Worldwide Enterprise Social Networks and Online Communities 2015-2019 Forecast and 2014 Vendor Shares - Toolbox.com

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MARKET ANALYSIS

Worldwide Enterprise Social Networks and Online

Communities 2015–2019 Forecast and 2014 Vendor Shares

Vanessa Thompson

IDC OPINION

The market for enterprise social networks (ESNs) evolved significantly in 2014. There is an increasing

presence of social workflow capabilities being surfaced inside business applications, but at the same

time, online communities to support customers, employees, partners, and suppliers are growing

rapidly. IDC expects the market for both standalone and embedded ESNs to continue to slow

significantly as many more enterprise applications become social in nature. However, the market for

online communities is growing rapidly. Toward the end of the forecast period, enterprise social

networks may not even be called out as a separate market. In addition:

IDC expects the worldwide enterprise social networks market revenue to grow from $1.46

billion in 2014 to $3.5 billion by 2019, representing a compound annual growth rate (CAGR) of

19.1%.

IDC expects the worldwide online communities market revenue to grow from $392.95 million in

2014 to $1.2 billion by 2019, representing a CAGR of 24.3%.

Connecting to customers, employees, partners, and suppliers has always been a mission-

critical activity. Alongside rapidly shifting expectations, communities have become a broker

between business networks and will only continue to contribute more value to organizations

trying to develop ongoing relationships.

July 2015, IDC #257492

IN THIS STUDY

This study examines the enterprise social networks market for the period from 2010 to 2019, with

vendor revenue trends and market growth forecasts. Worldwide market sizing is provided for 2014,

with trends from 2013. A five-year growth forecast for this market is shown for 2015–2019. Revenue

and market share of the leading vendors in both enterprise social networks and online communities

are provided for 2014.

Methodology

See the Methodology in the Learn More section for a description of the forecasting and analysis

methodology employed in this study.

In addition, please note the following:

The information contained in this study was derived from IDC's Worldwide Semiannual

Software Tracker database as of June 8, 2015.

All numbers in this document may not be exact due to rounding.

For more information on IDC's software definitions and methodology, see IDC's Software

Taxonomy, 2015 (IDC #256767, June 2015).

Enterprise Social Networks Market Definition

Enterprise social networks (ESNs) enable social workflow capabilities to be delivered to users that are

either inside or outside an organization's firewall. Users in non-customer-facing roles are the focus of

these solutions, but customer-facing interactions may also occur. Solution capabilities of enterprise

social networks should include, but are not limited to, activity streams, blogs, wikis, microblogging,

discussion forums, groups (public or private), ideas, profiles, recommendation engines (people,

content, or objects), tagging, bookmarking, and secure communities. An ESN provides a social

workflow or relationship layer in a business that can be an independent or a standalone solution and/or

a set of service-oriented APIs or integrated applications that coexist with other business and

communications applications. Vendors tracked in the enterprise social networks market can offer

discrete solutions supporting one type of social functionality (such as community management,

ideation, or innovation management) or a broad-based platform that encompasses many functionality

traits. A variety of deployment options (on-premises, software as a service [SaaS], hosted application

management, or software appliance) are made available.

Online communities is a subsegment of the enterprise social networks market and includes all online

communities.

Communities enable the collection and incorporation of user-generated feedback (content can include

files and rich media) and may also include capabilities such as blogs, discussion forums, profiles,

tagging, comments, and ratings/ranking. Communities operate on owned digital properties and can be

customer, employee, or partner/supplier based and serve a specific member/community-based

organization. Solutions may also enable aggregation of external social data sources into owned sites

though social log-in, social plug-ins (including proprietary connectors, Web services, or iFrames).

The communities market definition excludes:

©2015 IDC #257492 2

Social analytics functionality included in any of the CRM segments of sales automation,

marketing automation, customer service, or contact center.

Social media publishing capabilities; this also includes social media ad placement.

