Concept Benchmark Report for Domestic System - Restaurant Research

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Hardee's 2021/2022

Concept Benchmark Report for Domestic System

Executive Summary

Hardee's brand attributes as a regional chain with a Southeast & Midwest orientation include: made-from-scratch

breakfast biscuits; made-to-order charbroiled burgers (with over-sized patties & Black Angus options); hand-breaded

chicken sandwiches & tenders; charbroiled chicken line; hand-scooped ice cream shakes; and table service. Hardee's is

unique in that its high-margin breakfast business generates a material sales mix and efforts to extend breakfast hours to

2PM should increase brand appeal. The chain's comps turned positive/break-even in 2020 after 4 consecutive years of

declines as the system benefits from a significant increase in drive-thru demand post-covid. Building on this momentum,

YTD comps through the first 3 quarters of 2021 were positive mid-single-digits as the brand's menu and marketing

improvements gain traction while the brand continues to benefit from its QSR DT format and a return of breakfast. Also,

a significant innovation ramp-up beginning in 2020 helps increase trial/brand reach while efforts to compensate for a

relatively small scale/share of voice include an increased marketing allocation towards cost effective digital-first and

social-friendly content which targets a younger demo. Notably, the chain's historical sales pressure reflected: a struggle

around a premium lunch/dinner positioning at a time when QSR competitors had been emphasizing value; relatively slow

digital progress; a lack of a consistent, effective marketing message around its very important breakfast daypart; and

past efforts to migrate guests to higher priced LTOs. Hardee's is reluctant to compete with the larger, national players

around value/discounting as the brand lacks sufficient share of voice to promote both quality and value sufficiently to

overcome trade-down. Also, while co-branding with sister brand Carl's Jr. (West Coast orientation) helps provide

national scale, the demos for these 2 brands are notably different and Hardee's large breakfast mix (vs. Carl's)

represents a co-marketing challenge. Significant AUV underperformance, high labor costs (reflecting operational

complexities) and elevated ad spend (to compensate for relatively small scale) translates into EBITDAR margin under-

performance. In conclusion, while Hardee's is beginning to improve relevancy around its menu and marketing, the need

to strengthen its value positioning may still be required to drive the top and bottom lines.

Strengths

• Regional chain (Southeast & Midwest) with brand attributes that include: made-from-scratch breakfast biscuits; made-

to-order charbroiled burgers (with over-sized patties & Black Angus options); hand-breaded chicken sandwiches &

tenders; charbroiled chicken line; hand-scooped ice cream shakes; and table service.

• Unique high-margin breakfast business represents a 48% mix (higher in the Southeast & lower in the Midwest). While

breakfast historically has been offered only until 11AM (reflecting the operational challenge of preparing made-from-

scratch biscuits while simultaneously preparing lunch/dinner options), some stores have extended this until 2PM.

• Comps turned positive/break-even in 2020 after 4 consecutive years of declines as the system benefits from a

significant increase in drive-thru demand post-covid. Building on this momentum, YTD comps through the first 3 quarters

of 2021 were positive mid-single-digits as the brand's menu and marketing improvements gain traction.

• Current positioning benefits from its QSR DT format, a return of breakfast and improving relevancy around its menu &

marketing.

• Significant innovation ramp-up beginning in 2020 helps increase trial/brand reach.

• Efforts to compensate for relatively small scale/share of voice include an increased marketing allocation towards cost

effective digital-first and social-friendly content which targets a younger demo.

• Ad spend has pivoted from primarily local towards a split with national spend in an effort to balance brand consideration

(local) and brand awareness (national).

• National value LTOs features its 2$, $3 More breakfast menu platform which facilitates new news.

• Strong COGs out-performance reflects the chain's profitable breakfast mix and aversion to discounting & low price-

points.

• Parent company, Roark Capital Group, provides scale with regard to digital & tech investments, data mining and

analytical capabilities in addition to other cost synergies.

Challenges

• Relatively small scale as 11th largest player in the QSR sandwich category with just a 1.7%2021/2022

Hardee's share of segment sales

among the $1B+ chains.

• Historical sales pressure reflected: a struggle around a premium lunch/dinner positioning at a time when QSR

competitors had been emphasizing value; relatively slow digital progress; a lack of a consistent, effective marketing

message around its very important breakfast daypart; and past efforts to migrate guests to higher priced LTOs.

• Hardee's is reluctant to compete with the larger, national players around value/discounting as the brand lacks sufficient

share of voice to promote both quality and value sufficiently to overcome trade-down.

• While co-branding with sister brand Carl's Jr. (West Coast orientation) helps provide national scale, the demos for

these 2 brands are notably different. Also, Hardee's large breakfast mix (vs. Carl's) represents a co-marketing challenge.

• Operational complexity is increased by: made-from-scratch breakfast biscuits; made-to-order burgers (with different

patty varieties); hand-breading of chicken products; and hand-scooped ice cream. In any case, Hardee's drive-thru

speed is above average according to a 3rd party survey.

• Relatively slow progress around digital/loyalty although new digital order platform rolled-out in 2021.

• Post-lockdown sales are not as robust as other QSR drive-thru concepts because of the brand's exceptionally high

breakfast mix.

• Significant AUV underperformance, high labor costs (reflecting operational complexities) and elevated ad spend (to

compensate for relatively small scale) translates into EBITDAR margin underperformance.

• Modest pace for new remodeling initiative.

• Annual closure rates have exceeded the segment average as the weakest stores in this 60 year-old system continue to

be culled.

• While net units declined for the last 3 years, new CDO should help drive going forward development.

Parent Company Summary

Corp. Debt Net Debt/ EV/ Stock Performance

Parent Company Ticker

Rating EBITDA EBITDA 2020 TTM Sep-21

CKE Restaurants Holdings, Inc. Private Not Rated N/a N/a N/a N/a

$1B+ Chains 6.88 27.97 11.5% 36.3%

Table of Contents Page Page Page

RR Dashboard 3 Sales & Market Share 12Remodeling 19

System Statistics 4 Unit Economics 13 - 14

Franchise Summary 20

Marketing 5 - 6 New Build Costs 15Menu Exhibit 21

Menu 7 - 8 New Build vs. Buy Analysis 16State Unit Map 22

New Products & Promotions 9 Development 17State Unit Detail 23

Operations 10 Closings 18Photos 24

Tech & Equipment 11 RR Overview 25

Please refer to page 25 for Disclosures & Disclaimer of Liability. Copyright 2021 Restaurant Research® LLC.

Home

Hardee's Sandwich

RR Dashboard - Domestic System

Segment Segment

Chain Chain

Avg./Total Avg./Total

System Scale Store Level Labor Structure

System Sales ($'000) $2,000,000 $115,361,000 Total Hourly/Crew Employees 25 - 28 15 - 80

