Can the bull market continue? - Presentation to Momentum Think Tank 2020 Steven Bell, Chief Economist - Momentum Global Investment ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Private and confidential

Can the bull market continue?

Presentation to Momentum Think Tank 2020

Steven Bell, Chief Economist

21st September 2020

Key Issues The virus: is it winning?

US politics: likely outcomes, likely impact

Can the bull market continue?

2

Tracking Covid-19

US second wave turns, possibly in Europe too …new cases tumble in key US states

80,000 7%

Daily Coronavirus New Cases Daily % Increase in Total Coronavirus Cases

Increase in Confirmed Cases (7 day m.a.)

70,000

Daily Cases (7 day mov. ave.)

6%

Arizona Florida

60,000

5%

50,000

US 4% Texas

40,000

South Carolina

3%

30,000

2% California

20,000

Nevada

Europe

10,000 1%

0 0%

Mar Apr May Jun Jul Aug Sep 01 May 22 May 12 Jun 03 Jul 24 Jul 14 Aug 04 Sep

Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020 Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020

.

• Europe had been outperforming the US but the gap has narrowed markedly

• Global daily cases of COVID-19 continue to rise. Daily deaths have fallen from their peak.

• Medical progress in therapeutics and testing has been remarkable. Oxford vaccine trials are critical as it is months ahead of rivals and could be available in

large quantities by the autumn. Uncertainty remains until results are published and analysed. The recent halt to the trial is worrying but probably not critical.

Past performance is not indicative of future performance.

3Second Waves in Europe

Daily % increase in Total Coronavirus cases

3.0%

Increase in Confirmed Cases (7

UK

2.5%

France

day m.a.) 2.0%

Spain

1.5%

1.0%

Netherlands

0.5%

Germany Italy

0.0%

01 May 01 Jun 01 Jul 01 Aug 01 Sep

Source: BMO Global Asset Management and Bloomberg as at 7 September 2020

4Tracking Covid-19

Some EM countries are suffering badly … …but infections among the UK general public are flat

90,000

Daily Coronavirus New Cases % testing positive for COVID-19

80,000 0.5

Daily Cases (7 day mov. ave.)

India

70,000

0.4

60,000

50,000 0.3

Brazil

40,000

0.2

30,000

20,000 0.1

Russia

10,000 Mexico

Saudi Arabia 0.0

0 6 May to 20 May 3 Jun to 17 Jun to 1 Jul to 15 Jul to 29 Jul to 12 Aug to

Mar Apr May Jun Jul Aug Sep 19 May to 2 Jun 16 Jun 30 Jun 14 Jul 28 Jul 11 Aug 25 Aug

Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020 Source: ONS, as at 3 September 2020

.

• The virus seems to be out of control in certain EM where social distancing is impractical and health care systems are inadequate

• A high quality UK study of infection within the community (excluding those in hospital etc.) shows a rate of incidence that has been flat since lockdowns

were eased. Separate data show a sharp rise in new cases and a limited national lockdown has been reimposed.

Past performance is not indicative of future performance.

5A global recession

2020 growth forecasts are edging up except in UK .. …and data surprises remain positive

6 50 125

Forecasts GDP Growth

4 40 100

Global Economic

Forecast GDP (% year / year) 2 30 Surprise Index 75

(Goldman Sachs)

20 50

0

Canada 10 25

EM

Index

-2

Index

0 0

-4

US -10 -25

-6 -20 -50

Euro Area

-8 -30 Global Economic -75

Surpise Index (Citi)

-10 -40 -100

UK

-12 -50 -125

Jan Feb Mar Apr May Jun Jul Aug Sep 2015 2016 2017 2018 2019 2020

Source: Bloomberg, as at 3 September 2020 Source: Bloomberg, as at 3 September 2020

• Recent data for European economic activity have come in in weaker than expected. With strong second waves in

France and Spain and a more modest second wave in Germany, hopes of rapid recovery have receded.

• UK data have recently come in much stronger than expected but reimposed lockdown raises risks.

• Despite the well-documented problems with the virus in the US, recent data, notably on housing and the labour

market have been strong. This is a significant surprise. .

Past performance is not indicative of future performance.

6Massive monetary and fiscal support

Central banks cut rates aggressively… …along with very large fiscal support

80 US Budget Balance (% of GDP)

Recession 5

Cumulative Interest Rate cuts in

70

60 0

OECD countries

50

% of GDP

-5

40

30 -10

6m rolling sum

20

-15

10 Consensus

Forecast

0 -20

2000 2003 2006 2009 2012 2015 2018 1970 1980 1990 2000 2010 2020

Source: BMO Global Asset Management and Bloomberg as at September 2020. Note: Central Banks/ countries considered are Source: BMO Global Asset Management and Bloomberg as at September 2020.

