CY4GATE Initiation of coverage - Alessandro Cecchini +39 02 6204 859

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CY4GATE Initiation of coverage Alessandro Cecchini +39 02 6204 859 a.cecchini@equita.eu

CY4GATE | Initiation of coverage

Analyst:

BUY (prev. n.a.)

Alessandro Cecchini | a.cecchini@equita.eu|

+39 02 6204 856 Target: € 5.3 (prev. n.a.) | Risk: High

EQUITY RESEARCH A CYBER SENTINEL TO SECURE INVESTMENT RETURNS

Italy | Technology

If we think of the world of cyber software houses, US or Israeli companies

undoubtedly spring to mind. Italy has very few cyber software houses, none

STOCK DATA Ord of which has a military and law enforcement background...bar one: Cy4Gate

Price € 4.3 (CY4G). CY4 is a company that was established in 2015 with a portfolio of

Bloomberg code CY4 IM proprietary Cyber Intelligence, Cyber Security and Lawful Interception

Market Cap. (€ mn) 65 software solutions. The company went public to accelerate its growth path

Free Float 46% in highly appealing and rapidly expanding markets. We start the coverage on

Shares Out. (mn) 57.4 CY4G with a BUY rating and €5.3ps target price (2022 EV/EBITDA=c9.5x):

52-week range 3.9-4.9 CY4G is a unique company that offers sustained growth rates (2019-2023

Daily Volumes ('000) 18.9 Sales CAGR=+40%) backed up by its peculiar product portfolio and attractive

industry fundamentals.

MAIN METRICS 2020E 2021E 2022E

Revenues 10.0 14.5 23.5 ◼ CY4G: a pioneering company operating in the cyber world

Adjusted EBITDA 3.5 5.0 7.2 CY4G is a unique, pioneering company that was founded in 2015 thanks to

Net income 1.8 1.7 2.8 the idea of the company Elettronica SpA (which operates in the defence

Adj. EPS - € cents 10.1 11.4 17.9 electronics sector, is controlled by the Benigni family and counts Leonardo Spa

DPS ord - € cents 0.0 0.0 0.0

and Thales amongst its shareholders) and the software house Expert System

SpA to combine their entrepreneurial and financial resources and expertise

in order to create an entity that specialises in two rapidly expanding cyber

markets: Intelligence and Security.

MULTIPLES 2020E 2021E 2022E

Just five years later, CY4G:

P/E adj 43.0 x 38.1 x 24.2 x

• Boasts a complete and integrated portfolio of proprietary software

Adj. EV/EBITDA 15.5 x 11.5 x 7.7 x

solutions (#5) in both the Cyber Intelligence (D-Sint, Epeius, Hydra and

EV/Sales 5.4 x 4.0 x 2.4 x Gens.AI) and Cyber Security (RTA) markets and provides cyber services;

• Is a software house that is largely independent of its two founding

REMUNERATION 2020E 2021E 2022E companies with expertise in various segments (e.g. Big Data/Artificial

Div. Yield ord 0.0% 0.0% 0.0% Intelligence) and has a highly motivated and entrepreneurial management;

FCF yield -3.3% -5.1% 3.7% • Has a growing portfolio of high-standing clients, particularly in the

government sector (89% of 2019 sales) and corporate segment;

INDEBTEDNESS 2020E 2021E 2022E • Has a 38-strong workforce that is expected to grow in the coming years

NFP 10.8 7.5 9.9 (up to about 100 people over the medium-term);

Debt/EBITDA n.m. n.m. n.m. • Generated sales of around €7mn in 2019 (70% Italy/30% foreign markets)

Interests cov n.m. n.m. n.m. with positive margins (43.6% EBITDA margin) and a solid NFP (€-0.8mn).

◼ IPO main rationale: fresh resources to finance growth

The main purpose of the IPO was to raise funds (about €16mn) to finance organic

growth (e.g. salesforce expansion/product development/new branches) whilst

also enhancing visibility on the Group. The IPO enabled Expert System to monetise

its investment and use the proceeds to focus on its core business.

◼ BUY: unique company in the right markets

We are initiating coverage of CY4G with a BUY rating and €5.3ps target price

(implied 2022 EV/EBITDA=c9.5x and EV/Sales=c3x) because:

• We are confident of its sound growth opportunities (2019-2023 Sales and

PRICE ORD LAST 365 DAYS EBITDA CAGR=40%-30%) supported by attractive market fundamentals

(average 2018-2023 CAGR=c15%), the company’s unique product

portfolio (e.g proprietary solutions) and further market penetration (e.g

additional investment in marketing/distribution, international expansion,

growth in the under-penetrated corporate segment);

• CY4G is one of the few Italian stocks that can offer exposure to the mega

trends behind the Cyber security/intelligence world.

After the positive stock performance since the IPO (>+30%), s/t valuation is not

immediate (2020-21 EV/EBITDA=c15-11x vs NYSE Cyber Security Index=19-

17x) but coherent for such peculiar stock/business model with expected high

growth rates.

