5 FY 2019 - 2020 UES APPLICATION (JULY 1, 2019 TO JUNE 30, 2020) NORTHERN EUROPE (EUN) - Alaska Seafood Marketing Institute (ASMI) Denmark ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

5

Alaska Seafood Marketing Institute (ASMI)

FY 2019 – 2020 UES APPLICATION

(JULY 1, 2019 TO JUNE 30, 2020)

NORTHERN EUROPE

(EUN)

Denmark, Finland, Ireland,

Sweden, the Netherlands, United Kingdom

1

FY 2018-2019 UNIFIED EXPORT STRATEGY

Market Assessment Worksheet

Market: (EUN) EUROPEAN UNION, NORTHERN

Commodity Aggregate: SEAFD – Fish & Seafood

1. Market Assessment Update

A. Executive Summary

Following an unsettled 2016, 2017 saw much of the political attention in Europe turn to ‘Brexit’

negotiations between the UK and the EU. This complex process proved as challenging as

expected with much pressure on the negotiations over the ‘divorce’ payment before talks finally

moved onto trade negotiations. This caused political instability in the UK with a snap election

taking place in June. The Conservative party lost their majority and were forced to form a

Government with the support of a minority party.

The final ‘removal’ date for the UK remains March 2019, with a transition period of up to two

years. In the Netherlands election in March 2017, the far-right party was unsuccessful in

securing an anticipated majority and the resulting economy grew strongly.

The economic uncertainty witnessed throughout 2016 progressed through 2017 but forecasts

are for 2018 to be less volatile.

The current position is that the UK will leave the EU in March 2019 and will not be in a position

to enter trade talks with other nations until withdrawn. Further complexity is brought to the

table by the UK’s desire for a two year transition period which has still to be agreed. The full

process for Brexit is shown below.

2

3

Key Economic and Political:

Political stability has returned to large parts of Europe with the Right Wing factions in France

and the Netherlands being defeated in 2017 elections. In Germany however, Mrs. Merkel has

so far failed to establish a coalition and there are many commentators who believe she will not

survive this latest crisis. As the largest economy in Europe and the EU, instability in Germany

clearly has implications for the smaller nations and many Europeans are nervous that a further

election will be required.

Within Scandinavia, the next elections will take place in Sweden in 2018 with Denmark and

Finland following in 2019. Modest economic growth seems to be returning across the region

although unemployment remains higher than the European average.

Elections took place in The Netherlands in March 2017, with the liberalist government being

returned and the expected swing to the right, strong anti-Islamic views, and increasing

Euroscepticism not materializing due to an exceptionally high voter turnout. The UK elections

are set for 2020.

Economic Outlook No

102 November 2017

Variable GDP growth

Frequency Annual

Time 2013 2014 2015 2016 2017 2018 2019

Country Unit

Denmark % 0.935 1.616 1.606 1.967 2.180 1.991 2.026

Ireland % 25.50

1.628 8.305 1 5.136 3.643 2.717 2.201

Netherlands % -0.121 1.419 2.260 2.145 3.251 3.097 2.368

Sweden % 1.222 2.709 4.276 3.071 3.052 2.813 2.338

United Kingdom % 2.052 3.054 2.346 1.794 1.522 1.237 1.063

United States % 1.677 2.569 2.862 1.485 2.246 2.544 2.147

Data extracted on 1 February 2018 from

OECD.Stat

4OECD forecasts for the European area are that GDP growth will remain relatively strong due

to the ongoing recovery of global trade. Growth will continue steadily with the labor market

continuing to improve and employment across the EU.

Revised forecasts for 2019 show the weakness in the UK market with resulting growth

prospects reflected by currency depreciation. Monetary policy continues to try to mitigate

shocks to the system by attempting to stabilize markets and increase interest rates for the first

time in more than 10 years. This projection assumes the United Kingdom will operate with a

most favored nation status after Brexit in 2019, but this remains uncertain. Higher inflation

with increased food prices due to the price of imports is projected to hit households’ purchasing

power. As growth slows, the unemployment rate is projected to rise.

Confidence among British consumers fell to -13 in December 2017 from -5 at the start of the

year. Brexit uncertainties together with an awareness of price increases and likely job

instability reduced willingness to make major purchases.

British consumer prices including housing, believed to be the most accurate measure of

inflation (CPIH) rose +2.7% in the year to December 2017, up from +1.8 in the year to

December 2016. The primary drivers of price increases in 2017 came from food, housing and

5related services and transport all of which are impacted by higher import prices due to

currency weakness.

Showing lows of 1.21 in spring 2017, the £:$ exchange rate rebounded in 2017 showing more stability

in the final quarter and reaching 1.40 in early January 2018 with analysts expecting this rally could

continue throughout 2018.

The Dutch economy expanded more slowly than a year ago, posting growth of 0.4% percent

during the third quarter of 2017. At the end of the third quarter, the economy posted its

fourteenth straight quarter of growth. Private consumption remained solid, supported by

employment gains. It is expected that the full year data will show the fastest expansion in the

Netherlands for a decade. Dutch consumer confidence, which has been positive in the last three

years stood a 25 in December 2017, as consumers' opinion toward the economic climate was

6virtually unchanged. Domestic demand is expected to drive growth in 2018/19 with the fiscal

stimulus plan expected to boost household spending.

The Swedish economy continues to look strong with consumer prices increasing 0.4% in

December in line with market expectations. Industrial production figures were solid and

business sentiment showed broad-based optimism across sectors. This rosy outlook has

bolstered the labor market which has seen sustained job creation and the lowest unemployment

rate since 2008. This comes after GDP growth in the quarter to September 2017 of +0.8%,

matching market expectations. Growth was driven by capital investments with household

consumption softening slightly.

The Irish economy expanded 4.2% percent in the third quarter of 2017, following an upward

revised 2.7 percent growth in the previous period and well above market expectations of 1.4

percent. This was the strongest pace of expansion in almost a year, boosted by a rebound in

household consumption and a positive contribution from net exports. Unemployment has

continued to decline, and in January 2018, was at 6.1% compared with 7.2% the previous year.

Consumer confidence has decreased by 0.4 points to 103.2 in December 2017, retreating for

the third month following an 18-month high in September 2017.

Key Seafood Trends and Events:

Price inflation has been the key issue for the seafood sector in 2017, with prices continuing to

increase ahead of other proteins. Drivers for this include currency instability, increased fuel

costs and in some instances labor cost increases.

7Atlantic Salmon.

NEU countries rely heavily on imported seafood (EU 55%, UK 80%). Nielsen data at

December 2017 shows average price per unit increases of 7.3% compared to a food price

inflation of 3.9%. For many consumers, this underlines their established perception that

seafood is the most expensive protein. This increase in price is impacting unit (-3.4%) and

volume sales (-3.6%). These price increases are less acute in the frozen sector where price

increases are more in line with food inflation at +4.3%. This has had a marginally positive

increase in the frozen category where unit sales are flat.

