EQUITY OUTLOOK March 2021 - Verdant India

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

EQUITY OUTLOOK March 2021

MACRO

MARKET RALLY

The market rally has been supported by two drivers

Bounce back in corporate earnings as cost cuts,

Liquidity driven by lower rates globally tail winds in certain sectors like IT/pharma and

lower-than-expected stress in financials

Latest Monetary Policy Rates EPS growth(%)

Nifty-50 sectors, March fiscal

year-ends, 2021E-23E (based on

current constituents)

36

2021E 2022E 2023E

Nifty 50 Index 21.0 24.7 18.2

15

-0.1 0.25 0.1 0.25 2 0 3.85 4 0 0 3.75 0 4.25 1 4.25 Banks 38 35 20

Pharma 44 8 26

SOURCE: Kotak Institutional Equities, IMF

EMERGING MARKETS PERFORMANCE

FYTD Performance

72% 71% 69%

64% 61%

53% 51%

47%

41% 38%

33%

28%

23%

19%

SOURCE: Bloomberg

MARKET CAP TO GDP BY COUNTRY

World 121.22

US 207.26

China 77.93

Hong Kong 1933.57

Japan 135.51

UK 116.64

France 105.41

India 93.74

Canada 152.89

Germany 65.9

Saudi Arabia 298.56

South Korea 132.21

Switzerland 287.11

Taiwan 532.93

Australia 120.32

Sweden 219.41

SOURCE: Economic Times, Bloomberg

EQUITY FLOWS IN EMERGING MARKETS

• High liquidity and low interest rates

have led to inflows of equities in

Emerging markets.

SOURCE: Phillip Capital

GOLD, DOLLAR & BONDS • US Dollar Index has risen from a 31 month low in Dec • Gold in USD terms has appreciated by ~9.3% and in INR terms it has appreciated by ~9.6%. • Indian Bond yields too fell – India 10 year came down by 14 bps • US 10 year is up by 26 bps Particulars As on 29th February 2020 As on 28th February 2021 Change Gold INR/10gms 42352 46425 9.6% Gold USD/Oz 1585.85 1734.04 9.3% 10-Year G-Sec- India 6.37% 6.23% -2.2% 10-Year T Bill- USA 1.15% 1.41% 22.6% US Dollar Index 98.08 90.88 -7.3% SOURCE: Bloomberg

GOLD, DOLLAR & BONDS

Gold Futures, Brent Oil Futures, US Dollar Index & Nifty 50

160

140 Nifty 50, 131

Brent oil futures, 127

120

Gold Futures, 107

100

US Dollar, 93

80

60

40

20

0

Brent oil futures Nifty 50 Gold Futures US Dollar

• The Dollar Index is down by 7% while Gold has moved up by 7%

• In April-20, Brent Oil Futures were at the year low. It has appreciated since then, ending 27% higher

SOURCE:Investing.com

RELIEF PACKAGES, INFLATION & FISCAL DEFICIT

• US announced relief packages worth 13% of GDP to companies, small businesses and low income adults to

deal with the pandemic. Other countries which announced large relief packages are Japan, Canada and

Australia. YTD 2020 US Fed has increased the Balance sheet by 76% and since 2002 the number is 900%.

• In case of India, given the constraints on the fiscal deficit as well as the tightrope walk on the credit rating, the

size of fiscal stimulus announced is the optimum quantum of response (~ 1% of GDP) which maximizes the

support while minimizing the actual fiscal cost.

COVID-19 stimulus packages as share of GDP 2020

(as of October 2020)

21.1

16.4

14 13.2 12.8 12

8.9

7 6.9 6 6

4.9 4.4 4.3 3.4 3.4 0.7

SOURCE:Trading EconomiesRELIEF PACKAGES, INFLATION & FISCAL DEFICIT

• Inflation is below target rate across countries and in countries of Japan, Switzerland, Denmark and Eurozone have

negative central bank rates. US is holding rates at zero as inflation is running below target rate. Across the countries,

Central banks have cut rates and real rates are currently negative – US at -1.1%, UK at -0.6%, India at -3.6%

Country Rate Central Bank Rate CPI YoY Real Rates

US Fed funds 0.13% 1.20% -1.10%

UK Bank Rate 0.10% 0.70% -0.60%

Canada Overnight 0.25% 0.70% -0.50%

Switzerland Target Rate -0.75% -0.70% -0.10%

Eurozone Deposit rate -0.50% -0.30% -0.20%

Japan Policy rate -0.10% -0.40% 0.30%

Australia Cash rate 0.10% 0.70% -0.60%

South Korea Repo rate 0.50% 0.60% -0.10%

Taiwan Discount rate 1.13% 0.10% 1%

China Loan Prime rate 3.85% -0.50% 4.40%

India Repo rate 4% 7.60% -3.60%

Russia Key Policy rate 4.25% 4.40% -0.10%

SOURCE: BloombergINFLATION ▪ CPI, Core & Headline saw a dip ▪ Across Categories CPI saw dip, apart from a slight uptick in Fuel & Light category SOURCE:Macquare

GROWTH

▪ Global growth estimated to decline by 3.5% in 2020 but expected to rise by 5.5% in 2021

▪ Advanced economies likely to grow by 4.3% in 2021 on the back of early roll out of vaccines

▪ Emerging economies are expected to grow by 6.3% in 2021 on the back of a contracted base

GDP Growth Rates

SOURCE:World Economic Outlook, Jan 2021, IMF (Note- Data for India is presented on a fiscal year basis, remaining are on calendar year basis)INDIAN ECONOMY

▪ India’s GDP growth for FY21 is estimated to

decline by 7.7%, hit by the global pandemic Annual growth of GDP & demand components at constant prices

and the lockdown

▪ Private consumption estimated to contract by

9.5% in FY21 based on income loss, mobility

restrictions, and supply constraints

▪ Government consumption estimated to rise by

5.8% due to increased expenditure as part of

pandemic relief packages.

