2021-2022 Retirement Basics - City of Portland, Oregon

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2021-2022 Retirement Basics

Today we will discuss the following:

Transition to Health Deferred

Retirement Insurance Compensation

Tools for decision making

• Create an online account on the Social Security website • Get personalized retirement benefit estimates using the new Retirement Calculator

• Create an Online Member Service (OMS) account today at www.oregon.gov/pers • View current account balance, see employment history, salary information, and generate and save a benefit estimate • Contact PERS with questions at 503-598-7377

Attend a PERS presentations held online with PERS via their website Request a written benefit estimate from PERS if you’re within 24 months of retirement Sign up with PERS for a Retirement Application Assistance Session (RAAS) within 90 days of retirement

When can I retire?

Tier One Tier Two OPSRP Pension IAP

If you began working If you began working Everybody on The City contributes

for a PERS employer for a PERS employer

on or before 12/31/95 before 8/29/03 or after 8/29/03 6% of your monthly

salary

Normal / Full 58 (or 30 years) 60 (or 30 years) 65 (58 w/30 Members retire from

retirement age P&F = age 55 or 50 P&F = age 55 or 50 years) IAP when they retire

w/25 years w/25 years from PERS

Early retirement 55 (50 for P&F) 55 (50 for P&F) 55, if vested Members retire from

IAP when they retire

from PERS

Retirement calculation Money Match, Full Money Match or Full Formula

methods Formula, or Formula + Formula

Various account

Annuity (if eligible) payouts or rollover

Full Formula benefit 1.67 percent general 1.67 percent general 1.50 percent general N/A

factor

Formula + Annuity 1.00 percent general N/A N/A N/A

benefit factor

Lump-sum vacation

payout

- Included in covered Yes Yes No

salary (6%)

- Included in FAS Yes No No N/A

Unused sick leave Yes Yes No N/A

included in FAS

The Top 10 Retirement Decisions

When to Retire

When to claim Social Security

Health Coverage

How much you can safely spend each year?

How much investment risk

When to pay taxes on investments

Where to live

Other ways to finance retirement

Whether to keep working

What you will do with your free time?

Source US News and World Report

Health Care Expenses

Did you know….

A non-Medicare eligible person entering retirement

today can expect to spend at least $9,000, per person

per year, for healthcare premiums and medical

expenses

Options for Health Insurance

Federal Exchange: Shop around for

City of Portland: Stay on the City of

coverage for you and/or your

Portland’s coverage until you

dependents through the Federal

become Medicare eligible.

Exchange.

Medicare/Supplement: Are you or

your spouse eligible to be on a Spouse’s Plan: Is your spouse still

Medicare plan? If so, you may save working? If so you can move onto

money by enrolling in a Medicare their group health plan.

Plan outside of the city.

PERS: Are you or your spouse

eligible to be on a Medicare plan? If Military/Tricare: If you were in the

so, you may save money by enrolling service, you can move over to the

in Medicare Plan outside of the city, military’s health insurance.

such as PERS Health Insurance.

Retiree Monthly Cost

• City of Portland Retiree’s pay 100% of their premium.

• The cost per month will depend upon what plans you are

enrolled in and your family size.

• Below is an estimate for the monthly Retiree Rates:

Retiree Family (3+)

Retiree + 1

Only $2,020

$1,440

$760

The complete list of monthly retiree rates is located online at

www.portlandoregon.gov/retireeWhen does my employee coverage end?

Coverage ends at the end of the month in which you leave,

unless you are PPA, PPCOA & PFFA member

• Notify your bureau that you are retiring at least 2 weeks

or more in advance

• When BHR receives a final check request, a retiree

enrollment packet will be sent to your home

• If you have other coverage, you do not have to return

any forms

• If you are Medicare eligible you are not able to stay with

your current plan

• PERS requires employees to retire on the 1st of the

month2021

If February 1st is your

PERS retirement date…

…your last day at work would be in

January, the previous monthCOBRA vs. Retiree Coverage

COBRA Retiree

• You will be sent both COBRA & Retiree Election forms in your

Retiree packet.

• As a retiree, complete & return the Retiree Election formPayment Option

ACH

Comes out

City of

Bank on the 6th of Portland

Account

each month

DebitThe plans are the same for both active

and retired employees

• Your ID numbers will not change after you retire.

• Create online accounts to access resources or order new cardsWhile on Retiree Coverage

Annual Open Enrollment every

May – June

Keep the benefits office updated

with current contact information

Can change plans if you move out of

the service or network

Moda Participants: You or dependents living outside of the service area will

access the PHCS network for in-network services

Kaiser Participants: If you move outside of Kaiser’s Service area you are no

longer eligible to continue Kaiser coverage; you could move to a Moda planLeaving & Coming Back

Prior to turning 65 or becoming Medicare eligible,

retirees can choose NOT to elect Retiree coverage

and return to City coverage at a later time if … :