September 14, 2020 1 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT #305

CY4GATE | September 14, 2020

MAIN FIGURES € mn 2017 2018 2019 2020E 2021E 2022E

Revenues 2.1 5.2 7.1 10.0 14.5 23.5

Growth 41% 147% 36% 42% 45% 62%

Adjusted EBITDA -0.2 -0.6 3.1 3.5 5.0 7.2

Growth nm nm nm 14% 43% 44%

Adj.EBIT -0.8 -1.0 2.4 2.2 2.3 3.7

Growth nm nm nm -8% 6% 60%

Profit before tax -0.9 -1.0 2.3 1.9 2.1 3.5

Growth nm nm nm -20% 15% 64%

Net income -0.9 -1.0 1.9 1.8 1.7 2.8

Growth nm nm nm -5% -2% 64%

Adj. net income -0.9 -1.0 1.7 1.5 1.7 2.7

Growth nm nm nm -9% 13% 58%

MARGIN 2017 2018 2019 2020E 2021E 2022E

Ebitda adj Margin -10.0% -10.7% 43.6% 35.0% 34.7% 30.7%

Ebit adj margin -38.6% -18.3% 33.7% 21.9% 16.1% 15.9%

Pbt margin -42.1% -19.9% 32.7% 18.5% 14.7% 14.9%

Ni rep margin -42.1% -18.5% 26.2% 17.5% 11.9% 12.0%

Ni adj margin -42.1% -18.5% 23.5% 15.1% 11.8% 11.4%

SHARE DATA 2017 2018 2019 2020E 2021E 2022E

EPS - € cents n.a n.a n.a 11.7 11.5 18.9

Growth - - - - -2% 64%

Adj. EPS - € cents n.a n.a n.a 10.1 11.4 17.9

Growth - - - - 13% 58%

DPS ord - € cents n.a n.a n.a 0.0 0.0 0.0

BVPS n.a n.a n.a 1.5 1.6 1.8

VARIOUS - € mn 2017 2018 2019 2020E 2021E 2022E

Capital employed 2.1 4.7 6.1 11.9 17.0 17.4

FCF -0.8 -3.6 0.5 -2.1 -3.3 2.4

Capex 0.1 0.3 1.6 4.6 6.8 1.8

Working capital 1.2 4.0 4.5 5.1 6.1 8.3

INDEBTNESS - €mn 2017 2018 2019 2020E 2021E 2022E

NFP -1.7 -1.3 -0.8 10.8 7.5 9.9

D/E 4.4 x 0.4 x 0.2 x n.m. n.m. n.m.

Debt/EBITDA n.m. n.m. 0.3 x n.m. n.m. n.m.

Interests cov n.m. n.m. n.m. n.m. n.m. n.m.

MARKET RATIOS 2017 2018 2019 2020E 2021E 2022E

P/E n.a n.a n.a 36.9 x 37.7 x 23.0 x

P/E adj n.a n.a n.a 43.0 x 38.1 x 24.2 x

PBV n.a n.a n.a 2.9 x 2.7 x 2.4 x

EV FIGURES 2017 2018 2019 2020E 2021E 2022E

EV/Sales n.a n.a n.a 5.4 x 4.0 x 2.4 x

Adj. EV/EBITDA n.a n.a n.a 15.5 x 11.5 x 7.7 x

Adj. EV/EBIT n.a n.a n.a 24.7 x 24.7 x 14.9 x

EV/CE n.a n.a n.a 4.6 x 3.4 x 3.2 x

REMUNERATION 2017 2018 2019 2020E 2021E 2022E

Div. Yield ord n.a n.a n.a 0.0% 0.0% 0.0%

FCF yield n.a n.a n.a -3.3% -5.1% 3.7%

ROCE nm nm 28.2% 13.3% 9.9% 15.4%

ROE nm nm 35.1% 7.7% 7.0% 10.4%

Source: EQUITA SIM elaborations on Company Data and EQUITA SIM estimates

2 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

TABLE OF CONTENTS

INVESTMENT SUMMARY ......................................................................................... 4

SWOT AND RISK ANALYSIS .................................................................................... 14

ATTRACTIVE INDUSTRY FUNDAMENTALS ............................................................. 15

CY4GATE IN DEPTH ................................................................................................ 21

D-Sint: a sophisticated and modular product ................................................... 21

Epeius and Hydra: Lawful Interception 2.0 ....................................................... 23

Gens.AI: to gather info through avatars ........................................................... 27

RTA: to protect your infrastructure .................................................................. 28

Services: mainly training and educational services .......................................... 30

HISTORICAL NUMBERS: START-UP PROFILE. POSITIVE NUMBERS IN 2019 ........... 36

P&L analysis: positive profitability, personnel expenses account for a large

percentage of costs .......................................................................................... 36

BS/FCF analysis: limited assets. NWC “is” capital employed ............................ 38

ESTIMATES: EXPLOITING THE PRODUCT PORTFOLIO ............................................ 40

Top-line to grow significantly: 2019-2023 CAGR=40%! .................................... 40

EBIT to more than double in 2023 .................................................................... 42

Net Income to benefit from no financial charges and low taxes ...................... 43

FCF more skewed in the medium-term. Healthy financial structure................ 44

UPSIDE SCENARIO FROM NEW INITIATIVES .......................................................... 45

Increased contribution from partnership with SIO (Lawful Interception) ........ 45

Commercial partnership with an Italian Defence player .................................. 45

Sales from IGEA/HITS products (Cyber Intelligence for Covid-19).................... 45

MANAGEMENT TEAM ........................................................................................... 46

SHAREHOLDING STRUCTURE ................................................................................. 48

VALUATION ............................................................................................................ 49

PEERS COMPANY PROFILE ..................................................................................... 53

3 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

INVESTMENT SUMMARY

CY4G: a pioneering company operating in the cyber world

When we think of software houses operating in the world of cyber security or cyber

intelligence, it is not Italian firms but rather US companies or one of the many Israeli

start-ups that automatically spring to mind.

Although this might be so, Italy also has something to offer in this area.

There are very few Italian companies operating in the sector and none of them can

claim to have a military/government background, bar one: Cy4gate (CY4G).

CY4G is a unique, pioneering company that was founded in 2015 thanks to the idea

of the company Elettronica SpA (operating in the defence electronics sector with

shareholders such as the Benigni family, Leonardo Spa and Thales) and the software

house Expert System SpA (semantic software developer listed on the AIM market) to

combine their entrepreneurial and financial resources and expertise in order to

create an entity that specialises in two rapidly expanding cyber markets: Intelligence

and Security.

We believe this was a shrewd move given the increasingly cyber/digitally-oriented

and competitive world we live in and some underlying certainties:

• The amount of information/data to be found online is growing exponentially due

to the increasing number of "digital" users (corporate entities/individuals) and the

advent of the so-called Internet of Things;

• Corporate strategic decision-making is becoming increasingly complex (e.g the

world is ever more global, competitive, uncertain..);

• Wars are more often "electronic" (e.g. disabling strategic facilities) as opposed to

"traditional" (e.g. use of conventional weapons);

• Corporate entities are more and more prone to cyber attacks as their IT

infrastructures are increasingly vital and their assets interconnected: the risk of

cyber-attacks was included in the 2020 Global Risk Matrix of the World Economic

Forum as the world's greatest technological threat (on a par with climate change

and catastrophic event risks).

