2021 Kitchen & Bath Market Outlook-January 2021- Virtual Conference ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021 Kitchen & Bath

Market Outlook

—January 2021—

About This Report The National Kitchen & Bath Association commissioned the highly regarded John Burns Real Estate Consulting firm (JBREC) to work with them to produce this report. In addition to quantifying the overall size of the kitchen and bath market, this analysis reviews the housing industry factors and consumer preferences and behaviors impacting 2021 industry growth. JBREC’s analysis employed research from a wide variety of sources: (1) secondary research (e.g., U.S. Census American Housing Microdata, National Apartment Association (NAA) Spending, National Association of Realtors, Moody’s Analytics, Home Innovation Research Labs (HIRL) data), (2) home improvement estimates and forecasts from John Burns’ proprietary studies and consultants; and (3) a custom study conducted among 4,732 consumers who had initiated a home improvement project since the start of the COVID-19 pandemic. N K B A’ s 2 0 2 0 K i t c h e n & B a t h M a r k e t O u t l o o k p r o v i d e s a c o m p r e h e n s i v e v i e w o f t h e U . S . r e s i d e n t i a l k i t c h e n a n d b a t h i n d u s t r y. N e w c o n s t r u c t i o n s p e n d i n g estimates include both single family and multi-family units. Remodeling spending estimates include improvements to both owner-occupied and rental properties. All dollar figures cited in this report include both products and labor (installed costs).

Report Contents

Impact of COVID-19 on

4 Study Overview 31 K&B Projects

5 Executive Summary 43 Project Motivations/ Inspirations

Appendix

7 Industry Size and 2021 Growth 48 • Detailed Methodology

• Consumer Demographics

Housing Industry Factors

14 Impacting 2021 K&B Growth

Cover project designed by Jenny Madden,

with photography by Tory Williams.

Study Overview

Research Purpose and Objectives

Provide an objective, thorough assessment of how COVID-19 and related economic and housing market trends

are influencing the U.S. kitchen and bath industry. This includes changes in consumer spending patterns and an

estimate of current market size and a forecast for 2021.

The primary objects of this research include:

• Determining the size of the kitchen and bath industry, including spending by project type (kitchen

versus bathroom) and end-market application (new construction versus remodeling).

• Providing market growth estimates for 2021 based on the macroeconomic factors underlying the

kitchen and bath spending forecasts for new construction and remodeling.

• Analyzing changes in consumer spending patterns, including changes in the dollar budget of kitchen

and bath residential remodeling projects, and motivations for DIY versus PRO remodels.

• Analyzing the perceptions of the importance of areas of the home to determine how COVID-19 has

changed or reinforced prior views.

• Identifying how kitchen and bathroom features are remodeled together or in isolation, this

interaction allows for a better understanding of what features trigger additional remodels.

4

Executive Summary

The NKBA’s 2021 Kitchen & Bath Market Outlook provides a comprehensive review of current kitchen and

bath industry conditions and the macroeconomic factors that are expected to impact the industry in 2021.

Key Findings:

Residential kitchen and bath remodeling spend is poised for growth in 2021 based on a mix-shift to

bigger, more expensive and PRO-heavy interior remodels. Pent-up demand for more PRO-intensive

projects is a tailwind for spending growth in 2021.

New construction spending to benefit from the timing of starts in 2020 anticipated to dollarize in 2021;

strong housing starts in the latter half of 2020 and longer build times to favorably impact new construction

spending in 2021.

Total residential kitchen and bath spending to increase 16.6% in 2021, from $136.0 billion to $158.6

billion. This is driven by a 9.9% increase in kitchen and bath remodeling spending and a 22.3% increase

in kitchen and bath new construction spending.

Of the total $158.6 billion in total residential kitchen and bath spending, $68.6 billion represents residential

remodeling spending (43%) and $90 billion residential new construction (57%). This represents a two

percentage point mix-shift away from residential remodeling towards new construction spending, driven by

faster growth in new construction.

The overall dollar spend allocation between residential kitchen spending (48%) and residential

bathroom spending (52%) in 2021 is unchanged compared to the 2020 period.

5

Executive Summary

Homeowners indicate the kitchen and bathroom rank two times more important compared to other parts of

the home. The pandemic has reinforced this perception, as the kitchen slightly gained status since the

pandemic.

Due to COVID-19, budgets for kitchen remodels fell faster than all other areas of home improvement, which is

a unique backdrop for faster growth in 2021, when the health-risks associated with a PRO inside the home

are diminished.

One key learning from the study: Kitchens remodels lead to future bathroom remodels, supporting an

acceleration in bathroom remodeling activity.

