CONVERSE Title to come - DSP Mutual Fund

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

November 2022

#INVESTFORGOOD

CONVERSE

[Title to come]

[Sub-Title to come]

Metrics that matter NOW in Fixed Income

Date Strictly for Intended Recipients Only

* DSP India Fund is the Company incorporated in Mauritius, under which ILSF is the corresponding share class

Agenda

Overview: Major Driver of Yields

Markets View: Analysing the market drivers

• Monetary Policy

• Fiscal policy

• Global scenario

• Others

DSP FI Framework: Our process

• DSP FI checklist

• Duration decision

• Duration allocation

• Asset allocation

DSP Fixed Income Universe: Our offering

• DSP Preferred funds with scenario

• DSP Active Funds

• DSP Money Market Funds

• DSP Passive Funds

2

Our View - Snapshot

➢ Phase 1: Rallies likely to be muted with reversals – currency risks on yields still not over

We had mentioned three reasons for yields to be under pressure in this quarter. But supply fears have eased. As the states

continue to borrow lesser, the expected fears of supply have reversed – making supply a reason for rally, rather than sell-off.

1. Rupee depreciation: While rupee has appreciated recently, but it is likely to come under pressure again. The capital

account inflows may not be sufficient to fund current account deficit.

2. Liquidity: We expect liquidity to remain tight unless the global central banks pause/ease and risks to currency evaporate.

3. Supply pressures: The lower SDL supply has eased the pressure on bonds. The supply in YTD FY23 is ~Rs. 1.5 lac cr. lesser.

This has made supply lesser than demand – leading to easing of pressure.

➢ Phase 2: Yields likely to consolidate and rally by Q4FY23

We continue to expect rally to occur in Q4FY23. The three reasons we mentioned remain:

1. RBI OMOs, as liquidity tightens RBI will have to increase the money supply and push in liquidity. Since FX asset purchase

are not looking likely, RBI will have to fill in the gap through domestic asset purchases, i.e. Government bonds.

2. Bond index inclusion chatter: By March 2023 JP Morgan will again revisit the index. Every iteration brings India’s

inclusion closer and is an inevitability sooner or later

3. Global central banks should be closer to end of rate hike cycle.

➢ Risk/Reward may favor debt investment in Q4FY23

Yields have rallied in past month. Yet, we advise to wait till Q4 to add duration. Why?

Because how much can 5-year bond rally from 7.10% when (i) overnight rates after next MPC is expected to be close to

6.25%-6.5% (ii) CPI is still high, (iii) rupee risks remain, (iv) risks to SDL supply are in Q4, and (v) election year budget is

coming?

Thus, risks seem to be lopsided towards wait-and-watch and invest in Q4FY23. Especially when the curve is flat.

Source: Internal; MPC – Monetary Policy Committee; OMO – Open Market Operations; SDL – State Development Loan; CPI – Consumer Price Index; YTD – Year To Date

Overview: Major drivers of yields

Monetary Policy Fiscal Policy Global Drivers Others

Inflation Supply Global Yields RBI Regime

• CPI still above target • Supply worries abated • Why is the gap between • Is there a divergence

levels at 6.77% US and India bond yield so between MPC members?

• SDL supply muted low?

• Likely to remain clouded • Focused on curtailing

• Taxes stagnant • US CPI falling, yet high

with uncertainties inflation

• Recent focus on currency

Demand

Growth Geopolitics

• Probability of RBI OMO

• Domestic activity resilient in Q4 high • Ukraine war extension Misc.

• High trade deficit due to • Banks SLR/NDTL over

weak global demand • Prep for 2024 elections

30%

Bond Inclusion/FPI

Commodities

Currency/CAD/BOP • Binary event (CY23)

• Oil prices volatile

• Current Account Deficit • Could absorb supply &

still high support currency in FY24 • Other Commodities flat

• Capital outflows continue • Winter could lead to

higher energy prices

• Negative real rates

Takeaway:

Risks have mildly bearish bias, with sticky inflation and aggressive tightening by global central banks

Source – Internal CAD – Current Account Deficit; BoP – Balance of Payment; SLR – Statutory Liquidity Ratio; SDL – State Development Loans; NSSF: National Small 4

Saving Fund; RBI: Reserve Bank of India; G-Sec: Government Securities; CPI: Consumer Price Index; NDTL – Net Demand & Time LiabilitiesInflation: A difficult beast to predict

➢ CPI below 7% led by favorable base effects ➢ How closely do yields track inflation projection?

• Oct 22 CPI at 6.77% ( sharply ↓ from 7.4% in Sep 22) • CPI forecasts have low predictive power for Indian Yield

• Sequential uptick of 0.8% vs 0.6% in Sep’22 • The 1-Year future yields do not have much correlation

• Food inflation pushing inflation higher driven by cereals to with 1-Year future CPI forecasts

and vegetables • Primarily because CPI projections rarely get realized in

• Near term expected to remain volatile actual CPI

➢ CPI will have wide variance due to base effect • Since large part of CPI is volatile with low predictive

power – food and oil

• Scenario if CPI were to increase at 5% YoY going forward:

• CPI to be 6.4% in Nov 22, and sharply rise to 8.2% in

Feb 23

• RBI’s Q4FY23 projection of 5.8% to hold only if there is

marginal deflation

CPI Forecasted Inflation vs Bond Yields

8%

8.5

7% 7.5

6.5

6%

5.5

in %

5% 4.5

3.5

4%

2.5

Jun-22

Aug-22

Dec-22

Jun-23

Apr-22

Feb-23

Apr-23

Oct-22

1.5

Jan-18

Jan-19

Jan-20

Jan-21

Jan-22

Apr-20

Apr-18

Apr-19

Apr-21

Apr-22

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

Jul-18

Jul-19

Jul-20

Jul-21

Jul-22

0.5% MoM (6% annualized) 0.41% MoM (5% annualized)

0.33% MoM (4% annualized) RBI Projections 10Y IGB (%) 1Yr CPI Forecast (1 Yr Ago; in %) Actual CPI (%)

Actuals

Takeaway:

In our view, Inflation to remain volatile due to base effect.

Source: RBI, CSO ; CPI: Consumer Price Inflation;; RBI: Reserve Bank of India 5Growth: Domestic growth hitherto resilient, risks of global slowdown persist

➢ Domestic growth resilient, though risks remain ➢ How closely do yields track growth?

• Both manufacturing and services PMI have remained in

• Yields have usually tracked GDP growth, with

expansion at 55.3 and 55.1 respectively

correlation being stronger when growth slows,

• Healthy tax collections; barring

• GST collections have crossed INR 1.5 tn in October 22 • 2013, when rupee depreciation and debt outflow

• Despite higher inflation, GST undershooting Nominal growth • 2017, during demonetization

➢ Risks of global slowdown are playing out

• Trade deficit high at USD 26.7bn in October-22

• Exports de-grew by -16% yoy due to decline in global demand

20 10

India PMI Index 9

15

70 9

60 10 8

50 8

5

40 7

30 0 7

20 6

-5

10 6

0 -10 5

Apr-12

Apr-15

Apr-18

Apr-21

Jan-13

Jan-16

Jan-19

Jan-22

Oct-10

Jul-11

Oct-13

Jul-14

Oct-16

Jul-17

Oct-19

Jul-20

Oct-22

Jun-20

Jun-21

Jun-22

Feb-22

Feb-20

Feb-21

Oct-19

Oct-20

Oct-21

Oct-22

PMI Mfg PMI Ser Real GDP % YoY (LHS) 10Y IGB % (RHS)

Takeaway:

Growth while strong could suffer from global slowdown shocks

GDP: Gross Domestic Product; PMI: Purchasing Managers’ Index; GST: Goods and Service Tax; IGB: India Government Bond; Source: Bloomberg 6Comfort on currency – Optimism?

