Capstone Applied Project in Marketing 24100 Project 2A and 2B Daily Naturals

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Capstone Applied Project in Marketing 24100

Project 2A and 2B

Daily Naturals

Bachelor of International Marketing

University of Technology Sydney

15.06.2018

Marius R. Ekeland

This paper is done as a part of the undergraduate program at BI Norwegian Business

School. This does not entail that BI Norwegian Business School has cleared the

methods applied, the results presented, or the conclusions drawn.

PROJECT REPORT 2A

2

TABLE OF CONTENT

Internal Analysis ........................................................................................................................ 4

The Company/ Product Line overview ................................................................................... 4

Strengths and Weaknesses ..................................................................................................... 5

Strengths ............................................................................................................................. 5

Weaknesses ......................................................................................................................... 6

Business Model Canvas........................................................................................................... 6

External Analysis ........................................................................................................................ 9

Market Analysis, Opportunities and threats .......................................................................... 9

External Market Analysis ...................................................................................................... 13

External competitive analysis ............................................................................................ 13

Customer Analysis................................................................................................................. 17

Behavioural Analysis (Customer Buying Criteria).............................................................. 17

Behavioural Analysis (Purchase Process and Patterns) .................................................... 18

Customer Demographics ................................................................................................... 18

Macro environmental Analysis ............................................................................................. 19

PESTEL ............................................................................................................................... 19

Weighted SWOT Matrix..................................................................................................... 21

Three key issues ................................................................................................................ 22

Apendix 1 .............................................................................................................................. 28

3

Internal Analysis

The Company/ Product Line overview

The formulation chemist, John Sloan, established Dresslier & Co in 1930. Sloan´s

manufacturing of hair care products such as hair oils, shampoos, talcum powders and

aftershaves started in Adelaide. Dresslier has previously served as a key distributor for several

international brands, some of them being Joiken, Wella, Redken and American Crew.

Dresslier developed a new and innovative product range in the 1980s. A plant-based product

range with the name Davroe. After John and Mary Centofanti acquired the company in 2006,

Dresslier went from being a salon supplier to manufacturing their own brand and contract

packs. They also made the decision of removing petrochemicals, such as parabens and

sulphates from their products.

It became apparent that there was a demand for Davroe in the pharmaceutical market.

However, Dresslier was concerned that introducing Davroe to this market would cheapen the

brand. The solution Dresslier developed was to start a new product line - Daily Naturals (DN).

Dresslier introduced DN to the National Pharmacies in South Australia in 2011. The product

range consists of shampoos, conditioners, and various hair treatment products. This product

range is 100%- vegan, cruelty-free (no animal testing) and is Australian owned and made.

4

Strengths and Weaknesses

We have assessed the internal strengths and weaknesses of Dresslier, as a company, and DN

as a brand.

Strengths

Dresslier´s owner and director, Mary Centofanti, started her career with the company at 15

years of age as a receptionist. This provides her with an in-depth understanding of the

company's operations and how to operate in the industry. Dresslier has a minor HR advantage,

due to long-term employments such as their lead chemist which has been with the company

for several decades.

Dresslier has experienced success with Davroe, a recognized brand in the salon market. This

provides Dresslier with experience and knowledge in the industry at hand. This can be

leveraged to the DN branch as well.

Dresslier and all their products are both Australian owned and made. This represents a

domestic strength as shown by a survey conducted by the “Australian made association”,

stating that more than two-thirds of Australians would give preference to buying locally made

and grown goods (haircare, 2018). However, this might have some limitations and will be

examined in detail.

DN has a unique combination of natural ingredients in their product, that provides great

performance without any chemicals. DN provides high-quality products that are animal

cruelty-free and only tested on humans.

Dresslier specializes in hair-care products, whilst many of their competitors have a more

diverse product line. They are specialists in their industry and hasn’t diluted their brand to a

wide product portfolio.

5

Weaknesses

The fact that Dresslier has no website or online presence for DN is a weakness as this

prevents potential customers to gain knowledge about the brand and its products. This also

makes it harder for DN to gain brand recognition in a market where this is of value.

Dresslier´s factory is not geographically located to promote sales in Sydney. The long-

distance decreases the efficiency and lead-time from order to delivery and increases the cost

of distribution. In comparison, their main competitor (Sukin) has their facilities located in

Melbourne, which gives them an advantage in this area of distribution.

Dresslier has done no marketing for DN, which also means they have no market information

to base this report on. They also have no marketing department, and no staff fully allocated to

deal with marketing for their products. Their moderate allocation of funds to this marketing

campaign limits their potential marketing efforts, and therefore its effect ($500,000 AUD).

As Dresslier specializes in hair-care products, whilst many of their competitors diverse into a

broader product range, consumers will be less exposed to DN compared to other brands.

Business Model Canvas

DN currently has an indirect business model, where they rely on pharmacies and a website to

distribute their products. Therefore, their business model contains little consumer

relationships, but they retain a relationship with their b2b customer - National Pharmacies and

Flora & Fauna. You will find the model in the appendixes 1.

Customer segments

The customer segment is in the pharmacy market. This is where men and women of any age

can acquire a higher quality hair-care product than what the regular supermarkets offer. DN

want to target this market and be perceived as a high-quality brand.

6

Value proposition

DN tries to deliver an all-natural, cruelty-free and hair care solution to the pharmacy

market. With no harmful ingredients included, they have managed to create a quality product

from natural ingredients which supports Australian workers due to that its Australian made.

With the cruelty free and all-natural products, they bring a certain “status” for the people who

buy their product. The most important aspect of their value proposition is quality. With their

internal intellectual resources, they have developed quality over many years of production.

Channels

DN is sold through Flora and Fauna’s website and through National Pharmacies. There are no

noticeable online presence or marketing efforts towards creating brand awareness. This

creates a disconnected relationship between the consumer and DN.

Customer Relationships

Their customer relationships are retained with their distributors, but their consumer

relationships are retained through their distributors which can lead to diverse communication

to the end consumer and the intended message of the product might be misunderstood.

Revenue streams

DN uses asset sales as their revenue stream through fixed “menu” pricing – selling their rights

to the product so the consumer can do as he/she pleases with the product for a fixed price.

Key Resources

Physical resources

DN physical resources consist of manufacturing facilities. The products are produced and assembled

in Australia which is one of DN selling points – Australian made and owned. The fact that DN uses

Australian made and owned as a selling point promotes the importance of the facility as a key

resource.

7

Intellectual Resources

Intellectual resources are an intangible value for a business. Dresslier has been a company

since the 1930s and through many years of producing and distributing hair care products,

Dresslier has achieved ingredient and production knowledge to attain and sustain quality

products.