In addition, growth in cabinets, drives more widespread spending to other parts of the kitchen: product

attachment cascades from cabinets to the remodeling of other parts of the kitchen.

As COVID-19 behavior diminishes, reverting wallet share to services consumption is not likely to hurt

kitchen and bath; desire to save (given economic uncertainty) and health risks are the most influential

motivations: higher household precautionary savings is a potential source of financing for an anticipated

rebound in 2021 kitchen and bath spending.

These factors support a pronounced rebound in overall industry growth, from -5.9% in 2020 to 16.6% in

2021. Consistent with mix-shift away from less expensive remodels (pent-up COVID-19 related demand), the

high price-point for residential kitchen and bath spending is anticipated to lead growth (+19.8%),

followed by the mid price-point (+18.5%), with the low-price point posting strong, but lower rates of

growth (+9.7%).

6

Kitchen & Bath Industry Size & Growth

Kitchen design by Nyla Free, photography by Ema Peter

2021 Forecast

Projected Growth by Construction Type

Residential Kitchen and Bath Spending 2021 Spending Growth

(in billions of $U.S. Dollars) % change versus prior year

$158.6 Total

K&B

16.6%

New Construction

$90.0 22.3%

Remodel

$68.6 9.9%

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Dec 2020)

All dollars include both products and labor (installed costs).

8

2021 Forecast

Projected Value by Segment

Residential Kitchen and Bath Spending

(in billions of $U.S. Dollars)

$158.6 Total

K&B

Kitchens

$76.2

Bathrooms

$82.4

Kitchens

$76.2

New Residential

Construction Remodel

$39.5 $36.7

Bathrooms

$82.4

New Residential

Construction Remodel

$50.5 $31.9

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Dec 2020)

Notes: All dollars include both products and labor (installed costs).

9

2021 Forecast

Projected Value by Segment

Residential Kitchen and Bath Spending 2021 Spending Growth

(in billions of $U.S. Dollars) % change versus prior year

Kitchens

16.3%

$76.2

Bathrooms

$82.4 16.8%

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Dec 2020)

All dollars include both products and labor (installed costs).

10Kitchen & Bath Activities by Spend Level

$ $$ $$$

LOW MEDIUM HIGH

• Minor "update" • Medium-scale • Major full-service

remodels, often DIY. kitchen and bath remodels, usually

remodels. using a designer

• Low-cost products

and showroom.

often found in new • Products in first or

“starter” homes. second "move-up" • High-end products

homes. in new luxury

• Usually funded out-

homes.

of-pocket. • Partially funded

from cash proceeds • Upgrades financed

from home sale, via bank loan or

investments, etc. HELOC, in addition

to funding from

other sources.

Sources: John Burns Real Estate Consulting, LLC (Data: Nov-20, Pub: Dec-20)

11Spending in Mid-Price and High-Price Point

Tiers to Post Highest Rates of Growth

$ $$ $$$

Residential Kitchen & Low-spend Mid-spend High-spend

Bath Spending Price Point Price Point Price Point

(in billions of $U.S. Dollars)

$158.6 $40.4 $62.3 $55.9

18.5% 19.8%

2021 Growth

16.6%

9.7%

Sources: Census AHS Microdata, NAA, HIRL, John Burns Real Estate Consulting LLC (Pub: Dec 2020)

Note: Low-Spend, Mid-Spend and High-Spend price point estimates were computed using averages based on these project scale definitions: Small scale: $17,700 for kitchens.

12

12The Pandemic Caused a Decline in

Mid- and High-Price Point Spending

Before COVID-19 caused consumer spending to drop in 2020, total residential kitchen and bath

spending grew +9% in 2018 and +1% in 2019.

Residential Kitchen and Bath Spending by Price-Point Spend Level

(in billions of $U.S. Dollars)

2017 2018 2019 2020 2021

$70

$62

$60 $57 $57 $56

$53 $53

$50 $50 $47

$50 $45

$40

$40 $36 $37 $37

$33

$30

$20

$10

$0

Low Mid High

Sources: Census AHS Microdata, NAA, John Burns Real Estate Consulting LLC (Pub: Dec 2020)

Note: Low-Spend, Mid-Spend and High-Spend price point estimates were computed using averages based on these project scale definitions: Small scale: $17,700

for kitchens.

13

13Key Housing Industry Factors Impacting 2021 Kitchen & Bath Industry Growth

Real GDP Declined by 31% YOY in 2Q 2020 and

Rebounded 33% in Q3 2020 (annualized rate)

Real GDP – % Change Quarter-Over-Quarter Seasonally adjusted (annualized)

real GDP declined 31% in Q2 and

increased 33% in Q3, a sharper

rebound than was anticipated due

to COVID-19.