➢ RBI FX reserves stand at USD 545bn ➢ The economic environment in 2013 was similar to

• Forex adequacy ratio has ↓ significantly 2020

• Majority of the change in reserves caused by valuation • Low real rates with High Oil prices, High Current

Account Deficit & High Inflation

• Led to sharp depreciation of rupee – and rate hikes

➢ RBI FX Reserve / IMF FX adequacy ratio declined sharply

• Reserve buffer of ~USD 30 billion to reach 2013 and 2018

levels (~150% ratio) ➢ However, contrasting 2013 with current scenario

• Import cover is higher, albeit steadily declining, 8.6

months in Oct 22 vs. 7 months in 2013

➢ Yields may react adversely if RBI FX reserve reaches USD

• Global real rates are also negative, thus India is not an

500 bn outlier

700 240% Real rate vs USD/INR

600 220%

500 200% 85 6

400 180% 80 4

300 160% 75 2

200 140% 70

In %

0

100 120% 65

0 100% 60 -2

2006

2009

2012

2015

2018

2021

2002

2003

2004

2005

2007

2008

2010

2011

2013

2014

2016

2017

2019

2020

2022

55 -4

50 -6

IMF Reserve Adequacy Metric for India (LHS)

Apr-13

Apr-14

Apr-15

Apr-16

Apr-17

Apr-18

Apr-19

Apr-20

Apr-21

Apr-22

Oct-16

Oct-19

Oct-12

Oct-13

Oct-14

Oct-15

Oct-17

Oct-18

Oct-20

Oct-21

Oct-22

India Forex Reserves USD billion (LHS)

Fx Adequacy Ratio (RHS) USD INR (LHS) Real Rate (RHS)

Takeaway:

With depleting foreign exchange reserves, RBI’s ability to intervene in forex market is lower

RBI: Reserve Bank of India; IMF: International Monetary Fund; US FED: US Federal Reserve; Source: RBI, Bloomberg 7Rupee depreciation: Tail risks remain

➢ Rupee and Inflation have a strong correlation ➢ RBI has in past acted swifter to protect currency than

• There is a strong co-relation between rupee movement inflation

and CPI (barring 2018-2019) • In 2013 and 2018 RBI increased rates when rupee

depreciated

• Reaffirms that India bears risk of imported inflation • In 2018, in inflation was within RBI’s target levels

• RBI intervention visibly reduced as USD/INR touched

lows of 83 ➢ Risks of RBI intervening in rates to protect currency

increased – DXY will be important to watch

CPI (YoY %) LHS

USD INR (YoY %) RHS Repo CPI USD INR (RHS)

14% 20% 85

11 80

12% 15%

10% 9 75

10%

70

8% 7

In %

5% 65

6%

5 60

0%

4% 55

-5% 3

2% 50

0% -10% 1 45

Apr-13

Apr-14

Apr-15

Apr-16

Apr-17

Apr-18

Apr-19

Apr-20

Apr-21

Apr-22

Oct-12

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

Apr-14

Apr-16

Apr-15

Apr-17

Apr-18

Apr-19

Apr-20

Apr-21

Apr-22

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

Takeaway:

After recent currency slide, the risks of RBI influencing currency through policy rates increased

MPC – Monetary Policy Committee; CPI: Consumer Price Inflation ; Source: Bloomberg 8Overview: Major drivers of yields

Monetary Policy Fiscal Policy Global Drivers Others

Inflation Supply Global Yields RBI Regime

• CPI still above target • Supply worries abated • Why is the gap between • Is there a divergence

levels at 6.77% US and India bond yield so between MPC members?

• SDL supply muted low?

• Likely to remain clouded • Focused on curtailing

• Taxes stagnant • US CPI falling, yet high

with uncertainties inflation

• Recent focus on currency

Demand

Growth Geopolitics

• Probability of RBI OMO

• Domestic activity resilient in Q4 high • Ukraine war extension Misc.

• High trade deficit due to • Banks SLR/NDTL over

weak global demand • Prep for 2024 elections

30%

Bond Inclusion/FPI

Commodities

Currency/CAD/BOP • Binary event (CY23)

• Oil prices volatile

• Current Account Deficit • Could absorb supply &

still high support currency in FY24 • Other Commodities flat

• Capital outflows continue • Winter could lead to

higher energy prices

• Negative real rates

Takeaway:

Risks have mildly bearish bias, with sticky inflation and aggressive tightening by global central banks

Source – Internal CAD – Current Account Deficit; BoP – Balance of Payment; SLR – Statutory Liquidity Ratio; SDL – State Development Loans; NSSF: National Small 9

Saving Fund; RBI: Reserve Bank of India; G-Sec: Government Securities; CPI: Consumer Price Index; NDTL – Net Demand & Time LiabilitiesDemand-Supply: Lower SDL issuances have reduced the concern

➢ Banks SLR holdings consistently above 30% ➢ G-sec/SDL Demand supply worry subdues

• Only during the Covid and Demonetization did the levels

reach so high • According to our workings, the gap in demand supply is

reduced to ~Rs. 22 tn. for FY23

• However, during those periods' liquidity was in surplus

• Lower SDL issuances have alleviated supply concerns

➢ Banks purchases may reduce, though may not revert to

historical levels

• Total Return Swap and FRA (Forward Rate Agreement)

related bank purchases may keep SLR holdings elevated

for banks

• Yet, purchases of similar quantum as in H1FY23 by banks

seem unlikely in H2FY23 DSP Demand Supply workings (Rs tn)

Supply For FY23 Demand For FY23

Gross Borrowing 14.21 Banks 7.39

Banks SLR (in %) IGB redemption 3.13 Insurance 4.08

Net G-sec Borrowing 11.08 PFs 1.60

35

34

Gross SDL Borrowing 7.30 FPIs 0.00

33 SDL Redemption 2.2 MFs 0.70

32 Net SDL Borrowing 5.1 Corporates 0.50

31 NSSF -1.7 Total excl RBI 14.26

30

Total Supply (A+B) 14.48 Excess Supply 0.22

29

28

27

Nov-14

Nov-19

Dec-16

Dec-21

Jun-14

Jun-19

Jan-14

Apr-15

Sep-15

Feb-16

May-17

Mar-18

Aug-18

Jan-19

Apr-20

Sep-20

Feb-21

May-22

Oct-17

Oct-22

Jul-16

Jul-21

Takeaway:

Lower SDL Issuances have assuaged supply fears and reigned in bond yields

CIC – Currency In Circulation; OMO – Open Market Operations, SLR – Statutory Liquidity Ratio; G-Sec – Government Securities; SDL – State Development Loan 10

Source: Bloomberg, DBIE, Internal estimatesMoney markets too are currently driven by demand /supply