Market Share by Sales 1.7% Average Employees @ Peak Shift 9 - 11 6 - 20

System Units 1,759 57,471

Market Share by Units 3.1% Unit Economics FYE 2021P FYE '20E

Average Unit Volume "AUV" $1,180,000 $1,665,643

Growth COGs 27.3% 28.5%

System Sales 2 Yr. Avg. -2.4% 4.6% Labor 31.2% 28.9%

System Sales 10 Yr. Avg. 1.4% 4.0% EBITDAR (Pre G&A) 19.3% 21.9%

Gross New Units 2 Yr. Avg. 1.5% 1.7% Unit Level M&A Multiple 4.73 5.33

Gross New Units 10 Yr. Avg. 2.2% 2.0%

Unit Transfers

Same-Store-Sales (Systemwide Calendar Year) 2 Yr. Avg. (2019-2020) 1.2% 4.0%

2 Yr. Avg. -1.7% 3.7% 10 Yr. Avg. (2011-2020) 4.0% 4.5%

10 Yr. Avg. 0.7% 2.7%

RR SSS Index (Base Yr. 2011) 102.4 134.4 New Build Economics

New Build AUV $1,300,000 $1,571,786

Unit Closures New Build Costs (Ex. Land) $1,714,694 $1,489,918

2 Yr. Avg. 3.9% 1.7% Building Size (Sq. Ft.) 2,500 2,634

10 Yr. Avg. 1.8% 1.4% Sales-to-Investment Ratio 0.76 1.05

Sales/Sq. Ft. $520.0 $596.8

Marketing Investment/Sq. Ft. $685.9 $565.7

Gross Local Contribution 1.25% 0.8% New Build Cost/Acquisition Cost 4.14

Gross National Contribution 4.25% 2.8% Unlevered New Build ROI 9.6% 15.2%

Total Media Ad Spend ($ MM) $97 $2,953

Segment Market Share 3.3% System Condition

% of System New &/or Remodeled 28.4% 53.2%

Menu, Marketing & Promotions % of System Built in Last 7 Years 18.4% 19.4%

Menu Size 59 61

# New Products 2019 18 9 Franchise Summary

# New Products YTD 2020 13 5 Total # Franchised Units 1,561 52,438

Average check $7.50 $9.65 % of System Franchised 88.7% 91.2%

Total Franchisees 74 8,373

Daypart sales Avg. # Units/Franchisee 21.1 6.3

Breakfast 43% 13% Initial & Development Fees (Net) $35,000 $46,071

Lunch 34% 38% Royalty Fee 4.0% 4.5%

Dinner 12% 27% Minimum Net Worth Requirement $1,000,000 $2,522,727

Afternoon & Late Night 10% 22%

Franchisor Condition

S&P Debt Rating Not Rated

Stock Performance LTM N/a 36.3%

Leverage (Net Debt/EBITDA) N/a 6.88

Above Average Below Average

Source: RR Estimates for Domestic System Page 3 Report Not Licensed for Distribution

Home

Hardee's

(*)

Domestic System Statistics

2021 10 yr. Average

FYE January 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Outlook ('11-'20)

Systemwide Sales ($'000)

Systemwide Sales $1,818,800 $1,897,000 $1,957,000 $2,083,000 $2,165,000 $2,241,000 $2,166,000 $2,100,000 $2,037,000 $2,000,000

% Growth 3.9% 4.3% 3.2% 6.4% 3.9% 3.5% -3.3% -3.0% -3.0% -1.8% 1.4%

Segment % Growth 3.8% 4.7% 2.0% 3.3% 5.6% 3.7% 3.5% 3.7% 6.1% 3.2% 4.0%

Segment Market Share 2.2% 2.2% 2.3% 2.3% 2.3% 2.3% 2.1% 2.0% 1.8% 1.7%

Market Share Change 0.0% 0.0% 0.0% 0.1% 0.0% 0.0% -0.2% -0.1% -0.2% -0.1% 0.0%

Same Store Sales

Franchised 4.0% 3.9% 2.8% 4.6% 1.4% -0.6% -4.2% -0.5% N/a 0.8% N/a 1.4%

Company 5.2% 2.3% 1.7% 2.8% 2.2% 0.8% -6.5% -5.1% N/a -4.0% N/a -0.1%

Total System 4.3% 3.5% 2.5% 4.2% 1.5% -0.5% -4.3% -0.8% -3.8% 0.4% N/a 0.7%

Segment SSS 2.5% 3.9% 1.0% 1.5% 3.7% 2.2% 2.5% 2.7% 5.0% 2.4% 2.7%

Unit Counts

Franchised 1,226 1,233 1,264 1,363 1,687 1,733 1,745 1,727 1,630 1,561

Company 469 470 457 403 118 115 119 119 174 198

Total 1,695 1,703 1,721 1,766 1,805 1,848 1,864 1,846 1,804 1,759

% Net Growth 0.2% 0.5% 1.1% 2.6% 2.2% 2.4% 0.9% -1.0% -2.3% -2.5% 0.4%

Segment % Net Growth 0.5% 0.4% 0.6% 0.9% 0.7% 1.1% 0.9% 0.6% 0.5% -0.4% 0.6%

Gross New Unit Development

Franchised 16 20 32 49 53 66 51 35 40 14 24

Company 2 1 2 7 5 1 1 1 0 0 0

Total 18 21 34 56 58 67 52 36 40 14 24

% Growth 1.1% 1.2% 2.0% 3.3% 3.3% 3.7% 2.8% 1.9% 2.2% 0.8% 1.3% 2.2%

Segment % Growth 1.8% 1.8% 1.9% 2.2% 2.1% 2.3% 2.4% 2.0% 2.0% 1.5% 2.2% 2.0%

Transfers & Closure Rates

Franchised Transfers 0.2% 6.2% 8.4% 8.6% 3.4% 6.2% 1.4% 3.4% 1.6% 0.9% 4.0%

Segment Transfers 2.8% 4.4% 3.8% 4.8% 4.8% 5.8% 5.2% 5.7% 4.2% 3.8% 4.5%

Franchised Closings 1.1% 1.0% 0.9% 0.7% 1.4% 1.2% 2.1% 3.0% 4.2% 3.4% 1.9%

Company Closings 0.4% 0.2% 1.1% 0.4% 0.0% 3.4% 0.0% 0.8% 7.6% 1.7% 1.6%

System Closings 0.9% 0.8% 0.9% 0.6% 1.1% 1.3% 1.9% 2.9% 4.4% 3.3% 1.8%

Segment Closings 1.3% 1.4% 1.3% 1.3% 1.4% 1.2% 1.4% 1.4% 1.5% 1.9% 1.4%

(*) Concept results reflect company's fiscal year. Segment results reflect an average of individual concept results based on their fiscal year end closest to December.

Source: RR Estimates for Domestic System Page 4 Report Not Licensed for Distribution

Home

Hardee's

Target Market

• Regional chain has a Southeast & Midwest orientation.

• Hardee's targets 25 – 54 year olds for breakfast with seniors representing an important sit-down constituency.

• 18 – 54 year olds targeted for lunch & dinner.

• Women are targeted with chicken sandwiches and kids with its Star Pals menu (chicken tenders, small burgers or hot dog).

Marketing Strategy

• Brand attributes include: made-from-scratch breakfast biscuits; made-to-order charbroiled burgers (with over-sized patties & Black Angus options); hand-breaded chicken

sandwiches & tenders; charbroiled chicken line; hand-scooped ice cream shakes; and table service.

• While co-branding with sister brand Carl's Jr. (West Coast orientation) helps provide national scale, the demos for these 2 brands are notably different. Also, Hardee's large

breakfast mix (vs. Carl's) represents a co-marketing challenge.

• CKE's logo-turned-mascot (Happy the Star) is used to promote the products & LTOs of both brands and animated "Feed Your Happy" & "Wake Up Your Happy" (breakfast) tag

lines urge everyone to satisfy their cravings with indulgent burgers & biscuits. Marketing seeks to amplify core equities while also incorporating an aspirational tonality.

• Ad spend has pivoted from primarily a local only emphasis towards a split with national spend in an effort to balance brand consideration (local) and brand awareness (national).

• Recent TV ads: Hardee's wonders if you can handle the hot honey on its Hand-Breaded Chicken Sandwich & Biscuit; stop in & celebrate the summer with a BLT Ranch Hand-

Breaded Chicken Sandwich set to rap music; if your stomach is rumbling for something hot, juicy & nestled between 2 toasty buns, Hardee's has you covered with its Hand-

Breaded Chicken Sandwich; and customers can wake up happy with its $2, $3, More Breakfast Menu (featuring its $3 French Toast Dips).

• Movie tie-ins with Godzilla vs. Kong promoted its special edition Godzilla Burger, Kong Burger & Kong Chicken Sandwich. Fast & Furious Spy Racer toys also available to go

with kids meals.

• Efforts to compensate for Hardee's relatively small scale/share of voice include an increased marketing allocation towards cost effective digital-first and social-friendly content

which also targets a younger demo. As an example, a launch of a Happy the Star Instagram filter at the beginning of 2021 was promoted by Charlotte McKinney, encouraging

fans to give into their cravings for decadent burgers. Online ads also incorporate humor around "Happy".

• 5/17 launch of its new Hand-Breaded Chicken Sandwich platform (joining the chicken wars) was supported by a 360-degree marketing campaign including TV to go with custom

digital content on OnlyFans bolstered by a partnership with VICE's MUNCHIES.

• Recent launch of its Hot Honey Chicken Sandwich featured free figurines (with each order) from 6 Adult Swim shows including “Robot Chicken,” “Metalocalypse” and “Sealab

2021.”

• Partnership with iconic sneaker designer Dominic Chambrone (AKA The Shoe Surgeon) yielded new kicks inspired by its Steakhouse Angus Thickburger launch.

