2020 US CONSTRUCTION INDUSTRY ANALYSIS DURING COVID - RESEARCH & CONSULTING

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

November 2020

2020 US CONSTRUCTION INDUSTRY

ANALYSIS DURING COVID

Updated Analysis and Outlook for 2021

RESEARCH & CONSULTING

At a Glance

Ducker is a leading global

market intelligence and

consulting firm with 60 years 60 200+ 9 1 goal

years professionals offices to support our clients’

of experience in the growth mandates in their

construction industry and a most important markets

long-standing partner of USG

Deep Industry Expertise Global Capabilities Proven Research and Consulting Services

Dedicated sector practices for: Dedicated research Separate signal from noise to understand opportunities and

practices for 80+ markets across: market risks through:

• Automotive & Transportation • Asia Pacific • Deep construction expertise and renowned access to

• Building & Construction • Latin America decision makers

• Consumer Products • Europe • Valuable proprietary data and forecasts

• Healthcare • Middle East & North Africa • Custom research and analytics

• Heavy Equipment • Sub-Saharan Africa • Innovative research tools, methods across quantitative,

• Industrial • North America qualitative and digital

• Private Equity

• Technology

CONFIDENTIAL -DUCKER HOLDINGS LLC 2

Industry Insights Leading Up to COVID CRISIS

CONSTRUCTION ($) PIP TREND

$700,000

$600,000

$500,000

$400,000

$300,000

$200,000

$100,000

Great Recession

$-

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Residential Building Nonresidential Building Nonbuilding Construction

• Residential construction spending experienced significant decline in past recession due to unqualified lending and less

healthy consumers

• Residential was demonstrating an adjustment in 2019, however likely a false negative given excellent rebound in December

through February

• Nonresidential performing typical cycle behaviors with some concern for office/bank/retail activity in 2018 and 2019

• Infrastructure needs, improved state and local balance sheets and political alignment fueled slow, steady growth in spending

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

CONFIDENTIAL -DUCKER HOLDINGS LLC 3

Construction Has Not Kept Up with Household Growth

Residential construction has not kept pace with the minimum housing requirement – causing a shortage of available supply for new households and likely

long-term benefits beyond 2020.

MINIMUM HOUSING REQUIREMENTS VS. COMPLETIONS &

PLACEMENTS OF NEW HOUSING UNITS

Millions of units

▪ After a decade of low levels of

2.25

The Census Bureau indicates the U.S. building due to conservative

Housing market needs 350 K units per year development plans, housing stock

above new households just to replace lost is currently well short of US

units, which has not happened since 2008

2.00 demand

▪ In 2017 Freddie Mac estimated

1.75 the U.S. was ~2.5 million housing

units below what is needed to

match long term demand, with an

1.50 annual rate of construction

~370,000 units below the level

required to meet demand

1.25

▪ Single family builders cite labor

shortages, profitability concerns,

1.00 and land economics/availability as

reasons for inability to meet full

demand and likely a long runway

0.75 of build potential

Minimum Housing Requirement Completions & Placements of New Units

▪ New SF home rental communities

0.50

looking to fill the gap

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Sources: Ducker Analysis, JCHS, Freddie Mac

CONFIDENTIAL -DUCKER HOLDINGS LLC 4Industry Insights Leading Up to COVID CRISIS

Multifamily has outperformed single-family for the last several years. Very strong start to 2020 pre COVID and opportunities will continue

long term, particularly in nonurban areas for low - and mid-rise projects (rental living increases relative to ownership)

