Brookfield Global Listed Real Estate - Brookfield ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Brookfield Global Listed Real Estate

Q1 2019

© 2019 Brookfield Public Securities Group LLC

Brookfield’s Real Estate Business & Securities Team

Jason Baine Bernhard Krieg, CFA Iconic Brookfield Assets1

Portfolio Manager Portfolio Manager

23 Years of Investing Experience 21 Years of Investing Experience

18 Years with Brookfield 13 Years with Brookfield

Launched Brookfield’s real estate Extensive long/short and real estate

securities platform in 2001 securities experience

Supported by Nine Analysts

Average 13 years experience 5 Manhattan West | New York

Cross-border coverage with regular coverage rotations

Centralized team in Chicago

One of the largest real estate investors in the world1 CityPoint | London

Brookfield Place | Toronto

History of buying assets on a value basis

Own some the world’s most iconic real estate assets

Global operator for over 120 years1 Woodlands Mall | Houston Brookfield Place | New York

$188 billion1

REAL ESTATE ASSETS

UNDER MANAGEMENT Canary Wharf | London

As of December 31, 2018. 1. Assets under management for Brookfield Asset Management Inc. includes its affiliates. Brookfield Public Securities Group LLC has approximately $20

billion in total assets under management as of December 31, 2018 and includes discretionary, non-discretionary and administrative. Values may not add to the total due to rounding.

Iconic Brookfield Assets are not held be the fund.

2

Why Do Demographics Matter?

Population Growth Home Price Growth

(2001-2017) (2001-2017)

30% 120%

27%

101%

90%

20% ~2X ~2X

Growth Growth

14% 60%

52%

10%

30%

0% 0%

Population Median Home Price

U.S. Seattle U.S. Seattle

As of July 2, 2018. Source: Biggest US Cities by Population; Zillow Home Value Index

3

Cost of Living

2 Parent & 2 Child Households – Per Month

San Francisco Austin

Housing $3,121 -$1,870 Housing $1,251

Food $998 Food $738

Child Care $1,730 Child Care $1,108

Transportation $1,114 Transportation $1,150

Health Care $1,152 Health Care $964

Other Necessities $1,662 Other Necessities $802

Taxes $2,593 -$1,875 Taxes $718

Monthly Total $12,370 -$5,639 Monthly Total $6,731

New York City Nashville

Housing $1,789 -$787 Housing $1,002

Food $908 Food $792

Child Care $2,773 Child Care $1,052

Transportation $589 Transportation $1,170

Health Care $1,238 Health Care $1,170

Other Necessities $1,088 Other Necessities $724

Taxes $1,958 -$1,265 Taxes $693

Monthly Total $10,343 -$3,740 Monthly Total $6,603

As of March 2018. Source: Economic Policy Institute. Costs are in 2017 dollars

4

Quality of Life

Average One-Way Average Yearly

Commute Time Temperature

Austin 23.8 min Miami 77.05 F

Nashville 24.3 min Austin 69.4 F

Miami 28.5 min Nashville 59.25 F

Chicago 31.3 min San Francisco 57.3 F

San Francisco 32.4 min New York 55.15 F

New York City 40.3 min Chicago 51.3 F

As of December 20, 2017. Source: US Census Bureau 2016; usclimatedata.com

5

Current State Income Taxes

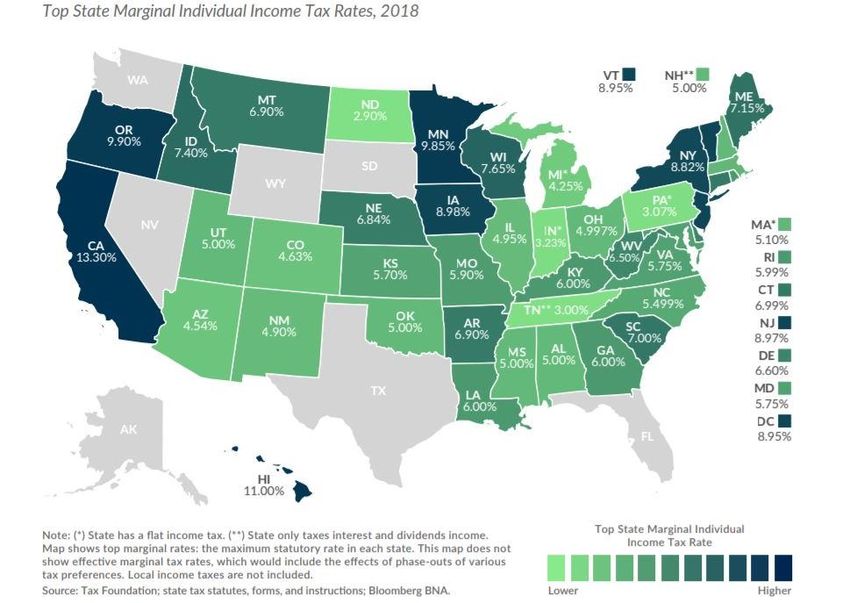

As of March 5, 2018. Source: taxfoundation.org 2018

6

Future Tax Liabilities – Pension Liabilities

Pension Promises Grew Faster than GDP Funded Ratios Declining

(2003-2016) (2003-2016)

New York New York

141% difference

New Jersey New Jersey

-62% difference

California

California

Illinois

Illinois

Tennessee

Tennessee

Texas

Texas

0% 20% 40% 60% 80% 100% 120% 140% 160% 180% 0% 20% 40% 60% 80% 100% 120%

2003

GDP

Accrued Liabilities 2016

As of July 20, 2018. Source: Overpromising has crippled public pensions. A 50-state survey by Ted Dabrowski and John Klinger

7

Future Tax Liabilities – Aging Infrastructure

Aging Infrastructure by Area

60%

50%

40%

30%

20%

10%

0%

CALIFORNIA NEW YORK ILLINOIS NORTH TEXAS TENNESSEE FLORIDA

CAROLINA

% of Roads in Poor Condition % of Structurally Deficient Bridges

As of April 10, 2018. Source: U.S. Department of Transportation; 2017 Infrastructure Report Card.

