CFA Institute Research Challenge - CFA Society of Thailand Thammasat University Hosted by - CFA Institute ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CFA Institute Research Challenge Hosted by CFA Society of Thailand Thammasat University

Industry: Property Construction Thammasat University Student Research Sector: Construction Material This report is published for educational purposes only by students competing on the CFA Institute Research Challenge. DYNASTY CERAMIC PCL Date: 21/12/2014 Current Price: THB 55.75 Target Price: THB 41.50 Ticker: DCC (SET) USD 1.00: THB 32.85 Recommendation: SELL (25.6% Downside) Company Overview Investment Highlights Founded in 1989, Dynasty Ceramic PCL We place a “SELL” recommendation. Despite the high Return on Equity (“ROE”) and solid financial (“DCC” or the “Company”) is one of the position, the absence of future growth opportunities as well as the intensifying competition largest tile manufacturers and distributors of ceramic tiles in Thailand. Listed on the implies that past stellar performance is unlikely to repeat again. With our valuation using Stock Exchange of Thailand in 1992. As of Dividend Discount Model (“DDM”) and Free Cash Flow to Firm (“FCFF”) model, the one-year December 2014, DCC operates 195 outlets target price is THB 41.50, which leads to our final recommendation. nationwide targeting low-to middle-income Limited ability to drive sales through store expansion leads to greater reliance on same store customer segments mainly in provincial areas. sales growth: With 195 stores covering almost all 77 provinces throughout Thailand, the Company is likely to experience difficulties in expanding its branch network. The declining trend DCC Relative to SET Index in the number of new stores opened annually from 10 stores in 2012 to only 4 stores in 2013 15% indicates deteriorating expansion opportunity. In fact, in year-to-date 2014, 1 store was closed 10% 5% while no stores were opened. This reflects management’s failure to meet the initially set 5 new 0% stores. Even in the scenario in which the company successfully achieves the expansion target, the -5% -10% impact on top line would be immaterial because of the current large store network. Going -15% forward, DCC is unlikely to achieve substantial growth of its existing business purely through -20% opening new stores as it used to experience in the past. Aug-13 Dec-13 Oct-13 Feb-14 May-14 Jul-14 Aug-14 Nov-13 Jan-14 Apr-14 Oct-14 Nov-14 Sep-13 Mar-14 Jun-14 Sep-14 Weak economic outlook implies low potential to boost same store sales: DCC’s main target DCC SET market is in upcountry areas, where the demand is closely tied to the agricultural products. With Source: Bloomberg the continuous declining in both farm income and agricultural price index by -7.7% YoY and -7.2% YoY in 3Q2014, the recovery of sales growth appears difficult. In addition, the level of DCC VS. SET Holding Period Return household debt has reached the record high of 84% of Thailand’s GDP, as of June 30, 2014. This Time horizon SET DCC can potentially slowdown house renovation market which is DCC’s key market. Combining these 1-year 26.63% 21.23% unfavorable macroeconomic indicators, the turnaround of same store sales growth is unlikely to 3-year 71.08% 9.36% take place in the near future. 5-year 160.02% 145.57% Intensifying competition adds risk to future growth prospect: The lower cost of imported tiles, Source: Bloomberg especially from China and Vietnam, has incentivized both local tile manufacturers and other home improvement retailers to outsource the production activities. It allows importers to sell their High ROE is offset by high P/BV products at 10-15% below market Average Selling Price (“ASP”). As a result, tiles imported value ROE has been increasing with the CAGR of 28% during 2009 to 2013. In addition, other competing (%) DCC TB 50.00 home improvement retailers, namely Global House and Thai Watsadu, have aggressively Average expanded their stores in both urban and provincial areas with number of stores increasing from 40.00 12 to 66 stores within last 5 years. The competitive advantage of DCC as being a low-cost 30.00 manufacturer and having the extensive store network is now being threatened. This changing SCC TB Average competitive landscape reflects in a gradual decrease in DCC market share from 24% in 2009 to 20.00 TTC VN 21% in 2013. DCC’s sales volume continues declining from -4.9% in 2013 and -5.2% in 2014. TGCI TB 10.00 GLOBAL TB Future plan to grow remains questionable: After domestic sales saturates, the clarity of the 0.00 next growth strategies is crucial to drive DCC forward. At the moment, international expansion 0.00 2.00 4.00 6.00 8.00 10.00 seems to be very attractive. However, the management has decided to put the expansion strategy P/BV (Times) Note: The label represents Bloomberg ticker on hold due to many uncertainties and risks involved. Therefore, the international expansion is Source: Bloomberg expected not to happen in the near future. An absence of the next growth engine makes DCC become less attractive. Relative DCC Peers Relative Valuations also indicate overprice for no growth company: The indicative valuation Multiples Average multiples obtained from the relative valuation, covering both local and regional comparable P/E 18.90 14.51 companies further confirms that DCC’s stock price is not justified by its growth outlook. Although PEG 7.43 3.00 DCC’s P/E ratio of 18.9x is considered in line with peers’ average P/E ratio at 14.5x, when the P/B 8.58 2.30 EV/EBITDA 13.68 10.17 Company’s growth is incorporated into multiple analysis, DCC’s PEG ratio of over 7.4x is, in fact, significantly higher than peers’, which is only 3.0x. With the expected growth rate of 2-3% per Source: Bloomberg and Team’s Estimates annum, the results from all valuation methods confirm that the current price of THB 55.75 per share is overvalued. Market Profile 52 weeks price range Key Financial Ratios 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F (THB/share) 48-61 Sales Growth 5.5% -0.7% -4.4% 2.4% 2.8% 2.4% 2.4% 2.3% Average daily volume (Shares) 306,100 Beta 0.57 Earning per Share Growth 1.8% 2.6% -7.9% 3.6% -2.8% -8.9% 21.5% 22.6% Dividend yield 5.76% Gross Profit Margin 39.2% 41.1% 40.5% 40.5% 40.5% 40.5% 40.4% 40.3% Market capitalization (Mn THB) 23,358 Net Profit Margin 16.7% 17.2% 16.6% 16.6% 16.5% 16.4% 16.3% 16.2% Share outstanding (Mn Shares) 408 Free float 36.07% Return on Equity 45.8% 46.8% 43.1% 43.5% 44.4% 45.0% 45.7% 46.3% Foreign limit 35.00% Debt-to-Equity Ratio 0.30 0.43 0.47 0.54 0.61 0.63 0.65 0.65 Source: Bloomberg Earning per Share (THB) 3.08 3.18 2.93 2.99 3.06 3.12 3.18 3.23 1