The frozen category, a long-term destination for Alaska seafood, has shown a value sales

increase in 2017 although volume sales continue to fall. Consumers are purchasing less

frequently than previously, making frozen seafood purchases less than monthly. Pollock

volumes are showing a marginal uptick potentially as a consumers look for value-based

alternatives - pollock being 40% cheaper than cod, on average.

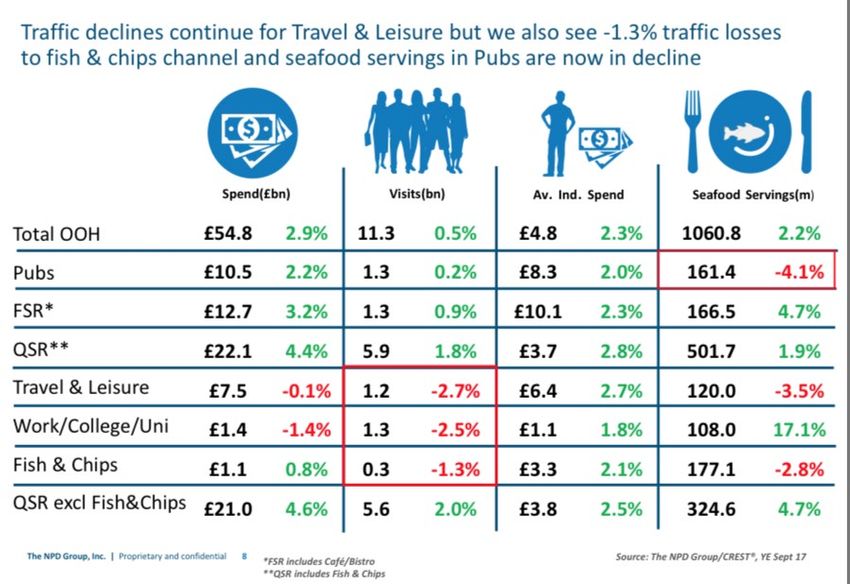

Within the eating out sector, spend and number of visits has increased driven by the quick

service sector. In areas where homemade alternatives can be consumed (e.g. work and

8education sectors) both visits and spend are declining. Overall seafood servings have increased

by 2.2% surprisingly given the reported foodservice inflation in seafood of +23%.

9B. General Assessment

Currency movements remain a key factor in trade flow changes between 2014 and 2017. The

following table compares the average exchange rate over a 12 month period:

USD / EUR USD / GBP USD / DKK

2014 0.754 0.607 5.618

2015 0.901 0.654 6.722

2016 0.940 0.810 7.010

2017 0.887 0.777 6.59

Value gain $ from 2014 vs 2016 24.6% 33.4% 24.8%

Value gain $ from 2014 vs 2017 17.6% 28.0% 17.3%

Recovery 2017 vs 2016 7% 5.4% 7.5%

Although having made a recovery since 2016, the currency impact in 2017 remained

significant, mostly in the UK market.

The shift towards discounted retails in the UK continues apace with Lidl and Aldi’s combined

share growing by 80% since 2013. Jointly they have permanently changed the dynamics of the

grocery market by forcing down margins and offering choice and value in easily accessible

stores. Meanwhile, Tesco and Sainsbury, and to a lesser extent Asda, are left with a portfolio

of stores which simply do not meet shoppers needs - shoppers are returning to smaller basket

sizes to manage budgets and out of town hypermarkets designed for monthly shops just do not

deliver. Lidl and Aldi have also continued to expand their range of chilled and luxury products,

delivering ranges which accommodate local needs where possible.

The retail sectors across the other NEU countries remain more stable with the small numbers

of retailers focused on value. Here, seafood ranges can extend over a broader range of species

but formats tend to be more limited and focused on natural products due to increased

acceptance and cooking skill.

Throughout the region, the communication and promotional activities of the larger retailers

continue to be disrupted by the discount retailers, causing reconsideration on store strategy,

product catalog, long-term pricing, and promotional practices. The larger retailers have been

10forced into rationalizing ranges, especially in non-core products, in order to remain

competitive.

In turn, shopper loyalty has diminished, and price has become the key driver - the emphasis

being on the price paid per item as opposed to bulk based BOGOF or TWOFOR style offers.

In larger stores, the chilled seafood counter is used as a destination for shoppers even if they

choose not to shop for it.

Retailers are continuing to invest in staff training for these areas in store as they struggle to

find points of differentiation from the discount operators although it is questionable to whether

this strategy will result in increased sales from this part of the store. History would suggest

that there is little correlation between trained staff and increased propensity to purchase

seafood.

The Northern European seafood market remains mature and any growth strategy requires

product differentiation through attributes known to be meaningful at a consumer level - value,

ease and flexibility of use, quality and positive sentiment. NEU is an important destination for

Alaska seafood, accounting for 8% of seafood imported directly - a total of 88,500 metric tons

and $276,800m.

Overall direct imports into NEU are outperforming, the total exports being up 22% in volume

and 16% in value versus performance for total Alaska product of +11% in volume value terms.

Attention is required to be given in particular to product development of the canned salmon

sector which is in significant decline and risks of delisting remain high.

In terms of volume, seafood sales at UK retailers contracted by -3.6% in the year to December

2017 with value sales increasing +3.6% due to a price increase of +7.5% across the category.

Chilled seafood declined in volume by -2.5% with value increasing by +3.6% and accounted

for over 50% of total unit sales.

Frozen seafood saw a +5% increase in value with volume dropping back marginally -0.9% with

unit sales flat. The ambient seafood category which has struggled due to price increases, range

reductions, and consumer disinterest, declined in volume terms by -9.9% but price increases of

+12.1% per kg delivered a value sales increase of +1.0%.

Salmon remains the most popular species despite a decline in volume of -10.6% in total,

accounting for a little over 51K metric tons up 3.1 percent and 0.2 percent in volume and value,

respectively, year-on-year.

11Chilled salmon, 81% of salmon volume, saw prices increase by 16.6% per kg to just under

£20k/kg - this increase begins to exclude salmon from price based multi-buy promotions where

it has worked hard to earn its place. Volume declines would continue to be expected.

Tesco and Sainsbury’s have managed to control their sales decline through large range

refreshes and share of trade for both has almost returned to its position in 2015. Morrisons,

Asda and Marks & Spencer lost share in 2017. This is the first share loss seen by M&S in some

time and a result of the increase in salmon prices which have tipped into ‘too expensive’ for

many consumers. Lidl and Aldi have delivered share gains and their combined share makes

them bigger than Sainsbury.

