DIE GROSSE WIEDERERÖFFNUNG: NEUE CHANCEN, BEKANNTE RISIKEN - WIE KANN IHR UNTERNEHMEN DAS WACHSTUM OPTIMAL FÜR SICH NUTZEN? - Euler Hermes

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DIE GROSSE WIEDERERÖFFNUNG:

NEUE CHANCEN, BEKANNTE RISIKEN.

WIE KANN IHR UNTERNEHMEN DAS

WACHSTUM OPTIMAL FÜR SICH NUTZEN?

Webinar 29.06.2021

IHRE REFERENTEN

Ludovic Subran Anna-Katharina Wichmann

Chef-Volkswirt Vertriebsdirektorin

Allianz und Euler Hermes Euler Hermes DACH

2

©Mārtiņš Zemlickis

GRAND

Textmasterformat bearbaiting

REOPENING:

NEW

OPPORTUNITIES,

OLD RISKS

Allianz Research

June 29, 2021

© Copyright Allianz

Textmasterformat bearbaiting

MESSAGE #1: VACCINES SECURITY MATTERS

Expected date of herd immunity Asia relapse: Sanitary situation vs. stringency & mobility

(at current vaccination speed) impact, as of end of May (bubble size = vaccine doses administered

as % of population; pink bubbles where stringency increased over past month)

1,5 EU Mexico 5

Argentina Indonesia South Africa New Zealand

Japan 0 South Korea

70% of adult1 Indonesia

population Thailand

Brazil Egypt -5 Hong Kong

Turkey

Stringency x Mobility

0,5 Chile Japan

USA -10 Australia Thailand

0 -15

Vietnam

-20

-0,5 EU Turkey

Brazil Philippines

Egypt -25 Singapore

Vulnerable-1 Japan

Thailand Taiwan

population Indonesia -30

Mexico

(+65y)

Chile USA Argentina -35

-1,5

01-21 07-21 02-22 08-22 03-23 10-23 04-24 11-24 05-25 12-25 06-26 -10 0 10 20 30 40 50 60

Daily new Covid-19 cases per 1mln people, 7-day average

Sources: Our World in Data, Duke University, Allianz Research Sources: Our World in Data, University of Oxford, Google, Allianz Research

Most countries should reach herd immunity (1st dose) by the Ultimately, vaccination is likely to determine the pace of the

summer, but demand-side hurdles will be more and more visible. return-to-normal. APAC is a case in point: many economies

Advanced economies seem overall closer to ‘normality’, while had managed the pandemic well in 2020, but they recently

EMs are still likely to remain ‘closed’ due to the supply gap in had to implement restrictions again amidst new outbreaks

vaccines.

© Copyright Allianz

and low vaccination rates. 4

Textmasterformat bearbaiting

MESSAGE #2: FROM K-SHAPE TO V-SHAPE

Mobility data, level compared to pre-crisis Global demand by sector Container traffic volumes

(New orders + Backlogs of work) (12m/12m)

30

Germany Belgium United Kingdom

20% North America to Asia

115

United States France Netherlands Europe to Asia

10

110

Asia to North America

15%

105 Asia to Europe

-10

100

10%

95

-30

90 5%

-50 85 Consumer Goods Consumer Services

0%

80

Industrials Technology

-70 75

Basic Materials -5%

70

01/01/2021

01/02/2021

01/03/2021

01/04/2021

H1 2010

H2 2010

H1 2011

H2 2011

H1 2012

H2 2012

H1 2013

H2 2013

H1 2014

H2 2014

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

-90

02-20 04-20 06-20 08-20 10-20 12-20 02-21 04-21

-10%

2016 2017 2018 2019 2020 2021

Sources: various, Euler Hermes, Allianz Research Sources: Markit, Euler Hermes, Allianz Research Sources: Markit, Euler Hermes, Allianz Research

Mobility has picked up strongly over the Global demand prospects have The US is indeed the driving force of the

course of May and should continue to accelerated strongly since the start of the recovery, but this is also capturing a lot of

recover significantly in June amid greater year and stand at a record high level the global transportation capacity, with

re-openings in most European countries. across all sectors. container prices at a record 5-year high.