S F, M F S TA R T S I N D E X E D , O O O s

300

250

200

150

Land mix

100 Labor shortage

Entry level segment

50

Great Recession

0

SF MF

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

CONFIDENTIAL -DUCKER HOLDINGS LLC 5Industry Insights Through COVID Crisis

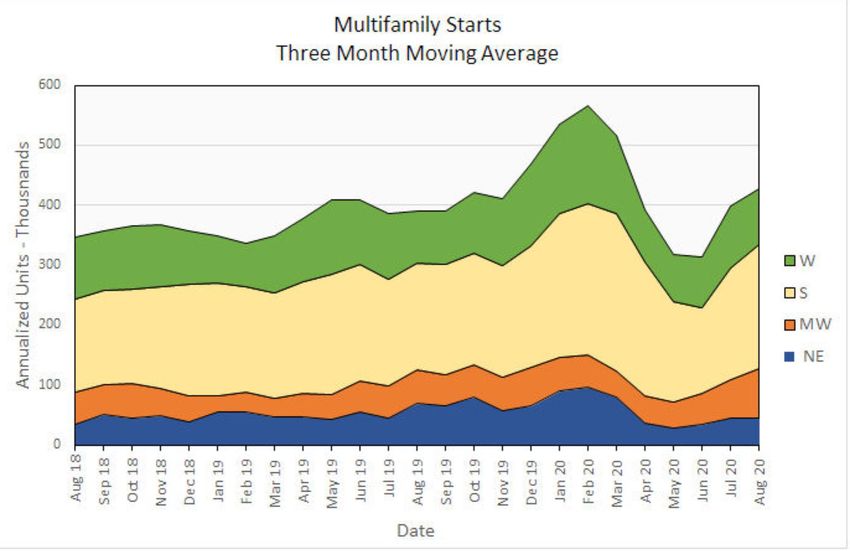

Multi-family has outperformed single family for the last several years but has Housing Starts 2019A 2020F change 2021F change

been more volatile through the COVID crisis. Single family to be the growth (‘000)

driver going forward, particularly in nonurban areas Single Family 888 938 +6% 1,047 +12%

120% 50% Multi-Family 402 410 +2% 349 -15%

100% 40%

Total Starts 1,290 1,348 +4% 1,395 +4%

80%

30%

60%

Existing Home Sales

20% ▪ Housing starts recovered rapidly after April-May collapse led by single

40% family activity

Starts

10%

20%

▪ Single family September YTD up 4 percent over prior year. Multi-family

0%

up 10 percent

0%

▪ Similar V curve for existing home sales which rose to a new 14 year

Jan Feb Mar Apr May Jun Jul Aug Sep

-20%

-10% high in September

▪ Home sales still 2% behind 2019 YTD

-40% -20%

▪ Activity still constrained by a lack of inventory but delayed selling

-60% -30% season - low interest rates and millennials coming to the market have

Single Family Starts Multi-Family Starts Total Starts Existing Home Sales fueled strong demand

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

CONFIDENTIAL -DUCKER HOLDINGS LLC 6Industry Insights Through COVID Crisis

• Retail building material expenditures have driven the growth in construction activity - significantly outpacing wholesale expenditures

• Price increases over the past year for most material categories, led by lumber and softwood lumber pricing

• Cost of new home builds increasing up to 20% from initial budgets

SEPTEMBER PRODUCER PRICE INDEX, 12 MONTH

Y E A R - O N - Y E A R C H A N G E I N C E N S U S B U I L D I N G M AT E R I A L

CHANGE

EXPENDITURES

20.0% Sep-20 PPP change vs. Sep-19

450 90%

400 81.2% 80%

15.0% Retail

change from Sep-19

YTD +10% 350 70%

300 60%

Sep-20 PPP

10.0% 52.4% 50%

250

Wholesale 40%

5.0% YTD +1% 200

28.4% 30%

150 20%

0.0% 100 10%

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20

50 5.5%

2.8% -0.1% 2.4% 0%

-5.0%

0 -10%

-10.0%

-15.0%

-20.0%

Retail Wholesale

*Structural, Architectural, Pre-Engineered Metal Products

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

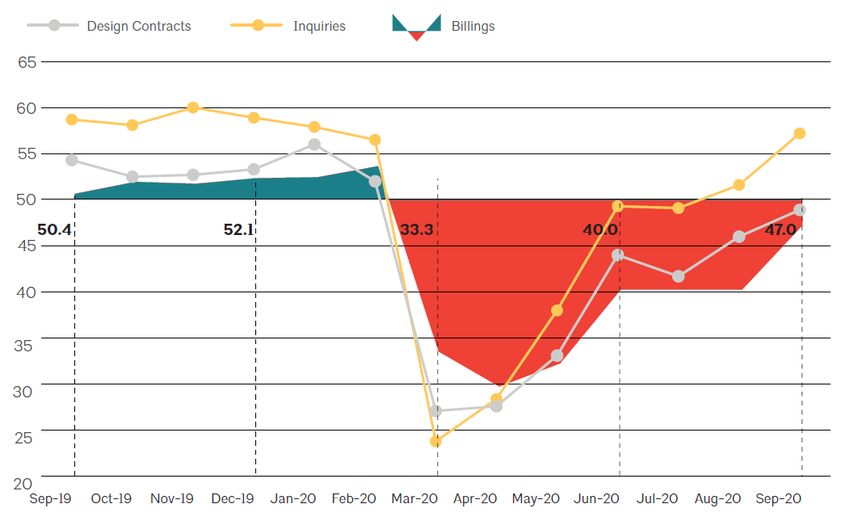

CONFIDENTIAL -DUCKER HOLDINGS LLC 7AIA Indicators and Recovery

A healthy, early indicator of future construction and major remodeling activity is the AIA/ABI Index on activities, inquiries and sentiment across the

architectural community. Data through September show improving conditions with a steady increase in inquiries.