Sources: BEA (Data: Q32020; Pub: Nov-20)

See Terms and Conditions of Use and Disclaimers. 15

15

Distribution to non-clients is prohibited. © 2020Downside Risk to the Economy Greatly Diminished;

Consensus of Continued Economic Growth

WSJ Survey of Economists: Real GDP Forecast Range

+6%

+4%

+2%

0%

Even outlier forecasts indicate

positive economic growth

-2%

Q4 2020 Q1 2021 Q2 2021 Q3 2021 Q4 2021

Sources: Wall Street Journal (Data: Oct-2020; Pub: Nov-2020). Monthly Survey of > 60 Economists

Notes: Dark horizontal line represents survey median; box represents interquartile range (1st to 3rd quartile) of real GDP forecasts

See Terms and Conditions of Use and Disclaimers. 16

16

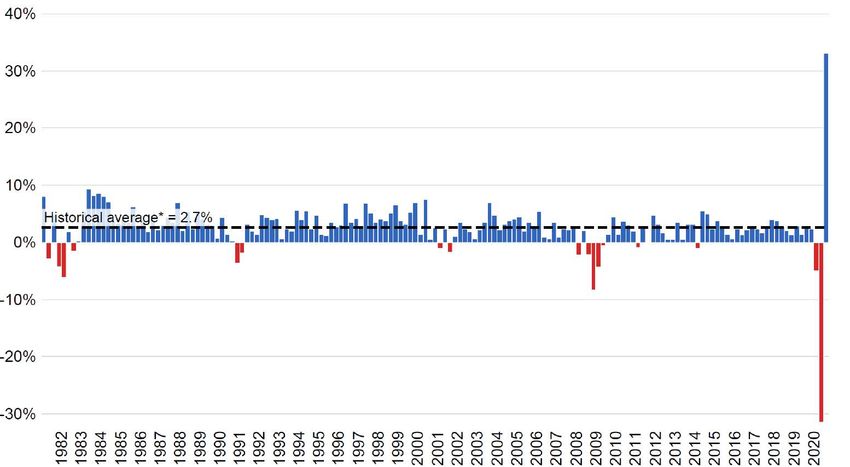

Distribution to non-clients is prohibited. © 2020Housing & Home Improvement is Leading Economy Out

of the Recession, Like the 2002 Recovery

Housing & home improvement leading

the economy out of recession

Source: BEA (Data: 2Q20, Pub, Aug-20) *Historical Average: 1Q59 through Present

Notes: Grey shaded areas indicate early 2000s recession and COVID-19 recession

See Terms and Conditions of Use and Disclaimers. 17

17

Distribution to non-clients is prohibited. © 2020Total Payroll Employment Growth has Slowed Since August; U.S.

Employment Down 9.8 Million From Cycle Peak

Total US Payroll Employment

153M

151M Job at Cycle High

149M

147M

145M

143M

141M Slowing

Employment

139M Growth

137M

135M

133M

131M

129M

2000

2000

2001

2001

2002

2002

2003

2004

2004

2005

2005

2006

2007

2007

2008

2008

2009

2009

2010

2011

2011

2012

2012

2013

2014

2014

2015

2015

2016

2016

2017

2018

2018

2019

2019

2020

Sources: Bureau of Labor Statistic, John Burns Real Estate Consulting, LLC (Data: Nov-20, Pub: Dec-20)

See Terms and Conditions of Use and Disclaimers. 18

18

Distribution to non-clients is prohibited. © 2020Employment Losses Greatest in Service Sectors with Higher In-

Person Contact; Leisure and Hospitality Down 3.4 Million

Cumulative Job Losses by Employment Sector Since Pandemic Began (in Thousands)

Leisure and Hospitality -3,449

Education and Health Services -1,256

Professional and Business Services -1,061

Manufacturing -599

Retail Trade -550

Other Services -432

Wholesale Trade -281

Information -280

Construction -279

Transportation and Warehousing -123

Financial Activities -115

Mining and Logging -90

Utilities -7

-4,000 -3,500 -3,000 -2,500 -2,000 -1,500 -1,000 -500 0

Sources: Bureau of Labor Statistic, John Burns Real Estate Consulting, LLC (Data: Nov-20, Pub: Dec-20)

See Terms and Conditions of Use and Disclaimers. 19

19

Distribution to non-clients is prohibited. © 20206 Million People Have Dropped Out of The Labor Force Since

February – Loss of Women a Concern for Growth and Productivity

6 million less people in the labor force …the recovery in the participation rate

since the pandemic began… of women has lagged that of men

Population Aged 16+ Not in the Labor Force Participation Rate:

Labor Force Men and Women

104 M 103 M 75

102 M

101 M 70

100 M

Labor Force Participation

65 Rate: Men

98 M

Labor Force Participation

96 M Rate: Women

95 M 60

94 M

55

92 M

50

90 M

Jan-19

Jan-20

Sep-19

Sep-20

Jul-19

Nov-19

Jul-20

Nov-20

May-19

May-20

Mar-19

Mar-20

Sep-19

Sep-20

Jul-19

Nov-19

Jul-20

Nov-20

Jan-19

Jan-20

Mar-19

Mar-20

May-19

May-20

Sources: Bureau of Labor Statistics, John Burns Real Estate Consulting, LLC (Data: Nov-20, Pub: Dec-20)

See Terms and Conditions of Use and Disclaimers. 20

20

Distribution to non-clients is prohibited. © 2020Employment Will Likely Take Longer to Return to Pre-Pandemic

Levels than Real GDP

43% of Economists

Expect Employment Will

Take 3 Years to Recover

See Terms and Conditions of Use and Disclaimers. 21

21

Distribution to non-clients is prohibited. © 2020CARES Act Kept Household Income Growing; More Stimulus

Needed until Economy is on Firmer Footing

Wages and Salary & Disposable Personal Income Growth

Year-Over-Year, 3-Month Moving Average

14%

12% Wages & Salary Disbursements

Disposable Personal Income

10%

8%

6%

4%

2%

Government Stimulus

0% Prevented Declines in

Household Income Growth

-2%

-4%

-6%

2011

2011

2011

2012

2012

2012

2013

2013

2013

2014

2014

2014

2015

2015

2015

2016

2016

2016

2017

2017

2017

2018

2018

2018

2019

2019

2019

2020

2020

Sources: BEA, John Burns Real Estate Consulting, LLC (Data: Oct-20, Pub: Nov-20)

See Terms and Conditions of Use and Disclaimers. 22

22

Distribution to non-clients is prohibited. © 2020~1% Lower Mortgage Rates Than 1 Year Ago Driving

Increased Demand for Homes Across Buyer Segments

Lower mortgage rates will drive home prices

higher in 2021 as more consumers qualify to buy

homes. At current rates, 71% of households

(83.6M) can afford a $200K mortgage, and 26%

(30M) can afford a $600 mortgage.

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

23

23Applications to Purchase a Home Rebounded to Pre-COVID

Levels in June and July After Severe Initial Decline in April

Purchase Mortgage Application Index

Seasonally adjusted weekly values

340

320

300

280

260

240

220

200

180

Jul-18

Nov-18

Dec-18

Jul-19

Nov-19

Dec-19

Jul-20

Jan-18

Jun-18

Jan-19

Jun-19

Jan-20

Jun-20

Aug-18

Sep-18

Aug-19

Sep-19

Apr-18

Apr-19

Apr-20

Oct-18

Oct-19

May-18

May-19

May-20

Feb-18

Mar-18

Feb-19

Mar-19

Feb-20

Mar-20

Note: The index does not capture cash transactions and thus understates actual total home buying activity.

Source: MBA (Data: Jul-20, Pub: Sep-20)

24

24Record Low For-Sale Inventory Indicates Housing Stock is Set

for Price Appreciation – a Tailwind for Large-Scale Remodels

Existing Home Inventory for Sale Existing inventory = 1.53 mil (-20% YOY)

Historical average* = 2.37 mil

3-month average (non seasonally adjusted)

4.0M

3.6M

3.2M

2.7M

2.3M

1.8M

1.4M

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Sources: NAR; John Burns Real Estate Consulting, LLC (Data: Jul-20, Pub: Aug-20) *Historical Average: Jun-82 through current

25

25~31% Total House Price Appreciation is Forecast between 2020-

2023; Driven by Supply Shortages and Underlying Demand

Projected Home Price Appreciation

10%

9% 8.7%

8.1%

8%

7%

6.0%

6%

4.9%

5%

4%

3%

2%

1%

0%

2020P 2021P 2022P 2023P

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020). December year-over-year house price appreciation growth.