8

Historical Population Growth

Coastal & Northern Sunbelt

3.5% 3.5%

3.0% 3.0%

2.5% 2.5%

2.0% 2.0%

1.5% 1.5%

1.0% 1.0%

0.5% 0.5%

0.0% 0.0%

2011

2012

2013

2014

2015

2016

2017

2011

2012

2013

2014

2015

2016

2017

San Francisco New York Austin Nashville

As of December 20, 2017. Source: U.S. Census Bureau, 2017.

9

Faster Growth in Sunbelt Talent Pools

Texas Tennessee

Residents with bachelor’s Residents with bachelor’s

degrees degrees

3.2M 21.0% 712K 16.7%

Total Growth Total Growth

(2010-2016) (2010-2016)

549K 102K

New since 2010 New since 2010

California New Jersey New York

Residents with bachelor’s Residents with bachelor’s Residents with bachelor’s

degrees degrees degrees

5.1M 13.7% 1.7M 2.7M 12.1%

Total Growth

Total

10.8% Total

Growth

(2010-2016) Growth

619K 138K (2010-2016) 286K (2010-2016)

New since 2010 New since 2010

New since 2010

As of December 20, 2017. Source: U.S. Census Bureau 2016.

10Recent Corporate Relocations and Expansions

Austin Nashville

Company Jobs Company Jobs

Apple 5k - 15,000 Amazon 5,000

Oracle 10,000 Alliance Bernstein 1,050

Charles Schwab 1,500 Asurion 400

Indeed 1,500 Tenneco 200

Amazon 800 Five Star Custom Foods 138

General Motors 500 Medline Industries 100

PIMCO 200

As of September 1, 2018. Source: Austin Chamber of Commerce (2017-2018); Nashville Chamber of Commerce (2017-2018).

11Dual Demographic Wave

Annual U.S. Population Change

Forecasted

Annual U.S. Population Change

Forecasted

(Ages 25-45) (Ages 65+)

2.2 2.2

2 2

1.8 1.8

1.6 1.6

1.4 1.4

1.2 1.2

Millions

Millions

1 1

0.8 0.8

0.6 0.6

0.4 0.4

0.2 0.2

0 0

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2012

2014

2016

2018

2020

2022

2024

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

As of December 20, 2017. Source: U.S. Census Bureau 2017 National Population Projection Data.

12Migration Pattern

As of December 20, 2017. Source: U.S. Census Bureau 2017

13Higher Growth in Sunbelt Office Jobs

Coastal & Northern Sunbelt

6% 6%

5% 5%

4% 4% 50% growth

3% 3%

40% growth

2% 21% growth

2%

1% 1%

7% growth

0% 0%

-1% -1%

-2% -2%

-3% -3%

-4% -4%

-5% -5%

-6%

-6%

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

San Francisco New York Austin Nashville

As of January 31, 2018. Source: Bureau of Labor Statistics (BLS) and Baird Research.

14Office Employment & Net Migration Forecasts

Q2 2018 – Q2 2020 Forecast

3.0% Austin

Orlando

Houston

Dallas

2.5%

Las Vegas Tampa

San Antonio

Office-using Employment Growth

Phoenix Raleigh

2.0%

Miami

Nashville

Memphis

1.5% Baltimore Charlotte

Atlanta U.S. National

Chicago

Sacramento

San Diego

1.0% Los Angeles Norfolk

Boston

San Francisco

New York

0.5%

Washington D.C.

0.0%

-2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Net Migration (% of Population)

Gateway Major Non-Gateway Secondary Sunbelt Secondary Snowbelt

As of September 13, 2018. Source: Cushman & Wakefield.

15Office Supply

San Francisco Austin

Forecasted

Forecasted

5% 40% 12% 40%

35% 35%

4% 10%

30% 30%

8%

3% 25% 25%

20% 6% 20%

2% 15% 15%

4%

10% 10%

1% 2%

5% 5%

0% 0% 0% 0%

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

Completions (% of existing stock) Vacancy Rate Completions (% of existing stock) Vacancy Rate

New York Forecasted Nashville

Forecasted

4% 20% 8% 25%

3% 18% 7%

2% 16% 20%

6%

1% 14%

12% 5% 15%

0%

10% 4%

-1%

8% 3% 10%

-2% 6%

-3% 2%

4% 5%

-4% 2% 1%

-5% 0% 0% 0%

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

Completions (% of existing stock) Vacancy Rate Completions (% of existing stock) Vacancy Rate

As of December 31, 2018. Source: CBRE Econometric Advisors.

16Office Rents

Cumulative Rent Growth

200%

164%

150% 158%

100%

75%

65%

50%

0%

-50%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

San Francisco Austin New York Nashville

As of December 31, 2018. Source: CBRE Econometric Advisors.

17Apartment Supply

San Francisco Austin

Forecasted

Forecasted

6% 9% 6% 9%

8% 8%

5% 5%

7% 7%

4% 6% 4% 6%

5% 5%

3% 3%

4% 4%

2% 3% 2% 3%

2% 2%

1% 1%

1% 1%

0% 0% 0% 0%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Completions (% of existing stock) Vacancy Completions (% of existing stock) Vacancy

New York Nashville

Forecasted

Forecasted

6% 9% 6% 9%

8% 8%

5% 5%

7% 7%

4% 6% 4% 6%

5% 5%

3% 3%

4% 4%

2% 3% 2% 3%

2% 2%

1% 1%

1% 1%

0% 0% 0% 0%

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Completions (% of existing stock) Vacancy Completions (% of existing stock) Vacancy

As of December 31, 2018. Source: Axiometrics, a RealPage Company.

