EUROCONTROL EUROPEAN AVIATION Comprehensive Assessment - 12 May 2022 - SUPPORTING EUROPEAN AVIATION

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

12 May 2022 EUROCONTROL Comprehensive Assessment EUROPEAN AVIATION SUPPORTING EUROPEAN AVIATION 1

Headlines (Week of 5 – 11 May 2022)

27,101 daily flights on average over past week (+2% vs previous week); 86% of 2019 levels.

Traffic slightly above the high EUROCONTROL Traffic Scenarios (6 Apr 2022): 86% for May vs 2019 so far.

Low-cost airlines are expanding capacities as well as traditional airlines to a lesser extent, notably

Turkish Airlines and Lufthansa. However, charter airlines reduced (reaching -23%) since Ukraine invasion

Preliminary CODA data show a significant increase of en-route ATFM delays in April vs March (+567%).

The invasion of Ukraine is affecting overflights in a number of countries, notably Lithuania, Poland,

Estonia and Latvia on the negative side; Armenia and Georgia on the positive side.

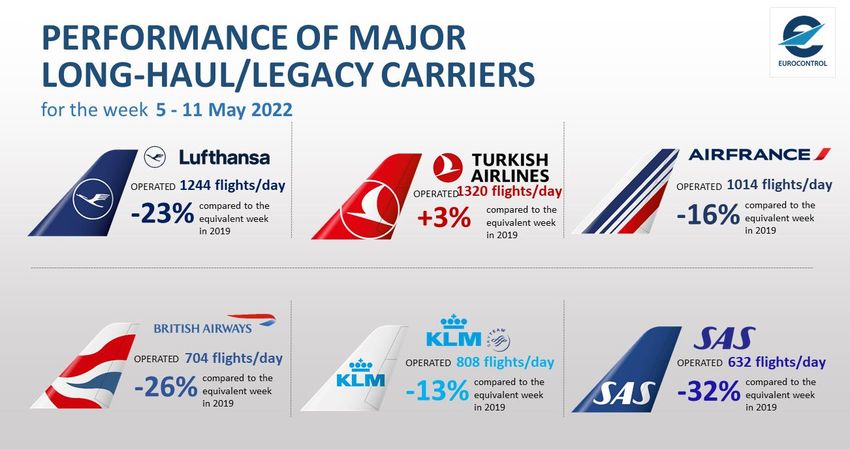

Ryanair was the busiest aircraft operator last week with 2,865 flights per day on average (+15% vs 2019),

followed by easyJet (1,559; -13% vs 2019), Turkish (1,320; +3% vs 2019), Lufthansa (1,244; -23% vs

2019), Air France (1,014; -16% vs 2019), KLM (808; -13% vs 2019) and Wizz Air (740; +24% vs 2019).

Domestic traffic vs 2019: Europe (-12%), USA (-14%), China (-68% - COVID) and Middle-East (+2%).

EU27 annual inflation rate increased from 1.7% in March 2021 to 7.8% in March 2022 with energy

prices reaching +40% in March.

