Development of the Bermuda Reinsurance Market - PASA General Assembly, Antigua, Guatemala

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Development of the Bermuda Reinsurance Market PASA General Assembly, Antigua, Guatemala Karl Mayr President & CEO of AXIS Re Europe April 30, 2012

Safe Harbor Disclosure

Statements in this presentation that are not historical facts, including statements regarding our estimates, beliefs, expectations,

intentions, strategies or projections, may be “forward-looking statements” within the meaning of the U.S. federal securities laws,

including the Private Securities Litigation Reform Act of 1995. We intend these forward-looking statements to be covered by the

safe harbor provisions for forward-looking statements in the United States securities laws. In some cases, these statements can

be identified by the use of forward-looking words such as “may,” “should,” “could,” “anticipate,” “estimate,” “expect,” “plan,”

“believe,” “predict,” “potential,” “intend” or similar expressions. Our expectations are not guarantees and are based on currently

available competitive, financial and economic data along with our operating plans. Forward-looking statements contained in this

presentation may include, but are not limited to, information regarding our estimates of losses related to catastrophes and other

large losses, measurements of potential losses in the fair value of our investment portfolio, our expectations regarding pricing

and other market conditions and valuations of the potential impact of movements in interest rates, equity prices, credit spreads

and foreign currency rates.

Forward-looking statements only reflect our expectations and are not guarantees of performance. Accordingly, there are or will

be important factors that could cause actual results to differ materially from those indicated in such statements. We believe that

these factors include, but are not limited to, the following:

• The occurrence and magnitude of natural and man-made disasters,

• Actual claims exceeding our loss reserves,

• General economic, capital and credit market conditions,

• The failure of any of the loss limitation methods we employ,

• The effects of emerging claims, coverage and regulatory issues,

• The failure of our cedants to adequately evaluate risks,

• Inability to obtain additional capital on favorable terms, or at all,

• The loss of one or more key executives,

• A decline in our ratings with rating agencies,

• Loss of business provided to us by our major brokers,

• Changes in accounting policies or practices,

• The use of industry catastrophe models and changes to these models,

• Changes in governmental regulations,

• Increased competition,

• Changes in the political environment of certain countries in which we operate or underwrite business, and

• Fluctuations in interest rates, credit spreads, equity prices and/or currency values.

This report is for informational purposes only. It should be read in conjunction with the documents that we file with the

Securities and Exchange Commission pursuant to the Securities Act of 1933 and the Securities Exchange Act of 1934.

2

Agenda

Historical Development

The Bermudian Reinsurance Market today

The Bermudian Business Model

Solvency II and Equivalency in Bermuda

Bermudian Players in Credit and Bond

Market Observations

3History of the Bermuda (Re)insurance Market

• 7 companies formed following September 11

• ACE and XL established to focusing on a broad mix of business

• Initial domicile of AIG address US commercial

(chosen by C.V. Starr) liability crisis • Total capital raised $15 Bn

1940’s 1960’s 1980’s 1992 2001 2005

• 8 companies formed following

Hurricane Andrew with > $500M of • 11 new companies formed

capital to address void in the following Hurricanes Katrina,

property cat reinsurance sector Rita and Wilma

• Captive insurance companies

formed (captive domicile of choice

• Total capital raised $14 Bn • Total capital raised $32 Bn

by the 1980s)

Bermuda has evolved as a world leader in taking on

all types of insurable risks

Source: Bank of America Merrill Lynch 2012 Property/Casualty Insurance Primer

4Developments since 2005

Parallel companies

Sidecars

No more new ‘Class’

Re-Domestication

Collateralized reinsurance offerings

5Bermuda Overview

Association of Bermuda Insurers and Reinsurers (ABIR)