18Apartment Rents

Cumulative Rent Growth

80%

70% 71%

60%

55%

50%

50%

40%

30%

25%

20%

10%

0%

-10%

-20%

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

1Q17

3Q17

1Q18

3Q18

San Francisco Austin New York City Nashville

As of December 31, 2018. Source: Axiometrics, a RealPage Company.

19Key Takeaways

Demographics drive demand for real estate

Demographic demand for Sunbelt cities is significantly

better

Strong case for both employees and employers to

migrate

We continue to watch supply closely, but not an issue

currently

Several attractively priced REITs with exposure to

Southern office and residential markets in the portfolio

As of June 30, 2018. Past performance is not indicative of future results.

20What We See As Benefits of REIT Investing

Exposure to

Real Estate

REIT Income

Equity

Investing Investing

Investing

Potential

Diversification

Diversification does not guarantee a profit nor protect from loss in a declining market. 21REITs – Attractive Investment Potential

Simple business

model, transparent Ability to access

quarterly reporting public and

monitored by private debt and

regulatory equity markets

agencies

Why

Invest in

REITs?

Professional Low

Management Leverage

Team

Daily

Liquidity

22REIT Company Examples

Major Cities - Office

Boston Properties SL Green

• Owns or holds interests in 197 commercial properties • New York City's largest owner of Office real estate

• Properties: Boston, Los Angeles, New York, San • Owns or holds interests in 30 Manhattan office buildings

Francisco and Washington, DC

Salesforce Tower (Rendering) San Francisco, CA, U.S. 420 Lexington Avenue New York, The Graybar Building.

Derwent London PLC Japan Real Estate Investment Corporation

• Derwent London owns predominantly an office portfolio in • The company owns a portfolio of 73 office properties

13 ‘villages’ in London’s West End and Tech Belt focused on the Tokyo market

The White Chapel Building London. Otemachi Financial City North Tower.

For illustrative purposes only. Information is as of March 31, 2019 and subject to change without notice. The mention of a specific security is not a recommendation to buy or sell.

Past performance is not indicative of future results.

23REIT Company Examples

Major Cities - Retail

Simon Property Group Inc Unibail-Rodamco-Westfield

• S&P 100 company with total market capitalization of $56 • One of Europe’s largest listed commercial property

billion companies, with a portfolio of over 150 retail assets

• Owns or has an interest in 200+ retail real estate properties throughout the EU, UK and US

Walt Witman Shops Huntington Station New York. Les Quatre Temps, Paris

Hammerson PLC Scentre Group

• Portfolio includes investments in 21 prime shopping • Scentre Group owns and operates 41 shopping centers in

centers in the U.K., Ireland and France Australia and New Zealand

Union Square Aberdeen, U.K. Westfield Bondi Junction, Sydney, Australia

For illustrative purposes only. Information is as of March 31, 2019 and subject to change without notice. The mention of a specific security is not a recommendation to buy or sell.

Past performance is not indicative of future results. 24Income and Capital Appreciation

Combination of Capital Appreciation and Income Return

(12/31/1996 – 3/31/2019)

Capital Appreciation

10%

8.90% Income

9%

8% Total Return

7% 3.65% 6.21%

6% 5.19%

5% 0.15%

4% 4.33%

3%

5.25% 5.04%

2%

1% 1.88%

0%

Global REITs Global Equities Global Bonds

Yield

(3/31/2019) 3.90% 2.65% 1.77%

Correlation with

Global REITs

(12/31/1996 – 1.00 0.77 0.57

3/31/2019)

As of March 31, 2019. Source: Bloomberg; Brookfield Public Securities Group LLC Reflects longest common available time period for all indexes shown. The index data presented above

includes is shown for illustrative purposes only. Global REITs represented by the S&P Developed REIT Index for the period 12/31/1996 through 1/31/2005 and the FTSE EPRA Nareit

Developed Index for the period 2/1/2005 to the latest date. Global Equities represented by the MSCI World Index; Global Bonds by the ICE BofAML Global Corporate Bond Index. See

end of this presentation for additional disclosures and definitions.

25Historical Hedge Against Inflation

• The growth in REIT distributions has historically outpaced the rate of inflation

• Property values have tended to rise during inflationary periods

REIT Dividend Growth vs. Inflation

12%

10.2%

9.6%

10%

8.6% 8.4%

8% 7.3%

6.5% 6.3%

6% 4.8%

4.1%

4% 3.0% 3.3% 4.4% Avg.

2.5% 2.7%

1.7% 2.1% 2.1% 1.9%

2% 1.5% 1.5%

0.5% 0.1%

0.8% 0.7% 1.9% Avg.

0%

-0.4% -0.4%

-2%

-4%

-6%

-8%

-7.5%

-10%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Global REITs Annual Growth in Dividends per Share

U.S. Consumer Price Index

Sources: Bloomberg and Morningstar. Global REITs reflects factors relevant to any such comparison such as differences differ given different tax treatment of income versus capital

the FTSE EPRA Nareit Developed Index. The above in the volatility, and regulatory and legal restrictions between gain and other factors, such as the capital structure of the

indexes do not reflect deductions for fees, expenses or the indexes shown and an actively managed investment investment. Past performance does not guarantee results.

taxes. Indexes are not managed, and investors cannot strategy. See index definitions at the end of this The Consumer Price Index is a measure of the average

invest directly in an index. Performance is shown for presentation. Investing in real estate securities involves change over time in the prices paid by urban consumers for

illustrative purposes only and does not predict or depict the different risks, including the loss of principal. The tax a market basket of consumer goods and services.

performance of any investment. There may be material treatment of returns of the asset classes listed above may

26REIT Dividend Growth Has Historically Outpaced Inflation

Annual Growth In Dividends and Major Expenses (2006-2018)

