USD 4 billion.

While the DOJ assessed the full USD 585 million penalty against SocGen, approximately half of

Société Générale S.A. (2018) it (USD 292.8 million) was paid to the French regulator, Parquet National Financier and

credited against the U.S. fine.

15Anti-Corruption Policy and

Enforcement UpdatesUpdated Guidance for Evaluating Corporate

Compliance Programs

• In June 2020, DOJ updated its guidance entitled “Evaluation of Corporate Compliance

Programs.” This guidance is structured around three “fundamental questions” that DOJ

prosecutors should ask in assessing corporate compliance programs in an investigation, in

making charging decisions, and in negotiating resolutions:

➢ Is the program well-designed?

➢ Is the program being applied earnestly and in good faith? In other words, is the

program adequately resourced and empowered to function effectively?

➢ Does the Program work in practice?

• The updated guidance groups 12 topics and sample questions that DOJ considers relevant

in evaluating a corporate compliance program.

• There is an emphasis on evaluating compliance programs on a case-by-case basis relative

to the individual company’s size, industry, geographic footprint, and regulatory landscape

and on whether control functions are provided with sufficient resources and data

access to discharge their responsibilities.

17SFO Guidance on Evaluating Compliance Programs

• In January 2020, UK’s Serious Fraud Office also published guidance on how the SFO

will evaluate a company’s compliance program when considering an enforcement

action and a sentence, in the event of a successful prosecution.

• The guidance begins by stating that a compliance program “needs to be effective and

not simply a ‘paper exercise.’”

➢A compliance program should be “proportionate, risk-based, and regularly-

reviewed.”

• The SFO will consider compliance programs at the time of the offense, at the current

time, and in the future, with respect to how it might change.

• The guidance also refers to “six principles” that compliance programs should reflect:

(i) Proportionate procedures; (ii) Top level commitment; (iii) Risk assessments;

(iv) Due Diligence; (v) Communications, including training; and (vi) Monitoring

and review.

• Directs prosecutors to evaluate compliance programs “early on” in an investigation.

18CFTC Enforcement Guidance for Evaluating Corporate

Compliance Programs

• In September 2020, the CFTC issued guidance outlining factors that will be considered in a

risk-based analysis when evaluating compliance programs in connection with enforcement

matters.

• The guidance considers whether a compliance program was reasonably designed and

implemented to: (i) prevent the underlying misconduct at issue; (ii) detect the misconduct;

and (iii) remediate the misconduct.

• Factors evaluated for a program’s ability to prevent misconduct include: (i) Written policies

and procedures in effect; (ii) Training of staff; (iii) Failure to cure any previously identified

deficiencies; (iv) Adequate resources; and (iv) Structure, oversight, and reporting of compliance.

• Factors evaluated for the effective detection of underlying misconduct include: (i) Internal

surveillance and monitoring; (ii) Internal-reporting system and handling of complaints; and (iii)

Procedures for identifying and evaluating unusual or suspicious activity.

• Factors evaluated for remediation include: (i) Effectively addressed the impact of the

misconduct; (ii) Appropriately disciplined responsible individuals; and (iii) Identified and

addressed any deficiencies.

19Update to the FCPA Resource Guide

• In July 2020, DOJ and SEC published its first comprehensive update to their FCPA

Resource Guide to the FCPA, which was first issued in November 2012.

➢ Inclusion of the FCPA Corporate Enforcement Policy

➢ Updated guidance on the application of the FCPA in M&A transactions

➢ Updates regarding the scope of the term “agent” for assessing corporate

liability

➢ Scope of the SEC’s disgorgement authority

➢ Requirements for criminal violations under the accounting provisions

20SEC Commissioners Rebuff Extensive Use of Internal Controls

• In October 2020, the SEC settled charges against Andeavor for allegedly failing to

devise and maintain a system of internal controls sufficient to provide reasonable

assurances that stock buyback transactions were executed in accordance with

management's authorization and without material nonpublic information.

➢ A majority of the Commission accepted the settled action, but Commissioners

Peirce and Roisman voted against it.

• In November 2020, Commissioners Pierce and Roisman issued a statement

explaining why they voted against the settlement, in which they said the FCPA

requires not “internal controls” but “internal accounting controls” and that

this matter as well as other recent ones “go well beyond the realm of

“accounting controls.”

➢ Insider trading cases are typically brought under the Exchange Act Section

10(b) and Rule 10b-5, which would have required proof that Andeavor acted

with scienter.

21SEC Approves Amendments to Whistleblower Program Rules

• On September 23, 2020, the SEC approved amendments to its whistleblower

program to “provide greater clarity to whistleblowers and increase the

program’s efficiency and transparency.”

➢ Revising the definition of “whistleblower” to cover only individuals who

report information in writing to the SEC per Digital Realty Trust (US 2018);

➢ Procedural changes to facilitate more efficient resolution of frivolous claims

and to bar individuals who have filed false or frivolous claims;

➢ Clarifying that DPAs, NPAs, and SEC settlements not resolved through

administrative or judicial proceedings are eligible for awards;

➢ Providing interpretive guidance of expected “independent analysis”; and

➢ Amendments to award determination process, allowing SEC to revise small

awards upward and clarify scope of SEC’s discretion in determining awards.

• Subject to challenge in Thomas v. SEC (D.D.C. 2021).