SITUATION OVERVIEW

The Worldwide Enterprise Social Networks Market in 2014

ESNs continue to become common place in the modern enterprise. Throughout 2014, there was

significant repositioning of the major ESN vendors. IBM continues to focus on IBM Connections as it

supports IBM Verse, the company's new email product. Jive Software has created a focus on

workstyles with a range of new products focused on individual productivity, from calendaring through to

mobile application messaging with Jive Chime. Microsoft is hastily increasing the capabilities and

scope of Office 365 that also includes Yammer, and the focus on Office 365 APIs is encouraging

where other business applications can be connected to the suite. Salesforce.com is aggressively

pushing the Community Cloud, and Chatter is now accounted for as part of the salesforce.com

platform business. Finally, Lithium Technologies is well placed to IPO in the coming year as its

customer base is maturing well.

Performance of Leading Vendors in 2014

Table 1 and Figure 1 display 2012–2014 worldwide revenue and 2014 growth and market share for

enterprise social networks vendors. Year-over-year (YoY) growth for almost all vendors in the market

was in double digits. The continued growth of salesforce.com is on the back of the change in

positioning of Chatter to become a more horizontal support layer to Salesforce1, alongside the addition

of the Community Cloud offerings for sales, marketing, and partner communities.

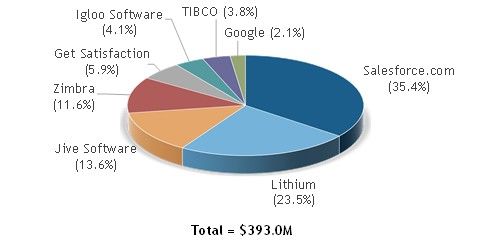

Table 2 and Figure 2 display 2012–2014 worldwide revenue and 2014 growth and market share for

online communities vendors. Online communities is a subsegment of the enterprise social networks

market and in its most basic form refers to a Web-based destination where people can connect, find

resources, and discuss issues around an industry, an organization, a product, or a set of values.

©2015 IDC #257492 3

TABLE 1

Worldwide Enterprise Social Networks Revenue by Vendor, 2012–2014 ($M)

2013–2014

2012 2013 2014 2014 Share (%) Growth (%)

IBM 142.7 172.7 185.5 12.7 7.4

Jive Software 102.3 130.5 162.2 11.1 24.3

Salesforce.com 29.6 91.2 161.6 11.1 77.2

Microsoft 44.0 76.0 97.2 6.7 27.9

Lithium 52.5 81.5 92.3 6.3 13.2

Zimbra 39.1 47.9 65.3 4.5 36.4

SAP 10.9 34.1 47.1 3.2 38.2

Socialtext 34.6 34.8 35.2 2.4 1.4

Mindjet 17.6 18.6 23.1 1.6 23.9

Get Satisfaction 14.9 18.5 23.0 1.6 24.4

INgage Networks 15.7 17.5 20.6 1.4 18.2

Google – 10.9 16.6 1.1 52.7

Igloo Software 10.4 13.5 16.0 1.1 18.0

TIBCO 10.0 12.2 14.9 1.0 22.2

Zyncro 5.7 9.5 12.6 0.9 32.9

ATOS 7.9 8.6 8.6 0.6 0.1

VMware 4.7 6.6 8.0 0.5 21.7

Cisco 2.0 1.4 1.6 0.1 18.0

TOTVS – 0.1 0.2 0.0 204.6

Subtotal 544.9 785.8 991.6 67.9 26.2

Other 414.1 491.3 468.1 32.1 -4.7

Total 959.0 1,277.1 1,459.7 100.0 14.3

Source: IDC, June 2015

©2015 IDC #257492 4FIGURE 1

Worldwide Enterprise Social Networks Revenue Share by Vendor, 2014

Source: IDC, June 2015

TABLE 2

Worldwide Online Communities Revenue by Vendor, 2012–2014 ($M)

2013–2014

2012 2013 2014 2014 Share (%) Growth (%)