22 companies deriving business income from over 100 countries

around the world

Highly capitalized with $90 Bn in total capital and surplus

$62 Bn in total gross written premiums

Market has grown in the last 25 years in response to market

demand

ABIR members are represented by 32’000 employees worldwide,

out of which 15’000 in the US and 1’700 in Bermuda

Source: Association of Bermuda Insurers and Reinsurers

Note: Data for calendar year 2010

6Significant Reinsurance Market

2010 Reinsurance NPW by Country – Top 40 Reinsurers Worldwide

UK France Japan

6,7% 6,2% 4,4%

Switzerland All Other

13,1% 6,3%

Germany

28,4%

Bermuda

15,8%

US

19,1%

Source: 2011 Standard & Poor’s Global Reinsurance Highlights

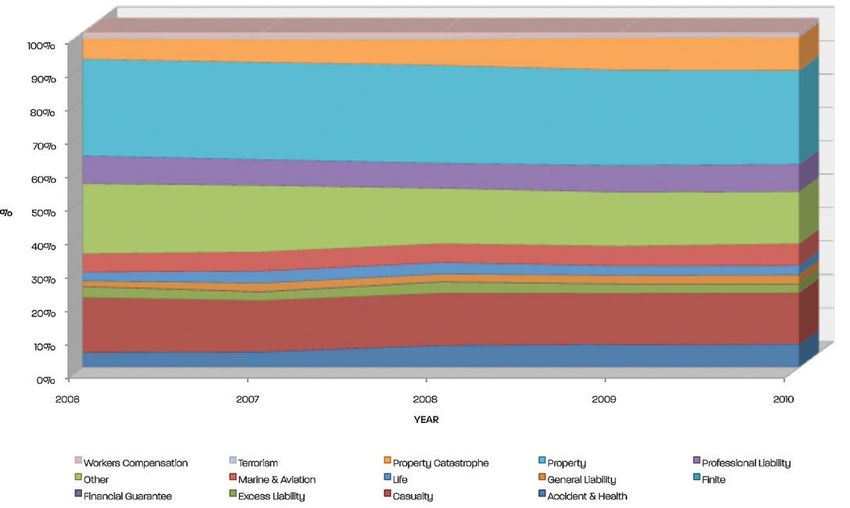

7Significant Product Diversity

Bermuda Gross Premiums Written by Line

Catastrophe

Property

Prof. Liability

Other

Marine & Aviation

Casualty

A&H

Source: Bermudian Business/Deloitte; Bermuda Insurance Survey April/May 2011

8Bermuda Reinsurers Cover the Globe

Principal underwriting operations in Bermuda, United States and

Europe

Share of Bermuda Re(insurers) of major catastrophe losses in 2010

and 2011:

29% of the international reinsured share for Japanese earthquake

25% of Gulf of Mexico oil spill

37% of Europe’s Windstorm Xynthia

51% of New Zealand’s earthquakes

38% of Chile’s earthquake

Geographic Diversification at Work

Source: Association of Bermuda Insurers and Reinsurers, March 2012

9Top 10 Bermuda (Re)insurers by Total Capital

As of December 31, 2011

($ in millions)

$29,436

$30,000

$25,000

$20,000

$15,000 $13,045

$10,000 $7,289 $6,889

$6,439

$5,028 $4,620

$3,985 $3,947 $3,671

$5,000

$-

Note: Financial data as of December 31, 2011

10Bermuda 10-Year Average ROACE

Publicly Traded Bermuda (Re)insurers (2002-2011)

25.0%

20.1%

20.0%

16.0%

14.2%

15.0% 12.9%

12.2%12.1%11.8% Mean = 10.7%

9.4% 9.2% 9.2% 9.2%

10.0%

7.1% 6.8%

5.0%

0.1%

0.0%

ROACE = Return on Average Common Equity

Source: Company reports, SNL

Note: Excludes “Class of 2005” companies

11Key considerations when establishing a Bermuda

based company

Bermuda proximity to US

Speed to market in Bermuda

Market acceptance

Business friendly environment

Bermuda Cat Market / London play

Physical locations to execute business plans in US, UK &

Europe

Attracting talent challenging

12The Bermudian Business Model

Entrepreneurial Spirit

Clear Strategy

Analytical, Technical, Disciplined Underwriting

Willingness to take measurable risk

Capacity

Lean Structure

Speed...Speed...Speed

Entrepreneurial, Technical, Bottom Line Focused

13Solvency II and Equivalency in Bermuda

EIOPA (European Insurance and Occupational Pension

Authority) assessed Bermuda for equivalency in 2011

Bermuda is partly equivalent to Solvency II based on a

preliminary assessment

Final assessment once Solvency II implementation

measures have been agreed upon (not expected before end

2013)

Solvency II has become a key component for the business

location in Bermuda

14Product Diversification into Credit & Bond

Reinsurers often seek to enter lines of business which are lowly

correlated, allowing Product Diversification (e.g. Credit & Bond,

Engineering, Agricultural, Aviation, Energy)

More than ten Bermudian companies with an estimated market

share of 20 to 25% write Credit and Bond

Bermudians with a dedicated Credit and Bond team:

– XL Re

– Partner Re

– Everest Re

– AXIS

– Arch (Ariel)

– Aspen

– Endurance

– Alterra

Some others are selectively offering Credit & Bond capacity

15Bermudians in Credit and Bond Reinsurance

Main ingredients for success:

Infrastructure and Capital

Understanding the products and the exposure

Talent

Senior Management involvement

Experience over cycles

Confidence in the business models of cedents

Commitment to Credit and Bond

Continuity, partnership and predictability

16Product and Geographical Diversification

Surety is rather local business compared to Credit; hence,

geographic expansion adds to diversification

LA Surety:

– Relatively new market

– Historically good results despite several crisis

– Growth potential

Surety cycle is different to the Credit cycle

Diversification with P&C but also within Credit and Bond over

various regions

17Zurich as Credit & Bond Reinsurance hub

Stable political environment

Well-established regulatory environment

Strategically located in the middle of Europe

Excellent infrastructure

Embracing an international mind-set

Availability of reinsurance talent

Ability to attract new talent and smooth integration of expatriates

18Market Observations

Bermudian (and other) entrants adding to the capacity supply

Increased competition on the Reinsurance side

(Over-)capacity provided by reinsurers fueling competition on

the primary side

As a result, we observe price and condition competition in

insurance

19You can also read