26

26At ~29%, Housing Payment to Income Levels are Around the

Historical Median

27

27Strong Single Family Residential Starts Growth Anticipated

in 2020 and 2021

Single Family Starts are anticipated to …this contrasts with ongoing weakness

post strong rates of growth… for Multifamily Starts

U.S. Single Family Residential Starts U.S. Multifamily Residential Starts

2,000K 1,000K

1,800K 2020: +10% 900K 2020: -3%

1,600K 2021: +9% 800K 2021: -36%

1,400K 700K

1,200K 600K

1,000K 500K

1108K

1070K

980K

800K 400K

390K

600K 300K

307K

400K 200K

250K

200K 100K

0K 0K

2020P

2021P

2020P

2021P

Cur.mo.SA*

Cur.mo.SA*

2019

2019

Cur. Mo. SA = Current month (seasonally adjusted annual rate)

Source: U.S. Census Bureau, John Burns Real Estate Consulting, LLC forecasts (Data: Oct-20, Pub. Nov.20)

See Terms and Conditions of Use and Disclaimers. 28

28

Distribution to non-clients is prohibited. © 2020Longer Cycle Times and Product, Labor, Entitlement Causing

Starts to Dollarize in 2021

29

29Strong Single Family Starts Growth and Timing of Starts Dollarizing

to Drive +17% Growth in New Residential Building Materials

Total Spending on New Construction Residential Building Materials

Billions

$160 New construction building material spending will grow

+17% in 2021, boosted by strong starts growth and $149.0B

favorable timing of building product orders.

$140

$126.1B

7%

$120 $113.6B

$107.9B +1

$100

$80

$60

$40

$20

$0

2019 2020P 2021P 2022P

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

30

30Impact of COVID-19 on Kitchen & Bath Projects

The Kitchen and Bathroom Rank More Important Than Other

Areas of the Home; the Pandemic has Reinforced this Perception

A higher share of homeowners indicate the kitchen and primary bathroom are “extremely important” compared to

other areas of the home – nearly two times greater than the average for all rooms.

Share of Homeowners Indicating Area of Home “Extremely Important”

70%

Prior to Pandemic

64% 65% 65% 64% 65%

Since Start of Pandemic

52%

49%

37%

Average 33%

30% 30% 30% 30%

27% 27% 27% 26% 27% 27%

23%

21% 22%

19% 18% 18% 18%

15% 16%

13%

10%

Primary Bathroom

Formal Dining Area

Indoor Kitchen

Exercise Space

Home Office Workplace

Guest Room / suite

Play areas / playroom

Outdoor Kitchen

Guest Bedroom

Indoor Entertainment Area

Primary Bedroom

Formal Living Room

Guest Bathroom

Family Living Area

Outdoor Area

Q1

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

32

32Indoor Kitchens Faced the Specter of Deferral in 2020;

Tailwind for Future PRO-Intensive Projects in 2021

Big interior projects (such as Indoor Kitchen remodels) are more PRO-intensive. Due to the invasive nature of

having a professional in the home since the start of the pandemic, these projects are likely deferred until there is

less health-risk associated with having a professional inside the home.

PRO Share of Remodels by Area of Home

Indoor Kitchen 43%

Guest Room / suite 42%

Formal Living Room 40%

Primary Bathroom 38%

Guest Bathroom 37% Indoor kitchen

remodels have

Formal Dining Area 37% the highest PRO

Play areas / playroom 35% share among

Exercise Space 35% areas of the home

Primary Bedroom 33%

Family Living Area or Great Room 33%

Indoor Entertainment Area 32%

Guest Bedroom 32%

Home Office Workplace 32%

Outdoor Area 29%

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

33

33Mix-Shift Down Positions for a Mix-Shift Up When the Health-

Risks Associated with a PRO Inside the Home are Diminished

The shift away from large invasive PRO remodeling projects since the start of the pandemic has had a

pronounced impact on the average spend of indoor kitchen remodels compared to other areas of the home. This

positions for a rebound in bigger, higher spend PRO-intensive remodels in 2021.

Percent Change in Average Remodeling Project Dollar Budget Since COVID-19 Pandemic

Indoor Kitchen Projects Projects other than Indoor Kitchen

10%

1%

0%

-10%

-20%

-30%

-40%

-50%

-60% -54%

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

34

34Cabinets Frequently Act as an Anchor for the Remodeling

of Other Kitchen Features

Cabinets are frequently remodeled within a basket of other kitchen features. This suggested that cabinets are an anchor for

additional kitchen remodels.

Cabinet Product Attachment

Cabinet remodels anchor

additional kitchen remodels

Note: Includes both indoor and outdoor kitchens.

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

35

35Cabinets Had the Highest Share of “Budget-Friendly” Remodels

Smart home products and water filtration systems were the focus of premium feature upgrades since the start of

the pandemic; cabinets received the lowest share of premium upgrades.