22DOJ FCPA Enforcement

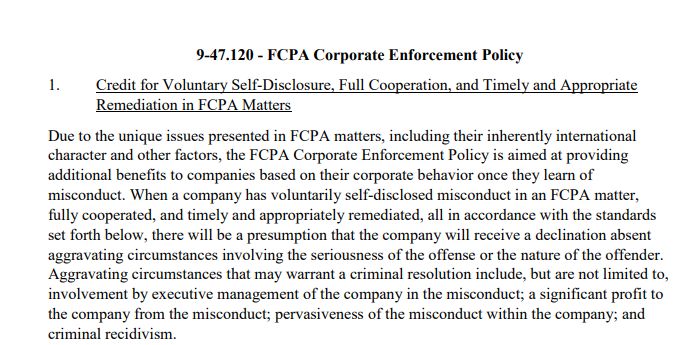

FrameworkDOJ FCPA Corporate Enforcement Policy

• Most recently updated in November 2019, DOJ’s FCPA Corporate Enforcement Policy

outlines the requirements for companies to receive credit for cooperation, disclosure,

and remediation in FCPA investigations.

To Qualify for a Presumption of Declination:

• Self-Disclosure, without aggravating circumstances

• Full Cooperation

• Timely and Appropriate Remediation

• Since 2016, there have been 14 declinations under this policy, including for World

Acceptance Corporation last year.

24DOJ FCPA Corporate Enforcement Policy

• Where a company (1) voluntarily self-discloses,

(2) fully cooperates, and (3) appropriately

remediates, DOJ will recommend a 50%

reduction off the low end of the USSG fine

range and generally not require a monitor.

• Even when a company does not voluntarily

disclose, full cooperation and appropriate

remediation will result in an up to 25%

reduction off the low end of the USSG fine

range.

Voluntary Self-Disclosure:

• Results in a “presumption that the company will receive a declination absent aggravating circumstances

involving the seriousness of the offense or the nature of the offender,” including involvement by

corporate executive management, significant profit, pervasive misconduct or criminal recidivism.

• Must occur “prior to an imminent threat of disclosure or government investigation” and reasonably

promptly after the company learns of the misconduct. The company must disclose all relevant facts.

25DOJ FCPA Corporate Enforcement Policy

• Full Cooperation: Maximum cooperation credit requires a series of actions

including:

➢ Timely disclosure of all facts relevant to the misconduct;

➢ Proactive, rather than reactive cooperation;

➢ Timely preservation, collection, and disclosure of relevant documents; and

➢ Making officers and employees available for interviews.

• Appropriate Remediation: Remediation requires a series of actions including:

➢ Thorough analysis of the causes underlying the conduct;

➢ Implementation of an effective compliance and ethics program;

➢ Discipline of employees; and

➢ Retention and non-destruction of business records.

26FCPA Trends and Enforcement

ActionsFCPA Trend 1: Blockbuster Penalties (2008 – 2020)

Millions

$3,000

$2,500

$2,000

$1,500

$1,000

$500

$0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

28Goldman Sachs - Facts

• In October 2020, Goldman Sachs reached a multi-billion dollar coordinated resolution in

connection with the 1MDB matter, making it the largest monetary corporate FCPA

resolution to date.

• U.S. authorities alleged that Goldman Sachs conspired with others to pay more than $1.6

billion to officials in Malaysia and Abu Dhabi to obtain and retain business for Goldman

Sachs from 1MDB, a Malaysian state-owned and state-controlled fund created to pursue

investment and development projects for the economic benefit of Malaysia and its people.

• Two Goldman Sachs former managing directors have also been charged in connection with

these allegations. One pled guilty to conspiring to launder money and to violate the FCPA,

and the other is awaiting trial on similar charges.

• The matter also involved coordination with the Money Laundering and Asset Recovery

Section and the DPA included self-reporting and compliance program requirements with

respect to anti-money laundering as well as anti-corruption.

29Goldman Sachs - Penalty

• Goldman agreed to pay more than $2.9 billion to criminal and civil authorities in the U.S., UK,

Singapore, and Hong Kong, PLUS $3.9 billion in penalities and disgorgement to Malaysian

authorities in connection with the 1MDB scandal.

• DOJ: A three-year Deferred Prosecution Agreement for an allegation of conspiracy to violate the

FCPA’s anti-bribery provisions and a $1,263,088,000 criminal penalty, after offsetting fines and

disgorgement paid to other regulators.

• SEC: A cease and desist order charging anti-bribery, books and records, and internal controls

violations, a $400 million civil penalty, and $606 million in disgorgement that was fully credited due

to the Malaysian settlement.

• Malaysia: $2.5 billion settlement and $1.4 billion in seized assets.

• Federal Reserve: $154 million

• New York State Department of Financial Services: $150 million

• UK Financial Conduct Authority/Prudential Regulation Authority: $63 million each

• Singaporean authorities: $122 million

• Hong Kong Securities and Futures Commission: $350 million

30Goldman Sachs – Penalty

31Goldman Sachs – Penalty

32Goldman Sachs – Penalty

• Goldman Sachs received a 10% cooperation discount off the bottom of fine range.

33Airbus - Facts

• In January 2020, Airbus agreed to pay a combined $3.9 billion

in penalties to the United States, France, and the UK for the

company’s alleged scheme to use third-party business partners

to bribe government officials to retain business.