© Copyright Allianz 5

Textmasterformat bearbaiting

MESSAGE #3: REVENGE SPENDING TO ABSORB

ONLY PART OF RESIDUAL SAVINGS

US retail sales (%, y/y) Eurozone consumer confidence Catch-up consumption expected

vs retail sales growth in 2021, % of GDP

3,0

20

2%

10

2,5

0%

0

-2%

2,0

-10 -4%

1,5

-20 -6%

-8%

-30 1,0

-10%

General economic expectation over the next 12 months

-40

-12% 0,5

Financial situation over the next 12 months

-50

Savings over the next 12 months -14%

0,0

Italy

Norway

Czechia

Netherlands

Germany

Austria

Spain

France

Poland

Denmark

Sweden

US

UK

Belgium

Portugal

Eurozone

-60 Retail sales (3M yoy, rhs) -16%

11 12 13 14 15 16 17 18 19 20 21

Sources: US Census Bureau, Allianz Research Sources: US Census Bureau, Allianz Research Sources: Eurostat, Euler Hermes, Allianz Research

Demand-supportive policies more than Consumer confidence in the Eurozone is close to pre-crisis levels. The glut of household

offset the lack of automatic stabilizers in savings could generate a consumption boom of EUR170bn in 2021. Looking at individual

the short-term. Household consumption is countries, we estimate pent-up consumption could reach 3% of GDP in the US and the UK

expected to grow by +7.8% y/y in 2021 vs in 2021, and around 1.5% in most European countries. Nevertheless, roughly EUR500bn

-3.8% y/y in 2020. of Covid-19 residual savings will still remain at the Eurozone level at end-2021.

© Copyright Allianz 6

Textmasterformat bearbaiting

MESSAGE #4: MULTI-FACETED RECOVERY

2019 2020 2021 2022

2022 GDP, compared to 2019 and to pre-crisis forecast

World GDP growth 2.4 -3.5 5.5 4.1

United States 2.2 -3.5 6.3 4.0

6 2022 GDP higher than 2019

and pre-crisis forecast

Latin America 0.2 -7.1 5.2 2.9 Turkey

% change from pre-crisis forecast

Brazil 1.4 -4.4 3.8 2.5 4

United Kingdom 1.4 -9.9 6.0 4.9 2

Netherlands US

Eurozone members 1.3 -6.5 4.2 4.2 0

Germany 0.6 -5.1 3.4 3.8 Germany Russia

France 1.5 -8.2 5.4 3.6 France Emerging Europe China

-2 Eurozone World

Italy 0.3 -8.9 4.4 4.6 Italy

Belgium Asia-Pacific

Spain 2.0 -10.8 5.1 5.3 -4 Japan Africa

South Saudi Arabia

Netherlands 1.6 -3.7 3.0 4.2 Brazil

-6 Africa UK

Belgium 1.8 -6.3 3.5 4.0 Latin

Spain

America

Russia 2.0 -3.1 3.1 3.2 -8 Middle East

Turkey 0.9 1.8 8.3 4.1 2022 GDP lower 2022 GDP higher than

-10 than 2019 and 2019 and lower than

Asia-Pacific 4.1 -1.1 6.3 4.8 pre-crisis forecast pre-crisis forecast

India

China 6.0 2.3 8.2 5.4 -12

Japan 0.3 -4.9 2.5 1.9 -5 0 5 10 15

India 4.1 -7.5 7.9 6.4 % change from 2019

Middle East 0.0 -5.0 2.8 3.0 Sources: various, Allianz Research

Saudi Arabia 0.3 -4.1 2.4 2.9

Africa 1.7 -2.8 2.7 3.5

South Africa 0.3 -7.0 2.2 1.9

© Copyright Allianz 7

NB: fiscal year for India

Textmasterformat bearbaiting

MESSAGE #5: STRONG TRADE MOMENTUM DESPITE

SHORT-TERM HURDLES DUE TO BOTTLENECKS

Global trade in goods and services, %y/y Global trade in goods & leading indicator Taiwan production shortfall vs. US &

Asia Pacific North America Eurozone input shortage

Western Europe Central and Eastern Europe

Latin America Middle East and Africa 30 54 6 Production shortfall - Taiwan (HP-filtered)

40

World (volume) World (value)

