Results for Q2 2020 - Barrick Gold Corporation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Results for Q2 2020…

Cautionary Statement on Forward Looking Information Certain information contained or incorporated by reference in this presentation, including any information as to our strategy, projects, plans or future financial or operating performance, constitutes “forward-looking statements”. All statements, other than statements of historical fact, are forward-looking statements. The words “expect”, “target”, “plan”, “project”, “goal”, “continue”, “budget”, “estimate”, “potential”, “may”, “will”, “can”, “could”, “would”, “should” and similar expressions identify forward-looking statements. In particular, this presentation contains forward-looking statements including, without limitation, with respect to: Barrick’s forward-looking production guidance and estimates of future costs; cash flow forecasts; projected capital, operating and exploration expenditures; Barrick’s engagement with local communities to manage the Covid-19 pandemic; future investments in community projects and contributions to local economies; Barrick’s response to the government of Papua New Guinea’s decision not to extend Porgera’s Special Mining Lease; the duration of the temporary suspension of operations at Porgera; our goals with respect to environmental, health and safety certifications for our operating mines; mine life and production rates; estimated timing for development of projects, including Goldrush, Turquoise Ridge underground third shaft, Gounkoto underground project and Zaldivar Chloride Leach Project; timing of resumption of mining operations at Bulyanhulu; our pipeline of high confidence projects at or near existing operations; potential for existing or newly acquired and/or developed assets to become Tier One gold assets; potential extensions to life of mine; potential exploration targets and potential mineralization and metal or mineral recoveries; our ability to convert resources into reserves; our project pipeline and results of our greenfield and brownfield exploration work; our non-core asset disposition strategy; and expectations regarding future price assumptions, financial performance and other outlook or guidance. Forward-looking statements are necessarily based upon a number of estimates and assumptions including material estimates and assumptions related to the factors set forth below that, while considered reasonable by the Company as at the date of this presentation in light of management’s experience and perception of current conditions and expected developments, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements and undue reliance should not be placed on such statements and information. Such factors include, but are not limited to: fluctuations in the spot and forward price of gold, copper or certain other commodities (such as silver, diesel fuel, natural gas and electricity); the speculative nature of mineral exploration and development; changes in mineral production performance, exploitation and exploration successes; risks associated with projects in the early stages of evaluation and for which additional engineering and other analysis is required; timing of receipt of, or failure to comply with, necessary permits and approvals, including the non-renewal of Porgera’s Special Mining Lease; the benefits expected from recent transactions being realized, including Nevada Gold Mines; diminishing quantities or grades of reserves; increased costs, delays, suspensions and technical challenges associated with the construction of capital projects; operating or technical difficulties in connection with mining or development activities, including geotechnical challenges and disruptions in the maintenance or provision of required infrastructure and information technology systems; failure to comply with environmental and health and safety laws and regulations; uncertainty whether some or all of Barrick's targeted investments and projects will meet the Company’s capital allocation objectives and internal hurdle rate; the impact of global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future cash flows; adverse changes in our credit ratings; the impact of inflation; fluctuations in the currency markets; changes in U.S. dollar interest rates; risks arising from holding derivative instruments; changes in national and local government legislation, taxation, controls or regulations and/or changes in the administration of laws, policies and practices, expropriation or nationalization of property and political or economic developments in Canada, the United States and other jurisdictions in which the Company or its affiliates do or may carry on business in the future; lack of certainty with respect to foreign legal systems, corruption and other factors that are inconsistent with the rule of law; risks associated with illegal and artisanal mining; risks associated with new diseases, epidemics and pandemics, including the effects and potential effects of the global Covid-19 pandemic; disruption of supply routes which may cause delays in construction and mining activities; damage to the Company’s reputation due to the actual or perceived occurrence of any number of events, including negative publicity with respect to the Company’s handling of environmental matters or dealings with community groups, whether true or not; the possibility that future exploration results will not be consistent with the Company’s expectations; risks that exploration data may be incomplete and considerable additional work may be required to complete further evaluation, including but not limited to drilling, engineering and socioeconomic studies and investment; risk of loss due to acts of war, terrorism, sabotage and civil disturbances; litigation and legal and administrative proceedings; contests over title to properties, particularly title to undeveloped properties, or over access to water, power and other required infrastructure; business opportunities that may be presented to, or pursued by, the Company; risks associated with the fact that certain of the initiatives described in this presentation are still in the early stages and may not materialize; our ability to successfully integrate acquisitions or complete divestitures, including our ability to successfully reintegrate Acacia’s operations; risks associated with working with partners in jointly controlled assets; employee relations including loss of key employees; increased costs and physical risks, including extreme weather events and resource shortages, related to climate change; and availability and increased costs associated with mining inputs and labor. Barrick also cautions that its 2020 guidance and ten year plan may be impacted by the unprecedented business and social disruption causes by the spread of Covid-19. In addition, there are risks and hazards associated with the business of mineral exploration, development and mining, including environmental hazards, industrial accidents, unusual or unexpected formations, pressures, cave-ins, flooding and gold bullion, copper cathode or gold or copper concentrate losses (and the risk of inadequate insurance, or inability to obtain insurance, to cover these risks). Many of these uncertainties and contingencies can affect our actual results and could cause actual results to differ materially from those expressed or implied in any forward-looking statements made by, or on behalf of, us. Readers are cautioned that forward-looking statements are not guarantees of future performance. All of the forward-looking statements made in this presentation are qualified by these cautionary statements. Specific reference is made to the most recent Form 40-F/Annual Information Form on file with the SEC and Canadian provincial securities regulatory authorities for a more detailed discussion of some of the factors underlying forward-looking statements and the risks that may affect Barrick’s ability to achieve the expectations set forth in the forward-looking statements contained in this presentation. We disclaim any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

Covid-19…focus on our employees

and communities

Focus during the Covid-19 outbreak on health and safety of our workforce and communities: proactive

response, preparedness, prevention and communication

Engaged with our host authorities, communities and employees as a supportive partner providing

Medical supplies and equipment for local clinics

Isolation centres

Support to communities

Provision of food parcels and other essentials for vulnerable groups such as the elderly, those with pre-

existing medical issues, school children and indigenous peoples

Setting up funds to help drive and support economic recovery for impacted local businesses

In Latin America – focus on infrastructural and equipment needs

In Africa – emphasis on improving existing healthcare facilities and capacity

Financial donations were conditional on government partnership and clear deliverables overseen by

Barrick management and also included sourcing equipment and supplies

Over $20 million contributed by the company in support of our host countries and communities in

Covid-19 infection prevention

Health & Safety…

Lost Time Injury Frequency Rate & Total Recordable

Injury Frequency Rate

LTIFR1 decreases by 16% quarter on 3.0

2.75

quarter; Total Recordable Injuries also

decreased from Q1 2.5

2.18 2.23

TRIFR2 1.65 in line with Q1

2.0 1.86

YTD LTIFR of 0.30 and TRIFR of 1.64; 1.64 1.65

significantly down from the same period in 1.5

2019 (LTIFR of 0.57 and TRIFR of 2.46)

1.0

0.61

0.52 0.47

0.5 0.41

0.32 0.27

0.0

Q1 19 Q2 19 Q3 19 Q4 19 Q1 20 Q2 20

LTIFR TRIFR Linear (LTIFR) Linear (TRIFR)