3,00,000 5,00,000

CD Supply CP Supply

2,50,000 4,00,000

2,00,000

3,00,000

1,50,000

1,00,000 2,00,000

50,000 1,00,000

0 0

Feb-21

Sep-21

May-21

Oct-21

Apr-22

Oct-22

Jan-21

Mar-21

Dec-21

Jan-22

Mar-22

Aug-22

Jun-21

Jun-22

Jul-21

Jul-22

Apr-21

May-21

Apr-22

May-22

Oct-21

Oct-22

Jan-21

Aug-21

Nov-21

Jan-22

Aug-22

Feb-21

Jul-21

Feb-22

Jul-22

Issued during fortnight Total amt O/s Issued during fortnight Total amt O/s

25.0%

Credit & Deposit Growth (Y-o-Y)

20.0%

15.0%

10.0%

5.0%

0.0%

May-21

Apr-21

Apr-22

Dec-21

May-22

Jan-21

Mar-21

Aug-21

Jan-22

Mar-22

Aug-22

Jun-21

Oct-21

Jul-21

Jun-22

Oct-22

Nov-21

Jul-22

Feb-21

Sep-21

Feb-22

Sep-22

Credit Growth Deposit Growth Investment Growth

Takeaway:

Credit growth disproportionately higher than deposit growth

Banking aggregates have started turning unfavorable

Source: RBI 11Demand-Supply: Supply Worries Abated

➢ SDL issuance picked up in Oct-22 ➢ Yields track RBI OMO purchases

• Lower SDL issuance by 33% in H1FY23 (~ ₹ 2.7tn vs ₹ 4tn • Yields have strong correlation with RBI OMO actions

calendar)

• OMO purchases lead to lower yields, vice-versa

• Lower only by 6% against calendarized in October 2022

• Demand/Supply mismatch is usually filled in by RBI

• Q3FY23 borrowing at ₹ 2.5tn

➢ Central government supply worries continue

• Govt. cut its borrowing plan by ₹ 10k crore, yet the supply

for the year is still large

• Incremental risks balanced

• Risks from fuel duty cuts, increased subsidies offset by

more than budgeted tax revenues

90,000 % G-Sec Yield (RHS) 3m rolling OMO (Purchase - Sale) LHS INR cr

SDL Supply: Indicative vs Actual

80,000 20 9.5

x 10,000 INR crore

70,000 9

15

60,000 8.5

In INR crore

10 8

50,000

7.5

40,000 5

7

30,000 0 6.5

20,000 6

-5

10,000 5.5

- -10 5

Apr-14

Apr-15

Apr-16

Apr-17

Apr-18

Apr-19

Apr-20

Apr-21

Apr-22

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

May-22

Jun-22

Apr-22

Aug-22

Sep-22

Oct-22

Jul-22

Takeaway:

Supply worries to continue in the second half

SDL – State Development Loan; NSSF – National Small Savings Fund; GST – Goods & Services Tax; Source: Bloomberg; CCIL 12Overview: Major drivers of yields

Monetary Policy Fiscal Policy Global Drivers Others

Inflation Supply Global Yields RBI Regime

• CPI still above target • Supply worries abated • Why is the gap between • Is there a divergence

levels at 6.77% US and India bond yield so between MPC members?

• SDL supply muted low?

• Likely to remain clouded • Focused on curtailing

• Taxes stagnant • US CPI falling, yet high

with uncertainties inflation

• Recent focus on currency

Demand

Growth Geopolitics

• Probability of RBI OMO

• Domestic activity resilient in Q4 high • Ukraine war extension Misc.

• High trade deficit due to • Banks SLR/NDTL over

weak global demand • Prep for 2024 elections

30%

Bond Inclusion/FPI

Commodities

Currency/CAD/BOP • Binary event (CY23)

• Oil prices volatile

• Current Account Deficit • Could absorb supply &

still high support currency in FY24 • Other Commodities flat

• Capital outflows continue • Winter could lead to

higher energy prices

• Negative real rates

Takeaway:

Risks have mildly bearish bias, with sticky inflation and aggressive tightening by global central banks

Source – Internal CAD – Current Account Deficit; BoP – Balance of Payment; SLR – Statutory Liquidity Ratio; SDL – State Development Loans; NSSF: National Small 13

Saving Fund; RBI: Reserve Bank of India; G-Sec: Government Securities; CPI: Consumer Price Index; NDTL – Net Demand & Time LiabilitiesGlobal Central Banks action & USD/INR driving yields?

➢ Why have Global Central Banks raised rates?

➢ Are rupee risks impacting Indian yields?

• High global inflation despite slowdown/potential recession

• US October CPI at 7.7% showed some signs of cooling off ➢ Rupee has weakened substantially, risks to upside

• Currently US Fed Funds “terminal rate” projected at 5.0% • Currency tail risks may materialize

➢ Are spreads of UST and IGB low? • If Fed tapering impact worsens,

• Historical spread of 10 Year US and 10 Year bonds was 5% • Trade deficit remains elevated then tail risks could

but has narrowed to 3.25% come to play

• But, bond yield spread mimics the inflation and policy rate

differential.

• RBI policy rate is low & has not tracked inflation spread ➢ Oil impact on yields taken a backseat last month

• 10Y yields seem to have priced in the inflation spread

Normalized Chart (%)

1.2 1.1

1.2

1.2 1.1

1.0

Normalized data (%)

1.1

0.8 1.1 1.1

0.6 1.0 1.1

0.4 1.0 1.0

0.9

0.2 1.0

0.9

0.0 0.8 1.0

Oct-21

Oct-07

Oct-08

Oct-09

Oct-10

Oct-11

Oct-12

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-22

Jun-22

Jun-22

Sep-22

Apr-22

Apr-22

Apr-22

May-22

May-22

Aug-22

Aug-22

Sep-22

Sep-22

Oct-22

Oct-22

Jul-22

Jul-22

Normalised Central Bank Policy rate spread

IGB10Y (RHS) Brent Crude (LHS) USD INR (RHS)

Normalised Inflation Spread

Normalised Spread (10Y IGB-10Y UST)

Takeaway:

India bond yields more driven by domestic factors than tracking global yields

IGB – Indian Govt. Bond, UST – US Treasury yields; CAD – Current Account Deficit; Source: Bloomberg, Internal Estimates 14Overview: Major drivers of yields

Monetary Policy Fiscal Policy Global Drivers Others

Inflation Supply Global Yields RBI Regime

• CPI still above target • Supply worries abated • Why is the gap between • Is there a divergence

levels at 6.77% US and India bond yield so between MPC members?

• SDL supply muted low?

• Likely to remain clouded • Focused on curtailing

• Taxes stagnant • US CPI falling, yet high

with uncertainties inflation

• Recent focus on currency

Demand

Growth Geopolitics

• Probability of RBI OMO

• Domestic activity resilient in Q4 high • Ukraine war extension Misc.

• High trade deficit due to • Banks SLR/NDTL over

weak global demand • Prep for 2024 elections

30%

Bond Inclusion/FPI

Commodities

Currency/CAD/BOP • Binary event (CY23)

• Oil prices volatile

• Current Account Deficit • Could absorb supply &

still high support currency in FY24 • Other Commodities flat

• Capital outflows continue • Winter could lead to

higher energy prices

• Negative real rates

Takeaway:

Risks have mildly bearish bias, with sticky inflation and aggressive tightening by global central banks

Source – Internal CAD – Current Account Deficit; BoP – Balance of Payment; SLR – Statutory Liquidity Ratio; SDL – State Development Loans; NSSF: National Small 15

Saving Fund; RBI: Reserve Bank of India; G-Sec: Government Securities; CPI: Consumer Price Index; NDTL – Net Demand & Time LiabilitiesRecency bias: Is 10-Year yield high?