▪ Investment estimated to decline by 14.5% due

to economic uncertainty and delay in

implementation of capital projects

SOURCE: Data until FY20 is taken from the first revised estimates of GDP (dated 29 Jan 2021); Growth rates for FY21 are taken from the first advanced estimates of

GDP (dated 7 Jan 2021)VALUATION

INDIA VALUATION VS EMERGING MARKETS

Nifty 50 Valuation premium vs Emerging Markets (MSCI) - %

80

70 Premium (RHS,%) Average

60

50

40

30

20

10

0 Mar-11

Mar-18

Jun-16

Aug-10

Aug-17

Oct-11

Feb-14

Sep-14

Oct-18

Feb-21

Dec-12

Jul-13

Dec-19

Jul-20

Jan-10

May-12

Apr-15

Jan-17

May-19

Nov-15

• Even after the rally we have seen so far, Indian markets are trading at near or slightly above its long-term

averages (@19.5x FY22).

• India’s valuation premium with respect to MSCI Emerging markets has remained stable at 40-45% over the last 4 months

indicating that the rally has been a global one.

• 1 year forward valuations for the Nifty stands at 21.4X PE which is at the higher end of the range in terms of historical

benchmarks.

• Weak dollar, strong Asian govt Balance sheets as compared to the West (debt as a % of GDP), earnings growth

differential / strong EM earnings recovery to favour EMs going ahead.

SOURCE: BloombergMID CAP VALUATION

NSE Midcap vs Nifty PE Prem/(Disc) %

120

100

80

60

40

20

0

-20

-40

-60

Mar'05 Dec'06 Sep'08 Jun'10 Mar'12 Dec'13 Sep'15 Jun'17 Mar'19 Dec'20

Prem/(Disc) (%) Average

• The headline valuations for Nifty Midcap 100 suggest that we are in an acceptable zone which can act as a platform for the

broader markets to do better from hereon.

• Midcaps in a growing market with market leadership and low leverage can be equally attractive investment option as any

large cap. Sector performance has so far been led by large caps, but gradually within sectors mid-caps and small caps are

emerging as top performers. In the sectors with post-Covid tailwinds viz. pharma, digitization, ecommerce, electronic

manufacturing, large caps and midcaps are adequately represented and in some cases even dominated by midcaps.

• Covid impacted most sectors, however certain sectors have emerged as relatively Covid-proof i.e. Pharma, Telecom,

Packaged foods, Chemicals, Digital spending and Digital transformation.

SOURCE: BloombergVALUATIONS

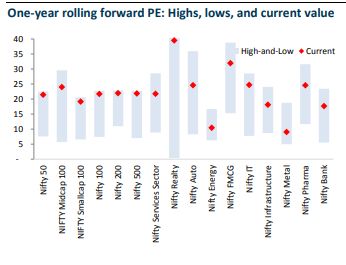

▪ Most segments are at one year highs in terms

of one year rolling forward PE-

▪ Nifty 50, Nifty Smallcap 100, Nifty 100, Nifty

200, Nifty 500

▪ Segments like Nifty Energy & Nifty Metal are at

the lower end of their 1 year range

SOURCE: Phillip CapitalSECTOR

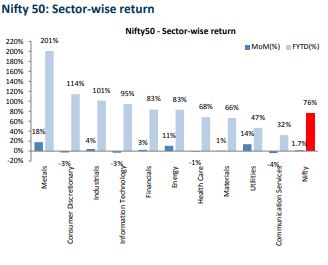

SECTOR WISE UPDATE – NIFTY 50

▪ Metals remains the highest contributor to

Nifty50 FYTD and for Feb’21

▪ Other significant contributors were – Utilities

& Energy

SOURCE: Phillip CapitalSECTORAL & MARKET CAP INDICES

▪ Metals & Small Cap indices are the highest

gainers FYTD & for Feb’21

▪ Auto, IT, Pharma & FMCG were negative in

Feb’21

▪ Energy, Realty & Mid Cap were amongst the

highest gainers in Feb’21

SOURCE: Phillip CapitalINFRASTRUCTURE THEME

INVESTMENT CYCLE

• Investment rate as a % of GDP declined steadily from about 35% in early 2010s to 27% by end of the decade.