• Cause marketing includes annual Stars for Heroes program which has raised $10.5MM for military-focused organizations including USA Cares and the Stand Up and Play

Foundation.

Marketing Budget

• A hybrid TV Media approach during 2020/21 supports both network and co-op TV. This contrasts with 2019 which was all co-op level, no network TV and minimal digital media.

In any case, many smaller markets are 100% national whereas the top 25 markets have a higher allocation to co-op & local.

• Minimum total ad fee of 5.5% is allocated as follows: 4.25% Hardee's National Advertising Fund; 0.75% local/regional marketing (LRM); and 0.50% co-op.

• HNAF funds: ad production, network TV, digital/social, print and local broadcast media plans.

• Co-op funds: DMA level media, sponsorships, incremental media, print, digital, etc.

• LRM funds: POP, outdoor, LRM programs and local sponsorships.

• Ad fees can be increased up to 7%, but no more than +0.5% per year.

Source: RR Estimates for Domestic System Pages 5 - 6 Report Not Licensed for Distribution

Home

Hardee's

National/ Brand Local/ Co- Total Marketing Contribution Total Marketing Admin 2020 Media Ad Spend (Net Overhead)

Ad Agency Year Hired

Fund % Op % of Sales $ Millions % of Sales $ Millions % of Sales $ Millions

72andSunny 2019 4.25% 1.25% 5.50% $110.0 -0.64% $12.8 4.86% $97.3

Sandwich N/a 2.80% 0.80% 3.70% $4,159.9 -1.07% $1,207.3 2.62% $2,952.6

2020 Estimated Net Marketing Spend Sandwich Segment Social Media Rank (Followers as of Dec. 2020)

$900 Chain Facebook Twitter Instagram

$769 Hardee's 1,151,598 74,100 71,100

$800

Arby's 8 9 7

$700 Burger King 4 2 4

Carl's Jr. 11 12 11

$600

Chick-fil-A 6 3 6

Millions

$500 Culver's 9 13 14

$400 $367 $356 Dairy Queen 2 6 8

$313 Five Guys 13 10 12

$300 Hardee's 14 15 13

$212 $191

$200 $154 $136 Jack in the Box 12 11 10

$115 $97

$83 $58 McDonald's 1 1 1

$100 $38

$0 Sonic Drive-In 7 7 9

$0 Taco Bell 3 4 3

Wendy's 5 5 1

Whataburger 10 8 5

Checkers/ Rally's 15 14 15

Source: RR Estimates for Domestic System Pages 5 - 6 Report Not Licensed for Distribution

Hardee's

Menu Size & Average Check Daypart Composition

Menu Menu Size Avg. Check/ vs. Change in Afternoon &

Breakfast Lunch Dinner

Size Change vs. '16 Check Segment Check vs. '16 Late Night

Hardee's 59 -31.4% $7.50 -22.3% 20.0% 43.2% 34.3% 12.4% 10.1%

Sandwich 61 -12.1% $9.65 19.2% 13.3% 37.8% 27.2% 21.5%

• Broad menu features: made-from-scratch breakfast biscuits; made-to-order charbroiled burgers (with 1/3 lb.

Angus options); hand-breaded chicken tenders & sandwiches; Deli Favorite sandwiches; and hand-scooped ice

cream shakes.

• Hardee's is unique in that its high-margin breakfast business represents a 48% mix (higher in the Southeast &

lower in the Midwest). While breakfast historically has been offered only until 11AM (reflecting the operational

challenge of preparing made-from-scratch biscuits while simultaneously preparing lunch/dinner options), some

stores have extended this until 2PM.

• Breakfast options include: traditional made-from-scratch breakfast biscuits which often incorporate eggs,

sausage/protein varieties & cheese; its new Hand-Breaded Chicken Biscuit & Chicken Waffle Sandwiches;

other sandwiches with waffle, croissant & sour dough carriers; cinnamon roll; breakfast burrito; breakfast

platters; and $2, 3, More breakfast menu (sausage biscuit, bacon egg & cheese burrito/French Toast & platter).

• Charbroiled burgers drive about 40% - 60% of lunch/dinner sales (lower end is for stores that also offer fried

chicken) and its platform includes 5 "Charbroiled Stars" which use smaller patties along with 5 third pound

Menu 100% Angus beef options. DT menu board also features its new BLT Ranch Thickburger and chicken options.

Strategy • Charbroiling technique entails flame-grilling machines that send meat along a conveyor-belt device with top

and bottom burners while “char rocks” collect beef fat (creating smoke) to add flavor.

• New chicken products (including its new Hot Honey Hand-Breaded sandwich/tender variety) feature 100%

premium white meat breast filets that are marinated in 13 signature seasonings and dipped in buttermilk before

going through a six-step hand-breading process in Southern-style flour.

• Chicken options also include regular hand-breaded chicken tenders and sandwich along with 2 charbroiled

chicken sandwiches.

• Deli Favorites include: Jumbo Chili Dog & Big Hot Ham.

• Desserts include Hand-Scooped ice cream shakes, mini swirl cones (local option), cinnamon roll, cookie and

apple turnover.

• ~14% of system units are dual-branded with the Mexican-inspired Red Burrito concept (Chicken Quesadilla &

Chicken Bowl; Grilled Burritos; Tacos; Super Nachos; & Taco Salad). While Red Burrito co-branding is no

longer part of Hardee's growth plans, the company continues to support existing restaurants.

• Menu item count is in-line with the segment average.

• Traditional QSR menu featuring charbroiled burgers (including its Black Angus platform) and hand-breaded

Core chicken options (100% premium white meat breast filet that is marinated in 13 signature seasonings & dipped in

Menu buttermilk before going through a 6-step hand-breading process in Southern-style flour & then cooked until

Equity golden brown) is unique because of an impressive 30% to 40% mix of its iconic made from scratch biscuits.

• In-store food is delivered to the table with an attractive presentation (open cardboard food boats).

Source: RR Estimates for Domestic System Pages 7 - 8 Report Not Licensed for DistributionMenu Size Trends

Hardee's 2015 Hardee's

2016 2017 Average

2018 Check

2019Trends

2020 2021

80 76

Hardee's 88 30% $15

86 70 69 76 59 51 25%

70 68 69Change

67Hardee's65

YOY N/a -2.3% -18.6% -1.4% 10.1% -22.4% -13.6%

Sandwich 59 61 70 20%

69 68 67 65 61 55 20%

60 55

51 $9.65

10.1% 10% $10 $8.31 $8.87

2014 2015 $8.09

2016 2017 $8.58

2018 2019 202015%

$7.50

40 0% $6.25 $6.50 $6.65 $6.76

-1.4%

10.9% 10%

Hardee's $5.90 -10% $5

$6.10 $6.25 $6.50 $6.65 $6.76 $7.50

20 -13.6%

-18.6% YOY Change

Hardee's 3.4% 2.5% 4.0% 2.3% 1.7% 10.9%5%

-22.4%$7.57 -20% 4.0%$8.31

Sandwich $7.82 $8.09

2.5% 2.3%$8.58 $8.87 $9.65

1.7%

0 -30% $0 0%

2017 2018 2019 2020 2021 2016 2017 2018 2019 2020

Hardee's Sandwich YOY Change Hardee's Hardee's Sandwich YOY Change Hardee's

Source: RR Estimates for Domestic System Pages 7 - 8 Report Not Licensed for Distribution7

Hardee's

Value

• Hardee's is reluctant to compete with the larger, national players around value/discounting as the brand lacks

sufficient share of voice to promote both quality and value sufficiently to overcome trade-down.

• Core breakfast biscuits start at $2 (plain sausage) but mostly cost $3+ to $4+.

• $2, 3, More breakfast menu includes $2 sausage biscuit, $3 bacon egg & cheese burrito/French Toast and $4

platter.

• Burgers start at $1.89 for a small but typically run $5 - $6+ (the Monster Angus Burger tops it off at $7.99).

• Hand-breaded chicken sandwiches and tenders are $3.99 with a $1 upcharge for the hot honey variety.

• All-Star Meals (including fries, drinks & cookie): 2 hot ham 'n cheese sandwiches for $6; and 3 pc. chicken tenders

for $5.

• Periodic use of national BOGO offers.