Human Resources

Mary Centofanti has worked with the company for several years. This provides her with an

in-depth understanding of the company’s operations. Furthermore, the DN chemist is the son

of the chemist who started the company i 1930 and has many years of experience.

Key activities

Production

Seeing as DN is strictly using second-hand retailers, the manufacturing of the products is key

to meet the demands of the consumers. According to the Dresslier owners, “there is no such

thing as a production advantage in this business”.

Key Partners

National Pharmacies

It became apparent that there was a demand for Davroe in the pharmaceutical market.

Dresslier created DN in order to capitalize on this demand without devaluing Davroe. Most of

DN´s revenue stems from sales through National Pharmacies.

Outsourced bottle makers

Currently, DN outsource their manufacturing of the bottles, making them a key partner.

Cost structure

Cost-driven business models

Cost-driven implies that the business tries to minimize cost wherever possible. DN outsource

manufacturing of their bottles and import ingredients from different suppliers and assemble

the product in Australia to achieve a lower price of their end product.

8

Fixed costs

DN’s fixed costs consist of salaries of employees and manufacturing facility.

Low variable costs

The company has a low variable cost per bottle made; only an significant increase when

production increases over a certain level that requires investment in workforce/manufacturing

External Analysis

Market Analysis, Opportunities and threats

The market analysis contains information about the total market Dresslier is in, the niche market that

DN product line is targeting, and measures to consider to be successful in the industry.

According to information gathered from IBISWorld, the Cosmetic & Toiletry Retailing industry in

Australia is a 4.1 Billion AUD industry, with an overall profit of 316.7 Million AUD, which leads to

an industry profit margin of 7.72%. It is estimated the industry will grow by 2.0% annually until 2018,

where the growth will slow down to 1.9% from 2018-2023. 2022-2023 revenues are estimated to be at

4.5 Billion AUD, which means there will be more revenues for Dresslier and DN to capture in the

future. (Richardson 2018) The population growth in Australia is expected to grow with a 1,4% annual

increase (Worldbank 2016), which means the industry has a net growth of 0,6%.

Some of the key economic drivers for the market is the female population above 18 years of age,

increase in household discretionary income, and the demand for online shopping. These factors have

been identified as the drivers that affect the industry in the most substantial way, both positively and

negatively. Despite there being a growing market for men within this market, it is still dominated by

women aged 18 and above, as this segment of the population is estimated to reach 9.9 Million in 2017-

2018 (Richardson 2018).

When discretionary income rises, consumers tend to use more money on luxurious products like the

product line DN are offering. Estimates indicate that discretionary income will fall 2017-2018.

(Richardson 2018)

The growing number of online-only cosmetics retailers is one of the biggest external threats to the

industry. More Australian consumers have been taking advantage of the discounted prices, parallel

9

imports and the greater range of brands that many online retailers offer. Online cosmetics sales are

expected to continue growing over 2017-18, to the detriment of industry retailers (Richardson 2018).

The increased confidence in online sales has reduced the unit prices due to more efficient business

models and smarter value-chains in general. This is something that has led to increased discounting

from pharmacies and discounts outlets, which has put downward pressure on industry profits in

combination with growing competitive pressure.

However, introduction to premium products and services with higher added value has helped to offset

these trends, allowing industry profits to have an overall growth in the period. This is most relevant for

cruelty-free, sustainable and environmental-friendly products with all-natural ingredients and no

chemicals as these product niches grow faster than the mainstream industry. A study from Canstar

Blue reveals that 34% of choose to purchase chemical free or low shampoo’s. (Professional Beauty

2011)

Cruelty-free products are expected to gain even more ground following the potential ban of cosmetic

& hair-care products tested on live animals. Should the relevant Industrial Chemicals Bill 2017 be

enacted, the ban is due to commence from 1. July 2018. (www.aph.gov.au 2018)

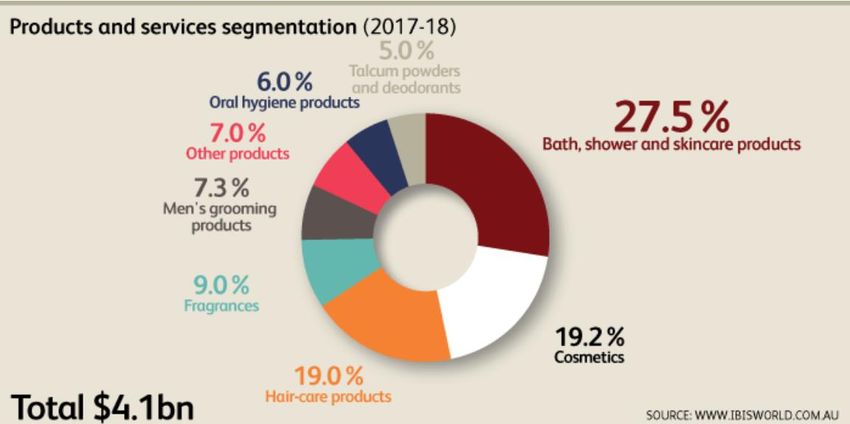

The industry is divided into differently weighted segments. You can argue that DN product

range can be seen as “Bath, shower and skincare products” (27.5%) and “Hair-care products”

(19.0%), leaving them with a potential market of 46.5%. (Richardson 2018) This is

furthermore backed up by numbers from Euromonitor defining the Australian shampoo

market at 430,4 MAUD and the conditioner market at 366,2 MAUD. Which gives DN a

combined market of 796,6 MAUD (Euromonitor 2017).

10Model from Euromonitor Industry analysis 2017.

The industry is labelled as mature, which means the large main players will control a lot of

mainstream areas such as discounted cheap shower-gel. However, it also means that there are

niche markets that are open and growing, such as eco-friendly, all-natural products as

mentioned. Both IBIS world industry report and Euromonitor report agrees that these niches

are in higher growth than the rest of the industry.

Industry demand determinants

The main factors that decide the demand for products in the industry:

• The fashion & beauty industry is often correlated to the cosmetic- & hair-care

industry. The fashion industry has been using Social Media as well as other non-

traditional channels to promote hair-care products.

• There is a growing trend of a holistic approach to beauty, meaning a more natural way

with natural ingredients in the beauty products instead of chemicals which is falling

out of flavour. Consumer trends are pointing towards natural products that repair hair

and gives volume. (Euromonitor 2017)

• Socioeconomic factors, this means that households usually respond to financial

difficulties by buying lower priced products. In other words, people want value for

their money in times of financial uncertainty.

11Most impactful risks moving forward

• The increasing trend in the industry of driving promotional offers with prices as low as

40%-50% on hair-care products. Combined with a stagnating revenue growth in the

market it will increase the competition the next years & squeeze profits.

• Not adapting to new consumer trends and preferences. Such as natural ingredients,

moisturizing and repairing hair-care products.