• For economic growth to sustain at 6-7%, investment cycle has to revive and play its role

• Three important levers required for a virtuous capex cycle seem to be falling in place- new global dynamics, domestic macro &

proactive government policy

PRIVATE CAPEX

• Private companies with high debt levels and weak balance sheet have either exited or been taken over, leaving behind a stronger Indian

Private Sector

• Government’s production-linked incentive (PLI) has witnessed remarkable early success and is likely to be widened to other “Champion”

sectors

• The emphasis of the PLI scheme is on encouraging scale in downstream capacities which will in due course lead to commensurate

additions in upstream capacities as well

• Production Linked Incentives to boost manufacturing across sectors like Pharma, Auto, Electronics, Solar PV etc

• Stable domestic macro in terms of lower interest rates and liquidity support will aid greater risk appetite in the private sector

• We are also witnessing green shoots in the capex cycle of the domestic centric sectors viz. Cement, consumer goods and paints.

SOURCE: CSO, Internal ResearchINFRASTRUCTURE THEME

GLOBAL DYNAMICS

• Global move towards reshaping of manufacturing supply chains from China has led to many global MNCs looking at India as a

manufacturing base.

• The trend has been accelerated by the COVID 19 pandemic

GOVERNMENT STEPS & BUDGET IMPACT

• The government has allocated significant spending on capital expenditure which is expected be beneficial for cyclical sectors such as

industrials, capital goods, metals & mining etc.

• Infrastructure and manufacturing revival is likely be a key theme for FY-22 due to the focus on growth in these sectors in the budget.

• Increased spending on key infrastructure such as Power, highways, gas distribution networks, renewable energy and transportation is also

a positive for infrastructure sector.

• Labour Reforms, consolidating various laws into 4 codes

SOURCE: CSO, Internal ResearchOUTLOOK

POST BUDGET OUTLOOK

• Overall, budget has provided for higher government spend without increase in personal and corporate taxes or

cess. coupled with reforms and greater privatisation thrust

• This will support economic recovery, create earning upgrades in FY22 and thus support India’s premium

valuations

• Though there is a likelihood of slightly higher interest rates as a result, it can get offset by superior earnings

momentum especially if the budget is successful in reviving the investment cycle

• No changes in capital gains structure is also a sentiment positive.

• Overall, positive for cyclical recovery in earnings at the expense of higher fiscal deficit.

• Big boost on capital expenditure for FY 22.

• For funding, significant institutional setup planned to execute and monitor monetisation of assets owned by

PSUs or government undertaking

• Three key reforms for financial markets: single securities market code, improve liquidity in bond markets and

increase in FDI limit to 74%

• Big push on privatisation - 2 PSU banks and 1 general insurance company also likely to be privatised. More PSUs

to be added to the list of privatisation and land monetisation also on the cards

• Setting up of ARC to buy stressed assets will enable faster resolution at the NCLINDIA: NEW PHASE OF ECONOMIC GROWTH BECKONS

▪ The government’s cautious approach in providing explicit fiscal support (contained at c1.5% of GDP) is now

coming in handy as the relatively stable macro variables (current account deficit, fiscal deficit, INR/USD) has

helped attract its due share of portfolio inflows.

▪ The initial sharp cut in corporate earnings FY22 forecast of 15-20% for BSE 200 has been followed up by almost

a 10% upgrade from the bottom

▪ The eventual FY22 earnings estimate may not look too different from the pre-Covid forecasts. This has been a

result of multiple factors

▪ certain sectors like IT services, Pharma and Telecom have gained from the emerging tailwinds post-Covid.

▪ cost declines has been the key reason for the disconnect between the positive EBIT growth of 15-17% in

BSE 200 companies for Sep-quarter as against GDP decline of 7.5%.

▪ lower-than-expected bad debt provisions in Banks and NBFCs.ORGANISED VS UNORGANISED

▪ the top corporates in the listed universe have coped with and bounced back from the pandemic much better

than the unorganised/informal sectors with the help of market share gains and cost cuts.

▪ the informal sector has been at the receiving end for last 3 years with demonetisation, GST implementation,

NBFC crisis and now Covid.

▪ It is here that the concern for the GDP growth arises as informal sector accounts for bulk of the employment

and a prolonged slowdown there would eventually impact consumption (60% of GDP in 2019) and economic

growth eventually.DEBT & GDP India’s public debt to GDP has been significantly low compared to other countries SOURCE: Economic Survey 2020-21

EQUITY INVESTMENTS

WHY INVEST IN EQUITIES

▪ Market are trading at 5-10% high compared to historical valuations, yet it may be the right time to

invest in equities because-

▪ Lower interest rates

▪ Weaker dollar

▪ Normal range of valuation premium amongst emerging markets

▪ Recovery of economy leading to opportunities to generate above average returns

SOURCE: BloombergSEGMENTS TO LOOK AT

▪ Infra/Manufacturing/Capital Goods - Post budget the momentum in the revival of capex cycle and investment

cycle has increased. The investment cycle is pushed by the government as well as the private sector through the

PLI schemes.

▪ Mid & small caps - Many companies in Infra/Manufacturing/Capital goods are Mid & Small Caps. The market is

expected to become more broad-based

▪ Pharma & IT - the sectors are still doing well but the stock performance has slowed down. Hence, the

valuations are better now.FUND HIGHLIGHTS

TATA BALANCED ADVANTAGE FUND - EQUITY ALLOCATIONS

(An open ended dynamic asset allocation fund.)