Salesforce.com 29.6 64.8 139.3 35.4 114.8

Lithium 52.5 81.5 92.3 23.5 13.2

Jive Software 26.6 37.8 53.5 13.6 41.5

Zimbra 27.4 33.5 45.7 11.6 36.4

Get Satisfaction 14.9 18.5 23.0 5.9 24.4

Igloo Software 10.4 13.5 16.0 4.1 18.0

TIBCO 10.0 12.2 14.9 3.8 22.2

Google – 5.4 8.3 2.1 52.7

Total 171.4 267.3 393.0 100.0 47.0

Source: IDC, June 2015

©2015 IDC #257492 5FIGURE 2 Worldwide Online Communities Revenue Share by Vendor, 2014 Source: IDC, June 2015 Performance by Geographic Region in 2014 North America makes up the lion's share of revenue in the enterprise social networks market. However, EMEA (Western Europe and CEMA) experienced good growth through 2014, in line with the deployment of cloud-based services in the region. Asia/Pacific (including Japan) (APJ) still represents a small portion of revenue in enterprise social networks as the market is still immature in relation to North America (see Figure 3). FIGURE 3 Worldwide Enterprise Social Networks Revenue Share by Region, 2014 Source: IDC, June 2015 ©2015 IDC #257492 6

FUTURE OUTLOOK

Forecast and Assumptions

The following factors are likely to drive revenue growth in enterprise social networks and online

communities during the forecast period:

Communicating with customers rather than just responding has become a business focus.

This shift signifies that organizations are wanting to drive more awareness of their brand as

well as have an ongoing conversation with customers. This is particularly suited to online

communities where brands can quickly build a trust relationship with customers, employees,

partners, and suppliers.

Social workflow is at the core of how companies can create competitive differentiation and

advantage, but it is far from simply implementing some new software/hardware and

automating processes. It should be inherent in how companies do business, with technology

being the enabler.

The rapidly changing nature of work means that the role of social workflow will become

increasingly important to enable users to get their work done wherever they choose to work.

Business decisions will be made via new outputs (likely mobile based) that integrate analytics

and data with people and systems.

There is an opportunity for online communities to become marketplaces of their own where

partners and suppliers are able to start transacting in the community to help solve other

customer or partner questions.

The following factors are likely to inhibit revenue growth in enterprise social networks during the

forecast period:

The level of deployment of enterprise social networks (the Americas region in particular)

indicates that many organizations have already deployed solutions, and the incremental

increase in revenue for standalone solutions will be nominal.

The IT department will be increasingly involved in deployment and integration to ensure social

solutions meet enterprise requirements for security, compliance, and IP protection.

Worldwide Enterprise Social Networks and Online Communities Forecast,

2015–2019

IDC's estimate of growth of the enterprise social networks and online communities markets through

2019 is presented in Table 3. The enterprise social networks market is expected to reach $3.5 billion

by 2019 at a CAGR of 19.1%. The online communities market is expected to reach $1.2 billion by 2019

at a CAGR of 24.3%.

IDC analysts around the globe supplied regional input and insight into the enterprise social networks

forecast. The worldwide forecast is the aggregation of this regional data. The forecast is for the

Americas region to retain a good growth rate throughout the forecast period, although EMEA and APJ

are expected to grow more aggressively. To date, the Americas region represents a disproportionately

high share of revenue, as the EMEA and Asia/Pacific (including Japan) regions can expect a longer

time frame for change with respect to standalone enterprise social networks and may transition directly

to embedded applications as more enterprise applications assume social workflow. Table 4 shows the

regional share breakdown for 2014 and 2019 and revenue forecast for 2014–2019. Figure 4 shows the

regional revenue data for 2014 and 2019 in graphical form.

©2015 IDC #257492 7TABLE 3

Worldwide Enterprise Social Networks and Online Communities Revenue,

2014–2019 ($M)

2014–2019

2014 2015 2016 2017 2018 2019 CAGR (%)

Enterprise social networks 1,459.7 1,707.2 2,031.7 2,422.3 2,898.4 3,498.7 19.1

Growth (%) 14.3 17.0 19.0 19.2 19.7 20.7

Online communities 393.0 477.7 590.7 736.5 925.5 1,167.2 24.3

Growth (%) 47.0 21.6 23.6 24.7 25.7 26.1

Note: See Table 5 for top 3 assumptions and Table 6 for key forecast assumptions.