15,9% 25

53 Input shortage - US & Eurozone (average),

20 rhs

4 30

52

13% 15

10,0% 9,5% 10 51 20

8,4% 2

8% 7,7%

5 50

6,2% 10

5,4% 0

4,3% 49 0

3,8%

3% 3,0% -5

2,4% 0

0,7% -10 48

1,8%

-2

-2% -15 47 -10

-2,0% -1,6%

-20 EH Trade Momentum Index (right 46 Stronger relationship

scale) -4

-7% -25 from April 2012 -20

-8,0% Value global goods trade growth 45

-30 y/y

-10,7%

-12% -9,9% -35 44 -6 -30

14 15 16 17 18 19 20 21 22 07 09 11 13 15 17 19 21 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

Sources: IHS Markit, IMF, Allianz Research Sources: CPB, Allianz Research Sources: IHS Markit, Allianz Research

We expect global trade to grow by +7.7% in Such a strong pace of growth for full-year The global supply-demand imbalance could

volume in 2021, and by +15.9% in value 2021 is partly ensured by favorable base be exacerbated in Q2 and the summer,

terms, likely driven by robust exports from effects and a stronger-than-expected given the new Covid-19 outbreak in Taiwan

APAC and strong imports in the US, momentum in the first months of the year. – on which the world has become

Europe and China. However, there are short-term risks. increasingly dependent in the electronics

© Copyright Allianz 8

sector.

Textmasterformat bearbaiting

MESSAGE #6: LIVING WITH HIGHER INFLATION

Assessment of shortages and selling price European companies’ pricing power Nominal wage growth (%)

expectations by firms, by sector (Europe) Eurozone

Risk on

profitability 6

Pricing

due to input

Shortage in factor of production - compared to Power

prices Eurozone USA

pre covid levels (*) Selling price

Electricity

Material, equipment & expectations (**)

Labor Pharmaceuticals 5

space

Wood & related 4 25 61 Computers

Paper & related 1 18 61 Consumer

Basic metals 2 8 51 Electronics

Furniture 0 22 47 Food & non-alcoholic 4

Rubber/plastics 0 32 43

beverages

Coke and refined products -2 19 40

Tobacco

Fabricated metal products 3 17 37

Wines from grapes

Electrical equipment 8 27 36 3

Textiles 4 5 35 Automobile

Machinery/equipment -1 14 32 Household

Chemicals -1 16 30 Appliances

Other non-metallic mineral 1 7 30 Diesel/Petrol 2

Food -4 -1 24

Textile

Motor vehicles -2 30 18

Printed media

Computer/electronic -2 22 17

Leather 3 3 14 Cleaning products

Repair/installation -4 10 13 Air transport 1

Other manufacturing -12 -8 13 Postal services

Construction 24 3 11

Telephone services

Beverages -2 -4 10

Restaurants, cafés

Pharmaceuticals -6 -9 4

and the like

0

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Wearing -2 1 4

Accommodation

Other transport equipment -7 -10 4

Printing 0 6 3 services

(*) Q2’21 vs. to Q4’19 levels; (**) As of May 2021 surveys

Sources: Eurostat, Euler Hermes, Allianz Research Sources: Allianz Research Sources: Allianz Research

Input shortages are particularly acute in the Indeed, the rise in input prices is not being Wages are likely to rise in those sectors

automotive and computer/electronic sectors transferred onto output prices. We find that that face labor shortages. However we

(semiconductors!). Surveys find that selling European companies in particular are most don't expect a blanket boost with total

prices could rise in Europe going forward, at risk, having limited pricing power for now. wages galloping out of control.

alleviating some pressure from cost inflation.

© Copyright AllianzMESSAGE #7: GOVERNMENTS TO OVERSTAY THEIR

Textmasterformat bearbaiting

WELCOME

Eurozone public debt (% GDP) US public debt (% GDP) EMs: Differential between past economic

growth and current cost of debt*

NGA

BRA

ZAF

UKR

KEN

RUS

COL

TUR

MEX

PER

CHL

IDN

IND

THA

MYS

HUN

CZE

ROU

PHL

CHN

POL

Sources: Refinitiv, Allianz Research. Sources: Refinitiv, Allianz Research. -5% 0% 5% 10% 15%

Differential Avg Coupon Avg YoY Nom. Growth 2015-2019

We still see EZ heavyweights France, Italy and US public debt is expected at close to 160% * A positive differential indicates future debt sustainability risks.