MARKET SCENARIOS AND CHANGE IN EQUITY ALLOCATIONS

70 16000

65 14000

64

60 61 12000

If a majority of macro factors58

Equity Allocation

55 are positive, equity 10000

Nifty 50

allocations are increased 53

50 8000

50

49 48 48 49 49 48 49

48 48 48 47

45 46 47 6000

44 43 44

40 41 4000

38

If a majority of macro

38

35 factors are negative, equity 2000

allocations are decreased

30 0

Jul-19

Jul-20

May-19

May-20

Mar-19

Apr-19

Oct-19

Mar-20

Apr-20

Oct-20

Nov-19

Dec-19

Jan-20

Nov-20

Dec-20

Jan-21

Jun-19

Aug-19

Sep-19

Feb-20

Jun-20

Aug-20

Sep-20

Feb-21

Equity Allocation Nifty 50

*Source: NSE, MFI

Category Average: Average of equity exposures of all Balanced Advantage Funds in MFINAVIGATING BULLS & BEARS

Fund Movement compared to Nifty 50

Market Rally

29th Apr'20 to 28th Feb'21

Average PE suggests low Equity

Allocation, Momentum indicators

26th Mar'20 to 29th Apr'20 have helped maintain higher levels

The fund is able to capture upside

23rd Mar'20 to 26th Mar'20

in rallies

In terms of the current Equity allocation,

Market Correction the portfolio is positioned to navigate both

18th Mar'20 to 23rd Mar'20

— market uptrend based on recovery hope

•Trailing PE based on past earnings and market correction

12th Mar'20 to 18th Mar'20 goes down

•Forward PE based on expected

future earnings falls by less

6th Mar'20 to 12th Mar'20

Equity allocations based on an

average of the two remains lower

than if based on only Trailing PE

18th Dec'19 to 6th Mar'20

The fund’s NAV drawdown is

-20.00% 0.00% 20.00% 40.00% 60.00% limited in market downturns

Nifty 50 Tata Balanced Advantage Fund

*Source: Internal CalculationTATA MULTI ASSET OPPORTUNITIES FUND - ASSET ALLOCATION

(An Open Ended Scheme investing in equity, debt & exchange traded commodity derivatives)

Scheme asset allocation(%) on a monthly basis

Current

Equity Commodities Commodities Treps, Repo Margin

Debt Assets/Liabilit

Unhedged Unhedged hedged & Cash Deposits

ies

Feb’21 64.52 8.32 7.40 11.64 16.91 2.25 -13.07

Jan’21 62.71 12.18 5.96 9.42 21.95 2.54 -16.97

Dec’20 66.70 9.51 2.92 6.08 20.04 2.66 -7.91

Nov’20 65.83 10.25 3.53 15.04 7.68 2.87 -5.24

Oct'20 67.09 11.06 3.49 12.89 7.74 3.1 -5.35

Sep'20 66.34 10.2 4.28 10.67 9.3 3.16 -3.95

Aug’20 65.1 10.38 1.97 18.46 4.57 3.83 -4.31

Jul ‘20 66.72 10.11 0.97 16.03 2.74 3.39 0.05

Jun ‘20 66.07 9.24 0.41 12.73 15.38 3.57 -7.39

May ‘20 65.88 8.16 0 6.44 20.88 3.67 -5.03

Apr ‘20 65.68 8.09 0.86 13.9 13.02 3.68 -5.23

Mar’ 20 57.18 8.67 0.82 - 30.8 3.41 -0.88TATA MULTI ASSET OPPORTUNITIES FUND - ASSET ALLOCATION

Fund Movement (Rebased to 100)

140 Tata Multi Asset

Opportunities Fund, 131

130

Nifty 50, 129

120

110 Fund Benchmark, 125

100

90

80

70

60

Tata Multi Asset Opportunities Fund Fund Benchmark Nifty 50TATA ARBITRAGE FUND – EXPIRY TO EXPIRY RETURNS

(An open ended scheme investing in arbitrage opportunities.)

▪ Expiry to Expiry returns have varied with some months showing higher returns

▪ Staying invested for the short to medium term is beneficial for the investor

14.03%

8.52%

7.06%

5.52%

5.12%

3.98%

3.37%

3.05%

2.68%

1.80% 2.00% 1.92%

1.10%

0.57% 0.68% 0.45% 0.42%

0.25% 0.28% 0.22% 0.33% 0.15% 0.17% 0.16%

-0.04%

-0.48%

Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21

Absolute Returns Annualized ReturnTATA LARGE & MID CAP FUND– PORTFOLIO CONSTRUCTION

(An open-ended equity scheme investing in both large cap & mid cap stocks.)

STEADY RETURNS LOW DEBT AND HIGH FREE CASH

FLOWS

Preference for stocks that have shown consistent

performance over the past. Companies that are low debt and therefore able to

retain a greater part of their revenues as profits.