While last year we were happily reporting volume stability in the canned salmon sector, 2017

has been a tough year with total volume declining in ambient by -9.9% and salmon declining -

21.0%. Fewer people buying less canned salmon, less often made for a perfect storm for the

subcategory. Price increases of +16.9% per kg make canned salmon more than double the price

of canned tuna and almost the same price as chilled haddock. Inevitably with this level of

performance, retailers may be expected to undertake significant range reviews to cull

underperforming SKUs.

Understandably, retailer rationalization is a threat to partners such as John West investing to

develop new and exciting products to encourage traffic down this aisle in store and increase

the propensity to purchase.

Although price levels and pressure on disposable income are beginning to change shopping

behavior, chilled seafood remains the category which is seen to be delivering quality, and

innovation and meeting shopper needs. Frozen and canned products are not associated with

positive sentiment in the same way - with both being perceived to deliver sub-standard seafood

which lacks innovation or excitement to shop or cook. This remains challenging for Alaska

pollock and budget products, such as pink salmon, and focus has turned to encouraging the

introduction of more chilled products which meet more needs more often.

ASMI activities continue to divert consumer attention away from price-based activities by

adding value through positive, origin-related consumer promotions supported by a recipe/dish

and sustainability inspired social media strategy. Trade support works directly with key

businesses in developing new business opportunities, making new introductions with suppliers

from Alaska, and promoting the wild, natural, and sustainable image of Alaska seafood. Direct

financial trade support has been strategically focused on mainstream businesses operating in

the frozen, canned, and chilled (refreshed) sectors.

The retail sector generally recognizes and appreciates the Responsible Fisheries Management

(RFM) program but a preference for Marine Stewardship Council (MSC) certified remains.

12Consumer awareness of sustainability labels and schemes remains lackluster although this is

expected to change in 2018 due to an intensified focus on ocean plastics and associated waste

and ocean damage by vocal consumer groups and the mainstream media. The issue of

microplastics and their consumption by ocean creatures is a small leap from ‘the fish you eat

are eating plastic.’ Although this is not directly relevant to seafood purchasing, an increased

interest in anything ‘ocean’ based is highly likely to peak interest in the broader subject of

ocean health, fish mortality and potential pollution of seafood products.

Traditionally in NEU countries, the majority of consumer demographics continue to divest

themselves of responsibility for seafood, passing the responsibility onto their retailer or

restaurant of choice. However, due to the mainstreaming of these issues, it is anticipated that

this could change.

Continued campaigning by NGO groups and wider bodies to procurement in particular in

foodservice and out of home teams is resulting in changes to the products on the menu. The

Marine Conservation Society ‘Good Fish Guide’ calling on retailers and foodservice operators

to remove red-listed species is expected. This refers to the Marine Conservation Society Good

Fish Guide avoid list which is updated regularly. In the UK, ASMI maintains open and frank

sourcing discussions with procurement personnel in order to address issues before they result

in delisting.

The wider issue of social ethics has become a relevant for the seafood industry, particularly in

the UK. Here, retailers remain concerned that the potential risk to their reputation by stocking

products which may be associated with bad ethical practice is high. The area of social ethics

moves the question beyond the methods and management of the catching sector and into labor

13and workplace practices beyond that of the ‘fish.’ Labor conditions on the vessel and in

processing plants are likely to be subject to scrutiny moving forward with the latest MSC

consultation now actively considering the inclusion of ‘social ethics’ within it. In the UK, the

Modern Slavery Act 2015 required businesses with a total turnover of £36m ($51.2m) to

publish an annual statement which sets out the steps they have taken to ensure slavery and

human trafficking are not taking place in their supply chains or any part of their business. This

scrutiny of full supply chains will continue to intensify in 2018/19.

C: Export Data

Exports to NEU have increased over the past year in volume and in value representing 10.6%

and 11.2% of all ASMI exports respectively. This is an increase of 22% and 25% year on year.

Within NEU there has been a shift in volume and value away from the UK towards NL due to

changes in routes to market for frozen pollock together with dramatic changes in UK canned

market. It is challenging to analyze product movements from NL to the UK due to data coding,

a lag effect in timeframes and stock holding changes. However, it is anticipated that there is a

correlation between the declines in UK direct pollock imports with the growing NL statistics.

Impending Brexit trade barriers may make these issues more pronounced as importers and

exporters seek the most efficient routes to market bearing in mind these may not be heavily

utilized today.

Examining data to July 2017, the exports via China declined -28.6% with declines across all

species except Alaska pollock where the UK showed a marginal increase and the Netherlands

+34% in volume terms.

As with direct supply into NL, it is anticipated that much of this volume is distributed through

Europe. The UK remains the largest market for the China supply route with Denmark, Ireland,

Finland insignificant in both volume and value terms.

Cod is the largest species exported to NEU countries via China although it has declined by one

third in the year to July 2017 although the price per ton has increased +8%.

