Earnings Season: Companies battle headwinds - CommSec

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economics | August 31, 2020

Earnings Season: Companies battle headwinds

Corporate Profit Reporting Season

Each ‘earnings season’ or ‘profit-reporting season’ CommSec tracks all the earnings results of S&P/ASX

200 companies to obtain a comprehensive picture of the aggregate health of Corporate Australia.

Overall, 137 of the ASX200 index group have reported full-year results for the 2019/20 year. A further 31

companies with a December 31 reporting date have issued half-year or interim results. A small number of

companies (AVH, COE, IFL, GOR and SKC are still to report).

In these turbulent times, only 75 per cent of companies reported statutory profits for the year to June. It is

the weakest outcome in over the decade that we have been tracking interim and final reports with an end-

June or December financial year. Aggregate full-year earnings fell by 38 per cent.

Just under 69 per cent of companies issued a dividend. Aggregate dividends fell by 36 per cent.

The Profit Reporting Season

Every six months CommSec tracks the earnings of Australia’s largest listed companies. Some analysts track

whether companies have met broker expectations. That tells you little about the financial performance of

companies. Unfortunately for investors only a few brokers ‘cover’ all the stocks.

Other analysts just track the earnings of those companies they ‘cover’ – the companies that they have detailed

information on. CommSec includes all ASX 200 companies in its macro (big picture) assessment of the reporting

season.

Of the 137 companies to report for the year to June 2020, 103 companies or 75 per cent managed to produce a

statutory profit (net profit after tax). The last time a similar low outcome occurred, around 80 per cent of

companies issued a profit for the 2014/15 year.

Overall, profits were down in the year to June, causing companies to slash or abandon dividend payments and

instead lift cash holdings.

Clearly for some companies it has been the toughest year in living memory. Other companies have done well,

riding the wave of monetary and fiscal stimulus. In 2019 the focus was the US-China trade war and Brexit

stalemate. In 2020 it has been the COVID-19 pandemic.

Craig James, Chief Economist; Twitter: @CommSec

Ryan Felsman, Senior Economist; Twitter: @CommSec

IMPORTANT INFORMATION AND DISCLAIMER FOR RETAIL CLIENTS

The Economic Insights Series provides general market-related commentary on Australian macroeconomic themes that have been selected for coverage by the

Commonwealth Securities Limited (CommSec) Chief Economist. Economic Insights are not intended to be investment research reports.

This report has been prepared without taking into account your objectives, financial situation or needs. It is not to be construed as a solicitation or an offer to buy or sell any securities or financial instruments, or as a recommendation and/or

investment advice. Before acting on the information in this report, you should consider the appropriateness and suitability of the information, having regard to your own objectives, financial situation and needs and, if necessary, seek

appropriate professional of financial advice.

CommSec believes that the information in this report is correct and any opinions, conclusions or recommendations are reasonably held or made based on information available at the time of its compilation, but no representation or

warranty is made as to the accuracy, reliability or completeness of any statements made in this report. Any opinions, conclusions or recommendations set forth in this report are subject to change without notice and may differ or be

contrary to the opinions, conclusions or recommendations expressed by any other member of the Commonwealth Bank of Australia group of companies.

CommSec is under no obligation to, and does not, update or keep current the information contained in this report. Neither Commonwealth Bank of Australia nor any of its affiliates or subsidiaries accepts liability for loss or damage arising

out of the use of all or any part of this report. All material presented in this report, unless specifically indicated otherwise, is under copyright of CommSec.

This report is approved and distributed in Australia by Commonwealth Securities Limited ABN 60 067 254 399, a wholly owned but not guaranteed subsidiary of Commonwealth Bank of Australia ABN 48 123 123 124. This report is not

directed to, nor intended for distribution to or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary

to law or regulation or that would subject any entity within the Commonwealth Bank group of companies to any registration or licensing requirement within such jurisdiction.

Economic Insights. Earnings Season: Companies battle headwinds

Admittedly a number of companies have prospered in the period. Gold companies have ridden the back of strong

demand and record prices for the precious metal (Newcrest Mining, Silver Lake Resource, and Saracen Mineral).

Iron ore miners (Fortescue Metals) are riding high with the steel-making ingredient recently hitting 6½-year highs

on the back of the strong Chinese industrial recovery and policy stimulus.