Environment…

Zero Class 1 (high severity)

environmental incidents3

Improvement in water reuse and

recycling rate – 78% in Q2; 77% year to

date

Quisqueya Power Plant,

Reduction in CO2 emissions quarter on Dominican Republic –

quarter – driven by conversion of the natural gas power generation

was fully operational in Q2

Quisqueya Power Plant in the Dominican

Republic from HFO to natural gas and Kibali, DRC – battery power

introduction of battery technology for grid installed for grid stabilisation

stabilisation at Kibali

Barrick on track to achieve its goal of

certifying all operational mines to

ISO 14001:2015 by the end of 2020

Community…

+$8.8 million YTD community development investment on top

of Covid-19 community related support

Covid-19 related community support > $20 million

Plus $1 billion spent at operational sites on local and national

procurement of goods and services

Western Shoshone Scholarship Foundation – Western Shoshone Scholarship Foundation –

2020 graduation reception held during the quarter 2020 Graduation Reception - Nevada

Total amount of $26 million committed by NGM to the fund

in support of education of Native American youth creating

employment opportunities

Reusable face masks issued to employees across Barrick’s

Africa and Middle East operations - proudly sourced from

members within our local communities providing a sustainable

source of income – to date approximately 50,000 reusable

face masks sourced from local community suppliers

Kakola Village tailor - Tanzania

Barrick…Q2 2020 KPIs Continued solid performance positions Barrick well within annual production guidance, despite Covid-19 challenges Improvement in safety management following increased focus Strong cash generation highlights quality of assets and leverage to gold price Barrick continues to be vigilant in its approach to contain the impact of Covid-19 Higher gold prices also result in higher royalty payments and costs Strong operating performance for copper with costs per pound at lower end of the guidance range Operating Cash Flow in excess of $1.0 billion and Free Cash Flow4 greater than $0.5 billion for the quarter Net debt down almost 25% to $1.4 billion with no significant maturities until 2033 Net earnings per share of 20 cents; adjusted net earnings per share5 up 44% to 23 cents for the quarter Strong operating performance from Tier One6 assets, with PV production impacted by planned maintenance shutdown Veladero production impacted by Argentina's Covid-19 movement and social distancing restrictions 30% of stockpiled concentrate shipped from Tanzania and first $100 million paid to Government Agreement reached in Mali to extend Loulo convention to 2038 Significant exploration drill results from Nevada, Dominican Republic, Mali and Tanzania PV expansion, Goldrush development, Turquoise Ridge shaft and other key projects remain on track despite Covid-19 challenges Non-core asset disposal strategy delivers $1.5 billion value realisation, including $1.25 billion in cash, with more to come Barrick increases quarterly dividend by 14% to $0.08 per share

Group operating results…

Solid Q2 2020 production despite Covid-19 pandemic

Gold operating results Q2 2020 Q1 2020 Q2 2019

Group year-to-date production of 2.4Moz at the mid-point Production (oz 000) 1,149 1,250 1,353

of guidance of 4.6Moz to 5.0Mozi for the year

Cost of sales ($/oz)7 1,075 1,020 964

Anchored by strong operating performance from Tier

One asset portfolio including NGM, Loulo-Gounkoto Total cash costs ($/oz)8 716 692 651

and Kibali All-in sustaining costs ($/oz)8 1,031 954 869

H2 2020 gold production expected to be in line with first Copper operating results Q2 2020 Q1 2020 Q2 2019

half of the year

Production (millions of pounds) 120 115 97

Higher royalty costs due to higher precious metal

prices now a common theme across the industry Cost of sales ($/lb)7 2.08 1.96 2.04

Copper portfolio continues to outperform C1 cash costs ($/lb)9 1.55 1.55 1.59

Best quarterly production from Lumwana in several All-in sustaining costs ($/lb)9 2.15 2.04 2.28

years

Per pound copper costs trending to low end of

guidance

iBarrick is closely monitoring the global Covid-19 pandemic and Barrick’s guidance may be impacted if the operation or development of our mines and projects is disrupted due to efforts to slow the spread of the virus

Group financial results…

Financial Results Q2 2020 Q1 2020 Q2 2019

Free cash flow4 increased by nearly 20% from Q1 to Revenue ($ million) 3,055 2,721 2,063

$522 million in Q2 given diversified and industry-leading Net earnings ($ million) 357 400 194

Tier One asset portfolio Adjusted net earnings ($ million)5 415 285 154

Captured benefit of higher gold prices through agile 1,697 1,466 972

Adjusted EBITDA10

management and operational execution

Net cash provided by operating

Debt net of cash at $1.4 billion, down almost 25% 1,031 889 434

activities ($ million)

from end Q1

Free cash flow ($ million)4 522 438 55

No significant public debt maturities until 2033

Net earnings per share ($) 0.20 0.22 0.11

Quarterly dividend increased to $0.08 per share

Adjusted net earnings per share ($)5 0.23 0.16 0.09

Doubled compared to a $0.04 per share quarterly

dividend a year ago Total attributable capital

402 364 361

A 14% increase on Q1 2020 dividend per share expenditures ($ million)11

Dividend underpinned by strong balance sheet and Cash and equivalents ($ million) 3,743 3,327 2,153

free cash flow4 outlook based on ten-year guidance Debt, net of cash ($ million) 1,425 1,852 3,654

Dividend per share ($) 0.08 0.07 0.04

Carlin…

Nevada, USA

Carlin12 (61.5%) Q2 2020 Q1 2020 Q2 2019

Lower production compared to Q1 2020 due to scheduled Total tonnes mined (000) 15,793 17,120 12,138

plant maintenance at the Goldstrike roaster

Average grade processed (g/t) 3.60 3.41 4.26

Mill 6 completed roaster maintenance in July

Ore tonnes processed (000) 2,835 3,229 1,961

Production also impacted by an increase in higher grade

Recovery rate (%) 80% 71% 71%

Cortez ore processed by the Carlin roasters, displacing

lower grade Carlin ore in the feed mix – a synergy Gold produced (oz 000) 235 253 181

captured due to the formation of NGM Gold sold (oz 000) 234 256 181

Costs in Q2 reflect lower throughput, plant maintenance Income ($ millions) 151 153 33

and throughput efficiency projects at the Goldstrike roaster EBITDA ($ millions)10 195 202 86

Capital expenditures ($

60 55 54

millions)

Minesite sustaining 60 55 54

Cost of sales ($/oz)7 1,037 970 1,116

Total cash costs ($/oz)8 850 776 769

All-in sustaining costs ($/oz)8 1,130 1,007 1,088

Refer to the Technical Report on the Carlin Complex, dated March 25, 2020, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on March 25, 2020Carlin trend…growth and discoveryi

Nevada, USA

Best intercept to date at North Leeville 21.3m at 35.3g/t -

geologic model upgraded to support resource evaluation

Bold step out drilling NE of Leeville continues to intersect

Carlin system with gold anomalism and significant alteration

north of Fence (assays pending)

Highest priority target along Post-Gen Fault corridor

successfully tested down plunge of Deep Post, multiple

zones of significant mineralisation and alteration

including 5.2m at 10.9g/t and 3.7m at 9.4g/t (additional

assays pending)

SW of Gold Quarry, framework drilling is answering key

geologic questions and showing down plunge continuation

of the system; gold anomalism associated with strong

decalcification and silicification

Framework drilling in Carlin Basin initiated

At Rain, sub-district scale model highlights new

opportunities; testing priority targets will begin in Q3

iSee Appendix A for additional details including assay results for the significant interceptsCortez…