Shift in Price Point of Kitchen Features

100%

90%

33%

80% 44% 43%

49% 46% 45%

54% 51% 51%

70% 57%

60%

50%

40% 52%

32% 38% 37% 39% 42%

31% 37%

30% 30%

32%

20%

10% 16% 18% 19% 16% 18% 16%

11% 12% 15% 15%

0%

Smart home Wa ter filtra tion Appliances Countertops Faucets / Backsplash Range hoods Flooring Lighting Cabinets

products systems plumbing

No upgrade in quality Budget friendly option Premium upgrade

Note: Includes both indoor and outdoor kitchens

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

36

36The Share of Premium Upgrades Rises Across All Kitchen

Features with Higher Household Incomes

Luxury and premium upgrades to kitchen features are more likely to be undertaken by higher income

households (earning more than $120,000).

Share of Households Indicating “Premium Upgrade” to Kitchen Feature

Households Earning Less than $120,000

100%

Households Earning More than $120,000

90%

80%

70% 65%

60% 60%

60% 58%

54% 54% 55%

50% 51% 50% 50% 50%

50% 48%

45% 44% 43%

40% 41%

40% 37%

29%

30%

20%

10%

0%

Smart home Water filtration Appliances Countertops Faucets / Backsplash Range hoods Flooring Lighting Cabinets

products systems plumbing

Note: Includes both indoor and outdoor kitchens

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

37

37In Addition to Household Income, Stage of Life Influences the

Choice of a Premium vs. More Budget-Friendly Kitchen Remodel

Drilling down further within the higher earning household cohort, the “Mature Households” (age 45+ with no

children) have the highest share of premium upgrades to the kitchen. This indicates stage of life and household

income jointly influence kitchen remodel cost considerations.

Share of All Kitchen Features Remodeled: Households Earning more than $120,000

100% 32 percentage point

increase in share of

90% premium upgrades

to kitchen features

Premium upgrade

80% 40% Premium upgrade

Premium upgrade 46%

70% 54%

Premium upgrade

60% 78%

50%

Budget friendly option

40% 40%

Budget friendly option

30% Budget friendly option 40%

33%

20% Budget friendly option

9%

No upgrade in quality

10% 20% No upgrade in quality No upgrade in quality No upgrade in quality

13% 14% 13%

0%

Young single or couple (under age 45) with no Family with childr en in the household, all Family with childr en in the household, some Mature single or couple (age 45+) with no

children in the household under age 12 (or all) older than age 12 (including adult children in the household

children)

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

38

38Kitchen Remodels Inspire Bathroom Remodels; Bathroom

Remodels Inspire Kitchen Remodels to a Lesser Degree

Longer-term kitchen remodels will be followed by future bathroom remodels. Deferred big project, PRO-

intensive kitchen remodels are likely to lead to strong bathroom remodeling activity.

% Respondents Indicating Next Project on the Remodeling “To-Do” list

Households are approximately two times more likely to

remodel their bathroom after an indoor kitchen remodel than

the other way round

18%

9%

B AT H R O O M R E M O D E L KITCHEN REMODEL

Following indoor kitchen remodel Following bathroom remodel

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

39

39Bathroom Remodels Did Not Mix-Shift Down as Did Kitchen

Remodels Since the Start of the Pandemic

The more invasive nature of having a PRO in the home for a large remodel had less of an impact on bathroom

remodels since the start of the pandemic, compared to kitchen remodels. Deferral of kitchen projects is more of

a story of aversion to having a PRO-in-the-home; bathroom remodels more of a DIY story.

Average Remodeling Budget: Primary Bathroom Remodels Since the Start of the Pandemic

$4,500

$4,000

$3,500

$3,000

$2,500

$2,000

$1,500

$1,000

$500

$0

Pre-Pandemic Since the Pandemic

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

40

40Bathroom Remodels Have Less of a Clear Anchor

to a Given Bathroom Feature

Bathroom remodels often touch other areas in the bathroom and have less of a clear anchor to a given bathroom feature

remodeled. Premium bathroom remodels, such as those which include smart home products, are often completed in

isolation and not with the addition of other areas of the bathroom.

Count of Bathroom Features Remodeled Together

Bathroom Remodels often involve multiple areas of

the bathroom; premium upgrades (smart home

products) equally likely to be done in isolation

.

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

41

41Plumbing and Cabinets Were the Focus of “Budget” Remodels

Since the Start of the Pandemic

Premium upgrades are concentrated in smart home products for bathrooms. Consumers are more likely to

choose “budget-friendly” options in their bathroom remodels than in their kitchens.