• Not being consumer-centric. This means knowing who your customer is and knowing

their every need even before they know they need it themselves. This is essential in a

very competitive market in the mature stage.

SuccessFactors to consider

• Ability to control inventory: increase efficiency & throughput for the stock at hand

to reduce inventory costs and increase turnover.

• Having a clear market position: Project a clear and consistent image to attract the

target segment. In the social media age, this is growing in importance.

• Production of goods currently favoured by the market: Ensure an appropriate

product mix and pricing strategy for the target market.

• Experienced workforce: In the prestige segment of the industry, it is important that

the staff is well informed, and educated in the area and able to convey the consumers

to try the product.

• Attractive product presentation: The placement in the store (pharmacy) will be

essential for how good the product does. The packaging will also play a role for this

point. Digital displays will increase over the next five years.

• Competitive advantage: Make sure your customer views your perceived competitive

advantage as an actual advantage over other brands.

• Attract the target market: Find different ways make your customers notice the

products and develop an interest in your brand. Creative & innovative ways of giving

your brand attention are welcome in the market.

12External Market Analysis

External competitive analysis

To be able to determine how competitors can impact DN we need to conduct a competitor

analysis by looking into the current market situation. Today, the global hair shampoo market

is relatively competitive with several large established vendors like L’Oréal, Schwarzkopf,

Head & Shoulders and Garnier. In June 2016, 73.9% of Australians purchased shampoo at

least once in an average six months. 14.5% of them purchased Alberto shampoo, right above

the 14.1% who bought Head & Shoulders (Inside FMCG, 2018).

Aside from the key vendors, there are several small, medium, and large size companies that

operate extensively in the global market. Some private brands are also making an entrance

into this market due to its high growth potential. Still, the threat of new entrants is moderately

low due to high competition and large companies. However, studies show that brand loyalty

amongst millennials are very low and that consumers brand loyalty amongst beauty products,

in general is around 50% (Global Cosmetic Industry, 2018). This makes it easier for new

products to get through the entry barriers.

13The threat of substitute products is high because hair products with different features are

constantly being developed. The growing hair-care industry and the various number of

substitutes in the market gives the companies relatively high bargaining power over the

different suppliers.

Customers have high bargaining power because they easily can get information about

different products and their attributes. This challenges the companies to stand out and offer

the best quality to the best price. The switching cost for the consumer is low due to low brand

loyalty and high similarity between products. One thing that could increase switching cost is

to have a product that really distinguishes from others. People who have problems with hair or

scalp conditions and struggle to find the right product will often have a stronger relationship

with their hair care brand and have a higher switching cost.

Due to an increased demand for organic and environmentally friendly products, the sales of

hair care products through specialty stores has witnessed dramatic growth over the last years.

The competition in the haircare industry is high because of continuous change in the market

and the consumers preferences (GmbH, 2018). Due to the growing concern about haircare and

different hair conditions, the development of new products and adopting of new technology

has become important to keep the customer loyalty and survive in the market.

DN largest competitors are brands that are sold in pharmacies or the same online stores. They

also share the same features as; natural, plant-based, vegan and cruelty-free. The two main

competitors are Sukin and Klorane.

Sukin is an Australian made brand with a large range of products for skin and hair. In 2007,

Sukin was launched in Melbourne, after identifying a gap in the market for high efficacy,

environmentally sustainable and affordable natural skincare. Since then Sukin has expanded

and is now sold in10 different countries and has become the largest natural skincare brand in

Australia.

14The company utilises botanicals, antioxidants, and oils to restore natural vitality to hair and

skin. All their products are made with ingredients that are vegan, cruelty-free and naturally

derived. All formulations are also 100% Carbon Neutral, biodegradable and grey water safe

(Sukinorganics.com, 2018).

Sukin is owned by BWX which is a developer, manufacturer, distributor and marketer of

branded skin and hair care products. In the first half of 2017, BWX reported that revenues

from Sukin increased 59.4% (compared to the prior corresponding period), accounting for

almost 83% of total sales and commands a 7.3% market share in the cosmetic skin care

market (Bwxltd.com, 2018).

Sukin is a well-known brand in Australia and they are a big threat for DN due to brand

awareness through their different product lines. DN is also sold at pharmacies for twice the

price as Sukin which make them even more of a threat. On the other hand, Sukin sells large

bottles of one liter and 500ml which appeals to customers that want to buy in bulk. Sukin sells

bottles of 250ml for $8.95, bottles of 500ml for $12.95 or $14.95 and 1L bottles for $20.95 or

$24.95 (Sukinorganics.com, 2018). This could mean that they are focusing on value-

customers and neglecting the premium/luxurious segment, due to cheap prices and large

bottles. This also means that they could target both families, bulk buyers and people that

prefer small bottles.

Sukin has a pure and simple homepage with nice colours and professional pictures of the

different lines combined with flowers, herbs and plants. They have put a lot of effort in their

Instagram profile and have 61.4K followers (as of May 2018) targeting young women that

emphasize a natural lifestyle. Sukin uses several female influencers with a lot of followers,

they sponsored the last season of The Bachelorette Australia and teamed up with Lé Buns and

Holland and Barrett to create awareness and get more customers (Instagram.com, 2018).

(Instagram.com, 2018)

15The advantage for DN is that Sukin does not focus much on hair care, but all over skin care.

This could make it easier for DN to target a smaller niche and penetrate the market from a

different angle by focusing on their hair products.

Klorane is not Australian made but is plant based, vegan and cruelty-free. The company

launched in South West of France by Pierre Fabre in 1965. Driven by his passion for the

health and beauty benefits of plants. Their products are based on one simple concept; one

concern, one plant, one benefit. They have further launched the first dry shampoo on the

market and shampoo based on plant milk.

In 1994 there was founded a botanical institute of Pierre Fabre to protect, explore and educate

on plant species and biodiversity (Laboratoire Klorane, 2018). They have later got rewards for

quality and sustainable development and have supported different environmental projects.

Klorane have a long history on the market but not as long in Australia. They have a broad

product line for hair and face but only sell their hair-care products in Australia.

Klorane sells their 200ml bottles for $13.99 which is in the same price range as DN. They

have a lot of shelf space at the pharmacies and are sold in Priceline and chemists around

16Australia. Klorane is sold at the National Pharmacies website and in the pharmacy together

with DN. We have also noticed them to be placed right above the DN products which give

them a better shelf placement.

Their website is very clean and easy to use with bright colours. They have a map where you

can find their products and they interact with the customer by providing a diagnosis of your

hair by answering a few questions about your lifestyle etc. Klorane also got tutorial videos

with the model Rebecca Judd showing their products (Laboratoire Klorane, 2018).