Nevada, USA

Production improved by 3% from prior quarter and total Cortez13 (61.5%) Q2 2020 Q1 2020 Q2 2019

cash cost per ounce8 on track Total tonnes mined (000) 20,719 22,696 31,598

Higher grades from Crossroads and Pipeline, plus

Average grade processed (g/t) 1.87 1.06 1.82

more Cortez Hills Underground Ore processed

through oxide mill Ore tonnes processed (000) 2,381 4,783 5,014

Cortez Hills Underground productivity continues to Recovery rate (%) 84% 84% 84%

outperform due to ongoing efficiency and availability Gold produced (oz 000) 132 128 280

initiatives

Gold sold (oz 000) 132 128 281

Improvements on the CIL tanks and ore

Income ($ millions) 109 89 158

characterization have boosted oxide mill recoveries

EBITDA ($ millions)10 144 122 223

Goldrush Capital expenditures ($

52 50 83

Construction of twin exploration declines ahead of millions)14

schedule Minesite sustaining14 42 46 15

Transition from contract to owner mining brought forward Project14 10 4 68

to Q4 2020 – six months earlier than planned Cost of sales ($/oz)7 870 876 719

Scheduled to intersect first ore in first half of 2021 Total cash costs ($/oz)8 613 614 489

Permitting timeline for a Record of Decision in Q4 2021

All-in sustaining costs ($/oz)8 950 1,009 561

is unchanged

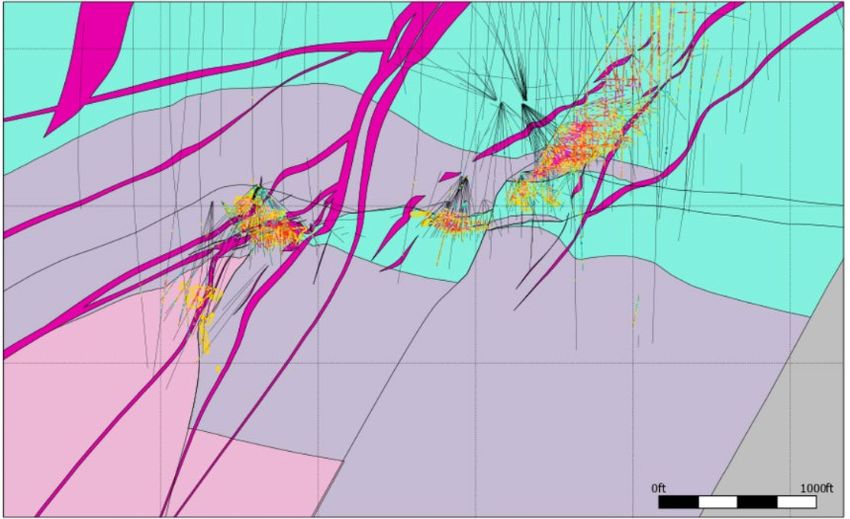

Refer to the Technical Report on the Cortez Joint Venture Operations, dated March 22, 2019, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on March 22, 2019Cortez Hills Underground (CHUG) Upside…

Hanson Footwall Target

A A’

Lithology 3900’ CHUG – Overview Map

Au g/t

A’ Au g/t

171.4

34.28

17.14

6.86

3.43

1.71

29.6m at 8.64g/ti 0.68

0.34

0.17

0.03

0

12.8m at 7.95g/ti

18.6m at 4.94g/ti

A

300m

Significant upside identified at CHUG

Tertiary Quartz Porphyry Current Reserves and Resource base15:

Devonian Wenban P&P: 3.9Moz at 10.03g/t

Silurian Roberts Mountain M&I: 4.7Moz at 8.85g/t (inclusive of P&P)

Ordovician Hanson Creek Inferred: 0.3Moz at 8.33g/t

Fault

N Drilling the Hanson Footwall – first upside target – confirmed

3.43 g/t (0.1 opt) grade shell

mineralisation ~100m below existing R&R

Upside Potential 1km

m m

Test targets to expand R&R and extend asset life of mine

iSee Appendix B for additional details including assay results for the significant interceptsFourmile…expanding high grade

mineralisationi

Nevada, USA FM20-154D

1.4 m @ 14.6 g/t 2019 Resource Footprint

N

9.4 m @ 17.9 g/t Exploration Upside

1.5 m @ 24.0 g/t Dorothy Drill intercepts > 5g/t Au

Significant mineralisation intersected west of Dorothy;

0.9 m @ 16.0 g/t No significant intercept

strong alteration intersected to the south

FM20-161D

Significant mineralisation in step-out holes west and 1.5 m @ 30.3 g/t FM20-169D

southwest of Sophia; strong alteration intersected in another 2.4 m @ 15.1 g/t6 9.1m, 2.0m, & 10.0m of

hole to the northwest 2.9 m @ 13.1 g/t significant alteration

3.2 m @ 10.5 g/t (assays pending)

Two holes between Fourmile and Goldrush intersected

Sophia

strong mineralisation and alteration at favourable FM20-153D

1.2 m @ 41.1 g/t

stratigraphic contact 3.2 m @ 12.7 g/t

Infill drilling program to de-risk Fourmile inferred resource 9.9 m @ 48.4 g/t Blanche

1.5 m @ 18.4 g/t

confirmed tenor; variability consistent with inferred 4.7 m @ 41.5 g/t Fourmile

classification FM20-170D

FM20-158D 20.4m of significant

Refinement of Fourmile ore controls and geologic model 8.4 m @ 21.5 g/t Rose alteration (assays

continues to yield strong results from target testing; footprint 0.9 m @ 10.6 g/t pending)

continues to grow Barrick

FM20-160D

Extracting maximum value from every drill hole to support 5.2 m @ 10.6 g/t

NGM

1.5 m @ 5.6 g/t

project design and execution Goldrush

3.9 m @ 7.3 g/t

400m

iSee Appendix C for additional details including assay results for the significant interceptsTurquoise Ridge…

Nevada, USA

Production and total cash costs per ounce8 impacted by Turquoise Ridge16 (61.5%) Q2 2020 Q1 2020 Q2 2019

lower head grade and recoveries for the autoclave versus

Ore tonnes processed (000) 821 862 -

the prior quarter, partially offset by higher grades for the

oxide mill but at lower throughput Average grade processed (g/t) 3.61 3.35 -

AISC per ounce8 slightly higher – up 3% from Q1 Overall recovery rate (%) 82% 84% 91%

Gold produced (oz 000) 79 84 65

TR Underground Third Shaft Gold sold (oz 000) 79 87 85

Construction of the third shaft remains on schedule and Income ($ millions) 48 47 53

within budget

EBITDA ($ millions)10 73 78 62

Shaft liner advanced to a depth of 509m below the collar

Capital expenditures

Commissioning expected in late 2022 9 19 19

($ millions)

Minesite sustaining 3 11 7

Exploration

Project 6 8 12

MRM and exploration teams continue to integrate the

geological models between Turquoise Ridge UG and Vista Cost of sales ($/oz)7 1,073 1,032 665

and Mega pits on the legacy Twin Creeks property Total cash costs ($/oz)8 753 668 569

Still more work required to deliver comprehensive All-in sustaining costs ($/oz)8 829 806 667

integrated orebody and grade control models

Refer to the Technical Report on the Turquoise Ridge mine, dated March 25, 2020, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on March 25, 2020Other Nevada Gold Mines…