• Coupon drops approximate 1x month with deals such as: price discounts on core products; buy one get one offers;

and free fry & drink offer with the purchase of an LTO burger.

• Average check is -22% below segment average which reflects high mix of lower breakfast tickets.

Promotional Strategy

• Multi-layer promotional strategy has been recently focused on value ($2, 3 More breakfast menu) to go with new

product news & repurposed promotions like a March offer of its Steakhouse Angus Thickburger with A.1. Sauce &

its "New" Really Big Hardee's which was first introduced in 1995 to compete with the Big Mac & Whopper.

Menu Innovation

• Significant innovation ramp-up starting in 2020 helps increase trial/brand reach as the brand seeks to find new

ways to “Feed Your Happy” by satisfying their fans’ ultimate cravings.

• Recent innovation includes: French Toast Dips; hot honey chicken lineup; BLT ranch menu (chicken sandwich,

Angus Thickburger & Bacon Ranch Fries); hand-breaded chicken & waffle sandwich/hand-breaded chicken

biscuit/hand-breaded chicken sandwich in May 2021 as Hardee's joined the chicken sandwich wars; and a Fiery

Menu (including a Fiery Famous Star burger & Fiery Sauce as a side for tenders) at the beginning of the year.

• Corporate reports that it is already starting to test the next half dozen hand-breaded chicken products.

Number of Annual New Products

2017 2018 2019 2020 YTD 2021

Hardee's 9 12 8 18 13

Sandwich 13.2 12.6 11.4 8.7 5.4

Hardee's Promotional Activity

18 100%

16

% of Total Promotions

14 80%

# of Promotions

12

60%

10

8

40%

6

4 20%

2

0 0%

Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

Hardee's Total Promotions Avg. # Sandwich Promotions Hardee's Value % Sandwich Value %

Monthly New Product Calendar (Includes LTOs)

Nov-20 Jan-21 Feb-21 May-21 Jun-21 Aug-21 Sep-21

Fiery Menu (Fiery BLT Ranch Menu Hot Honey Chicken Sandwich

Hand-Breaded Chicken

Famous Star; (BLT Ranch Hand- Lineup (Hot Honey Hand-Breaded

Monster and Waffle Sandwich; French

Chicken Tenders The Really Breaded Chicken Chicken Sandwich; Hot Honey

Angus Hand-Breaded Chicken Toast

Dipped in Fiery Big Hardee Sandwich; BLT Hand-Breaded Chicken Biscuit;

Thickburger Biscuit; Hand-Breaded Dips

Sauce); Fiery Ranch Angus Hot Honey Hand-Breaded Chicken

Chicken Sandwich

Super Star Thickburger) and Waffle Sandwich)

Source: RR Estimates for Domestic System Page 9 Report Not Licensed for DistributionHome

Hardee's

Operations Strategy

• Operational complexity is increased by: made-from-scratch breakfast biscuits; made-to-order burgers (with different patty

varieties); hand-breading of chicken products; and hand-scooped ice cream. Biscuits require a specialized prep team and a

specialized cooking platform. This contrasts with most competitors which use a single flat grill platform for breakfast, lunch & dinner

and explains why Hardee's is not currently able to offer breakfast items all day long (although breakfast hours are being extended to

2PM in some markets).

• In any case, Hardee's drive-thru speed is above average according to a 3rd party survey with good order accuracy.

• Continued efforts to improve service speed include: streamlined back-of-the-house processes; the ability to hold smaller patties;

and the use of double drive-thrus in some cases.

• Staff training follows Restaurant Operating System & Breakfast Operating System standards, procedures and labor deployment

practices. Franchisor offers “Star Academy” training to help franchisees best analyze and improve their business.

Corp. Oversight & Quality Control

Avg. # Company Stores/ # Franchise Stores/ Average Units/

Restaurant Inspections Food Safety

Area Supervisor Consultant Franchisee

EcoSure operational assessments

EcoSure 3x/yr. 5 to 8 40 to 50 21.1

3x/year.

• Parent company, Roark Capital Group, provides scale with regard to digital & tech investments, data mining and analytical

capabilities in addition to other cost synergies.

• Ned Lyerly was appointed as CEO of CKE in April 2019, replacing Jason Marker who was promoted to the post in 2017 with a

plan to separate Hardee's & Carl's Jr. Lyerly, who has been with CKE for more than three decades, was previously president of

international. Marker's leadership overhaul included a new CMO, COO, CIO and Chief People Officer.

• Subsequently, Lyerly appointed Lance Tucker as CFO (previously CFO at Jack in the Box & Papa John's) and Phil Crawford as

Chief Technology Officer responsible for brand marketing and vision & strategy. Crawford (formerly global chief technology officer

at Godiva Chocolatier & Shake Shack's CIO before that) is charged with building a technology roadmap to transform CKE into a

technology-forward, data-driven organization. John Dunion, a 25-year company veteran, was promoted to COO in October 2021 to

oversee operations and the supply chain.

• Quality control initiatives include: Operation Quality Service Cleanliness (processes & procedures for efficient store operations);

Super Star Service (focuses on hospitality & energizing the crew); Operation Drive-Thru (labor scheduling optimization); Learning

Management System (web-based tool allowing for the delivery & tracking of learning throughout the organization); and the

Breakfast Operating System (improves biscuit freshness through better demand forecasting & more efficient production methods).

• Operations further benefit from practice of deploying balanced scorecards.

• EcoSure operational assessments are conducted 3x year.

Consumer Ratings

Customer Feedback Toll Free Estimated Responses/

Website Mystery Shops

Program Number Month/ Store

Service Management (877) 799- https://www.carlsjrandhardees

N/a No

Group STAR (7827) survey.com/

• Internally generated guest surveys are collected at www.TellHappyStar.com in exchange for a BOGO offer.

Typical Store Level Labor Structure (Assumes Concept AUV)

Total Hourly/Crew Employees per Store Total Employees During Peak Shift

Hardee's 25 - 28 9 - 11

Sandwich 15 - 80 6 - 20

Source: RR Estimates for Domestic System Page 10 Report Not Licensed for DistributionHardee's

POS System

Roll-Out Date N/a % of System Complete N/a

PAR ES600, PAR ES8500 or

Current POS System Auras J1900 with PAR Brink $35k - $45k (5 POS terminals & 6 kitchen

POS Cost

Provider software or StarPOS software (to display monitors)

be discontinued 2021)

• Franchisees have the option to choose either Xpient or Par Brink (mobile order capability) POS systems. Par Brink

cloud based POS software upgrade costs range from a few thousand dollars per store up to $10k for a complete upgrade.

• Franchisees can be required to upgrade or replace systems at anytime during the franchise term without limitations on

the cost or frequency.

Store Equipment

• Digital menu boards ($10k - $15k) are installed during new builds. 23% of the system has digital drive-thru menu boards

and 61% has pre-sell menu boards in place.

• Drive-thru headsets were implemented to improve speed of service and accuracy.

• The use of virtual reality to test and implement different kitchen configurations as well as new equipment has helped

drive significant cost efficiencies.

Customer Access

Off Premise Sales Composition Delivery Detail Sales Channels

Drive- Total Off- % Units Digital Credit/

Take-out % Delivery % In House or 3rd Party

Thru % Premise % w/Delivery Orders Debit Mix

Hardee's 83% 11% 2% 96% 55% Uber Eats & DoorDash N/a 50%

Sandwich 75% 10% 4% 89% N/a N/a N/a 61%

• Historical 75% DT mix increased to 90%+ during 2020 and is expected to settle in-between these 2 ranges (although

they are not expected to return to 75%).

• Online ordering platform was recently added in March 2021 including order-ahead capabilities on its app (which is not

available at all locations) and is generating a low single digit sales mix.

• Delivery sales margins are lower, but the dollar profit is higher due to a larger check average (~$17 vs. $7.50).

Source: RR Estimates for Domestic System Page 11 Report Not Licensed for DistributionHome

Hardee's

Sales Trends

• Comps turned positive/break-even in 2020 after 4 consecutive years of declines as the system benefits from a significant

increase in drive-thru demand post-covid. Building on this momentum, YTD comps through the first 3 quarters of 2021 were

positive mid-single-digits as the brand's menu and marketing improvements gain traction.

• All-the-same, 2020 results underperformed the segment average by -2%, reflecting the system's material breakfast mix (a

daypart that suffered disproportionately post-covid).