College

5.0%

Tuition

REIT

4.5% Costs

Dividends

4.0%

Healthcare

3.5% Costs

3.0%

2.5% 75% 72%

Total Total

Core

2.0% Increase Increase 53% Inflation

Total

Increase

1.5% 28%

Total

1.0% Increase

0.5%

0.0%

REIT Dividend growth has outpaced core inflation as well as Healthcare Costs while also

keeping pace with the rapid rise in College Tuition Costs

Sources: Bloomberg and Bureau of Labor Statistics. Global REITs reflects the FTSE EPRA Nareit Developed Index. Core CPI represents U.S. CPI Urban Consumers; Healthcare Costs

represented by US CPI Urban Consumers Medical Care Services; College Tuition Costs represented by U.S. CPI College Tuition & Fees

27Real Estate Has Low Correlation With Equities

The correlation with broader equities has been below 0.5 during most periods

Trailing 5 year correlation between

U.S. REITs and U.S. Equities

0.9

0.8

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

Sources: Bloomberg U.S. REITs reflects the MSCI US REIT Total Return Gross Index. U.S. Equities represents the S&P 500 Total Return Index.

28Global Real Estate vs. Global Equities

Global Real Estate has underperformed Global Equities since the Fed began

raising rates, providing an attractive opportunity to add exposure

135

Global Equities

returned ~33% Global Equities

130 through 9/30/2018+30% During the period

125

120

Global

Global Equities Real Estate

fell

115 +15% During the period

13.3% in Q4

110 Global Real Estate

Global

returned ~6% Real Estate

105 was down only

through 9/30/2018

5.5% in Q4

100

95

90

Global Real Estate Securities Global Equities

As of March 31, 2019. Sources: Bloomberg, MSCI, FTSE EPRA Nareit. Global Real Estate represented by FTSE EPRA Nareit Developed Total Return Index USD; Global Equities

represented by MSCI World Gross Total Return USD Index.

29REIT Fund Flows

U.S. Mutual Fund and ETF Flows and AUM Japan Mutual Fund AUM

Source: Citi Research and Lipper as of 3/28/2019 Source: Citi Research and Bloomberg as of 3/28/19

30Balance Sheets Over The Past Decade

We believe significantly improved balance sheets decrease the risk associated with

rising rates

Debt to Total Assets: All listed U.S. equity REITs

70

65

FOMC Tightening Cycle

60

Debt/Market Assets

Debt to Total Assets (%)

55

50

45

40

35

30

25

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

As of September 30, 2018. Source: Nareit. FOMC: Federal Open Market Committee

31Average Global Valuations

Global Historical Premium (Discount) to NAV

30%

20%

10%

0%

-10%

Historical Average: -7.4% Current:

-5.9%

-20%

-30%

-40%

-50%

Global Premium (Discount) to NAV

Historical Average

As of March 31, 2019. Represents data beginning January 1995. Represents estimated average public market valuations relative to estimated average private market valuations for

global real estate. NAV or Net Asset Value is the "market value" of all a company's assets, including but not limited to its properties, after subtracting the “market value” of all its

liabilities and obligations. Source: UBS Global Real Estate Research; Brookfield Public Securities Group LLC research and estimates.

32Global Real Estate – Valuation Dispersions Across Geographies

Although global real estate in aggregate trades near its historical average, many

regions trade at meaningful discounts to their long-term averages

Premium (Discount) to NAV by Geography

80%

180%

60%

160%

40%

140%

20%

120%

0%

100%

-20%

80%

-40%

60%

-60%

40%

-80%

20%

Current

Historical 10th to 90th Percentile

Historical Maximum/Minimum

As of March 31, 2019. Represents data beginning January 1995. Valuation dataset duration varies by geography and is dependent on data availability for each individual market.

Represents estimated average public market valuations relative to estimated average private market valuations for each real estate market. NAV or Net Asset Value is the "market value"

of all a company's assets, including but not limited to its properties, after subtracting the “market value” of all its liabilities and obligations. The geographies and sectors are defined by

UBS Global Research and BMO Capital Markets and do not necessarily reflect any widely followed indexes. Source: UBS Global Real Estate Research; Brookfield Public Securities

Group research and estimates. Canada data sourced from BMO Capital Markets.

33U.S. Real Estate – Wide Valuation Spreads in Select Sectors

Intra-sector valuations remain wide in most U.S. sectors

Premium (Discount) to NAV by Sector

70%

60%

50%

40%

30%

20%

10%

0%

-10%

-20%

-30%

-40%

-50%

-60%

-70%

-80%

Office Industrial Diversified Apartment Healthcare Regional Mall Strip Center Net Lease Hotels Self-Storage

Current Sector Average

Current Range from Sector Minimum to Sector Maximum

As of March 31, 2019. Represents estimated average public market valuations relative to estimated average private market valuations for each real estate sector. NAV or Net Asset

Value is the "market value" of all a company's assets, including but not limited to its properties, after subtracting the “market value” of all its liabilities and obligations. Sectors are defined

by Brookfield Public Securities Group LLC research and estimates and do not necessarily reflect any widely followed indexes. Source: Brookfield Public Securities Group LLC research.

Information referenced herein represents U.S. Real Estate Securities and not specific Fund or Strategy information.

