China's latest Covid symptom: a loss of GDP growth - ING Think

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Economic and Financial Analysis

7 April 2022

Article

China’s latest Covid symptom: a loss of GDP

growth

The cost of China's latest clampdown against Covid, notably in Shanghai, isn't

just limited to its people; the cost to growth is huge. We're going to try to put

a number on it, but we can't give the full picture as the government will

provide stimulus to repair at least some of the economic damage. That said,

we are revising our forecasts

Lockdowns in Shanghai due to Covid-19 are hurting China's overall growth rate

Content

- Covid cases in Shanghai reach another peak

- Our estimate of GDP loss from this round of Covid outbreak in Shanghai

- Other cities are at a risk of similar measures

- Forecast downgrades

Covid cases in Shanghai reach another peak

Shanghai is one of China's major finance, commerce, and trade centres. But right now, its

population is locked down because of surging Covid-19 infections.

Confirmed and asymptomatic cases were 76,000 as of 5th April 2022 in the city, which is 0.3%

of the city's population. This number is big for the country, but more than 85% of cases found in

mass testing are asymptomatic. Right now, the policy is to only release people from lockdown

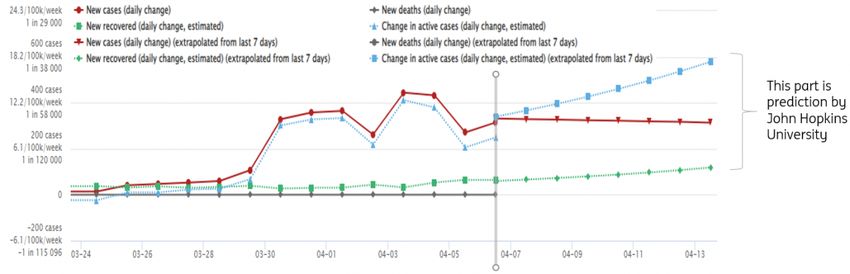

once no more positive cases are found. John Hopkins University estimates the number of Covid cases will continue to climb, mainly among people showing no symptoms. The number could surpass the previous peak on 4th April. In that case, we can assume most locations in Shanghai city will have positive cases, and tests will continue for most of the month. That means GDP activities will mostly be wiped out this month as factories can't operate with any sense of normality. Office work, especially for those in the financial industry, should be fine as most employees can work from home. But it is uncertain whether they can work from isolation facilities as network connections can be poor. Covid cases are predicted to surpass the previous peak Source: John Hopkins University, ING Our estimate of GDP loss from this round of Covid outbreak in Shanghai We estimate that Shanghai will suffer a 6% GDP loss if the current lockdowns persist in this month alone; that's a 2% GDP loss for the whole of China. Remember, the authorities are being incredibly strict. One infected person could affect the whole of a factory's workforce. Ports suspend operations for disinfection if one person is found to have the virus. But that's not the whole picture. The government, both locally and nationally, will deliver relief and stimulus. These measures will be around 1% to 1.5% of GDP. But timing is crucial. The full extent of those measures isn't yet known and we need to see implementation before we can adequately calculate the impact. Measures from central government, such as export tax rebates, can't come too soon. We also expect the People's Bank of China to cut the Reserve Requirement Ratio for small and medium enterprises and to lower interest rates, maybe as early as this month.

China's possible relief measures and stimulus Source: ING Monetary policy projections in 2022 Source: ING Other cities are at a risk of similar measures We need to compare the model of Shenzhen and Shanghai in how they're handling Covid to see what the local government will do next if Covid cases are found in their cities. From the chart, we can see that Shenzhen had a very short lockdown, and the damage to economic activities was not large at all. The difference between Shenzhen and Shanghai is that Shenzhen decided to lockdown even though the number of cases was small. One reason for this is Shenzhen is located next to Hong Kong, and Hong Kong had many cases; the lockdown after mass testing broke the infection link and the city recovered quickly. Shanghai hesitated to go into a full lockdown because it worried about the harm to the economy. But the delay led to an out-of-control situation meaning the harsh restrictions were needed for longer. Comparing the two models indicates that other cities are likely to do mass testing early to avoid Shanghai's harsh predicament. There is, of course, also another possibility and that is to live with Covid. But as we see in Shanghai, that's unlikely not least because hospital capacity is small compared to the size of the population. So far, there are no signs that China is prepared to change tack and deal with Covid as an inconvenience rather than a widespread medical emergency that needs to be

totally eliminated.

Two different stories from the Shenzhen and Shanghai lockdowns

Source: ING

Forecast downgrades

We are revising down China's GDP growth rate to 4%YoY from 5%YoY for the second

quarter of this year after considering the timing of relief measures. GDP growth for

2022 is downgraded to 4.6% from 4.8%.

On any PBoC interest rate cut, we expect a 20bps cut and a targeted RRR cut of 50 bps

for SMEs in 2Q22.

We are keeping the USD/CNY exchange rate forecast at 6.5 for now, but we're

monitoring it closely as the lockdown factor seems to be playing a more important role

now compared to the safe-haven status we saw even just one month ago.

Iris Pang

Chief Economist, Greater China

iris.pang@asia.ing.comDisclaimer

This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. ("ING") solely for information purposes

without regard to any particular user's investment objectives, financial situation, or means. ING forms part of ING Group (being for this

purpose ING Group NV and its subsidiary and affiliated companies). The information in the publication is not an investment recommendation

and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Reasonable care has been

taken to ensure that this publication is not untrue or misleading when published, but ING does not represent that it is accurate or complete.

ING does not accept any liability for any direct, indirect or consequential loss arising from any use of this publication. Unless otherwise stated,

any views, forecasts, or estimates are solely those of the author(s), as of the date of the publication and are subject to change without notice.

The distribution of this publication may be restricted by law or regulation in different jurisdictions and persons into whose possession this

publication comes should inform themselves about, and observe, such restrictions. Copyright and database rights protection exists in this

report and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All

rights are reserved. ING Bank N.V. is authorised by the Dutch Central Bank and supervised by the European Central Bank (ECB), the Dutch

Central Bank (DNB) and the Dutch Authority for the Financial Markets (AFM). ING Bank N.V. is incorporated in the Netherlands (Trade Register

no. 33031431 Amsterdam). In the United Kingdom this information is approved and/or communicated by ING Bank N.V., London Branch. ING

Bank N.V., London Branch is deemed authorised by the Prudential Regulation Authority and is subject to regulation by the Financial Conduct

Authority and limited regulation by the Prudential Regulation Authority. The nature and extent of consumer protections may differ from

those for firms based in the UK. Details of the Temporary Permissions Regime, which allows EEA-based firms to operate in the UK for a limited

period while seeking full authorisation, are available on the Financial Conduct Authority’s website. ING Bank N.V., London branch is registered

in England (Registration number BR000341) at 8-10 Moorgate, London EC2 6DA. For US Investors: Any person wishing to discuss this report or

effect transactions in any security discussed herein should contact ING Financial Markets LLC, which is a member of the NYSE, FINRA and SIPC

and part of ING, and which has accepted responsibility for the distribution of this report in the United States under applicable requirements.You can also read