PORTFOLIO

CONSTRUCTION

EARNINGS SURPRISE GROWTH AT REASONABLE PRICE

Stocks that the fund managers have a more positive The fund manager pricks stocks on individual merit

view on than the market consensus and thus will be and is not wedded to the benchmark

able to surprise on earnings

*Current portfolio construction strategy, and is subject to change in the futureTATA LARGE & MID CAP FUND– FUND PERFORMANCE

Tata Large & Mid Cap Fund Nifty Large Midcap 250 TRI* S&P BSE Sensex TRI#

Period Return % Rs. Return % Rs. Return % Rs.

1 Year 31.66% 13,157 36.62% 13,650 30.00% 12,990

3 Year 12.19% 14,116 11.01% 13,674 14.22% 14,894

5 Year 16.65% 21,593 18.54% 23,391 17.89% 22,764

Since Inception 12.59% 277,245 NA NA 12.32% 259,497

Managed by: Chandraprakash Padiyar (Managing Since 3-Sep-18) & Meeta Shetty (Managing Since 1-Nov-19)

Tata Large & Mid Cap Fund Nifty Large Midcap 250 TRI* S&P BSE Sensex TRI#

Period Amt. invested Return % Rs. Return % Rs. Return % Rs.

1 Year 120,000 72.59% 162,156 80.52% 166,407 64.31% 157,657

3 Year 360,000 22.19% 496,678 21.96% 495,124 20% 481,847

5 Year 600,000 15.80% 889,431 16.37% 901,956 16.62% 907,381

Since Inception 2,460,000 17.85% 20,639,303 14.13% 6,564,089 15.28% 14,841,217

Inception Date 25-Feb-93 First Installment date 01-Mar-93 Managing since 03-Sep-18SWINGS IN LONG TERM SIP PERFORMANCE

SIP 5 Year CAGR

Scheme

As on 31st March 2020 As on 28th Feb 2021

Tata Hybrid Equity Fund -4.33% 10.38%

(An open ended hybrid scheme investing predominantly in equity & equity related instruments.)

B: Crisil Hybrid 25+75 - Aggressive Index 0.03% 14.47%

Tata Large & Mid Cap Fund -3.83% 15.80%

(An open-ended equity scheme investing in both large cap & mid cap stocks.)

B: Nifty Large Midcap 250 TRI -4.77% 16.37%

Tata India Tax Savings Fund -3.64% 14.24%

(An open ended equity linked savings scheme with a statutory lock in of 3 years and tax benefit)

B: S&P BSE Sensex TRI -1.25% 16.62%

Tata Large Cap Fund -5.59% 12.77%

(An open-ended equity scheme predominantly investing in large cap stocks.)

B: S&P BSE Sensex TRI -1.25% 16.62%

Tata Mid Cap Growth Fund -4.27% 17.95%

(An open-ended equity scheme predominantly investing in mid cap stocks.)

B: Nifty Midcap 100 TRI -11.05% 14.40%

Tata Equity PE Fund -5.25% 11.74%

(An open ended equity scheme following a value investment strategy)

B: S&P BSE Sensex TRI -1.25% 16.62%PERFORMANCE IN SEBI FORMAT,

OTHER PERFORMANCES & PRODUCT LABELS

Data as on 28th Feb 2021TATA ARBITRAGE FUND

Fund performance in SEBI format

Tata Arbitrage Fund Nifty 50 Arbitrage Index* Nifty 50 TRI#

Period Return % Rs. Return % Rs. Return % Rs.

1 Year 3.97% 10,396 1.86% 10,186 31.37% 13,127

3 Year NA NA NA NA NA NA

5 Year NA NA NA NA NA NA

Since Inception 5.41% 11,227 4.43% 10,999 15.31% 13,669

Managed by: Sailesh Jain (Managing Since 10-Dec-18)

Performance of other schemes managed by the FM

Sailesh Jain 1 Year 3 Year 5 Year

Tata Balanced Advantage Fund 22.67 NA NA

CRISIL Hybrid 35+65 - Aggressive Index 25.90 NA NA

Tata Nifty Exchange Traded Fund 31.29 NA NA

Nifty 50 TRI 31.37 NA NA

Tata Equity Savings Fund 12.71 6.75 8.02

NIFTY Equity Savings Index 15.44 9.35 10.69

Tata Nifty Private Bank Exchange Traded Fund 15.23 NA NA

Nifty Private Bank TRI 16.37 NA NA

Tata Quant Fund 8.66 NA NA

S&P BSE 200 TRI 33.70 NA NATATA LARGE & MID CAP FUND

Fund performance in SEBI format

Tata Large & Mid Cap Fund Nifty Large Midcap 250 TRI* S&P BSE Sensex TRI#

Period Return % Rs. Return % Rs. Return % Rs.