Consequently, all those whose:

• Primary concern is to protect citizens from crimes/health emergencies (e.g. public

prosecutors, intelligence agencies, armed forces, law enforcement);

• Aim is to protect their assets (e.g government and private entities);

• Aim is to improve the effectiveness of their strategic decisions.

....must therefore keep pace with the times and adopt an increasing number of new

advanced solutions. It is here that CY4G plans to make its mark with its proprietary

products and services based on its multi-layered and consolidated expertise in

various areas that range from Big Data to AI algorithms (e.g. machine learning, data

mining, etc).

Need an in-depth report on "El Chapo's" successor in Mexico? Is your CEO asking for

detailed information on a client or a supplier that is based in an area with a high

crime rate? Do you need to equip your drone detection system with a solution able

to scout the new commercial models in the market?

CY4G has developed a sophisticated modular software called D-Sint.

An intelligence agency needs to tap and monitor all the data traffic of a suspected

criminal (text messages, photos, calls, etc.)? CY4G's Epeius software is the solution.

The police need a criminal's detailed digital profile (what do they use on their cell

phone)? CY4G's Hydra is the answer.

4 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

Need an avatar to monitor the behaviour of potential terrorists on social networks?

CY4G has developed Gens.AI.

Need to secure a tank or industrial facility? CY4G can offer RTA (Real time Analytics),

which monitors data in real time and identifies potential problems and serious virus risks.

Just five years after it was set up, CY4G:

• Boasts a complete and integrated portfolio of proprietary software solutions (#5)

in both the cyber intelligence (D-Sint, Epeius, Hydra and Gens.AI) and cyber

security (RTA) segments. From these “standard” products, CY4G has already

developed derivative solutions (e.g IGEA/HITS);

• Provides advanced cyber services (e.g penetration tests, reverse engineering,

training sessions etc..);

• Is a software house that is independent of its two founding companies

(Elettronica and Expert System) with expertise in Big Data/Semantics/Machine

Learning/IoT/Artificial Intelligence;

• Has a growing portfolio of high-standing clients, particularly in the government

sector and corporate segment;

• Has a 38-strong workforce that is expected to grow in the coming years (about 100

people over the medium-term);

• Generated sales of around €7mn in 2019 with positive margins (43.6% EBITDA

margin) and a solid net financial position (NFP €-0.8mn).

CY4G: SALES BREAKDOWN (2019)

BY END MARKET BY GEOGRAPHY BY PRODUCT

Corporate

11%

Export Services

30% 32%

Government

89%

Licences

Italy 68%

70%

Source: Company data

CY4G: HISTORY (2014-2019)

Source: Company presentation

Thanks to the IPO, investors has become a real partner for Elettronica by supporting

the company’s medium-term development.

5 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

We find that CY4G has the following appealing features:

◼ Attractive industry fundamentals: double digit growth rates with low

correlation to GDP

CY4G’s products could be included in three wide reference markets (AIRO, OSINT and

Global Lawful Interception) with a total estimated value of >$25bn on a global level

(2023E).

These markets are expected to generate attractive growth rates (2018-2023

CAGR=15% on average) driven by a number of factors, many of which have a low

correlation to the GDP trend (an important characteristic, especially in the current

situation).

Cyber Intelligence and Cyber Security products and services (excluding Lawful

Interception products) can be included in the following two markets:

• AIRO (Analytics, Intelligence, Response and Orchestration);

• OSINT (Open Source Intelligence).

AIRO MARKET (2017A-2023, $BN)

Source: IDC, 2019

OSINT MARKET (2018A-2023, $BN)

Source: Global OSINT market report

6 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

Among the main drivers we highlight:

• Cyber-physical system attacks are expected to have an increasing financial impact

due to the continuous evolution of operational technology (OT), smart buildings,

smart cities, connected cars which expose organisations to risks, threats and

vulnerabilities;

• Complexities and compliance stemming from trade wars and political instability

will boost investments in cyber security;

• Organisations will experience an increasing need to add expertise to newer IT and

security personnel in order to protect their IT systems;

• The use of Open Source Intelligence platforms to combat criminal activity

(becoming increasingly sophisticated and often hidden on the web) and for

corporate strategic decision-making (corporate demand) will become more and

more common.

CY4G’s Lawful Interception products are included in a market with a value of around

$1bn on a global level (2019).

GLOBAL LAWFUL INTERCEPTION MARKET (2018A-2023E, $BN)

Source: Technavio

We see the following drivers for the Lawful Interception market (last point specifically

for the Italian market):

• Technology: messages are subject to end-to-end encryption (e.g. WhatsApp

messages) and wire taps and surveillance are no longer sufficient (as they were

around 4-5 years ago). As a result, demand is growing for so-called Trojans (e.g.

Epeius), which can be installed directly on cell phones without the need to involve

telecom operators;

• Socio-behavioural: more and more communication/criminal activity is taking place

on the deep-dark web/social networks;

• Legislation: as of 1st May 2020, the “Spazzacorrotti" (anti-corruption) law greatly

increases the number of criminal offences (e.g. crimes committed against public

authorities) that may be monitored using digital interception.

7 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

◼ An integrated product portfolio to meet diversified needs

In our view, one of CY4G's most appealing features is what we consider to be a highly

unique product portfolio.

Indeed, CY4G is practically unrivalled in Italy in both Intelligence and Cyber Security,

and its competitors are lacking in terms of proprietary products: we estimate that

most operators in Italy are either re-sellers of foreign products or act as service

providers.

CY4G – PRODUCT PORTFOLIO (2020)

Source: Company presentation

One-stop-shop of integrated solutions in the cyber-Intelligence world

CY4G's portfolio is unique, particularly in the key market of Intelligence, given that:

• Its portfolio is comprised entirely of proprietary products that combine its

expertise in various fields;

• Solutions can be integrated to offer a complete package: the competition might

currently have potentially more sophisticated solutions in one area, but CY4G's

rivals are unlikely to have a complete package of products that can be combined

with each other, especially its Italian rivals.

For example, if we take client X, which is targeting individual/situation Y: using

CY4G products, the client could choose to simply focus on passive interception (e.g.