Sources: Refinitiv, Allianz Research.

Spain boast debt ratios close to or notably above of GDP at the horizon of 2030. The

100% of GDP in 2035. In contrast, Germany, sustainability of US public debt won't be at Nigeria, Brazil, South Africa, Ukraine and

Ireland and the Netherlands cement their position risk as the spread r-g is expected to remain Kenya face high debt rollover risks in the

as low-debt countries by pushing debt notably pretty low alongside cooperative monetary medium term.

below the 60% Maastricht target by 2035.

© Copyright Allianz

policy and resilient growth 10Textmasterformat bearbaiting

MESSAGE #8: CREDIT RISK UNDER CONTROL

Changes in EBITDA margin between EH S&P credit rating monitoring Global sectors, timeline recovery

FY2019 and FY2020, by sector – debt weighted sector rating (baseline scenario)

(1 = AAA ; 20 = Default)

Sources: Refinitiv, Allianz Research Sources: S&P, Euler Hermes, Allianz Research Sources: Euler Hermes, Allianz Research

The sectorial asymmetry of the shock lead to wide heterogeneity across sectors in terms of revenue, profits and ultimately margins, with

a stronger hit in sectors in front face with social and mobility restrictions such as hotels and restaurants and transportation, and

conversely with substantial positive performance in chemicals, pharmaceuticals, retail and agrifood. We expect the recovery to lead a

‘rebalancing’ in credit ratings from the wave of deteriorations posted in 2020, but the former will be gradual and uneven due to the multi

speed recovery among sectors.

© Copyright Allianz 11Textmasterformat bearbaiting

MESSAGE #8B: INSOLVENCY NORMALIZATION TO

ACCELERATE IN 2022

Business insolvencies – Year-to-date figures (selected countries) Yearly changes in insolvencies in 2021 and 2022 (in %)

Share in the Last point (y/y change in %)

Global

Country Last Last Last Ytd vs Ytd vs

Insolvency As of Last m Comments

3m 6m 12m 2020 2019

Index

U.S. 28,7% 2021 Q1 -29% -21% -14% -29% -25% Steady decrease

Canada 2,3% 04-2021 37% -5% -18% -19% -16% -40% Steady decrease

Brazil 2,8% 05-2021 -13% 8% -6% -22% -1% -25% Steady decrease

Colombia 0,4% 2020 Q4 18% 21% 2% 2% Upside trend

Chile 0,4% 04-2021 15% 3% 11% 9% 4% 15% Upside trend

Germany 5,3% 05-2021 5% 3% -9% -17% -9% -15% Recent upside trend reversal

France 3,8% 05-2021 34% 20% -21% -29% -15% -49% Recent upside trend reversal

United Kingdom 4,1% 05-2021 8% -14% -25% -34% -31% -42% Steady decrease

Italy 2,9% 05-2021 456% 191% 42% 0% 57% -12% Upside trend

Spain 1,9% 03-2021 85% 29% 16% 0% 29% 38% Upside trend

The Netherlands 1,2% 05-2021 -52% -51% -49% -39% -52% -51% Steady decrease

Sw itzerland 1,0% 04-2021 121% 10% -5% -13% -1% -20% Recent upside trend reversal