14Alaska Seafood Exports

To Northern Europe 2016/2017

2016 2017 % of Change

MT Val. (000) MT Val. (000) Volume Value

Other Shellfish & Miscellaneous

Clam 0 $ - 0 $ - - -

Geoduck 0 $ - 0 $ - - -

Octopus 0 $ - 0 $ - - -

Oysters 0 $ - 0 $ - - -

Scallops 70 $ 533 0 $ - -100% -100%

Sea Cucumber 0 $ - 0 $ - - -

Sea Urchin 0 $ - 0 $ - - -

Shrimp 0 $ - 0 $ - - -

Squid 22 $ 35 0 $ - -100% -100%

Seaweed 0 $ - 0 $ - - -

Other/NSPF 0 $ - 0 $ - - -

Subtotal 91 $ 568 0 $ - -100% -100%

Crab

King Crab (Frozen) 10 $ 330 7 $ 265 -27% -20%

King Crab (Other/Live) 0 $ - 0 $ - - -

Snow Crab (Frozen) 2 $ 14 1 $ 17 -42% 19%

Snow Crab (Other/Live) 0 $ - 0 $ - - -

Dungeness Crab 0 $ - 0 $ - - -

Other/NSPF Crab 0 $ - 0 $ - - -

Total Crab 11 $ 344 8 $ 282 -29% -18%

Salmon

Chinook (Frozen H&G) 128 $ 856 113 $ 358 -12% -58%

Chum (Frozen H&G) 1,325 $ 3,098 952 $ 3,315 -28% 7%

Coho (Frozen H&G) 328 $ 2,316 429 $ 1,895 31% -18%

Pink (Frozen H&G) 263 $ 716 558 $ 1,206 112% 68%

Sockeye (Frozen H&G) 1,606 $ 10,539 2,157 $ 15,414 34% 46%

Other/NSPF (Frozen H&G) 30 $ 217 14 $ 137 -54% -37%

Canned Chum 146 $ 444 171 $ 610 17% 38%

Canned Pink 4,486 $ 15,780 1,482 $ 5,964 -67% -62%

Canned Sockeye 3,145 $ 21,111 2,989 $ 16,858 -5% -20%

Other/NSPF (Canned) 4,170 $ 16,138 2,885 $ 13,464 -31% -17%

Other/NSPF (Roe) 70 $ 1,983 116 $ 1,806 66% -9%

All Fresh H&G 6 $ 42 2 $ 4 -63% -91%

All Fresh Fillets 4 $ 64 35 $ 465 849% 625%

All Frozen Fillets 1,656 $ 15,041 2,582 $ 18,565 56% 23%

All Smoked 15 $ 272 1 $ 18 -96% -94%

All Other Products 1 $ 10 116 $ 494 21072% 5036%

Total Salmon 17,376 $ 88,626 14,601 $ 80,573 -16% -9%

Herring

Herring (Roe) 0 $ - 0 $ - - -

Herring (Frozen) 0 $ - 0 $ - - -

Herring (All Other) 0 $ - 0 $ - - -

Total Herring 0 $ - 0 $ - - -

Groundfish

Pollock (Frozen Fillet) 35,016 $ 95,716 54,187 $ 142,191 55% 49%

Pollock (Frozen H&G) 1,338 $ 3,242 1,039 $ 2,373 -22% -27%

Pollock (Roe) 0 $ - 601 $ 6,580 - -

Pollock (Surimi) 3,328 $ 8,743 5,151 $ 12,362 55% 41%

Pollock (Mince) 2,022 $ 4,532 646 $ 1,319 -68% -71%

Pacific Cod (Frozen H&G) 6,101 $ 18,599 3,616 $ 11,786 -41% -37%

Pacific Cod (Frozen Fillet) 40 $ 101 52 $ 143 30% 41%

Pacific Cod (Dried/Salted) 0 $ - 0 $ - - -

Pacific Cod (Mince) 0 $ - 0 $ - - -

Sablefish 131 $ 2,494 248 $ 4,299 89% 72%

Rockfish 0 $ - 0 $ - - -

LingCod 0 $ - 0 $ - - -

Atka Mackerel 0 $ - 0 $ - - -

Shark/Dogfish 22 $ 120 0 $ - -100% -100%

Other/NSPF (Frozen Fillet) 0 $ - 0 $ - - -

Other/NSPF (Frozen H&G) 0 $ - 0 $ - - -

Other/NSPF (Mince) 463 $ 901 465 $ 920 0% 2%

All Other Products 0 $ - 67 $ 195 - -

Total Groundfish 48,460 $ 134,448 66,071 $ 182,167 36% 35%

Flatfish

Halibut 0 $ - 0 $ - - -

Greenland Turbot 0 $ - 0 $ - - -

Sole 38 $ 91 0 $ - -100% -100%

Plaice 0 $ - 0 $ - - -

Skates 0 $ - 0 $ - - -

Other/NSPF Flatfish 9 $ 40 0 $ - -100% -100%

Total Flatfish 46 $ 132 0 $ - -100% -100%

NSPF and By-Products

Composites (Sticks) 281 $ 1,153 33 $ 235 -88% -80%

NSPF (Frozen H&G) 0 $ - 0 $ - - -

NSPF (Livers/Roe) 0 $ - 0 $ - - -

NSPF (Mince) 6,232 $ 11,984 7,769 $ 12,786 25% 7%

NSPF (Surimi) 99 $ 286 0 $ - -100% -100%

Fish Meal 0 $ - 0 $ - - -

Fish Oil 0 $ - 0 $ - - -

All Other NSPF & By-products

Total NSPF & By-Products

42

6,653

$

$

769.5

14,192

42

7,844

$

$

826.5

13,847

-1%

18%

7%

-2%

15

Total 72,639 $ 238,310 88,525 $ 276,868 22% 16%

Source: NMFS export dataSpecies by Species Assessment:

ASMI’s mission is to increase the economic value of Alaska’s finite seafood resource to the

fishers and processors in Alaska. This means working to obtain higher prices for the limited

amount of seafood we have, as opposed to simply promoting higher sales volumes. To

convince NEU consumers to pay more for Alaska seafood, ASMI’s promotional activities

must above all strengthen the Alaska Seafood brand i.e. promote greater awareness,

understanding of and preference for Alaska seafood’s high quality and its wild and

sustainable attributes.

Shellfish and Crab

Shellfish and crab imports into NEU dropped to almost zero in 2017 with no scallops being

imported at all and only a very minor quantity of frozen king crab into NL. Although chefs

enjoy working with and showcasing king crab, imports into the market are scarce.

Salmon

Total direct salmon imports into NEU declined by -16% in volume and -9% in value.

Accordingly, the share of total Alaska products from 24% to 16.5% in volume terms.

Salmon accounts for 17% by volume and 25% by value of trade from Alaska into the NEU,

with volume declining markedly into the UK although the price per kilo increased +16%.

Species by species analysis is difficult due to the increasing use of NSPF codes making

species analysis impossible. The UK and Netherlands together account for 95% of the salmon

imports.

16Alaska salmon has many opportunities and challenges. While canned salmon has been in

decline in the market, growth in value added and canned pink sales in the Netherlands will

offer opportunity. Chilled/refreshed continues to be an exciting sector for ASMI, showing

strong growth potential. Chilled fish is the largest sector with chilled wild salmon growing

much faster (+21.1%) than total salmon with value now over £28million. The frozen sector

has seen value, volume and unit growth despite inflation as more households are shopping the

category.

Functional fitness continues to be a theme for creating consumer awareness of the postive,

healthy attributes of Alaska salmon. ASMI NEU will continue to promote Alaska salmon

through the “We are Wild” campaign with emphasis on the nutritional benefits of

incorporating Alaska salmon into the healthy living and fitness lifestyle.

Groundfish

Total groundfish species increased 35% in both volume and value terms, with over 80% of

this being frozen Alaska pollock fillets. Of this Alaska pollock frozen fillets, 97% is being

imported into NL where it is redistributed throughout Europe. In the UK, Pollock was down

by almost half in volume terms reflecting currency fluctuations and the ongoing switch back

to cod by the major retailers.

ASMI NEU has found opportunities to raise awareness of Alaska pollock through influencer

campaigns, special promotions with chefs, and continued education of the versatility of

Alaska pollock through hands-on experience.

Flatfish

There were no flatfish direct imports direct into NEU in 2017. However, the UK does see

reprocessed flatfish in the market and will continue to work with importers to learn of

opportunities to label Alaska flatfish in the market.