• In the United States, Airbus entered into a DPA and agreed to pay $527 million

for violations of the FCPA and International Traffic in Arms Regulations (ITAR),

which requires disclosure of political contributions for certain defense sales.

• Airbus signed similar resolutions in the UK with the Serious Fraud Office

(“SFO”) and in France with the Parquet National Financier (“PNF”), agreeing to

pay $2.3 billion and $1.1 billion to those government enforcers, respectively.

• The resolution is the second largest global foreign bribery resolution.

34Airbus – Notable Jurisdictions

• The alleged conduct spanned at least 16 jurisdictions, with the DOJ, SFO, and

French CJIP splitting jurisdictions.

• UK • France • Saudi Arabia

• United States

• Malaysia • China • Taiwan

• China

• Sri Lanka • Colombia • Russia

• Taiwan • Nepal

• Indonesia • South Korea

• Ghana • UAE

35Airbus – Notable Observations

• FCPA Jurisdiction:

36Airbus – Notable Observations

• Anti-Piling On:

37Airbus – Notable Observations

• Forfeiture:

38FCPA Trend 2: The CFTC Dives into FCPA Waters

• In 2019, the CFTC published an advisory on self-reporting and cooperation for

“violations involving foreign corrupt practices” and announced its intent to bring

enforcement actions stemming from foreign bribery.

• Since then, several companies have announced investigations by the CFTC with a

potential foreign bribery nexus.

• On December 3, 2020, DOJ and CFTC announced their first coordinated foreign

corruption resolution with Vitol Inc., the U.S. affiliate of one of the world’s largest

energy trading firms.

• Vitol also entered into a leniency agreement with Brazilian authorities for the alleged

conduct.

39Vitol Inc.

• Vitol was alleged to have paid bribes to state oil companies in Brazil, Ecuador, and

Mexico to obtain preferential treatment, access to trades with the oil companies, and

confidential information, including specific prices at which Vitol understood it would

win a particular bid or tender.

➢Two former oil traders were also charged with FCPA and FCPA-related charges

for their roles in the alleged conduct.

• Vitol entered into a DPA with DOJ and agreed to a $135 million fine, with $45

million credit applied for payments to Brazil’s Federal Public Ministry.

• Vitol also consented to a cease-and-desist order by the CFTC for “manipulative and

deceptive conduct” under the Commodity Exchange Act and over $95 million in civil

penalties and disgorgement, with $67 million credit applied for the DOJ penalty.

40FCPA Trend 3: The Cautionary Tale of Beam Suntory

• In 2018, Beam Suntory entered into an agreement with the SEC to settle FCPA

allegations that senior executives at Beam Suntory’s Indian subsidiary directed efforts

by third parties to make improper payments to increase sales and facilitate

distribution, among other things.

➢$2 million civil penalty, $5,264,340 disgorgement, and $917,498 prejudgment

interest.

• In October 2020, Beam Suntory entered into a DPA with DOJ for the same general

conduct, with the lead corrupt payment allegation involving a ~$18,000 payment to a

senior government official in exchange for a license.

➢$19,572,885 fine, with no credit for the SEC resolution.

➢DOJ did not provide Beam Suntory with voluntary disclosure credit or with full

cooperation or full remediation credit.

41FCPA Trend 3: The Cautionary Tale of Beam Suntory

42FCPA Trend 4: No Monitorships

Monitors in Corporate FCPA Enforcement Actions (2016-2020)

9

8

7

6

5

4

3

2

1

0

2016 2017 2018 2019 2020

External Monitor Hybrid Monitor

43Sargeant Marine - Facts

Recent

• On September 22, 2020, Sargeant Marine Inc. (“SMI”),

a Florida-based asphalt company, pleaded guilty to conspiring

to violate FCPA anti-bribery provisions.

• SMI is alleged to have bribed foreign officials in Brazil,

Venezuela, and Ecuador between 2010 and 2018 with the

purpose of obtaining contracts with oil companies.

➢ The allegations involve consulting agreements to funnel bribes to government

officials and state-owned oil company executives and commissions to offshore

bank accounts controlled by intermediaries.

➢ According to DOJ, co-conspirators communicated using draft emails, which they

would edit and save in a U.S.-based shared email account.

➢ DOJ alleged that SMI and affiliated companies earned profits of approximately

$26.5 million from alleged conduct in Brazil; $8.2 million in Venezuela; and $3.2

million in Ecuador.

44Sargeant Marine - Penalty

Recent

• The Sentencing Guidelines penalty range was between $120 million and $240

million.

• SMI and DOJ agreed that the appropriate criminal penalty was $90 million, which

reflected a 25% discount off the bottom of the applicable sentencing range for full

cooperation and remediation.

➢ SMI did not receive voluntary disclosure credit.

• After demonstrating an inability to pay, SMI and DOJ ultimately agreed to reduce its

criminal fine by more than $73 million to a fine of $16.6 million over eight months.

• SMI also agreed to self-report to DOJ for three years regarding the company’s

remediation and corporate compliance program.

45Sargeant Marine - Penalty

Recent

• SMI received full cooperation credit for:

➢ Conducting a thorough internal investigation;

➢ Promptly meeting requests from DOJ;

➢ Proactively identifying issues and facts likely to be of interest to DOJ;

➢ Making factual presentations;

➢ Producing relevant documents; and

➢ Voluntarily making foreign-based employees available.

