Company Presentation November 2021 - cloudfront.net

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Company Presentation November 2021

Legal Disclaimer

This presentation includes “forward-looking statements.” Such forward-looking statements are subject to a number of risks and uncertainties, many of which are not under AR’s

control. All statements, except for statements of historical fact, made in this presentation regarding activities, events or developments AR expects, believes or anticipates will or

may occur in the future, such as those regarding expected results, future commodity prices, future production targets, completion of natural gas or natural gas liquids

transportation projects, future earnings, future capital spending plans, improved and/or increasing capital efficiency, continued utilization of existing infrastructure, gas

marketability, estimated realized natural gas, natural gas liquids and oil prices, acreage quality, access to multiple gas markets, expected drilling and development plans

(including the number, type, lateral length and location of wells to be drilled, the number and type of drilling rigs and the number of wells per pad), projected well costs and cost

savings initiatives, future financial position, future technical improvements, future marketing and asset monetization opportunities, the amount and timing of any contingent

payments, the participation level of our drilling partner and the financial and operational results to be achieved as a result of the drilling partnership, estimated Free Cash Flow

and the key assumptions underlying its projection and AR’s environmental goals are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933

and Section 21E of the Securities Exchange Act of 1934. All forward-looking statements speak only as of the date of this presentation. Although AR believes that the plans,

intentions and expectations reflected in or suggested by the forward-looking statements are reasonable, there is no assurance that these plans, intentions or expectations will be

achieved. Therefore, actual outcomes and results could materially differ from what is expressed, implied or forecast in such statements. Except as required by law, AR expressly

disclaims any obligation to and does not intend to publicly update or revise any forward-looking statements.

In addition, many of the standards and metrics used in preparing this presentation and the ESG Report continue to evolve and are based on management expectations and

assumptions believed to be reasonable at the time of preparation but should not be considered guarantees. The standards and metrics used, and the expectations and

assumptions they are based on, have not been verified by any third party. In addition, while we seek to align these disclosures with the recommendations of various third-party

frameworks, such as the Task Force on Climate-Related Financial Disclosures ("TCFD"), we cannot guarantee strict adherence to these framework recommendations.

Additionally, our disclosures based on these frameworks may change due to revisions in framework requirements, availability of information, changes in our business or

applicable governmental policy, or other factors, some of which may be beyond our control. The calculation of methane leak loss rate disclosed in this release conforms with ONE

Future protocol, which is based on the EPA Greenhouse Gas Reporting Program. With respect to its Scope 1 emissions goal, Antero Resources anticipates achieving Net Zero

Scope 1 emissions by 2025 through operational efficiencies and the purchase of carbon offsets.

AR cautions you that these forward-looking statements are subject to all of the risks and uncertainties incident to the exploration for and the development, production, gathering

and sale of natural gas, NGLs and oil, most of which are difficult to predict and many of which are beyond AR’s control. These risks include, but are not limited to, commodity

price volatility, inflation, lack of availability of drilling and production equipment and services, environmental risks, drilling and other operating risks, regulatory changes, the

uncertainty inherent in estimating natural gas and oil reserves and in projecting future rates of production, cash flow and access to capital, the timing of development

expenditures, impacts of world health events, including the COVID-19 pandemic, cybersecurity risks and the other risks described under the heading "Item 1A. Risk Factors" in

AR’s Annual Report on Form 10-K for the year ended December 31, 2020.

Any forward looking statement speaks only as of the date on which such statement is made and AR undertakes no obligation to correct or update any forward looking statement

whether as a result of new information, future events or otherwise, except as required by applicable law.

This presentation and the ESG Report contain statements based on hypothetical or severely adverse scenarios and assumptions, and these statements should not necessarily

be viewed as being representative of current or actual risk or forecasts of expected risk. These scenarios cannot account for the entire realm of possible risks and have been

selected based on what we believe to be a reasonable range of possible circumstances based on information currently available to us and the reasonableness of assumptions

inherent in certain scenarios; however, our selection of scenarios may change over time as circumstances change. While future events discussed in this presentation or the report

may be significant, any significance should not be read as necessarily rising to the level of materiality of certain disclosures included in Antero Resources' SEC filings

This presentation also includes (i) Free Cash Flow, (ii) Adjusted EBITDAX, (iii) Net Debt and (iv) leverage which are a financial measures that are not calculated in accordance

with U.S. generally accepted accounting principles (“GAAP”). Please see “Antero Non-GAAP Measures” for definitions of these measures as well as certain additional information

regarding these measures.

Antero Resources Corporation is denoted as “AR” in the presentation and Antero Midstream Corporation is denoted

as “AM”, which are their respective New York Stock Exchange ticker symbols.

• Antero Resources | May 2019 Presentation 2

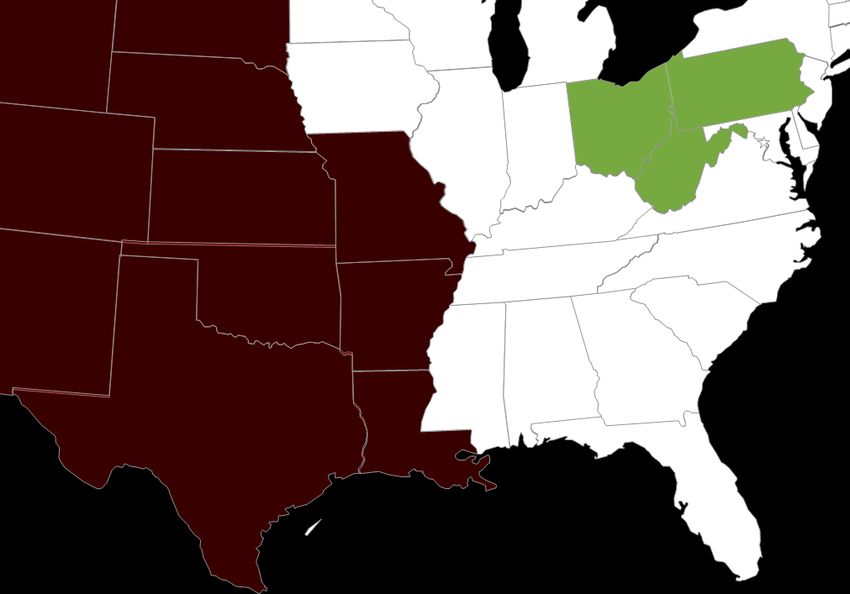

Antero Resources Snapshot Denver, CO Antero Resources Acreage Map HEADQUARTERS Antero Marcellus Rig Industry Marcellus Rig $8.8 B Industry Utica Rig Antero Acreage ENTERPRISE VALUE (1) SW Marcellus Core Ohio Utica Core 5th Largest U.S. GAS PRODUCER (2) 2nd Largest U.S. NGL PRODUCER (2) Own 38% OF CORE LIQUIDS-RICH UNDRILLED LOCATIONS IN APPALACHIA(3) ~950 ADDITIONAL DRY GAS LOCATIONS IN DRILLING INVENTORY (3) Core Liquids-Rich Appalachian $900 MM+ Undrilled Locations(3) Forecast Free Cash Flow in 2021 (4) ) 29% Midstream AR Peers ~38% ~62% AM VALUE HELD BY AR $1.5 B Note: Rigs on map as of 9/30/21, per Rig data. AM value based on 11/01/21 share price. 1) AR share price as of 11/01/2021 and indebtedness as of 9/30/2021. 2) Natural gas and NGL rankings based on 3Q21 reported production. 3) 4) AR drilling inventory as of 12/31/2020. Industry location count based on Antero technical analysis of undeveloped acreage in the core of the Marcellus and Ohio Utica Shales. Free Cash Flow is a Non-GAAP metric. Please see appendix for additional disclosures, definitions, and assumptions. 3