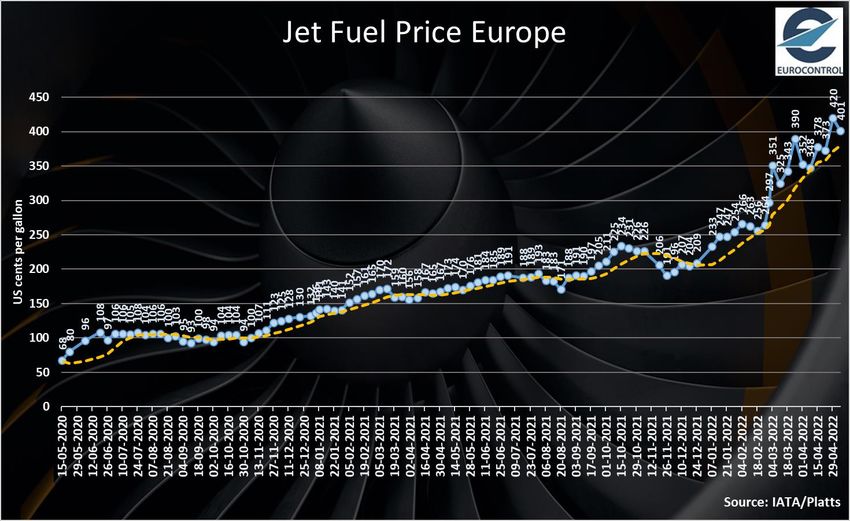

Jet fuel prices increased at 401 cts/gallon on 6 May (+14% over one month, +72% since early January).

2

2

Economics

EU27 annual inflation

rate increased from 1.7%

in March 2021 to 7.8% in

March 2022.

Energy prices have

recorded the highest

annual rate and reached

40% in March 2022 (vs.

March 2021)

SUPPORTING EUROPEAN AVIATION 3

Top 10 Busiest Airports, Flows, Market segments & Fuel price

Economics

(6 May 2022)

Fuel price

401

cents/gallon

compared to

373 cents/gallon on 22 April 2022

Source: IATA/Platts

4

SUPPORTING EUROPEAN AVIATION 4

Overall traffic situation at network level

On week 5 – 11 May:

27,101 average daily

flights.

+2% on previous week.

86% of 2019 traffic

levels.

Constant increase since

mid April 2022.

SUPPORTING EUROPEAN AVIATION 5

Current situation compared to the latest EUROCONTROL traffic

scenarios

EUROCONTROL has

published new traffic

scenarios on 6 April 2022.

For the first 11 days of

May, network traffic is at

86% of 2019 levels,

slightly above the high

scenario.

On a year to date basis,

network traffic in 2022

stands at 73% of 2019.

SUPPORTING EUROPEAN AVIATION 6

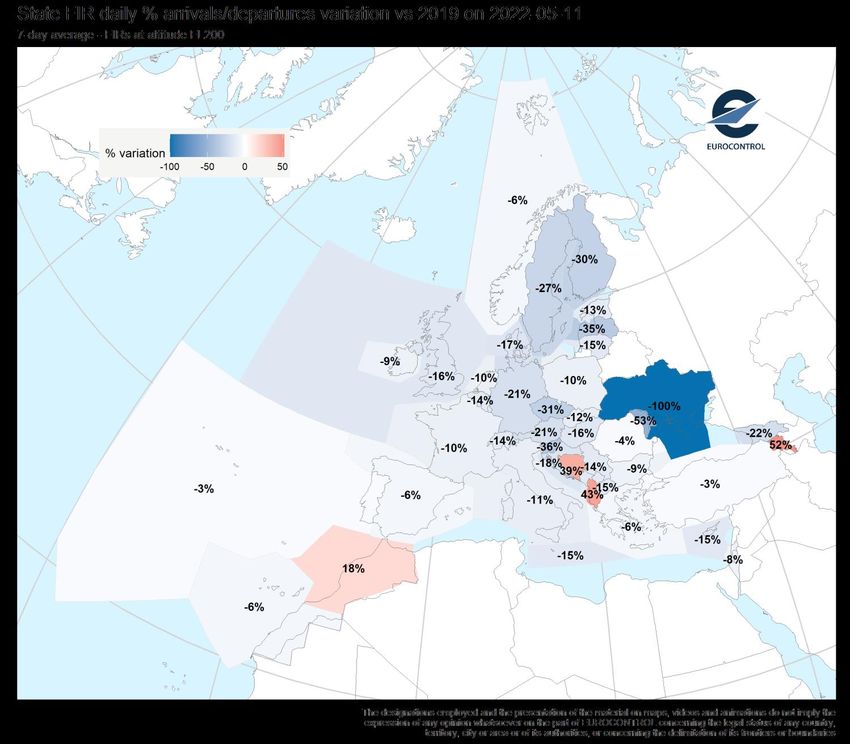

Ukraine invasion

Evolution of overflights (between Week 2-8 May 2022 and Week 2-8 May 2019)

Variation of overflights between

week 2-8 May 2022 and

week 2-8 May 2019

The invasion of Ukraine is affecting

overflights in a number of countries,

notably:

Negatively: Lithuania, Poland,

Estonia and Latvia.