46Sargeant Marine – Notable Observations

Recent

• Inability to Pay:

47Sargeant Marine – Notable Observations

Recent

• Remedial Measures and No Monitorship:

48Sargeant Marine – Notable Observations

Recent

• Shell Companies, Consultants, & Due Diligence:

49FCPA Trend 5: International Coordination and Focus in

Latin America

50J&F Investimentos - Facts

Recent

• In October, DOJ and SEC announced a combined $155 million FCPA resolution with

Brazil-based holding company J&F Investimentos S.A. and its affiliated global meat

and protein producer and ADR-issuer, JBS, S.A.

• J&F pleaded guilty to conspiracy to violate the FCPA’s anti-bribery provisions based on

allegations that over many years, millions in payments were made to high-level

Brazilian officials to obtain hundreds of millions of dollars of financing and an

approval for a corporate merger.

• The SEC charged JBS and two of its executives under the accounting provisions.

• J&F had previously entered into a settlement with Brazilian authorities for $3.2 billion.

51J&F Investimentos - Penalty

Recent

• DOJ: $256,497,026 fine, reduced to $128,248,513 after applying credit for payments

to resolve the matter in Brazil.

➢ Self-reporting at least annually, for three years.

➢ Partial cooperation credit

52J&F Investimentos - Penalty

Recent

• SEC: $26.8 million in disgorgement for conduct by J&F, JBS, and two executives for internal controls

and books and records violations related to Pilgrim’s Pride Corporation.

➢ J&F Investimentos, S.A. is a private company, but the SEC settled with it for conduct related to

the issuers.

➢ JBS is a J&F subsidiary, and it is a US issuer because its Brazilian shares are listed on a U.S.

exchange as ADRs.

➢ The executives who resolved with the SEC had already pleaded guilty in Brazil.

➢ The legal violation the SEC focused on related to the internal controls and books and records of

Pilgrim’s Pride, a relatively new subsidiary acquired by a U.S. subsidiary of JBS.

▪ The SEC’s consent order described that Pilgrim’s Pride did not engage in any intentional

misconduct, but its funds were mixed up with JBS’s funds, which did engage in misconduct.

Pilgrim’s Pride’s books and records did not reflect this fact, and its controls did not prevent

it.

▪ And so, the SEC brought an action against J&F, a private company, JBS, a Brazilian issuer,

and Brazilian executives who had pleaded guilty in Brazil, for causing accounting violations

to Pilgrim’s Pride and did not bring an action against Pilgrim’s Pride.

▪ This may be a first for the SEC.

53J&F – Notable Observations

Recent

• New Corporate Compliance Program Requirements

54J&F – Notable Observations

Recent

• New Corporate Compliance Program Requirements

55J&F – Notable Observations

Recent

• New Corporate Compliance Program Requirements

56J&F – Notable Observations

Recent

• New Corporate Compliance Program Requirements

57J&F – Notable Observations

Recent

• New Corporate Compliance Program Requirements

58J&F – Notable Observations

Recent

• New Corporate Compliance Program Requirements

59J&F – Notable Observations

Recent

60J&F – Notable Observations

Recent

61FCPA Trend 6: Intersection Between Anti-Corruption,

AML, Antitrust, and Trade Sanctions

Recent cases show that prosecutors are increasingly combining corruption charges with other criminal

offenses

AML: U.S. authorities continue

Trade Sanctions: In addition to AML: An Indonesian court

to prosecute former Venezuelan

FCPA charges, Airbus entered into convicted Emirsyah Satar, former

officials and their co-conspirators

a deferred prosecution agreement CEO of Garuda Indonesia,

involved in public corruption

with the DOJ to resolve Indonesia’s state-owned airline,

schemes using anti-money

allegations of conspiracy to of corruption and money

laundering laws. In 2020, DOJ

violate the Arms Export Control laundering after finding that he

brought money laundering

Act and the International Traffic received bribes from Airbus and

charges against former National

in Arms Regulations. DOJ Rolls-Royce in exchange for

Treasurer of Venezueala Claudia

alleged that the company made procurement contracts for aircraft

Patricia Diaz Guillen and her

false reports to the U.S. and aircraft parts. Satar was

huband. Diaz Guillen’s

government to facilitate the sale sentenced to eight years in prison

predecessor at the Treasury also

or export of defense articles and and ordered to pay a fine of USD

pleaded guilty to money

services. 1.4 million.

laundering charges.

• We have also seen intersections between FCPA and antitrust.

62Mitigation: Coordinate Your Compliance Program

and Disclosure Strategy

It’s not just the FCPA!

• Compliance programs should account for global compliance standards, not just the FCPA.

• In the Airbus matter, U.S. authorities also alleged violations of the Arms Export Control Act (“AECA”)

and its implementing regulations, the International Traffic in Arms Regulations (“ITAR”).

Voluntary Self-Disclosure Should be a Carefully Considered Decision, Part of a

Coordinated Global Strategy

• The Goldman Sachs and Airbus actions reflect that Coordination is Key

regulators expect self-disclosure, particularly in matters of In 2020, Beam Suntory did not receive

this scope, and that self-disclosure should be considered credit from the DOJ for settlement

amounts paid to the SEC to resolve

as part of a coordinated global strategy. charges based on the same conduct

• Airbus disclosed the AECA and ITAR conduct to DOJ in a because, according to the DOJ, Beam

did not seek a parallel resolution.