NSPF, (non-specified product form)

Materials in this category increased by 18% in volume terms with value declined marginally,

-2%. This was mainly due to large declines in sticks and surimi. However, mince products

increased +25% in volume terms with the price dropping back and value only increasing by

+7%. Coding of these products prevents analysis by species, most likely due to increasing use

of mixed containers.

D. Market Strategy

1. SWOT Analysis – Wild Alaska Seafood

Strengths Weaknesses

Consumers have a low awareness of the attributes of

Consistent sustainability messaging over time Alaska seafood.

17Poor understanding of species differentiation among

Increased adaption of ‘wild’ on pack and in store chefs.

Canned market continues to decline with average

Positive health attributes of products ahead of

audience now 65+.

farmed species.

Not all Alaska seafood entering the market is of the same

Variety of species - fish for every occasion and

quality.

budget.

Poor understanding in foodservice of product attributes

Vast fisheries resources and range of fishing

and use of frozen.

methods.

Narrow species use/availability in NEU from Alaska.

Exemplary fisheries management.

Lack of product innovation in canned (e.g large can size

and no ring pull) limits ability to broaden the appeal of

High-quality premium products.

canned salmon.

Lack of (frozen) storage facilities in small kitchen-based

Alaska wild and natural and historical positioning. restaurant chains.

Alaska aspirational destination adding value and

desirability to product marketing.

Versatility and range of products available.

Opportunities Threats

Health messaging – Alaska seafood is well-placed Consumer/chef preference for locally sourced

to maximize opportunities around this consumer ingredients.

trend.

Health benefits of Alaska seafood a key attribute Wide variety of seafood available at cheaper prices in

for growing sports participation market. what is a predominantly price-led market.

Refreshed category growth and innovation in the Consistency of supply due to fluctuations in volumes

retail sector. caught each year.

Schools and institutional catering using of Alaska Traditional bricks and mortar retailing continues to be

origin and messaging to differentiate and under threat and increased role for discount retailing with

encourage healthy eating. minimal ranges.

Differentiation of salmon species for differing Rationalization of SKUs across retailers and pressure on

usage opportunities. space esp in canned.

Increase in farmed salmon prices provides Consumers don’t understand the difference between

salmon species and often the difference between wild and

competitive advantage for wild salmon.

farmed.

Increased viewing of fast recipe films and food Increasing coverage around plastic pollution in the ocean

content via social media platforms. and the impact on wild fish stocks globally.

18Innovation by partners such as John West leading Increasing demand from industry for proof of social ethic

some growth in canned salmon. integrity and enhanced labor standards.

Growth of recipe based meal kit and grocery Pressure on retail margins makes cheaper, inferior

delivery services. products look more attractive.

Opportunity for RFM to be recognized as an

independent brand, as MSC is challenged by Volatility of exchange rates due to geopolitical instability

senior management change and slowness to leading to sector inflation.

respond to social ethics standards.

The color of sockeye is perceived as unnatural.

Increased use of vegan and flexitarian diet approaches by

consumers and broadly represented in mainstream media.

192. Long-term Strategy in this Market

Objectives:

• Increase consumer and trade awareness of the key merits of Alaska seafood, namely

wild, natural and sustainable.

• Encourage demand for wild Alaska provenance across consumer, trade, and HRI

groups.

• Educate consumers, trade and HRI on benefits, usages and sustainability credentials

of wild Alaska seafood.

• Inspire consumers and chefs to cook with wild Alaska product.

• Encourage foodservice innovation to offer Alaska seafood as an alternative protein for

fast casual dining

• Provide specific support for wild Alaska pollock.

• Continue to support activity to halt the decline in canned salmon consumption.

• Continue to find new trade partners for new species beyond salmon and pollock.

Strategy:

To ensure consumer preference for Alaska product, differentiation of wild Alaska seafood is

the most important facet when promoting the product to trade and consumers.

To achieve consistency with our marketing outreach we have continued to use the “we are

wild” creative across our consumer campaigns.

Consumer outreach has continued to focus on athletes, foodies and day to day seafood

consumers targeted through retail campaigns.

Much of the consumer outreach has been focused online with a noticeable increase in the

outreach via social media.

A wholesale review of positioning concluded that marketing wild Alaska seafood as fit fish to

a consumer audience with a UK bias across the southeast where research shows there is

higher consumption of premium seafood.

Consumer outreach on social media has integrated trade campaigns ensuring a holistic

approach encouraging consumers to buy Alaska and showing them clearly how and where to

buy Alaska.

The NEU website has been updated to include new content from women in seafood across

the Alaska industry and this content was syndicated to maximize outreach ensuring

provenance continues to be a major part of our story.

20As ASMI moves consumer spend from print to social and digital campaigns, the website will

continue to be updated to offer current recipe ideas, food trends and content.

Campaign themes will center on:

• Eating wild Alaska seafood for fitness/health

• Eating wild Alaska seafood for an alternative protein source to meat

• Encouraging the use of frozen Alaska seafood to minimize food waste

• Supporting canned salmon sales

• Increased promotion of wild Alaska pollock

• Ongoing education around sustainable

Campaign themes will have different messaging but will all pivot around the “we are wild”

messaging driving customers to the microsite and extending the look and feel of this high-

impact campaign.

ASMI NEU will maintain a continuous presence in the market with up-weighted activity at

key tactical moments throughout the year such as January (healthy eating), Easter, Christmas,

and spring sports event training. These key moments will be underpinned by campaign

themes such as summer BBQ, spring fitness, etc.

Finally, this calendar will be complemented with relevant national weeks (e.g. British

sandwich week, BBQ week, seafood week and U.S. events such as the Superbowl/July 4th).

Tactics

I. Consumer

• Continue to focus consumer activity online to generate maximum return on

investment and measurability.

• Grow consumer-focused social media pages Facebook, Twitter, and Instagram.

• Content strategy to focus on key calendar moments and sales periods.

• Creation of new videos for use on social media timed with key calendar events for

maximum engagement.

• Use brand ambassadors as social influencers – use the ambassadors to gain extended

social reach.

• Generate a bank of social media influencers/food bloggers as endorsers of Alaska

seafood.

• Use consumer sampling at sporting events as an opportunity to promote Alaska

seafood to sports fans and participants.

• Work with trade, retail, and restaurant partners to maximize PR outreach for Alaska

seafood with a particular focus on health and sports.

21• Develop a consumer marketing campaign focusing on wild Alaska pollock.

• Continued outreach of the virtual reality film to showcase the provenance of the

product.

• Continue to promote sustainability as a key USP for Alaska Seafood.

II. Trade

• Develop multi-channel marketing campaigns to ensure coverage at all consumer

purchase points online and in store.

• Integration of social media consumer touch points with trade campaigns.

• Continue to work with strategic partners engaging with the supply chain on a one-to-

one basis to get their buy-in.

• Focus on new product development and new trade partners.

• Support sales of new species.