Sw eden 0,8% 05-2021 -22% -30% -18% -18% -25% -14% Steady decrease

Norw ay 0,6% 04-2021 24% -11% -17% -21% -23% -34% Steady decrease

Belgium 0,7% 05-2021 56% 8% -30% -30% -23% -45% Recent upside trend reversal

Austria 0,6% 2021 Q1 -59% -59% -52% -59% -63% Steady decrease

Denmark 0,5% 05-2021 -29% -11% -4% -11% 3% -10% Recent dow nside trend reversal

Finland 0,4% 2021 Q1 -13% -25% -24% -13% -1% Steady decrease

Portugal 0,3% 02-2021 -41% -6% -10% -6% -4% -10% Steady decrease

Ireland 0,5% 2021 Q1 -30% -11% -1% -30% -43% Recent dow nside trend reversal

Luxembourg 0,1% 05-2021 95% 73% 15% 17% 39% -4% Upside trend

Russia 2,0% 03-2021 -1% -25% -28% -22% -25% -11% Steady decrease

Turkey 1,3% 04-2021 138% 33% 2% 8% -15% -11% Recent upside trend reversal

Poland 0,7% 03-2021 207% 116% 110% 67% 116% 99% Steady increase

Romania 0,3% 04-2021 731% 82% 13% 8% 44% -3% Upside trend

Lithuania 0,1% 03-2021 16% -47% -53% -57% -25% -61% Steady decrease

Latvia 0,0% 05-2021 -47% -44% -32% -33% -43% -65% Steady decrease

South Africa 0,5% 03-2021 49% 19% 20% 5% 19% 11% Upside trend

Morocco 0,2% 03-2021 246% 15% na na 15% 6% Recent upside trend reversal Sources: Euler Hermes, Allianz Research

China 17,2% 05-2021 -37% -24% -18% -11% -19% -9% Steady decrease

Japan 7,5% 05-2021 50% -12% -22% -15% -22% -23% Steady decrease By 2022, business insolvencies are likely to exceed pre Covid-

India 1,9% 2021 Q1 -52% -70% -75% -52% -44% Steady decrease

Australia 1,9% 04-2021 14% -34% -42% -51% -37% -49% Steady decrease 19 levels in most countries (by 17% on average) with the US to

South Korea 2,3% 05-2021 -30% -29% -24% -19% -27% -60% Steady decrease

Taiw an 0,8% 12-2020 -28% -2% -5% -2% -2% Steady decrease see low-for-longer insolvencies and uneven dynamics among

Singapore 0,5% 04-2021 -26% -9% -51% -50% -40% -9% Steady decrease

Hong Kong

New Zealand

0,5%

0,3%

05-2021

04-2021

-

37%

300%

-4%

153%

-14%

75%

-16%

183%

-13%

7% Recent upside trend reversal

-22% Steady decrease

European countries (due to different share of Covid-19

TOTAL 100% -8% -16% -16% -17% -21%

sensitive sectors and differences in support packages.

© Copyright AllianzTextmasterformat bearbaiting

USA: THE FED COMFORTABLE WITH A TEMPORARY

OVERHEATING OF THE ECONOMY

US housing prices and shelter CPI index Labor shortages in the US Fed's balance sheet (USD bn)

(% y/y)

Sources: BLS, Allianz Research Sources: BLS, Allianz Research Sources: Fed, Allianz Research

Overheating in the housing market: We Labor shortages are still half-way of their The Fed will envisage an operation twist

expect the shelter subcomponent of the maximum level (expected for H1 2022). by allocating less to MBS and more to

CPI to be heading toward levels > 3.5% y/y Average salaries are now expected in US Treasuries starting from Q2 2022 and

before the end of 2022. overheating areas at around +3.8% y/y then progressively reduce securities

compared with 3.5% y/y in our previous purchases from USD120bn per month to 0

scenario. at the horizon of H2 2023. 13

© Copyright AllianzTextmasterformat bearbaiting

A NEW US PATERNALISM UNTIL THE MID-TERM

ELECTIONS IN 2022?

Economic Policy Uncertainty index

Towards a leadership by the law

• “A family approach” by adopting a multilateral

strategy with a comeback to international

organizations and a leading role in

international discussions

• “Educating” by sanctioning in the short-term

but opening the door to improvements of

relations over the long-term with Russia and

China

• “Protecting” by continuing the America First

Policy initiated by Barack Obama and

reinforced by Donald Trump

• “Making the law” by imposing new norms at

Sources: EPU, Allianz Research

the level of digital, tax and environment

policy (a diplomacy aiming at establishing Biden's administration, until recent events in the Middle

leadership by the law) East, had contributed to attenuate global political risk.