Antero Family at a Glance 50/50 JV Exploration & Gathering & Natural Gas C3+ NGL Production Compression Processing Fractionation Water Delivery & Blending 4

Recent Credit Enhancements Received corporate ratings upgrades from Moody’s and S&P Global to Ba2 and BB, respectively (10/6/21 - 10/8/21) Extended credit facility to 2026, with a borrowing base increase to $3.5 B and lender commitments of $1.5 B (10/26/2021) Letters of credit have been reduced by $127 MM as a result of ratings upgrades and recently released FT capacity (Oct-21) Replaced $80 MM of letters of credit with surety bonds, further enhancing liquidity (10/27/21) Credit Facility + Pro Forma Liquidity Summary $3,500 $3,500 Pro forma 9/30/21 $3,000 liquidity: $2,500 ~$743 MM (1) Borrowing Base $2,000 $1,500 Liquidity Lender $1,000 Commitments Revolver: $222 $500 LCs: $535 $1,500 $0 Revolver Borrowings Credit Facility + LCs 1) Pro forma liquidity represents borrowing availability under AR’s credit facility based on $1.5 B of lender commitments and $535 MM of letters of credit. ~$222 MM of borrowings as of 9/30/2021 pro forma for the redemption of $116 MM of the 2029 Senior Notes at $107.625, plus accrued and unpaid interests. 5

Antero Strategy Evolution Antero’s business strategy has evolved to match the U.S. shale industry life cycle AR Net Production (Right Axis) & Capital Investment (Left Axis) ($MMs) (1) (MMcfe/d) We are $3,500 Production (MMcfe/d) Capital Spend here 4,000 $3,000 3,500 $2,500 3,000 2,500 $2,000 2,000 $1,500 1,500 $1,000 1,000 $500 500 $0 - 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E Shale 1.0 Shale 2.0 Shale 3.0 • Acquire acreage • Grow production • Maintain production • Support infrastructure • Aggressively hedge • Generate Free Cash Flow through long-term • Consolidate acreage • Reduce debt & commitments commitments • Innovate through drilling and • Delineate resource • Sustain low leverage completion techniques • Maintain commodity • Access low cost capital exposure • Optimize FT • Return capital • Prioritize ESG 1) Represents drilling and completion + leasehold capital expenditures. 6

Positioned for Success in Shale 3.0 World Antero is well positioned with a strong balance sheet and differentiated operating leverage to higher commodity prices Peer-leading 6 ESG Performance Supportive 5 Commodity Fundamentals Optimal 4 Takeaway Capacity Deep Liquids-Rich 3 Inventory Sustainable 2 Development and Free Cash Flow Strong 1 Balance Sheet 7

1 Peer Leading Debt & Leverage Reduction Sustainable long-term leverage reduction is achieved only through absolute debt reduction, not just EBITDA expansion in a commodity price upswing Year-over-Year Change in Total Debt (1) $3,000 $2,450 Absolute $2,500 Debt $2,000 $1,793 $1,500 $1,000 $500 $0 EBITDA ($500) ($312) ($224) ($1,000) ($817) AR RRC CNX SWN EQT Y-O-Y LTM EBITDAX Change ($MM) (2) Net Debt to LTM EBITDAX (9/30/2021)(3) $700 $652 3.0x 2.7x 2.8x 2.8x $600 $498 2.0x $500 2.0x $381 1.6x $400 $323 $300 $181 1.0x $200 $100 $0 0.0x SWN AR EQT RRC CNX AR CNX EQT SWN RRC Source: Company public filings and press releases. Note: Please see appendix for additional disclosures, definitions, and assumptions. 1) As of 9/30/2021. Excludes contribution for announced acquisitions not yet closed. 2) 3) Represents year-over-year change in LTM EBITDAX from 3Q 2020 to 3Q 2021. Excludes contribution for announced acquisitions not yet closed. As of 9/30/2021. Excludes contribution for announced acquisitions not yet closed. 8

1 Strong and Sustainable Balance Sheet AR has no near-term senior note maturities and has reset debt levels to insulate leverage against a downside commodity price scenario Antero Resources Debt Term Structure (Pro Forma 9/30/2021) (1) AR Senior Notes $2,000 AR Convertible Notes $1,800 AR Credit Facility Commitments $1,600 $1,400 $1,200 No near-term maturities $1,000 $800 $590 $584 $600 $600 $222 $400 $82 $200 $325 5.00% 8.375% 7.625% 5.375% $0 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 $2.0 Billion Absolute Debt Target is Designed to Limit Leverage in the Event of a Commodity Cycle Downturn 9 Note: Please see appendix for additional disclosures, definitions, and assumptions. 1) Pro forma for credit facility extension to 2026 on October 26, 2021. Pro forma for the redemption of $116 MM of the 2029 Senior Notes at $107.625, plus accrued and unpaid interests.

2 Significant Commodity Price Leverage As one of the largest natural gas and NGL producers in the U.S., Antero has significant cash flow upside in a rising commodity price environment Top 5 U.S. Natural Gas Producers (MMcf/d) Top 5 U.S. NGL Producers (MBbls/d) 6,000 250 5,050 5th largest U.S. Natural 219 2nd largest NGL 5,000 Gas producer 200 producer 159 158 157 4,000 148 150 MMcf/d 2,945 48 3,000 2,728 2,701 Ethane 2,232 100 112 2,000 C3+ 50 NGLs 1,000 - - EQT CTRA SWN XOM AR OXY AR EOG PXD DVN AR Leverage to Natural Gas Prices ($MM) (1) AR Leverage to C3+ NGL Prices ($MM) (2) $450 $450 $407 $407 Every $0.10 per Every $2 per Bbl move $400 $400 MMBtu move in natural in C3+ NGL prices results $350 gas prices results in an $326 $350 $326 in a $81 MM unhedged $300 $81 MM unhedged $300 annual revenue impact (2) annual revenue impact (1) $244 $244 $250 $250 $200 $200 $163 $163 $150 $150 $100 $81 $100 $81 $50 $50 $0 $0 +$0.10 / +$0.20 / +$0.30 / +$0.40 / +$0.50 / +$2.00 / +$4.00 / +$6.00 / +$8.00 / +$10.00 / MMBtu MMBtu MMBtu MMBtu MMBtu Bbl Bbl Bbl Bbl Bbl Note: Natural gas and NGL producer rankings reflect company 3Q21 reports and public filings. 1) Assumes 3Q 2021 natural gas production of 2.2 Bcf/d. 2.2 Bcf/d of AR natural gas volumes are hedged through 2021 at a weighted average of $2.77/MMBtu and 1.2 Bcf/d hedged in 2022 at a weighted average 10 price of $2.50/MMBtu. 2) Assumes 3Q 2021 C3+ NGL production of 112 MBbl/d.