Figure 1: Sales by distribution channels Export Business Description Franchise 2% Real Estate 3% Founded in 1989, Dynasty Ceramic Public Company Limited (“DCC” or the “Company”) is one Developers 10% of the largest ceramic tile manufacturers in Thailand. The Company manufactures and sells a great variety of ceramic wall/floor tiles as well as other tile-related products under its own brands Home (Appendix 1 & 2). DCC targets low to lower-middle income customer segments mainly in Improvemen provincial areas. The Company distributes its products through various sales channels; however, Outlet Stores t Centers 67% the main sales channel is DCC’s own outlet stores (Figure 1). As of December 2014, DCC has 195 18% outlet stores located nationwide and 2 factories in Saraburi with total annual production capacity of 69 Mn sq.m. In June 2014, DCC has conducted a group restructuring by Entire Business Transfer of three of the Source: Company Data and Team’s Estimates, Company’s subsidiaries, with an intention to reduce interrelated work process and general and Average 9M2014 administrative expenses, leaving Tile Top Industry Public Co., Ltd as DCC’s only subsidiary company with 97% controlling stake (Appendix 3). Product Types Description Low-price products 16x16” tiles and smaller Company Strategies High-price Hybrid and rectified products 16x16” tiles and larger Product line extension: Aiming to capture the higher market segment, DCC has recently launched the high-price products, i.e. Digital and larger-sized tiles. And to further ensure the success of new Figure 2: Average selling price and market penetration, DCC has been renovating its outlet stores hand-in-hand with the launch of sales contribution by product types new products. THB/Sq.m 225 88% 12% Distribution channel expansion: DCC has been continuously expanding through its new outlet 200 stores. This allows the Company to further reduce its reliance on other distributors. However, after the slowdown in sales from outlet stores, it also aims to expand the distribution channels by 175 187.7 focusing on other markets such as; new home market, wholesale, and construction projects in 150 Overall ASP order to expand its customer base. Nevertheless, this might still be questionable whether it is 125 136.9 going to benefit DCC enough because it may lead to the decrease in margin and increase in 128.2 accounts receivable days. 100 Low-price products High-price products Cost reduction: In order to achieve gross margin target of 43% in 2014, DCC has been trying to ASP Sales Contribution reduce the cost of production. Both natural gas and chemicals, the main cost components (Figure Source: Company data and Team’s estimates, As of September 2014 3), were reduced through the production process adjustments. In addition, the company also improves kilns in order to increase the production efficiency and capability. Figure 3: Cost structure Shareholders Structure Others The Saengsastra family and some of the Board of Directors (“BOD”) own and control 47% of total Gas 27% 30% common shares. Other major shareholders are institutional and individual investors who own 17% (Figure 4). As of December 19, 2014, free float is accounted for 36% with the daily turnover rate of 0.075% or 306,100 shares per day. Labor 7% Chemicals Corporate Management Materials 16% 20% Mr. Roongroj Saengsastra became the Chairman of DCC since 2001 (Appendix 4). Under his leadership, the Company has been going through many strategic changes, expanding its own Source: Company data, As of September 2014 outlet stores, and has built up its scale to become the leader in tiles manufacturing business. Figure 4: Shareholders structure DCC’s operating performance has improved significantly with earning growth stands at approximately 14% CAGR since year 2008. Despite well-planned business strategy, the management has failed to achieve their plan. This can be proved by the under-targeted number of new outlet stores opened over the past years. Public Saengsastra 36% Family & Board of directors Corporate Governance and Social Responsibility 47% Corporate Governance Other major shareholders 17% DCC has been implementing good corporate governance practices by organizing its Code of Conduct to fight against corruptions as well as verifying its working procedure to be in Source: Company data, As of November 2014 accordance with established corporate governance policies. Apart from the Annual General Meeting, the Company regularly holds the Opportunity Day and company presentation, in order Figure 5: Corporate governance score to keep investors and other concerned parties being updated. However, we observe that recently ranking among listed companies the Company provides less information in detail than before causing more difficulty for investors No. of Cumulative to analyze the company data. DCC is a family-run company, with 3 out of 9 seats in BOD come Rating companies ranking from Saengsastra family aligning with the management positions and shareholders structure. The Excellent 29 29 rest of BOD are professionals and independent directors. In terms of CG rating, DCC has been Very good 108 137 Good 171 308 evaluated as “Good” by Thai Institute of Directors Association (Appendix 5). This rating Satisfactory & below 242 550 represents the average CG rating score of all companies listed on SET index (Figure 5). Total 550 550 Source: Thai Institute of Directors Association (IOD), As of December 2014 2

Figure 6: Quarterly GDP and Growth Corporate Social Responsibility GDP Growth DCC has been actively seeking opportunities to give back to the society. The Company has (Bn THB) (% YoY) 1,300 30 organized the official committee and set rigorous policy towards becoming a socially responsible 1,250 19.1 20 company. DCC initiated various CSR activities aiming to improve the local community such as 1,200 1,150 2.9 2.7 10 donating tiles to rural schools and sponsoring vocational training session to prisoners. 1,100 0.6 -0.5 0.4 0.6 3.1 5.4 0 1,050 1,000 -10 Industry Overview and Competitive Positioning Quaterly GDP GDP Growth (YoY) Macro-economic Analysis Source: National Economic and Development Board The overall Thai economy is still under pressure Figure 7: Debt Service Ratio by Income DSR (%) The GDP growth is forecasted to be 1.5%-2% in 2014 and 3.5%-4.5% in 2015 resulted from a 60 49 slower-than-expected economic recovery. In order to achieve the forecast of 2014, it will require 50 40 29 25 23 23 Average a substantial growth of approximately 7% in 4Q2014, which tends to be unachievable by many 30 DSR constraints (Figure 6). First, Thai exports is experiencing a low growth due to vulnerable global 20 28 economy. Manufacturing Production Index (MPI) is still at low level indicating by -3.9 in 10 0 3Q2014. Moreover, government policy to stimulate economy has still not been taken into action as much as targeted. Currently, there is only THB 55 Bn from the total budget of THB 365 Bn Household being injected into the system. Income (THB/month) Source: SCB Economic Intelligence Center, As of Vigorous recovery of household consumption is unlikely October 2014 Household debt is already at high: Household debt has been continuously expanding in terms of Figure 8: Change in Farm Income Index both absolute and relative. In 2Q2014, the most recent updates, household debt had increased to and Agricultural Price Index 84% of GDP which is accumulated up to the all-time-high of THB 10bn with a growth of 8.1% YoY. (Appendix6). At this level, low-income people are crucially in concern, due to lower debt % YoY 5 3.3 repayment ability indicated by high debt service ratio (Figure 7). 1.2 2.9 0 -0.8 Agricultural prices remain at low level: Thailand is now facing low agricultural product prices, 0.9 -4.6 -3 particularly the main products: such as rice, rubber, and palm oil. Each contributed to a drop in -0.9 -5 -4 overall agricultural price index. This has caused an effect to more than 30% of Thai labor that are -7.2 farmers. The problem is crucially driven by market mechanism, an oversupply, and the -7.1 -6.9 -6.9 -7.7 -10 competition from other countries. This low price level has caused a direct effect to farm income 1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014 3Q2014 that had experienced a slump of -7.7% YoY in 3Q2014 (Figure 8). Farm Income Index Agricultural Price Index Stagnant Consumer Confidence Index (“CCI”) signals weak purchasing demand: After a Source: Office of Agricultural Economic continuous increase in CCI, it has ceased in 3Q2014 and remains at around 80. This number below 100, the 125th consecutive month, indicates outlook of overall economic directions that has Figure 9: Stable Consumer Price Index not yet been fully recovered (Figure9). 90 85 80.1 79.2 These unfavorable economic indicators are expected to lessen the purchasing power of low- 80 75 71.5 69.9 68.8 78.2 80.178.9 income people who are DCC’s main target customers. This could also pass on the pressure to 70 75.1 home renovation market, since it is not a daily necessary cost. Thus, the sales turnaround 70.7 65 67.8 will be difficult to achieve (Appendix 7). 60 55 50 Industry Analysis In the ceramic tile industry, there are six key domestic players including DCC competing head-to- Source: University of Thai Chamber of Commerce head with one another in terms of design, brand presence, and price (Appendix 8). DCC, however, positions itself as the leader in low-price market and is able to gain the largest share based on Figure 10: Increasing in imported tiles domestic sales. The barrier to entry is relatively high, as the business requires large amount of market value capital investment (Appendix9). Also, the industry seems to be matured with slightly growth and Bn THB 10 8.7 limited demand. On the other hand, the competition within the industry itself has become more 7.3 intense after a coming of imported tiles, mainly from China and Vietnam. These tiles are being 8 sold at highly competitive selling price. 6 5.3 4.8 4 3.3 Industry Highlights 2 Low demand for tiles resulted from a slowdown in property sector: The property sector is - expected to encounter a downward trend reflected by the decline in number of approved 2009 2010 2011 2012 2013 construction areas by 1.5% YoY in 9M2014. This is caused by the massive amount of unsold Source: The Customs Department and Team’s properties from real estate boom in 2012-2013. Also, slow recovery of overall economy will likely Estimates to pass on pressure to new project developments. Hence, we see a direct negative effect on DCC’s sales to developers. More intense competition highlighted by imported tiles and house brand: The industry can observe the growing trend of imported tiles from low-cost producers in China and Vietnam. The tiles are imported and sold by local manufacturers and modern trades under house brand. With an average selling price of THB 125 per sq. m. compared to those local ones of THB 137 per sq. m., these imports have been gaining the market share from 13% in 2009 to 24% in 2013 (Figure10). This implies that the overall domestic tile market has been growing on an expense of the local 3