Phoenix Phoenix (61.5%) Q2 2020 Q1 2020

Consistent performance with production in line compared to

Gold produced (oz 000) 35 35

the prior quarter at lower total cash cost per ounce8

Cost of sales ($/oz)7 1,726 1,583

AISC per ounce8 5% higher due to increased capitalised

stripping, in line with mine sequencing Total cash costs ($/oz)8 725 737

All-in sustaining costs ($/oz)8 957 914

Long Canyon Long Canyon (61.5%) Q2 2020 Q1 2020

Production 54% higher than prior quarter due to a focus on Gold produced (oz 000) 40 26

pad inventory reduction as mining and stacking moves Cost of sales ($/oz)7 1,009 1,025

towards main part of the Cut 7 orebody

Total cash costs ($/oz)8 308 345

Together with a decrease in capitalised stripping in Cut 7,

All-in sustaining costs ($/oz)8 430 561

AISC per ounce8 fell by 23% compared to the prior quarterHemlo…

Ontario, Canada

Production slightly lower than prior quarter due to lower

Hemlo (100%) Q2 2020 Q1 2020 Q2 2019

throughput, partially offset by higher grades from the

underground C-Zone Ore tonnes processed (000) 472 493 779

Average grade processed (g/t) 3.89 3.64 2.38

2020 Outlook Recovery rate (%) 96% 95% 94%

Production remains on track to achieve guidance Gold produced (oz 000) 54 57 55

Costs higher as a result of –

Cost of sales ($/oz) 1,268 1,119 953

Increase in royalty expense from higher gold prices and

mining in underground zones that incur a higher NPI Total cash costs ($/oz)8 1,080 945 822

royalty burden All-in sustaining costs ($/oz)8 1,456 1,281 1,015

Temporary delay in new underground contractor arriving

at site due to movement restrictions in response to

Covid-19, resulting in increased proportion of higher

cost stockpiled material being processed

New underground contractor started mobilising to site at

end of Q2 2020, with ramp-up of underground

development now underway

Refer to the Technical Report on the Hemlo Mine, Marathon, Ontario, Canada, dated April 25, 2017, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on April 25, 2017Hemlo deposit…growth upside

Golden Giant David Bell

3 Williams

1

2

4 N

5 B ZONE

6

1000m

MINE ZONES [Series] Western Discovery potential for new orebodies

(Blackfly) [100 & 300 series]

1. B ZONE [MAIN] Recent field evidence of plunging zones

Moose Lake Porphyry [300-series] 2. B ZONE [FW] Western extension of known orebodies [100 & 300

series] in C Zone

Volcaniclastics [100-series] 3. C ZONE [100]

Focus of significant future drill targeting

WOC/GG/DB headframes 4. BLACKFLY [100] Down-plunge extension of C Zone

Williams open pit extents 5. C ZONE [300] Recently confirmed by ultra-deep drilling

Down-plunge extension of B Zone [FW]

Further western extension potential 6. SOUTH RIM [FW]

Future deep drill-testingPueblo Viejo…

Dominican Republic

Pueblo Viejo17 (60%) Q2 2020 Q1 2020 Q2 2019

As expected, production 22% lower than the prior quarter Open pit tonnes mined (000) 4,647 4,039 6,116

due to a total plant maintenance shutdown Average grade processed (g/t) 3.45 3.44 3.56

Production expected to be higher in H2 2020 with Ore tonnes processed (000) 1,088 1,471 1,212

major scheduled maintenance shutdowns now Recovery rate (%) 89% 89% 90%

complete for the year

Gold produced (oz 000) 111 143 124

Together with higher royalties from higher gold prices, total

Gold sold (oz 000) 115 144 132

cash cost per ounce8 and AISC per ounce8 increased from

prior quarter due to lower throughput from planned Income ($ millions) 92 102 75

shutdown – partially offset by lower energy costs EBITDA ($ millions)10 125 134 104

Commenced early works expenditures for proposed plant Capital expenditures

21 17 18

and tailings expansion ($ millions)

Minesite sustaining 15 17 18

Project 6 - -

Cost of sales ($/oz)7 935 767 852

Total cash costs ($/oz)8 579 502 557

All-in sustaining costs ($/oz)8 720 626 702

Refer to the Technical Report on the Pueblo Viejo mine, Sanchez Ramirez Province, Dominican Republic, dated March 19, 2018, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on March 23, 2018Pueblo Viejo expansion… Dominican Republic Plant expansion project environmental impact study submitted to authorities – no issues identified in subsequent field visit Engineering of process plant facilities progressed to plan during Q2 and orders placed for critical long lead items – including an LOI for the oxygen plant which is on the critical path for the plant expansion schedule Field work for baseline environmental assessment of additional tailings capacity commenced. Discussions continue with national authorities to obtain the necessary tenure and permitting Implementation strategy for the expansion project is focused on utilising local Dominican businesses – targeting over $100 million contribution to the local construction industry by the end of 2022 Agribusiness project team engaged with stakeholders and will now commence pilot projects with local cocoa farmers

Pueblo Viejo JV…new targets

Foundational geology (structural framework) with state-of-the-art

N

geophysics unveils new targets in proximity to a significant orebodyi

Anomaly analogous to known deposits (scale, tenor and orientation)

DPV20778 Arroyo El Rey

target

Initial drilling intersected zones of sulphides

Arroyo

Hondo Two holes drilled with evidence of sulphides and potential

mineralisation

Geophysics to be expanded along structural intersections and

Growth projected into new Pueblo Grande JV property

Pit

275 RL

Arroyo DPV20778

Hondo

Favourable alteration

Monte and sulphides

Negro intersected but low

Mejita

NE grade so far

Au contours

0.72g/t

Structural

Framework

Moore

Inferred Faults

iAs at December 31, 2019, orebody estimated to contain 25Moz of measured and indicated resources and 3.7Moz of inferred resources with 7.9Moz historical contained ounces processed. Refer to endnote 24 for further details.Veladero…

Argentina

As previously reported, production and costs at Veladero Veladero18 (50%) Q2 2020 Q1 2020 Q2 2019

in Q2 2020 were impacted by: Average grade processed (g/t) 0.93 0.80 0.75

A mandatory nationwide quarantine Ore tonnes processed (000) 2,609 3,243 2,828

Followed by movement and social distancing Gold produced (oz 000) 49 75 75

restrictions that limited remobilisation back to site 35 57 74

Gold sold (oz 000)

Further impacted by severe winter weather that Income ($ millions) 16 24 12

impacted both mining and processing operations

EBITDA ($ millions)10 29 46 43

2020 Outlook Capital expenditures ($ millions) 20 40 19

Demobilisation of contractors working on capital projects in Minesite sustaining 20 25 19

accordance with government’s pandemic response Project - 15 -

delayed construction and commissioning of leach pad

Cost of sales ($/oz) 1,228 1,182 1,186

phases

Total cash costs ($/oz)8 801 788 746

Production at Veladero currently trending below guidance

for 2020 at slightly higher per ounce costs All-in sustaining costs ($/oz)8 1,383 1,266 1,046

Refer to the Technical Report on the Veladero Mine, San Juan Province, Argentina, dated March 19, 2018, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on March 23, 2018Veladero…next steps

Argentina

Due to the Covid-19 pandemic in Q2, the Argentinian government limited personnel on site which impacted mining

and project activities. Proposed easing of restrictions in September will allow remobilisation of contractors and

personnel

Mining

Open pit operations stopped for 17 days and were at 30% capacity for a further 23 days. Pit has since

operated at 85% capacity due to personnel restrictions on site contributing to a 10Mt waste stripping deficit in