• Historical sales pressure reflected: a struggle around a premium lunch/dinner positioning at a time when QSR competitors had

been emphasizing value; relatively slow digital progress; a lack of a consistent, effective marketing message around its very

important breakfast daypart; and past efforts to migrate guests to higher priced LTOs.

• Also, operational complexities associated with its hand-crafted positioning (particularly as it relates to its biscuits) translate into a

lack of all-day breakfast/extended late-night hours and slower service speeds. In any case, the system is seeking to expand

breakfast from 11AM to 2PM currently.

• Evidence of the brand's efforts to increase its menu and marketing relevancy is reflected by record 1/21 comp growth.

• Because of the system's concentration in the Southeast & Midwest, sales performance tends to reflect the economic environment

of these regions.

• Hardee's positioning benefits from its QSR DT format, a return of breakfast and improving relevancy around its

menu & marketing.

Sales Outlook • However, Hardee's challenge to compete with the larger, national players around value/discounting (given an

insufficient share of voice to promote both quality & value without prompting trade-down) may have implications

as lower income consumers struggle post-stimmy.

Hardee's Same Store Sales vs. Sandwich Segment

6%

4% 4.3% 4.2%

3.5%

2% 2.5%

1.5%

0% 0.4%

-0.5% -0.8%

-2%

-4% -4.3% -3.8%

-6%

-8%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Hardee's Franchise SSS Hardee's Company SSS Hardee's System-wide SSS Sandwich SSS

Market Share Analysis - 2020 vs. 2019

% Change in Net Unit Counts '20/'19 Change In Same Store Sales '20/'19 Net Change in Market Share '20/'19

Hardee's -2.5% 0.4% -0.09%

Sandwich -0.4% 2.4% Not Meaningful

Segment Market Share Rank Based on Estimated

Hardee's Share of $1B+ Sandwich Chains FYE 2020 Sales ($ Billions)

Chain System Sales % Market Share

2.5% McDonald's $40.5 35.1%

2.3% 2.3% 2.3% 2.3% Chick-fil-A $13.7 11.9%

2.2% 2.2%

2.1% Taco Bell $11.3 9.8%

2.0% 2.0% Wendy's $10.2 8.9%

1.8%

1.7% Burger King $9.7 8.4%

1.5% Sonic Drive-In $5.1 4.4%

Arby's $4.2 3.7%

Dairy Queen $4.1 3.5%

1.0% Jack in the Box $3.7 3.2%

Whataburger $2.8 2.4%

Hardee's $2.0 1.7%

0.5% Zaxby's $2.0 1.7%

Culver's $2.0 1.7%

Five Guys $1.8 1.5%

0.0% Carl's Jr. $1.5 1.3%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Checkers/ Rally's $0.9 0.8%

Segment Total $115.4 100.0%

Source: RR Estimates for Domestic System Page 12 Report Not Licensed for DistributionHome

Hardee's

Franchisee Unit Economics

% Change '21/'20

• 2020 AUV posted a y/y increase for the first time since trending down from its 2015 peak and is currently -32% below the segment average.

• This reflects the chain's significant low-ticket breakfast mix and the system's hesitancy to increase its emphasis on value/discounting given concerns that guests will

AUV 4.1%

simply trade-down.

• Projected FYE 2021 AUV is on track to increase an additional 4% which would be just under the 10-year high.

• 2020 COGs represented an all-time best, reflecting diminished value and favorable commodity costs.

Food & Paper • A 150 bps outperformance reflects the chain's profitable breakfast mix and aversion to discounting & low price-points.

0.3%

(Net of Rebates) • COGs for breakfast (20% to 25%) compares favorably to lunch/dinner (typically low 30's but up to 40% with discounting).

• McClane is responsible for delivering food and packaging to the Hardee's system.

Fiscal Year Commodity • While the BLS Foodstuff Index has increased significantly YTD for the first 3 quarters of 2021, recent trends are beginning to moderate (although they remain highly

Cost Outlook elevated).

• 2020 labor margin improved by 180 bps y/y reflecting the advantage of an entirely drive-thru focused operating model which eliminated staffing requirements at the

Labor & counter and in the dining rooms.

0.2%

Benefits • In any case, the labor margin underperforms the segment average by -210 bps, reflecting previously discussed operational complexities.

• Labor efficiency is better at breakfast as this daypart does not entail a made-to-order process incorporated during lunch/dinner.

• Significant AUV underperformance, high labor costs and elevated ad spend (to compensate for relatively small scale) translates into a -220 bps EBITDAR margin

underperformance.

EBITDAR

-0.5% • In any case, the system's actual EBITDAR margin improved 2% y/y in 2020 reflecting favorable labor & food costs.

(Pre G&A)

• Slightly higher COGs and labor margins are expected to pressure the projected 2021 EBITDAR margin by ~50 bps.

• Rent runs around 8% to 9% and corporate overhead 3% to 5%.

Source: RR Estimates for Domestic System Pages 13 - 14 Report Not Licensed for DistributionHome

Hardee's

Franchisee Unit Economics

Hardee's Hardee's

Historical Range FYE '21E Versus:

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021P

High Low 10 Yr. Best Company Stores

AUV (Net Sales) $1,107,000 $1,137,000 $1,189,000 $1,206,000 $1,199,000 $1,149,000 $1,143,000 $1,125,000 $1,134,000 $1,180,000 $1,206,000 $1,107,000 -2.2% N/a

Food & Paper 29.0% 29.3% 30.1% 28.0% 27.5% 28.3% 27.8% 27.5% 27.0% 27.3% 30.1% 27.0% 0.3% N/a

Labor & Benefits 30.3% 30.3% 30.3% 30.5% 30.8% 31.5% 32.0% 32.8% 31.0% 31.2% 32.8% 30.3% 1.0% N/a

Royalty 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 0.0% N/a

Advertising 5.0% 5.0% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.5% 5.0% 0.5% N/a

Other Op. Ex. 11.8% 11.8% 11.9% 12.0% 12.0% 12.3% 12.3% 12.5% 12.8% 12.7% 12.8% 11.8% 1.0% N/a

EBITDAR 20.0% 19.7% 18.2% 20.0% 20.3% 18.5% 18.5% 17.8% 19.8% 19.3% 20.3% 17.8% -1.0% N/a

EBITDAR $ $221,400 $223,989 $216,398 $241,200 $242,798 $212,565 $211,455 $199,688 $223,965 $227,740 $242,798 $199,688 -$15,058 N/a

Sandwich FYE '20 vs Segment Sales/Sq. Ft.

AUV $1,359,154 $1,367,643 $1,420,429 $1,482,786 $1,498,071 $1,512,500 $1,533,184 $1,588,929 $1,665,643 $1,665,643 $1,359,154 -31.9% Hardee's

Food & Paper 31.7% 31.5% 32.0% 30.8% 29.8% 30.1% 29.7% 29.2% 28.5% 32.0% 28.5% -1.5% $472.0

Labor & Benefits 28.2% 28.3% 28.2% 28.2% 28.7% 29.0% 29.5% 29.6% 28.9% 29.6% 28.2% 2.1% Sandwich

Royalty 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% 4.5% -0.5% $632.5

Advertising 4.2% 4.3% 3.9% 4.5% 4.5% 4.5% 4.4% 4.4% 4.4% 4.5% 3.9% 1.1%

Other Op. Ex. 11.4% 11.7% 11.7% 11.5% 11.7% 11.9% 11.9% 12.0% 11.8% 12.0% 11.4% 0.9%

EBITDAR 20.0% 19.8% 19.4% 20.5% 20.8% 20.0% 20.0% 20.3% 21.9% 21.9% 19.4% -2.2%

EBITDAR $ $271,844 $270,590 $275,157 $303,865 $311,866 $303,148 $306,856 $322,269 $365,014 $365,014 $270,590 -$141,049

Hardee's Franchisee AUV & EBITDAR Trends

$1,800,000

29%

$1,500,000 27%

EBITDAR %

$1,137,000 $1,189,000 $1,206,000 $1,199,000 $1,149,000 $1,143,000 $1,134,000 $1,180,000

$1,200,000 $1,107,000 $1,125,000 25%

AUV

$900,000 23%

21%

$600,000 20.0% 19.7% 20.0% 20.3% 19.8% 19.3% 19%

18.2% 18.5% 18.5%

$300,000 17.8%

17%

$0 15%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021P

Hardee's AUV Sandwich AUV Hardee's EBITDAR % Sandwich EBITDAR %

Source: RR Estimates for Domestic System Pages 13 - 14 Report Not Licensed for DistributionHome

Hardee's

New Build Costs (Excluding Land)

Building Prototype Name Year Introduced

American Classic 2018

• Investment costs in our model reflect the new American Classic design (only a limited number of these stores have been

built so far) which celebrates small-town America, highlighting Hardee’s down-home roots while reintroducing the brand

and its quality food focus/preparation.