manufacturers including DCC. Moreover, modern trade, especially specialty store, has been continuously growing by 4.5% in 1H2014 despite the economic slowdown. This is considered as a threat to DCC due to a change in competitive landscape and a difficulty to attract customers to shop at DCC outlet stores (Appendix 10). Figure 11: Domestic Manufacturers Competitors Analysis Market Share by Sales Local Tiles Manufacturers RCI-Rci TGCI- 4% Campana The Siam Cement (SCC): SCC has introduced its tiles into the market under the brand “Cotto” Casa 9% with premium quality aiming to capture middle-to-high income people. After an investment in DCC- Dynasty Prime Group Ceramic, the production capacity could reach over 100 Mn sq.m. per year, 28% UMI- Dulagres comparing to 69 Mn sq.m. of DCC. With the leading position of premium tiles of SCC, the strategy 14% of DCC to expand product line to capture high-price is crucially hardened. SCC-Cotto Sosuco Ceramics: Sosuco is one of the leading tiles manufacturers with a strategy to retain its top SOSUCO 28% 17% 3 domestic market shares and increase proportion of exports. Currently, the company has an annual production capacity of 58 Mn sq.m. Sosuco offers wide range of product to broad customer segments, which could potentially be a threat to DCC. Source: Company Data Union Mosaic Industry (UMI): UMI is one of the key players in local tiles manufacturer market with the tiles product being sold under the brand “Duragres”. The company can produce up to 16.8 Mn sq.m. per year. For the distribution, it is mainly focusing on agents. Even though UMI does not own any outlet stores, the threat to DCC could be in terms of targeted customers. Previously, UMI has bought a stake in TT Ceramic, allowing the company to expand its product lines to cover all segments including low-price market. With an active strategy, UMI could share the pie and pass on pressure on future DCC’s sales. Thai-German Ceramic Industry (TGCI): TGCI is considered a direct competitor to DCC since both their product offerings and target customer segment are exactly the same. The only difference is that TGCI distributes the tiles mainly to agents under the brand “Casa” and “Campana”; whereas DCC mainly distributed via its own outlet stores. For the capacity, the tiles could be produced up to 20 Mn sq.m per year. Royal Ceramic Industry (RCI): The tiles product of RCI includes glazed tiles, clayed tiles and porcelains with an aim to capture middle-income people. Currently, the company distributes the tiles through agents and own only 2 outlet stores. For the production side, it could reach the maximum level of only 6.8 Mn sq.m. per year. By combining low capacity and different target customer, RCI could pass on a minimal effect on DCC. High Note: size represents the COTTO production capacity and (SCC) color represents the level DCC of threat to DCC Target UMI SOSUCO Aiming to capture RCI High Low Market middle-to-high segment TGCI Low DCC Own retail stores Dealer / modern trade Concentration of Distribution Channel Source: Team’s Estimates Figure 12: Number of stores and sales Local home improvement retailers growth (2014F) Siam Global House (GLOBAL): Global House operates as a building materials and home Number of Sales Growth Stores (2014F) improvement retailer, with 27 branches located most in North-East of Thailand. The company DCC 195 -4.40% mainly targets home contractors and homeowners. The growth of GLOBAL would adversely affect DCC as the Company is planning to increase sales from developers. GLOBAL 27 16% Thai Thai Watsadu: The company offers wide variety of products relate to construction materials. It 39 15-20% Watsadu targets a range of customers such as real estate contractors and homeowners with total of 39 Source: Company Data, Team’s Estimates, branches concentrate largely in Central and North-East of Thailand. The company also imports Finansia Syrus Research tiles and sells under its own house brand. Both store expansion and house brand would be a threat to DCC that mainly sell the products through its own outlet stores. 4