Positively: Armenia and Georgia.

SUPPORTING EUROPEAN AVIATION 7

Aviation Sustainability

Network:

- Traffic variation -27%

- CO2 variation -30%

SUPPORTING EUROPEAN AVIATION 8

Market Segments

Up until the 11 May 2022, compared

to 2019:

Two segments are above 2019

levels: All-cargo (+2%) and Business

Aviation (+10%).

Low-Cost (-9%) records a continuous

increase since the beginning of 2022

Charter (-23%) decrease mainly

since the start of the Russian

invasion of Ukraine.

Mainline and Regional (-24%)

continued to catch up vs 2019 since

the beginning of 2022.

Note: a new Segment “Regional” has been

created by selecting commercial flights

operated by aircraft types between 19 and

120 seats.

SUPPORTING EUROPEAN AVIATION 9

Aircraft operators (Average daily flights for the last week)

Top 10 Within the top 10, 8 airlines posted increases over the

previous week, highest being:

Lufthansa (+44 flights; +4%) mainly due to

domestic as well as flows with UK, US and France.

easyJet (+39 flights; +3%) mainly due to Greece-UK,

Spain-UK, France-France, France-UK and Italy-UK.

Ryanair (+36 flights; +1%) mainly due to Italy-Italy,

Spain-UK and France-UK.

SAS (+33 flights; +6%) mainly due to Norway-

Norway, Sweden-Sweden, Norway-Sweden and

Poland-Sweden.

British Airways (+23 flights; +3%) mainly due to UK-

UK, Germany-UK, UK-US, Spain-UK, Greece-UK and

Netherlands-UK.

Ryanair is the busiest Aircraft Operator with 2,865 flights per day

Vueling (+19 flights; +3%) mainly due to Spain-

on average over last week, followed by easyJet (1,559), Turkish

Spain, Spain-UK, Germany-Spain, Italy-Spain and

Airlines (1,320), Lufthansa (1,244), Air France (1,014), KLM (808)

Portugal-Spain.

and Wizz Air (740).

The rankings remained unchanged compared with previous week. SUPPORTING EUROPEAN AVIATION 10Aircraft operators (Average daily flights for the last week)

Top 40

Largest increases in flights vs previous week for TUI (+17%), Lufthansa (+4%),

easyJet (+3%), Ryanair (+1%), SAS (+6%), Jet2.com (+10%), BA (+3%), Vueling

(+3%), United Airlines (+13%) and Delta Airlines (+17%).

Traffic levels ranging from -45% (Air Europa) to +24% (Wizz Air) vs 2019.

SUPPORTING EUROPEAN AVIATION 11New Aircraft Deliveries (Airbus vs. Boeing)

Airbus to deliver more new

aircraft to European

operators in the next 5 years.

In 2022 (year to date): 67

more sustainable NEO (28)

and MAX (39) aircraft

delivered.

In 2022 (year to date) Ryanair

leading the way with (18) 737

MAX 8200 deliveries.

SUPPORTING EUROPEAN AVIATION 12Aircraft operators (Average daily flights for the last week)