“timely” manner, but disclosed FCPA issues only after it

had disclosed to the UK’s SFO. Remember that coordinating voluntary

disclosure, cooperation, and settlement

• DOJ specifically noted in its settlement with Goldman negotiations with multiple enforcement

Sachs that it had “reached this resolution with Goldman agencies, including with non-U.S.

based on a number of factors, including the Company’s regulators, may yield benefits.

failure to voluntarily disclose the conduct to the

Department[.]”

63FCPA Trend 7: Focus on Compliance, Controls, and

Internal Audit

• In legislation, regulations and enforcement/prosecution decisions, authorities are

increasingly emphasizing the need for a well-developed compliance program.

• As recent landmark U.S. enforcement actions show, authorities will not credit

companies for having internal conrols if they are easily circumvented. On the other

hand, they have shown a willingness to credit the state of a compliance program after

remediation following the discovery of misconduct.

• Recent FCPA enforcement actions have also highlighted the importance of Internal

Audit and the need to address issues uncovered by auditors.

64Cardinal Health – Facts

• In February 2020, U.S.-based pharmaceutical company Cardinal Health, Inc. entered

into a cease-and-desist order with the SEC to resolve charges under the internal

accounting controls and recordkeeping provisions of the FCPA.

• The settlement arises out of charges that Cardinal Health’s internal accounting controls

were not sufficient to detect improper payments made by employees of its former

Chinese subsidiary.

➢ The order states that Cardinal China employees, who were marketing products for

the benefit of a European company with whom Cardinal had a profit sharing

agreement, directed payments to government-employed healthcare professionals and

employees of state-owned retail companies who had influence over purchasing

decisions.

65Cardinal Health – Penalty

• Penalty amount: $2.5 million civil penalty, and $5.4 million in disgorgement.

• Cardinal voluntarily disclosed the results of its internal investigation and significantly

cooperated in the SEC’s investigation.

• Cardinal China undertook significant remedial measures including:

➢Terminating the marketing accounts and employment contracts with marketing

employees;

➢Adding anti-bribery representations and obligations to relevant contracts; and

➢Strictly limiting the use of the remaining balance of the European company’s

funds to low risk expenses with robust controls and monitoring over their

payment.

66Cardinal Health – Notable Observations

• Acquisition and Integration Risks:

67Cardinal Health – Notable Observations

• Focus on Compliance, Controls, and Internal Audit:

68Cardinal Health – Notable Observations

• Healthcare Focus: Several U.S. and foreign anti-corruption enforcement actions of

late have involved the healthcare sector.

69Eni S.p.A. – Facts

• In April 2020, Italian multinational oil and gas company Eni S.p.A. entered into a

cease-and-desist order with the SEC to resolve charges under FCPA’s books and

records and internal accounting controls provisions.

• The settlement arises out of allegations that Eni’s subsidiary, Saipem S.p.A., which it

held a 43% interest in, made payments to an intermediary who “directed at least a

portion of that money through offshore shell entities to Algerian officials or their

designees.” Saipem was awarded at least 7 projects during the relevant time period

from Algeria’s state-owned oil company.

➢ The allegations involve executive conduct.

• The cease-and-desist order found that a senior executive at Saipem orchestrated the

scheme, and continued to facilitate Saipem’s improper payments after he was hired to

be CFO of Eni.

70Eni S.p.A. – Penalty

• Penalty: $19.75 million in disgorgement, and $4.75 million in prejudgment interest.

• The SEC considered the remedial efforts and cooperation, including:

➢ Compiling financial data and analysis of the transactions at issue;

➢ Making substantive presentations; and

➢ Providing translations of key documents and foreign proceedings.

• In 2010, Eni settled another FCPA matter with the SEC, based on bribery conduct by its

then-wholly owned Dutch subsidiary Snamprogetti Netherlands, B.V.

71Eni S.p.A. – Notable Observations

• Minority interest risks and executive involvement impact:

72Eni S.p.A. – Notable Observations

• Third Parties and Due Diligence:

73Mitigation: Establish An Effective Corporate

Compliance Program

DOJ Criminal Division Updated Guidance

Key Takeaways

▪ Starting with a Risk Assessment: A company’s compliance program should be based on the result of a

risk assessment to ensure that the program is appropriately tailored.

▪ Building on Lessons Learned: The risk profile should be “periodically updated,” and the program should

be reexamined and revised on an ongoing basis in light of lessons learned.

▪ Importance of Compliance: A number of factors are considered, such as where within the company the

compliance function is housed and how the compliance function compares with other functions in terms of

stature, compensation, rank/title, reporting lines, resources, and access to key decision-makers.

▪ Responsibility for Third Parties: The 2020 update places increased focus on a company’s third-party

oversight. DOJ will consider whether a company has appropriate business rationale for third parties. It

will also consider the process for supplier selection and for ensuring third parties cannot be re-engaged

without appropriate authorization once terminated.

▪ Cascading Tone from the Top: Emphasizes a “culture of compliance.” Messaging from the top is

inadequate. DOJ will consider cultural leadership by middle management and whether managers were

held accountable for misconduct that occurred under their supervision.