2 Enhanced Free Cash Flow Profile Antero expects to generate over $6.0 B of Free Cash Flow through 2025 Free Cash Flow (Before Changes in Working Capital) ($MM) 2021E – 2025E Free Cash Flow: Free Cash Flow Outspend 10/25/2021 Strip Pricing (1) 5-Year Avg. Strip $7,000 Through YE 2025 NYMEX: $3.75/MMBtu $6,000+ WTI: $68/Bbl $6,000 C3+ NGLs: $43/Bbl $5,000 $4,000 $3,000 We Are Here $2,000 $900+ $1,000 $0 ($1,000) 2018A 2019A 2020A 2021E 2022E 2021E - 2025E Cumulative FCF (5-year strip) Note: Free Cash Flow, which is shown before changes in working capital, is a Non-GAAP metric. Excludes $51 MM contingent payment that was received in 2Q 2021 upon meeting certain volume thresholds. Please see appendix for additional disclosures, definitions, and assumptions. 1) Assumes strip pricing as of 10/25/2021. 2021 strip pricing reflects NYMEX natural gas average price of $3.88/MMBtu, WTI oil price of $68/Bbl and Mont Belvieu C3+ NGL pricing of ~$50/Bbl . 2022 – 2025 strip pricing reflects NYMEX natural gas average price of $3.71/MMBtu, WTI oil price of $68/Bbl and Mont Belvieu C3+ NGL pricing of ~$41/Bbl. 11

2 Well Positioned Financially vs Appalachian Peers Appalachian Leading YTD 2021 Free Cash Flow…(1) ($MM) $700 $612 $600 $500 $400 $324 $300 $200 $143 $84 $100 $0 ($100) ($200) ($300) ($202) AR CNX RRC SWN EQT Drives $600 MM of Absolute Debt Reduction (2) …and Reduces Leverage Well Below Peers (3) ($B) $8.0 12/31/2020 9/30/2021 12/31/2020 9/30/2021 $7.2 6.0x $7.0 5.2x $6.0 5.0x $4.9 $5.0 4.0x 3.5x $3.8 3.1x 3.2x $4.0 2.7x 2.8x 2.8x $3.0 $3.0 $2.7 $3.1 3.0x 2.6x $3.0 $2.4 $2.2 $2.3 2.0x 2.0x 1.6x $2.0 $1.0 1.0x $0.0 0.0x CNX AR RRC SWN EQT AR CNX EQT SWN RRC Source: Company reports. 1) Represents nine months ended 9/30/2021. Please see appendix for additional disclosures, definitions, and assumptions. 12 2) Represents net debt as of 12/31/2020 and 9/30/2021, respectively. Excludes contribution for announced acquisitions not yet closed. 3) Represents net debt / LTM EBITDAX as of 12/31/2020 and 9/30/2021, respectively. Excludes contribution for announced acquisitions not yet closed..

2 Best Positioned to Return Capital in Appalachia Antero currently has the highest Free Cash Flow to Enterprise Value yield (1) and the most advanced debt reduction program among its Appalachian peers 2021E – 2023E Cumulative Corporate FCF Yield vs 1.0x Leverage Threshold 40% (1) 39% Cumulative 2021E – 2023E FCF as % of Enterprise Value 35% Peer 3 AR is projected to achieve ≤1.0x 30% 30% leverage by 1Q 2022 (2) 27% 26% Peer 1 Peer 2 25% 24% Peer 4 20% Consensus Price Forecast (2021E – 2023E) (2): WTI - $66.50/Bbl 15% Henry Hub - $3.81/MMBtu 10% 5% 0% 2023+ 1.0x Net Debt / LTM EBITDAX Note: Represents Factset consensus estimates as of 11/1/2021. 1.0x Net Debt / LTM EBITDAX 1) Free Cash Flow Yield represents consensus cumulative 2021E – 2023E divided by Enterprise value as of 11/1/2021. Current balance sheet data as of 9/30/2021 pro forma for any acquisitions announced to date. 2) Free Cash Flow is a Non-GAAP metric. Please see appendix for more information. Assumes consensus price forecast as of 11/1/2021. 13

3 Peer Leading Premium Core Drilling Inventory Antero’s technical and management teams have performed an extensive update on acreage positions, undrilled locations, well performance and EURs across the basin – Led to division of the SW Marcellus and Ohio Utica into Premium Core and Tier 2 Core acres Premium Core Marcellus Inventory: SW Appalachia Core • ~5,200 undeveloped locations • AR holds ~1,865 locations, or 36% Utica Core Premium Core Utica Inventory: • ~1,100 undeveloped locations • AR holds ~210 locations, or 19% Premium Liquids-Rich Core Undrilled Locations Peers 62% AR 38% Tier 2 Core Marcellus Inventory: • ~1,600 undeveloped locations SW Marcellus • AR holds ~150 locations, or 9% Core Antero Leasehold & Minerals Drilled Wells Notes: AR drilling inventory as of 12/31/2020. Industry location count based on Antero technical analysis of undeveloped acreage in the core of the Marcellus and Ohio Utica Shales. 14

4 Right-Sizing Firm Takeaway Commitments • AR’s under-utilized firm transportation commitments are expected to decline by over 1.0 Bcf/d by year-end 2025, resulting in a >$100+ MM reduction in annualized net marketing expense and an optimized takeaway position to premium demand markets – Released 400 MMcf/d in commitments year-to-date, reducing annual transportation demand fees by $60 MM Firm Transportation (Year-End) AR Gross Residue Gas Forecast BBtu/d 200 MMcf/d, or $45 MM annualized, 4,500 of unutilized Midwest capacity 4,147 rolled off October 2021 Appalachia 4,000 Regional FT 3,757 3,652 3,500 3,377 3,330 3,130 3,000 TCO 2,500 Midwest 2,000 Premium 1,500 FT 1,000 U.S. Gulf Coast 500 Atlantic Seaboard - 12/31/19 12/31/20 12/31/21 12/31/22 12/31/23 12/31/24 12/31/25 Note: Please see appendix for additional disclosures, definitions, and assumptions. 15

4 Diversity of Product & Destination Antero’s liquids-rich strategy and diversified firm transportation portfolio allows it to capture commodity price upside both domestically and internationally Leader in Liquids Production Leader in Premium Natural Gas and Realized Pricing Takeaway and Realized Pricing (2) Liquids Production (MBbl/d) (1) Percent Sold Out of Basin 200 120% 171 AR leaves ~150 MBbl/d 100% of incremental ethane 100% in the gas stream 83% 150 80% 107 104 61% 56% 100 60% 49% 50 40% 50 17 20% - 0% AR RRC SWN EQT CNX AR RRC SWN EQT CNX C2+ NGL Price as % of WTI (1) Price Differential to NYMEX (3) 60% $0.40 $0.28 53% 55% 48% $0.20 50% 45% 45% 43% $0.00 40% 40% ($0.20) 35% ($0.25) ($0.30) ($0.40) 30% ($0.37) 25% ($0.60) 20% ($0.80) ($0.74) AR CNX RRC EQT SWN AR CNX RRC EQT SWN Source: Company presentation and filings. 1) Represents YTD 2021 results as of 9/30/2021. Liquids production includes C2+ NGLs and oil. 2) 3) Based on company disclosure of firm transportation commitments. Represents YTD 2021 results as of 9/30/2021. AR price differential excludes $0.13/Mcf positive impact from 1Q21 WGL settlement. 16