1 Year 31.66% 13,157 36.62% 13,650 30.00% 12,990

3 Year 12.19% 14,116 11.01% 13,674 14.22% 14,894

5 Year 16.65% 21,593 18.54% 23,391 17.89% 22,764

Since Inception 12.59% 277,245 NA NA 12.32% 259,497

Managed by: Chandraprakash Padiyar (Managing Since 3-Sep-18) & Meeta Shetty (Managing Since 1-Nov-19)

Performance of other schemes managed by the FM

Chandraprakash Padiyar 1 Year 3 Year 5 Year

Tata Hybrid Equity Fund 23.73 7.84 11.33

Crisil Hybrid 25+75 - Aggressive Index 28.36 12.04 15.82

Tata Small Cap Fund 38.57 NA NA

Nifty Smallcap 100 TRI 43.58 NA NA

Meeta Shetty 1 Year 3 Year 5 Year

Tata Digital India Fund 62.80 24.47 20.36

S&P BSE IT TRI 66.65 27.45 21.40

Tata India Pharma And Healthcare Fund 49.20 18.10 8.48

Nifty Pharma TRI 58.69 10.85 2.00TATA HYBRID EQUITY FUND

Fund performance in SEBI format

Tata Hybrid Equity Fund Crisil Hybrid 25+75 - Aggressive Index* S&P BSE Sensex TRI#

Period Return % Rs. Return % Rs. Return % Rs.

1 Year 23.73% 12,366 28.36% 12,827 30.00% 12,990

3 Year 7.84% 12,540 12.04% 14,060 14.22% 14,894

5 Year 11.33% 17,099 15.82% 20,835 17.89% 22,764

Since Inception 15.33% 374,922 NA NA 12.55% 201,879

Managed by: Chandraprakash Padiyar (Managing Since 3-Sep-18), Murthy Nagarajan (Managing since 1-Apr-17) & Satish Chandra Mishra (Managing Since 1-Nov-19)

Murthy Nagarajan 1 Year 3 Year 5 Year

Performance of other schemes managed by the FM Tata Retirement Savings Fund - Progressive Plan 21.83 8.66 17.67

S&P BSE 200 TRI 33.70 12.06 17.63

Chandraprakash Padiyar 1 Year 3 Year 5 Year Tata Retirement Savings Fund - Moderate Plan 20.60 8.26 15.41

Tata Large & Mid Cap Fund 31.66 12.19 16.65 Crisil Hybrid 25+75 - Aggressive Index 28.36 12.04 15.82

NIFTY Large Midcap 250 TRI 36.62 11.01 18.54

Tata Retirement Savings Fund - Conservative Plan 11.17 7.31 10.04

CRISIL Short Term Debt Hybrid 75+25 Fund Index 15.16 10.04 10.89

Tata Small Cap Fund 38.57 NA NA

Nifty Smallcap 100 TRI 43.58 NA NA Tata Equity Savings Fund 12.71 6.75 8.02

NIFTY Equity Savings Index 15.44 9.35 10.69

Tata Gilt Securities Fund 4.09 7.90 7.38

Satish Chandra Mishra 1 Year 3 Year 5 Year

Crisil Dynamic Gilt Index 6.64 9.47 8.41

Tata Resources & Energy Fund 54.55 12.60 18.51

Nifty Commodities TRI 45.76 5.12 17.51 Tata Medium Term Fund 8.13 1.71 4.13

Crisil Medium Term Debt Index 8.30 9.07 8.89

Tata Small Cap Fund 38.57 NA NA

Tata Medium Term Fund (Segregated Portfolio 1) -25.09 NA NA

Nifty Smallcap 100 TRI 43.58 NA NA Crisil Medium Term Debt Index 8.30 NA NA

Tata Short Term Bond Fund 7.07 5.67 6.27

CRISIL Short Term Bond Fund Index 7.52 8.53 8.16TATA INDIA TAX SAVINGS FUND

Fund performance in SEBI format

Tata India Tax Savings Fund S&P BSE Sensex TRI*

Period Return % Rs. Return % Rs.

1 Year 26.07% 12,599 30.00% 12,990

3 Year 9.45% 13,108 14.22% 14,894

5 Year 16.99% 21,902 17.89% 22,764

Since Inception 18.69% 716,044 13.11% 215,777

Managed by: Rupesh Patel (Managing Since 1-Apr-15) & Ennette Fernandes (Managing Since 18-Jun-18)

Performance of other schemes managed by the FM ENNETTE FERNANDES 1 Year 3 Year 5 Year

Tata India Consumer Fund 20.24 7.32 18.84

*

Nifty India Consumption TRI 20.43 7.69 14.19

RUPESH PATEL 1 Year 3 Year 5 Year

Tata Mid Cap Growth Fund 30.72 13.57 19.34 Tata Retirement Savings Fund - Moderate Plan 21.83 8.66 17.67

Nifty Midcap 100 TRI* 39.98 6.79 16.24 Crisil Hybrid 25+75 - Aggressive Index* 33.70 12.06 17.63

Tata Infrastructure Fund 33.64 5.04 14.75 Tata Retirement Savings Fund - Progressive Plan 20.60 8.26 15.41

S&P BSE India Infrastructure TRI* 49.26 0.11 13.59 S&P BSE 200 TRI* 28.36 12.04 15.82

Tata Large Cap Fund 25.41 9.41 14.05 Tata Retirement Savings Fund - Conservative Plan 11.17 7.31 10.04

*

S&P BSE Sensex TRI 30.00 14.22 17.89 CRISIL Short Term Debt Hybrid 75+25 Fund Index* 15.16 10.04 10.89

Tata Focused Equity Fund 28.99 NA NA Tata Ethical Fund 33.44 9.87 12.93

S&P BSE 200 TRI 33.70 12.06 17.63 Nifty 500 Shariah TRI 41.75 11.82 17.89

Effective from 9th March 2021, this fund will be managed by Tejas Gutka and Ennette FernandesTATA LARGE CAP FUND

Fund performance in SEBI format

Tata Large Cap Fund S&P BSE Sensex TRI*

Period Return % Rs. Return % Rs.