ABI ACTIVITY TRACKING AIA SENTIMENT FOR SERVICES BY

BUILDING TYPE

• Since mid-May – inquiries increasing at significant rate for architectural and design services, both for new construction but also for built out and remodel

for post-covid environment – occupancy protection, management, densify/open plan etc.

• Contracts kept pace through early July - rebound after holiday vacation dip and slower processes to award work

• Broad categories of commercial and industrial had the biggest decline but also are seeing a V shaped recovery given scale of demand and opportunities

across many geographies and applications

Sources: Ducker, AIA

CONFIDENTIAL -DUCKER HOLDINGS LLC 8Industry Insights Post COVID

CONSTRUCTION ($) PIP FORECAST –

Residential - rapid recovery after spring drop. Single

OCTOBER 2020 SCENARIO FOR FUTURE family strength with low interest rates and new market

(POST-COVID) OPTIMISTIC entrants unleashing short-term pent-up demand.

Flattening over next 2 years with lagged impact of

ABI ACTIVITY TRACKING Healthy Q1 2020

SF AND MF rapid

severe economic downturn dampening continued

$700,000 recovery post increase in existing home sales.

COVID

$600,000

Nonresidential - greater negative impact and declines

$500,000 for a period depending on suburban growth, vaccine.

Healthcare and services offer unique opportunities of

$400,000

demand.

$300,000

The long-term growth of infrastructure will pause until

Infrastructure OPEX

typically outperforms Federal stimulus kicks in. Some tail of activity will

$200,000

CAPEX continue due to recent bonds passage and multi-year

funded projects. Future local government balance

$100,000

sheets likely to be strained – tax revenues down,

reducing project spend and a lag period of impact. OPEX

$0 likely to outperform CAPEX.

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020F 2021F 2022F 2023F

Residential Nonresidential Building Nonbuilding

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

CONFIDENTIAL -DUCKER HOLDINGS LLC 9Industry Insights Post COVID – Forecast Scenarios

CONSTRUCTION ($) PIP FORECAST – APRIL 2020 SCENARIO FOR FUTURE (POST COVID)

All scenarios show an overall decline but with different projections for each segment. Residential housing impact very different to previous recession and shorter

and less severe than originally forecasted. Non-residential building hardest hit and recovery likely to be delayed for 2 to 3 years. Nonresidential building

dependent on future government policy.

DOWNSIDE - POST COVID PIP $,000 BASE CASE - POST COVID PIP $,000 UPSIDE - POST COVID PIP $,000

$700,000 $700,000 $700,000

$600,000 $600,000 $600,000

$500,000 $500,000 $500,000

$400,000 $400,000 $400,000

$300,000 $300,000 $300,000

$200,000 $200,000 $200,000

$100,000 $100,000 $100,000

$0 $0 $0

Residential Nonresidential Building Residential Nonresidential Building Residential Nonresidential Building

Nonbuilding Construction Nonbuilding Construction Nonbuilding Construction

2019-2023 2019-2023 2019-2023

CAGR CAGR CAGR

Residential Building 0.9% Residential Building 2.1% Residential Building 3.9%

Nonresidential Building -5.6% Nonresidential Building -4.4% Nonresidential Building -2.3%

Nonbuilding Construction 0.0% Nonbuilding Construction 0.9% Nonbuilding Construction 2.1%

Total PIP Construction -1.5% Total PIP Construction -0.3% Total PIP Construction 1.4%

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

CONFIDENTIAL -DUCKER HOLDINGS LLC 10Five Key Factors Representing New Norm in Construction

The COVID crisis has shifted practices, housing preferences and regional construction dynamics offering new opportunities with new strategies and business

models.

POST VIRUS SOCIETY DRIVES A NEW NORM IN CONSTRUCTION

• Severe shock to society drives conservancy in spending, balance sheet and affordability

1 • Refocus on what’s most important to protect, maintain business and living

• Building owner and homeowners focus on home improvement and “quality of home”

2 • Accelerating digitalization in each stage of design and construction process

• Governments upgrading communications, digital competencies

• Network bandwidth expansion for infrastructure across public, private data demand

• Purposeful, disciplined construction process that favors longer cycles, prefab construction

3 • Decrease in open plan environments, increase in private spaces (social distance friendly)

• Increased square footage in demand, value trade-off against premium finishes

• Increase in storage, warehousing and multi-function areas

• Healthcare facilities upgrade, retrofit and build out

4 • Expanding distribution and last-mile storage/delivery

• Finally addressing infrastructure needs – road and communications investments

5 • Growth of lower density construction areas – suburban, rural in demand

• More renting- rental communities with homes, single payment will thrive

• Luxury and Custom construction/remodel to lead the rebound in 2021

• Bump to existing home sales and remodeling outside of large urban areas

Sources: Census, NAHB, AIA, FRED, CBRE, HUD, NAR, Ducker Interviews and Expertise