➢ Yields had been been lower only during generational

events: 10Y IGB yield (%)

• Global Financial Crisis (2008) 9

• Demonetization (2016/17) 8.5

Only outlier

• Covid pandemic (2020/21) 8

Demonetization

7.5

Irrespective of levels of inflation, GDP, currency and demand/supply Covid

dynamics, the yields have usually been higher than the current levels – 7

unless there is an event risk. 6.5

Sell-off always end

6 above 8%

➢ Is bond inclusion the next such event?

5.5

If bond inclusion occurs, it could end up being an event that leads to

Oct-11

Oct-16

Oct-10

Oct-12

Oct-13

Oct-14

Oct-15

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

rally, despite headwinds. However, with announcement pushed to

next year near term impact unlikely.

Takeaway:

While recently yields have spiked, but past data suggests that current yield levels are not extremely high

Source – Internal, Bloomberg 16Portfolio Creation: Multi-step process

DSP Fixed Income Funds follow a defined methodology for fund portfolio construction

Fund’s Risk

Appetite

Empirical

Analysis

FINAL PORTFOLIO

Step I: Step II: Step III:

Fundamental Decide Fund Decide Duration Asset Market

Market Views Duration distribution: Allocation Risk Filter

Boundary Barbell/Bullet/Ladder

Relative value

analysis

Asset Spread

analysis

➢ We apply market risk filter which can help the Fund Managers not to take extreme risks. Thus, Value at Risk is limited by

ensuring the positions are balanced.

Investment approach / framework/ strategy mentioned herein is currently followed & same may change in future depending on market conditions & other factors. 17DSP FI Framework checklist : What is our view on yields movement?

Drivers 1Y 5Y 10Y >10Y Remarks

Monetary Policy Negative Negative Neutral Neutral

Inflation Neutral Neutral Neutral Neutral Volatile Inflation may be priced in

Growth Positive Positive Positive Positive Lower growth adds chances of lower peak rates

CAD/BOP/ CAD was at 2.8% in Q1FY23. While it will ease, but absolute still high.

Currency Negative Negative Negative Negative Import cover reducing sharply

Fiscal Policy Neutral Neutral Negative Neutral

Expenditure matched by increased taxes

Current supply will put pressure. Long bonds have demand.

Supply Neutral Negative Neutral Negative SDL supply continues to be anaemic.

RBI may conduct OMO in H2.

Banks demand should wane after large HTM purchase in H1

Demand Neutral Neutral Negative Neutral Expect higher deposit as the credit to govt and pvt. sector increases

FPI Flows Neutral Neutral Neutral Neutral No meaningful flows expected in H2 until bond index inclusion

Global Negative Negative Neutral Neutral

Global yields Negative Neutral Neutral Neutral Policy rates not in sync, but 10Y adjusted to global markets

Geopolitics Neutral Neutral Neutral Neutral Risks balanced

Commodities Neutral Neutral Neutral Neutral Risks balanced

Others Negative Neutral Neutral Neutral

RBI wary of inflation.

RBI Regime Negative Neutral Neutral Neutral Increased currency monitoring

FY24 issuances will be sizeable

Miscellaneous Neutral Neutral Neutral Neutral Unlikely RBI/Govt will be tolerant on inflation entering 2024

Mildly Mildly Mildly Mildly

Total Bearish Bearish Bearish bearish

Takeaway:

Markets should consolidate – rallies will be muted and reversed – currency risks not over.

18Step I - Duration decision: How much of yield movement is priced in?

➢ In short tenor the bearishness is priced in

India Sovereign Forward Curve*

• Upside risks are largely priced in –seen in the sharp uptick

in short tenor in forward curve

7.6

• The roll-down benefit negates the impact of yield uptick

7.4

➢ In long tenor, the bearishness is partially priced in

Yield %

7.2

• The longer tenor forward curve is pricing just 5bp-10bp

7 up-move. We believe not all bearishness is priced in.

6.8

➢ Where to invest?

6.6

1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 7 Yr 9 Yr 10 Yr 30 Yr

• Short tenor yields have moved higher, and have already

priced in further rate hikes.

Current 3 Mo Ahead 1 Yr Ahead 3 Yr Ahead • To find the best maturity to invest, one needs to take into

account higher price risk in longer duration. This is

covered in next slide.

The chart shows how much yield rise is already priced in the current

curve. Large gap between the current yield and forward yield shows

that yield rise spike is priced in – and yield uptick may not lead to

losses. Similarly small gap means that the market is not pricing

yields to rise significantly.

Maturity 1Y 5Y 10Y >10Y Remarks

Mildly Mildly Mildly Mildly

What’s expected (Total) From previous slide

Bearish Bearish Bearish bearish

Short tenor has priced in rate hikes, but longer tenor has

Is expectation (above row) priced in ? Yes Partially Partially Partially

only partially priced in expected yield rise

Source – Bloomberg; *as on 10th Nov 2022 19Step II - Duration distribution: Relative Value & Scenario Analysis

After assessing (i) what’s expected (slide #18), and (ii) what’s priced in (slide #19) , we determine relative value between the

separate maturities. This helps determine the best investment maturity after incorporating duration risks.

How do we do this?

• Calculate the expected returns based on three scenarios

‣ Our Base Case

‣ Bearish Case

‣ Bullish Case

• Thereafter calculate the expected payoff for each maturity based on

‣ Summation of expected returns for each scenario and its probability

Our preferred

Base Scenario Bullish Scenario Bearish Scenario

maturities

Probability 50% 25% 25%

Rise in yield Rise in yield Rise in yield

HPR for 3 HPR for 3

Maturity expectation in HPR for 3 month expectation in expectation in next ∑ Probability*HPR

month month

next 3 month next 3 month 3 month

1y 0.15% 6.97% -0.10% 7.68% 0.40% 6.26% 6.97%

2y 0.10% 6.75% -0.20% 8.60% 0.30% 5.53% 6.91%

3y 0.05% 6.69% -0.25% 9.49% 0.25% 4.84% 6.93%

5y 0.10% 5.59% -0.25% 11.51% 0.25% 3.08% 6.44%

10y 0.10% 4.81% -0.25% 13.70% 0.30% -0.17% 5.79%

The above table is for illustration purpose only

Source – Internal Estimates *HPR – Holding Period Returns. Returns are annualised; 20Step III – Asset Allocation: Corporate bonds vs. sovereign bonds

➢ Demand for corporate bond has been exceeding the ➢ The corporate bond spreads are low

supply keeping the spreads low • The spreads across all tenors have compressed

• The issuance has increased since low of 2020 significantly.

o The issuances so far (till Sep) in FY23 have • We expect long the spreads to remain narrow

increased to Rs. 2.50 lac cr • But with no extra yield, we have lower allocation

• Share of AAA and increased to long tenor corporate bonds.

o But with govt. on path to reduce off-balance sheet • Tighter liquidity, and high credit offtake could

borrowing, issuances may not increase mean that CD (Commercial Deposit) issuances

meaningfully from banks will remain elevated.