• Exterior enhancements include: a raised red roofline over the brick entry & drive-thru; gray border around the top of the

building; white lower half of the building and black band in the center of the building featuring the phrase "Made From

Scratch Biscuits".

• Interior elements include: distressed wood paneling; black window frames; brick accents; and white subway tiles.

• 0.76x sales-to-investment ratio under-performs 1.04x segment average.

• An additional cash window in conjunction with a single or double drive-thru lane can add $65k to $115k to new build

costs.

• In new markets, breakfast mix tends to start very low before building during the first 3 - 6 months while lunch and dinner

declines.

• Preferred site guidelines within a 2-mile radius: (1) minimum daily traffic count of 20,000, (2) residential population of

25,000+ with minimum daytime work population of 11,000+, and (3) average household income of $35k - $60k.

• New franchisees may also be required to pay Opening Training Support Team Fees (at an estimated cost of between

$30k to $70k) which entitles franchisee to opening assistance support for the first 2 newly developed restaurants.

• The system is developing a new prototype (Urban Lite) with smaller dining rooms (0 to 30 seats) and more space

reserved for things like extra drive-thru lanes, designated curbside pickup parking and easily accessible delivery windows

for third-party drivers. Prototype also incorporates redesigned kitchens optimized for off-premise.

New Build Incentives

• Initial fees depend on the number of units to be built - $35k (1-2 units), $30k (3-4 units) and $25k (5+ units).

• Restaurant Development Incentive Program offers a $15k reduction to the initial fee and reduced royalty fees (save 4%

first 6 months, 3% months 7 - 12, 2% months 13 - 18 and 1% months 19 - 24) for new or rebuilt stores opened by

12/31/22. Any additional restaurants opened by 12/31/22 are eligible for the Accelerator Incentive (save 4% during year 1,

2% year 2 and 1% year 3).

Hardee's Segment Average

Primary Format Sandwich

Building Type Freestanding

New Build AUV $1,300,000 Costs $1,571,786 Costs

% of Total % of Total

Building & Sitework $1,100,000 61.5% $985,071 60.6%

Furniture, Equipment, POS & Signs $510,000 28.5% $479,679 29.5%

Small Wares & Inventory $20,000 1.1% $20,714 1.3%

Initial Franchise Fee $35,000 2.0% $46,071 2.8%

Soft Costs (1) $125,000 7.0% $94,786 5.8%

Total Before Incentives $1,790,000 100.0% $1,626,321 100.0%

Franchisor Incentives (2) ($75,306) -4.2% ($119,353) -7.3%

Total After Incentives $1,714,694 95.8% $1,506,969 92.7%

Typical New Unit Requirements

Land (sq. ft.) 27,000 36,095

Building Size (sq. ft.) 2,500 2,634

# Seats 54 57

Key New Build Ratios (Excluding Land Costs)

Sales/sq. ft. $520.00 $596.83

Investment Costs/sq. ft. $716.00 $617.53

Sales/Investment (Before Incentives) 0.73 0.97

Sales/Investment (After Incentives) 0.76 1.04

(1) Soft costs include pre-construction costs such as architectural and engineering fees, permits, opening advertising, training expenses

and utility deposits, but excludes liquor license (if applicable) due to the extreme range in costs.

(2) Includes cash incentives, free equipment and/or food credits plus royalty, ad and initial fee reductions discounted at 5%.

Source: RR Estimates Page 15 Report Not Licensed for DistributionHome

Hardee's

New Build vs. Buy Analysis (Excluding Land)

New Build vs. Acquisition of Existing Store

AUV 1,300,000 AUV 1,180,000

EBITDA (post G&A) 87,440

Purchase Price Multiple 4.73

Building Costs Ex. Land 1,714,694 Business Value 413,779

Sales/Investment 0.76 Sales/Acquisition Price 2.85

Unlevered New Build ROI 9.6% Unlevered Acquisition ROI 21.1%

Segment Unlevered New Build ROI 15.2% Segment Unlevered Acquisition ROI 20.2%

Acquisition Assumptions

Annual Rent 8.5% G&A per Unit $40,000

Build/Buy Ratio 4.14

Sales to Investment Trends

Hardee's Sales/Investment Ratio vs. $1B+ Sandwich Chain Average

1.4

1.2

1.0 1.06 0.99

0.91 0.91

0.8 0.76

0.6

0.4

0.2

0.0

2016 2017 2018 2019 2020

Hardee's Sandwich

Valuation Trends (for Transactions Under $500k in Aggregate EBITDA)

• Unit level M&A valuation multiple is trending up from a 2H20 bottom but remains at -11% below the segment average.

• The system has been consolidating under larger operators that span multiple geographies.

Hardee's EBITDA Multiple (Enterprise) vs. $1B+ Sandwich

5.5 5.29 2%

% Difference vs. Segment

5.08 5.10 5.04 5.08 5.13

4.96 0%

Concept Multiple

5.0 -0.9% 4.68 4.73 -2%

-2.0% 4.54

-3.0% -3.1% -3.3% -3.0%

4.5 4.34 -4%

-5.3% -6%

4.0 -8%

3.5 -11.0% -10.7% -11.2%-10%

-12.2% -12%

3.0 -14%

Jun-16 Dec-16 Jun-17 Dec-17 Jun-18 Dec-18 Jun-19 Dec-19 Jun-20 Dec-20 Jun-21

Hardee's % Difference Relative to Segment

Source: RR Estimates for Domestic System Page 16 Report Not Licensed for DistributionHome

Hardee's

Unit Development

10 Year Average Growth • Net units declined for the last 3 years.

Hardee's 2.2% • Notably, CKE appointed Matthew Walls as its first chief global development officer (previously SVP of global franchise development at Domino’s). Walls' strategy is to

Sandwich 2.0% incorporate omnichannel stores with smaller dining rooms, order ahead capabilities with drive-thru or curbside pickup, third-party delivery partnerships and other guest-facing

10 Year Total New Builds upgrades. Walls is focused on developing the upper Midwest (particularly Michigan and Ohio), Texas and New England.

Hardee's 394 • Hardee's recently announced plans with RSMG Holding LLC to develop 25 new locations in West Palm Beach.

Hardee's Gross New Unit Development Composition

80

1

60

7 5 1

40 0

2 66 1

49 53 51 0

20 2 1 35 40

32 0 24

16 20 14

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Outlook

Franchise Units Company Units

Hardee's Gross Unit Development vs. Sandwich Segment

4%

3.7%

3.3% 3.3%

3% 2.8%

2% 2.0% 2.2%

1.9%

1.2% 1.3%

1% 1.1%

0.8%

0%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Outlook

Hardee's Gross Unit Growth % Sandwich Gross Unit Growth %

Net Unit Development vs. Sandwich Segment

3%

2.6% 2.4%

2% 2.2%

1% 1.1% 0.9%

0.5%

0% 0.2%

-1% -1.0%

-2%

-2.3% -2.5%

-3%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Hardee's Net Unit Growth % Sandwich Net Unit Growth %

Source: RR Estimates for Domestic System Page 17 Report Not Licensed for DistributionHardee's

Unit Closings

10 Year Average Closures • Annual closure rates have exceeded the segment average as the weakest stores in this 60 year-old system continue to be culled.