1 Year 25.41% 12,534 30.00% 12,990

3 Year 9.41% 13,095 14.22% 14,894

5 Year 14.05% 19,291 17.89% 22,764

Since Inception 19.62% 596,913 13.34% 174,429

Managed by: Rupesh Patel (Managing Since 18-Jun-18), Venkat Samala (Managing Since 26-Nov-20) & Ennette Fernandes (Managing Since 18-Jun-18)

Performance of other schemes managed by the FM ENNETTE FERNANDES 1 Year 3 Year 5 Year

Tata India Consumer Fund 20.24 7.32 18.84

RUPESH PATEL 1 Year 3 Year 5 Year *

Nifty India Consumption TRI 20.43 7.69 14.19

Tata India Tax Savings Fund 26.07 9.45 16.99

S&P BSE Sensex TRI* 30.00 14.22 17.89 Tata Retirement Savings Fund - Moderate

Plan 21.83 8.66 17.67

Tata Infrastructure Fund 33.64 5.04 14.75 Crisil Hybrid 25+75 - Aggressive Index* 33.70 12.06 17.63

S&P BSE India Infrastructure TRI* 49.26 0.11 13.59

Tata Retirement Savings Fund - Progressive

Tata Mid Cap Growth Fund Plan 20.60 8.26 15.41

30.72 13.57 19.34

S&P BSE 200 TRI* 28.36 12.04 15.82

Nifty Midcap 100 TRI* 39.98 6.79 16.24

Tata Retirement Savings Fund -

Tata Focused Equity Fund 28.99 NA NA Conservative Plan 11.17 7.31 10.04

S&P BSE 200 TRI 33.70 12.06 17.63 CRISIL Short Term Debt Hybrid 75+25 Fund

Index* 15.16 10.04 10.89

VENKAT SAMALA 1 Year 3 Year 5 Year

Tata Digital India Fund Tata Ethical Fund 33.44 9.87 12.93

62.80 24.47 20.36

S&P BSE IT TRI* Nifty 500 Shariah TRI 41.75 11.82 17.89

66.65 27.45 21.40

Effective from 9th March 2021, this fund will be managed by Amey Sathe & Venkat SamalaTATA MID CAP GROWTH FUND

Fund performance in SEBI format

Tata Mid Cap Growth Fund Nifty Midcap 100 TRI* Nifty 50 TRI#

Period Return % Rs. Return % Rs. Return % Rs.

1 Year 30.72% 13,062 39.98% 13,985 31.37% 13,127

3 Year 13.57% 14,643 6.79% 12,177 12.88% 14,378

5 Year 19.34% 24,193 16.24% 21,217 17.29% 22,189

Since Inception 12.78% 247,214 NA NA 10.81% 154,637

Managed by: Rupesh Patel (Managing Since 27-Jun-17) & Ennette Fernandes (Managing Since 18-Jun-18)

Performance of other schemes managed by the FM ENNETTE FERNANDES 1 Year 3 Year 5 Year

Tata India Consumer Fund 20.24 7.32 18.84

RUPESH PATEL 1 Year 3 Year 5 Year

Nifty India Consumption TRI* 20.43 7.69 14.19

Tata India Tax Savings Fund 26.07 9.45 16.99

S&P BSE Sensex TRI* 30.00 14.22 17.89

Tata Retirement Savings Fund - Moderate Plan 21.83 8.66 17.67

Crisil Hybrid 25+75 - Aggressive Index* 33.70 12.06 17.63

Tata Infrastructure Fund 33.64 5.04 14.75

S&P BSE India Infrastructure TRI* 49.26 0.11 13.59

Tata Retirement Savings Fund - Progressive

Plan 20.60 8.26 15.41

Tata Large Cap Fund 25.41 9.41 14.05 S&P BSE 200 TRI* 28.36 12.04 15.82

S&P BSE Sensex TRI* 30.00 14.22 17.89

Tata Retirement Savings Fund - Conservative

Tata Focused Equity Fund 28.99 NA NA Plan 11.17 7.31 10.04

CRISIL Short Term Debt Hybrid 75+25 Fund

S&P BSE 200 TRI 33.70 NA NA

Index* 15.16 10.04 10.89

Tata Ethical Fund 33.44 9.87 12.93

Nifty 500 Shariah TRI 41.75 11.82 17.89

Effective from 9th March 2021, this fund will be managed by Satish Chandra Mishra & Abhinav SharmaTATA EQUITY PE FUND

Fund performance in SEBI format

Tata Equity P/E Fund S&P BSE Sensex TRI*

Period Return % Rs. Return % Rs.