• The spreads in lower maturity may widen

Corporate Bond Issuances

500

6,00,000

400

5,00,000

300

Spreads in bps

4,00,000

INR Crore

3,00,000 200

2,00,000 100

1,00,000

0

-

Nov-14

Sep-15

Aug-18

Nov-19

Sep-20

Dec-16

May-17

Jan-19

Jun-19

Dec-21

May-22

Feb-21

Apr-15

Feb-16

Mar-18

Apr-20

Oct-17

Oct-22

Jul-16

Jul-21

2017-18 2018-19 2019-20 2020-21 2021-22 YTD FY23 -100

AAA AA A A1 BBB BB B C NA

1Y Spread 5Y Spread 10Y Spread

Takeaway:

In our view, corporate spreads to remain narrow in medium term – may widen in long term. Prefer limited

exposure in corporate bonds until spreads widen

Source – Bloomberg, CCIL 21Our View - Snapshot

➢ Phase 1: Rallies likely to be muted with reversals – currency risks on yields still not over

We had mentioned three reasons for yields to be under pressure in this quarter. But supply fears have eased. As the states

continue to borrow lesser, the expected fears of supply have reversed – making supply a reason for rally, rather than sell-off.

1. Rupee depreciation: While rupee has appreciated recently, but it is likely to come under pressure again. The capital

account inflows may not be sufficient to fund current account deficit.

2. Liquidity: We expect liquidity to remain tight unless the global central banks pause/ease and risks to currency evaporate.

3. Supply pressures: The lower SDL supply has eased the pressure on bonds. The supply in YTD FY23 is ~Rs. 1.5 lac cr. lesser.

This has made supply lesser than demand – leading to easing of pressure.

➢ Phase 2: Yields likely to consolidate and rally by Q4FY23

We continue to expect rally to occur in Q4FY23. The three reasons we mentioned remain:

1. RBI OMOs, as liquidity tightens RBI will have to increase the money supply and push in liquidity. Since FX asset purchase

are not looking likely, RBI will have to fill in the gap through domestic asset purchases, i.e. Government bonds.

2. Bond index inclusion chatter: By March 2023 JP Morgan will again revisit the index. Every iteration brings India’s

inclusion closer and is an inevitability sooner or later

3. Global central banks should be closer to end of rate hike cycle.

➢ Risk/Reward may favor debt investment in Q4FY23

Yields have rallied in past month. Yet, we advise to wait till Q4 to add duration. Why?

Because how much can 5-year bond rally from 7.10% when (i) overnight rates after next MPC is expected to be close to

6.25%-6.5% (ii) CPI is still high, (iii) rupee risks remain, (iv) risks to SDL supply are in Q4, and (v) election year budget is

coming?

Thus, risks seem to be lopsided towards wait-and-watch and invest in Q4FY23. Especially when the curve is flat.

Source: Internal; MPC – Monetary Policy Committee; OMO – Open Market Operations; SDL – State Development Loan; CPI – Consumer Price Index; YTD – Year To DateWhat will make us change our view

➢ What will make us increase duration earlier in Q3FY23

• In case currency remains stable, we may purchase duration earlier as the tail risks may not materialize (possible).

• If RBI announces OMO purchases earlier than expected (unlikely)

• If global recession prompts central banks to become less hawkish (possible).

• If govt announces ease in FPI process – an indicator for bond global index inclusion (unknown).

➢ What will make us delay adding duration even in Q4FY23

• In case currency fears percolate to debt markets and lead to panic (possible).

• If liquidity becomes tighter, and RBI does not show intent to ease it (likely).

• If global inflation keeps the central banks in hawkish trajectory (possible).

• If bonds global index inclusion does not occur (unknown)

Investment approach / framework/ strategy mentioned herein is currently followed & same may change in future depending on market conditions & other factors.DSP Scenario analysis and preferred Funds – No change

Fund expectation is highlighted in green background.

Positive Negative

Monetary Policy As macro data softens, RBI pauses and indicates growth

supportive measures like liquidity etc. Currency fears get realized, trade deficit high. RBI hawkish

Positive Negative Positive Negative

Supply reduced as taxes, NSSF Banks reduce SLR/NDTL ratio Supply reduced as taxes, Banks reduce SLR/NDTL ratio

increase. SDL make up for lower H1 NSSF increase. SDL make up for lower H1

Fiscal Policy

States borrow lesser than the issuances States borrow lesser than issuances

calendar Taxes unable to offset higher the calendar. Taxes unable to offset higher

RBI OMO purchases in Q4 subsidies RBI OMO purchases in Q4 subsidies

Positive Negative Negative

Positive Positive Positive

unlikely unlikely Negative

Negative

- Inflation scenario - scenario -

falls. - Inflation falls. - Inflation falls. - Inflation falls.

that global that global Global

Global - Commodity - Commodity - Commodity Global Inflation - Commodity

central banks central banks Inflation

hawkish, but Fall hawkish, but Fall remains Fall

Fall remains

MPC turns - Central banks MPC turns - Central banks elevated - Central banks

- Central elevated

banks pause dovish pause dovish pause pause

Long Tenor bond Rally Sell-off Flat Sell-off

Short Tenor bond Rally Flat Sell-off Sell-off

DSP 10Y G-Sec DSP Low

DSP Short term Fund DSP Savings Fund

Fund Duration Fund

DSP Nifty SDL

Plus G-Sec Jun DSP Short Term DSP Nifty SDL Plus G-Sec Jun 2028

Recommended DSP Low Duration Fund

2028 30:70 Index Fund 30:70 Index Fund

funds Fund

DSP Strategic DSP Strategic

DSP Strategic Bond Fund DSP Ultra-Short Fund

Bond Fund DSP Bond Fund

DSP Savings

DSP Bond Fund DSP Government Securities Fund DSP Strategic Bond Fund

Fund

Source – Internal NDTL- Net Demand and Time Liabilities; FPI – Foreign Portfolio Investment; SLR – Statutory Liquidity Ratio; SDL – State Development 24

Loans; NSSF: National Small Saving Fund; RBI: Reserve Bank of India; G-Sec: Government SecuritiesDSP Fixed Income Universe

25DSP Fixed Income Fund Universe (Active Funds)

7.70%

7.60%

DSP Credit Risk Fund

7.50%

7.40%

7.30% DSP Bond Fund

YTM (%)

DSP Short Term Fund

7.20%

DSP Banking & PSU Debt Fund

7.10%

DSP Low Duration Fund

7.00%

6.90% DSP Strategic Bond Fund

DSP Floater Fund

6.80%

DSP Government Securities Fund

6.70%

0.00 0.50 1.00 1.50 2.00 2.50 3.00 3.50 4.00 4.50 5.00 5.50 6.00 6.50 7.00

Mac. Duration

as on 31st October 2022;

the horizontal bars represent the duration range that we intend to keep. The ranges are wide currently as we want to prepare for binary decision of bond inclusion

the horizontal lines are regulatory / Fund’s operative duration boundary

• The dots is Macaulay Duration of funds as of 31st October 2022

Investment approach / framework/ strategy mentioned herein is currently followed & same may change in future depending on market conditions & other factors. 26DSP Bond Fund Duration: 3.13 years

7.60%

• The Fund is a medium-term fund which has a 7.50%

Macaulay duration of between 3 to 4 years.

• It is meant for medium-term investors who 7.40%

want to take interest rate risk associated with

longer-term papers, but not take significant

credit risks. 7.30%

YTM (%)

YTM: 7.28%

• The fund manager intends to invest in bonds

by analyzing value in various points in the 7.20%

yield curve and credit spreads.