Some retailers – especially those with a good on-line presence – have reported higher sales and profits (Nick

Scali, Adairs, and JB Hi-Fi). Woolworths doubled online capacity over the year and plans to expand it by another

30-50 per cent. On-line sales are still only around 5.5 per cent of its total sales.

Electrical goods and homewares retailers have clearly out-performed. People have been locked down or have

continued to work from home and they have been keen to buy goods that enable them to work efficiently at home

and be comfortable. This has shown up in several months of strong retail trade data from the Bureau of Statistics.

Services companies – especially those firms dependent on domestic and global mobility (travel operators) – have

experienced the toughest conditions over 2020, especially late in the first quarter and through the June quarter.

And the ongoing digitisation and shift to streaming has weighed on media companies, which have

underperformed. Australia’s uncertain energy policy weighed on Woodside Petroleum’s bottom line.

Bank profitability has been weaker due to lower interest rates, the build-up of liquid assets and accelerating cost

pressures.

The Numbers

So to the numbers. And these numbers refer to those companies reporting full-year earnings to June 30, 2020.

Profits

As noted above, 75 per cent of companies have reported statutory profits (net profit after tax) for the year to June.

On average over the past decade around 88 per cent of companies have reported a profit rather than a loss. In

fact, 92 per cent of the companies that announced interim results for the half year to December 2019 reported a

profit.

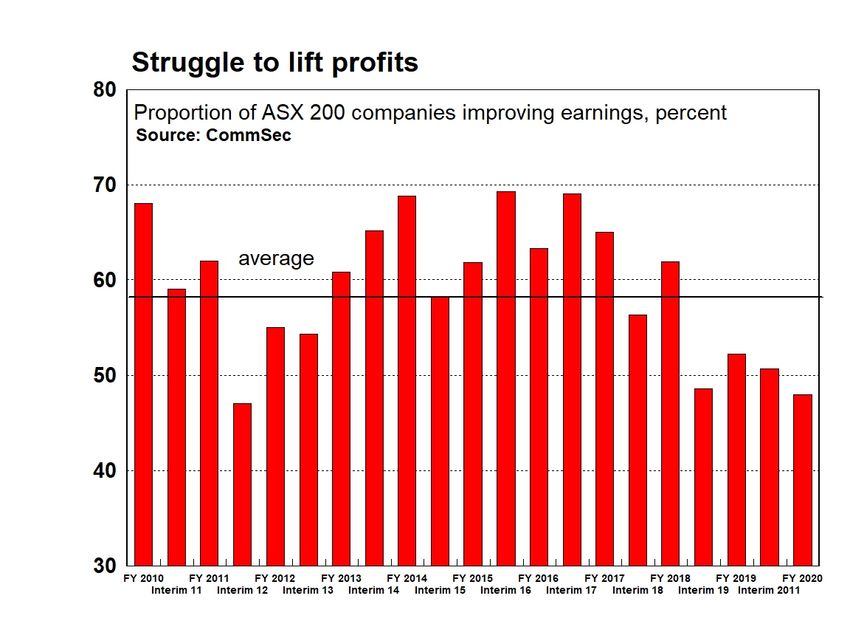

Of the companies to report a profit for the year to June, 48 per cent managed to lift earnings while 52 per cent

recorded a fall in earnings.

In aggregate (summing all the profit results), earnings were down 38 per cent on a year ago. Revenues were up in

total by 3.4 per cent, which were more than matched by a 4.1 per cent lift in expenses.

Dividends

Looking back over the six months to December 2019 (interim results), just over 87 per cent of the ASX 200

companies issued a dividend. But for the full year to June 2020, only 69 per cent of companies have elected to

pay a return to shareholders. The average over the past 20 reporting seasons stands at 86 per cent.

Almost 23 per cent of companies lifted dividends; 12 per cent held dividends steady; 53 per cent of companies

reduced dividends or didn’t pay a dividend; and 12 per cent of companies that didn’t pay a dividend last time (in

February) also didn’t pay a dividend this time.

Of those trimming dividends, 20 per cent of all companies or 27 companies that paid a dividend last time indicated

that they won’t be paying a final dividend. And 47 companies (34 per cent) paid a reduced dividend.

Of the 94 companies paying a dividend, 33 per cent lifted dividends; 17 kept the payout steady; and 50 per cent

cut the dividend.