Figure 13: DCC failed to meet target Investment Summary expansion plan # Stores We place a “SELL” recommendation. Despite the high Return on Equity (“ROE”) and solid financial 20 15 15 position, the absence of future growth opportunities as well as the intensifying competition 15 13 12 10 10 implies that past stellar performance is unlikely to repeat again. With our valuation methods of 10 7 7 5 5 Dividend Discount Model (“DDM”) and Free Cash Flow to Firm (“FCFF”) model, the one-year 4 5 0 target price is THB 41.50, which leads to our final recommendation. 0 2009 2010 2011 2012 2013 2014F Limited ability to drive sales through store expansion leads to greater reliance on same store Target Actual sales growth: With 195 stores covering almost all 77 provinces throughout Thailand, the Source: Company Data and Team’s Estimates Company is likely to experience difficulties in expanding its branch network. The declining trend in the number of new stores opened annually from 10 stores in 2012 to only 4 stores in 2013 Figure 14: Declining sales volume and indicates deteriorating expansion opportunity. In fact, in year-to-date 2014, 1 store was closed growth (In Thousands Sq.m.) while no stores were opened. This reflects management’s failure to meet the initially set 5 new 60,000 20.0% stores (Figure13). Even in the scenario in which the company successfully achieves the expansion 58,000 target, the impact on top line would be immaterial because of the current large store network. 10.0% 56,000 Going forward, DCC is unlikely to achieve substantial growth of its existing business purely 54,000 0.0% through opening new stores as it used to experience in the past. 52,000 50,000 -10.0% Weak economic outlook implies low potential to boost same store sales: DCC’s main target 2011 2012 2013 2014E market is in upcountry area, where the demand is closely tied to the agricultural products. With Total Sales volume (LHS) the continuous declining in both farm income and agricultural price index by -7.7% YoY and - YoY Volume growth (RHS) 7.2% YoY in 3Q2014, the recovery of sales growth appears difficult. In addition, the level of Source: Company Data household debt has reached the record high of 84% of Thailand’s GDP as of June 30, 2014. This can potentially slowdown house renovation market which is DCC’s key market. Combining these Figure 15: Higher sales contribution from unfavorable macroeconomic indicators, the turnaround of same store sales growth is unlikely to high-price product take place in the near future (Figure 14). 30 138 140 137 135 136 Product line extension has little impact on profit: The launch of high-price products confirms 134 133 136 20 the weak market conditions in low-price market segment. Despite higher contribution of high- 14 132 13 price product sales from 9% in 1Q2014 to 14% in 3Q2014, the ASP of the Company has not 9 10 7 128 picked up as expected to reflect the higher contribution of such product sales. In addition, during 4.3 4.7 124 the same period, overall gross margin remained flat at 40%. Thus, we believe that DCC’s ongoing 0 120 efforts in promoting its high-price products are unlikely to have immaterial impact on overall profitability of the Company (Figure 15). ASP (RHS) Sales contribution from high-end product (LHS) Intensifying competition adds risk to future growth prospect: The lower cost of imported tiles, especially from China and Vietnam, has incentivized both local tile manufacturers and other home Source: Company Data improvement retailers to outsource the production activities. It allows importers to sell their products at 10-15% below market Average Selling Price (“ASP”). As a result, tiles imported value has been increasing with the CAGR of 28% during 2009 to 2013 (Appendix 11). In addition, other Figure 16: Declining DCC market share competing home improvement retailers, namely Global House and Thai Watsadu, have through 2019 aggressively expanded their stores in both urban and provincial areas with number of stores % 22 increasing from 12 to 66 stores within last 5 years. The competitive advantage of DCC as being a 21 low-cost manufacturer and having the extensive store network is now being threatened 20 (Appendix 12-14). This changing competitive landscape reflects in a gradual decrease in DCC -2.2 18 -0.5 markets share from 24% in 2009 to 21% in 2013 (Figure 16). DCC’s sales volume also continues -0.6 16 -0.7 15.2 declining from -4.9% in 2013 and -5.2% in 2014. -0.8 14 Future plan to grow remains questionable: After domestic sales saturates, the clarity of the 12 next growth strategies is crucial to drive DCC forward. At the moment, international expansion 10 seems to be very attractive. However, the management has decided to put the expansion strategy 2013 2014F 2015F 2016F 2017F 2018F 2019F on hold due to many uncertainties and risks involved. Therefore, the international expansion is Source: Kasikorn Research Center, Team’s Estimates expected not to happen in the near future. An absence of the next growth engine makes DCC become less attractive Figure 17: Market recovery from Relative Valuations also indicate overprice for no growth company: The indicative valuation Thailand’s political unrest multiples obtained from the relative valuation covering selected comparable companies further 15% confirms that DCC’s stock price is not justified by its growth outlook. Although DCC’s P/E ratio of 10% 5% 18.9x is considered in line with peers’ whose average P/E ratio currently stands at 17.0x, when 0% the Company’s growth is incorporated into multiple analysis, DCC’s PEG ratio of over 7.5x is, in -5% -10% fact, significantly higher than peers’ whose average PEG ratio is only 3.5x. With the expected -15% growth rate of 2-3% per annum, the results from all valuation methods confirm that the current -20% price of THB 55.75 per share is overvalued. Aug-13 Dec-13 Feb-14 Apr-14 May-14 Jul-14 Aug-14 Oct-13 Nov-13 Jan-14 Oct-14 Nov-14 Sep-13 Mar-14 Jun-14 Sep-14 Low beta does not lead to expected diversification benefit: Despite DCC’s low beta of 0.57 DCC SET relative to SET Index, we found the high discrepancy between the beta during the bullish market Source: Bloomberg 5

(0.48) and that during the bearish one (0.73). This indicates that DCC has limited upside during the bullish period and yields low diversification benefit in the bearish market (Figure 17), just simply the time when the investors need such benefit most. Thus, DCC might not be a good investment choice for investors who want to reduce their portfolio risk through diversification (Appendix 15). Event Analysis Share Price (THB) 80 Household debt reached to 84% of GDP 70 First announced 100% 60 dividend payout 50 50% Decrease in natural 40 gas price during Continuous drop 30 Sept 08- May 09 in agricultural Thailand Great product price 20 Flood 10 0 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 DCC stock price significantly skyrocketed in year 2008-2011 due to the huge drop in natural gas price, the continuous store expansion, and the announcement of 100% dividend payout. The great flood in Thailand was also a big event that drove the demand in home improvement market in 2011. However, in recent years the stock price has been sideway reflecting the impact from consumption problem in low-price segment e.g. household debt and the huge drop in agricultural product price. Valuation As a single business company with stable cash flow streams, we use Discounted Cash Flow (DCF) method in arriving the target price for DCC. The Company is perceived as a dividend stock from investor perspectives since it has been consistently paying stable and high dividend with the payout ratio of 100%. Hence, Dividend Discount Model (DDM) is used for the valuation of DCC. However, to better reflect intrinsic value of the Company, we also include Free Cash Flow to Firm (FCFF) method in our valuation in order to capture the controlling aspect of the largest group of shareholders, the family owner and the board of directors. Five-Year Projected Cash Flow Assumptions Figure 18: Sales growth drops during the forecast period Expected decline in sales growth: Sales for DCC is forecasted by distribution channel, with ASP Mn THB and volume as the key drivers. 12,000 CAGR Outlet Sales: DCC’s main revenues are from sales through its own outlet stores, 10,000 1.29% approximately 70% of total revenue, which are driven by expected number of stores 8,000 8.20% and same store sales for each region. The assumptions are estimated based on economic 6,000 outlook and store coverage in the areas. As the store expansion opportunity becomes 4,000 limited and higher competition is expected, we estimate the SSS to slightly decline. 2,000 Other distribution channels: Selling prices are discounted by 3-5% from the outlet - selling prices. We expect 1-4% growth of sales volume for wholesale customers such as 2008 2013 2019F home improvement retailers and real estate contractors. Source: Company Data and Team’s Estimates With all factors combined, sales growth is estimated to drop to 1.29% CAGR during the forecast period, compared to 8.20% in the past five years (Figure 18). Figure 19: COGS driven by Gas price Millions THB/M Costs of production driven by natural gas price: Cost of goods sold (COGS) consists of three THB MBTU main components: Natural gas cost, other variable costs and fixed costs. Natural gas is the main 6,000 500 cost of production with approximately 30% contribution to the total cost. It is calculated from (1) 5,000 400 Natural gas usage per unit, which is expected to remain constant at 0.06 MMBTU per sq.m. and 4,000 300 (2) Natural gas price per MMBTU, expected to increase by 3.5% annually (Figure 19). 3,000 2,000 200 Net profit grows slower than sales: Other income and SG&A expenses are expected to increase 1,000 100 proportionately to sales. Cost of financing for DCC is based on the Company’s historical short- 0 0 term borrowing rate of 2.85%. With the increase in COGS and SG&A, which are driven by higher depreciation and expected natural gas price, DCC’s net profit margin is estimated to decline from 17.25% in 2013 to 16.24% in 2019. Gas cost Variable costs Fixed costs Gas Price Capital Expenditures on store expansion and production capacity maximization: The annual Source: Company Data and Team’s Estimates CAPEX is forecasted to range between THB 336Mn to 441Mn during 2014 to 2019 and invested in 6