Hydra) or to use active interception solutions (Epeius) or potentially obtain a

detailed analysis of data gathered from all systems to gain a "God's eye view" using

the sophisticated modular software D-Sint;

8 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORT

CY4GATE | September 14, 2020

CY4G: A TARGET CENTRIC APPROACH, CYBER INTELLIGENCE

Source: Company presentation

• Solutions are highly customisable and versatile: CY4G's IGEA (Integrated Guest

Easy Access) platform for management and planning of the post Covid-19 peak

phase is a clear example of the versatility of its solutions given that IGEA was

derived from D-Sint.

RTA: to protect your infrastructure (e.g pipelines, industrial sites, ships, tanks)

RTA (Real Time Analytics) is a cyber security software solution used to protect/monitor

IT/industrial infrastructure based on Big Data Analytics technology.

Noteworthy this sophisticated software is mostly devoted to protecting industrial

(e.g pipelines, industrial sites etc.) and military (e.g ship/tank/plane etc.)

infrastructures from cyber attacks (we can name this world as “Cyber resilience”).

These end-markets are “green field” (so far corporate/military departments have paid

little attention to protect this kind of infrastructures) leading to significant

opportunities for CY4G.

Both cyber intelligence and cyber security solutions

While its competitors are often focused on either Intelligence or Security, CY4G is

exposed to both and also offers the relevant products and services.

9 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ Government roots plus Elettronica as main shareholder: great strength!

Another aspect we like about CY4G is that the management team and main

shareholder have a background in government and the latter is a solid and important

company (4th place globally in military defence electronics with roughly 900

employees and >€200mn sales in 2019. NFP was roughly neutral).

Management team members come from the following backgrounds:

• Military (CEO Eugenio Santagata, Operations & Quality director Massimiliano

Romeo);

• Defence and Security (Chairman Domitilla Benigni, CEO Eugenio Santagata and

Marketing & Sales director Enrico Fazio).

As for Elettronica, it is private company set-up and controlled by the Benigni family

(35.3%) with a large portion of the capital held by two government companies

(Thales at 33.3% and Leonardo 31.3%).

Leonardo has not in its Italian product portfolio Electronic Warfare solutions and in

the Cyber Security world does not have the same product portfolio of CY4G.

ELETTRONICA: BUSINESS DESCRIPTION AND KEY FINANCIALS

Source: Company data

We believe that these features are a winning card from a business perspective,

particularly in Intelligence (as well as security) given that:

• Government clients (law enforcement, armed forces, public prosecutors, etc)

speak the same language as CY4G, which could benefit from having such

prestigious contacts;

• Clients and investors may be reassured by the fact that although CY4G is still a

small company with just a short history that generates turnover of just a few

million euros, it still has a heavyweight shareholder structure!

Furthermore, Elettronica is a real asset for CY4G (and CY4G is a real asset for

Elettronica as well) given that Elettronica’s Electronic Warfare solutions (e.g solutions

installed in military aircrafts or war vessels able to detect potential threats like enemy

radars) need more and more Cyber Security software like RTA/D-Sint.

10 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ IPO main rationale: resources to finance international growth and expansion

in the corporate sector

The primary focus of the IPO was to:

• Raise enough capital to finance organic growth;

• Improve visibility on the company (CY4G seen not simply as a "division" of

Elettronica but also as an "independent" company).

Of the roughly €16mn that the company raised, we estimate that:

• Around €7-9mn will be spent on the development of currently existing Lawful

Interception products (e.g. new functions, applications, features) to: 1) penetrate

the international market, which offers larger dimensions and significant

opportunities (international contracts can sometimes amount to tens of millions),

but will also bring competitors (e.g. Israeli) that sometimes offer more

sophisticated solutions (e.g. in terms of infection methods) and 2) furtherly widen

the current gap to competitors in Italy catching all the market opportunities;

• Around €3-4mn of the proceeds may be used for a 3-year plan to: 1) strengthen

the salesforce (we estimate 6 new salespeople between seniors/specialists) to

better penetrate mainly international/corporate channels, 2) increase marketing

investments and 3) forge commercial partnerships (indirect channel), which

always require initial investments (e.g. conventions, trials, etc).

We underline that: 1) CY4G generated €7mn in sales in 2019 despite a very small

sales force (4 salespeople including the CEO) and 2) CY4G will benefit from the

Elettronica’s International offices to sell its products (as it did in 2019 in a still

limited way given the recent set-up of its proprietary portfolio).

In addition to increasing capital, the IPO allowed Expert System, to monetise its

investment and reinvest the proceeds in expanding its core business.

We underline that Expert System's shareholder structure changed in 2019 with the

arrival of new shareholders (Claudio Costamagna, Diego Piacentini and Francesco Caio

through the holding Ergo Srl).

CY4G: IPO RATIONALE

Source: Company presentation

11 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

Additional considerations:

• We believe that Elettronica could also have provided the resources required to

finance growth (it launched a €4mn capital increase back in 2018 thus increasing

its stake from 75.5% to 82%) but that management pushed for an IPO in order to

improve visibility on the company (currently not very well known outside the

sector);

• We do not think Expert System's departure is a problem given that: 1) CY4G will

continue regardless to purchase the semantic intelligence module developed by

Expert (amongst the various modules, 7 in total, that are required for D-Sint), which

can if necessary also be replaced by products from other suppliers and 2) relations

between the two companies are excellent.

◼ Estimates: targeting significant business growth

CY4G is a young company considering that it only really began to sell its proprietary

products in 2019.

We expect numbers to greatly improve in the coming years, driven mainly by the

effective penetration of key markets (which themselves are expected to enjoy rapid

growth), partly thanks to the investment of the €15.8mn proceeds from the capital

increase (we estimate €8mn in capex for product development and €4-5mn to

strengthen the sales/marketing team).

Our estimates:

• Sales from €7.1mn in 2019 to €27.3mn in 2023;

• Adj. EBITDA from €3.1mn in 2019 to €8.8mn in 2023;

• Net profit from €1.9mn in 2019 to €4.1mn in 2023;

• NFP from €-0.8mn in 2019 to €14mn in 2023 (following €15.8mn capital increase).

In the shorter term (2020-22), prudently we do not expect positive operating leverage in

light of the salesforce expansion, international growth and company structuring after the

IPO.

We estimate that the most tangible effects of the IPO proceeds (in terms of EBITDA)

will be seen as of 2022.