74Mitigation: Collaboration Between Internal Audit,

Legal, and Compliance Functions

Consider whether audits should be conducted with legal oversight when sensitive topics are

at issue

• Involve the legal department if an audit addresses compliance with the law.

➢ Implement a policy with defined escalation steps, particularly where involving indicia of fraud,

corruption, or other legal violations.

➢ Include compliance- and corruption-related areas in your company’s regular audit rhythm.

Consider implementing best practices for a working relationship between internal audit,

legal, and compliance

• Confirm Legal direction and the scope of the review in a formal communication.

• Keep audit issue summaries and reports strictly factual. Avoid conclusions especially when referring the

matter to another group, i.e. compliance.

• Use precise wording in audit reports.

➢ Avoid sweeping or overly broad statements. Words on legal exposure, risk, and liability can be taken

out of context.

➢ Be clear about if/when findings are limited.

• Label documents appropriately. When a document contains information that is confidential, proprietary,

or privileged, mark it as such. Documents not in final form should be labeled as drafts.

• Ensure that remedial steps are practical and workable, and there is a process to follow through on any

action items.

75FCPA Trend 8: Third Parties Remain The Greatest Area

of Corruption Risk

• Third parties continue to pose the greatest FCPA

risk and feature in enforcement actions.

• It is estimated that over 90% of reported FCPA

matters involve third parties.

• Third parties often handle a wide range of services

and activities that can create additional compliance

risks, such as:

➢Participation in government tenders for state-

owned customers;

➢Handling licensing or other regulatory permits

required to distribute products in other countries;

and

➢Handling customs formalities for the import of

products, warehousing, or inventory management.

76Alexion Pharmaceuticals - Facts

Recent

• On July 2, 2020 Boston-based Alexion Pharmaceuticals

(“Alexion”) agreed, without admitting or denying the SEC’s

allegations, to pay more than $21 million to resolve charges

that it violated the FCPA books-and-records and internal accounting controls

provisions.

• The SEC alleged that from 2010 to 2015, Alexion’s Turkish subsidiary bribed Turkish

government officials in order to obtain approval for patient prescriptions and secure

favorable regulatory treatment for its drug, Soliris, and that from 2011 to 2015,

Alexion’s Russian subsidiary did the same with respect to Russian government health

care officials.

• The SEC further alleged that Alexion’s subsidiaries in Brazil and Colombia created, or

directed third parties to create, inaccurate financial records.

77Alexion Pharmaceuticals - Penalty

Recent

• Penalty: $14,210,194 in disgorgement and $3,766,337 in prejudgment interest, as well

as a $3.5 million civil penalty.

• The SEC considered Alexion’s remediation and cooperation in finalizing the terms of

the order.

• Cooperation included:

➢ Regular briefings to the SEC regarding findings from its internal investigation;

➢ Forensic accounting review; and

➢ Identifying and providing translations of key documents.

78Alexion Pharmaceuticals - Penalty

Recent

• Remediation included:

➢ Strengthening and expanding its global compliance organization;

➢ Enhancing policies and procedures regarding payments to third parties, including

the implementation of a centralized system to track and monitor third-party

payments;

➢ Revamping its HCP engagement process and oversight;

➢ Enhancing its internal audit function;

➢ Conducting proactive compliance market review; and

➢ Improving anti-corruption training.

79Alexion Pharmaceuticals – Notable Observations

Recent

• Third Parties: This resolution reflects the SEC’s continued focus on

interactions with third parties as areas ripe for FCPA compliance issues.

Looking beyond Alexion’s own direct handling of its books and records,

the order alleged that Alexion’s subsidiaries in Brazil and Columbia

directed third parties to create inaccurate records regarding payments to

patient advocacy organizations.

80Alexion Pharmaceuticals – Notable Observations

Recent

• Geographic Risk and Adequate Diligence and Documentation

81Alexion Pharmaceuticals – Notable Observations

Recent

• “Other” Conduct Captured

82Mitigation: Carefully Monitor High-Risk Third

Parties

Third parties are an inevitable part of doing business in an emerging market. Pre-

engagement screening, as well as close monitoring, can help offset the decreased

transparency and control that comes with agents and intermediaries.

BEST PRACTICES

• Identify the specific functions that are prone to corruption and handled by third parties.

• Involve legal and compliance in contract negotiations/drafting to ensure that services are specifically and

accurately described and allow for an efficient control (e.g., finance) to assess whether the services have

actually been rendered and whether prices are reasonable in light of those services and are in line with

market rates.

• Include audit rights with a trigger in third-party agreements to allow for audits when indicated.

• Conduct specific training for employees working with third parties and with end customers.

• Use a risk-based approach to periodically select third parties for an audit review.

• Ensure that rebates, credit notes, and other payments provided to the third party are made to the

contracting entity, including identifying any offshore arrangements.

• Understand interaction between sales force in emerging markets, involved third parties (e.g., distributors,

agents) and end-customers, and conduct function-specific compliance training with these employees.

• Understand whether margins of intermediaries are passed on to end-customers by reviewing publically

available tender materials or conducting audit reviews.

83FCPA Trend 9: Continued Focus on Individual

Enforcement Actions

PDVSA Individuals - Background and Notable Developments

• In August 2020, the latest in a line of Venezuela

state-owned energy company PDVSA employees

was charged under the FCPA and certain money

laundering statutes.