In aggregate, dividends fell by 36 per cent on a year ago.

August 31 2020 2

Economic Insights. Earnings Season: Companies battle headwinds

Cash

Profits are down, so companies have elected to trim or not pay a dividend and instead use the cash to shore up

stretched balance sheets. Cash conservation has been a highlight of recent business-related surveys.

Aggregate cash at hand (cash as at June 30) rose by 31 per cent on a year ago (up from $84 billion to $110

billion)

Overall 70 per cent of companies lifted cash levels from a year ago, notably real estate investment trusts (REITS).

Once the half-year reporting companies are added in, cash levels totalled a record $141 billion as at June 30

2020, up from $111 billion as at June 30, 2019.

Themes

Usually each quarter there are a number of themes, covering a range of issues. This reporting season COVID-19

has understandably dominated. Investors have been interested to know:

Are companies able to provide future guidance?

What action have companies taken in response to the crisis? Have they trimmed expenses; slashed capital

expenditure; devoted more resources to on-line spending; or perhaps fundamentally re-assessed the

business model?

What have companies done on staffing levels, especially companies in receipt of JobKeeper?

What action has been taken on longer-term strategies as opposed to short-term responses?

How has the capital position been managed?

And how have those companies caught up in escalating Australia-China political tensions responded?

Solid retail sales featured over the reporting period, especially on-line sales. Some have benefited from low or

lower rents. Retailers to benefit most in the lockdown were in homewares, electrical or have been focussed on

home delivery. There was a bigger pay-off from companies that already had invested in an on-line presence

(sales and distribution). Solid results include those from: ARB, Adairs, JB Hi-Fi, Nick Scali, Coles, Breville, Baby

Bunting, Domino’s Pizza, Treasury Wine, Premier Investments, Kogan, Wesfarmers (Bunnings and Officeworks)

and Woolworths.

Retailers, supermarkets, gold stocks, mining-more-generally, and stay-at-home stocks have out-performed in the

COVID environment. Energy, tourism, travel-dependent companies and some REITS have been buffeted.

Companies have mostly refrained from providing guidance for investors – especially dollar figures or ranges.

Clearly the environment is unpredictable. It only takes one cluster to get out of control and other states will

experience ‘second wave’ challenges like Victoria. But while guidance has been vague or non-existent, investors

will value more regular updates from companies to keep them informed and ensure dynamic market valuation is

being maintained. That said, Wisetech, Goodman Group, Amcor, CSL and Brambles were just a few companies

guiding for growth.

August 31 2020 3

Economic Insights. Earnings Season: Companies battle headwinds

Discussion points

A raft of interesting discussion points have come out of the earnings season.

Ingenia: The property group noted that requests for rental relief were ‘non-existent’. The company also noted that

business was booming for holiday parks.

Abacus: The REIT also downplayed issues of rent, saying that it had collected rent from 90 per cent of office

tenants and 98 per cent of self-storage facilities.

Nick Scali: The furniture retailer has forecast a 60 per cent lift in December half-year profit.

Monadelphous: The engineering group painted a positive outlook on the back of new contracts in Australia and

Chile.

BHP: Discussion centred on the future for coal including a possible demerger.

ARB: The maker of 4WD equipment has noted record order books. People are keen to take intra-state regional

and camping holidays.

Aurizon: The rail freight operator reported minimal disruption from COVID. There was reduced coal demand as

Asian factories shut down.

Goodman: Supported by its industrial warehouses operation, it beat guidance for the 9th year. Only 10 per cent of

its employees were working at head office in Castlereagh Street Sydney.

Gold outperformers include: Evolution, Newcrest, Saracen, Silver Lake Resource, and Northern Star.

GPT: has reduced operating costs; deferred development projects and non-essential capital expenditure.

Coca-Cola Amatil: cut costs $60 million in the June half-year and plans to cut $80 million in the current

December half year.

Retailers vs landlords: Retailers have generally done well but landlords like Scentre Group have been trimming

rents and writing down the value of properties.

Cost of COVID: While some observers have been quick to criticise companies that have accepted government

financial assistance – JobKeeper or otherwise – less focus has been on the costs that have been incurred in

keeping customers and staff safe in the COVID era. Woolworths noted that it had spent $404 million on ‘COVID

costs’ in the second half of 2019/20 and a further $107 million in the eight weeks to August 23.