Figure 20: DCC Cost of Capital Estimates 3 main activities: (1) Store expansion and relocation, expected at 10 relocations with 1-3 new stores each year; (2) Store renovation, to maintain the quality and meet customers’ need; (3) WACC Computation Production capacity maximization, targeted at 2 kilns modification per year. The assumptions are Risk-Free Rate 2.86% estimated based on management’s target announcement and past achievements. Market Return 11.98% Country Risk Premium 2.50% Unsustainable high dividend payout: DCC can maintain its dividend payout ratio at 100% for Beta 0.57 the past years and it is expected continue throughout the forecast period, in accordance with the Cost of Equity 9.48% management’s intention to be a high dividend payout stock. However, to maintain the debt level Cost of Debt 3.38% in long run, the Company is likely to retain the earnings at a level that is sufficient for operation. Marginal Tax Rate 20.00% Terminal growth assumption determined by target earning retention: The sustainable Cost of Debt, post tax 2.71% retention rate is estimated to be 5%, which is the level that the Company will be able to maintain Effective WACC 8.99% its capital structure. Using the sustainable growth formula, the perpetual growth rates are Source: Bloomberg and Team’s Estimates derived in 2 stages, 2.32% and 1.31%, with the assumption that the Company will be able to maintain ROE at 46.32% in the first stage, and reduce down to 26.24% as profit margin will Figure 21: Target Price converge to industry average in the long run (Appendix 16). Weight Price Additional country risk premium added to reflect political instability: The cost of equity is FCFF 47% 40.64 calculated using CAPM with 10-year Thai government bond risk-free rate of 2.86%. Market return DDM 53% 42.14 of 11.98% and beta of 0.57 are derived from 10-year weekly data. With additional country risk Target Price 41.50 premium to reflect the higher risk during political and economic instability, the final cost of equity is 9.48% (Figure 20). Source: Team’s Estimates Weighted average cost of capital: The cost of debt of 3.38% is derived from company’s historical short-term borrowing rate, and 20% tax rate is applied. As the capital structure changes during the forecast period, we calculate different WACC for each forecasted year to include the effect of Figure 22: Valuation Range DCC higher leverage (Appendix 17 & 18). With all components combined, we arrive the effective WACC of 8.99% (Figure 20). DDM FCFF Weighting of Valuation Models PE The shareholder structure serves as a good proxy for the allocated weights to the models. 47% is PE Band assigned to FCFF representing the portion owned by the family and board of directors whereas EV/EBIT… the remaining 53% reflects the minor shareholders. The long-term holding period reflects the 20 30 40 50 60 investment for dividend purpose. Hence, DDM is used to value DCC for this group of investors, Price (THB) representing 53% of the firm’s value. By combining both valuation methods, the fair price for DCC Target Price THB 41.50 is THB 41.50 (Figure 21). Current Price THB 55.75 Target Price Relative valuation also confirms: Apart from DCF methods, we also consider relative valuation Relative Valuation by using P/E, P/E Band and EV/EBITDA multiple analyses in order to reflect better market view (THB/share) P/E Band 39.13 on DCC. DCC fundamentally has exposure in both manufacturing and retailing businesses. Since P/E 43.33 there are no perfect comparable companies, cross-sectional peers were chosen for better comparison. All the chosen comparable companies can be classified into 3 tiers based on their EV/EBITDA 45.64 business fundamentals: (1) local construction material manufactures (2) local home Source: Team’s Estimates improvement retailers (3) regional tile manufacturers (Appendix 19 - 22). Valuation confirms stock overvalued: Both DCF and relative valuation give the target price estimates that are in line with each other (Figure 22). However, we choose DDM and FCFF for our Figure 23: High ROE is offset by high P/BV ROE valuation of DCC as it best suits the nature of Company’s stock. At the current price of THB 55.75, (%) DCC TB DCC is overvalued with the potential downside of 25.56% by the end of 2015. Hence, we ground 50.00 for the “SELL” recommendation with the target price of THB 41.50. Average 40.00 In addition, the indicative valuation multiples obtained from PEG further confirms that DCC’s 30.00 stock price is not justified by its growth outlook. After incorporate the Company’s growth, DCC SCC TB Average has PEG ratio of 7.4x, which significantly higher than peer’s average of 3.0x. Hence, with the 20.00 TTC VN expected growth rate of 2-3% per annum, the results from all valuation methods confirm that the TGCI TB 10.00 current price of THB 55.75 per share is overvalued. GLOBAL TB P/BV 0.00 0.00 2.00 4.00 6.00 8.00 (Times) 10.00 Current price implies unobtainable growth rate PBV Based on the current market price of THB 55.75, it implied the sustainable growth rate of 4.12%. Note: The label is Bloomberg ticker This data reflects an over-expectation from the market since DCC is a matured company, and Source: Bloomberg expected to be threatened by many external factors. With the changing competitive landscape and having no clear growth drivers, achieving such ambitious growth expectation might be Figure 24: DCC P/E Band challenging for DCC. PER (Times) 25 20 +2.0 SD Market view on DCC +1.0 SD 15 +0.5 SD LT average As of December 2014, DCC is trading at current P/E Ratio of 18.9x, which is higher than historical 10 -0.5 SD -1 SD long-term average P/E Ratio +1 SD, and higher than current PER of SET which is 16.9x (Figure 5 24). Therefore, current trading price of DCC is quite expensive while the Company is in mature 0 stage with slowing down trend leading to less attractive in terms of current valuation. In addition, 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 recently DCC’s daily trading volume is only 17 million Baht indicating the low daily turnover of Source: Bloomberg 0.075%. Furthermore, comparing DCC to SET in the bullish trend in the past, DCC tends to underperform SET (Appendix 23 & 24). 7