Bathroom Features Remodeled Since the Start of the Pandemic

100%

90%

33%

80% 43% 42% 42% 42%

47% 46% 45% 45%

70% 58%

60%

50%

40% 38% 36% 52%

35% 35% 35% 39% 43%

38%

30%

31%

20%

10% 19% 20% 20% 18% 20% 22%

11% 15% 16% 15%

0%

Smart home Flooring Lighting Bathtubs Toilets Cabinets Countertops Mirrors Faucets / Cabinets

products plumbing

No upgrade in quality Budget friendly option Premium upgrade

Note: Includes both indoor and outdoor kitchens

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

42

42Project Motivations / Inspirations

The Desire to Save, Time Allocation and Health-Related

Motivations Drive Choice to Do Recent DIY Projects

The pandemic has shifted the focus towards DIY projects for reasons related to saving money, more free time to pursue

projects, the direct health risk of the pandemic (avoiding a PRO in the home) and shifting wallet share. These projects are,

in general, less costly and smaller remodels compared to those requiring a PRO. A vaccine, or other measures to reduce

the public health impact of the virus, is likely to reverse or mitigate these DIY boosting trends.

Reasons Cited as a “Significant Factor” for Recent DIY Projects

Shifting wallet share trails

more influential reasons for

25% a DIY project

23% 22%

15%

12%

3%

Desire to save money More free time to Health and safety Availability of Inability to find an Other

pursue DIY projects concerns discretionary funds industry professional

previously spent on to do the work

Increased savings activities

potentially a source of

financing for larger kitchen

and bath projects in 2021

Source: JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

44

44Discretionary Spend Motivations Dominate other Reasons

for a Remodel Since the Pandemic Began

Households indicated that considerations such as improving the home’s aesthetics, maximizing quality and

durability, and increasing the value of the home are primary motivations for both kitchen and bathroom remodels

since the start of the pandemic. Increasing storage appears to be a stronger motivation for kitchen remodels,

compared to bathroom remodels.

Motivations for Kitchen and Bathroom Remodels Since the Start of the Pandemic

Bathroom

18% Discretionary reasons for a

16% remodel lead other categories Kitchen

16% 15%

14%

12%

12% 11% 11%

10% 11% 10%

10% 10%

10% 9%

8%

8% 7% 7% 7% 7% 7% 7% 7%

6% 6% 6%

6%

4%

2% 1% 1%

0%

Improve your Maximize Increase value Increase Replace similar Repair existing Create a more Minimize cost Promote or Add luxury for Improve safety / Other

home's quality / of your home storage existing item products or functional protect our your enjoyment accessibility

aesthetics durability installations floorplan health

Source: NKBA/ JBREC Online Survey Panel, John Burns Real Estate Consulting LLC (Data: Nov-19, Pub: Dec 2020)

45

45Google Search and Social Media are the Primary Inspirations

for Kitchen & Bathroom Remodels

Google Search is the primary inspiration for kitchen and bathroom remodels. This is followed by a variety of

other sources where homeowners find inspiration. Households frequently indicate they rely on more than

one source to inspire them prior to a remodel.

Sources of Inspiration for Kitchen and Bathroom Remodels (% of Responses)

Google search

Kitchen

Instagram

Bathroom

Television show / HGTV

Design professional

Pinterest

Facebook

Other homes I have seen in person

Other

Houzz

Magazine

Design blog

E-design website

0% 5% 10% 15% 20% 25%

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

46

46The Importance of Google and Social Media is Robust Across

Most Life Stages, Particularly Younger Households

Mature adults (45+) put greater weight on “other homes seen in person” than social media. This contrasts

with other Stage of Life categories.

Top Three Sources of Inspiration for Kitchen Remodels by Stage of Life (% of Responses)

30%

25%

Google

Google

Google

20%

Other Homes Seen in Person

Instagram

15%

Instagram

Google

Instagram

Television

Design Pro

Television

10%

FB

5%

0%

Young Single or Couple Family with Young Children Family with Older Children Matures Singles or Couples

YOUNG SINGLE FA M I LY W I T H FA M I LY W I T H M AT U R (45+)

E SINGLES

OR COUPLE YOUNG CHILDREN OLDER CHILDREN OR COUPLES

(45+)

Source: John Burns Real Estate Consulting LLC (Data: Nov-20, Pub: Dec 2020)

47

47Appendix

Kitchen design by Karen Swanson, photography by Jared KuziaDetailed Methodology

New Construction: John Burns Real Estate Consulting (JBREC) analyzed construction costs for new construction spending by

category within new home kitchens and bathrooms. Homes were segmented by size and price point. Due to regional differences in

home price points, segmentation was conducted by nine census divisions, then rolled up. All figures include both products and

labor (installed costs).

Kitchen and Bath Remodel: Spending values are JBREC calculations from tabulations of U.S. Census American Housing Survey

home-improvement projects microdata, NAA spending (rental), JBREC home-improvement estimates, and forecasts of single-

family rental renovation spending. All values include labor and materials, including all major elements within kitchen and bath

spending (plumbing fixtures, faucets, tile, vanities, countertops, lighting, showers and baths, etc.).