Market reaction

Some brokers maintain estimates for companies on metrics like profits and dividends. So they determine if the

earnings results were ‘good’ – or perhaps less positive – based on whether the companies met, beat or missed

their forecasts.

In normal times, companies themselves will provide guidance on future results. But clearly these aren’t normal

times. During February and March the majority of companies abandoned previous guidance; some raised extra

capital; some cut recurrent and capital spending; and some did all three.

This earnings season, companies have again been understandably reluctant to provide guidance on future sales

and profits.

So the best way to determine whether investors were encouraged or discouraged by a company’s profit result is

to examine the sharemarket reaction on the immediate days after the report was delivered.

Overall 53 per cent of ASX 200 companies that reported results saw a lift in share prices on the day of earnings

release with an average gain of 0.7 per cent and a gain of 0.8 per cent after two days.

What are the implications for interest rates and

investors?

Australian companies understandably withdrew earnings

guidance as the virus crisis unfolded due to the

heightened level of uncertainty. So expectations were set

low ahead of the start of earnings season. It was a similar

story in both the US and Europe. With the bar set so low,

companies safely cleared the lower height.

COVID-19 still dominates the landscape. But investors

will likely show lower tolerance from here. Crisis-time

responses have been made such as raising capital and

cutting or trimming dividends. And some balance sheets

and employment levels have been supported by the

government’s JobKeeper wage subsidy. But now

August 31 2020 4

Economic Insights. Earnings Season: Companies battle headwinds

investors want to know what positive strategies will be followed in the short and longer-term.

There has been discussion of the fact that some of the companies that received the JobKeeper wage subsidy

have reported profits or even higher profits. But any criticism relies on perfect hindsight. At the time that

JobKeeper was announced there was significant risk of large scale job losses. The companies supported by

JobKeeper – especially profitable companies – are more likely to retain or lift jobs. And that is the whole point of

the scheme – saving jobs – and keeping the jobless rate down to hasten economic recovery.

Corporate Australia remains in good shape with strong balance sheets being maintained. But the economic

outlook remains very uncertain – especially with the government tapering stimulus. Still, the significant fiscal and

monetary policy measures provide encouragement together with the success by many states and territories in

‘flattening the curve’. Infrastructure spending will be important in driving economic recovery and will support

prospects for industrials, especially engineering and construction materials. The success in keeping the jobless

rate down will be important for consumer-focussed companies, especially retailers.

The closure of international borders has hit travel-dependent areas of the economy hard. But the full impact of the

drying up of in-bound migration is still to be felt more broadly across the economy, especially home construction,

office demand and agriculture. The shift from international and inter-state tourism to intra-state travel is still to be

played out.

The recovery of the Chinese economy remains encouraging for mining and engineering sectors. Australia is a

key global exporter of gold, copper and iron ore, in particular. However there are challenges for the agricultural

sector due to fractious relations between China and Australia.

CommSec expects the All Ordinaries to be in a range of 6,350-6,750 by end-2020, with the range for the ASX 200

between 6,200-6,600 points. We expect sharemarket returns to be largely flat over 2020, supported by easy

monetary and fiscal conditions. While shares remain ‘expensive’ valuation-wise relative to history, clearly these

are not normal times. Earnings from financial assets are low. Corporate earnings will remain challenged in the

near-term and dividend payouts are likely to be lower. From here much depends on virus containment, finding a

vaccine and opening domestic and international borders.

Current investor positioning in Aussie shares suggests that the profit reporting season was better-than-expected

(albeit off low expectations). Some investors covered their ‘short’ positions in companies whose results surprised

on the upside. According to Bloomberg and ASIC data, total weighted short interest of the ASX 200 index

members was 1.7 per cent on August 27 – the lowest since November 2017 – down around 25 per cent since the

March 23 low.

Craig James, Chief Economist, CommSec;

Twitter: @CommSec

Ryan Felsman, Senior Economist, CommSec;

Twitter: @CommSec

August 31 2020 5

Economic Insights. Earnings Season: Companies battle headwinds

August 31 2020 6

Economic Insights. Earnings Season: Companies battle headwinds

August 31 2020 7

Economic Insights. Earnings Season: Companies battle headwinds

August 31 2020 8

Economic Insights. Earnings Season: Companies battle headwinds

August 31 2020 9You can also read