• You’ve been enrolled in an employer/group

health plan

• You’ve been enrolled in a federal exchange

plan or individual plan*

• Proof of other coverage is required

* This provision is limited to one time per participant for

those who have had a federal exchange plan

or individual planWhat if I continue to work after I retire? • You can continue active employee coverage for 1 year & delay enrolling in retiree coverage • If you’re age 65, you can delay signing up for Medicare Part B because of the SEP (special enrollment period) and your creditable employer coverage • You would need to sign up for Medicare at least 60 days prior to your employer coverage ending; contact our office to get an “employer verification form” to submit to Social Security - Contact Mt. Hood Community College for free “Welcome to Medicare” class or SHIBA (Senior Health Insurance Benefits Assistance): 800-722-4134 - SHIBA in WA (800-562-6900) - Enroll in Medicare online at www.medicare.gov

Medicare Basics

Parts A and B are called original Medicare;

administered by the federal government

Part A

Hospital

Parts C and D are individual plans purchased

Insurance

through private insurance companies or

under a group such as PERS to supplement

original Medicare

Part D

Medicare Part B

Prescription has 4 Medical

Drug Plan Insurance

Parts

Part C

Medicare

Advantage

PlansLog on to view plans, rates, presentations

www.pershealth.comEmployee Assistance Program (EAP)

• FREE Counseling Sessions

• 30 minute free consultation

Eldercare/Child Care with an attorney

Services • Financial Coaching

• Eldercare Assistance

• Wills & Advanced Directives

assistance

To Access: (800) 433-2320

1. Go to www.cascadecenters.com www.cascadecenters.com

2. Click “Member Log-In”

3. Register as a new user

4. For Company Name enter: City of PortlandContinuing Life Insurance

You may choose to port up to

Minimum Amount: $20,000

$200K & continue to pay the same Maximum Amount: $200,000

active employee rates Supplemental

until age 75 Life Insurance

$200,000

Basic Life

Insurance

$50,000 Spouse/DP

A life Insurance

portability application Supplemental Minimum Amount: $20,000

Life Insurance Maximum Amount: $30,000

will be included in your

retiree packet $30,000

Dependent

Supplemental

Life Insurance

Minimum Amount: $5,000

Maximum Amount: $25,000Keep in mind… If you are enrolled in healthcare FSA, “spend” your contributions on or prior to your last day of work You can’t switch plans when you enroll in retiree coverage until the next open enrollment If you drop your dental coverage at the time of enrolling in retiree coverage, you can NOT re-enroll in dental coverage

City of Portland

457(b) Deferred

Agenda

Compensation Plan

Deferred Compensation

Basics

A 457(b) Deferred Compensation Plan is an important

retirement plan offered by the City, created to allow public Enrollment & Contribution Changes -

employees, like you, to set aside money from each Employee Self Serve (SAP CityLink)

paycheck toward retirement. A Deferred Compensation Plan

may help bridge the gap between what you have in your Deferred Compensation

pension and other retirement benefits, and how much you’ll Provisions

need for retirement, or simply add additional funds to your

retirement portfolio. Deferred Compensation

Before Retirement

The City’s Deferred Compensation plan (the Plan) is a

Deferred Compensation

voluntary plan available to eligible employees that helps you After Retirement

save for retirement on a tax-deferred basis.Deferred Compensation Basics

May contribute Traditional Pre-tax or Roth

Post-tax amount

IRS limit for 2021 is $19,500

Minimum contribution 1% of pay or $10 per

pay period

Electronic/paper election forms completed and

received by the 15th of each month are

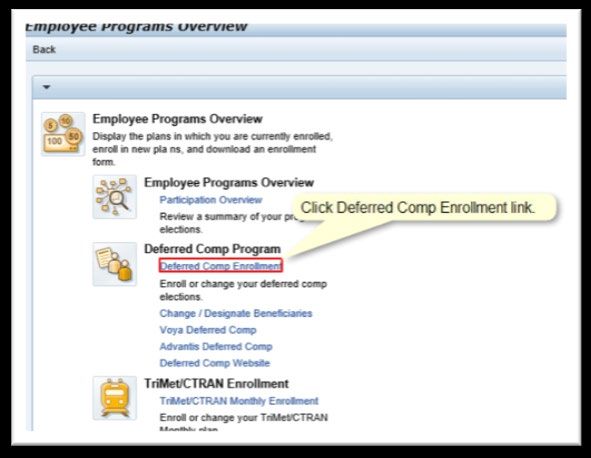

effective the first payday of the next monthEmployee Self Service

(SAP CityLink)

Through your Employee Self Service Portal, you can:

• Enroll in Deferred Comp

• Increase/Decrease or change your Deferred Comp election

• Designate beneficiaries

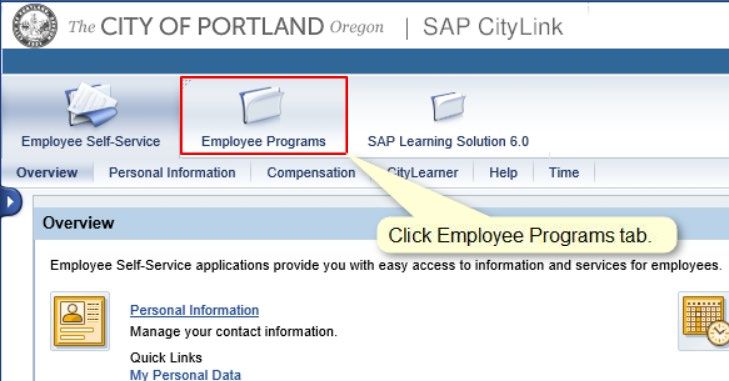

• Stop your contributionsEmployee Self Serve

(SAP CityLink)

On a City computer, log on to your

Employee Self Service portal at

www.portlandoregon.gov/ep. Once

logged in, navigate to the Employee

Programs tab.