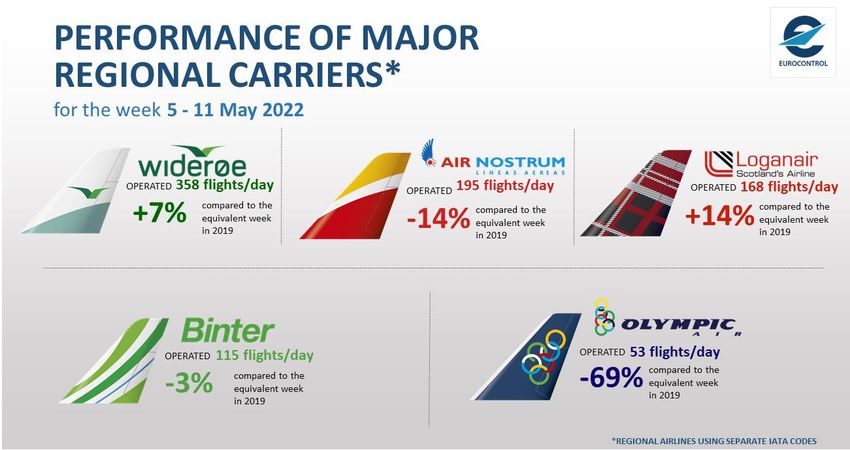

Cargo, Legacy, Low Cost and Regional Carriers

SUPPORTING EUROPEAN AVIATION 13States (Average Daily Departure/Arrival flights for the last week)

Within the top 10, all States posted flight

increases over the previous week, amongst

which:

UK (+196 flights; +4%): mainly TUI,

Jet2.com and easyJet. Domestic flows by

far and flows with Greece, Spain and US.

Greece (+112 flights; +10%): TUI,

Corendon, Jet2.com and easyJet. Flows UK

by far followed by domestic flows.

Spain (+82 flights; +2%): Mainly light AOs,

Vuelinf, TUI and Iberia. Domestic flows by

far as well as flows with UK.

Italy (+68 flights; +2%): Mainly Ryaniar,

Avionord, Italian Air Force and ITA. Flows

UK is the State with the highest number of dep/arr flights on average over

with Germany, Italy, US and UK.

last week (5,230) followed by Germany (4,758), Spain (4,581), France (3,985)

Germany (+60 flights; +1%): Mainly

and Italy (3,413).

Lufthansa. Flows with Greece, Italy, France,

The rankings remained unchanged compared with the previous week. US and Turkey.

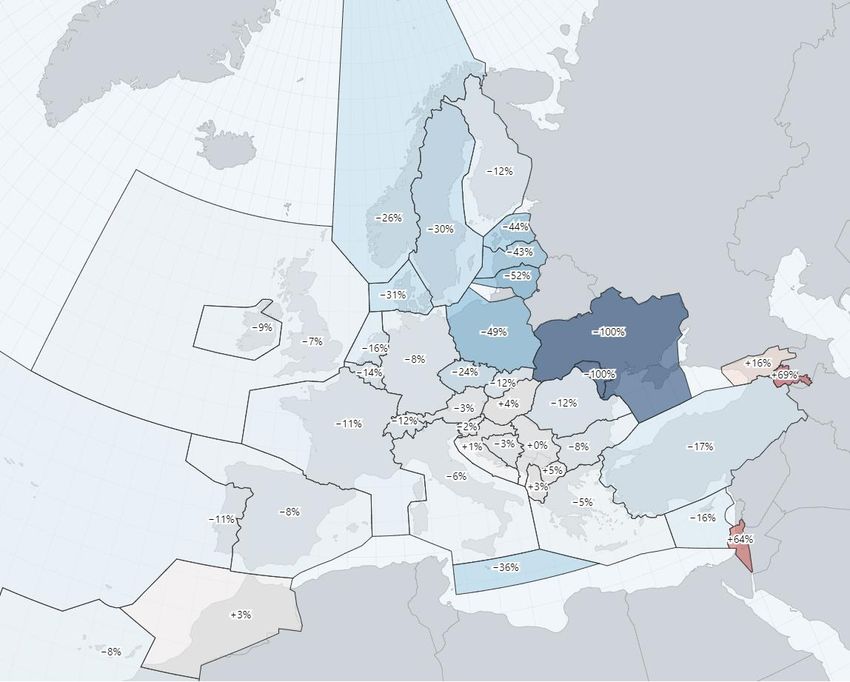

SUPPORTING EUROPEAN AVIATION 14States (Average Daily Departure/Arrival flights for the last week)

SUPPORTING EUROPEAN AVIATION 15States (Average Daily Departure/Arrival flights for the last week)

Top 40

Highest increases in flights vs previous week for UK (+4%), Greece (+10%), Spain (+2%),

Italy (+2%), Germany (+1%), Morocco (+9%), Denmark (+5%) and Poland (+4%)

Highest decreases for Romania (-5%).