34The Real Estate Securities Team

Seasoned leadership team supported by a deep roster of analysts

Investment Jason Baine Bernhard Krieg, CFA

Leadership Portfolio Manager Portfolio Manager

23 Years of Investing Experience 21 Years of Investing Experience

18 Years with Brookfield 13 Years with Brookfield

Launched Brookfield’s real estate Extensive long/short and real estate

securities platform in 2001 securities experience

Analysts James Allison Jamieson Duff, CFA Anar Isman, CFA

Continental, Central and Eastern U.S. Industrial; U.S. Residential and Timber;

Europe; Nordic Countries Japanese REITS Japanese Developers; Canada

16 Years of Experience 8 Years of Experience 15 Years of Experience

7 Years with Brookfield 8 Years with Brookfield 7 Years with Brookfield

Kevin Mueller Julian Perlmutter, CFA Michael Shoemacher

Generalist U.S. Student Housing; Storage; Data U.S. Healthcare; United Kingdom;

2 Years of Experience Centers and Towers; Hong Kong; China Australia

1 Year with Brookfield 16 Years of Experience 15 Years of Experience

7 Years with Brookfield 7 Years with Brookfield

Richard Sweigard John Wallace, CFA Matt Wenman, CFA

U.S. Office, Diversified and U.S. Strip Center Retail; Product Specialist;

Regional Malls; Singapore Triple Net Lease; Global Hotels Portfolio and Market Analytics

18 Years of Experience 18 Years of Experience 13 Years of Experience

14 Years with Brookfield 3 Years with Brookfield 13 Years with Brookfield

Trader Rob Kosar

23 Years of Experience

14 Years with Brookfield

35Brookfield Global Listed Real Estate Fund Portfolio Characteristics

March 2019

Asset Allocation Allocation Changes

N. America -2.7% N. America +0.9%

U.S. Sectors

U.S. Portfolio U.S.

U.S. Sectors Current

Healthcare 10.0% Healthcare 10.0%

6.9% 6.2%

Residential 9.1% Residential 9.1%

8.7% 10.5%

Office 8.7% Office 8.7%

7.3% 5.6%

Net Lease 5.3% Net Lease 5.3%

5.9% 2.5%

Retail 4.9% Retail 4.9%

7.7% 11.1%

Self Storage 4.0% Self Storage 4.0%

3.6% Benchmark 2.3% One Year Ago

Hotel 3.6% Hotel 3.6%

3.3% 5.2%

Industrial 3.5% Industrial 3.5%

4.9% 3.0%

Data Centers 1.5% Data Centers 1.5%

2.1% 3.2%

Specialty 0.0% Specialty 0.0%

1.3% 2.7%

0.0% Diversified 0.0%

Diversified 1.4% 0.0%

Canada 2.5% Canada

Canada 2.5%

Canada 2.7% 0.0%

Asia Pacific +0.8% Asia Pacific +3.1%

12.2% Japan 12.2%

Japan 11.1% 12.3%

8.5% Hong Kong/China 8.5%

Hong Kong/China 8.5% 5.2%

3.8% Australia/N.Z. 3.8%

Australia/N.Z. 4.8% 3.7%

3.3% Singapore/Other 3.3%

Singapore/Other 2.7% 3.6%

Europe +1.0% Europe -2.2%

10.9% Continental Europe 10.9%

Continental Europe 12.4% 10.0%

7.2% U.K. 7.2%

U.K. 4.8% 10.4%

Active Weight

One Year Change

Portfolio

Current Portfolio

Benchmark

Portfolio One Year Ago

As of March 31, 2019 and includes Cash. Benchmark refers to the FTSE EPRA Nareit Developed Index. Weights and portfolio holdings are subject to change. Due to rounding,

amounts presented herein may not add up precisely to the total. See end of this presentation for additional disclosures and definitions. 36Southeastern & Midwest Multifamily REIT

o Established owner and operator of

multifamily apartment communities in

the Southeast and Midwest United Market Exposure

(% of Net Operating Income)

States

o Portfolio of over 100,000 units in 17

states

o $11.5B market capitalization 13%

o $126 million development pipeline

32%

9%

7%

4% 6%

5% 4%

6% 7%

7%

Acklen Apartments - Nashville

Atlanta, GA Dallas, TX

Charlotte, NC Austin, TX

Nashville, TN Washington, DC

Tampa, FL Orlando, FL

Canyon Point Apartments - Austin Raleigh/Durham, NC Fort Worth, TX

Other

As of June 30, 2018. Source: Company filings. Properties identified in the image are held indirectly by the Fund as of March 31, 2019. .

37Hong Kong – Office Landlord

Central portfolio creates a network effect of international commerce

Source: Company filings. Properties identified in the image are held indirectly by the Fund as of March 31, 2019. .

38Hong Kong – Office Landlord

Gross Assets as of June 30, 20181

90% Investment Properties

77% Hong Kong

Central office portfolio average rent

Central office market

continues to have

stable rent growth

As of June 30, 2018. Source: Company filings. Shown for illustrative purposes only

39Hong Kong – Office Landlord

Worries of a U.S./China trade war have caused a Portfolio trades well below replacement cost at

selloff for Hong Kong landlords, we believe this is US$1,800/SF

overdone • Henderson Land purchased an adjacent land site for

US$6,400/sf ($3bn) and are under-writing US$8,000/sf

Attractive Current Valuation total construction costs.

• 7.5% implied cap rate • Cheung Kong Assets Sold its “The Center” which is on

• Implied US$1,800/SF the border of Central for US$5bn or US$4,300/sf

• 13x Price/FFO • Private transactions have had cap rates of 2-3%

• 3.1% dividend yield

• 0.43x Price/Book, near a 10 year low (57% Discount) High barriers to entry

• Hong Kong Island will see virtually no new supply in

Price to Book Ratio coming years

1.2x

• Landlord’s high-quality Central portfolio has only 1%

1.1x

vacancy

1.0x

0.9x Management proactively addressing valuation

0.8x • Enacted first share buyback since 2008, repurchased

Average = 0.66x

0.7x $130m of securities year to date

0.6x • We expect share buybacks to continue if pricing

0.5x dislocation persists

0.4x

Current = 0.43x

0.3x

As of March 31, 2019. Source: Brookfield Public Securities Group LLC and company filings. 1) Valuation example provided for illustrative purposes only . SF: Square feet. FFO: Funds from operations

40Real Estate Universe

Historical Investment Characteristics

• Many lease agreements have contractual increases $1.5 trillion

tied to inflation, leading to generally attractive Total market capitalization

revenues and cash flows

(>400 companies)

• Assets with a history of pricing power—the ability to

pass along rising costs to customers—which has

been beneficial in periods of elevated inflation

• Companies, which are bound by the REIT structure,

are generally required to distribute 90% of income

Healthcare Shopping Centers Industrial Single Family Rental Self Storage

Longer Lease Term Shorter Lease Term

Triple Net Lease Regional Malls Office Multifamily Hotels

As of December 31, 2018. Source: Brookfield Public Securities Group LLC research and estimates

41Is the correlation between REITs and rates a myth?