• Continue to explore the opportunities presented by the meal kit and meal delivery

service market.

• Continue to work across industry to promote Women in Seafood through tactical

sponsorship, media events and partnerships.

• Develop joint promotions with other US cooperator groups to make budgets stretch

further and to reinforce provenance of product.

• Partner with Billingsgate Seafood School Sustainability events to deepen trade

engagement; educate trade on current Alaska seafood species and new species, as well

as sustainability.

• Develop profiling opportunities in the media for ASMI and partners.

• Social media outreach in partnership with trade members, sharing social plans to

ensure leverage can be gained by tagging trade companies to develop reach.

• Reinforce the validity of RFM using GSSI benchmarking results in the context of

Alaska’s sustainability heritage encouraging trade to reference GSSI in their

procurement policies.

III. HRI

• Engage with chefs, school cooks, and development executives to raise the profile and

awareness of Alaska Seafood.

22• Educate this sector from the grassroots up, with a focus on student chefs within

catering colleges and young chefs.

• Work with innovation teams to investigate opportunities for underutilized species and

new products for wild Alaska seafood in foodservice.

• Roll out e-learning to all catering colleges supported by a marketing campaign.

• Participate in presentations to catering colleges and provide product for them.

• Participate in buyers’ trade events to enable one-on-one meetings with potential new

customers.

• Participate in call center training events for wholesaler sales teams.

• Participate in school and university outreach program with a focus on more children

eating more seafood, and more schools using Alaska seafood.

• Maximize the distribution of the Virtual Reality video to inspire chefs, trade, and

colleges.

23A. Past Performance and Evaluation Results:

II. Financial allocations and resources

MAP $ 745,331

RSS $ 197,500

TOTAL $ 942,831

III. Exports – Market Level Impact

2017 GOAL 2017 ACTUAL

VOLUME: 88,525 MT

VALUE: $240,000,000 $276,868,203

in $ Terms

Table 1. Northern Europe

Year Volume (MT) Value ($) Market Share (%) Status

2005 88,617 $239,040,196 3.105% Actual

2006 81,645 $247,895,716 2.738% Actual

2007 71,101 $234,136,683 2.335% Actual

2008 61,532 $246,408,322 2.384% Actual

2009 51,292 $189,315,743 1.986% Actual

2010 57,378 $213,069,936 2.052% Actual

2011 83,092 $295,937,423 2.551% Actual

2012 66,746 $241,118,607 2.145% Actual

2013 70,681 $244,448,649 1.924% Actual

2014 74,400 $248,965,853 1.800% Actual

2015 71,353 $244,794,186 1.957% Actual

2016 72,639 $238,310,166 1.694% Actual

2017 88,525 $276,868,203 1.897% Actual

2018 Goal

24COUNTRY PROGRESS REPORT FINDINGS FY: 2017 – 2018

1. Performance Measures table

Target: Consumers in the UK, 25-54 years old who prefer wild caught seafood over

farmed.

CONSTRAINT-PERFORMANCE MEASURE TABLE

SECTOR: CONSUMER

CONSTRAINT:

Constraint: Limited consumer awareness of the origin and product attributes

(taste, natural, healthy, abundant, sustainable, nutritious and versatile for the use in

traditional and contemporary dishes) of wild Alaska seafood.

Constraint: Limited consumer awareness/knowledge within the 25 to 54 age group

about new and traditional canned salmon use, especially in hot, cooked main meal

dishes in the UK.

FY 16 FY16 ACTUAL

PERFORMANCE MEASURES FY15

Goal

ACTUAL

1 Index 1 Wild vs. Farmed 13% 14% 13%

2 Index 2 Sustainability 28% 29% 28%

3 Index 3 Comfort and preparation 84% 85% 83%

4 Index 4 Purity and Safety 46% 47% 45%

5 Index 5 Health 67% 68% 66%

6 % of target consumers who state 42% 43% 35%

they have purchased Alaska

seafood in the last six months

7 % consumers age 25-54 who state 47% 45% 49%

an intention to purchase canned

Alaska salmon in next 12 months

8 % of consumers who state intent to 78% 79% 78%

purchase if Alaska seafood was

available and offered at a

reasonable price

PM 1-8 measured by Rose Research through online surveys, 750 participants, 40% male,

60% female, average income at least $50,000 a year.

2. Results of evaluations/Impact on constraint or opportunity:

The Wild and Farmed Index (PM1), is a basket of measures covered by questions about:

Awareness of the difference between wild and farm-raised fish/seafood;

Preference for purchasing wild fish/seafood;

All AK fish/seafood is wild and not farm-raised;

25AK fish/seafood is better quality & texture than farmed product;

AK fish/seafood is nutritionally superior to farmed product;

AK fish/seafood tastes better than farmed product.

Last year’s actual result was 13% with a target of 14%. Actual for this year was 13% so no

change in this index.

ASMI NEU continues to promote “Wild” as a claim for all marketing for Alaska seafood. All

marketing material for Alaska seafood endorses the key points of provenance and source as

well as the health and taste benefits of wild. We do not compare negatively to farmed product

but continually promote the superior benefits of wild. This year, reduced budgets for the

region meant consumer advertising in print was reduced in favor of more spend online, which

reduced our consumer outreach.

In consumer marketing, ASMI has continued with the narrowing of the target demographic

from ‘family food purchasers (mums)’ and ‘foodies,’ to ‘fitness & nutrition’ and ‘foodies’.

The narrowing of the demographic to interest groups enables ASMI to better target funds and

budget, gaining an improved return on investment.

A “We are Wild” campaign ran online through 2016. The launch was timed to coincide with

a consumer focus on health and outdoor eating. The campaign included the launch of the “We

are Wild” microsite to educate consumers about the variety of seafood and inspire them with

recipes. An online advertising campaign ran across titles including Runners World, Men's

Health, Women's Health, Delicious, Eat Healthy, BBC Good Food, and Healthy Food Guide.

Some print ads also appeared in Eat Healthy, Women's Health, Olive Magazine and

Restaurant Magazine.

Increasingly brands suppliers and retailers are increasing their support promoting all Alaska

product as wild. Suppliers such as John West and retailers own label products are using wild

on the pack. John West labels pink and red pacific salmon as wild and all Waitrose own label

products call out “Wild Alaska”.

Finally, it should be noted that the anticipated reduction in availability due to a low harvest in

2016 led to low performance. A limited supply of salmon from Alaska forced supply from

other destinations who do not promote wild as a key form of differentiation.

With no forecast supply issues expected we would increase this index measure to 14 next

year.

The sustainability index (PM 2) is generated from questions about:

At least some fish/seafood is sustainable;

All AK fish/seafood is sustainable;

Look for sustainable fish/seafood when purchasing;

Sustainable fish/seafood is important when purchasing.