1 Year 27.82% 12,774 30.00% 12,990

3 Year 5.53% 11,752 14.22% 14,894

5 Year 17.52% 22,405 17.89% 22,764

Since Inception 18.22% 163,058 16.54% 128,380

Managed by: Sonam Udasi (Managing Since 1-Apr-16) & Amey Sathe (Managing Since 18-Jun-18)

Performance of other schemes managed by the FM

Sonam Udasi 1 Year 3 Year 5 Year Sonam Udasi 1 Year 3 Year 5 Year

Tata Flexi Cap Fund (previously known as Tata Multicap Fund) 23.01 NA NA Tata Banking And Financial Services Fund 19.01 13.03 21.81

S&P BSE 500 TRI 34.42 NA NA Nifty Financial Services TRI 18.92 16.07 23.32

Tata Index Fund - Sensex Plan 27.86 13.24 16.77 Tata India Consumer Fund 20.24 7.32 18.84

S&P BSE Sensex TRI 30.00 14.22 17.89

Nifty India Consumption TRI 20.43 7.69 14.19

Tata Retirement Savings Fund - Progressive Plan 21.83 8.66 17.67

S&P BSE 200 TRI Tata Value Fund Series - 1 21.03 NA NA

33.70 12.06 17.63

S&P BSE 200 TRI 33.70 12.06 17.63

Tata Index Fund - Nifty Plan 29.59 12.06 16.25

Nifty 50 TRI 31.37 12.88 17.29 Tata Value Fund Series - 2 20.24 NA NA

S&P BSE 200 TRI 33.70 12.06 17.63

Tata Retirement Savings Fund - Moderate Plan 20.60 8.26 15.41

Crisil Hybrid 25+75 - Aggressive Index 28.36 12.04 15.82

Amey Sathe 1 Year 3 Year 5 Year

Tata Digital India Fund 32.30 8.01 11.15

Tata Retirement Savings Fund - Conservative Plan 11.17 7.31 10.04

CRISIL Short Term Debt Hybrid 75+25 Fund Index S&P BSE IT TRI 33.70 12.06 17.63

15.16 10.04 10.89PERFORMANCE DISCLAIMERS

▪ 1) Scheme returns in terms of CAGR are provided for past 1 year, 3 years, 5 years and since inception.

▪ 2) Point-to-point returns on a standard investment of Rs. 10,000/- are in addition to CAGR for the schemes.

▪ 3) Different plans shall have a different expense structure. The performance details provided herein are of regular plan growth option except for Tata India Tax Savings

Fund & TATA Mid Cap Growth Fund where performance details given is for regular plan dividend option.

▪ 4 ) NA stands for schemes in existance for more than 1 year but less than 3 years or 5 years, or instances where benchmark data for for corresponding period not

available.

▪ 5) Period for which schemes performance has been provided is computed basis last day of the month - ended preceding the date of adversiment.

▪ 6) Past performance may or may not be sustained in future. For computation of since inception returns the allotment NAV has been taken as Rs. 10.00 *All payouts

during the period have been reinvested in the units of the scheme at the then prevailing NAV. Load is not considered for computation of returns. While calculating

returns dividend distribution tax is excluded. Schemes in existence for less than 1 year, performance details for the same are not provided.

▪ 7) For Benchmark Indices Calculations , Total Return Index(TRI) has been used. Where ever TRI not available Composite CAGR has been disclosed .Please refer

Disclaimer sheet for composite CAGR disclosureDISCLOSURES

Name of the Scheme This product is suitable for investors who are seeking* Risk-O-Meter

• Long Term Capital Appreciation.

Tata Hybrid Equity Fund • Investment predominantly in equity & equity related instruments (65% - 80%) & some portion (between 20% to 35%) in fixed

income instruments.

• Long Term Capital Appreciation.

Tata Equity P/E Fund • Investment (minimum 70%) in equity & equity related instruments of companies whose rolling P/E is lower than rolling P/E of

S&P BSE Sensex.

• Long Term Capital Appreciation. • An equity linked savings scheme (ELSS) Investing predominantly in Equity & Equity related

Tata India Tax Savings Fund

instruments.

• Long Term Capital Appreciation. • Investment in equity & equity related instruments of well researched value and growth

Tata Large & Mid Cap Fund

oriented Large & Mid Cap Companies

Tata Large Cap Fund • Long Term Capital Appreciation. • Investment predominantly in equity & equity related securities of large cap companies.

• Long Term Capital Appreciation. • Investment predominantly in equity & equity related instruments of growth oriented mid cap

Tata Mid Cap Growth Fund:

companies

• Income over a short term investment horizon. • Investments predominantly in arbitrage opportunities in the cash and derivative

Tata Arbitrage Fund

segments of equity markets and by investing the balance sheet in debt and money market instruments

*Investors should consult their financial advisors if in doubt about whether the product is suitable for them.THANK YOU

Disclaimer: The views expressed in this article are personal in nature and in is no way trying to predict the markets or to time them. The views expressed are for

information purpose only and do not construe to be any investment, legal or taxation advice. Any action taken by you on the basis of the information contained

herein is your responsibility alone and Tata Asset Management will not be liable in any manner for the consequences of such action taken by you. Please consult your

Financial/Investment Adviser before investing. The views expressed in this article may not reflect in the scheme portfolios of Tata Mutual Fund. This is for information

only and is not to be considered as sales literature. Not to be used for solicitation of business in schemes of Tata Mutual Fund.

Mutual Fund investments are subject to market risks, read all scheme related documents carefullyYou can also read