Traffic levels ranging from -100% (Ukraine) to +52% (Armenia), compared to 2019.

SUPPORTING EUROPEAN AVIATION 16Traffic flows (Average Daily Departure/Arrival flights for the last week)

The main traffic flow is the intra-Europe flow with 21,999 flights on average the most recent week, increasing by 2%

over the previous week.

Flows between Europe and Other Europe (incl. Russia) are at -82% compared to 2019.

Important lockdown in China, owing to a surge in COVID-19 cases is affecting Chinese domestic flows (next slide).

Intra-Europe flights are at -12% compared to 2019 while intercontinental flows are at -25%.

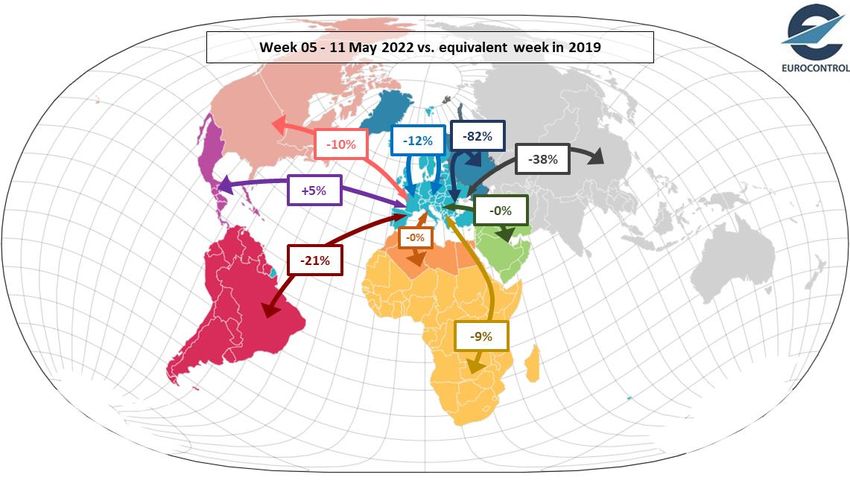

SUPPORTING EUROPEAN AVIATION 17Outside Europe (traffic situation over the last week vs 2019)

Week 5-11 May2022 vs equivalent week in 2019

USA (2-8 May)

Domestic -14%

China (3-9 May)

International -14% Europe (5-11 May)

Domestic -68%

Intra European -12%

International -75%

International -25%

Middle East (3-9 May)

Domestic +2%

International -13%

SUPPORTING EUROPEAN AVIATION 18Long haul Airport-Pairs (Average Daily flights for the last week)

Top 20

Within the top 20, long-haul airport pairs,

over the last week:

Increases for:

London Heathrow – New York JFK (+1 flight)

London Heathrow – Los Angeles (+2 flights)

London Heathrow – New York Newark (+1 flight)

London Heathrow – Chicago O Hare (+1 flight)

London Heathrow – San Francisco (+1 flight)

Frankfurt – New York JFK (+2 flights)

Decreases for:

Paris CDG –Dubai (-2 flights)

London Heathrow – Washington (-1 flight)

Frankfurt – Seoul (-2 flights)

SUPPORTING EUROPEAN AVIATION 19Country pairs (Average Daily flights for the last week)

Top 10

Within the top 10, five flows posted an

increase over the previous week for:

Spain-Spain (+41 flights; +4%): mainly

due to light AOs, Iberia, Vueling and One

Air.

UK-UK (+32 flights; +4%): mainly due to

BA Shuttle, West Atlantic UK, TUI and

Loganair.