• Jose Luis De Jongh Atencia, a dual U.S.-Venezuelan citizen, was a procurement

officer and manager in Citgo’s Special Projects group, and was charged with accepting

$2.5 million in bribes in exchange for business with Citgo and PDVSA.

• FCPA Jurisdiction: PDVSA employees like Atencio, and others, including citizens of

Venezuela and Switzerland, have been considered “foreign officials” under the FCPA.

This includes those acting on behalf of PDVSA’s U.S.-based companies, such as

Citgo.

• Wide Ranging Investigation: The PDVSA investigation, parallel to other diplomatic

and prosecutorial U.S. pressure on Venezuela in recent years, has resulted in charges

against 27 individuals, 20 of whom have pleaded guilty.

84FCPA Trend 9: Continued Focus on Individual

Enforcement Actions

Alstom Employees - Background and Notable Developments

• In February 2020, two former executives of French

power company Alstom were charged (in an

unsealed, superseding indictment) with violating

the FCPA and committing certain money laundering offenses.

• Reza Moenaf (former president of Alstom’s subsidiary in Indonesia) and Eko Sulianto

(former director of that subsidiary) were both alleged to have paid bribes via external

consultants to high-level Indonesian officials in exchange for assistance in securing a

$118 million contract for Alstom’s US and Indonesia subsidiaries.

• FCPA Jurisdiction: The indictment asserted that Moenaf and Sulianto were both

agents of a “domestic concern”—Alstom’s U.S. subsidiary--under the FCPA for their

role in securing contracts that Alstom Power US would benefit from.

• Wide Ranging Investigation: This prosecution dates back to the 2013 FCPA action

against Alstom, which includes the Hoskins Second Circuit case.

85Panelists

F. Joseph Warin

1050 Connecticut Avenue, N.W., Washington, DC 20036-5306 USA

TEL:+1 202.887.3609

fwarin@gibsondunn.com

F. Joseph Warin is chair of the 200-person Litigation Department of Gibson Dunn’s Washington, D.C. office, and he is co-chair of the firm’s global White Collar Defense and

Investigations Practice Group. Mr. Warin’s practice includes representation of corporations in complex civil litigation, white collar crime, and regulatory and securities

enforcement – including Foreign Corrupt Practices Act investigations, False Claims Act cases, special committee representations, compliance counseling and class action civil

litigation.

Mr. Warin is continually recognized annually in the top-tier by Chambers USA, Chambers Global, and Chambers Latin America for his FCPA, fraud and corporate investigations

expertise. Who’s Who Legal named Mr. Warin a “Global Elite Thought Leader” in its 2020 and 2019 Investigations guides list for Business Crime Defense – Corporate and

Investigations. In 2020, Mr. Warin was selected by Chambers USA as a “Star” in FCPA, a “Leading Lawyer” in the nation in Securities Regulation: Enforcement, and a “Leading

Lawyer” in the District of Columbia in Securities Litigation and White Collar Crime and Government Investigations. In 2017, Chambers USA honored Mr. Warin with the

Outstanding Contribution to the Legal Profession Award, calling him a “true titan of the FCPA and securities enforcement arenas.” He has been listed in The Best Lawyers in

America® every year from 2006 – 2020 for White Collar Criminal Defense. U.S. Legal 500 has repeatedly named him as a “Leading Lawyer” for Corporate Investigations and White

Collar Criminal Defense Litigation. He has been recognized by Benchmark Litigation as a U.S. White Collar Crime Litigator “Star” for nine consecutive years (2011-2019), and was

named to Securities Docket’s “Enforcement 40” for 2017. In 2020, Mr. Warin was also named a Leading Individual by Legal 500 Latin America in a new category, “International

Firms: Compliance and Investigations. In 2019, Latinvex named Mr. Warin one of Latin America’s Top 100 Lawyers in the category of FCPA & Fraud. In 2018, Washingtonian

Magazine named Mr. Warin as one of Washington’s “Top Lawyers” in White Collar Criminal Defense. BTI Consulting named Mr. Warin to its 2017 “BTI Client Service All-Stars”

List.

Mr. Warin’s group was recognized by Global Investigations Review in 2020 as the leading global investigations law firm in the world. This is the fifth time in six years to be so

named. Global Investigations Review reported that Mr. Warin has now advised on more FCPA resolutions than any other lawyer since 2008. In 2016 Who’s Who Legal and Global

Investigations Review named Mr. Warin to their list of World’s Ten-Most Highly Regarded Investigations Lawyers based on a survey of clients and peers, noting that he was one of

the “most highly nominated practitioners,” and a “’favourite’ of audit and special committees of public companies.” Best Lawyers® named Mr. Warin the Lawyer of the Year in

2020 and in 2016 for White Collar Criminal Defense in the District of Columbia, and he was named among the Lawdragon 500 Leading Lawyers in America in 2016.