ECB, Fed, BoE, Australia, Canada, Chile, Denmark, Hungary, Iceland, Israel, Japan, South Korea, Mexico, New Zealand, Norway,

Poland, Sweden, Switzerland and Turkey.

• Cutting interest rates helps a little but non-traditional measures by central banks help more. Fed buying credit, QE

to infinity and measures by ECB notable.

• Huge fiscal response underway. Many of the massive US measures expire soon and a new package is needed.

Progress has been limited.

Past performance is not indicative of future performance.

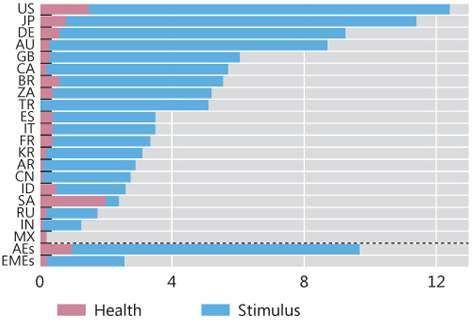

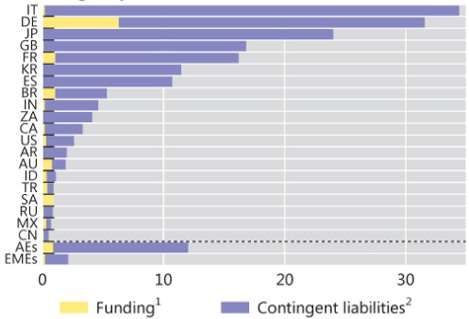

7Pledged Fiscal Packages

Budgetary measures Non-budgetary measures

Source: IMF, Fiscal Monitor, April 2020 and update June 2020; IMF, World Economic Outlook; BIS calculations.

Estimates focus on government discretionary measures that supplement existing automatic stabilisers, which differ across countries in their breadth and scope. AEs = AU, CA, DE, ES, FR, GB, IT, JP

and US; EMEs = AR, BR, CN, ID, IN, KR, MX, RU, SA, TR and ZA. For regions, weighted averages based on GDP and PPP exchange rates.

1 Equity injections, asset purchases, loans and debt assumptions, including through extra-budgetary funds. 2 Guarantees on loans and other contingent liabilities such as loans channelled through

public financial agencies.

• Huge support globally is unevenly distributed and hard to gauge.

• The US has led the way of fiscal support but many lower income countries have been unwilling or unable to do

much on this front. Loan guarantees have been a big feature in many countries, notably Japan and Germany (who

can easily afford it) and Italy (who cannot).

Past performance is not indicative of future performance.

8Long-term US real rates fall ever lower

Risk-free rate is very low… …but US jobs needs continued fiscal support

Yield on 10 year US inflation protected security 5000 17.0

1.5

Peak = 1.16 15.0

1 4000

US 13.0

Claims (thousands)

0.5 Unemployment

3000

Rate 11.0

%

%

0

Average US Initial Jobless 9.0

2000

2017 = 0.44 Claims (4 week

-0.5 moving average) 7.0

Latest 1000

-1 = 5.0

-0.99

-1.5 0 3.0

2017 2018 2019 2020 1990 1994 1998 2002 2006 2010 2014 2018

Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020 Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020

• The yield on 10-year US Treasury Inflation-Protected Securities - a key component of the discount rate for assets like equites whose income is likely to rise

with inflation – fell heavily since late 2018 and has recently hit a record low.

• Massive fiscal support, notably in the US has cushioned the blow of sudden, sharp, deep recession. Many forecasters are worried about further economic

weakness as fiscal support is withdrawn. Many measures expired at the end of July and a new package is needed. But low interest rates limit the pressure to

reduce deficits.

Past performance is not indicative of future performance.

9US economy now stronger than Europe again

60

US

Composite PMI Index

50

40

30

Eurozone

20

10

Sep 17 Mar 18 Sep 18 Mar 19 Sep 19 Mar 20

15

Composite PMI Index

US - Eurozone

10

5

0

-5

Sep 17 Mar 18 Sep 18 Mar 19 Sep 19 Mar 20

Source: BMO Global Asset Management and Bloomberg as at 7 September 2020

10US Economy: High Frequency Measures

Big Data Mobility Measures US Daily Travel, dining measures YoY Change

160 20

140 0

Driving

Mar 20 Apr 20 May 20 Jun 20 Jul 20

120

-20

100

Walking Homebase Total

-40

80 Hours Worked

60 Transit -60

US TSA Traveler

40 -80 Throughput

20

-100

OpenTable Seated

0

Diners

Jan 20 Feb 20 Mar 20 Apr 20 May 20 Jun 20 Jul 20 -120

• The recovery in mobility data has largely flattened since mid-June.