Last year’s results showed 28% and established a target of 29% for this year. Actual results

for this year is 28%, so we have held position not gained.

26ASMI NEU has continuously communicated with trade the advancements achieved with

Responsible Fisheries Management (RFM) gaining GSSI recognition.

Retailers continually promote their sustainability credentials as many customers value

sustainability credentials over brand or price. This is particularly true amongst millennials

(18-34 year olds) with 52% rating eco credentials higher than price or brand. This age group

continues to be targeted by NEU consumer marketing through online consumer campaigns

and through social media.

Going forward, sustainability is taking on a wider remit addressing social issues. Modern

slavery, child labor, and working conditions are all under scrutiny. ASMI NEU is in ongoing

dialogue with seafood buyers, retailers, and their customers to ensure their understanding of

wild Alaska seafood and the commitment the seafood industry in Alaska makes ensuring the

supply of seafood is sustainable now and forever.

Activity in this area has included a series of presentations throughout the year to customers of

the seafood cooking school at Billingsgate where ASMI present a case study on their

sustainable practices to consumers and chefs who are learning about buying and cooking

seafood.

The changes in consumer awareness of sustainability and all the issues that surround the

seafood industry worldwide will continue to be a challenge. Growth is slow going on many

messages to the workplace and it is hard to envisage much growth in this index in the next

year, we would suggest an index rating of 29 next year.

Index measure three covers comfort and preparation and is an expression of the following

questions:

Purchase fish/seafood that needs to be prepared;

Comfortable preparing fish/seafood at home (not microwave/ready meals);

Comfortable preparing fresh and frozen seafood for the household.

This year’s research showed an 83% score against performance measure three showing that

high levels of the demographic are comfortable preparing seafood at home.

We are seeing in the NEU region that there are more pre-prepared seafood meals available in

retailers. At fish counters within larger retail chains, fish portions are being sold with added

value herbs and sauces to facilitate easy cooking “in the bag” at home.

A growth in the market of delivery boxes – sending recipe ingredients to consumers in pre-

weighed measures, also offer an opportunity for non-traditional seafood consumers to try

cooking fish at home.

The proliferation of food delivery brands such as Deliveroo and Just Eat show eating out of

home at home is the key growth areas in today’s food society.

ASMI will seek to partner with a delivery brand in coming years and maintenance of the

index at the previous level of 84% is the proposed target.

27Index measure four, purity and safety is developed from the matrix of questions linked to this

heading:

AK fish/seafood is high quality;

AK fish/seafood is safe to eat;

AK fish/seafood is natural;

AK fish/seafood is traceable;

AK fish/seafood is pure/clean – free of contaminants.

This year we achieved 46% in this performance measure, the same as last year but not

achieving the target of 47%.

Our educational activity around the points of differentiation of Alaska seafood coming from

the clean waters of Alaska are a continued part of our consumer marketing.

A growth in consumer campaigns concerning plastic in the ocean and how it affects seafood

may affect this rating going forward.

We are aiming to maintain this momentum with a target of 46% in the forthcoming year.

Index 5 assesses health perceptions by asking questions about:

AK fish/seafood is nutritious;

AK fish/seafood has Omega-3 fatty acids;

AK fish/seafood is good for the heart;

AK fish/seafood is a good source of protein;

AK fish/seafood is an important part of a healthy diet.

The result for performance measure five on health perceptions has remained at 66% after a 5-

point growth the previous year.

Neilsen data shows that when prompted, 50% of UK adults see fish as having healthy heart

benefits. 49% say that fish contributes to healthy skin, hair and nails and 48% that it helps

contribute to the maintenance of normal brain function. 28% associate fish with maintaining

healthy blood pressure and 23% that it helps maintain healthy vision.

ASMI NEU continues to focus on activity targeting athletes and consumers who participate

in sports. These campaigns heavily promote the health values of wild Alaska seafood as a

pure source of protein with exceptional nutritional merit. This year we also ran sampling

campaigns at sporting events such as half marathons and Go Fest a sporting event targeting

families and children.

Performance measure six is a single question about “the percent of target consumers who

state they have purchased Alaska seafood in the last six months.” This result is the highest

decline in the consumer research decreasing 7% from 42% to 35%.

Two factors have contributed to this decline. Lack of availability of canned red salmon and

currency/seafood inflation.

28The total UK canned fish category has a value of £501m with canned salmon valued at £83.6

million. Within this, canned red salmon has the largest volume and has noticeably led the

decline of the sector with a year-on-year unit sales decline of 10.8%.

An uncertain economic future has meant a rise in price and food inflation +4.1%. The Fish

Consumer Price Index has reached a high of 13.6% compared to meat CPI of 3.2%. This

inflation is driving value growth but, reducing volume consumption.

The certification of Atlantic cod and decline in expected availability of Pacific cod next year

will continue to challenge this performance measure although we would expect to see some

redress to 38%.

Performance measure seven is an assessment of consumer’s intent to buy canned salmon. The

result has seen a slight increase from 47% to 49% bucking the trend of slow decline in the

canned sector.

Research shows there are 70 million occasions when canned salmon is consumed over the

year, 90% of the time this is at home and mostly at lunchtime or informal “TV dinners”. The

consumers who buy canned salmon are aging with 53% over 65 years.

ASMI NEU has been working to slow this decline over the years aiming to introduce new

younger buyers to the category and to introduce new menus and opportunities to use.

In the UK, which accounts for 85% of NEU exports of canned salmon, canned fish showed

an overall 2.4% decrease in unit and volume sales but an increase in value sales of 3.2%

driven by price inflation. Within the canned fish category, salmon decreased in value sales

10.8% and volume decreased 21.1%.

Instore sales continue to dominate this sector and ASMI NEU continues to support retailers

by running promotions with key partners such as John West and Princes.

Timed to coincide with key buying moments, an Easter campaign with Princes saw a 514%

increase in sales over the previous period based on an online, print and in-store promotion.

Princes are investing money to appeal to new customers working with bloggers and

influencers to reach young mums. Their marketing is focused on new ways to use canned

salmon and endorsing the health values of Alaska salmon.

The sole area of growth within this category is value added canned salmon. Led by John

West, these value-added products offer smaller single size ring pull cans with added flavors

such as chili and lemongrass. These value-added products are far exceeding sector sales with

growth of 57% year on year a 23% increase the previous year.

ASMI NEU continues to promote canned salmon to new, younger customers through

sampling and recipe development ideas. ASMI continues to issue recipes and inspiration to

the media on a monthly basis and across social media each week to generate interest and

ultimately consumer preference for Alaska seafood. Additionally, ASMI has created a new

recipe book for distribution at consumer events. The recipe book follows the ‘We are Wild’

campaign theme.