We suggest focussing (at least in the short term) on analysing/monitoring the

evolution of the business in terms of turnover growth, number of clients, launch of

new applications, where we believe CY4G has ample room for growth!

Considering the new initiatives currently in place we have included in our report a

dedicated paragraph named “Upside scenario from new initiatives”.

Estimates included in this report incorporate minor adjustments to those showed in

our IPO research:

• Capital increase of €15.8mn instead of €15mn;

• €0.25mn of annual non-recurring items at the P&L level relating to the IPO costs

(included in D&A).

12 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ M&A optionality is not ruled out

Although we do not think that M&A is the most appealing part of the CY4G equity

story, we do believe that it could be a driver of further growth (possibly with

subsequent capital injections).

We believe that end point cyber protection and security orchestration are amongst

the most appealing sectors.

CY4G: POTENTIAL M&A PIPELINE

Source: Company presentation

Regarding passive M&A, although we do not believe there is a possibility that CY4G

could become a takeover target, partly considering that it is protected by Italy's

"Golden Power" legislation (covering assets that are considered strategic for Italy), on

the other hand, we cannot completely rule out the possibility that the current

shareholders/government companies may attempt to tighten their grip on the

company sometime in the medium-long term.

13 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

SWOT AND RISK ANALYSIS

Strengths:

• Wide range of proprietary products with cutting-edge technology backed by years

of experience in Cyber Intelligence and Security;

• CY4G has built and sold its proprietary software portfolio while most operators

in Italy are either re-sellers of foreign products or act as service providers;

• Exposure to growing reference sectors and bolstered by structural drivers;

• Strong shareholder structure: Elettronica Group is an important company owned

by the Benigni family and by two large Aerospace&Defence companies (Leonardo

and Thales);

• Growing portfolio of high-standing clients, particularly in the government sector

(89% of 2019 sales) and corporate segment;

• High-standing management team with strong credibility in the defence industry.

Opportunities:

• Gaining market share in the Italian public prosecution sector (Lawful Interception

products) where there is ample room to grow;

• Expanding sales outside Italy and in the corporate sector where the penetration

rate is basically negligible. Outside Italy, CY4G can leverage its relationship with

Elettronica;

• Expanding sales in the Cyber resilience sector (to secure both military and

corporate infrastructures) that is “green field” and suitable for RTA software;

• Enlarging the product range even though the current range is already sufficient;

• Increasing features and applications of the current product portfolio, which is an

important barrier to entry;

• M&A deals to reinforce know-how, positioning and to expand end-markets.

Weaknesses:

• Limited size of the company compared to some larger competitors;

• Limited track-record on historical profitability and potential volatility of future

earnings;

• Current high NWC to sales (65% of sales). Nevertheless, this ratio is expected to

be improved by the management over the next years;

• Low visibility on some contracts (a small portion) and clients relating to

Government activity;

• Poor liquidity expected given the limited free-float (in absolute terms).

Threats:

• Increase in the cost and complexity of finding the workforce necessary to keep

up with the company's technological advancement/development in a scenario in

which resources of this kind are becoming increasingly scarce;

• Potentially "disruptive" technological innovation by competitors.

Risks:

• Although it has a strong and cohesive management team, the company is

undoubtedly inextricably linked to the current management;

• Inability to expand abroad/in the corporate sector properly with a decent

profitability level;

• Need for additional financial resources to step-up R&D investments and/or to

attract talent following subdued financial results/negative FCF.

14 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

ATTRACTIVE INDUSTRY FUNDAMENTALS

As we have seen, CY4G operates in some Cyber Intelligence and Cyber Security

market niches.

These are enormous, fragmented sectors, that are constantly evolving.

For this reason, it is not easy to quantify or identify their worth.

That said, we think that CY4G’s products could be included in three wide reference

markets with a total estimated value of >$25bn on a global level (2023E).

◼ Global Lawful Interception market - Epeius, Hydra and Gens.AI

Global lawful interception market (digital only) – $0.9bn (2019)

According to Technavio, globally (excluding China, Russia and other countries) this

market was worth around $ 0.9bn in terms of turnover in 2019 and is the key market

for CY4G products Hydra, Epeius and Gens.AI (we estimate roughly 20% of CY4G sales

in 2019).

The market gives us an accurate picture of the key market for CY4G given that it does

not include electronic interception/wiretaps (e.g. bugs, microphones, sensors),

markets that CY4G does not cover given the low technological content and large

number of potential competitors.

It is a relatively small market (compared, for example, to Cyber Security) but the

future CAGR (2018-2023) is expected to be significant (+24.6%).

GLOBAL LAWFUL INTERCEPTION MARKET ($, BN)

Source: Company presentation

15 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

Italian Lawful Interception market (digital only) – €36mn (2017E)

Whereas this is the global market, the Italian market (probably the most relevant for

CY4G, at least in the short term) is estimated by management to be worth around €

36mn in 2017 (excluding wiretaps, electronic surveillance and sale of licences).

It is a relatively new market, with little correlation to GDP trends (for obvious reasons)

and is expected to grow exponentially in the coming years, partly thanks to the

following:

• Technology: communication is increasingly subject to end-to-end encryption (e.g.

Whatsapp messages) and wiretaps/network surveillance are no longer sufficient

(as they were 4-5 years ago). Demand is rising for trojans and other surveillance

software that can be installed directly on cell phones (e.g. Epeius) without the need

to involve telecom operators;

• Socio-behavioural: an increasing amount of communication/criminal activity takes

place on the deep-dark web / social networks;

• Legislation: as of 1st May 2020, the "Spazzacorrotti" law greatly increases the

number of criminal offences (e.g. against public authorities) that may be monitored

using digital surveillance.

ITALIAN LAWFUL INTERCEPTION MARKET (DIGITAL)

Source: Company presentation (1) management estimates take into consideration only the digital interception market

16 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ OSINT – D-Sint and derivative products

The OSINT market (Open source Intelligence) includes all the products that

collect/process and analyse public information in order to take a decision.

Global OSINT market report expects this market to grow with a 2018-2013

CAGR=16.8%.

The use of Open Source Intelligence platforms to combat criminal activity (becoming

increasingly sophisticated and often hidden on the web) and for corporate strategic

decision-making (corporate demand) will become more and more common.