Financial Analysis 2012 2013 2014 F 2015 F 2016 F 2017 F 2018 F 2019 F LIQUIDITY RATIOS Current Ratio 1.01 0.89 0.87 0.82 0.79 0.78 0.78 0.78 Quick Ratio 0.17 0.13 0.13 0.12 0.12 0.12 0.12 0.12 Cash Ratio 0.10 0.08 0.08 0.07 0.07 0.07 0.07 0.07 PROFITABILITY RATIOS Gross Profit Margin 39.17% 41.06% 40.51% 40.49% 40.51% 40.46% 40.39% 40.29% Operating Profit Margin 21.89% 22.00% 21.28% 21.21% 21.20% 21.13% 21.05% 20.95% Net Profit Margin 16.70% 17.25% 16.65% 16.57% 16.50% 16.40% 16.33% 16.24% Return on Equity 45.79% 46.83% 43.12% 43.52% 44.40% 45.03% 45.71% 46.32% Return on Assets 27.42% 25.99% 22.90% 22.41% 21.93% 21.61% 21.54% 21.57% LEVERAGE RATIOS Debt-to-Equity Ratio 0.30 0.43 0.47 0.54 0.61 0.63 0.65 0.65 Interest Coverage Ratio 105.34 69.54 45.43 41.91 37.16 33.70 33.02 32.17 Cash Flow to Debt Ratio 1.35 1.22 1.08 0.94 0.87 0.88 0.83 0.89 Debt-to-EBITDA Ratio 0.46 0.63 0.74 0.83 0.91 0.92 0.94 0.92 EFFICIENCY ACTIVITY RATIOS Assets Turnover 1.64 1.51 1.38 1.35 1.33 1.32 1.32 1.33 Inventory Days 111.13 129.45 138.50 139.50 142.00 143.00 143.50 144.00 Accounts Receivable Days 6.43 5.87 5.90 6.30 6.50 6.70 6.90 7.00 Accounts Payable Days 53.68 52.41 52.41 53.00 53.00 53.50 53.50 54.00 Cash Conversion Cycle 63.88 82.91 91.99 92.80 95.50 96.20 96.90 97.00 Earnings per Share (THB) 3.10 3.18 2.93 2.99 3.06 3.12 3.18 3.23 Dividend per Share (THB) 3.08 3.18 2.93 2.99 3.06 3.12 3.18 3.23 Figure 25: Decreasing in sale growth Earnings: With the slower-than-expected Thai economic recovery as well as the increasing in Mn THB % YoY 10,000 8.0 competition in the tile market, we expect DCC’s earnings growth to slow down with the revenue 8,000 4.0 and net income CAGR of 1.29% and 0.27% during 2013-2019, respectively (Figure 25). 6,000 0.0 Slowdown in store expansion: From past aggressive store expansion, we are convinced that the 4,000 -4.0 Company has already captured the opportunity both in Bangkok and provincial areas. An 2,000 -8.0 international expansion is also unlikely to take place, thus, the decreasing trend in store - -12.0 expansion is expected to continue. In year 2014, we expect number of stores to remain unchanged, at 195 stores, due to weak demand in upcountry area. Afterward, the number of new Sales(LHS) Net Income(LHS) stores open is expected to decline; from 3 new stores in 2015 to only 1 store by 2019, with the Sales growth(RHS) NI growth(RHS) total of 206 stores by the end of 2019 (Figure 26). Source: Company Data and Team’s Estimates Unsustainable same store sales growth: Looking forward, there will be less opportunity to capture new market since DCC has already had an extensive store coverage throughout Thailand. Figure 26: Slowdown in store expansion Moreover, the weak economic condition is expected to pressure SSS growth down to -5.75% in Stores 210 2014 due to lower purchasing power of DCC’s target customers. With a slow effect from 1 2 government continuous attempt to boost the economy, we expect the recovery to start in 2015 2 200 -1 3 3 and 2016. This will lead to a slight SSS growth of 1.31% YoY. However, the increasing SSS growth 4 is unlikely to remain throughout the forecast period due to cannibalization from store expansion 190 192 as well as the change in competitive landscape of tile market. We expect a slowdown in SSS 195 195 198 201 203 205 180 growth from 1.56% in 2016 to 0.91% in 2019. Slight decrease in profit margin: DCC has already enjoyed the benefits from the reduction in Existing stores New stores amount of natural gas used in production. However, the further improvement might be limited. Source: Company Data and Team’s Estimates According to Ministry of Energy, looking forward natural gas supply will be lower which will lead to the increase in imported natural gas that is sold at higher price. Hence, we expect the gross Figure 27: Increasing in Cash Conversion profit margin to slightly decrease from 41.06% in 2013 to 40.29% in 2019 due to the increase in Cycle natural gas price. Also, operating profit margin and net profit margin are expected to slightly 2019F drop. 2018F 2017F Cash Flows: The Company has planned to expand sales by capturing more wholesales customers: such as real estate contractors and home improvement retailers, and increasing the product lines 2016F offered. These ongoing strategies are expected to result in the longer accounts receivable and 2015F inventory days. Cash conversion cycle is expected to increase from 83 days in 2013 to 97 days in 2014F 2019 (Figure 27). 2013 2012 High potential of increasing in debt financing: In previous years, the Company has financed its Days -40 10 60 110 160 operation mainly through equity and short-term debt. As the cash conversion cycle increases, Account Payable Days more funding is needed. We expect the incurring of short-term debt to support company Operating Cycle (Days) Cash Conversion Cycle (Days) operation. Debt-to-equity ratio is expected to increase from 0.43 in 2013 to 0.65 times in 2019 Source: Company Data and Team’s Estimates (Figure 28). The ability to pay interest will decline as interest expense increases, supported by 8