100%

80%

60%

40%

R2 = 0.10

20%

Global REITs

One Year 0%

Total Return

-20%

-40%

-60%

Positive GDP Growth

-80%

-2.5% -2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Negative GDP Growth

10-Year U.S. Treasury Yield

Year-Over-Year Change

The correlation is very weak; we believe GDP growth is likely a better indicator

As of September 30, 2018. Source: Bloomberg; Brookfield Public Securities Group LLC Reflects trailing 12-month returns and GDP growth for each quarterly observation for the period

12/31/1992- latest. Reflects longest available time period. Global REITs represented by the S&P Developed REIT Index for the period 12/31/1992 through 1/31/2005 and the FTSE

EPRA Nareit Developed Index for the period 2/1/2005 to the latest date.

42Brookfield Global Listed Real Estate Fund Key Holdings

Top Ten

Market Cap Active

Ticker Company Region Sector Weight

(billions) Weight1

VNA.GY Vonovia SE Continental Europe Residential $26.9 4.5% 2.7%

AVB AvalonBay Communities Inc U.S. Residential $27.8 3.8% 2.0%

KRC Kilroy Realty Corp U.S. Office $7.7 3.4% 2.9%

MAA Mid-America Apartment Communities Inc U.S. Residential $12.5 3.3% 2.5%

VTR Ventas Inc U.S. Healthcare $22.8 3.2% 1.8%

PSA Public Storage U.S. Self Storage $38.0 3.0% 0.9%

8802.JP Mitsubishi Estate Co Ltd Japan Office $25.2 2.9% 1.6%

8801.JP Mitsui Fudosan Co Ltd Japan Office $24.9 2.9% 1.4%

MGP MGM Growth Properties LLC U.S. Net Lease $2.9 2.7% 2.7%

SGP Simon Property Group Inc U.S. Retail $56.3 2.6% -1.0%

Total 32.3%

Top Overweight Positions

Market Cap Active

Ticker Company Region Sector Weight

(billions) Weight1

KRC Kilroy Realty Corp U.S. Office $7.7 3.4% 2.9%

VNA.GY Vonovia SE Continental Europe Residential $26.9 4.5% 2.7%

MGP MGM Growth Properties LLC U.S. Net Lease $2.9 2.7% 2.7%

MAA Mid-America Apartment Communities Inc U.S. Residential $12.5 3.3% 2.5%

DOC Physicians Realty Trust U.S. Healthcare $3.4 2.3% 2.1%

As of March 31, 2019. 1. Relative to the FTSE EPRA Nareit securities identified and described do not represent all of the precisely to the total. Performance data quoted represents

Developed Index (Net of WHT). Weights and portfolio securities purchased, sold or recommended for the Fund. past performance, which does not guarantee future

holdings are subject to change. The mention of specific The reader should not assume that an investment in the results. No guarantee that the Fund currently holds any of

securities is not a recommendation or solicitation for any securities identified was or will be profitable. Due to the names referenced herein. See end of this presentation

person to buy, sell or hold any particular security. The rounding, amounts presented herein may not add up for additional disclosures and definitions.

43Brookfield Global Listed Real Estate Fund Performance Summary

(BLRAX, BLRCX, BLRYX)

Performance Summary as of 3/31/19

Inception One Three Five Since

(Net of Fees) Date QTD YTD Year Years

1

Years

1

Inception

1

Brookfield Global Listed Real Estate Fund (Class A – excluding sales charge) 4/30/12 15.16% 15.16% 10.39% 5.79% 6.51% 8.36%

Brookfield Global Listed Real Estate Fund (Class A – including sales charge) 4/30/12 9.67% 9.67% 5.15% 4.08% 5.48% 7.60%

Brookfield Global Listed Real Estate Fund (Class C – excluding sales charge) 4/30/12 14.97% 14.97% 9.52% 5.01% 5.71% 7.55%

Brookfield Global Listed Real Estate Fund (Class C – including sales charge) 4/30/12 13.97% 13.97% 8.52% 5.01% 5.71% 7.55%

Brookfield Global Listed Real Estate Fund (Class Y) 11/30/11 15.29% 15.29% 10.66% 6.06% 6.75% 10.34%

FTSE EPRA Nareit Developed Index (Net of WHT) 14.59% 14.59% 13.27% 5.68% 6.41% 7.30%2

FTSE EPRA Nareit Developed Index (Gross of WHT) 14.86% 14.86% 14.33% 6.67% 7.36% 8.20%2

Performance

Growth of $10,0002 $16,594

$17,000

$16,000

$15,000 $16,277

$14,000

$13,000

$12,000

$11,000

$10,000

$9,000

$8,000

Apr-12 Jan-13 Oct-13 Jul-14 May-15 Feb-16 Nov-16 Sep-17 Jun-18 Mar-19

Brookfield Global Listed Real Estate Fund (Class A – including sales charge) (Net of Fees)

FTSE EPRA Nareit Developed Total Return Index (Net of WHT)

1) Annualized. As of March 31, 2019. or CDSC and if reflected, the sales charge or fee would of the Fund.

2) References Class A’s inception date. reduce the performance quoted. Investment performance The chart illustrates the performance of a hypothetical

3) Relative to Class A – including sales charge against the reflects fee waivers, expenses and reimbursements in $10,000 investment made in the Fund since inception. Results

FTSE EPRA Nareit Developed Index (Net of WHT). effect. In the absence of such waivers, total return and for the Fund are net of management and performance fees.