Sources: U.S. Transportation Security Agency, Opentable, Homebase, Bloomberg, Apple Mobility Trends Reports. Data through August 2, 2020.

11Politics and Policy

Image source: istock photo

12Who will win the US election?

Trump approval rating has fallen Betting markets pricing Democrat clean sweep

48 100

Trump Approval Rating 90

46 80 Democratic Controlled House

70

44

60 Democratic President

50

%

%

42

40

40 30

20 Democratic Controlled Senate

38

10

36 0

2017 2018 2019 2020 Sep 19 Nov 19 Jan 20 Mar 20 May 20 Jul 20 Sep 20

Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020 Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020

• US election is a major risk for this year and Trump’s approval rating has fallen significantly since the virus struck

• Betting markets and polls suggest the election will be very close but the odds on Democrats regaining the Senate and the White House have risen

• The race remains close

Past performance is not indicative of future performance.

13Europe

Purchasing managers’ indices bounce … …but markets see continue low inflation

Euro Area PMIs German 10y Breakeven

70 1.6

1.4

60

1.2

50

1

PMI Index

Manufacturing

%

40 0.8

0.6

30

0.4

Services

20

0.2

10 0

2017 2018 2019 2020 2016 2017 2018 2019 2020

Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020 Source: BMO Global Asset Management and Bloomberg, as at 7 September 2020

Europe is well on the way to easing the lockdown and the economy has responded.

But second waves are evident in many countries and lockdown easings have been delayed or reversed

Past performance is not indicative of future performance.

14UK overtakes Europe

60

Composite PMI Index

50

UK

40

30

Eurozone

20

10

Sep 17 Mar 18 Sep 18 Mar 19 Sep 19 Mar 20

8

UK - Eurozone

Composite PMI Index

4

0

-4

-8

Sep 17 Mar 18 Sep 18 Mar 19 Sep 19 Mar 20

Source: BMO Global Asset Management and Bloomberg as at 7 September 2020

15UK High Frequency Data shows strong pick up

Electricity Usage normalised for temperature Spending Trends

and long term trend

115 30

Online

Spending Trends (28 day and 7

20

Electrical Power Actual Load

110

10

day averages, % y/y)

Total

Usge (5 day m.a.) 105

0

100 -10

-20

95

-30

90 Offline

-40

85 -50

80 -60

Jan 20 Mar 20 May 20 Jul 20 Jan Feb Mar Apr May Jun Jul Aug Sep

Source: Barclays, as at 7 September 2020 Source: Barclays, as at 7 September 2020

Past performance is not indicative of future performance.

16China versus the world

China’s PMIs back close to pre-covid levels… …and the rest of the world is catching up

60

70 Global Services Jan10-Dec19 Avg: 53.2

Construction Jan10-Dec19 Avg: 59.9 Current:

65 55

Current: 60.2 51.9

60 50

Current: Global Manufacturing Jan10-Dec19 Avg: 51.7

55 55.2 45

PMI Index

50 Current:

Non-Manufacturing Jan10-Dec19 Avg: 55.1 Current 40

45 : 51.0 51.8

Manufacturing Jan10-Dec19 Avg: 51.0 35

40

35 30

30 25

25

20

Source: BMO Global Asset Management and Bloomberg as at 7 September 2020 Source: BMO Global Asset Management and J. P. Morgan as at 8 September 2020.

• China’s more severe lockdown has limited second waves and allowed almost complete recovery.

• The RoW was catching up fast but second waves and higher infection rates means that lockdowns in the US and

parts of Europe have been reimposed or easings delayed. EM countries like India and Brazil are still suffering badly

from the virus.

Past performance is not indicative of future performance.

17Emerging Markets

EM easing on all fronts… …EM PMIs above DM

50 Composite PMIs

Recession 60

Cumulative Interest Rate cuts in

45

55 Emerging Markets

EM (largest 15 by GDP)

40

35 50

30 45

PMI Index

25 40

6m rolling sum

20

35

15 Developed Markets

30

10

5 25

0 20

2000 2003 2006 2009 2012 2015 2018 2018 2019 2020

Source: BMO Global Asset Management and Datastream, as at September 2020 Source: BMO Global Asset Management and Bloomberg, as at September 2020

• Emerging market central banks have turned incrementally dovish year-to-date motivated by slowing growth expectations, continued disinflation and

monetary policy easing in developed economies. There is plenty of headroom for sustained policy accommodation.

• The shift in monetary policy stance seems sustainable given the dovish shift in DM central banks; a broad-based slowdown in both export and domestic EM

growth; continued disinflation from lower energy prices

Past performance is not indicative of future performance.