Tactical multilateralism is the new leitmotiv of

international relations, which is less confrontational

© Copyright Allianz though this does not mean lower protectionism. 14Textmasterformat bearbaiting

CHINA: SUPPORTIVE EXTERNAL CONDITIONS AND

THREE LAYERS OF DOMESTIC RECOVERY

Exports and leading indicator Investment by sector, 2y CAGR (%) Household survey and savings rate

estimate

40% 20% 100

64 28,0 22,0 23,3 22,3

30% 15% 80

59

25,0 25,3 28,6

20% 10% 26,3

54 60

10% 5% 40

49

0% 0%

44 20

-10% 45,7 53,0 51,4 49,1

39 -5%

0

01-19

04-19

07-19

10-19

01-20

04-20

07-20

10-20

01-21

Infrastructure (value)

-20% 34 -10%

Exports 2y CAGR (%)

Housing starts (volume), HP-filtered

-30% -15% More consumption

29

Official manufacturing PMI - new export More investment

Manufacturing (value)

orders (rhs) More saving

-40% 24 -20%

08 09 10 11 12 13 14 15 16 17 18 19 20 21 10-2019 04-2020 10-2020 04-2021 Savings as % of disposable income

Sources: National Bureau of Statistics of China, China Customs, Allianz Research

We maintain our GDP growth forecasts Domestically, the 2020 recovery was To make the domestic recovery fully

for China at +8.2% in 2021 (after +2.3% driven by a first layer of public and broad-based, a third layer is private

in 2020) and +5.4% in 2022. The policy-driven investment (infrastructure consumption. Labor market indicators

external environment continues to be and real estate). 2021 is likely to be are encouraging (unemployment rate

supportive

© Copyright Allianz and domestic growth drivers more focused on a second layer, lowest since 2019), but household 15

are gradually shifting. private investment (manufacturing). confidence is not back to normal.Textmasterformat bearbaiting

EUROZONE: ECONOMIC REBOUND UNDERWAY (+4.2%

IN 2021-22), BUT NO SWIFT HAPPY END FOR ALL

Real GDP (Index: 100=Q4 2019) EU Recovery & Resilience facility (EUR bn)

Sources: Refinitiv, Allianz Research Sources: EU Commission, Allianz Research

The Eurozone as a whole will return to pre-crisis GDP The NGEU fund is supposed to keep divergence at bay,

levels in Q1 2022, however will Germany will already hit however we think it could be 18% (EUR150bn) smaller than

that milestone later this year, for Spain it will take until advertised given the lackluster uptake of loans. Hence, we

2023. Divergent recovery speeds will complicate policy are more cautious on the expected growth impact: +1ppt in

setting in the monetary union.

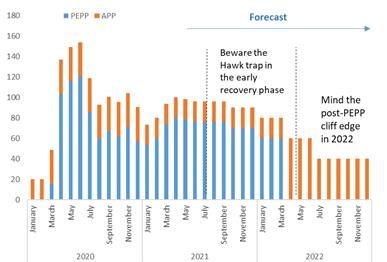

© Copyright Allianz 2022 assuming no meaningful implementation delay.ECB: MIND THE H2 ‘HAWK TRAP’, THE PEPP CLIFF

Textmasterformat bearbaiting

EDGE & GERMAN DEBT LIMITS FROM 2022 ONWARDS

ECB public sector asset purchases under PEPP & PSPP Germany: public sector debt outstanding (EURbn)

Sources: Refinitiv, ECB, Allianz Research Sources: Refinitiv, ECB, Allianz Research

The ECB will have to navigate challenging moments soon: Bigger headaches loom ahead as the ECB looks

Engage in a dovish tapering while avoiding the hawk trap in increasingly set to run into its self-imposed limits. Given our

H2 – i.e. pre-committing to a lower PEPP pace in the early expectations for German net issuance, the ECB will have

recovery phase which then calls for communication flip- enough room for maneuver for max. 10 months of QE at a

flopping should spreads widen. And prepare markets for a life pace of EUR40bn per month unless limits are lifted or eased.

after PEPP

© Copyright Allianz and navigate the looming cliff edge. The substitution via higher supranational purchases would 17

hurt peripheral spreads.FRANCE: RECOVERY IGNITED BUT WATCH OUT FOR

Textmasterformat bearbaiting

POLITICS!

Household bank deposits (EURbn) and confidence (index) French elections: stumbling along in a summer haze

30 000 (index) 110

Industrial

25 000 competitiveness

105 • What economic incentives to bring strategic industries back to

20 000

France and boost exports?

15 000 • Going beyond the -EUR10bn/year with the production cost cut?

100 • Which policies to tackle skill shortages, improve human capital

10 000 and R&D performance?

5 000 95 Fiscal reforms

0 • Pension reform: A cosmetic or profound solution? Where to push

the retirement age? A systemic or parametric reform?