• The fund will have a mix of GSEC, SDLs and 7.10%

highly rated corporate bonds, and generally

will not invest in papers beyond 10 years.

• Basis current market view, the fund has a 7.00%

duration of ~ 3.2 years, and intends to run in

a Macaulay duration boundary between 3.1y-

6.90%

3.6y in current market conditions.

2.5 3 3.5 4 4.5

Macaulay Duration (years)

Strategy boundary Regulatory boundary

3.1 – 3.6 years 3 – 4 years

Source: Internal; Data as on 31/Oct/22DSP Short Term Fund Duration: 1.63 years

7.50%

• The Fund has a regulatory duration boundary 7.40%

of 1y – 3y

• The fund is meant for investors who do not 7.30%

want extreme risks. The fund’s duration

boundary ensures that the duration risk is YTM: 7.25%

curtailed. 7.20%

YTM (%)

• For now, the fund intends to maintain

duration between 1.5y – 2.25y. The fund may 7.10%

duration as yields rise, as yields peak.

• The fund intends to optimizes returns by

playing between corporate and G-sec spreads 7.00%

and take strategic and tactical duration calls

• Currently the fund has no investment in 6.90%

lower than AAA rated assets. The fund can invest

up to 20% in AA+ rated assets

6.80%

• The fund usually avoids investing in more 0.5 1 1.5 2 2.5 3 3.5

than 5-yr maturity papers – unless few days Macaulay Duration (years)

tactical play.

Strategy boundary Regulatory boundary

1.5 – 2. 25 years 1 – 3 years

Source: Internal; Data as on 31/Oct/22DSP Low Duration Fund

Duration: 0.54 years

7.30%

7.20%

• The Fund operates in a duration range of 6-

12 months

7.10%

• It is meant for investors, who want to intend

to earn higher returns, yet not expose YTM: 7.09%

themselves to significant interest rate risks. 7.00%

• The fund intends to maintain duration

YTM (%)

between 0.5y-0.85y currently, and may increase 6.90%

duration as fund manager gets comfort on

pause in RBI actions and ease in supply 6.80%

pressures from bank CDs.

• The fund intends to invest in a mix of CPs, 6.70%

CDs, AAA Corporate Bonds and sovereign

securities.

6.60%

• The fund intends to avoid any papers beyond

5-year maturity.

6.50%

0.25 0.75 1.25

Macaulay Duration (years)

Strategy boundary Regulatory boundary

0.50 – 0.85 years 0.50 – 1 years

Source: Internal; Data as on 31/Oct/22DSP Strategic Bond Fund

Duration: 0.70 years

7.20%

• The fund is driven by the principle of running

7.15%

a strategic boundary based on medium term

view.

7.10%

• The fund is meant for investors who want to

leverage the interest rate cycles and are willing to 7.05%

be patient.

7.00%

• The DSP Strategic Bond Fund sharply cut the

YTM (%)

duration as bond index inclusion is delayed. 6.95%

• Based upon the above philosophy, the

Strategic bond fund is running lower duration as 6.90%

currency and supply issues remain. YTM: 6.88%

6.85%

• Given the current rates volatility, the fund

could operate in a wider duration range of 0.5y- 6.80%

4.5y.

• The fund intends to add duration by end of 6.75%

H2FY23 as we expect yields to peak by then.

6.70%

• The current duration will most probably 0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7

increase every month, such that by end of FY23 Macaulay Duration (years)

the fund is at a duration greater than 4Y.

Strategy boundary Regulatory boundary

0.5 – 4.5 years No boundary

Source: Internal; Data as on 31/Oct/22DSP Banking & PSU

Debt Fund Duration: 1.50 years

7.60%

7.50%

• The fund is suitable for investors willing to

leverage duration and the term premium. 7.40%

• Regarding the duration movement, the fund

can be thought of as mix of the Short-Term Fund 7.30%

and Bond Fund. In times of rising rates, the fund

YTM (%)

moves to duration of Short-Term Fund, else 7.20%

towards Bond Fund.

• The fund will currently run duration between 7.10%

YTM: 7.13%

1y and 2y.

• The fund will add duration probably in next 6 7.00%

months as we expect yields to peak in H2FY23.

• The fund is actively managed with duration 6.90%

calls as it has no regulatory duration boundary.

Yet, the fund maintains its duration between the

strategy duration of 1-2 Y. 6.80%

0.5 1 1.5 2 2.5 3 3.5 4

• The fund intends to invests in AAA Banking & Macaulay Duration (years)

PSU bonds (minimum 70%) as well as sovereign

bonds (maximum 30%).

Strategy boundary Regulatory boundary

1 - 2 years No boundary

Source: Internal; Data as on 31/Oct/22DSP Government

Securities Fund Duration: 1.61 years

7.50%

7.30%

• The fund is meant for investors who want to

leverage the changing market dynamics and want

7.10%

the fund manager to tide through the changing

yields

6.90%

YTM (%)

• The DSP Government Securities Fund is

running a duration of 1.5 - 4 years. YTM: 6.75%

6.70%

• The fund, while maintaining the strategic

limits, is more reactive to tactical moves and can

6.50%

continue to actively manage duration as market

dynamics change.

6.30%

• The fund only invests in Government

Securities, State Development Loans and T-bills. 6.10%

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

Macaulay Duration (years)

Strategy boundary Regulatory boundary

1.5 – 4 years No boundary

Source: Internal; Data as on 31/Oct/22DSP Credit Risk Fund Duration: 1.58 years

• The fund’s duration ranges between 1 - 3 8.10%

years and aims at capture steady accrual with

better risk adjusted returns

7.90%

• The Credit Risk Fund has a stipulated

minimum percentage of investments in AA and

below rated corporate bonds (of 65%, but could 7.70%

be lower depending on liquidity calculations).

YTM: 7.60%

• The fund is meant for investors who are

YTM (%)

7.50%

comfortable in assuming credit risk in line with

the scheme profile. This includes, besides credit

risk, liquidity risk (impact costs) and spread risk 7.30%

(widening of credit spreads).

• The fund endeavours to invest in Companies 7.10%

with reputed Indian groups so that there is

sufficient liquidity for the portfolio.

6.90%

• Governance of the underlying

Companies/Parent groups will be given

importance. 6.70%

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

Macaulay Duration (years)

Strategy boundary Regulatory boundary

1.0 – 2.5 years No boundary

Source: Internal; Data as on 31/Oct/22DSP Floater Fund Duration: 0.85 years

7.30%

7.20%

• The DSP floater fund is running a duration of

0.9 yrs.

7.10%

• Currently, the floater fund is running 7.00%

diversified strategy (i) 2024 FRB (Floating Rate

Bond), (ii) 1 Yr T-bill, and (iii) Long 3Yr bond vs 6.90%

YTM (%)

Short 18m OIS.

YTM: 6.85%

6.80%

• While the fund intends to exit the Bond-OIS

6.70%

strategy in some time by executing 3Y Bond vs

short tenor OIS (Overnight Index Swap)

6.60%

• The fund is for investors who want to have a 6.50%

hedge during rising rates.