Spain-UK (+29 flights; +4%): mainly due

to TUI by far, Jet2.com, BA, easyJet and

Ryanair.

Seven of the top 10 flows are domestic.

Spain-Spain is the country-pair with the highest number of dep/arr flights Highest decreases for:

(1,188) followed by France-France (1,008), Turkey-Turkey (874), Norway- Turkey-Turkey (-31 flights; -3%): mainly

Norway (864), Italy-Italy (853), UK-UK (824), Spain-UK (807) and Germany- due to Turkish Airlines, light AOs and

Germany (714). Pegasus.

The rankings remained almost unchanged compared with the previous week.

SUPPORTING EUROPEAN AVIATION 20Country pairs (Average Daily flights for the last week)

Top 40

Highest increase in flights vs previous week for Greece-UK (+26%), Spain-Spain (+4%),

UK-UK (+4%), Spain-UK (+4%), UK-US (+10%), Germany-Greece (+12%), Poland-

Poland (+13%), Germany-Italy (+4%) and Greece-Greece (+4%).

Highest decrease for Turkey-Turkey (-3%).

SUPPORTING EUROPEAN AVIATION 21Airports (Average Daily Departure/Arrival flights for the last week)

Top 10

Within the top 10, all airports recorded

increases over the previous week:

Frankfurt (+47 flights; +4%): Lufthansa and

Air Dolomiti. Mainly Germany, US, UK and

Austria.

London Gatwick (+37 flights; +6%): easyJet,

BA, TUI and Vueling. Flows with Greece,

Italy and Spain.

Paris/CDG (+35 flights; +3%): Air France.

Flows with Germany, France, US and Italy.

Munich (+30 flights; +4%): Lufthansa. Flows

with UK, Italy, Denmark, US and France.

Amsterdam is the airport with the highest number of dep/arr flights (1,303) London/Heathrow (+29 flights; +3%): BA,

followed by IGA Istanbul (1,197), Paris CDG (1,190), Frankfurt (1,167) and Delta Lufthansa and United Airlines. Flows

London Heathrow (1,137). with US, UK and Germany.

The rankings remained unchanged compared with the previous week.

SUPPORTING EUROPEAN AVIATION 22Airports (Average Daily Departure/Arrival flights for the last week)

Top 40

Highest increases in flights vs the previous week for Frankfurt (+4%), Gatwick (+6%),

Paris CDG (+3%), Munich (+4%), Heathrow (+3%), Manchester (+6%), Copenhagen

(+5%), Madrid (+3%), Warsaw (+7%), Barcelona (+3%) and Oslo (+4%).

Highest decreases for Paris/Orly (-4%), Istanbul/Sabiha (-14%) and Berlin (-2%).

Traffic levels ranging from -33% (Dusseldorf) to +6% (Palma), compared to 2019.

SUPPORTING EUROPEAN AVIATION 23Airports (Evolution of Network daily departure delay in 2022)

Security, Immigration, Custom & Health related delays

Preliminary data for April 2022

already show an increase of

average daily departure delays per

flight in April compared to March:

• Airline related delays: +84%

reaching 5.7 min/departure.

• en-route ATFM delays: +567%

reaching 0.8 min/departure.

• Governmental related delays

(Security, Immigration, Custom

& Health): +33% reaching 0.8

min/departure.

• Airport related delays: +30%

reaching 1.3 min/departure.

Note: Data for April 2022 are still

preliminary.

SUPPORTING EUROPEAN AVIATION 24Top 40 Global airports (Average Daily Departure flights for the last week)

Comparing last week

(right) with the same week

in 2019 (left):

Eight European airports

are ranked in the top 40

global airports, with four

(Amsterdam, IGA

Istanbul, Paris CDG,

Frankfurt and London

Heathrow) in the top 20.

The top 10 global

airports are currently all

based in the US except

Amsterdam.

The first Asian airport is

currently New Delhi

(14th) where it used to

be Beijing (6th in 2019).