Source: IDC, June 2015

TABLE 4

Worldwide Enterprise Social Networks Revenue by Region, 2014–2019 ($M)

2014 2019

Share 2014–2019 Share

2014 2015 2016 2017 2018 2019 (%) CAGR (%) (%)

North America 1,046.3 1,138.4 1,245.3 1,347.8 1,452.4 1,550.5 71.7 8.2 44.3

EMEA 346.4 493.9 702.4 979.9 1,339.8 1,829.4 23.7 39.5 52.3

APJ 67.0 74.9 84.0 94.6 106.3 118.7 4.6 12.1 3.4

Total 1,459.7 1,707.2 2,031.7 2,422.3 2,898.4 3,498.7 100.0 19.1 100.0

Note: See Table 5 for top 3 assumptions and Table 6 for key forecast assumptions.

Source: IDC, June 2015

©2015 IDC #257492 8FIGURE 4 Worldwide Enterprise Social Networks Revenue by Region, 2014 and 2019 Source: IDC, June 2015 Assumptions Table 5 shows the top 3 assumptions for the enterprise social networks market, and Table 6 shows the key forecast assumptions underlying this forecast. ©2015 IDC #257492 9

TABLE 5

Top 3 Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Changes to This

Assumption That Could

Market Force IDC Assumption Significance Affect Current Forecast Comments

Economy Economic A down economy The forecast assumes At present, the fallout

performance has been affects business and that the benefits of from global hot spots

mixed in 2015. Low oil consumer confidence, lower, and stable, remains contained. It

prices have boosted the availability of energy prices will assist would require a

confidence in energy- credit and private growth, and therefore significant and

importing countries investment, and IT spending, in both material geopolitical

like India, and Western internal funding. A industrialized and crisis to have a

Europe has continued global recession developing economies, worldwide price

to show moderate would cause without triggering a erosion on the overall

improvements (despite businesses to delay spike in interest rates. ICT market.

continued uncertainty IT upgrades and Slower growth in China

over Grexit). On the some new projects; a is manageable at

other hand, rising economy does present levels but could

momentum has the opposite. A crisis drag down global GDP

slowed in China and (perhaps triggered by growth should the

Japan, while the U.S. more volatility in situation worsen.

economy was weaker emerging markets)

in the first quarter. We could create a chain

assume that the of events that would

United States will drive tech spending

improve in the second much lower in the

half of the year and near term.

that China will use

policy to stabilize

growth at around 7%.

But with Russia and

Latin America

stuttering, the global

economy will grow by

less than 3%.

©2015 IDC #257492 10TABLE 5

Top 3 Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Changes to This

Assumption That Could

Market Force IDC Assumption Significance Affect Current Forecast Comments

Enterprise The need to support Collaboration and Upside: Over-the-top It is no longer good

decision making ad hoc decisions personal productivity mobile application enough to just offer

becomes increasingly are rapidly changing, messaging will become APIs to extend existing

critical. Companies will and new features are coupled with ad hoc business processes.

look to native being defined and decision making. The user interface and

collaboration incorporated to meet usability workflow

Downside: Business

applications and other emerging business aspects must also be

processes that are rigid

lightweight SaaS- needs. streamlined so that

in nature will require

based and mobile users have the same

additional user

collaboration tools to experience across any

interaction. This means

support other business device.

that the information to

decisions.

decision process will

take longer.

User centricity Consumerization of Initiatives from Upside: Increasing User expectations will

the enterprise vendors to launch business pressures and continue to change

continues with social workflow the change in user rapidly, but often this

consumer devices and features as a workstyles have is not in step with the

Web applications complement to created the opportunity enterprise IT buying

brought into the existing collaboration to build and architect cycle, so organizations

workplace as well as applications and applications and will need to become

vendors positioning business workflow will processes directly from more agile and deliver

products/solutions to continue. For user behavior rather experiences to users

increasingly suit user instance, content than delivering mobile that they expect

needs, not IT. repositories and versions of current outside of the work

enterprise social enterprise business context.

networks will become applications.

accessible from inside

Downside: Many

other applications. A

organizations do not

number of enterprise

yet have clarity around

social software

an enterprise mobility

vendors have

strategy and are

launched mobile OS

investing in both mobile

SDKs in support of

device management

this trend.

and mobile application

management. This

creates a significant

spending increase to

manage both devices

and applications.