4 FT Protects Basis and Provides Flow Assurance AR’s firm transportation portfolio provides price stability, production flow assurance, and premium pricing vs. Appalachia-dependent producers Antero Basis vs. Appalachia Basis ($/Mcf) (1) (2) Appalachia Differentials Antero Realized Differential Appalchian Average Basis Antero Average Basis AR’s 3Q21 realized price was an $0.30/Mcf $2.00 Since the beginning of 2018, AR had premium to NYMEX vs. an average Appalachian discount of ($0.77)/Mcf Antero Basis access to its entire FT portfolio and has realized an average $0.13/Mcf $1.50 premium to NYMEX over that time • Low volatility, high reliability $1.00 • Premium to NYMEX AR • “Insurance policy” for +$0.13 3Q21: consistent production $0.50 +$0.30 flow • Ability to hedge NYMEX $0.00 Henry Hub index Appalachia ($0.50) 3Q21: ($0.82) ($0.77) Appalachia Basis ($1.00) • High volatility, low reliability ($1.50) • Significant discount to NYMEX ($2.00) • Frequent shut-ins • Less liquid hedge markets Note: Pricing reflects pre-hedge pricing. 1) 2) Reflects discount to NYMEX for Appalachia in-basin pricing at Dominion South & TETCO M2 indices. Represents simple average discount to NYMEX for Antero firm transportation capacity. Includes BTU adjustment for 1100 BTU gas. 17

5 Strong Natural Gas and NGL Price Momentum – Natural gas and NGL prices have strengthened as global demand continues to increase while supply flattens – Propane storage levels at five year lows provide a bullish set up for winter 2021/2022 U.S. Natural Gas U.S. NGLs Supply Supply • The U.S. is forecast to be undersupplied natural gas • U.S. NGL supply remains flat despite high prices as for the second consecutive year in 2021 driven by barriers to entry remain high (ie: capital moderated drilling activity in shale oil basins commitments for processing & infrastructure) • Flat production from gas producers who are • U.S. producer discipline is expected to continue in focused on capital discipline 2022, resulting in an insufficient supply response • Natural gas directed rig counts are ~45% below the • Record setting LPG exports have led to propane peak in 2019, moderating the supply growth outlook inventories 18% below the 5-year average Demand Demand • LNG feedgas demand has increased to over 11 Bcf/d • Resilient domestic and international demand from petrochem and residential/commercial sectors • Mexican exports remain elevated at over 6 Bcf/d • Rising living standards in developing countries, • European natural gas storage is nearing historic particularly in Asia, create an inelastic demand pull lows for this time of year putting upward pressure on LNG pricing Outlook for NGLs • Resilient U.S. demand from higher res/com and • Excess U.S. export capacity incentivizes selling NGL power sectors barrels into premium priced international markets, Outlook for Natural Gas resulting in an undersupplied U.S. market • Bullish – Global demand growth and flat supply has • Bullish - $4.00/MMBtu+ backwardated strip in already driven C3+ pricing from $15/Bbl in 2Q 2020 2022/2023 due to growing demand and flat supply to over $65/Bbl today Sources: October EIA Short Term Energy Outlook, S&P Global Platts estimates and J.P. Morgan Commodities Strategy Team Research. LPG is comprised of NGL components propane and butane. 18

5 Natural Gas Fundamentals Are Strong U.S. production growth has meaningfully slowed and exports have increased dramatically compared to 2018 U.S. Dry Natural Gas Production – Lower 48 (Bcf/d) Jan-20: Dec-22E: 100.0 94.3 Sep-21: Jan-21: 95.6 95.0 Jan-19: 91.6 92.4 90.0 87.9 85.0 Jan-18: 80.0 77.1 Jan-17: 75.0 69.6 70.0 65.0 60.0 U.S. LNG Exports (Bcf/d) Mexico Exports (Bcf/d) 16.0 8.0 14.3 6.8 14.0 12.6 7.0 6.0 12.0 11.0 6.0 5.2 5.0 10.0 5.0 4.4 4.5 8.0 8.0 4.0 6.0 4.6 3.0 4.0 3.1 2.0 2.0 1.0 - - YE YE YE YE YE YE YE YE YE YE YE YE 2017 2018 2019 2020 2021E 2022E 2017 2018 2019 2020 2021E 2022E Source: Point Logic for U.S. dry natural gas production and Platts for LNG exports and NextEra for Mexico exports. Supply and export forecasts as of 11/01/2021. 19

5 2021 Supply/Demand Balance Detail The U.S. is forecast to be undersupplied in 2021 with demand outweighing supply by 1.4 Bcf/d − This backdrop should continue to support higher NYMEX prices − Weather remains a key variable to watch 150 Total Supply 97 93 96 95 95 96 95 96 97 97 98 98 100 Bcf/d 50 0 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Onshore Prod Offshore Prod LNG Imports Canadian Imports Total Supply 150 122 119 Total Demand 115 97 102 100 90 88 89 91 88 83 84 Bcf/d 50 0 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Power Burn Industrial Res Comm Pipe Loss LNG Exports Mexican Exports Total Demand Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Avg. Net (Supply - Demand) (22.0) (29.7) (1.3) 5.5 11.6 8.1 5.9 4.6 12.3 8.9 (4.3) (16.9) (1.4) Source: S&P Global Platts. 20

5 Propane Market Fundamentals A repeat of the same weekly withdrawals as last winter would result in the U.S. ending withdrawal season with only about 16 million barrels in storage, significantly below 5-year minimum storage level U.S. Propane Inventories (MMBbls) 120 2021 injection season projected to end at ~75 100 MMBbls per industry estimates 80 Million Barrels 2020 60 Repeating winter 2021E 2020-2021 weekly 40 2021 20 2022E ...Results in ending withdrawal season at only ~16 MMBbls, 0 or just 5 to 7 days of supply Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 5-Yr Range 2020 5-Yr Avg 2016-2020 2021 Actual 2021 Forecast 2022 Forecast Source: EnVantage Inc. and Energy Information Administration (EIA) as of 10/22/21. 21

5 Propane Export Arb Despite the dramatic increase in domestic propane pricing in 2021, the export pricing arb has remained attractive, and has recently reached a yearly high of +6.25 cents per gallon Propane Export Arb (Cents per Gallon) (¢/Gallon) +7.00 +6.25 +6.00 +5.00 +4.00 +3.00 +2.00 +1.00 +0.00 . Note: Represents U.S. Gulf Coast export Houston closing prices. Includes all shipping fees 22

5 Strategy Transition For Commodity Price Exposure AR’s significant scale, strong balance sheet, commodity product diversity and development program flexibility allows AR to capture commodity price upside AR Hedges as a % of Guided Production at January 1 of Each Year 100% 80% 60% 40% 20% 0% 2014 2015 2016 2017 2018 2019 2020 2021E 2022E 2023E Prudent Hedging Strategy Prudent Exposure Strategy • Single commodity product (dry gas only) • Diversity of product (NGLs & Oil) • Growth mode to achieve scale • Maintenance capital mode to harvest free • Unutilized FT and less flexible capital cash flow budget • Utilized FT and flexible capital budget to • Northeast basis exposure & shut-in risk commodity prices • Near-term maturities • NYMEX exposure & flow assurance • Contango futures prices • Pushed out maturities 4+ years • Backwardated futures prices Note: Percent of production hedged assumes 2021 production guidance and maintenance mode, or flat production thereafter. • Bullish supply / demand fundamentals 23

5 Peer Hedging Comparison Antero has not added any natural gas hedges in ~18 months and is essentially unhedged on its 4Q21 and going forward propane production % Hedged 2022 Total Production and Natural Gas Production (1) % Total Production Hedged % Natural Gas Production Hedged 100% 95% 88% 89% 90% Peer average hedged natural 80% gas production: 80% 74% 70% 70% Peer average hedged total 63% 59% production: 67% 60% 50% 50% 50% 40% 34% 30% 20% 10% 0% AR RRC SWN EQT CNX 24 1) Represents percent of hedged 2022 total production and natural gas production. 2022 production based on consensus production as of 10/27/2021. Hedge positions as of 9/30/2021 for AR, CNX, EQT and RRC based on company filings. Pro forma for any acquisitions announced to date.