Performance data quoted represents past performance; NAV would be reduced. Investment performance reflects Represents performance since inception of the Fund:

past performance does not guarantee future results. The fee waivers, expenses and reimbursements in effect. In November 30, 2011 through March 31, 2019. The quoted

investment return and principal value of an investment the absence of such waivers, total return and NAV would benchmarks do not reflect deductions for fees, expenses or

will fluctuate so that an investor’s shares, when be reduced. The gross operating expense ratio for the taxes. Benchmark performance is shown for illustrative

redeemed, may be worth more or less than their original Class A, C, and Y Shares are 1.22%, 1.97%, 0.97%, purposes only and does not predict or depict the performance

cost. Current performance of the Fund may be lower or respectively. The FTSE EPRA Nareit Developed Index is an of any investment. There may be material factors relevant to

higher than the performance quoted. Performance data unmanaged market-capitalization-weighted total-return index, any such comparison such as differences in the volatility, and

current to the most recent month end may be obtained by which consists of publicly traded equity REITs and listed regulatory and legal restrictions between the indices shown

calling 855.244.4859. Performance shown including sales property companies from developed markets. The Index is and the Fund. See end of this presentation for additional

charge reflects the Class A maximum sales charge of unmanaged and, unlike the Fund, is not affected by cash disclosures and definitions.

4.75% and the Class C Contingent Deferred Sales Charge flows, trading and expenses. It is not possible to invest directly

(CDSC) of 1.00%. Performance data excluding sales in an index. Index performance is shown for illustrative 44

charge does not reflect the deduction of the sales charge purposes only and does not predict or depict the performanceBrookfield Global Listed Real Estate Fund

Fund Characteristics

Fund AUM Fund Inception

BLRAX BLRCX BLRYX Benchmark

$1.9 billion Nov-11

Distribution Rate1 3.78% 3.13% 3.99% 4.04%

Concentration in names and themes

30 Day SEC Yield

• Best ideas globally: generally 40 to 70 securities

(subsidized)2 2.36% 1.74% 2.73% --

• Top 10 holdings represent approximately 30% to 40% of

total portfolio 30 Day SEC Yield

(unsubsidized)2 2.35% 1.72% 2.71% --

Individual holdings Weighted Average

• High conviction/large cap 3% to 10% Market Cap $15.8B $15.8B $15.8B $15.6B

• Other 1% to 3%

Number of

Holdings 58 58 58 333

Active weights

Top 10

• Limited underweight positions

Concentration 32.3% 32.3% 32.3% 20.2%

• Typical overweight per position 0.5% or 2.0%

• Target portfolio active share generally ~65% Non-Benchmark

• Benchmarked to the FTSE EPRA Nareit Developed Index Exposure 4.2% 4.2% 4.2% --

(Net of WHT3)

As of March 31, 2019. As of December 31, 2018 the Fund estimates approximately 33.87% of its distributions is a return of capital. Targets are subject to change without notice.

The manager makes no warranty that the targets will be achieved. 1) The distribution rate is calculated as the annualized amount of the most recent quarterly distribution declared

divided by March 31, 2019 Net Asset Value per share. This calculation does not include any non-income items such as loan proceeds or borrowings. The Fund estimates that it

has distributed more than its net investment income and net realized capital gains; therefore, a portion of your distribution may be a return of capital. 2) Class A. As of March 31,

2019, 30 Day SEC Yield does not include income that is determined to be from return of capital. Assets are preliminary and subject to change. 3) Withholding Tax (WHT). Assets

reflect the Brookfield Global Listed Real Estate Fund. Benchmark performance is shown for illustrative purposes only and does not predict or depict the performance of any

investment. There may be material factors relevant to any such comparison such as differences in the volatility, and regulatory and legal restrictions between the indices shown

and the Fund. Past performance is not indicative of future results.

45Disclosures

Must be preceded or accompanied by a current prospectus. by a fund in lower-rated and non-rated securities presents a

greater risk of loss to principal and interest than higher-rated

Mutual fund investing involves risk. Principal loss is possible.

securities. Some securities held may be difficult to sell,

Investing in real estate securities involves different risks,

particularly during times of market turmoil. If a fund is forced

including the loss of principal. The tax treatment of returns of

to sell an illiquid asset to meet redemption, the fund may be

the asset classes listed above may differ given different tax

forced to sell at a loss. Using derivatives exposes a fund to

treatment of income versus capital gain and other factors such

additional risks, may increase the volatility of a fund’s net

as the capital structure of the investment. Unlike bonds, REIT

asset value and may not provide the result intended. Since a

distributions are not fixed and may fluctuate (positively or

fund will invest more than 25% of its total assets in securities

negatively) over time based on market conditions. Moreover,

in the real estate industry, a fund may be subject to greater

the underlying property values of a REIT may increase or

volatility than a fund that is more broadly diversified. Past

decline over time causing the value of the REIT to increase or

performance is no guarantee of future results. Opinions

decline accordingly. Investors in bonds receive a principal

expressed are subject to change at any time, are not guaranteed

payment are par value upon maturity, unless the bond defaults

and should not be considered investment advice.

or is called. Below are real estate related risk disclosures that

apply to Brookfield real estate mutual funds. Property values Diversification does not guarantee a profit or protect from loss in a

may fall due to increasing vacancies or declining rents declining market.

resulting from unanticipated economic, legal, cultural or

Fund holdings and sector allocations are subject to change and are

technological developments. REITs are dependent upon

not recommendations to buy or sell any security. Current and future

management skills and generally may not be diversified. REITs

portfolio holdings are subject to risk.

are subject to heavy cash flow dependency, defaults by

borrowers and self-liquidation . Of course, along with any INDEX PROVIDER DISCLAIMER

benefits realized through the effects of rising inflation, Brookfield Public Securities Group LLC does not own or participate

companies that own and operate real assets will likely in the construction, or day-to-day management of the indices

experience rising operating costs associated with the goods referenced in this document. The index information provided is for

and services they provide. As inflation rises, there is no your information only and does not imply or predict that a Brookfield

assurance that they will have the pricing power to pass along Public Securities Group LLC product will achieve similar results.