To better understand project activity in-light of COVID-19, a total of 4,732 online surveys were conducted in mid-November of 2020

among homeowners who had initiated a home improvement project since the start of the COVID-19 pandemic.

• Target household income distribution to approximate AHS 2019 survey of homeowners

• Target household head age distribution to approximate AHS 2019 survey of homeowners

Respondents were represented across four noncontiguous U.S. regions as defined below:

• Northeast: Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, Vermont, New Jersey, New York, Pennsylvania

• Midwest: Indiana, Illinois, Michigan, Ohio, Wisconsin, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, South Dakota

• South: Delaware, District of Columbia, Florida, Georgia, Maryland, North Carolina, South Carolina. Virginia, West Virginia, Alabama, Kentucky,

Mississippi, Tennessee, Arkansas, Louisiana, Oklahoma, Texas

• West: Arizona, Colorado, Idaho, New Mexico, Montana, Utah, Nevada, Wyoming, Alaska, California, Hawaii, Oregon, Washington

Source: NKBA/ JBREC Online Survey Panel; n=4,732

49Consumer Demographics

Age Range

40%

33%

30%

20%

14% 15%

10% 9%

10% 5% 5% 6%

3%

0%

Under 30 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65 or over

Annual Household Income Distribution

30%

23%

20%

7% 9% 8% 8% 6% 8% 7%

10%

4% 6% 6%

3% 4%

0%

< $10K $10K - $20K - $30K - $40K - $50K - $60K - $70K - $80K - $90K - $100K - $110K - > $120K

$19.9K $29.9K $39.9K $49.9K $59.9K $69.9K $79.9K $89.9K $99.9K $109.9K $119.9K

Source: NKBA/ JBREC Online Survey Panel; n=4,732

Notes: Raw data shown. Target sample weights determined according to the 2019 AHS survey; subset of homeowners.

50Limiting Conditions

The conclusions and recommendations presented in this report are based on our analysis of the information available to

us from our research as of the date of this report. We assume that the information is correct and reliable and that we

have been informed about any issues that would affect project marketability or success potential.

Our conclusions and recommendations are based on current and expected performance of the national, and/or local

economy and real estate market. Given that economic conditions can change and real estate markets are cyclical, it is

critical to monitor the economy and real estate market continuously, and to revisit key project assumptions periodically to

ensure that they are still justified.

The future is difficult to predict, particularly given that the economy and housing markets can be cyclical, as well as

subject to changing consumer and market psychology. There will usually be differences between projected and actual

results because events and circumstances frequently do not occur as expected, and the differences may be material. We

do not express any form of assurance on the achievability of any pricing or absorption estimates or reasonableness of the

underlying assumptions.

In general, for projects out in the future, we are assuming “normal” real estate market conditions, and not a condition of

either prolonged “boom” or “bust” market conditions. We do assume that economic, employment and household growth

will occur more or less in accordance with current expectations. We are not taking into account major shifts in the level of

consumer confidence; in the ability of developers to secure needed project entitlements; in the cost of development or

construction; in tax laws that favor or disfavor real estate markets; or in the availability and/or cost of capital and

mortgage financing for real estate developers, owners and buyers. Should there be such major shifts affecting real estate

markets, this analysis should be updated, with the conclusions and recommendations summarized herein reviewed and

reevaluated under a potential range of build-out scenarios reflecting changed market conditions.

We have no responsibility to update our report analysis for events and circumstances occurring after the date of our

report. This analysis represents just one resource that should be considered when assessing a market opportunity.

51All NKBA research reports can be accessed by clicking here and visiting the Market Research page at NKBA.org. About the National Kitchen & Bath Association The National Kitchen & Bath Association (NKBA) is the not-for- profit trade association that owns the Kitchen & Bath Industry Show® (KBIS), as part of Design and Construction Week® (DCW). With nearly 50,000 members in all segments of the kitchen and bath design and remodeling industry, the NKBA has educated and led the industry since the association’s founding in 1963. The NKBA envisions a world where everyone enjoys safe, beautiful and functional kitchen and bath spaces. The mission of the NKBA is to inspire, lead and empower the kitchen and bath industry through the creations of certifications, specialty badges, marketplaces and networks. For more information, visit www.nkba.org or call 1-800-THE-NKBA (843-6522). KBIS ® and NKBA ® are registered trademarks of the National Kitchen & Bath Association. Kitchen design by Sarah Robertson, AKBD, photography by Adam Kane Macchia

You can also read