OSINT MARKET ($, BN)

Source: Company presentation

17 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ AIRO – RTA, services and D-Sint

The consulting firm IDC terms a market that includes three large segments "AIRO":

Analytics and Intelligence, Response and Orchestration.

CY4G software solutions that can be included in these markets are: D-Sint, RTA and

all services (total turnover at roughly 80% of sales in 2019).

THE AIRO MARKET ($, BN)

Source: Company presentation based on IDC Estimates

It is worth noting that most of the activities of the large consulting/system integration

firms (e.g. Capgemini/Deloitte) that produce Cybersecurity manuals and of cyber

companies that offer services such as penetration tests/vulnerability assessments are

to be found in the "Response" segment.

These markets are estimated to be worth a total of roughly $10.5bn on a global level

(2019) with an expected growth rate of 11.5% (2018-2023) driven by factors not

strictly correlated to the economic cycle:

• Cyber-physical system attacks are expected to have an increasing financial impact

due to the continuous evolution of operational technology (OT), smart buildings,

smart cities, connected cars, which expose organisations to risks, threats and

vulnerabilities;

• Complexities and compliance stemming from trade wars and political instability

will boost investments in cyber security;

• Organisations will experience an increasing need to add expertise to newer IT and

security personnel in order to protect their IT systems.

18 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

AIRO MARKET (2017-2023, $BN)

Source: IDC, 2019

◼ How is big the addressable market for CY4G?

Having said that, if we look specifically at CY4G and its economic / commercial and

product opportunities, management estimates very precisely that the addressable

market (2023E) for CY4G could value approximately 2% of the total Lawful

Interception digital market + AIRO + OSINT ($ 0.6bn vs $ 25.7bn).

Products and geographies that are relatively inaccessible for commercial and

regulatory reasons (e.g. USA, China, Russia, Israel and other markets) have been

excluded.

CY4G: ADDRESSABLE MARKET (2023, $MN/BN)

Note: addressable market estimated excluding USA, China, Russia, Israel and other not accessible market

Source: Company presentation

19 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

A large percentage of the opportunities are concentrated in Italy (around 30%) but

the biggest market opportunities lie outside Italy (around 70%, i.e. Middle-East /

Africa / Asia) and this is also one of the main reasons for the IPO (fresh resources to

finance growth on these markets).

In terms of end-markets by client type, we highlight the following:

• Unsurprisingly, the market that is most easily accessible in the field of cyber

intelligence is government agencies (e.g. public prosecutors, police, intelligence,

etc.) but the corporate world is also an appealing target market thanks to the

strategic value of D-Sint (top managers are increasingly in need of critical/rapid/

easy-to-read data) and of the derivative product IGEA (companies/businesses need

to have systems in place to monitor points of entry in the post Covid-19 peak

world);

• Cyber security includes a huge (51% of the total), as yet mainly unexplored

market i.e. military (ship/tank/plane security through RTA/services) as well as

significant opportunities in the corporate world (42% of the total), where CY4G

aims to focus mainly on plant security (e.g. pipelines, industrial sites).

20 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

CY4GATE IN DEPTH

CY4G operates in the cyber intelligence/lawful interception and cyber security

markets. CY4G solutions in these segments are as follows:

• Proprietary, customisable software products (68% of 2019 sales) that can be used

in combination with each other (Cyber intelligence/Lawful interception: D-SINT,

Hydra, Epeius and Gens.AI, and in Cyber security: RTA);

• Services (32% of 2019 sales), i.e., anything other than the sale of proprietary products

and/or services dedicated strictly to the application of the products. At present, the

majority of services involve on-the-job training (CY4G Academy) and services such as

Penetration Tests, Vulnerability Assessments, Reverse Engineering, etc. CY4G mainly

sells man-hours but sometimes also infrastructure (e.g. digital laboratory).

◼ D-Sint: a sophisticated and modular product

"Who is El Chapo's successor in Mexico?", "Where are all my employees at the

moment?", "What's going on in Nigeria?", "Are potentially dangerous criminal cells

being created in South-east Asia?", "Where do the people who have officially contract

ed Covid-19 live?

D-Sint can answer all these questions quickly, efficiently and correctly!

D-Sint (which we estimate accounted for around 30% of CY4G 2019 sales) is a

technologically advanced software and offers:

• A high level of sophistication (using a number of AI algorithms) and allows for rapid

and accurate object recognition (i.e. recognition without digital noise). The fact that

management has been working on the product since 2010-2011 proves just how

complex D-Sint is;

• Versatility given that it can be used by government agencies and private firms for

various purposes (e.g. identifying criminals, analysing markets, travel management,

post Covid-19 peak management);

• Varied customisation options (customising the product can take weeks/months)

and modularity (D-Sint is a modular software solution with

text/image/video/audio modules);

• High price (compared to other products) with a licence that we estimate may be

worth roughly € 0.5-1mn;

• Unique features on the European/Italian market.

General description and how it works:

D-Sint ("Data & Signal Intelligence") software is a sophisticated data analysis system that

can:

• Gather (from various sources);

• Process;

• Correlate

a large amount of both:

• Structured (e.g. alphabetical-numerical symbols/tabular) and

• Unstructured (e.g. text, videos/images/audio, etc.)

data on a specific target (e.g. individual, object, or company) for the purpose of

transforming a large amount of mixed data into a usable analysis/report for so-called

"decision-makers" (e.g. special forces).

Where does it get this information? D-Sint (once the

research input has been entered) uses data gathered

from sources within the organisation (e.g. closed

source databases), open sources (e.g. web/social

networks), deep/dark web sources and reports and

emails.

21 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

How does it process the data? D-Sint uses artificial intelligence technology such as

machine learning and semantic intelligence as well as data mining to:

• "Understand" the content of text, videos, audio files etc.

• Organises it according to concept, subject, location and size, and then correlates it.

Then what? Once data has been correlated and analysed, D-Sint:

• Extracts the content most relevant to the input using a series of AI algorithms

(image tagging, data mining, cognitive computing, machine learning, etc...) and

complies it into easy-to-read graphs/documents/reports;

• It can offer suggestions on how an analyst could improve an analysis.

How is it sold? Either under a software licence (typically chosen by government agency

clients) or through a software-as-a-service model (whereby the client pays for use and

not ownership of the software).