18Earnings outlook improves…

2020 EPS heavily revised down… …but Q2 results have beaten low expectations

40 20

MSCI All Country EPS Growth S&P 500 2020 Quarterly EPS

30 10

EPS Growth (% y/y)

% growth (year / year) 2021

20 2017 0

2018

2013 2014

10 -10 Q4

2016

2012 2019 Q1

0 -20

2015 Q3

-10 -30

2020 Q2

-20

-40

-30

-50

2012 2013 2014 2015 2016 2017 2018 2019 2020

Jan Feb Mar Apr May Jun Jul Aug Sep

Date forecast made Date Forecast Made

Source: BMO Global Asset Management and Datastream, as at September 2020 Source: BMO Global Asset Management and Bloomberg, as at September 2020

• EPS forecasts for 2020 have been slashed but projections for 2021 are above 2019. Q2 reporting season has seen

a high % of companies beating analysts’. Significant beats on a cap-weighted basis are less impressive. With

economic data surging, estimates for earnings in 2020H2 may start to improve but a setback to economic recovery

in the US and Europe could lead to a double dip unless a vaccine come to the rescue.

Past performance is not indicative of future performance.

19…and could improve further

Bounce in EPS forecasts … …and guidance is strong

US Earnings 30% 75

50

Earnings Revisions (%, 4w mov av)

40 20% S&P 500 Earnings Revisions

S&P 500 12m forward ((Upgrades - Downgrades) / Total)

EPS Growth (%yoy) 30 EPS change (% yoy) 10%

20 0% 50

10

Index

-10%

0

-20%

-10

-30% US Company Profit 25

-20 Outlook Index

Model -40%

-30 estimate

-40 -50%

-50 -60% 0

1998 2001 2004 2007 2010 2013 2016 2019 Jan 19 Apr 19 Jul 19 Oct 19 Jan 20 Apr 20 Jul 20

Source: BMO Global Asset Management, Bloomberg and Datastream, as at September Source: BMO Global Asset Management, Bloomberg and Datastream, as at September

2020 2020

• The recent Q2 earnings season at -35% y/y is the worst since the GFC but came in better than expected. EPS surprise (+22%) for those that have reported

has been the strongest since 2009 but sales surprise has not been as strong (+2%). U.S. companies profit-outlook index, compiled by Bloomberg and

based on corporate revisions to forecasts was recently at a record high and remains elevated.

Past performance is not indicative of future performance.

20What news on a vaccine? Classification: only to be shown if not public

• Phase 1/II trials in UK show Oxford vaccine is safe and produces T-cells and

antibodies

• Phase III trials started in June. Recent halt to trials may merely be temporary

setback

• 100 million doses ordered by UK, 300 million by US, 300million by EU

• 30mn due in the UK by September, US may have the vaccine by 3 November

• Moderna started Phase III trials in late July. 9 vaccines in Phase III trails

• High probability that one or more of the vaccines will be successful

Source: BMO Global Asset Management

21Classification: only to be shown if not public

Conclusions:

The virus is fighting back but wil probably be

defeated by a vaccine. This would be a game

changer

US suffering serious second wave, Europe’s second

wave is gathering force

Political uncertainty headed higher in the US. Major

market implications

Life will never be the same again but pre-covid levels of

economic activity and earnings regained by end 2021.

Risk assets would receive boost from good news on a

vaccine

22 22Acronyms, definitions and explanations

EPS = earnings per share. P/E = ratio of share price to earnings

US CPI and PCE deflator There are two common measures of inflation in the US today: the Consumer Price Index (CPI) and the Personal Consumption Expen ditures price

index (PCE) The CPI gets more press, it is used to adjust social security payments and is the reference rate for Treasury Inf lation Protected Securities (TIPS) and inflation swaps.

The Federal Reserve, however, states its goal for inflation in terms of the PCE.

Core consumer prices exclude volatile for and energy. In Japan the core measure excludes fresh food (notably fish); the core core measure also excludes food and energy.

Trimmed mean inflation excludes the extremes of price movements. The closely-followed US PCE version compiled by the Cleveland Federal Reserve excludes the bottom and

top 8% of monthly movements. We think it is a better measure of underlying inflation than the core.

Purchasing managers’ indices, PMIs The Purchasing Managers' Index (PMI) is an index of the prevailing direction of economic trends in the manufacturing and service

sectors. An index of construction is also provided for a few countries. In China, we tend to use the indices complied by the National Bureau of Statistics. The Canadian PMI

relates purely to manufacturing which is more volatile; we use a six month moving average.

Breakeven inflation This is derived either directly from the swap market or as the difference between the yield on conventional government bonds and their inflation-protected

equivalent. 5x5 measures the 5 year breakeven inflation rate 5 years ahead.

BOC. Bank of Canada, BoE Bank of England, Fed, FOMC the FOMC is the rate setting body in the US, part of the Federal Reserve

FTA a free trade agreement that imposes zero tariffs between the countries concerned

Sources: BMO GAM, Cleveland Federal Reserve, Investopedia

23You can also read