2020

Equipment orders brought forward to catch up on stripping deficit and phase designs being optimised to

reduce impact of waste stripping. Recommissioning of ore conveyor also under review

Leach Pad Expansions

Phase 6 pad construction works stopped at start of pandemic causing 6 month construction delay due to

winter season. Additional resources to be mobilised at end of the winter season to accelerate construction

works

Phase 4B/5B upgrade program continued throughout winter season and inspections of liner and collection

system in progress

Other Capital Projects

New Veladero airstrip to be completed by end of 2020

Construction of powerline from Chile to recommence dependent on easing of current government restrictionsAlturas - Del Carmen…exploration

drives update of project economics

Argentina

Alturas - Del Carmen District Exploration upside of the district now in a range from

N 352.0 to 374.5 Mt at 1.07 to 1.08 g/t Auii

Outcropping ore in Rojo Grande could provide early

71m at 1.56g/t from 152mi

ore feed

28m at 3.38g/t from 211mi

Rojo Grande

Including 17m at 5.20g/t Exploration upside Updated mineral estimation and pit optimisation in

63.5 to 77.0 Mt at

0.6g/t to 0.9 g/t Auii

progress

Update of scoping level economics scheduled for Q4

Project team engaged and full development timeline

Alturas established with near term strategic filters defined

Inferred Resource C° Amarillo

8.9Moz at 1.1g/t Auiii Exploration upside Structural framework study initiated to establish

15.0 to 18.5Mt at controls to high grade mineralisation

1.75g/t to 2.2g/t Auii

>0.50 Au ppm Block Model

Chile Argentina

Ladera

Exploration upside

iSee Appendix D for additional details including assay results for the significant intercepts

22.0 to 27.0Mt at iiPotentialquantities and grades in these preliminary results are conceptual in nature and there has been insufficient exploration to

1.2g/t to 1.5g/t Auii 1km define a mineral resource at this time and it is uncertain that further exploration will result in the target being delineated as a mineral

resource. Exploration upside has not been optimised in a pit design

iiiBased on a 2018 optimised pit. See endnote 19Porgera…

Papua New Guinea

As previously disclosed, Porgera entered care and Porgera20 (47.5%) Q2 2020 Q1 2020 Q2 2019

maintenance on April 25 654 2,809 3,655

Total tonnes mined (000)

Due to the uncertainty related to the timing and scope

Average grade processed (g/t) 3.16 2.98 3.25

of future developments at Porgera, 2020 guidance for

Ore tonnes processed (000) 200 736 557

this site has been withdrawn

Recovery rate (%) 91% 90% 90%

Special Mining Lease Extension Gold produced (oz 000) 24 62 61

In response to a request from PNG Prime Minister Gold sold (oz 000) 24 63 63

Marape, Barrick proposed a benefit-sharing Income ($ millions) (13) 29 16

arrangement in 2019 that would deliver more than half EBITDA ($ millions)10 (7) 39 24

the economic benefits from Porgera to PNG Capital expenditures ($

stakeholders for 20 years 2 8 12

millions)

Barrick believes the government’s decision not to Minesite sustaining 2 8 12

extend the SML is without due process and in violation Cost of sales ($/oz) 1,141 1,097 1,032

of the government’s legal obligations to BNL

Total cash costs ($/oz)8 875 941 893

All-in sustaining costs ($/oz)8 1,046 1,089 1,112Loulo-Gounkoto…

Mali

Production in line with prior quarter as lower feed grade and Loulo-Gounkoto21 (80%) Q2 2020 Q1 2020 Q2 2019

throughput was offset by higher recovery Total tonnes mined (000) 8,736 7,572 8,048

Total cash cost per ounce8 slightly higher from Q1 due to Average grade processed (g/t) 4.92 4.96 4.74

increased royalties as a result of higher gold prices and Ore tonnes processed (000) 972 980 1,034

marginally higher operating costs Recovery rate (%) 92% 90% 93%

AISC per ounce8

increased by 16% versus prior quarter due Gold produced (oz 000) 141 141 147

to increased capitalised stripping at the Gounkoto open-pit,

Gold sold (oz 000) 157 123 148

in-line with plan

Income ($ millions) 107 68 32

EBITDA ($ millions)10 167 115 102

Projects and Exploration Capital expenditures ($

55 32 31

millions)

Gounkoto underground remains on track to start

Minesite sustaining 55 32 29

development in Q4 2020

Project - - 2

Potential minelife extensions continue to be confirmed in

Cost of sales ($/oz)7 1,012 1,002 1,072

Q2. Drilling at the Yalea Transfer Zone extended

mineralisation by an additional 160m and is currently Total cash costs ($/oz)8 639 614 598

480m south of the extent of the 2019 block model All-in sustaining costs ($/oz)8 1,030 891 811

Refer to the Technical Report on the Loulo-Gounkoto Gold Mine Complex, Mali dated September 18, 2018 with an effective date of December 31, 2017, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on January 2, 2019Loulo District…strong drill results to drive

mine life extensionsi

Loulo:

Baboto Loulo 3 new intersections confirmed high grade

mineralisation is still open down plunge. Footwall intercepts

N Yatela Gara Loulo 3 include 19.25m at 6.06g/t and 6.85m at 5.81g/t

Sadiola Yalea High-grade Yalea transfer zone extended 480m beyond

2019 block model and still open down plunge. Significant

intercepts include 14.95m at 7.34g/t and 8.70m at 22g/t

Senegal Structural thickening at base of Yalea Transfer Zone

supports wider intercepts including 66.0m at 4.83g/t,

Gounkoto 28.0m at 4.10g/t, 25.4m at 4.61g/t, 17.8m at 3.22g/t and

Loulo

District

Faraba 17.4m at 15.68g/t – further enhancing significant resource

Sabodola potential

Tabakoto

Gara Gounkoto:

Yalea

Massawa Mali >1 km long mineralised trend confirmed south of

Gounkoto Gounkoto open pit. Significant results include

Petowal Saraya Kenieba 9m at 3.42g/t and 7m at 7.23g/t

Bambadji JV Bambadji:

Second phase of auger drilling extends Kora-Latifa

Kedougou Fekola

Diakha prospective corridor over 11km. New diamond drilling

25km Boto confirms significance of Gefa mineralised system. Follow

5km

Fekola up drilling in Faleme volcanics highlights positive results

Strong results from prefeasibility studyii at Sabodala-

Focus Areas Massawa complex

iSee iiThe website link to the Teranga press release titled “Teranga Gold Announces Positive Pre-Feasibility Study Results for Top-Tier Sabodala-Massawa Gold Complex” can be found here

Appendix E for additional details including assay results for the significant interceptsTongon…

Côte d'Ivoire

Production 5% higher than the prior quarter due to

Tongon (89.7%) Q2 2020 Q1 2020 Q2 2019

stronger throughput

Per ounce costs improved from Q1 driven by lower Ore tonnes processed (000) 1,013 982 945

processing and mining costs Average grade processed (g/t) 2.34 2.34 2.31

Recovery rate (%) 83% 83% 85%

Delivering Mine Life Extension Gold produced (oz 000) 64 61 61

At Mercator, a revised geological model optimised that Cost of sales ($/oz)7 1,275 1,368 1,562

resulting in higher grades at similar metal content

Total cash costs ($/oz)8 688 762 750

Conceptual economic analysis with final pit designs

underway for this satellite deposit located 15km All-in sustaining costs ($/oz)8 745 788 802

from the Tongon plant

Exploration during Q2 focused on several priority targets

located on three major structures

Follow-up drilling will continue in Q3, including the

evaluation of four targets along the western flank of

the Badenou trendNielle…exploring new corridors for

opportunities to extend LoM

Côte d'Ivoire

Djinni PFS and EISA underway

N SZ and NZ cut back evaluations underway

Stabilo Trend

Tongon West (2) Seydou N-Jubula Stabilo Trend:

Satellite (6) Koro

Sekala Seydou N – Jubula, 5.1km structure beneath

2019 Probable Mineral Reserve:

510kt at 1.85g/t for 30.5koz

Seydou S. ferricrete plateau tested with Auger program for

2019 Probable Mineral follow up in Q3

Reserve:

Djinni 408kt at 1.95g/t for 26koz Moyet Trend:

2019 Indicated Resource:

1.9Mt at 2.30g/t for 139koz North Zone Pit First phase Scout RC at Tiebila East evaluated

2019 Inferred Resource: target prospectivity, alteration system open along

South Zone Pit

1.2Mt at 2.41g/t for 94koz strike supporting prospectivity of the trend

Mercator

Tekono Trend

(2) Soumo Tekono Trend: AC drilling in progress at Soumo

Satellite (6) Rokubo target, 3.6km strike opportunity, 5km from plant

Badenou Trend Badenou Trend:

(10) Kanon

(9) Zulu area Moyet Trend Mercator: Added drilling and updated model

(11) Kamino N

(12) Sougo

(4) Tiebila

(7) Loko drives increase in potential for mineral resource

(5) Rhodia

(8) Mira

definition

Known Deposits 4 targets: Zulu West, Kanon, Zulu main and

Active/historic targets

Kamino North prioritised. Follow up AC drilling

Early stage (map + litho)

10km started to evaluate targets

Q1 generated targets parkedKibali…

DRC

Kibali22 (45%) Q2 2020 Q1 2020 Q2 2019

Kibali continued to deliver consistent results, with Total tonnes mined (000) 3,253 3,175 2,938

production in-line versus Q1 3.68 3.77 3.88

Average grade processed (g/t)

Total cash cost per ounce8 was 6% higher than the prior

Ore tonnes processed (000) 857 838 850

quarter due to increased labour and logistic charges as

well as higher royalties from higher gold prices Recovery rate (%) 89% 89% 89%

Despite this, AISC per ounce8 was 4% lower than Q1 Gold produced (oz 000) 90 91 95

due to decrease in underground development Gold sold (oz 000) 96 88 95

Income ($ millions) 64 48 43

EBITDA ($ millions)10 106 89 74

Capital expenditures ($ millions) 10 15 10

Minesite sustaining 9 15 10

Project 1 - -

Cost of sales ($/oz)7 1,067 1,045 868

Total cash costs ($/oz)8 617 582 540

All-in sustaining costs ($/oz)8 739 773 651

Refer to the Technical Report on the Kibali Gold Mine, Democratic Republic of the Congo dated September 18, 2018 with an effective date of December 31, 2017, and filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov on January 2, 2019North Mara…

Tanzania

North Mara (84%)23 Q2 2020 Q1 2020 Q2 2019

Gold production in Q2 5% higher than prior quarter primarily Total tonnes mined (000) 766 2,448 2,709

due to higher processed grade as open pit mining ceased Average grade processed

3.75 3.42 5.37

during the quarter and mill feed was mainly sourced from (g/t)

higher grade underground zones at Gokona Ore tonnes processed (000) 611 636 467

Total cash cost per ounce8 was 12% higher than Q1 due to Recovery rate (%) 93% 93% 94%

higher direct mining costs from transition to underground

Gold produced (oz 000) 68 65 76

mining

Gold sold (oz 000) 67 70 66

We continue to evaluate sequencing at North Mara and expect

to update the mineplan in due course for an optimised restart Income ($ millions) 44 49 31

of open pit mining EBITDA ($ millions)10 65 70 47

Capital expenditures in Q2 were significantly higher than Q1 Capital expenditures ($

30 13 10

due to our investment in the tailings storage facility, other millions)

water management initiatives and land acquisitions Minesite sustaining 29 11 7

We expect this capital investment to reduce over time as Project 1 2 3

legacy issues in Tanzania are addressed Cost of sales ($/oz)7 1,040 959 800

Total cash costs ($/oz)8 724 646 539

All-in sustaining costs ($/oz)8 1,166 816 675North Mara…Gokona targets

Extensive upside potential, open in all directionsi

West

+2.8km East

GOKONA UG GENA OP

Open Open

KOFIA

Drill Drill

Gap Gap

Shoot

Upper East

Extn. Potential Phase 1 Shoot Phase 2

Reserve Au g/t

Replacement

2.5-5

Deep Gena Conversion Area 5-10

Open Central Potential resource extn. >10

UGKD674 UGKD664 Open

UGKD666: UGKD688: 19.7m @ 37.51g/t UGKD665

6m @ 4.82g/t Priority Targets

6m @ 2.65g/t 7m @ 2.66g/t No sig intercept

UGKD672: 6m @ 30.43g/t UGKD679 Mid 2020 conversion

No sig. intercept UGKD690: Lower West Deep 17m @ 3.44g/t Q2 conversion drilling EOY 2020 conversion

6m @ 3.40g/t Potential Reserve Deep

East UGKD680 Scout drilling

UGKD681: Scout drilling in Q3

6m @ 8.03g/t 7m @ 3.50g/t Extension Centr 5.8m @ 4.01g/t

7m @ 2.50g/t 6.08m @ 7.57g/t al

7m @ 4.38g/t UGKD687: UGKD648 UGKD697 Current targets have capacity to replace 2020 and 2021 depletion

9m @ 11.35g/t UGKD692 No sig intercept 17m @ 18.94g/t

UGKD682:

5m @ 2.35g/t In Q2, re-logging extended geological model 900m along strike,

9m @ 3.62g/t 5.6m @ 3.81g/t UGKD655 7m @ 4.15g/t

9m @ 4.58g/t 5.4m @ 3.74g/t covering Gena

UGKD671: UGKD695

5m @ 3.64g/t UGKD693 8m @ 6.52g/t Scout exploration drilling to test potential for extra resources

6m @ 3.02g/t 6m @ 2.96/t UGKD694A 11m @ 4.03g/t Gena conversion drilling aims to inform a larger pit cutback decision

6m @ 6.83g/t 5m @ 3.43g/t 5.5m @ 22.57g/t 6m @ 2.40g/t end of year 2020

iSee Appendix F for additional details including assay results for the significant interceptsNorth Mara…Kofia target

Potential extension opportunity

Upper Westi

UGKD688 UGKD687

Initial scout drilling aims to extend 7m @ 2.66g/t 9m @ 11.35g/t

Gokona system 500m west of current 6m @ 30.43g/t 5.6m @ 3.81g/t

block model UGKD690 UGKD671

6m @ 3.40g/t 5m @ 3.64g/t

Previous drilling 300m east of Kofia 7m @ 3.50g/t 6m @ 3.02g/t

N

returned strong mineralisation (Upper 6.08m @ 7.57g/t 6m @ 6.83g/t

West)