Their Australian Instagram account have 10.8K followers (as of May 2018) which is not a lot

compared to Sukin which is well known in Australia. Their profile targets young females and

uses Instagram influencers to reach their target group. The profile is clean and focuses on the

product and includes also information about ingredients and application to interact with the

customer (Instagram.com, 2018).

Due to the fact that Klorane is not that big in Australia, DN should use this advantage and try

to take a larger market share before Klorane and similar brands with moderately low brand

awareness get more visible in their target market.

Customer Analysis

Behavioural Analysis (Customer Buying Criteria)

The customers vary in purchasing criteria, but some of the most important attributes

appreciated by the consumers are that the products are all-natural and cruelty-free

(Stephenson Personal Care, 2018). The fact that a product is cruelty-free is attractive to the

consumers in the purchasing decision. It gives them a sense of wellbeing seeing as most

17people prefer products that do good and preserve animal rights. (The Business of Fashion,

2018).

Price is always an important factor when consumers consider purchasing natural shampoo.

All-natural products are often priced higher than non-natural products, which also means DN

need to target segments thereafter. It is a trend to purchase all-natural and cruelty-free

products. Natural ingredients have more trust from the end users than what non-natural

ingredients have (Prnewswire.com, 2018). Natural ingredients may not have a better effect

than products with chemicals, however, some customers value these products and are willing

to pay a higher price.

Behavioural Analysis (Purchase Process and Patterns)

The information the customers seek is if the product´s perceived effect is something that can

help them satisfy their needs or solve their problem(s). Purchasing patterns will vary on

demographics, brand loyalty, and behavioural criteria. Our customers are ethically persuaded

and favour products that are sustainable. The involvement of hair-care products will vary for

the different customers. Some will have high involvement due to pain-removing (dandruff &

scalp issues), and others will view it as a low involvement product.

Word of mouth (WOM) is a crucial part of being recognized by our consumers. They will

seek information from family and/or friends to find out if the product covers their needs. In an

age with advertising noise everywhere, people tend to hold the opinion of people they know

in the highest regard. (Research, 2018) In a B2B context, there are many parties that need to

agree on the purchase. While in a B2C context, the end user will always have the final say in

the decision and are easier to influence on non-cost factors.

Customer Demographics

The customer demographic of the target market is women from 20-35 years. It is becoming

more and more popular to purchase all-natural products, contributing to the wellness of the

world and its animals. Females are more interested in these products and are, therefore, our

target segment as a survey conducted in Australia say: “73 to be exact—of millennial women

seek out cleaner, all-natural products” (Kinonen, 2018).

18Our segment does not just pick any alternative off the shelves without some consideration.

The users will know the impact of their purchase and which effect it will have on them and

the environment. It is necessary to acknowledge that customers are much more aware of what

ingredients they expose themselves to and the perception of all-natural products is that it has a

positive and natural effect on your hair, skin and overall wellbeing. (Stephenson Personal

Care, 2018)

Macro environmental Analysis

PESTEL

P

Political

• China’s legislation towards new products (must currently be tested for 6 months on

animals). This could be a problem on some online stores or if DN expands

• Legislation toward animal cruelty and eco-friendly products.

• Industrial Chemicals Bill 2017 be enacted, the ban is due to commence from 1. July

2018.

E

Environmental

• Sourcing of materials might be disrupted due to natural events.

• Bottle makers shipments get delayed due to natural events

• Increase in gasoline prices might increase transport costs for DN (From Adelaide to

Sydney)

• Their European and American suppliers move away from “All-natural ingredients”

• Loreal or another big player buys up one of DN’s main competitors and provide them

with unlimited funding until Dresslier runs out of money

• Pharmacies dilute the DN brand equity by using discounts as a tool to sell more

product from their shelves

S

Social-cultural

• Vanity, growing trend of all natural and green consumers via social media.

• Increased awareness of animal cruelty and more people are turning to all-natural

products.

19• People are moving towards online shopping

• Environmental-purchasing, people do research before shopping.

• Growing awareness for environmental issues, which increases the demand for eco-

friendly and sustainable products.

• Increased information in society about firms and how they practice CSR

• Growing trend on social media towards influencers, their lifestyle and what products

they use

• Growing interest in tutorial videos on styling and beauty products

• The population is getting older

• A trend towards people colouring their hair

• An increased trend towards buying products in pharmacies an specialty stores

T

Technological

• An increasing importance of competing on online platforms, both for sales and

marketing/branding

• New ways of making the product in a more efficient and eco-friendly way.

• New ways of distributing the product e.g. more efficient packaging, more spacious

trailers.

• New ways of making the value-chain more efficient (LEAN). Lower labour costs with

more automation at the factory. Inventory management to reduce waste and excess.

• New main channels to reach the customer (online, social media)

E

Economic

• Disposable income is a big determinant of how much consumers use on products that

are all natural and of a higher quality than the cheaper discount products.

• Good economic times provide a more lucrative market for DN.

• Interest rates and currency fluctuations might affect sales in the industry, especially if

they move the product abroad like Davroe.

• Asset appreciation which leads to higher consumer spending.

L

Legal

20• Strawberry.net thought about buying DN, but due to regulations in China, it is

required that hair-product is tested on animals for 6 months this was not done. DN

could also face restrictions like that when expanding their market.

• Tariffs might increase transaction costs of shipping the product to other countries, e.g.

the US.

• Legislation toward the hair-care industry will have a direct impact on DN.

• Labelling law (Chinese labels/packaging)

Weighted SWOT Matrix

Weighted SWOT Matrix Opportunities Threats

- Establish online presence - Not keeping up with trends

(Influencers)

- Economic recession

- Focus on a concentrated segment

- Not having a CLEAR market

- Make additional revenue from position

the Asian market

- Getting outcompeted by the

- Take advantage of holistic beauty harsh competition

trends

- Low brand loyalty in the market

- Co-branding with a company that

- Not getting the desired results

has a similar segment

from the marketing campaign

- Improve bottle design

- Subscription-based online shop

- Recommendation-based guide

Strengths • Unique product focused • Not keeping up with

on a concentrated trends can be countered

- Minor HR advantage

segment by the HR advantage

- Experienced success in the

• Experienced staff from DN • Providing a unique

industry before DN

to help establish online an product of higher quality

- Australian made & owned presence will keep the competition

at bay.

- Unique product: Salon • Combine their unique

performance, product and experience

21Environmentally friendly and with social media to reach • Having an experienced

animal cruelty-free a niche market workforce in times of

economic recession

- Chemical free • Co-branding combined

with their experience in

- Hair-care specialists

the industry to attract

higher

Weaknesses • Establishing an online • Not having a CLEAR

presence from scratch market position

- No online presence

combined with a low

• Focus on a concentrated

- No sustained competitive campaign budget

segment since we don't

advantage

have a sustained • No sustained competitive

- Low campaign budget competitive advantage advantage and not

keeping up with trends

- No marketing information • With no marketing

due to the fact that they information, Daily Naturals • Hard keeping up with

have done no marketing have a chance to create trends with bad

research their own position marketing and zero

information from the

- No marketing department

market.