Mr. Warin has handled cases and investigations in more than 40 states and dozens of countries. His clients include corporations, officers, directors and professionals in regulatory,

investigative and trials involving federal regulatory inquiries, criminal investigations and cross-border inquiries by dozens of international enforcers, including UK’s SFO and FCA,

and government regulators in Germany, Switzerland, Hong Kong, and the Middle East. His credibility at DOJ and the SEC is unsurpassed among private practitioners – a reputation

based in large part on his experience as the only person ever to serve as a compliance monitor or counsel to the compliance monitor in three separate FCPA monitorships,

pursuant to settlements with the SEC and DOJ: Statoil ASA (2007-2009); Siemens AG (2009-2012); and Alliance One International (2011-2013). He has been hired by audit

committees or special committees of public companies to conduct investigations into allegations of wrongdoing in a wide variety of industries including energy, oil services,

financial services, healthcare and telecommunications.

87Patrick Stokes

1050 Connecticut Avenue, N.W., Washington, D.C. 20036-5306

Tel: +1 202.955.8504

PStokes@gibsondunn.com

Patrick Stokes is a litigation partner and a member of the firm's White Collar Defense and Investigations, Securities Enforcement, and Litigation Practice

Groups.

Mr. Stokes' practice focuses on internal corporate investigations, compliance reviews, government investigations, and enforcement actions regarding

corruption, securities fraud, and financial institutions fraud. He has tried more than 30 federal jury trials as first chair, including high-profile white-collar

cases, and handled 16 appeals before the U.S. Court of Appeals for the Fourth Circuit. Mr. Stokes is equally comfortable leading confidential internal

investigations, negotiating with government enforcement authorities, or advocating in court proceedings. Mr. Stokes is ranked nationally and globally by

Chambers USA and Chambers Global as a leading attorney in FCPA.

Prior to joining Gibson Dunn, Mr. Stokes spent nearly 18 years with the U.S. Department of Justice (DOJ). From 2014 to 2016 he headed the FCPA Unit,

managing the DOJ's FCPA enforcement program and all criminal FCPA matters throughout the United States, covering every significant business sector, and

including investigations, trials, and the assessment of corporate anti-corruption compliance programs and monitorships. Mr. Stokes also served as the DOJ’s

principal representative at the OECD Working Group on Bribery working with law enforcement and policy setters from 41 signatory countries on anti-

corruption enforcement policy issues.

From 2010 to 2014, he served as Co-Chief of the DOJ's Securities and Financial Fraud Unit. In this role, he oversaw investigations and prosecutions of

financial fraud schemes involving accounting fraud, benchmark interest rate manipulations, insider trading, market manipulation, Troubled Asset Relief

Program (TARP) fraud, government procurement fraud, and large-scale mortgage fraud, among others.

From 2002 to 2008, Mr. Stokes served as an Assistant United States Attorney in the Eastern District of Virginia, where he prosecuted a wide variety of

financial fraud, immigration, and violent crime cases. From 1998 to 2002, he served in the DOJ's Tax Division as a trial attorney in the Western Criminal

Enforcement Section.

Mr. Stokes received various awards while at the DOJ, including the Attorney General's Distinguished Service Award in 2013 and 2014 and the Assistant

Attorney General's Exceptional Service Award (Criminal Division) in 2011 and 2014.

88John W.F. Chesley

1050 Connecticut Avenue, N.W., Washington, DC 20036-5306 USA

TEL:+1 202.887.3788

jchesley@gibsondunn.com

John Chesley is a litigation partner in Gibson Dunn’s Washington, D.C. Office. He focuses his practice on white collar criminal enforcement and

government contracts litigation. He represents corporations, audit committees, and executives in internal investigations and before government agencies

in matters involving the Foreign Corrupt Practices Act, procurement fraud, environmental crimes, securities violations, sanctions enforcement, antitrust

violations, and whistleblower claims. He also has significant trial experience and appears regularly in federal and state courts and administrative tribunals

throughout the Washington Metropolitan Region and nationwide.

Among his recent engagements, Mr. Chesley served as the Interim Chief Ethics & Compliance Officer of a publicly-traded, multi-national corporation,

responsible for managing a global team of compliance personnel. In this role, Mr. Chesley conducted and oversaw internal investigations, managed a

whistleblower hotline, provided compliance advice, created and updated compliance policies, and administered compliance training for tens of thousands

of employees worldwide. This opportunity provided Mr. Chesley with first-hand insights into the day-to-day challenges experienced by in-house counsel,

which he uses to bring practical solutions to the table for all of his clients.

Mr. Chesley has been recognized repeatedly as one of the leading lawyers of his generation. Specifically, he was named one of the “world’s leading young

investigations specialists” by Global Investigations Review “40 Under 40,” as well as a “Rising Star” in the Government Contracts field by Law 360. Most

recently, Mr. Chesley was recognized by Benchmark Litigation as a “Future Litigation Star” in Washington, D.C. (2019) and by Who’s Who Legal

Investigations guide as a “Future Leader” in Investigations (2018). The National Law Journal named Mr. Chesley to its list of 2015 D.C. Rising Stars, noting

his white-collar defense practice and pro bono work, and Legal Bisnow identified him as one of “Washington’s 2015 Trending 40 Lawyers Under 40.” Mr.

Chesley also has been recognized as a “Rising Star” by LMG 500 (2015-2018) and Washington DC Super Lawyers (2014-2018).

Mr. Chesley publishes and speaks regularly on legal developments, particularly involving the FCPA. In addition, he is frequently quoted in print

publications such as Bloomberg BNA, Compliance Week, Corporate Counsel, Global Investigations Review, Law 360, The FCPA Report, and SEC Today and

has appeared as a legal commentator on the Fox News Channel.

89You can also read