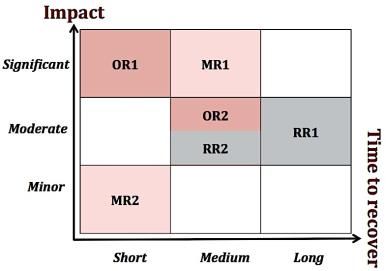

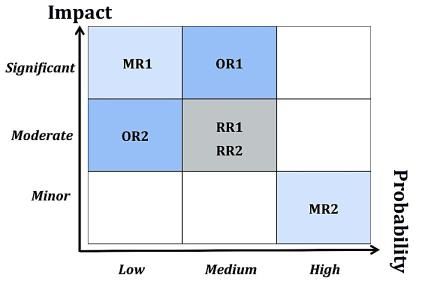

Figure 28: Rise in Debt-to-Equity ratio the decrease in interest coverage ratio from 69.54 in 2013 to 32.17 times at the end of forecast 0.80 0.61 0.63 0.65 0.65 period, 2019. 0.60 0.54 0.47 0.43 Du Pont Analysis: DCC has historically been able to maintain its ROE within the range of 40- 0.40 0.30 46%. Throughout our forecast period, DCC is expected to retain its ROE at around the same level, 0.20 with a slight decline from 46.8% in year 2013 to 46.3% in year 2019. However, our Du Pont - analysis indicates that the key drivers for such high ROE is an increase in leverage, as reflected by a higher equity multiplier (“EQM”) of 1.80 in 2013 to 2.15 times in 2019 (Figure 29). Hence, the Source: Company Data and Team’s Estimates higher return on equity doesn’t necessarily caused by the margin improvements. (Appendix 25). Figure 29: Du Pont Analysis indicates rise in ROE Investment Risks Regulatory Risks RR1: Increase in rule and regulations for imported tiles Tax charged and regulation for imported tiles still remain a key factor to prevent Thai companies to outsource from low cost tile manufacturers oversea. The success of Quality Assurance introduced by Thai government will help decrease the amount of imported tile due to higher quality control. This will reduce competition in local tile market and enhance DCC’s future growth opportunity. Source: Team’s Estimates Figure 30: Risk Analysis Matrix RR2: Success on government stimulus packages Thai government has been trying to reduce the effect on household debt from the past policy of first car, first house, as well as rice subsidy scheme. The success of reducing household debt will help enhance purchasing power of Thai people, mainly low-to-middle income segment who are DCC’s main target customers. Macro Risks (Market Risks) MR1: Early economic recovery results in increase in DCC sales DCC’s sales are highly correlated with Thai GDP at the correlation of 0.97. The faster-than- expected economic recovery and stable political situation will help enhance overall sales. The rise in volume to 58.73 million sq.m. will increase our target price to THB 47.39 and change our Regulatory Macro Operational risks risks risks recommendation to hold, while, further increase to 72.90 million sq.m. will change our recommendation to buy. Source: Team’s Estimates Figure 31: Impact-Recovery Matrix MR2: Possibility of foreign fund flow coming into Thai equity market Given the current global economy, we believe that there might be some foreign funds flowing into Thailand’s equity market. Despite the high possibility of equity market booming, we believe that the fund flow will likely to be a selective buy due to the high valuation of SET. In addition, DCC tends to receive less benefit from fund flows because it has just been taken out of SET100 Index, which represents the top 100 listed companies on SET in terms of large market capitalization with high liquidity. This indicates characteristics of DCC that will be some fund limitations: small market capitalization and low trading liquidity. Hence, the impact from fund flows on DCC stock price may be very limited. Operational Risks Regulatory Macro Operational risks risks risks OR1: Decrease in gas price results in better profit Note: Time to recover is the time we expect One of the main manufacturing costs is coming from natural gas, with contribution of 30% to the effect from risk factors to last. Source: Team’s Estimates overall cost of production. Natural gas price has been fluctuating and unpredictable (Figure 32); however, the decrease in gas price will help reduce cost of product. The reduction in natural gas Figure 32: Company’s historical Natural price to THB 354.6 will change our recommendation from sell to hold and further fall to THB Gas cost THB/MM 227.7 for a buy recommendation. BTU 500 OR2: Success on the introduction of digital and larger-sized tiles 400 By successfully increasing larger-sized and digital tile sales, it will help increase Company average 300 selling price (ASP) since these tiles are sold at 40-50% higher than normal tile price. Instead of seeing an increase in sales contribution, we would like to see more effect on average selling price 200 since the contribution can be misleading if there is any sales promotion. The ASP needs to 100 increase to THB 142.7 to change our recommendation to hold and increase to THB 154.8 to result - in buy recommendation. Valuation Risk Source: Company data To test the effect of the macro and operational risks on our recommendation, we perform Figure 33: Scenario Analysis scenario analysis of changes in sales volume, ASP, and natural gas price. The better and best cases Scenario Analysis will change our target price to THB 51.25 and THB 60.50 respectively and result in hold recommendation. Please see Appendix 28 for more detail on the analysis (Figure 33). In addition, Base Better Best we run Monte Carlo Simulation to further examine the probability of changing our 41.50 51.25 60.50 recommendation. Using 5-year historical standard deviation, the simulation analysis shows that there is only a 4% chance that would trigger a change in our recommendation from sell to buy Source: Team’s estimates and 28% to hold. On the other hands, the possibility of a downside is as high as 68% (Figure 34). 9

Sensitivity Analysis Since Terminal value accounts for the major part of the DCF model, we perform sensitivity Figure 34: Monte Carlo Simulation analysis of changes in perpetual growth rates to our target price. Dividend payout ratio and ROE 68% 28% 4% are used as the sensitive variables as they are the main components of the terminal growth SELL HOLD BUY (Appendix 29). The upper and lower bounds of long-term ROE are the forecast ratio of last period and WACC respectively, while the range of dividend payout ratio is estimated based on the ability to payback debt of the company. Terminal ROE 41.43 9.48% 17.86% 26.24% 36.28% 46.32% Terminal 90.0% 43.45 46.19 49.64 55.13 63.03 Dividend 92.5% 41.27 43.05 45.15 48.20 52.04 Source: Team’s Estimates Payout 95.0% 39.25 40.29 41.50 42.98 44.75 Ratio 97.5% 37.39 37.84 38.31 38.91 39.55 100.0% 35.66 35.66 35.66 35.66 35.66 Figure 35: Real Option Valuation Other Upside Potentials Summary Announcement of international expansion plan Real Option Summary (In Mn THB) The opening of AEC will present an opportunity for DCC to expand its business oversea. This can Spot Value 1,459 be done by both expanding the production base and establishing Company’s own outlet stores. However, from the statement made by DCC’s management team, the most likely case is to open its Strike Value 1,614 own outlet stores. We see this opportunity as an option to expand internationally whose Volatility (%) 50% characteristic is similar to call option. This can be valued using Black-Scholes option pricing 3-Y Risk free rate (%) 2.3% model (Appendix 30). The real option value is THB 473.1 million or THB 1.16 on per share basis (Figure 35). The option is currently out-of-the-money due to the riskiness of entering into new Real Option Value 473 market that has no prove of success. Number of shares outstanding (Mn) 408 DCC as a potential target acquisition company Real Option Value/share (THB) 1.16 Construction material industry in Thailand has been growing toward the consolidation trend. Source: Team’s estimates SCC, the largest cement-building material company in Thailand, has been acquiring various companies in the industry. It partially staked in TGCI, a tile manufacturer, in 2008 and also in GLOBAL, a one-stop shopping home center, in 2012. Those target companies help enhance and strengthen business of SCC. By looking at both side of the acquisition, being an acquirer as well as being a target company, we believe that there is low chance for DCC to be an acquirer due to its excess production capacity throughout the forecast period (Appendix 31). On the other hand, as one of the leader in tile market with a large production capacity and strong brand reputation in particular market; DCC can potentially be a target company for acquisition. Observing from past transactions, the company is likely to be bought at premium of around 6.70% to 26.44% at a price range of 60.12 to 70.10 Baht per share (Appendix 32). Additional Downside Risk Probable increase in Value-Added Tax will slow down the consumption The government is considering increasing the Value-Added Tax or VAT, which is planned to be lifted from current 7% to 8% next year and to 10% in following years. This could potentially slowdown the recovery of economy as observed from Japan. Especially in low-price segment, DCC’s main customers, tend to have less incentive to spend because they are more sensitive to the change in VAT. Given the increase in VAT take place, we expect the money to be spent mostly on daily necessities with a small leftover spared for home renovation as necessary. 10