6.40%

0 0.5 1 1.5 2 2.5

Macaulay Duration (years)

Strategy boundary Regulatory boundary

0.6 – 1.5 years No boundary

Source: Internal; Data as on 31/Oct/22DSP Money Market Funds

➢ Current drivers of money market rates:

Rates are currently driven by two additional factors, apart from the RBI rate hikes

1. Core liquidity has tightened due to reduction of RBI’s FX assets and seasonal increase in currency in circulation.

2. Credit offtake has picked up (17.9% YoY). The banks have had to manage their liabilities through the open market. This has led

to a spate of CD issuances from PSU and Private banks in recent months.

Further, temporary shortages of liquidity due to tax outflows cause overnight rates to swing towards MSF rate from time to time.

2. Our positioning:

With core liquidity reducing in recent weeks, even temporary build-up in government cash balances has started impacting money

market rates, by squeezing out overnight liquidity. All in all, reducing banking liquidity, increased CD supply and further actions by

the MPC in the coming policies will likely drive money market rates higher. In this environment, a staggered investment pattern on

the money market curve should balance out risk of higher volatility with reinvestment risk.

DSP Ultra Short Fund DSP Liquidity Fund DSP Overnight Fund

• The Fund operates in a duration • The Fund operates in a average • Fund invests primarily in

range of 3-6 months. maturity range of up to 91 days. overnight instruments.

• It is meant for investors, who want • It is meant for investors, who • Currently, the overnight

to benefit over liquid category over a would like to park cash for a short instruments consist solely of repos

short-term period (2-3 months). time (7 days – 2 months). backed by sovereign securities.

• The fund intends to have a mix of • The fund invests in a mix of CPs, • Fund also invests up to 5% in

CPs, CDs, Corporate Bonds and sovereign CDs, Corporate bonds and sovereign sovereign securities up to 30 days

securities. securities with maximum maturity of maturity as permitted by SEBI for

• With persistence in liquidity 91 days. placing as margin.

tightness in Oct’22, the fund tempered • The fund could invest in a • The fund has never invested in

its duration to ~0.37 years, with staggered manner maintaining a corporate bond/debt repos or

staggered allocations across parts of the lower maturity profile, which can CPs/CDs of 1-day residual maturity,

money market curve. benefit from the current rising rate ensuring that the entire exposure is

environment. sovereign in nature.

CRR – Cash Reserve Ratio; FX – Foreign Exchange; CD – Commercial Deposits; CP – Commercial Papers; MPC: Monetary Policy Committee; Source: Internal; Data as on 30/Oct/22

MSF: Marginal Standing FacilityDSP Fixed Income Fund Universe (Passive / Roll Down)

7.60%

DSP Nifty SDL Plus G-Sec Jun 2028 30:70 Index Fund – 2028 Target Maturity Roll-down

DSP Corporate Bond Fund – 2027 Roll-down

7.50%

DSP 10Y G-Sec Fund – 10Y Constant Maturity

7.40%

7.30%

7.20%

DSP Savings Fund – Annual March Roll-down

7.10%

7.00%

0.00 1.00 2.00 3.00 4.00 5.00 6.00 7.00

*as on 31st October 2022; the horizontal bars represent the duration range

Investment approach / framework/ strategy mentioned herein is currently followed & same may change in future depending on market conditions & other factors. 36DSP Corporate Bond Fund Duration: 3.57 years

YTM: 7.54%*

Performance of various strategies

5 Year Gsec 3Y Roll Down

• The fund is currently following a 2027 14.00%

corporate roll down strategy i.e., it is largely 1Y to 5Y Ladder 3Y Constant Maturity

invested in papers having a maturity mid 2026- 10.50%

mid 2027 . 12.00%

• Fresh inflows and coupon investment will 9.50%

likely be invested in 2026-27 bonds. 10.00%

• The fund invests largely invests in AAA

8.50%

corporate bonds (which will be ~2/3rds of the

5y G-Sec (%)

8.00%

YTM (%)

portfolio) and sovereign bonds.

• The fund has a duration of ~3.57 yrs. and will 6.00%

7.50%

gradually reduce close to zero as we come closer

to maturity of the bonds (2026-27).

6.50%

4.00%

• The Fund’s relative performance will be

impacted by credit spreads movement, but the

fund manager will broadly aim to keep the 2.00% 5.50%

portfolio on a held to maturity basis, thereby

improving the predictability towards the roll

down date. 0.00% 4.50%

Oct-12

Oct-09

Oct-10

Oct-11

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

The fund can do much better if the peak rates are achieved and markets

may rally soon – followed by period of range trading.

*Yields are annualized yields

Source: Internal; Data as on 31/Oct/22DSP Savings Fund Duration: 0.31 years

YTM: 7.11%*

• The fund strategy is to operates as a one Year Performance of various strategies

roll-down.

5 Year Gsec 3Y Roll Down

• The fund buys one year money market 12.00%

instruments in Feb/Mar of each year. 1Y to 5Y Ladder 1 Year roll down 10.50%

• Additional flows received during the year are 10.00%

deployed in the same maturity. 9.50%

• The fund’s average maturity progressively

reduces during the year. Thus the boundary of 8.00%

the funds duration is 1 yr. (at inception of new 8.50%

5y G-Sec (%)

rolldown), to less than 1 month(a end of the

YTM (%)

rolldown). 6.00%

7.50%

• The fund invests in a mix of CPs, CDs carrying

rating of A1+ and sovereign securities.

4.00%

6.50%

• The fund has an average maturity of 0.40

years, with an allocation of 48% to CDs, 31% to

CPs & 17% to sovereign securities 2.00% 5.50%

0.00% 4.50%

Oct-12

Oct-09

Oct-10

Oct-11

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

The Savings fund strategy typically performs well if the rates remain stagnant

or rise and gives lesser return in falling rates. It’s NAV volatility is less due to

low duration.

*Yields are annualized yields

Source: Internal; Data as on 31/Oct/22DSP Nifty SDL Plus G-Sec

Jun 2028 30:70 Index Duration: 4.22 years

Fund YTM: 7.57%*

Performance of various strategies

5 Year Gsec 3Y Roll Down

14.00%

1Y to 5Y Ladder 3Y Constant Maturity

10.50%

12.00%

• The fund is a 2028 target maturity fund. The 9.50%

fund invests in papers having a maturity up to 10.00%

June 2028.

8.50%

• The Fund invests 70% in Government

5y G-Sec (%)

8.00%

securities and 30% in State development loans.

YTM (%)

The Fund follows the prescribed Nifty SDL Plus G- 7.50%

sec June 2028 30:70 Index 6.00%

• The investment is done as per the index i.e.

in states that have better fiscal metrics i.e., 6.50%

4.00%

outstanding liabilities / total state GDP.

2.00% 5.50%

0.00% 4.50%

Oct-12

Oct-09

Oct-10

Oct-11

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

The roll down funds do much better if the peak rates are achieved and

markets may rally soon – followed by period of range trading.

*Yields annualized yields

Source: Internal; Data as on 31/Oct/22DSP 10Y G-sec Fund Duration: 6.82 years

YTM: 7.48%*

Performance of various strategies

5 Year Gsec 3Y Roll Down

14.00%

1Y to 5Y Ladder 3Y Constant Maturity

10.50%

12.00%

9.50%

• The 10Y G-sec fund invests in 10Y 10.00%

government bond

8.50%

• The fund runs a duration similar to 10 year

5y G-Sec (%)

8.00%

YTM (%)

benchmark Government Security

7.50%

• Currently the fund has a duration of 6.82 6.00%

years.