SUPPORTING EUROPEAN AVIATION 25Economics

Jet fuel prices

continued to climb

and hit 401 cts/gallon

on 6 May (+14% vs.

one month ago).

Jet fuel prices in 2022

increased by 72%

compared to January

2022.

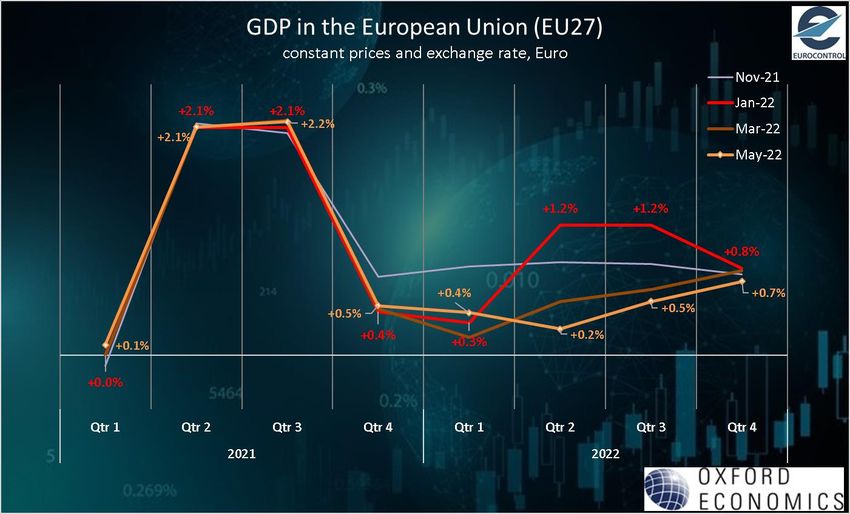

SUPPORTING EUROPEAN AVIATION 26Economics

Due to Russia’s invasion of

Ukraine, Oxford Economics

GDP growth forecasts for 2022

Q2 and 2022Q3 are revised

downward (-1pp and -0.7pp

respectively compared to

Jan22 forecast), a combination

of higher-for-longer inflation

and lower growth, mainly via

more-subdued consumption.

For 2022, EU27 GDP is

expected to record a 2.9%

growth in the base scenario.

Uncertainty remains very high,

with risks skewed to the

downside.

SUPPORTING EUROPEAN AVIATION 27To further assist you in your analysis, EUROCONTROL provides the following additional

information on a daily basis (daily updates at 7:00 CET for the first item and 12:00 CET for the

second) and every Friday for the last item:

1. EUROCONTROL Daily Traffic Variation dashboard:

www.eurocontrol.int/Economics/DailyTrafficVariation (or via the COVID-19 button on the

top of our homepage www.eurocontrol.int)

• This dashboard provides traffic for Day+1 for all European States; for the largest airports;

for each Area Control Centre (ACC) and for the largest airline operators.

2. COVID Related-NOTAMS with Network Impact (i.e. summary of airspace restrictions):

https://www.public.nm.eurocontrol.int/PUBPORTAL/gateway/spec/index.html

• The Network Operations Portal (NOP) under “Latest News” is updated daily with a

summary table of the most significant COVID-19 NOTAMs applicable at 12.00 UTC.

3. NOP Recovery Plan.

https://www.public.nm.eurocontrol.int/PUBPORTAL/gateway/spec/index.html

• This report, updated every Friday, is a special version of the Network operation Plan

supporting aviation response to the COVID-19 Crisis. It is developed in cooperation with

the operational stakeholders ensuring a rolling outlook. © EUROCONTROL - May 2022

This document is published by EUROCONTROL for information purposes. It may be copied in whole

or in part, provided that EUROCONTROL is mentioned as the source and it is not used for commercial

purposes (i.e. for financial gain). The information in this document may not be modified without

For more information please contact aviation.intelligence@eurocontrol.int prior written permission from EUROCONTROL.

www.eurocontrol.int

SUPPORTING EUROPEAN AVIATION 28You can also read