Appendix Index Financial Statements Page Appendix A: Income Statement 13 Appendix B: Income Statement (Common-Size) 13 Appendix C: Balance Sheet 14 Appendix D: Balance Sheet (Common-Size) 15 Appendix E: Statement of Cash Flow 16 Business Description Appendix 1: Brands under DCC 17 Appendix 2: Product Types 18 Appendix 3: Business Structure and Subsidiaries 19 Appendix 4: Key Management Personnel 21 Corporate Governance Appendix 5: Corporate Governance 27 Industry analysis Appendix 6: Absolute and Relative Increase in Household Debt 28 Appendix 7: Growth of Renovation Market 28 Appendix 8: Domestic Manufacturers Market 29 Appendix 9: DCC’s Five Forces Analysis 30 Appendix 10: Growth of Specialty Store and Overall Modern Trade 31 Investment summary Appendix 11: Imported Tiles 32 Appendix 12: Home improvement centers (modern trade) 33 Appendix 13: Comparison among DCC and other improvement centers 34 Appendix 14: Home Improvement Centers store footprint 34 Appendix 15: Calculations of upside and downside beta between DCC stock price and SET 100 index 35 Valuation Appendix 16: DCF Assumptions 36 Appendix 17: WACC Assumptions 41 Appendix 18: DCF Analysis 42 Appendix 19: Relative Valuation 43 Appendix 20: DCC Expected Return-to-Beta comparison 45 Appendix 21: DCC Price-to-Earnings Ratio to Earning Growth Comparison 46 Appendix 22: DCC Return on Equity to Price-to-Book Value Comparison 47 Appendix 23: PE Band 48 Appendix 24: DCC underperforms SET over the past 3 years 48 Financial Analysis Appendix 25: Du Pont Analysis 49 Investment Risks 11

Appendix 26: Impact-Probability Risk Analysis Matrix 50 Appendix 27: Impact-Time to recover Risk Analysis Matrix 50 Appendix 28: Scenario Analysis 51 Appendix 29: Sensitivity Analysis 51 Appendix 30: Real Option Valuation 52 Appendix 31: Production Capacity Analysis 53 Appendix 32: Comparable M&A Transaction 55 Others Appendix 33: Management Structure 56 Appendix 34: Tile manufacturing factories 57 Appendix 35: Major shareholders structure 58 12

Appendix A: Income Statement Income Statement (Mn THB) 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F Revenue from sales 7,603 7,546 7,211 7,388 7,595 7,779 7,963 8,148 Costs of goods sold (4,625) (4,447) (4,290) (4,396) (4,518) (4,632) (4,747) (4,865) Gross income 2,978 3,099 2,921 2,991 3,077 3,148 3,216 3,283 Other income 35 18 21 22 22 23 24 24 Selling expenses (761) (755) (721) (739) (760) (778) (796) (815) Administrative expenses (588) (701) (687) (707) (729) (749) (767) (785) Income before finance costs income tax 1,664 1,661 1,534 1,567 1,610 1,644 1,676 1,707 Finance costs (16) (24) (34) (37) (43) (49) (51) (53) Income before income tax 1,648 1,637 1,500 1,530 1,567 1,595 1,625 1,654 Income tax (379) (335) (300) (306) (313) (319) (325) (331) Net Income 1,270 1,302 1,200 1,224 1,253 1,276 1,300 1,323 Appendix B: Income Statement (Common-Size) Income Statement (Common-Size) 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F Revenue from sales 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% Costs of goods sold 61% 59% 59% 60% 59% 60% 60% 60% Gross income 39.2% 41.1% 40.5% 40.5% 40.5% 40.5% 40.4% 40.3% Other income 0.5% 0.2% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3% Selling expenses 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% 10.0% Administrative expenses 7.7% 9.3% 9.5% 9.6% 9.6% 9.6% 9.6% 9.6% Income before finance costs income tax 21.9% 22.0% 21.3% 21.2% 21.2% 21.1% 21.1% 20.9% Finance costs 0.2% 0.3% 0.5% 0.5% 0.6% 0.6% 0.6% 0.7% Income before income tax 21.7% 21.7% 20.8% 20.7% 20.6% 20.5% 20.4% 20.3% Income tax 5.0% 4.4% 4.2% 4.1% 4.1% 4.1% 4.1% 4.1% Net Income 16.7% 17.2% 16.6% 16.6% 16.5% 16.4% 16.3% 16.2% 13

Appendix C: Balance Sheet Balance Sheet (Mn THB) 2012 2013 2014F 2015F 2016F 2017F 2018F 2019F ASSETS Cash and cash equivalents 189 169 180 185 190 194 199 204 Trade accounts and notes receivable - net 137 106 127 128 143 143 158 154 Inventories - net 1,550 1,605 1,651 1,709 1,806 1,823 1,910 1,929 Other current assets 36 35 35 36 37 38 39 40 Total Current Assets 1,911 1,915 1,994 2,058 2,176 2,198 2,306 2,326 Other investment - net Property, plant and equipment - net 2,701 2,942 3,073 3,238 3,392 3,472 3,512 3,529 Goodwill 104 104 104 104 104 104 104 104 Intangible assets - net 7 15 16 16 17 17 17 17 Deferred income tax - asset 119 127 122 125 128 131 134 137 Other non - current assets 37 38 35 36 37 38 39 40 Total Non - Current Assets 2,967 3,226 3,350 3,519 3,678 3,762 3,807 3,827 TOTAL ASSETS 4,877 5,141 5,343 5,577 5,854 5,960 6,112 6,154 LIABILITIES AND SHAREHOLDERS' EQUITY LIABILITIES Short - term loans from financial institutions 840 1,185 1,312 1,520 1,712 1,781 1,861 1,852 Trade accounts and notes payable 689 588 644 633 679 678 713 726 Accrued income tax 183 148 141 145 149 153 156 160 Other current liabilities 176 236 201 206 212 217 222 227 Total Current Liabilities 1,887 2,157 2,298 2,504 2,752 2,829 2,953 2,965 Unfunded provident fund 51 53 55 57 59 61 63 65 Employee benefits obligation 118 136 151 166 181 196 211 226 Deferred income tax - liability 23 33 32 33 34 34 35 36 Total Non - Current Liabilities 193 222 238 255 273 291 309 327 TOTAL LIABILITIES 2,080 2,379 2,536 2,760 3,025 3,120 3,262 3,292 SHAREHOLDERS’ EQUITY Issued and paid - up - 408,000,000 shares 408 408 408 408 408 408 408 408 Premium on share capital 506 506 506 506 506 506 506 506 Retained earnings - Appropriated for legal reserve 41 41 41 41 41 41 41 41 - Unappropriated 1,797 1,757 1,799 1,804 1,812 1,817 1,823 1,829 Shareholders' equity of the Company 2,752 2,711 2,753 2,759 2,767 2,772 2,778 2,784 Non-controlling interests in subsidiaries 46 50 54 58 62 67 72 78 TOTAL SHAREHOLDERS' EQUITY 2,798 2,761 2,807 2,817 2,829 2,839 2,851 2,862 TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY 4,877 5,141 5,343 5,577 5,854 5,960 6,112 6,154 14

You can also read