6 ESG Momentum Continues Antero’s peer-leading ESG ranking reflects the internal efforts to prioritize ESG performance and disclosures 2025 Goals Progress World Bank Zero Routine Flaring Initiative (1): COMMITMENT TO NO ROUTINE FLARING IN 2021 Project Canary (July 2021): ANNOUNCED PILOT TO PURSUE RESPONSIBLY SOURCED GAS CERTIFICATION 2020 ESG Report (October 2021): MSCI UPGRADE REPORT IS EXPECTED TO DRIVE (August 2021): FURTHER RATINGS UPSIDE BBB ESG RATING 1) Antero has not flared produced natural gas since the infancy of the Marcellus and Utica shale projects in West Virginia and Ohio. 25

6 Social Responsibility and Safety Exported approximately 60,000 Bbls/d of LPG in 2020, including approximately one-third to developing nations Paid approximately $375 million in lease and royalty payments to Ohio and West Virginia land owners Generated and paid property and severance taxes of $112 million in Ohio and West Virginia Invested $26 million on community road improvements Antero Foundation contributed over $682,000 in direct community donations in 2020 Reduced Total Recordable Incident Rate (TRIR) by 35% from 2016 to 2020 Reduced Lost Time Incident Rate (LTIR) by 68% from 2016 to 2020 LPG Export by Destination Community Relations Inquiries Other 67% Developing Tickets Created: 3,006 98% Nations RESOLUTION 33% RATE Tickets Closed: 2,959 26

6 Environmental and Sustainability Leadership Total Direct GHG Emissions and Intensity (CO2e) Thousand Metric Tons Tons/MBOE 3.4 Antero has zero routine flaring of 2.7 457 produced gas and one of the lowest 427 2.3 GHG intensity metrics in the industry 422 2.0 (upstream independents and majors) 398 2017 2018 2019 2020 Methane Leak Loss Rate (1) 1% Industry leading methane leak loss rate – nearly half the industry peer average and well ahead of the ONE 0.28% 0.09% Future cumulative industry 2025 goal 0.05% OF Industry Upstream 2019 OF AR 2020 Target 2025 Sector Target Upstream Sector Avg. Note: Antero has not flared produced natural gas since the infancy of the Marcellus and Utica shale projects in West Virginia and Ohio. 1) The methane leak loss rate is calculated by dividing methane emitted by the methane produced. The methane leak loss rate represented in this presentation conforms with the ONE Future calculation protocol. 27

6 Governance and Gender Diversity 88% of the Board of Directors are independent 43% of independent directors are female Established ESG Committee of Board of Directors Aligned executive compensation with ESG performance & launched ESG advisory council 28

The Antero Investment Opportunity Antero is positioned to deliver sustainable Free Cash Flow, with a peer-leading leverage profile Strong • Leverage at 1.6x and targeting below 1.5x at YE 2021 (1) Balance • Absolute debt reduction of $800 MM in 2020 and over $1.0 B Sheet expected in 2021 Scale and • 2nd Largest NGL Producer in the U.S. Operating • 5th Largest Natural Gas Producer in the U.S. Leverage • Differentiated operating leverage to higher commodity prices Sustainable • $900 MM+ of forecast Free Cash Flow in 2021 (2) • $6.0 B+ of forecast Free Cash Flow 2021 - 2025 (2) Business • Over 2,000 premium undeveloped premium core locations Model • ~$1.07/MMBtu natural gas breakeven price, unhedged (3) • One of the industry’s lowest GHG emission intensity metrics • No routine flaring – very low methane leak loss rate (0.046%) Leading • 84% of produced water generated was reused/recycled in 2020 ESG Metrics • Partner with Project Canary for Responsibly Sourced Gas certification • Goal to reach Net Zero carbon emissions by 2025 1) Leverage is a non-GAAP metric, which represents approximate debt to LTM Adjusted EBITDAX level as of 9/30/2021 2) Free Cash Flow, which is shown before changes in working capital, is a non-GAAP metric. Excludes $51 MM contingent payment received in 2Q 2021 relating to the ORRI transaction. Please see appendix for additional disclosures, definitions, and assumptions. 3) Represents AR internal 2021-2022 weighted average breakeven price and is defined as full cycle pre-tax ROR of 15%. Assume WTI price of $82.81/Bbl and $77.45/Bbl in 2021 and 2022, respectively. Assumes C3+ NGL price of $56.31/Bbl and $52.60/Bbl in 2021 and 2022, respectively. 29

Appendix

Antero Guidance and Long-Term Target Assumptions Long-term Outlook Assumptions 2021 2021-2025 NYMEX Henry Hub Natural Gas Price ($/MMBtu) (1) $3.88 $3.75 NYMEX WTI Oil Price ($/Bbl) (1) $68.26 $68.08 AR Weighted C3+ NGL Price ($/Bbl) (1) $50.53 $43.04 Marcellus Well Costs ($MM / 1,000’ assuming 12,000 ft lateral) $660 / 1,000’ $635 / 1,000’ AR ownership in AM (shares) and annual AM dividend per share (2) 139 MM shares ($0.90/share annual dividend) Current Plan (Maintenance Capital) Assumptions: 2021 2021-2025 Annual Net Production (MMcfe/d) – Net to AR 3,300 – 3,400 Wells Drilled – Net to AR 65 - 70 250 Wells Completed – Net to AR 60 - 65 255 Wells Drilled (Gross to AR/QL) 80 - 85 310 Wells Completed (Gross to AR/QL) 65 - 70 315 Cash Production & Net Marketing Expense ($/Mcfe) (3) – Net to AR $2.33 - $2.40 $2.14 – $2.19 (4) G&A Expense (before equity-based compensation) ($/Mcfe) – Net to AR $0.08 - $0.10 1) Represents Mont Belvieu strip pricing as of 10/25/2021 assuming C3+ NGL component barrel consists of 56% C3 (propane), 10% isobutane (Ic4), 17% normal butane (Nc4) and 17% natural gasoline (C5+). 2) AM dividend determined quarterly by the Board of Directors of Antero Midstream. 3) 4) Includes lease operating expense, gathering, compression, processing, transportation, production & ad valorem taxes and net marketing expense. Excludes cash G&A. Represents average cash production and net marketing expense for 2022 – 2025. Increase in expense is primarily due to increases in commodity pricing, resulting in higher ad valorem and fuel costs. 31