CY4G: D-SINT

Source: Company presentation

22 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

IGEA: to manage the post Covid-19 peak world

D-Sint's versatility was confirmed by the launch of IGEA (Integrated guest Easy

Access).

The current health crisis requires measures and solutions to both contain the spread

of Covid-19 and also to manage our "return to normality", e.g., to manage crowd

safety responsibly and effectively.

The IGEA solution is an integrated system that is able to manage this problem by using

a number of sensors, algorithms and instruments that are able to balance access

restrictions.

The solution:

• Identifies each individual anonymously (using mobile phones via Bluetooth);

• Measures their body temperature (using a thermocamera);

• Calculates the level of risk (using an AI algorithm) that may then: 1) permit access;

2) require specific actions; 3) deny access and require the person to undergo

further testing ("Pulse Oximeter Integrated Workstation") and 4) deny access and

require the person to take a rapid swab test.

The IGEA system also includes a simple "collaborative" access mode whereby

individuals use a phone app (HITS) that calculates their risk profile automatically and

issues a "gate pass" that can be shown directly at entry points.

The app (named HITS – Human Interaction Tracking System) and the design of the

HW/SW infrastructure are proprietary.

CY4G has sold its first solution (IGEA with its app HITS) to Elettronica.

◼ Epeius and Hydra: Lawful Interception 2.0

As we mentioned in an earlier section describing the markets, the world of Lawful

Interception is evolving on the back of technological advancements and legal

changes.

In the segment digital Lawful Interception, CY4G sells two proprietary solutions that

can be integrated and have an extremely intuitive interface: Hydra (passive Lawful

Interception) and Epeius (active Lawful Interception).

Hydra and Epeius are software platforms used to collect data from personal

electronic devices such as smartphones, tablets and personal computers.

Legal background: only available to law enforcement and intelligence agencies

Before describing the products, we should first underline some of the legal aspects:

• Use of these products is strictly limited to national and international Law

Enforcement and Intelligence Agencies;

• In Italy, the products may be used exclusively for the prevention and/or

investigation of certain crimes following the issue of an interception warrant by

a judge (valid for a specific amount of time), in accordance with Italian law;

• The products may be sold internationally but only with government authorisation

since this involves the export of sensitive technology on a par with military

equipment. For example, CY4G can sell its solutions to France but not Myanmar;

• CY4G software solutions are comprised by two "components":1) data collection

software and 2) servers "controlled" exclusively by the judiciary where the

collected data is stored (CY4G does not have access to any data).

Moreover, CY4G provides training, technical assistance and technical support to

public prosecutors in order to maximise the potential of the software.

23 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

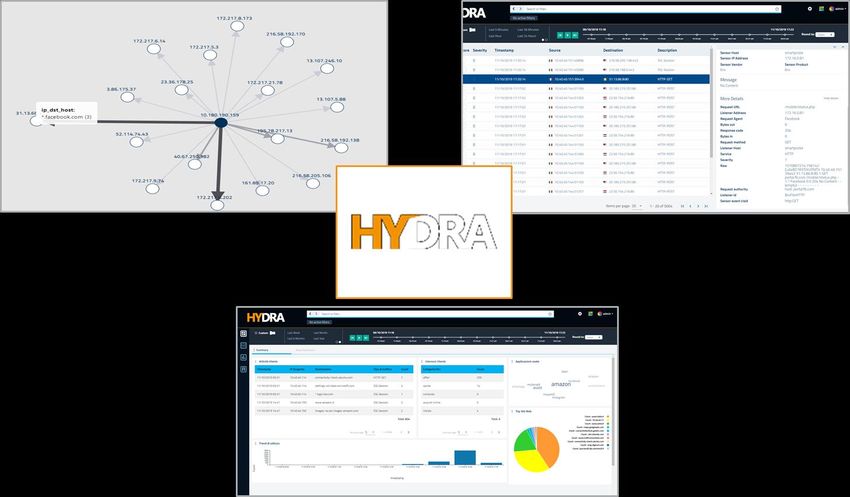

Hydra: digital profiling

Hydra is a software solution used for passive interception i.e. analysis of metadata

rather than content (which is encrypted), thus allowing it to create a digital profile of

the target without analysing the specific content.

It is a "simpler" product than Epeius, but no less important.

CY4G does not install anything on a client's device, but rather it "listens" to network

data (so-called unencrypted traffic).

Therefore, it can answer the following questions on digital behaviour: "How many

times a day does my target access the internet? "Which websites does my target visit

and when? Which apps have been installed and how often are they used?

But does not answer the following questions: "What did my target buy on Amazon?",

"What did my target write on day X to person Y on WhatsApp?"

For a public prosecutor it may be very interesting to learn that a target is always out of

the house between 9:00 and 10:00 in the morning or that the target visits certain

websites.

Once data has been collected, it is not presented in "raw" form but rather it is

"enriched" and presented using intuitive dashboards/clusters (e.g. number of online

shopping sites visited per day, number of information sites, etc).

When and how was it created? Hydra was developed starting from 2015 and derives

from RTA software.

How is it sold? Hydra is sold on a "per use" basis with an estimated price of around €50

per day for a single warrant, or otherwise under licence.

CY4G: HYDRA

Source: Company presentation

24 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

CY4G: HYDRA

Source: Company presentation

Epeius: do you remember the legend of the Trojan horse?

The product was named after its original creator: It was Epeius who built the mythical

Trojan horse!

Epeius is an active interception product, i.e. data is collected directly from the target's

device.

Active interception goes one step further than passive interception by collecting the

content of the target's digital traffic in addition to metadata.

Therefore, it collects both private/personal data as well as unencrypted traffic: it

allows the user to read chat conversations, record telephone calls (including VOIP),

watch shared videos/see shared images, etc.

Two aspects need to be considered with these types of products:

• Product type: does it work on Android and/or Apple devices? Does it capture all

means of communication precisely and quickly? Is the layout easy to read?;

• Installation method: this is often what separates one product from another.

For example, based on our analysis, Epeius can be installed via "temporary" apps

that the target unwittingly installs on their device (downloaded from a site their

digital profile created by Hydra shows they may be interested in) or a malfunction.

More sophisticated methods include the simple access to a single web page.

When and how was it created? Epeius was developed starting from 2015 based on

Trojans used for military purposes.