- Low brand awareness

• Low brand awareness

- The geographical position combined with no

of factory compared to marketing department

competitors

Three key issues

1. Combine their unique product and experience with social media to reach

a niche market

DN has an advantage of having a unique product and a lot of experience in the

haircare industry. They also focus solely on hair care compared to their

competitors which make them specialists in their field. This is an advantage

that DN should focus on towards the consumers. Combined with the fact that

they have no presence on social media they have a chance to start from scratch

and really try to reach their niche market. To do that DN should focus on their

expertise and the performance of their product combined with interaction with

22the customer through social media. This can be done through tutorial videos,

influencers, competitions and making DN about more than just a brand.

Creating a platform where DN can communicate with their target market is

essential to keep up with the competitors and to create a bond with the

customers in a market with low brand loyalty and high competition. It is

important for DN to create awareness through social media to be a part of the

consumer’s decision-making process. Due to fact that they also have a low

budget on marketing social media is maybe one of the cheapest and easiest

ways to create awareness if it is done right.

2. Low brand awareness combined with no marketing department

In the industry of hair care, shampoo and conditioners the brand awareness is

low. The consumer changes brands based on convenience, price and are on a

constant search for better products that suit them better. Combined with DN

not having a dedicated marketing department there is nothing to influence the

consumer towards buying their product besides from other users, pharmacy

promotion, placement in shelves or the design of the shampoo itself. DN is

placing a lot of trust in their quality of the product for the consumers to share

with word of mouth. When there are products like L’Oréal and other big names

that are heavily invested in marketing, DN is easily overshadowed by not only

big brands but also might look like any other shampoo bottle for a consumer

influenced by marketing campaigns. When the market has a low brand loyalty

of a product in an industry, a consumer is more inclined to buy a product they

have heard of from a commercial than one that they have not. Low brand

awareness is a threat for DN. Combined with the low marketing efforts, DN

will not be able to fill the potential profit margin if consumers don’t know

about their brand.

3. Co-branding combined with their experience in the industry to attract

higher

Dresslier can leverage their long experience in the industry by using their

network to gain access to higher performing brands than they would have had

the chance to if they were a new company on the market. Dresslier has a long

history in Australia and this is something other companies will consider when

23deciding to do co-branding. The reason co-branding is an effective strategy is

that it allows us to access the core segment of the brand we do the cooperation

with. The company needs to have the same or very similar customer segment

that is drawn to the same values, attributes and branding strategies as our

segment has. If done correctly, co-branding will open and expose us to a

concentrated group of people that will increase our niche customer group

favourably and increase sales to achieve our marketing goals.

24REFERENCES

Aph.gov.au. (2018). Industrial Chemicals Bill 2017 – Parliament of Australia. [online]

Available at:

https://www.aph.gov.au/Parliamentary_Business/Bills_Legislation/Bills_Search_Results/

Result?bId=r5885 [Accessed 14 May 2018].

Brookins (2018). Critical Success Factors in the Cosmetic Industry. [online]

Smallbusiness.chron.com. Available at: http://smallbusiness.chron.com/critical-success-

factors-cosmetic-industry-12747.html [Accessed 14 May 2018].

Euromonitor International (2017). Hair Care in Australia Country Rapport 2017. [online]

Portal.euromonitor.com.ezproxy.lib.uts.edu.au. Available at:

http://www.portal.euromonitor.com.ezproxy.lib.uts.edu.au/portal/analysis/tab [Accessed

14 May 2017].

Professional Beauty. (2011). Survey: 34% of Australian women choose chemical free

shampoo - Professional Beauty. [online] Available at:

https://www.professionalbeauty.com.au/news/survey-34-of-australian-women-choose-

chemical-free-shampoo/ [Accessed 14 Dec. 2011].

Richardson (2018). IBISWorld Industry Report G4271b. [online]

Clients1.ibisworld.com.au.ezproxy.lib.uts.edu.au. Available at:

http://clients1.ibisworld.com.au.ezproxy.lib.uts.edu.au/reports/au/industry/default.aspx?e

ntid=1879 [Accessed 14 Feb. 2018].

GmbH, f. (2018). Hair Care Market - Global Industry Analysis, Size, Share, Growth, Trends,

and Forecast 2016 - 2024 | Markets Insider. [online] markets.businessinsider.com.

Available at: http://markets.businessinsider.com/news/stocks/hair-care-market-global-

industry-analysis-size-share-growth-trends-and-forecast-2016-2024-1001839738

[Accessed 14 May 2018].

25Inside FMCG. (2018). Australia's best selling shampoo brands - Inside FMCG. [online]

Available at: https://insidefmcg.com.au/2016/11/04/australias-best-selling-shampoo-

brands/ [Accessed 14 May 2018].

Kinonen, S. (2018). Survey: Millennials Want Cleaner Beauty Products. [online] Allure.

Available at: https://www.allure.com/story/millennial-women-green-beauty [Accessed 5

May 2018].

Prnewswire.com. (2018). The Global Shampoo Market 2014-2019 Trends, Forecast, and

Opportunity Analysis. [online] Available at: https://www.prnewswire.com/news-

releases/the-global-shampoo-market-2014-2019-trends-forecast-and-opportunity-

analysis-269209321.html [Accessed 14 May 2018].

Research, i. (2018). WOM has a large impact on sales. [online] Ifwom-research.com.

Available at: http://www.ifwom-research.com/journal/wom-insights/wom-has-a-large-

impact-on-sales.html [Accessed 14 May 2018].

Stephenson Personal Care. (2018). [online] Available at:

http://www.stephensonpersonalcare.com/blog/2017-02-28-category-insight-the-rise-of-

organic-beauty-products [Accessed 13 May 2018].

Stephenson Personal Care. (2018). KNOWLEDGE CORNER: GLOBAL HAIRCARE TRENDS

2016. [online] Available at: http://www.stephensonpersonalcare.com/blog/2016-07-26-

knowledge-corner-global-haircare-trends-2016 [Accessed 9 May 2018].

haircare, D. (2018). Davroe Haircare - Our Mission. [online] Dresslier.com. Available at:

http://www.dresslier.com/davroehistory.htm [Accessed 14 May 2018].

Flora & Fauna. (2018). Vegan & Eco Friendly Products Australia | Flora & Fauna. [online]

Available at: https://www.floraandfauna.com.au/ [Accessed 14 May 2018].