AR Drilling Partnership Announcement (2/17/2021) Announced Drilling Partnership With QL Capital Partners (“QL”), an Affiliate of Quantum Energy Partners • Entered into Drilling Partnership to fund drilling of 60 incremental wells between 2021 and 2024, enabling Antero to fill unutilized firm transportation and achieve LP incentive fee rebates from Antero Midstream • QL will fund 20% of total development capital spending in 2021 and between 15% to 20% of development capital on an annual basis from 2022 through 2024, $500 MM to $550 MM of capital to QL, in exchange for a proportionate working interest percentage in each well spud • QL will pay a drilling carry to Antero if certain return thresholds are achieved • Antero’s net capital spending, wells drilled and completed and net production will remain unchanged from maintenance capital level from 2021 – 2025 in the new development plan 2021 Development Program (1) 2021-2024 Development Program (1) Drilled Completed Drilled Completed 90 85 350 310 315 80 70 70 300 80 65 250 255 70 250 60 65 65 50 60 200 40 150 30 100 20 50 10 0 0 AR Drilling AR Drilling AR Drilling AR Drilling Maintenance Partnership Maintenance Partnership Maintenance Partnership Maintenance Partnership Note: Assumes, among other things, current strip pricing and full participation by QL in the drilling partnership. Please see appendix for additional disclosures, definitions, and assumptions. 1) Drilling Partnership wells represent gross wells to the Partnership. On a net to Antero basis, wells drilled and completed will have no impact to the AR maintenance plan. 32

Continued Operational Momentum 2021 D&C Capital Guidance of $590 MM (net to Antero) • Announced 2021 drilling and completion guidance of $590 MM in 2021, a 20% decrease from 2020 spending • $900+ MM of estimated 2021 Free Cash Flow (1) Reduced Cost Structure • 22% well cost reduction from initial 2020 AFE budget to $635/lateral foot expected in 2H 2021 (2) • >80% of well cost reductions were driven by sustainable process changes and cycle time efficiencies D&C Capital Spending ($MM) Marcellus Well Cost ($/Lateral Foot) (2) $1,600 $1,490 Well Completions $1,200 $1,400 $1,270 $970 $1,000 $1,200 $1,150 $810 $1,000 $800 $715 $675 $660 $635 $800 $735 $600 $590 $600 $400 $400 $200 163 131 125 105 68 (3) $200 $0 $0 2018A 2019A 2020 2020A 2021 (3) Jan-19 Initial Revised 2H 2020 Current 2H 2021 Initial Budget Guidance Budget 2020 AFE 2020 AFE AFE 2021 AFE AFE 1) Free Cash Flow, which is shown before changes in working capital, is a non-GAAP measure. Excludes $51 MM contingent payment expected to be received in 2Q 2021 contingent on achieving certain volume thresholds relating to the ORRI transaction. Please see appendix for additional disclosures, definitions, and assumptions. 2) Well costs include ~$1 MM or ~$80/ft for facilities, pads and road costs per well assuming a 13,000’ lateral. 3) Drilling and completion capital is net to AR with Drilling Partnership and assumes 80% working interest. 2021 well completions based on midpoint of 65 to 70 wells. 33

Attractive Breakeven Well Economics • Antero has some of the lowest natural gas breakeven prices in Appalachia as highlighted in a recent JP Morgan research report – Breakeven gas prices for rich gas producers like AR are actually lower today due to higher liquids prices than assumed by JP Morgan (2) – AR’s internally calculated breakeven natural gas prices for its 2021 and 2022 development program is $0.89/MMBtu and $1.10/MMBtu, respectively (3) 2021-2022 Natural Gas Unhedged Breakevens - 15% ROR Full Cycle Breakeven Prices(1)(2) AR Internal Breakevens Rich Gas Producers (2021) Dry Gas Producers (2021) $3.20 as of 10/29/2021 (3) Rich Gas Producers (2022) Dry Gas Producers (2022) $2.80 $2.63 $2.57 $2.55 $2.50 $2.42 $2.40 $2.40 $2.42 $2.48 $2.40 $2.31 $2.07 $2.00 $2.00 $1.60 $1.20 $1.10 $0.89 $0.80 $0.40 $0.00 COG AR EQT GPOR RRC SWN Breakeven analysis source: J.P. Morgan Equity Research estimates in December 8, 2020 report. 1) Breakeven price is defined as full cycle pre-tax ROR of 15%. 2) 3) JPM breakevens assume average WTI price of $45.22/Bbl and $44.63/Bbl in 2021 and 2022, respectively. JPM assumed Antero C3+ NGL price of $26.67/Bbl and $24.78/Bbl in 2021 and 2022, respectively. AR internal breakevens assume WTI price of $82.81/Bbl and $77.45/Bbl in 2021 and 2022, respectively. Assumes C3+ NGL price of $56.31/Bbl and $52.60/Bbl in 2021 and 2022, respectively. 34

Drilling & Completion Efficiencies Average Lateral Length per Well Lateral Drilling Feet per Day 20,000 18,998 14,000 12,118 18,000 12,000 Achieved February 2021 New 16,000 U.S. Achieved June 2021 10,000 14,000 12,539 12,696 Record 12,000 8,000 6,409 6,984 10,000 6,000 8,000 6,000 4,000 4,000 2,000 2,000 - - Completion Stages per Day Drill Out Feet per Day 6,017 16.0 6,000 13.8 14.0 5,000 12.0 4,098 Achieved March 2020 Drill Out Feet/Day Achieved April 2021 9.9 4,000 3,771 10.0 8.0 8.0 3,000 6.0 2,000 4.0 1,000 2.0 - - 35 Note: Percentage increase arrows for average lateral length per well and drill out feet per day represent change in Marcellus data from 2014 through 3Q2021. Percentage increase arrows for lateral drilling feet per day and completions stages per day represent change from 2020 to 3Q2021.

Natural Gas and NGLs Are Essential Antero plays a critical role in producing reliable energy for consumers 5 Largest U.S. 2 Largest U.S. Natural Gas NGL Producer Producer Natural Gas Natural Gas Liquids (NGLs) Natural gas is a low-cost, low-emission NGLs play an essential role in the domestic and hydrocarbon based fuel that can reduce GHG international industrial, residential, commercial emissions by more than half, as compared to coal and transportation industries Electricity Generation Transportation Heating & Cooking Recyclable food packaging Health Care Products & Industrial & Manufacturing Protective Equipment Source: Natural gas and NGL rankings based on 3Q21 reported production. 36

NGL Price Strength NGL prices remain elevated on an absolute basis and relative to WTI due to sufficient export capacity and resilient global demand AR Monthly Realized C3+ NGL Price $/Bbl AR C3+ Realized Price ($/Bbl) WTI Price % of WTI 11/08/2021 AR Spot C3+ Price: $63.41/Bbl 77% of WTI $90 100% $80 90% WTI Price 80% $70 70% $60 % of WTI 60% $50 50% $40 40% $30 30% $20 20% AR C3+ Price $10 10% $0 0% Source: Bloomberg actuals through October 2021. Forecasted C3+ pricing based ICE pricing and on Antero C3+ NGL component barrel consisting of 56% C3 (propane), 10% isobutane (Ic4), 17% normal butane (Nc4) and 17% natural gasoline (C5+). Assumes blended sales of 50% domestic and 50% international. 37