such costs to customers. There are also independent factors This information is subject to change without notice.

that could hinder their ability to perform in periods of rising

inflation. For example, unfavorable changes in the regulatory The Indices referenced in this document do not reflect any fees,

environment, rapidly rising interest rates or unforeseen expenses, sales charges, or taxes. It is not possible to invest

imbalances in supply and demand could make it difficult for directly in an index. The index sponsors permit use of their indices

real estate, infrastructure, natural resource, and commodity and related data on an "As Is" basis, makes no warranties regarding

securities to keep pace with inflation. Please see important same, does not guarantee the suitability, quality, accuracy,

disclosures at the end for additional risk considerations.A fund timeliness, and/ or completeness of their index or any data included

may invest in small and mid-cap companies, which involve in, related to, or derived therefrom, assumes no liability in

additional risks such as limited liquidity and greater volatility. connection with the use of the foregoing. The index sponsors have

A fund may invest in foreign securities which involve greater no liability for any direct, indirect, special, incidental, punitive,

volatility and political, economic and currency risks and consequential, or other damages (including loss profits). The index

differences in accounting methods. Investing in emerging sponsors do not sponsor, endorse, or recommend Brookfield Public

markets may entail special risks relating to potential Securities Group LLC or any of its products or services.

economic, political or social instability and the risks of There may be material factors relevant to any such comparison

nationalization, confiscation or the imposition of restrictions such as differences in the volatility, and regulatory and legal

on foreign investment. Debt securities rated below investment restrictions between the indices shown and the strategy.

grade are commonly referred to as “junk bonds” and are

considered speculative. Increases in interest rates can cause

the prices of fixed income securities to decline, and the level

of current income from a portfolio of fixed income securities

may decline in certain interest rate environments. Investment

46Disclosures

INDEX DEFINITIONS DEFINITIONS

The FTSE EPRA Nareit Developed Total Return Index is an FOMC is the Federal Open Market Committee; the monetary

unmanaged market-capitalization-weighted total-return index, which policymaking body of the Federal Reserve System.

consists of publicly traded equity REITs and listed property

Active Share is a measure of the percentage of stock holdings in a

companies from developed markets.

manager's portfolio that differs from the benchmark index.

The FTSE EPRA Nareit Developed Index is calculated by the FTSE

Alpha is a measure of the difference between a fund's actual

Group. Performance is calculated by price, total return and net total

returns and its expected performance, given its level of risk as

return and the Index is calculated daily. Constituents must meet

measured by beta.

minimum market capitalization, liquidity requirements, and real

estate activity requirements in order to be included within the Index. Annualized Return is periodic returns rescaled to a period of one

North American and Asian companies must be of a minimum of year.

US$200 million in market capitalization with liquidity of US$100 Bps = basis points.

million. European companies are bound by €50 million market cap

minimum and liquidity of €25 million. The Net version of the index is Cash flows refer to the amount of cash generated and used by a

calculated net of applicable withholding tax, however does not company over a given period.

reflect deductions for fees, expenses, or other taxes. Consumer Price Index (CPI) is a measure that examines the

The S&P Developed REIT Index serves as a benchmark of publicly weighted average of prices of a basket of consumer goods and

traded equity REITs domiciled in developed markets. services, such as transportation, food and medical care. It is

calculated by taking price changes for each item in the

The NCREIF Fund Index – Open End Diversified Core Equity (NFI- predetermined basket of goods and averaging them.

ODCE) is a capitalization-weighted, gross of fee, time-weighted

return index with an inception date of December 31, 1977. Open- Correlation, in the finance and investment industries, is a statistic

end funds are generally defined as infinite-life vehicles consisting of that measures the degree to which two securities move in relation

multiple investors who have the ability to enter or exit the fund on a to each other. Correlations are used in advanced portfolio

periodic basis, subject to contribution and/or redemption requests, management, computed as the correlation coefficient, which has a

thereby providing a degree of potential value that must fall between -1.0 and +1.0.

The MSCI World Gross Total Return Index is a free float-adjusted Pice-to-book ratio, or P/B ratio, is a financial ratio used to

market-capitalization-weighted index that is designed to measure compare a company's current market price to its book

the equity market performance of developed markets. investment value.

liquidity

R2 is a percentage measure of how often one variable changes

The ICE BofA Merrill Lynch Global Corporate Index is an when another variable changes. In statistical terms, it is a measure

unmanaged, commonly accepted measure of the performance of of how correlated a group of actual observations are to a model’s

global investment grade corporate securities. predictions.

The above-mentioned indexes do not reflect deductions for fees, Standard Deviation measures the degree to which an investment’s

expenses or taxes. The indexes are unmanaged and cannot be return varies from its mean return.

purchased directly by investors. Index performance is shown for

The SEC yield is based on a 30-day period ending on the last day

illustrative purposes only and does not predict or depict the

of the previous month. It is computed by dividing the net investment

performance of any investment.

income per share earned during the period by the maximum

The MSCI US REIT Index is a free float-adjusted market offering price per share on the last day of the period.

capitalization weighted index that is comprised of equity Real Estate

Yield refers to the earnings generated and realized on an

Investment Trusts (REITs).

investment over a particular period of time, and is expressed in

The S&P 500® Index is an unmanaged weighted index of 500 large terms of percentage based on the invested amount or on the

company stocks that is widely-recognized as representative of the current market value or on the face value of the security.

performance of the U.S. stock market. Indexes are not managed

Quasar Distributors, LLC is the distributor of Brookfield Investment

and an investor cannot invest directly in an index.

Funds and Brookfield Public Securities Group LLC is the Investment

Advisor. 47You can also read