Brand Brief for Daily Naturals. (2018).

Inside FMCG. (2018). Australia's best selling shampoo brands - Inside FMCG. [online]

Available at: https://insidefmcg.com.au/2016/11/04/australias-best-selling-shampoo-

brands/ [Accessed 14 May 2018].

26Global Cosmetic Industry. (2018). Brand Loyalty in the Beauty Industry. [online] Available

at: https://www.gcimagazine.com/marketstrends/segments/skincare/Brand-Loyalty-in-

the-Beauty-Industry-270177131.html [Accessed 14 May 2018].

Statista. (2018). Brand loyalty of conditioner and hair mask consumers U.S. 2017 | Statistic.

[online] Available at: https://www.statista.com/statistics/721216/brand-loyalty-of-

conditioner-and-hair-mask-consumers/ [Accessed 14 May 2018].

Mordorintelligence.com. (2018). Hair Care Market Size, Share | Industry Trends | Forecast

(2018-2023). [online] Available at: https://www.mordorintelligence.com/industry-

reports/hair-care-market-industry [Accessed 14 May 2018].

Sukinorganics.com. (2018). Natural Skin Care Products Australia | Sukin Natural Skin Care.

[online] Available at: https://sukinorganics.com/ [Accessed 14 May 2018].

Bwxltd.com. (2018). [online] Available at: http://www.bwxltd.com/wp-

content/uploads/2017/08/BWX%20Results%20Presentation%20FY17%2016%20Aug.pd

f [Accessed 14 May 2018].

Instagram.com. (2018). Sukin Natural Skincare (@sukinskincare) • Instagram-bilder og -

videoer. [online] Available at: https://www.instagram.com/sukinskincare/?hl=nb

[Accessed 14 May 2018].

Laboratoire Klorane. (2018). Laboratoire Klorane. [online] Available at:

https://www.klorane.com/au-en [Accessed 14 May 2018].

Instagram.com. (2018). Klorane Australia (@kloraneau) • Instagram photos and videos.

[online] Available at: https://www.instagram.com/kloraneau/ [Accessed 14 May 2018].

Inkwood Research. (2018). Hair Care Market | Global Trends, Size, Share | Forecast 2017-

2024. [online] Available at: https://www.inkwoodresearch.com/reports/hair-care-market/

[Accessed 14 May 2018].

Transparencymarketresearch.com. (2018). Hair Care Market - Global Industry Size, Share,

Growth, Trends, Forecast 2024. [online] Available at:

https://www.transparencymarketresearch.com/hair-care-market.html [Accessed 14 May

2018].

27Marketing-schools.org. (2018). Marketing Shampoo | Understanding consumer psychology

and marketing Shampoo .... [online] Available at: http://www.marketing-

schools.org/consumer-psychology/marketing-shampoo.html [Accessed 14 May 2018].

Bloomberg.com. (2018). Here’s How China Is Moving Away From Animal Testing. [online]

Available at: https://www.bloomberg.com/news/articles/2018-01-16/ending-china-animal-

tests-is-salve-for-big-beauty-quicktake-q-a [Accessed 14 May 2018].

Appendix 1

Key partners Key activities Value Customer Customer

propositions relationships segments

National Production

Pharmacies Quality product B2B Direct Pharmacy

B2C Indirect market

Outsourced bottle Improved quality

makers of life

Key Channels

Resources Animal friendly

Partnered online

Physical Supporting store

Australian

Human workers National

Pharmacies

Intellectual Status

Cost Structure Revenue streams

Cost-driven business model Asset sales

Fixed costs Fixed “menu” pricing

Low variable

costs

28PROJECT REPORT 2B

29TABLE OF CONTENT

1.0 Executive summary 31

2.0 Issues resulting from the situation analysis 31

2.3 Creative communication efforts combined with their experience in the industry to attract higher

perceived value brands 32

3.0 Marketing objectives 32

3.1 Promotion strategy 33

3.2 Distribution strategy 33

3.3 Differentiation 34

4.0 Target market and positioning 34

4.1 Positioning 36

5.0 Key Strategies 37

5.1 Promotional Strategies 37

5.1.1 Pull Strategy 37

5.1.2 Product launch campaign and free samples 37

5.1.3 Lifestyle branding as part of Daily Naturals value proposition 37

5.1.4 Cause marketing 38

5.2 Distribution strategies 38

5.2.1 Online distribution 38

5.2.2 subscription-based purchase 38

5.2.3 Increase sales points 39

5.3 Differentiation strategies 39

5.3.1 Differentiation focus strategy 39

5.3.2 Marketing strategy 39

6.0 Key recommendations 40

7.0 References 41

8.0 Appendices 42

301.0 Executive summary

By conducting an external and internal analysis based on primary and secondary research

gathered, the three most impactful issues & opportunities for Daily Naturals was:

Creative communication

Combine their unique Low brand awareness

efforts combined with

product and experience combined with no

their experience in the

with promotional efforts assigned marketing

industry to attract higher

to focus on a niche market department/responsible

perceived value brands

Daily Naturals are in a rare position where they can leverage the expertise of their mother

company Dresslier to better combine their unique product in a promotional package. The

experience & strong brand name of Dresslier also allows DN to aim for higher quality

partners in their supply chain to maintain the qualitative perception of the brand while getting

access to the ‘conscious millennial women’ segment.

Three key objectives to deal with the issues has been established:

1. Promotional objectives: Increase brand awareness of 25% in the target

segment. Increase sales of 50% within a year – monthly sales growth of 4,16%.

2. Distribution objectives: Expand to 10 additional stores in NSW. Receive 10%

of revenue from the online distribution channel.

3. Differentiation objectives: Become the top 3 brand in the all-natural hair-care

niche within 1 year. Achieve a total Social Media following of 10.000+ within 1 year.

To achieve desired sales growth, brand awareness and social media following there will be

implemented strategies for promotion, distribution and differentiation. The strategic measures

outlined in the report should be implemented in a time prioritized matter to achieve maximum

effect. The strategies that are used is justified by thorough research and implementation of

strategic and marketing models & theories.

2.0 Issues resulting from the situation analysis

312.1 Combine their unique product and experience with promotional efforts to

focus on a niche market

Use DN’s strength of having an experienced staff within the hair-care industry leveraged

towards promotional efforts on social media and other channels to promote DN in the best

possible way.

2.2 Low brand awareness combined with no assigned marketing

department/responsible

DN has low brand awareness in the market. The shampoo & conditioner market has low

customer loyalty, and customers are easily swayed to try new products if it offers the right

value proposition to them. DN has no assigned marketing responsible from Dressliers

marketing team, this is neglecting a big opportunity that could increase sales substantially.