Strong NGL Price Recovery Domestic and international LPG prices have improved on a relative basis to crude oil, driven by resilient global demand for LPG from petrochemicals and res/comm C3+ NGL Prices & % of WTI (1) Far East Index (FEI) Propane Prices & % of Brent (2) ($/Bbl) (2) ($/Bbl) % of Brent FEI Propane ($/Bbl) % of WTI Mont Belvieu Propane ($/Bbl) FEI Propane Price $70 C3+ Price as 100% $80 as % of Brent 100% Historical MB % of WTI 92% $65 C3+/WTI% 87% 90% 90% $70 84% 83% 5-year avg: 80% $60 79% ~62% 80% $55 77% 80% $60 72% 67% $50 66% 70% 70% 64% 66% 65% 63% $45 $50 60% 58% 60% $40 $40 50% $35 48% 50% C3+ NGL Price FEI Propane Price 40% $30 $30 40% $25 30% 30% $20 $20 20% $15 20% $10 10% $10 10% $5 $0 0% $0 0% Source: ICEdata Mont Belvieu, Far East Index, WTI and Brent strip pricing as of 10/28/2021. 38 1) Based on Antero C3+ NGL component barrel consists of 56% C3 (propane), 10% isobutane (Ic4), 17% normal butane (Nc4) and 17% natural gasoline (C5+). 2) Forecasted C3+ NGLs represent ICEdata Mont Belvieu strip pricing as of 10/28/2021. Forecasted FEI propane represents ICEdata Far East Index propane strip pricing as of 10/28/2021.

Natural Gas Liquids Primer NGLs play an essential role in the domestic and international industrial, residential, commercial and transportation industries Gas Linked Pricing Crude Linked Pricing Iso- Methane Ethane Propane Butane Butane Pentane Natural Gas C2 C3 C4 IC4 C5 Industrial Primary Chemical Residential Industrial All Industrial Transportation Sectors Industrial Commercial, Transportation Chemical Heating, Ethylene Winter Alkylate feed Primary Crop drying, Gasoline blend Power Production Gasoline to produce Uses Commercial, and diluent (For plastics) Blending gasoline Propylene Higher Heating Value 1000 BTU 4000 BTU 39

Focus on Liquids Rich Drilling Antero currently recovers only 30% of the ethane in its rich gas stream while rejecting 70% of the ethane, sending it to pipeline sales in the natural gas stream Antero NGL Barrel Composition (2021 Guidance) Remaining 70% of ethane Natural Gas 1100 BTU Gas stays in natural gas stream Processing and enhances gas BTU Ethane (C2) ~128,000 Bbl/d of C2 50,000 Bbl/d 165,000 Bbl/d C2+ NGLs 1250 BTU Rich Gas AR recovers ~30% of ethane ~115,000 Bbl/d C3+ NGLs in its rich gas stream Ethane ~50,000 Bbl/d 30% of Barrel Propane (C3) 56% Liquids Rich Production C3+ NGLs ~115,000 Bbl/d 70% of Barrel Normal Butane (C4) 17% IsoButane (iC4) 10% Pentanes (C5+) 17% AR’s C2+ NGL Barrel Composition AR’s C3+ NGL Barrel Composition 40 Note: Based on Antero 2021 production guidance. Antero C3+ NGL component barrel consists of 56% C3 (propane), 10% isobutane (Ic4), 17% normal butane (Nc4) and 17% natural gasoline (C5+).

Premium NGL Price Realizations Producer Disadvantaged: Producer Advantaged & Unconstrained: E&Ps in Permian, Rockies, Mid-Con & Bakken Antero Resources in Appalachia AR is the largest C3+ producer with the most international exposure in Appalachia Mariner East Anchor shipper on ME2 FROM ROCKIES Conway Who Captures the Arb at Marcus Hook? Answer: AR and other Appalachian E&P’s • Direct sales to most attractive international (ARA & FEI) & domestic markets • Fixed terminal rates • Local fractionation & marketing to sell purity products in-basin for local demand Results in “Mont Belvieu plus” pricing netbacks captured “at the dock” by AR Mont Belvieu Who Captures the Arb at the Gulf Coast? Answer: Midstream & LPG off-takers (not E&P’s) • No direct E&P access to international markets (i.e. producers only receive Mont Belvieu linked pricing) • No local fractionation to sell marketable purity products in-basin Results in “Mont Belvieu Minus” pricing “before the dock” 41

Balance Capex with Cash Flow – Low Maintenance Capital Antero Average Development Well 3,600 Net Production Rate: 3.4 Bcfe/d Avg. Lateral Length per Well 13,000’ 3,400 Bcfe/1,000’ 2.70 3,200 Replacement Volume 198 Bcfe ~16% of 2022 Volume Wellhead Gas BTU 1265 3,000 Well Cost ($660/ft) $8.6 MM 2,800 2,600 Net F&D Cost $0.288 Mcfe 2,400 C2 Recovery (1) 40% 2,200 Well Spacing 830’ 2,000 First Year Recovery Volumes Gross (Bcfe) 6.05 Net (Bcfe) 5.14 Maintenance Capital Calculation Field and Operating Capital • The average AR rich Marcellus well • Roads produces 3.16 Bcfe net in the calendar • Working interest year when brought online mid-year optimization • Assume new wells average ½ year of • Pad construction costs production Production can be held flat with ~63 wells Maintenance Field $556 MM 198 ÷ 3.16 Capital: Maintenance D&C = 63 Capital Maintenance D&C Capital ~$14 MM 63 $8.6 = $542 MM Note: Maintenance capital is net of VPP transaction. Net F&D cost assumes 85% net revenue interest. Net F&D is a non-GAAP financial measure, see the appendix for more information. 1) Reflects increased ethane volume with start up of Shell Cracker in 2022. Ethane sold at a premium to natural gas price. 42 42

Antero Non-GAAP Measures Adjusted EBITDAX: Adjusted EBITDAX as defined by the Company represents income or loss, including noncontrolling interests, before interest expense, interest income, gains or losses from commodity derivatives and marketing derivatives, but including net cash receipts or payments on derivative instruments included in derivative gains or losses other than proceeds from derivative monetizations, income taxes, impairment, depletion, depreciation, amortization, and accretion, exploration expense, equity-based compensation, contract termination and rig stacking costs, simplification transaction fees, and gain or loss on sale of assets. Adjusted EBITDAX also includes distributions received with respect to limited partner interests in Antero Midstream Partners common units prior to the closing of the simplification transaction on March 12, 2019. The GAAP financial measure nearest to Adjusted EBITDAX is net income or loss including noncontrolling interest that will be reported in Antero’s condensed consolidated financial statements. While there are limitations associated with the use of Adjusted EBITDAX described below, management believes that this measure is useful to an investor in evaluating the Company’s financial performance because it: • is widely used by investors in the oil and natural gas industry to measure operating performance without regard to items excluded from the calculation of such term, which may vary substantially from company to company depending upon accounting methods and the book value of assets, capital structure, and the method by which assets were acquired, among other factors; • helps investors to more meaningfully evaluate and compare the results of Antero’s operations from period to period by removing the effect of its capital and legal structure from its consolidated operating structure; and • is used by management for various purposes, including as a measure of Antero’s operating performance, in presentations to the Company’s board of directors, and as a basis for strategic planning and forecasting. Adjusted EBITDAX is also used by the board of directors as a performance measure in determining executive compensation. There are significant limitations to using Adjusted EBITDAX as a measure of performance, including the inability to analyze the effects of certain recurring and non-recurring items that materially affect the Company’s net income or loss, the lack of comparability of results of operations of different companies, and the different methods of calculating Adjusted EBITDAX reported by different companies. In addition, Adjusted EBITDAX provides no information regarding a company’s capital structure, borrowings, interest costs, capital expenditures, and working capital movement or tax position. Net Debt: Net Debt is calculated as total debt less cash and cash equivalents. Management uses Net Debt to evaluate its financial position, including its ability to service its debt obligations. Leverage: Leverage is calculated as LTM Adjusted EBITDAX divided by net debt. 43