6.50%

4.00%

2.00% 5.50%

0.00% 4.50%

Oct-12

Oct-09

Oct-10

Oct-11

Oct-13

Oct-14

Oct-15

Oct-16

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

Oct-22

The constant maturity typically performs well when rates are nearing

their peak, or when yields stagnate. They usually have more NAV

volatility.

Source: Internal; Data as on 31/Oct/22 *Yields are annualized yieldsKey Risks associated with investing in Fixed Income Schemes

Interest Rate Risk - When interest rates rise, bond prices fall, meaning the bonds you hold lose value. Interest rate

movements are the major cause of price volatility in bond markets.

Credit risk - If you invest in corporate bonds, you take on credit risk in addition to interest rate risk. Credit risk is the

possibility that an issuer could default on its debt obligation. If this happens, the investor may not receive the full value of

their principal investment.

Market Liquidity risk - Liquidity risk is the chance that an investor might want to sell a fixed income asset, but they’re

unable to find a buyer.

Re-investment Risk: If the bonds are callable, the bond issuer reserves the right to “call” the bond before maturity and pay

off the debt. That can lead to reinvestment risk especially in a falling interest rate scenario.

Rating Migration Risk - If the credit rating agencies lower their ratings on a bond, the price of those bonds will fall.

Other Risks

Risk associated with

• floating rate securities

• derivatives

• transaction in units through stock exchange Mechanism

• investments in Securitized Assets

• Overseas Investments

• Real Estate Investment Trust (REIT) and Infrastructure Investment Trust (InvIT)

• investments in repo of corporate debt securities

• Imperfect Hedging using Interest Rate Futures

• investments in Perpetual Debt Instrument (PDI)

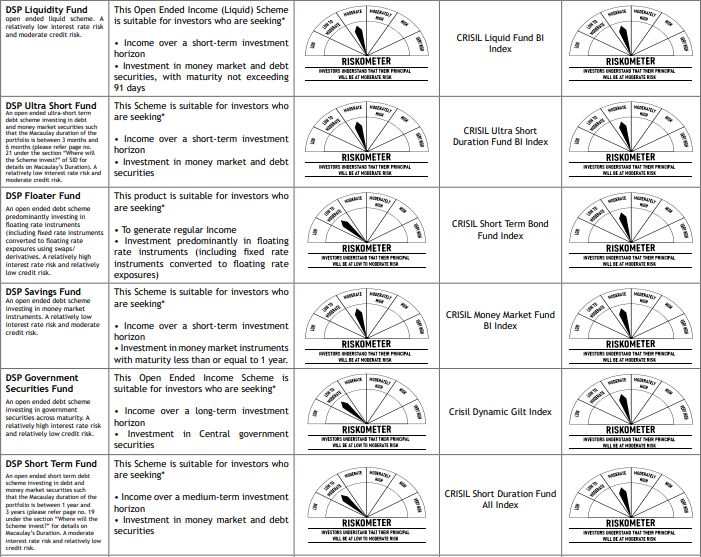

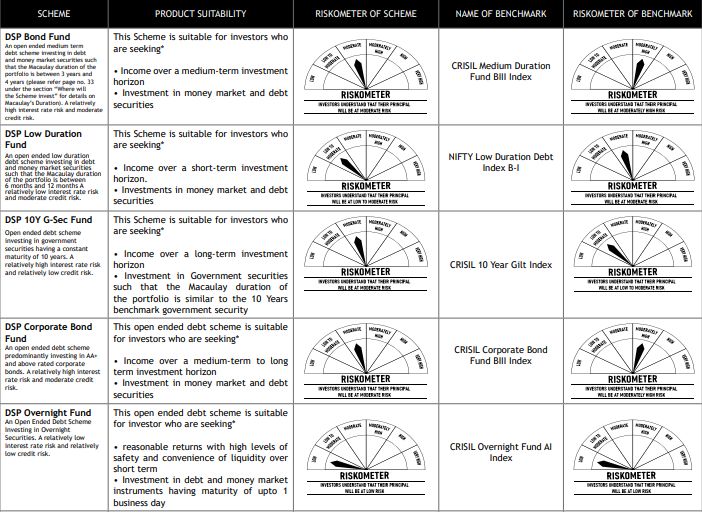

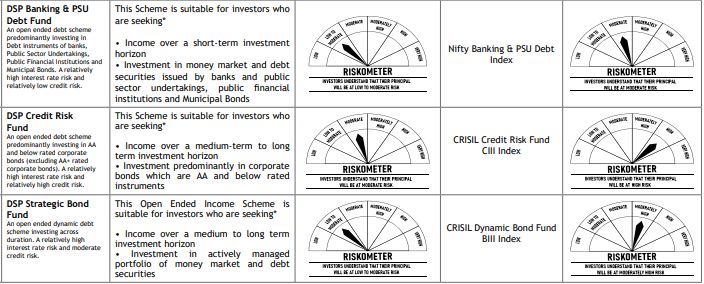

41Product Labelling

42Product Labelling

43Product Labelling

*Investors should consult their financial advisers if in doubt about whether the Scheme is suitable for them. 44Potential Risk Class Matrix For Debt Scheme(s) Of The Fund

45Potential Risk Class Matrix For Debt Scheme(s) Of The Fund

46Disclaimer & Product Labelling

In this material DSP Investment Managers Private Limited (the AMC) has used information that is publicly available, including information developed in-house.

Information gathered and used in this material is believed to be from reliable sources. The AMC however does not warrant the accuracy, reasonableness and / or

completeness of any information. The data/statistics are given to explain general market trends in the securities market, it should not be construed as any research

report/research recommendation. We have included statements / opinions / recommendations in this document, which contain words, or phrases such as “will”,

“expect”, “should”, “believe” and similar expressions or variations of such expressions that are “forward looking statements”. Actual results may differ materially from

those suggested by the forward looking statements due to risk or uncertainties associated with our expectations with respect to, but not limited to, exposure to market

risks, general economic and political conditions in India and other countries globally, which have an impact on our services and / or investments, the monetary and

interest policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices etc. The

stock(s)/issuer(s) mentioned in this presentation do not constitute any research report/recommendation of the same and schemes of the Fund may or may

not have any future position in these stock(s)/issuer(s). The portfolio of the schemes is subject to changes within the provisions of the Scheme Information

document of the schemes. There is no assurance of any returns/potential/capital protection/capital guarantee to the investors in schemes of the DSP Mutual

Fund. Past performance may or may not sustain in future and should not be used as a basis for comparison with other investments. This document indicates

the investment strategy/approach/framework currently followed by the schemes and the same may change in future depending on market conditions and

other factors. All figures and other data given in this document are as on October 31, 2022 and the same may or may not be relevant in future and the same should not

be considered as solicitation/ recommendation/guarantee of future investments by the AMC or its affiliates. Investors are advised to consult their own legal, tax and

financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to the units of schemes of DSP Mutual Fund. For

complete details on investment objective, investment strategy, asset allocation, scheme specific risk factors please refer the scheme information document and key

information memorandum of the schemes, which are available at AMC and registrar offices and investor service centres/AMC website- www.dspim.com For Index

Disclaimer click Here

“Mutual Fund investments are subject to market risks, read all scheme related documents carefully”.

47#INVESTFORGOOD

You can also read