How is it sold? Like Hydra, Epeius is often sold on a "per use" basis at a price that we

estimate at roughly € 150 euro per day (average duration of use may be around 40 days).

Other sales methods: under licence.

25 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

CY4G: EPEIUS

Source: Company presentation

CYFG: EPEIUS

Source: Company presentation

26 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ Gens.AI: to gather info through avatars

Gens. AI is CY4G's latest product in the segment of Virtual Humint.

Whereas

• D-Sint allows the user to gather data online;

• Hydra/Epeius can monitor digital data on target devices subject to legal permission;

……Gens. AI takes it one step further: by creating and actively managing virtual Avatars

("virtual identities") that cannot be traced back to CY4G or the software user,

information can be obtained by interacting with online users (subject to legal

authorisation).

Gens. AI creates fake online users with a history, life, precise location which access

social networks in order to monito r and prevent crimes such as drug trafficking, child

pornography, terrorism and related offences.

For example, it proves very useful for identifying paedophiles who use the internet to

search for potential victims (the avatar in this case might be a pretty 17-year-old girl).

Avatars are created, trained and actively managed (for example, interrupting or

changing automated activity) by an authorised human CY4G operator.

When and how was it created? Gens.AI was developed in 2018 and is based on AI

algorithms. Sales were limited at the end of 2019.

How is it sold? The product is sold under licence.

CY4G: GENS.AI

Source: Company presentation

CY4G: GENS.AI

Source: Company presentation

27 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ RTA: to protect your infrastructure

RTA (Real Time Analytics) is a cyber security software solution used to protect/monitor

IT/industrial infrastructure based on Big Data Analytics technology.

In the segment of cyber security, the product is included in the markets of SIEM

(security information and Event Management) and NTA (Network Traffic Analyzer).

Put simply, the process is as follows:

• Collection and analysis of event flows (standard and non-standard data such as

emails, telephone traffic, sensor traffic) from multiple sources (e.g. PCs, mobile

phones, industrial sites);

• Real-time contextualisation of monitored activities;

• Indexing of all contextualised data in a "time-machine";

• Automatic identification of risky situations / anomalies and consequent

classification (various levels of risk) and categorisation;

• Suggested solutions for each problem.

RTA is not an antivirus software in the sense that it stops the intrusion, but it tells the

client if they have a problem or not and provides potential solutions.

Two examples:

Example 1

In the corporate segment, RTA allows analysts to identify whether any warnings,

anomalies, attacks on the IT infrastructure have taken place.

Once any potential anomalies have been identified, the system flags if they have

already occurred in the past (thanks to the Time-machine) and suggests any potential

solutions.

One example of a red flag might be if an employee's company computer were accessed

from Brazil and then from Europe immediately afterwards.

Example 2

In the military sector, it is becoming increasingly important to be able to monitor all

military infrastructure (e.g. drones, planes, tanks) in real-time and RTA can help in this

respect.

Regarding applications sold by Elettronica, the company sells Electronic Warfare

systems that are composed of hardware and software components. RTA helps to

ensure that these solutions are secure.

When and how was it created? RTA started to be developed in 2017 and marketed as

of 2019.

How is it sold? Either under a software licence (typically preferred by government

agency clients) or software-as-a-service (where the client pays for use and not

ownership of the software).

We estimate that licences may be worth around € 0.2/0.3mn.

28 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

CY4G: RTA

Source: Company presentation

CY4G: RTA

Source: Company presentation

29 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ Services: mainly training and educational services

Within the services category ("Cy4Sec"), CY4G includes all turnover that is not

considered the sale of proprietary products and / or services dedicated strictly to

product implementation.

At present, the majority of this category is accounted for by on-the-job training (CY4G

Academy), which is essentially a transfer of know-how (e.g. CY4G teaches military

personnel to defend themselves from Cyber-attacks), and some services such as

Penetration Tests, Vulnerability Assessments, Reverse Engineering, ISoc (virtual

environment) rental, cyber security policy manuals etc ...

As for services, CY4G mainly sells man hours in addition to any infrastructure /

software (e.g. digital laboratory in Digilab) that may be required.

When it comes to orders for multi-year "services" (such as a contract included in the

FY19 backlog worth € 6mn), this entails providing a complete package of man hours

(e.g. on-the-job training), software and hardware to ensure that the client improves

their Cyber Security expertise (e.g. crypto analysis, malware analysis, penetration

testing etc.).

The following tables show some of CY4G's key services:

CY4G: ISOC CSIRT

Source: Company presentation

CY4G: CY4GATE ACADEMY

Source: Company presentation

30 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

CY4G: DIGILAB

Source: Company presentation

CY4G: SECURITY ASSESSMENT SERVICES

Source: Company presentation

CY4G: CYBER RESILIENCE FOR MILITARY SYSTEMS

Source: Company presentation

31 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTCY4GATE | September 14, 2020

◼ How are CY4G’s solutions sold?

CY4G's proprietary products are sold in three different ways:

• Sale of (perpetual) licences including a semi-recurring component in the form of

updates (we estimate about 20% of the value of a licence in year T + 2).

On average: 1) licences are sold in 3 instalments (first the basic software followed

by additional functions) which are spaced around 2 months apart (1: we estimate

60% of the value of the licence; 2 = we estimate 20% and 3 = the remaining 20%)

and 2) government clients / intelligence agencies prefer this sales format;

• SaaS (software as a service): the client does not actually own the product but

purchases the right to use it for a certain amount of time, typically one year.

Corporate clients tend to prefer this option given that the outlay is much smaller;

• Per use basis: typically used for the sale of Lawful Interception products

(Hydra/Epeius) to public prosecutors (number of days' use multiplied by the price

per day).

Services are sold by billing the total number of man hours (if any) plus the sale of any

hardware.

◼ How much of CY4G’s business is recurring?

CY4G is a very new company and as such we do not have much historical information

at our disposal.

That said, in qualitative terms, "recurring sales" could be comprised by:

• Licence updates (we estimate 20% of the value of the licence at T +2);

• Sales on a per use basis of Lawful Interception services to public prosecutors

(negligible at FY19).

32 IMPORTANT DISCLOSURES APPEAR AT THE BACK OF THIS REPORTYou can also read