Antero Non-GAAP Measures Free Cash Flow: Free Cash Flow is a measure of financial performance not calculated under GAAP and should not be considered in isolation or as a substitute for cash flow from operating, investing, or financing activities, as an indicator of cash flow, or as a measure of liquidity. The Company defines Free Cash Flow as Net Cash Provided by Operating Activities, less drilling and completion capital and leasehold capital plus earnout payments. The Company has not provided projected Net Cash Provided by Operating Activities or a reconciliation of Free Cash Flow to projected Net Cash Provided by Operating Activities, the most comparable financial measure calculated in accordance with GAAP. The Company is unable to project Net Cash Provided by Operating Activities for any future period because this metric includes the impact of changes in operating assets and liabilities related to the timing of cash receipts and disbursements that may not relate to the period in which the operating activities occurred. The Company is unable to project these timing differences with any reasonable degree of accuracy without unreasonable efforts. See assumptions slide for more information regarding key assumptions. Free Cash Flow is a useful indicator of the Company’s ability to internally fund its activities and to service or incur additional debt. There are significant limitations to using Free Cash Flow as a measure of performance, including the inability to analyze the effect of certain recurring and non-recurring items that materially affect the Company’s net income, the lack of comparability of results of operations of different companies and the different methods of calculating Free Cash Flow reported by different companies. Free Cash Flow does not represent funds available for discretionary use because those funds may be required for debt service, land acquisitions and lease renewals, other capital expenditures, working capital, income taxes, exploration expenses, and other commitments and obligations. 44

Antero Resources Adjusted EBITDAX Reconciliation LTM Adjusted EBITDAX Reconciliation Twelve Months Ended September 30, 2021 Reconciliation of net loss to Adjusted EBITDAX: Net loss and comprehensive loss attributable to Antero Resources Corporation $ (1,018,454) Net income and comprehensive income attributable to noncontrolling interests 1,637 Unrealized commodity derivative losses 1,623,610 Payments for derivative monetizations 13,635 Amortization of deferred revenue, VPP (43,165) Gain on sale of assets (2,479) Interest expense, net 185,036 Loss on early extinguishment of debt 82,239 Loss on convertible note equitizations 50,777 Provision for income tax benefit (313,883) Depletion, depreciation, amortization, and accretion 776,944 Impairment of oil and gas properties 137,426 Exploration expense 6,280 Equity-based compensation expense 21,505 Equity in (earnings) of unconsolidated affiliate (78,369) Dividends from unconsolidated affiliate 148,080 Contract termination and rig stacking 6,278 Transaction expense 3,684 1,600,781 Martica related adjustments (1) (104,419) Adjusted EBITDAX $ 1,496,362 1) Adjustments reflect noncontrolling interests in Martica not otherwise adjusted in amounts above. 45

Antero Resources Adjusted EBITDAX Reconciliation Three Months Ended September 30, Nine Months Ended September 30, 2020 2021 2020 2021 Reconciliation of net loss to Adjusted EBITDAX: Net loss and comprehensive loss attributable to Antero Resources Corporation $ (535,613) (549,318) (1,337,727) (1,088,284) Net loss and comprehensive loss attributable to noncontrolling interests (18,233) (17,257) (17,997) (23,846) Unrealized commodity derivative losses 748,791 834,334 875,811 1,774,410 Payments for (proceeds from) derivative monetizations (18,073) — (18,073) 4,569 Amortization of deferred revenue, VPP (5,175) (11,404) (5,175) (33,833) Loss on sale of assets — (539) — (2,827) Interest expense, net 48,043 45,414 152,956 138,120 Loss (gain) on early extinguishment of debt (55,633) 16,567 (175,365) 82,836 Loss on convertible note equitizations — — — 50,777 Provision for income tax benefit (168,778) (158,656) (421,167) (337,568) Depletion, depreciation, amortization, and accretion 239,533 183,638 655,460 567,113 Impairment of oil and gas properties 29,392 26,253 155,962 69,618 Impairment of equity method investment — — 610,632 — Exploration expense 454 235 895 6,092 Equity-based compensation expense 5,699 5,298 17,001 15,189 Equity in (earnings) loss of unconsolidated affiliate (24,419) (21,450) 83,408 (57,621) Dividends from unconsolidated affiliate 42,755 31,285 128,267 105,325 Contract termination and rig stacking 1,246 3,370 12,317 4,305 Transaction expense 524 626 6,662 3,102 290,513 388,396 723,867 1,277,477 Martica related adjustments (1) (18,072) (30,197) (21,172) (80,436) Adjusted EBITDAX $ 272,441 358,199 702,695 1,197,041 1) Adjustments reflect noncontrolling interests in Martica not otherwise adjusted in amounts above. 46

Free Cash Flow Reconciliation Working capital adjustments in 2021 include $60.5 million in changes in current assets and liabilities and $35.9 million in accounts payable and accrued liabilities for additions to property and equipment. See the cash flow statement in this release for details. Three Months Ended September 30, 2020 2021 Net cash provided by operating activities $ 175,870 312,680 Less: Net cash provided by (used in) investing activities 65,545 (202,577) Less: Proceeds from VPP sale, net (215,833) — Less: Distributions to non-controlling interests in Martica (17,249) (18,755) Free Cash Flow $ 8,333 91,348 Changes in Working Capital (1) 63,305 30,651 Free Cash Flow before Changes in Working Capital $ 71,638 121,999 1) Working capital adjustments in 2021 include $28.3 million in changes in current assets and liabilities and $2.3 million decrease in accounts payable and accrued liabilities for additions to property and equipment. See the cash flow statement in this release for details. 47

Total Debt to Net Debt Reconciliation Total Debt to Net Debt Reconciliation December 31, September 30, 2020 2021 Credit Facility $ 1,017,000 97,500 5.125% senior notes due 2022 660,516 — 5.625% senior notes due 2023 574,182 — 5.000% senior notes due 2025 590,000 590,000 8.375% senior notes due 2026 — 325,000 7.625% senior notes due 2029 — 700,000 5.375% senior notes due 2030 — 600,000 4.250% convertible senior notes due 2026 287,500 81,570 Net unamortized premium (111,886) (28,780) Net unamortized debt issuance costs (15,719) (24,257) Consolidated total debt $ 3,001,593 2,341,033 Less: Cash and cash equivalents — — Net Debt $ 3,001,593 2,341,033 48

You can also read