2.3 Creative communication efforts combined with their experience in the

industry to attract higher perceived value brands

Use Dressliers strong position as an established player in the hair-care industry to attract

partnerships with higher perceived value brands to access their quality-focused segment of

millennials. Co-branding, better distribution networks, and goodwill with suppliers are some

of the opportunities.

3.0 Marketing objectives

Marketing objectives are defined as goals a business sets when they want to promote their

product to potential customers that will be achieved within a set timeframe. (Business

dictionary 2017) These following objectives follow the SMART framework and are made to

solve and take advantage of our three key issues. Incorporation in detail is set in the action

plan in the appendix (figure 13)

323.1 Promotion strategy

Specific: Create IMC plan to promote Daily Naturals as a hair-care brand

Issue: Low brand awareness combined with no assigned marketing department/responsible

Objective: Increase brand awareness by 25% in the target segment. Increase sales of 50%

within a year – monthly sales growth of 4,16%.

Measure: Social media-following, SEO & Quarterly sales report

When: Create IMC plan by 01.10.18. Reach the goal within 01.10.19.

Strategy: 1. Pull strategy 2. Product launch strategy 3. Cause marketing

The objective of promotional efforts is made to increase the awareness of DN’s product in the

market, increase customer knowledge, and most importantly, increase sales. This objective is

linked to the low brand and product awareness of DN in the market. This objective is essential

as it will help differentiate DN from the competition, averting Sukin and Klorane to take

additional market share.

The expected growth for natural products is expected to grow at a much more rapid rate than

the main-stream hair-care market. (Richardson 2018) DN should position themselves through

promotional efforts to capitalize on this trend as it is more profitable, less competitive and

long-term sustainable. DN is still in its early life-cycle stage and have good potential to grow

with the millennials as their main segment.

3.2 Distribution strategy

Specific: Expand points of penetration in the market to more sales point, as well as online

channels

Issue: Low brand awareness and low market penetration

Objective: Expand to 10 additional stores in NSW. Receive 10% of revenue from the online

distribution channel.

Measure: Quarterly & annual reports for sales

When: Within 01.10.19

Strategy: 1. Expand market penetration width 2. Expand channels to online

By expanding and improving the current business model of DN, they will be more exposed

and have a wider penetration of the market. This objective addresses the issue of low brand

awareness and the fact that they can leverage their existing experience & recognition to

33achieve good product placement in spa’s, massage places and other pharmacies. Although

distributors will sell their product, it is important that DN keeps strong partnerships and an

open information flow with the distributors to continuously improve the product, promotion,

process, and placement.

DN should create an online channel to sell their product to make it more convenient and

friction-free for consumers to purchase the product, this is especially important because many

of the promotional measures will be conducted online.

3.3 Differentiation

Specific: Focus on a niche market with high profitability, and differentiate through marketing

& branding

Issue: Competitors have a dominant position in the niche areas of the market. Ineffective

communication efforts.

Objective: Become the top 3 brand in the all-natural hair-care niche within 1 year. Achieve a

total Social Media following of 10.000+ within 1 year.

Measure: Annual sales report vs. industry

When: Within 01.10.19

Strategy: 1. Differentiation focus strategy 2. Marketing strategy

The differentiation strategy is necessary for major success in the market. Our research has

uncovered what our segment looks for in brands, and to capitalize on this will set DN in a

higher perceived value than their competitors. If done right, brand image is a sustainable

competitive advantage.

The objective addresses low brand awareness, their high industry experience, and their unique

product to create a package that will increase sales sustainably over the long-term. The

strategies utilized will be in combination with promotional efforts such as cause marketing

and co-branding to differentiate effectively.

4.0 Target market and positioning

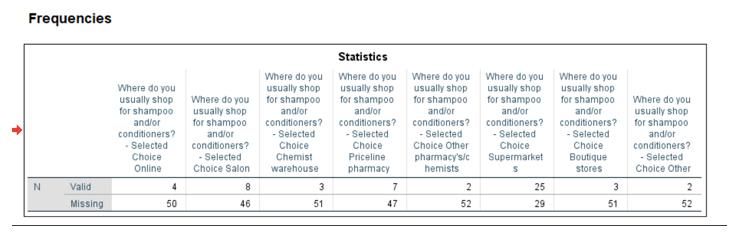

Based on respondent’s answers in the analysis shown in figure 1 & secondary research

(Richardson 2018), we have decided that women in NSW are the best match for our product.

34Women have a clear preference towards DN’s bottles in comparison to men, which prefer

Klorane. This was also confirmed by an interviewee: “I like the simple packaging with little

information.” And the 24-year-old women also told us: “It looks intelligent and classy… that

doesn’t have heaps of writing on it in order to sell”. This reinforces the idea.

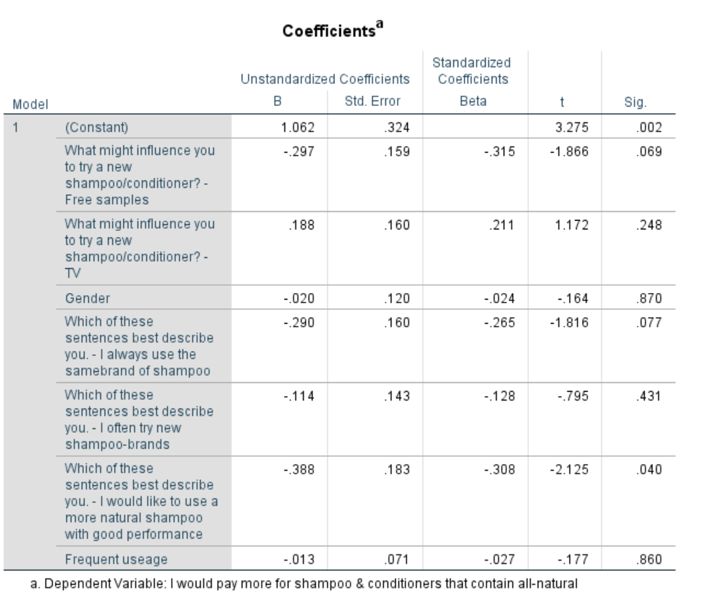

The target market prefers all-natural, cruelty-free products, but they also want the same

performance as the saloon. Figure 4 shows that 24,1% of the sample would pay more for all-

natural products, and 14,8% would pay more for cruelty-free products. This means that DN

can justify a higher price, and it can be used in marketing efforts. Figure 2 shows that the

current awareness of our sample is only around 31% regarding all-natural and cruelty-free

products, which means that most people in the sample don’t have much knowledge in the

field. This was also confirmed in an in-depth interview, where one girl admitted: “I would

purchase their product if I knew it was cruelty-free now.” This is also something DN can use

in their marketing, teaching & informing. Figure 5 shows us a significant correlation between

people that claim to be all-natural hair product users and the fact that they would pay more for

the product.