Kofia has Gokona style potassium 900m

feldspar alteration and the same host

sequence (andesitic porphyry and Nyabigena

sediment). Chargeability anomalies

Gokona

are located on the HW and FW

contacts

Good continuity mapped in geology,

alteration and geophysical response

600m

Kofia Exploration Targetii

Area: 500m strike x 350vm Upper Westi

Average TWiii: 5m (range 3.8m to 6.8m) UGKD666: UGKD681: Tertiary Fault (dextral)

Drillhole geology Potential Grades: 4g/t to 5g/t 6m @ 2.65g/t 6m @ 8.03g/t HW Contact (MSC)

Mafic Schist (MSC) UGKD672: 7m @ 2.50g/t FW Contact (VAN)

iiPotential grades are conceptual in nature and there has No sig intercept 7m @ 4.38g/t

Host Sequence (CAP + SED) been insufficient exploration to define a mineral resource

UGKD682: IP Chargeability Anomaly

at this time and it is uncertain that further exploration will

Volcanic Andesite (VAN) result in the target being delineated as a mineral resource.

iiiTrue width

9m @ 3.62g/t Logged Alteration (A1 to A3)

iSee Appendix F for additional details including assay results for the significant interceptsBulyanhulu and Buzwagi…

Tanzania

Bulyanhulu

Bulyanhulu (84%)23 Q2 2020 Q1 2020 Q2 2019

On track to resume underground mining operations

Gold produced (oz 000) 7 7 6

by end of 2020, in line with guidance

Gold sold (oz 000) 30 7 6

Shaft refurbishment scheduled to start in August

Cost of sales ($/oz)7 1,658 1,685 1,217

Buzwagi Total cash costs ($/oz)8 950 686 525

Focus is on optimising throughput and managing All-in sustaining costs ($/oz)8 1,014 906 666

grade from stockpile processing

Scout drilling to validate the exploration model for Buzwagi (84%)23 Q2 2020 Q1 2020 Q2 2019

upside potential at depth has commenced, totaling Gold produced (oz 000) 20 22 19

2,720m

Gold sold (oz 000) 56 24 20

Exports of Concentrate Stockpiled Cost of sales ($/oz)7 909 1,373 1,198

Approximately 30% of concentrate shipped by Total cash costs ($/oz)8 751 1,275 1,099

end of Q2 with remainder shipped in Q3 All-in sustaining costs ($/oz)8 770 1,288 1,150

First $100 million tranche of settlement paid to

Government of Tanzania in May 2020Central and East Africa…

Congo – Tanzania Craton

Kibali

Central African

Republic South Sudan Drilling in progress confirming presence at depth of plunging

controls on mineralisation at KCD and satellite deposits

Kalimva – deeper drilling scheduled to test for underground

Kibali potential

Uganda

N Follow up work begins on regional anomalies outside the KZ

Ngayu Belt

trend

Kenya

Democratic

Lake

Victoria

Tanzania

North Mara

Republic of North Mara

Congo Bulyanhulu Gokona drill results validate revised geology model and

Gold deposits Buzwagi exceed grade expectations pointing to anticipated

Exploration focus resource increase

District scale mapping and modelling reveals new target

Greenstone Belt area

Tanzania

Archean Granitoid

Nyabigena conversion drilling aims to inform a larger pit

Phanerozoic

cutback decision end of year 2020

Proterozoic

Archean Gneiss Bulyanhulu

Visible gold intersected ~400m below M&I resource

supporting down plunge continuity of high grade Deep

500km

West ShootsCopper mines….

Lumwana, Zambia Lumwana (100%) Q2 2020 Q1 2020 Q2 2019

Best quarterly production from Lumwana in several years

Copper produced (lbs million) 72 64 49

Production 13% higher than Q1 due to improved head grade,

Cost of sales ($/lb) 2.06 1.94 2.07

combined with solid throughput performance at the plant

C1 cash costs ($/lb)9 1.55 1.63 1.70

Higher grades and cost control resulted in a 5% decrease in C1

cash costs per pound9 from Q1 All-in sustaining costs ($/lb)9 2.27 2.26 2.78

Jabal Sayid, Saudi Arabia (50%) Jabal Sayid (50%) Q2 2020 Q1 2020 Q2 2019

Production in line with the prior quarter, delivering Q2 per pound Copper produced (lbs million) 20 20 16

costs below the bottom end of 2020 guidance Cost of sales ($/lb)7 1.41 1.28 1.45

Concentrate filter expansion project to improve milling rates and C1 cash costs ($/lb)9 1.14 0.97 1.22

availability continues to advance to completion for H2 2020

All-in sustaining costs ($/lb)9 1.41 1.11 1.31

Zaldívar, Chile (50%)

Zaldívar (50%) Q2 2020 Q1 2020 Q2 2019

Production lower than Q1 mainly due to lower grades and

recoveries, partially offset by improved heap leach throughput Copper produced (lbs million) 28 31 32

Chloride Leach Project - mobilisation of contractors ramped up Cost of sales ($/lb)7 2.52 2.39 2.32

in July with onsite activities expected to commence in August. C1 cash costs ($/lb)9 1.79 1.71 1.61

Project remains on-budget with efforts underway to minimize All-in sustaining costs ($/lb)9 2.09 1.99 1.85

delays due to Covid-19Relative Share Price Performance…

Relative Share Price Performance

since merger with Randgold announced Relative Share Price Performance YTD

300 Base = 100 170 Base = 100

275

160 Barrick

Barrick:59%

59%

Barrick

Barrick:183%

183%

150

250

140

225

130

200 120

175 110

150

100 SpotGold:

Spot Gold 29%

29%

90

GDX: 49%

125 GDX 49%

80

Spot Gold: 63% GDX: 132%

100 Spot Gold 63% GDX 132% 70

75 60

Sep-18 Jan-19 May-19 Sep-19 Jan-20 May-20 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20

Market data as at July 28, 2020. Share price performance based in USD. Source: Bloomberg Financial MarketsEndnotes

1. Loss time injury frequency rate (LTIFR) is a ratio calculated as follows: number of loss time injuries x 1,000,000 hours divided by the total number of hours worked.

2. Total reportable incident frequency rate (TRIFR) is a ratio calculated as follows: number of reportable injuries x 1,000,000 hours divided by the total number of hours worked. Reportable injuries include fatalities, lost time

injuries, restricted duty injuries, and medically treated injuries.

3. Class 1 - High Significance is defined as an incident that causes significant negative impacts on human health or the environment or an incident that extends onto publicly accessible land and has the potential to cause

significant adverse impact to surrounding communities, livestock or wildlife.

4. “Free cash flow” is a non-GAAP financial performance measure which deducts capital expenditures from net cash provided by operating activities. Barrick believes this to be a useful indicator of our ability to operate without

reliance on additional borrowing or usage of existing cash. Free cash flow is intended to provide additional information only and does not have any standardized meaning under IFRS and may not be comparable to similar

measures of performance presented by other companies. Free cash flow should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. For further details on this

non-GAAP measure, please refer to page 80 of the MD&A accompanying Barrick’s second quarter 2020 financial statements filed on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

5. “Adjusted net earnings” and “adjusted net earnings per share” are non-GAAP financial performance measures. Adjusted net earnings excludes the following from net earnings: certain impairment charges (reversals) related

to intangibles, goodwill, property, plant and equipment, and investments; gains (losses) and other one-time costs relating to acquisitions or dispositions; foreign currency translation gains (losses); significant tax adjustments

not related to current period earnings; unrealized gains (losses) on non-hedge derivative instruments; and the tax effect and non-controlling interest of these items. The Company uses this measure internally to evaluate our

underlying operating performance for the reporting periods presented and to assist with the planning and forecasting of future operating results. Barrick believes that adjusted net earnings is a useful measure of our

performance because these adjusting items do not reflect the underlying operating performance of our core mining business and are not necessarily indicative of future operating results. Adjusted net earnings and adjusted

net earnings per share are intended to provide additional information only and do not have any standardized meaning under IFRS and may not be comparable to similar measures of performance presented by other

companies. They should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. For further details on these non-GAAP measures, please refer to page 79-80 of the

MD&A accompanying Barrick’s second quarter 2020 financial statements filed on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

6. A Tier One Gold Asset is a mine with a stated life in excess of 10 years, annual production of at least 500,000 ounces of gold and total cash costs per ounce over the mine life that are in the lower half of the industry cost

curve.