CONFIDENTIAL -DUCKER HOLDINGS LLC 11Residential Construction COVID Developments

Business Profitability

01 • Profitability of select producers and suppliers far better through the crisis than forecasted – some note record quarterly performance

• Financials lifted through improving demand, lower SG&A costs and ability to sell out inventories

• Lower cost of sales with favorable input prices helped several sectors outperform adjusted forecast or YOY targets

Significant Pricing Dynamics

02 •

•

Import challenges increase domestic source demand and improve average pricing through the channel

Lumber price appreciation significant- negative impact to framing and new housing costs

• Resin/plastic price favorability leading contributing to improved cost basis and better margins - remodeling

• Many sectors launching price increases for early 2021 - ranging from 4-9% upside

Big Box Retail Performance

03 • Essential business status led to significant store traffic and purchases by DIY and DIFM

• Transition from renter to home-buyer increased variety of interior project/décor spend

• New digital programs by Lowes and Home Depot – and healthy inventory attracted professionals

Continued home remodeling, outdoor and exteriors pent up demand

• COVID themes and risks driving more outdoor living, family and pet friendly environments

04 • Migration from apartment living to existing single-family increasing upgrades and improvements

• Long lead times for windows, siding, fencing, decking will create pent-up demand through Q2 2021 as industry works to balance new

construction growth and remodeling demand

CONFIDENTIAL -DUCKER HOLDINGS LLC 12Nonresidential COVID Related Developments

Nonresidential Backlog Delayed Office Vacancy Decline

While nonresidential, new construction reached Federal and state stimulus helped businesses

peak in late 2019, starts in Q4 allowed progress complete lease payments through the early COVID

on backlog through Q3 2020 –however, future crisis. Some businesses returning. Full affect of

activity likely to slow with completion of backlog office vacancy and lease levels yet to be

and reduction in permits/starts. experienced with many implementing office layout

improvements or posting return to office in H2

2021.

Building Stock MRO and Reset REIT $ Shift to Detached Rental Housing

Aging nonresidential building stock still With pressures on nonresidential lease rates,

represents a significant opportunity for the vacancy levels and new construction projects,

industry. Planned expenditures and major more REIT development and investment moving

improvements paused in April/May but resumed funds to address trend in large single-family rental

in June with many MRO participants. Interiors communities. New partnerships and ventures

redesign post-COVID to enclosed workspaces forming with REIT players and independent

represent new opportunities for occupancy builder/developer - new trend to watch in 2021.

safety, health and design.

CONFIDENTIAL -DUCKER HOLDINGS LLC 13Industry Developments Our Experts are Watching for in 2021

For a more comprehensive analysis of these developments, please look for Ducker’s 2021 Industry Outlook and Key Opportunity/Risk

Analysis for the US construction industry coming in early 2021

CONFIDENTIAL -DUCKER HOLDINGS LLC 14USG Post COVID Opportunities

D U C K E R ’ S W O R K A C R O S S T H E C O R P O R AT E A N D P R I VAT E E Q U I T Y S P E C T R U M Y I E L D I M P O R TA N T N E W D I S C I P L I N E S

AND AREAS OF FOCUS FOR BEST -IN-CLASS BUILDING PRODUCT BUSINESSES FOR POST COVID SUCCESS.

BNC CORPORATE STRATEGY FOCUS

Portfolio and Digital Channel Pricing Audits and

Adjacency Profile

Market Mix and UX Experience Program

and Pursuit

Optimization Update Optimization

Innovation: Modular Systems

Product, Service, and Design-to-

Business Model Install Programs

CONFIDENTIAL -DUCKER HOLDINGS LLC 15RESEARCH & CONSULTING THIS CONCLUDES OUR PRESENTATION. THANK YOU. Today’s presentation was prepared by Ducker Research and Consulting/Ducker Holdings LLC. To the fullest extent permissible by applicable law, all information contained herein is for informational purposes only and is provided “AS IS”. The information is provided (i) with no guaranty of BANGALORE | BERLIN | DETROIT | LONDON | NEW YORK | PARIS | SHANGHAI accuracy, completeness, timeliness or that any defects will be corrected and (ii) without any representations, warranties or other contractual terms of any kind including, without limitation, warranties of title, merchantability or fitness for a particular purpose. Even if Ducker was advised, knew www.ducker.com or should have known that claims or damages could arise from the use, misuse or delay of use of the information, Ducker assumes no legal liability for any direct, indirect, consequential, special, punitive or similar claims or damages. The information contained herein does not represent financial, legal, regulatory or other advice and recommendations from Ducker. Any use of the information is undertaken at your sole risk.

You can also read