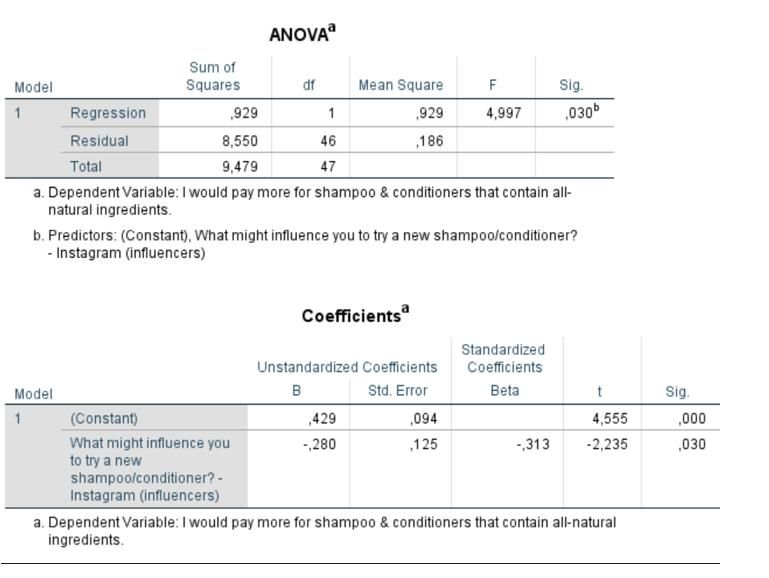

Our segment is also very influenced by Instagram (IG), and other platforms online. This will

make our marketing more effective as we can reach a wide number of people with less costs

than traditional marketing efforts would allow. This is confirmed by figure 8 which tells there

is a significant coefficiency between people that are influenced by IG and people that would

pay more for all-natural products. And figure 10 that tells us there is also a significant

relationship between people influenced by IG and how much people spend on hair-care

products.

Daily Naturals should target the conscious women millennial segment. Of the current

Australian workforce, 37.0% is millennials between 16-35 years. (Figure 14) This segment is

in constant growth and they have a substantial purchasing power that only will grow as they

get older and into more executive, senior positions in their work-life-cycle. (Ruthven P. 2017)

A BCG report concluded that millennials trust has shifted from looking to experts with a

professional or academic background to recommend the products, to potentially anyone with

firsthand experience, which ideally should be a peer or a friend. (Barton C. 2012) We can

further justify this claim up by our primary research, as our in-depth interviewees were clear

about how easily influenced they were from friends and coworkers.

35Another reason to target this segment is the fact that they have larger social networks than

other generations. 79% of millennials use social media platforms regularly and have more

connections on the platforms than non-millennials. (Barton C. 2012) Millennials want to

make the world a better place, in general. A study found that millennials would be less

inclined to make a one-off charitable donation, and rather integrate their causes into daily life

by being an ‘ethical buyer’ or ‘conscious purchaser’. (Barton C. 2012) This means buying

products that are aligned with their values of sustainability, like ‘fair trade’, or other products

that have a cause behind them.

Figure 15 is a summary of the ‘Conscious Millennials women’ segment’s characteristics.

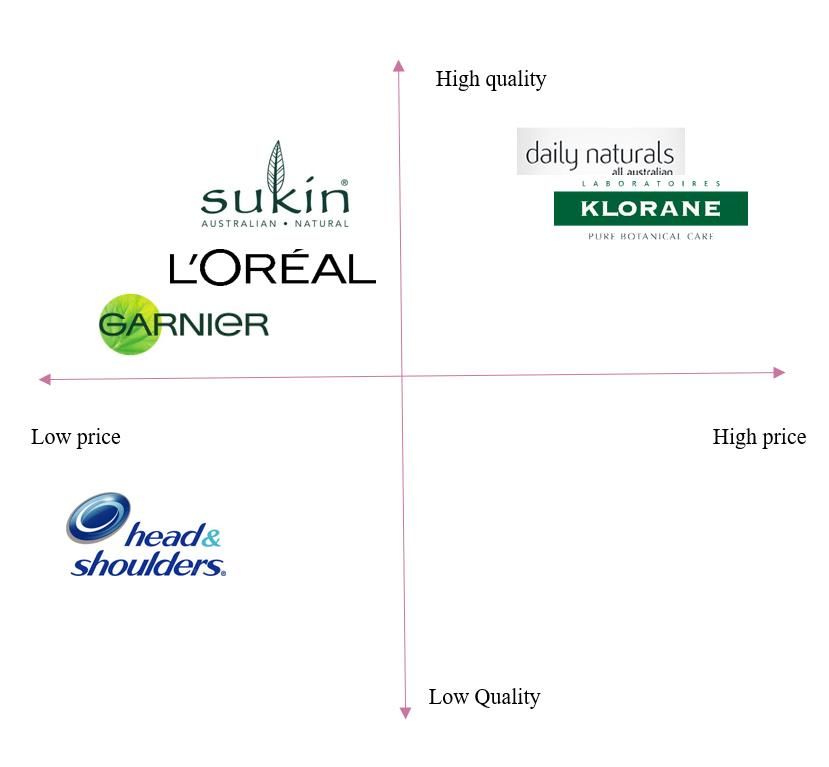

4.1 Positioning

Sukin as the main competitor is positioned as an all-natural hair-care brand with a medium

price range. The main weakness of Sukin is the fact that they are skin-specialists. Daily

Naturals should position themselves as a hair-specialist, providing a premium, high-quality

product with a cause (Being all-natural & cruelty-free). By claiming to be a specialist you can

defend the high pricing, and consumers will have a higher perceived quality in relations to the

product. As uncovered in our survey, our main segment wants all-natural products, and are

willing to pay more for them. This is more important than being Australian made & owned

and should be communicated in a higher regard. The primary research done for this report has

revealed a potential attractive niche in the hair-care market that Daily Naturals should exploit

by investing into an IMC campaign.

A report conducted by Euromonitor claims “The health and wellness trend will also support

the growth of natural hair care brands … brands with a strong natural positioning are expected

to perform well” (Euromonitor 2018) This means that current trends are supporting the

positioning recommendation which can furthermore be justified by claims from IBISWorld

(Richardson 2018). If Daily Naturals can position themselves as a ‘strong natural’ brand they

will take advantage of sociocultural trends in the market. They will also operate in a niche

market that has a much higher growth than the traditional mainstream hair-care market.

The perceptual map in the appendix (figure 12) is the all-natural pharmacy hair-care products

in Australia, where we have included the most relevant to this case. We can currently see

where in the map there is a room that represents an opportunity for Daily Naturals.

36You can also read