Hardee's 1.8% • For franchise agreements terminated for default, franchisees are obligated to pay the net present value of the royalty fee for the balance of

Sandwich 1.4% the initial term or 3 years (which ever is less) based on the average weekly royalty for the preceding 52 week period prior to the default

10 Year Total Closures (unless waived by the franchisor).

Hardee's 329

Hardee's Unit Closings

90

80 9

70

60 3

50 1

40

0 73

30 56

53

20 0 4

36

2 1 5

10 2 19 20

13 12 11 9

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Franchise Units Company Units

Hardee's Closure Rates vs. Sandwich Segment

10.0%

8.0%

6.0%

4.0% 4.4%

2.9% 3.3%

2.0% 1.9%

0.9% 1.1% 1.3%

0.9% 0.8% 0.6%

0.0%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Hardee's Closure Rate Hardee's Transfer Rate Sandwich Closure Rate

Source: RR Estimates for Domestic System Page 18 Report Not Licensed for DistributionHome

Hardee's

System Condition

Current Program Start

N/a Projected Completion Date: N/a

Date:

% System Units Built in Last 7 % System Remodeled and/or Stipulated Remodel Frequency

Year Founded

Years (as a % of Current Total) Newly Built in Current Image (in Years)

Hardee's 1960 18% 28% N/a

Sandwich N/a 19% 53% 7.7

Remodel Program Overview

• Current remodels incorporate some of the American Classic elements including a focus on drive-thru and off-premise upgrades, new digital exterior menu

boards, metal seam roof, new paint, small tower elements and new dining room package. In any case, only ~10% of the system has been remodeled to the

current image while an additional ~18% represents new buildings from all designs over the last 7 years.

• The previous Contemporary Star design reimage program (targeting Millennials) ran from Spring 2016 to early 2018 (10% of system was updated during

2016 with little subsequent progress) and cost $150k to $175k for interior (floor tile, beverage bar, bathroom tile, new seating package and ADA compliance)

and $25k to $50k for exterior elements including new metal seam red roof ($175k to $225k total). These costs included digital menu boards ($10k - $15k) and

excluded optional kiosks ($3k - $5k). Costs varied around: whether new tile floors ($20k) and new roofs ($15k - $20k) were installed in previous remodel; and

extent of required ADA modifications. The addition of an optional exterior parapet wall with LED lighting added $100k to costs (although we understand only a

few high AUV stores opted for this feature).

• Franchisees can be required to perform extensive remodels, but not more often than once every 5 years. The franchisor can also require new/modified

menu boards, but not more often than once every 3 years.

Cost & ROI

Scope Total Cost Cost/ Sq. Ft. Sales Lift Year 1 ROI (1)

Refresh N/a N/a N/a N/a

American Classic $200,000 $80.0 Minimal 4.5%

Major N/a N/a N/a N/a

Scrape & Rebuild N/a N/a N/a N/a

Incentives

• None

(1) Assumes year 1 sales lift and flow through of 2x EBITDAR divided by remodel cost.

Source: RR Estimates for Domestic System Page 19 Report Not Licensed for DistributionHome

Hardee's

Franchisee Composition

# Franchised Total 10 Largest Franchisees

Year Franchising Initiated Avg. Units/ Franchisee

Units Franchisees Unit Count % Franchise System

1961 1,561 74 21.1 1,144 73.3%

Franchise Policy (New Franchisees)

Per Unit

Per Unit Development Renewal Territory

Development Fee/ Term Renewal Fee Transfer Fee Royalty

Initial Fee Fee Credit? Term Protection

Deposit

5 yrs. or 10

$35,000 $10,000 Yes 20 $5,000 or $10,000 $2,500 1st unit / $500 each additional unit None 4.00%

yrs.

Financial Requirements

Actively Seeking New Franchisees? Minimum Unit Development Minimum Net Worth Minimum Liquidity

Yes 3 Units $1,000,000 $300,000

Franchisee Associations Info

Year Independent or Franchisor

Name Web Address

Founded Managed

Independent Hardee’s Franchisee Association (IHFA) 1997 Independent www.ihfa.com

Franchise Unit Ownership % 10 Largest Franchisees

Company Franchisee Unit Count

100% 1 Boddie-Noell Enterprises, Inc. William Boddie 342

93.5% 93.8% 93.6% 93.6% 90.4% 88.7%

80% 77.2% 2 Capstone Restaurant Group Buddy Brown 257

72.3% 72.4% 73.4% 3 Doro, Inc. & Northland Restaurant Group, LLC Jon Munger 106

60%

4 Starcorp HD, LLC Eric Lester 93

40% 5 Phase Three Star LLC/Ponder Enterprises Jack Kemp 83

20% 6 Paradigm Investment Group, LLC Don Wollan 81

7 Franceico., L.P. 65

0% 8 J&S Restaurants/DBJ Enterprises, Inc. Mark Johnson 42

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 9 Morning Star, LLC Brian Bergeron 39

Hardee's Sandwich 10 Saddle Peak, LLC Nick Shurgot 36

Total 1,144

Source: RR Estimates for Domestic System Page 20 Report Not Licensed for DistributionHardee's

Category Price Category Price

Sides 3 Breakfast 15

Beer Battered Onion Rings $2.49 Bacon, Egg & Cheese Biscuit $3.69

Crispy Curls $2.49 Biscuit 'N Gravy $2.79

Natural-Cut French Fries (Med.) $2.19 Country Fried Steak Biscuit $2.99

Country Ham Biscuit $2.99

All Star Meals (Starting at $5) 2 Frisco Breakfast Sandwich $3.99

Hand Breaded Chicken Tender (3 pcs.) All Star Meal $5.00 Hand-Breaded Chicken Biscuit $3.79

Two Hot Ham N' Cheese Sandwiches All Star Meal $6.00 Hardee Breakfast Platter w/Bacon $4.00

Hash Rounds (Med.)

2*3*More Menu 3 Loaded Breakfast Burrito

Sausage Biscuit $2.00 Loaded Omelet Biscuit $3.19

French Toast Dips $3.00 Monster Biscuit $4.39

Hardee Breakfast Platter with Sausage $4.00 Pork Chop 'N' Gravy Biscuit $3.69

Sausage & Egg Biscuit $2.99

Burgers 15 Sausage Biscuit $2.00

Bacon & Cheese Angus Burger $6.09 Sunrise Croissant

Big Cheeseburger $3.69

Double Cheeseburger $2.79 Dessert 6

Double Western Bacon Cheeseburger $5.99 Chocolate Chip Cookie $0.59

Famous Star with Cheese $4.49 Chocolate Hand-Scooped Ice Cream Shake $3.59

Frisco Angus Burger $5.59 Vanilla Hand-Scooped Ice Cream Shake $3.59

Monster Double Angus Burger $7.99 Strawberry Hand-Scooped Ice Cream Shake $3.59

Mushroom and Swiss Burger $5.99 Apple Turnover $0.59

Orginial Angus Burger $5.59 Cinnamon Roll $2.49

Small Cheeseburger $2.39

Small Hamburger $1.89 Red Burrito - Co-Brands 15

Super Star with Cheese $5.89 Beef Grilled Burrito

The Big Hardee $4.99 Chicken Grilled Burrito

The Really Big Hardee Hard Chicken Taco

Western Bacon Cheeseburger $4.79 Chicken Soft Taco

Soft Taco (Beef)

Chicken 5 Hard Beef Taco

Hand-Breaded Chicken Tenders (3 pcs.) $3.99 Chicken Quesadilla

Hand-Breaded Chicken Sandwich $3.99 Cheese Quesadilla

Charbroiled BBQ Chicken Sandwich $5.49 Taco Salad (Beef)

Charbroiled Chicken Club Sandwich $5.49 Taco Salad (Chicken)

Hand-Breaded Chicken & Waffle Sandwich Super Nachos (Beef)

Super Nachos (Chicken)

Other 7 Chicken Bowl

Original Hot Ham ‘N’ Cheese $2.79 Beef Bowl

Big Hot Ham ‘N’ Cheese™ $4.69 Bean, Rice & Cheese Burrito

Jumbo Chili Dog $2.59

Original Roast Beef Sandwich Star Pals Kids Menu 4

Big Roast Beef Sandwich Kid's Meal Hamburger $3.39

Beer-Battered Fish Sandwich Kid's Meal Cheeseburger $3.39

Monster Roast Beef Hand-Breaded Chicken Tenders™ Kids Meal (2) $3.39

Hot Dog Kids Meal

Rise and Shine Coffee (Med.) $1.99

Soft Drink Brand - Coke (Med.) $2.09

Total Menu Items (*) 51

(*) Total menu item count excludes value menu items, Red Burrito and Kid's Menu. Bold items are new/upgraded since

last review.