You’ll then be able

to see the Deferred

Comp categoryEmployee Self Serve

(SAP CityLink)

On a City computer, log on to your

Employee Self Service portal at

www.portlandoregon.gov/ep. Once

logged in, navigate to the Employee

Programs tab.

You’ll then be able

to see the Deferred

Comp categoryEmployee Self Serve

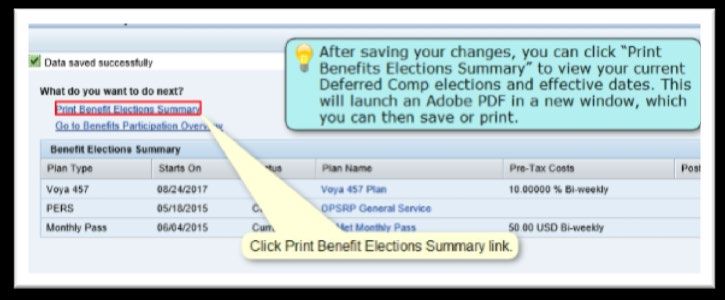

(SAP CityLink)

Be sure to review your plan

choices, then click SAVE.

You can save/print a summary

of your enrollments, or return to

the main menu.

* New enrollments entered in the system by

the 15th of the month will be reflected on the

first paycheck received the following month.

Enrollments entered after the 15th of the

month are reflected the month after.Deferred Compensation Provisions Age 50 Catch-Up • The regular contribution limit is $19,500 for those under age 50. The age 50 catch-up limit is $26,000 for 2021 (Normal $19,500 limit + $6,500 for 2020 = $26,000) • Qualify for this catch-up provision at age 50 (anytime in calendar year). 3 Years Prior to Normal Retirement Age (NRA) • The 3 Year Catch-up provision allows participants to make up contributions for prior eligible years where the maximum contribution was not deferred. • Available 3 years prior to Normal Retirement Age. May contribute twice the regular deferral limit ($19,500 + $19,500 = $39,000 for 2021). • This may change if the IRS announces new contributions limits. • One-time Application is required for the 3 Year Catch-up. • The maximum age to apply is 70 ½.

Before Retirement:

Deferred Compensation

Final Paycheck Election

You may elect on your final check when you retire to contribute your eligible payout accruals (based

on the union contract you fall under) to your Deferred Compensation Plan account.

You must meet the following requirements:

1. Have a City Deferred Compensation account established. It’s not too late to Enroll!

2. Return the Final Paycheck Election form to the Health & Financial Benefits Office prior to

your last day of work and prior to your final paycheck processing.

3. The contribution of your eligible payouts would have to fall within your maximum limit for

the year reduced by how much have already contributed for 2020.

If you are eligible for the 3 year special catch up, you may exceed the $19,500 in this

calendar year. For future catch-up years, the additional $19,500 may increase if the IRS

announces increased limits.After Retirement:

Deferred Compensation

When Can I Access My Money?

• Retirement or Termination of Employment

• Unforeseen Emergencies (Application Required)

What Can I Do With My Money After I Leave?

• Leave it the City’s Deferred Compensation Plan and begin mandatory minimum

distributions at age 72*

• Can move assets within the Plan just as you did as an active employee or rollover funds to an

outside Investment Provider.

• Start drawing money from the account (pay taxes on withdrawals). Set-up automatic payments

or take a lump sum distribution.

• You may choose to receive your payments by specific amount, specific period, or a lifetime

payment (an annuity) to be payable monthly, quarterly, semi-annually or annually.

• Rollover to qualified plans (traditional IRA, 403(b), 401, and other government 457 plans) are

permitted. 457 assets rolled to a non-457 plan may not be rolled back to a 457 plan.Deferred Compensation Contact

• Create online access to your account

• Meet with a local Voya Rep to review investment

allocations or financial planning assistance

• Online appointment system

• 503-937-0378

Participants can:

• Contribute to both options and/or rollover prior • Complete electronic beneficiary

retirement funds elections

• Apply for unforeseen emergency withdrawals • Manage Voya changes through

custom websiteQuestions? We are Here to Help!

Debi Danielson

Retiree Coordinator

(503) 823-6240

Debi.Danielson@portlandoregon.gov

Anne Hogan

Benefits Analyst

(503) 823-6228 View rates, retiree checklist

Anne.Hogan@portlandoregon.gov & other presentations online:

www.portlandoregon.gov/retiree

General Benefits Line

Deferred Compensation Questions

(503) 823-6031

benefits@portlandoregon.gov

Retiree Benefits

Email Inbox

retireebenefits@portlandoregon.govYou can also read