7. Cost of sales applicable to gold per ounce is calculated using cost of sales applicable to gold on an attributable basis (removing the non-controlling interest of 40% Pueblo Viejo; 20% Loulo-Gounkoto; 10.3% Tongon; 16%

North Mara, Bulyanhulu and Buzwagi starting January 1, 2020, the date the GoT's 16% free carried interest was made effective (36.1% from January 1, 2019 to September 30, 2019; notwithstanding the completion of the

Acacia transaction on September 17, 2019, we consolidated our interest in Acacia and recorded a non-controlling interest of 36.1% in the income statement for the entirety of the third quarter of 2019 as a matter of

convenience); 63.1% South Arturo from cost of sales from July 1, 2019 onwards as a result of its contribution to Nevada Gold Mines (and on a 40% basis from January 1, 2019 to June 30, 2019); and our proportionate share

of cost of sales attributable to equity method investments (Kibali, and Morila until the second quarter of 2019), divided by attributable gold ounces. Also removes the non-controlling interest of 38.5% Nevada Gold Mines from

cost of sales from July 1, 2019 onwards. Cost of sales applicable to copper per pound is calculated using cost of sales applicable to copper including our proportionate share of cost of sales attributable to equity method

investments (Zaldívar and Jabal Sayid), divided by consolidated copper pounds (including our proportionate share of copper pounds from our equity method investments).Endnotes

8. “Total cash costs” per ounce and “All-in sustaining costs” per ounce are non-GAAP financial performance measures. “Total cash costs” per ounce starts with cost of sales applicable to gold production, but excludes the

impact of depreciation, the non-controlling interest of cost of sales, and includes by-product credits. “All-in sustaining costs” per ounce begin with “Total cash costs” per ounce and add further costs which reflect the additional

costs of operating a mine, primarily sustaining capital expenditures, sustaining leases, general & administrative costs, minesite exploration and evaluation costs, and reclamation cost accretion and amortization. Barrick

believes that the use of “total cash costs” per ounce and “all-in sustaining costs” per ounce will assist investors, analysts and other stakeholders in understanding the costs associated with producing gold, understanding the

economics of gold mining, assessing our operating performance and also our ability to generate free cash flow from current operations and to generate free cash flow on an overall Company basis. “Total cash costs” per

ounce and “All-in sustaining costs” per ounce are intended to provide additional information only and do not have any standardized meaning under IFRS. Although a standardized definition of all-in sustaining costs was

published in 2013 by the World Gold Council (a market development organization for the gold industry comprised of and funded by gold mining companies from around the world, including Barrick), it is not a regulatory

organization, and other companies may calculate this measure differently. Starting from the first quarter of 2019, we have renamed "cash costs" to "total cash costs" when referring to our gold operations. The calculation of

total cash costs is identical to our previous calculation of cash costs with only a change in the naming convention of this non-GAAP measure. These measures should not be considered in isolation or as a substitute for

measures prepared in accordance with IFRS. For further details on these non-GAAP measures, please refer to pages 81-98 of the MD&A accompanying Barrick’s second quarter 2020 financial statements filed on SEDAR at

www.sedar.com and on EDGAR at www.sec.gov.

9. “C1 cash costs” per pound and “All-in sustaining costs” per pound are non-GAAP financial performance measures. “C1 cash costs” per pound is based on cost of sales but excludes the impact of depreciation and royalties

and production taxes and includes treatment and refinement charges. “All-in sustaining costs” per pound begins with “C1 cash costs” per pound and adds further costs which reflect the additional costs of operating a mine,

primarily sustaining capital expenditures, general & administrative costs and royalties and production taxes. Barrick believes that the use of “C1 cash costs” per pound and “all-in sustaining costs” per pound will assist

investors, analysts, and other stakeholders in understanding the costs associated with producing copper, understanding the economics of copper mining, assessing our operating performance, and also our ability to generate

free cash flow from current operations and to generate free cash flow on an overall Company basis. “C1 cash costs” per pound and “All-in sustaining costs” per pound are intended to provide additional information only, do

not have any standardized meaning under IFRS, and may not be comparable to similar measures of performance presented by other companies. These measures should not be considered in isolation or as a substitute for

measures of performance prepared in accordance with IFRS. For further details on these non-GAAP measures, please refer to pages 99-100 of the MD&A accompanying Barrick’s second quarter 2020 financial statements

filed on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

10. EBITDA is a non-GAAP financial measure, which excludes the following from net earnings: income tax expense; finance costs; finance income; and depreciation. Management believes that EBITDA is a valuable indicator of

our ability to generate liquidity by producing operating cash flow to fund working capital needs, service debt obligations, and fund capital expenditures. Management uses EBITDA for this purpose. Adjusted EBITDA removes

the effect of impairment charges; acquisition/disposition gains/losses; foreign currency translation gains/losses; other expense adjustments; unrealized gains on non-hedge derivative instruments; and the impact of the

income tax expense, finance costs, finance income and depreciation incurred in our equity method accounted investments. We believe these items provide a greater level of consistency with the adjusting items included in

our Adjusted Net Earnings reconciliation, with the exception that these amounts are adjusted to remove any impact on finance costs/income, income tax expense and/or depreciation as they do not affect EBITDA. We believe

this additional information will assist analysts, investors and other stakeholders of Barrick in better understanding our ability to generate liquidity from our full business, including equity method investments, by excluding these

amounts from the calculation as they are not indicative of the performance of our core mining business and not necessarily reflective of the underlying operating results for the periods presented. EBITDA and adjusted

EBITDA are intended to provide additional information only and do not have any standardized meaning under IFRS and may not be comparable to similar measures of performance presented by other companies. They

should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. For further details on these non-GAAP measures, please refer to pages 101-102 of the MD&A

accompanying Barrick’s second quarter 2020 financial statements filed on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

11. These amounts are presented on the same basis as our guidance and include our 60% share of Pueblo Viejo, 80% share of Loulo-Gounkoto, 89.7% share of Tongon, 45% share of Kibali, 40% share of Morila and 60% share

of South Arturo (36.9% of South Arturo from July 1, 2019 onwards as a result of its contribution to Nevada Gold Mines), our 84% share of Tanzania starting January 1, 2020, the date the GoT's 16% free carried interest was

made effective (63.9% share from January 1, 2019 to September 30, 2019; notwithstanding the completion of the Acacia transaction on September 17, 2019, we consolidated our interest in Acacia and recorded a non-

controlling interest of 36.1% in the income statement for the entirety of the third quarter of 2019 as a matter of convenience, and 100% share from October 1, 2019 to December 31, 2019) and our 50% share of Zaldívar and

Jabal Sayid. Starting July 1, 2019, it also includes our 61.5% share of Nevada Gold Mines.You can also read