Source: RR Estimates Page 21 Report Not Licensed for DistributionHome

Hardee's

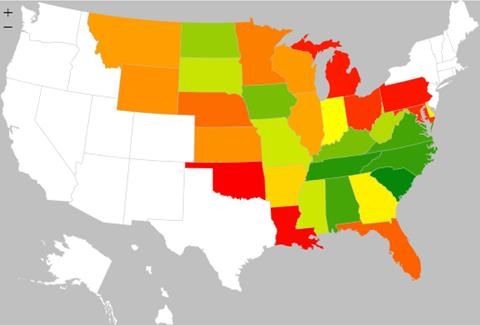

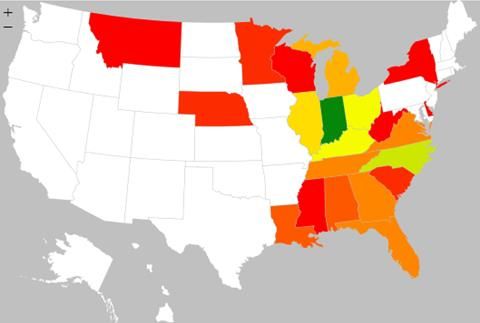

2020 State Unit Concentration (Units/Million People)

Lowest Concentration Highest Concentration

Least Development Most Development

Total Gross New Unit Development (2019-2021P)

Source: FDD and RR Estimates Page 22 Report Not Licensed for DistributionHardee's

Unit Activity by State

2020 Unit Count Gross Openings Closings Net Openings Transfers

State Total Franchised Company % Total 2017 2018 2019 2020 2021E 2017 2018 2019 2020 2017 2018 2019 2020 2017 2018 2019 2020

Alabama 104 91 13 5.9% 1 2 3 0 0 1 8 16 3 0 (6) (13) (3) 0 0 3 0

Alaska 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Arizona 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Arkansas 30 30 0 1.7% 4 0 0 0 0 2 2 5 0 2 (2) (5) 0 0 0 0 0

California 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Colorado 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Connecticut 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Delaware 11 11 0 0.6% 0 0 1 0 0 0 1 0 0 0 (1) 1 0 0 0 0 0

Dist. of Columbia 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Florida 101 101 0 5.7% 5 4 3 0 1 0 0 3 2 5 4 0 (2) 6 13 0 0

Georgia 119 116 3 6.7% 6 2 0 2 2 1 2 4 5 5 0 (4) (3) 2 8 0 1

Hawaii 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Idaho 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Illinois 99 99 0 5.6% 0 2 3 2 1 9 2 6 2 (9) 0 (3) 0 0 18 0 0

Indiana 80 79 1 4.5% 1 5 10 0 3 2 2 3 1 (1) 3 7 (1) 0 0 0 0

Iowa 59 59 0 3.3% 1 1 0 0 0 1 1 2 2 0 0 (2) (2) 0 0 0 10

Kansas 20 20 0 1.1% 0 2 0 0 0 0 0 1 0 0 2 (1) 0 0 0 0 0

Kentucky 83 81 2 4.7% 1 3 3 2 2 1 1 0 2 0 2 3 0 1 0 0 0

Louisiana 2 2 0 0.1% 2 0 3 0 0 1 11 5 3 1 (11) (2) (3) 8 8 0 0

Maine 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Maryland 15 15 0 0.9% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Massachusetts 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Michigan 15 14 1 0.9% 1 2 1 2 2 1 0 0 2 0 2 1 0 0 0 0 0

Minnesota 34 34 0 1.9% 0 0 0 0 2 3 0 0 0 (3) 0 0 0 0 9 0 1

Mississippi 43 39 4 2.4% 1 0 1 0 0 0 1 1 1 1 (1) 0 (1) 0 0 16 0

Missouri 88 88 0 5.0% 0 0 0 0 0 4 2 4 2 (4) (2) (4) (2) 0 0 0 0

Montana 8 8 0 0.5% 2 0 1 0 0 0 0 1 2 2 0 0 (2) 0 0 0 0

Nebraska 10 10 0 0.6% 1 1 0 1 1 0 0 0 0 1 1 0 1 0 0 0 1

Nevada 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

New Hampshire 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

New Jersey 0 0 0 0.0% 0 0 0 0 0 1 0 1 0 (1) 0 (1) 0 0 0 0 0

New Mexico 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

New York 0 0 0 0.0% 0 0 0 0 1 3 0 0 0 (3) 0 0 0 0 0 0 0

North Carolina 231 196 35 13.1% 12 5 3 2 3 3 6 5 12 9 (1) (2) (10) 1 0 0 0

North Dakota 13 13 0 0.7% 1 0 0 0 0 0 0 0 1 1 0 0 (1) 0 3 0 0

Ohio 31 29 2 1.8% 5 1 3 1 3 0 0 1 0 5 1 2 1 5 0 8 0

Oklahoma 1 1 0 0.1% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Oregon 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Pennsylvania 16 16 0 0.9% 1 0 0 0 0 0 0 0 1 1 0 0 (1) 0 0 0 0

Rhode Island 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

South Carolina 126 62 64 7.1% 2 2 2 0 0 0 6 12 3 2 (4) (10) (3) 0 0 0 1

South Dakota 13 13 0 0.7% 1 0 0 0 0 1 0 1 0 0 0 (1) 0 0 0 0 0

Tennessee 156 78 78 8.8% 2 1 1 1 2 0 5 3 8 2 (4) (2) (7) 0 1 0 0

Texas 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Utah 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Vermont 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Virginia 182 182 0 10.3% 1 3 2 1 1 0 0 1 3 1 3 1 (2) 0 0 0 0

Washington 0 0 0 0.0% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

West Virginia 28 28 0 1.6% 0 0 1 0 0 0 4 1 0 0 (4) 0 0 0 0 0 0

Wisconsin 42 42 0 2.4% 1 0 1 0 0 2 0 3 4 (1) 0 (2) (4) 1 0 0 0

Wyoming 4 4 0 0.2% 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Total 1,764 1,561 203 100.0% 52 36 42 14 24 36 54 79 59 16 (18) (37) (45) 24 60 27 14

% YOY Growth -2.5% -4.2% 13.4% 2.8% 1.9% 2.3% 0.8% 1.4% 1.9% 2.9% 4.3% 3.3% 0.9% -1.0% -2.0% -2.5% 1.4% 3.4% 1.6% 0.9%

Please note state unit data is derived from FDDs and may vary from figures reported in 10-Ks and annual reports.

Source: FDD and RR Estimates Page 23 Report Not Licensed for DistributionHardee's

American Classic Building & Dining Room

Previous Contemporary Star Building & Dining Room

Source: RR Company website Page 24 Report Not Licensed for DistributionVisit www.chainrestaurantdata.com or contact us at

(704) 441-3131 or info@ChainRestaurantData.com to:

• Add your colleagues to our client distribution list

• Ask us about custom research projects

• Inquire about RR Thermometer email marketing opportunities

Copyright: This Restaurant Research LLC document is copyrighted material. Due to the No Electronic Theft (NET) Act of

1997, electronic forwarding or other forms of redistribution, without the express permission of Restaurant Research LLC, are

violations of law and could be subject to fines of up to $250,000 and up to five years of imprisonment, even when no financial

gain or commercial advantage accrues to the forwarder/re-distributor. Copyright 2021 Restaurant Research® LLC. All

rights reserved.

Sources: All data represents RR estimates which are derived from various private and public sources.

Disclosure: Restaurant Research LLC often sells report subscriptions to concepts under our coverage.

Disclaimer of Liability: Although the information in this report has been obtained from sources Restaurant Research® LLC

believes to be reliable, RR does not guarantee its accuracy. The views expressed herein are subject to change without

notice and in no case can be considered as an offer or solicitation with regard to the purchase or sales of any securities.

Restaurant Research’s analyses and opinions are not a guarantee of the future performance of any company or individual

franchisee. RR disclaims all liability for any misstatements or omissions that occur in the publication of this report. In making

this report available, no client, advisory, fiduciary or professional relationship is implied or established. This report is intended

to provide an overview of the restaurant industry, but cannot be used as a substitute for independent investigations and

sound business judgment.

REPORT NOT LICENSED FOR DISTRIBUTIONYou can also read