90

-5 000 • How to reduce the deficit of the Social Security system?

• Universal income? What fiscal solutions to support the poor?

-10 000 Overnight deposits With agreed maturity

85

Savings accounts Total deposits Green Policy

-15 000

Consumer confidence (rhs) •What evolutions to the current climate law?

-20 000 80 •Who will push for a European solution for a CO2 tax at the EU

03/19

05/19

07/19

09/19

01/20

03/20

05/20

07/20

11/20

01/21

03/21

05/21

01/19

11/19

09/20

borders?

•Which financial support to NFCs that bear the cost of Green transition?

Sources : Markit, Euler Hermes, Allianz Research Source: Euler Hermes, Allianz Research

Household excess savings reached EUR142bn in Q1 The unemployment insurance reform (as of 1st

2020 on the back of continued state support and July) is suspended because of unions’ appeal. End

precautionary motives. With improving confidence as 2021, the Government may choose to move

of Q2 2021, the unleashed savings may boost forward with a softer version of the controversial

consumption up to +2pps.

© Copyright Allianz

‘pension reform’, this can lead to social unrest with 18

detrimental economic consequences.Textmasterformat bearbaiting

ITALY: EUROPE’S AMERICA – GOING BIG ON FISCAL

Italy with 2nd largest Recovery Plan (2021-26) Lifting growth potential back to early 2000s levels?

(in % of GDP) (real GDP and potential GDP, Index 100 = 2000)

20% 112 Projection

108

15%

104

10%

100

5%

96

0% 92

Greece Italy Portugal Spain France Germany 2000 2005 2010 2015 2020 2025 2030

EU Grants EU Loans Domesting Funding Real GDP Potential GDP

Sources: National Recovery Plans, Allianz Research Sources: Refinitiv, Allianz Research

Italy with 2nd largest recovery plan in EU in terms of Recovery plan projects a raise of potential growth by

GDP (15%) and the largest in absolute terms (EUR 0.4% to 0.6% p.a. This would add up to 3.6% of

248bn) of GDP) of which EUR192bn will be funded growth until 2026 and reach growth potential last

by NGEU with EUR69bn being grants. seen shortly after Italy entered the euro area.

© Copyright Allianz 19Textmasterformat bearbaiting

GERMAN ELECTIONS: EVOLUTION, NO REVOLUTION

Germany: Election poll (%) What could a Black-Green coalition (baseline scenario) entail?

Source: Infratest Dimpa Source: Allianz Research

Current election polls suggest three feasible coalitions to emerge from Agreeing on a coalition contract will prove challenging as

the September vote, with the Green Party and the FDP likely to be positions on a number of key topics are far apart between

kingmakers: 1) CDU/CSU & Green Party (plus FDP), 2) CDU/CSU, the CDU/CSU and the Green Party (the most likely

SPD & FDP and 3) Green Party, SPD & FDP. Approaching the election scenario). Even under the pragmatic leadership of Baerbock

date, we expect the governing CDU/CSU to receive more support in and Laschet a deal could take several months to be sealed,

polls, withAllianz

© Copyright progress on the vaccination front and an improvement in the as agreement will require deviating from party lines. 20

outlook.©Mārtiņš Zemlickis

Textmasterformat bearbaiting

THANK YOU

Allianz Research

June 25, 2021

© Ekaterina Pokrovsky - stock.adobe.com

© Copyright AllianzIM DIALOG

Ludovic Subran Anna-Katharina Wichmann

Chef-Volkswirt Vertriebsdirektorin

Allianz und Euler Hermes Euler Hermes DACH

22WIR BEANTWORTEN IHRE FRAGEN.

Fragen können Sie über

die Chatfunktion stellen.

23SICHER WACHSEN

WIR HELFEN IHNEN, DIE BESTEN CHANCEN ZU ERKENNEN

24GESCHÄFTE MACHEN – MIT

VERTRAUEN

WIR KENNEN DIE RISIKEN UND ÜBERNEHMEN SIE

25VIELEN DANK FÜR IHRE TEILNAHME

Bei Fragen wenden Sie sich gerne an Ihren persönlichen

Ansprechpartner bei Euler Hermes oder an:

Tel.: 040 / 8834 3536

E-Mail: service.de@eulerhermes.com 26You can also read