29We do not anticipate any restrictions in supply in the year ahead but equally as the category is

in overall decline would set a target an index of 49%.

Performance measure eight measures consumers who would purchase Alaska seafood if it

was available and offered at reasonable price. This percentage, 78%, is one of our highest

scoring performance measures although it does not reflect a change from last year.

This year availability and price have been issues for this market. However, the brand value of

“Alaska” cannot be underestimated. Never more have the key merits of the destination, wild,

natural and sustainable, been more relevant. In the UK there are issues around price inflation

for seafood and this offers a great opportunity for growth in demand and sales of Alaska

pollock.

3. Conclusion/What did you learn?

Chilled/refreshed continues to be an exciting sector for ASMI, showing strong growth

potential. Chilled fish is the largest sector with chilled wild salmon growing much faster

(+21.1%) than total salmon with value now over £28million.

This growth is a result of increased penetration up from 6.2 to 7% of the overall chilled

market. There is huge growth potential in this sector and ASMI will continue to promote the

merits of wild to grow demand and awareness within this category.

The frozen sector has seen value, volume and unit growth despite inflation as more

households are shopping the category. While the retail space for frozen is being reduced in

some stores, we are still seeing innovation in this sector from market giants such as Youngs.

NEU will continue to work with these brand partners to find opportunities for product

innovation and potentially the introduction of new species to the mix.

One fifth (19%) of 25-34 year olds now doing all of their grocery shopping online, with 36%

of this group shopping for groceries online more often now than 12 months ago. This trend is

expected to grow with the advent of meal delivery services in the future. ASMI will continue

to target online shoppers investing in online marketing campaigns with key media titles and

through retailer partner social media sites. Social media campaigns will underpin all targeted

activity.

While the canned category has its challenges, growth in value added and canned pink sales in

the Netherlands will offer opportunity. Shoppers in the UK are returning to own label

purchases and ASMI will continue to support these customers working with companies such

as LDH who provide Tesco own label and CKS who provide Dunnes Stores in Ireland.

The continued promotion of Alaska seafood to consumers who enjoy sports and are aware

their personal nutrition has continued to deliver success. We have seen higher levels of

engagement from this interest group who are very keen to learn about nutrition and ASMI

messaging. ASMI will continue to target this demographic in the coming years to introduce

new consumers to Alaska seafood.

301. Performance Measures Table

Target audience: major importers in the UK and the Netherlands, retailers in NEU, smokers

in the Netherlands, re-processors throughout the region.

CONSTRAINT-PERFORMANCE MEASURES TABLE

SECTOR: Trade

Constraint: Limited handling of Alaska seafood and limited awareness among major

importers and retailers in the UK and the Netherlands, and among re-processors (Birdseye and

Findus) within the whole region of the availability, sustainability, distinction, advantages and

preference of wild Alaska salmon and other Alaska seafood over farmed salmon and other

seafood competition.

Constraint: Limited awareness among smokers of sockeye salmon as a high-end alternative

to farmed salmon within the Netherlands.

PERFORMANCE MEASURES FY15(15/16) FY16 FY16

ACTUAL (16/17) (16/17)

Goal ACTUAL

1. Number of Alaska products included in 247 249 252

long-term product ranges (Imp/Ret/Dist)

2. Additional new Alaska seafood products 47 49 38

promoted by major retailers

3. Awareness among trade (Imp/Ret/Dist) of 93% 94% 88%

the long-term sustainability of Alaska seafood

and the inherent advantages over other seafood

competition

4. Number of smokers using Alaska sockeye 10 11 12

and ASMI POS

PM 1: Based on quarterly retail tracking survey.

PM 2: Based on retail tracking survey and information provided by trade partners including

distributors, importers, and buyers.

PM 3: Based on Rose Research online surveys 24 responses.

PM 4: Based on information provided by trade partners including distributors, importers and

buyers: Farne Salmon & Trout, Pinneys of Scotland, Franks Smokehouse NL, MaCrae

Seafoods, Severn and Wye, New England Seafoods, Barts Fish Tales, Harbour Salmon Co,

Lossie Seafoods, Bleikers Smokehouse, H. van Wijnen B.V., Roots Fish Smokery and

Forman and Sons.

2. Results of evaluations/Impact on constraint or opportunity:

PM 1: Tesco still has the highest value of seafood sales in the UK with 23.2% market share.

Sainsbury sit in second place at 15.2%, the recent accolade from MSC (Best sustainable

31seafood supermarket in the world) may have a positive impact in the future. Retail

distribution continues to evolve as Amazon and meal kit delivery services start to challenge

the status quo.

Salmon consumption has continued to grow over the past eight years despite a 36% increase

in price. Despite the decline in canned salmon sales, ASMI NEU ran successful campaigns

with Princes and Sainsbury to promote the sale of canned red salmon in the run up to Easter.

The campaign included a recipe for advertorial in the Sainsbury Magazine, trolley advertising

instore and online banner advertising. Over a four week period, the campaign generated sales

of over 91,000 units compared to an average weekly sale of 23,000. Sales were up 506% with

a 4.67 return on investment.

Waitrose has 7.5% market share, higher than Lidl, and Iceland, fractionally behind M+S

(7.6%) and Asda (8%).

With a more affluent demographic and a bias in the South of the UK Waitrose outperforms

Lidl, Aldi, and ASDA in chilled seafood sales and continues to offer the opportunity to

ASMI.

Waitrose continues to innovate offering king salmon for sale for the first time for Christmas

2016, demand for the same product in 2017 is expected to double. Equally, product

innovation such as wild Alaska keta salmon fillets with Yozo Dressing.

Throughout the year ASMI has supported trade partner New England Seafood with product

launches through Waitrose and Waitrose.com. A month long pre-Christmas campaign

including recipe cards, emails to the customer database and advertising on Waitrose.com

generated incremental sales of £280K over a four week period.

In-store sales still account for the largest volume of retail sales but online sales continue to

grow across NEU particularly with the under 40’s.

One in six Dutch consumers will buy their groceries online in 2017, with total revenue of

online supermarkets in the Netherlands expected to increase by 30 percent. As in the UK,

consumers in the Netherlands still buy most groceries instore but expectations are online

supermarkets will grow 30 percent in terms of revenue by 2017.

Albert Heijn’s online store is the most popular online supermarket with 60% of online

grocery shoppers using this website.

Analysis of products stocked online v instore products shows very little duplication between

online and instore. Larger ranges are available online and there are new products which are

not available instore showing a preference to test new products online rather than committing

to retail stocks.

ASMI continues to work with suppliers to encourage product innovation. Innovation Days

have been attended within the retail and wholesale sector and we will continue to look at

ways to introduce Alaska seafood in different ways.

Last year 247 products were listed in long-term product ranges with a target to increase to

249. Actual products counted were 252.

32You can also read