Source: IDC, June 2015

©2015 IDC #257492 11TABLE 6

Key Forecast Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Macroeconomics

Economy Economic performance has High. A down economy affects

been mixed in 2015. Low oil business and consumer

prices have boosted confidence confidence, the availability of

in energy-importing countries credit and private investment,

like India, and Western Europe and internal funding. A global

has continued to show recession would cause

moderate improvements businesses to delay IT

(despite continued uncertainty upgrades and some new

over Grexit). On the other hand, projects; a rising economy does

momentum has slowed in the opposite. A crisis (perhaps

China and Japan, while the triggered by more volatility in

U.S. economy was weaker in emerging markets) could create

the first quarter. We assume a chain of events that would

that the United States will drive tech spending much lower

improve in the second half of in the near term.

the year and that China will use

policy to stabilize growth at

around 7%. But with Russia

and Latin America stuttering,

the global economy will grow by

less than 3%.

Crisis duration/ Although there is increased High. A crisis in economic

potential relapse uncertainty surrounding the confidence will shake IT

future of Greece in the spending to the core within a

eurozone, the overall European short time frame, as observed

economy appears less likely to in 2009. With modular IT

relapse into crisis than a year spending dominating IT buyer

ago. A debt crisis is possible in strategy, businesses stand

China as the economy ready to delay or postpone

continues to grapple with the capital spending and new

overhand of its response to the projects. On the flip side, this

financial crisis, but we currently creates pent-up demand,

assume that the government especially in emerging markets.

has enough firepower in its

policy arsenal to avert the

worst-case scenarios.

©2015 IDC #257492 12TABLE 6

Key Forecast Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Vertical industries The main drag on IT spending High. A downturn in major

is from the public sector, with contributors to IT revenue (e.g.,

government spending cuts in the financial services sector)

the United States and austerity can have a major impact on IT

measures in most of Europe. spending. Momentum in vertical

Dynamic industries include sectors (e.g., healthcare) can

healthcare, which continues its drive overall IT spending.

pace of modernization to deal Industry-specific solutions are

with aging populations in increasingly a major contributor

mature economies, and the to growth.

services sector. Manufacturing

firms are investing to improve

their global competitiveness,

while telecom operators are

engaged in customer retention

efforts. Industry-specific

solutions will be a major driver

for IT spending.

©2015 IDC #257492 13TABLE 6

Key Forecast Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Global

megatrends

Cloud Cloud is a new paradigm of High. The key advantage to

computing that will shape IT cloud services should be the

spending over the next several ability of IT organizations to

decades — the logical evolution shift IT resources from

of what IDC called "dynamic IT" maintenance to new initiatives.

for years. It entails shared This in turn could lead to new

access to virtualized resources business revenue and

over the Internet. IDC estimates competitiveness as well as

that cloud services spending create new opportunities for IT

will continue to grow at double- vendors in SMB and emerging

digit rates for the next few markets. The benefits will be

years, gradually accounting for offset by cannibalization in the

a larger proportion of all IT short term though, resulting in

spending. In the short term and shorter service engagements,

the medium term, this will have price model disruption, and

a negative impact on IT some hardware

spending, enabling end users commoditization. A stronger

to lower their overall spending economy would see most

on certain solutions. However, organizations shift resources to

in the long term, we believe that new IT development and

cloud will have a positive adoption areas in the long term.

overall impact on industry We see cloud adoption as an IT

growth as more users adopt spending driver overall, despite

more advanced computing these cannibalization effects in

solutions at a faster rate. the next few years.

©2015 IDC #257492 14TABLE 6

Key Forecast Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

The digital The impact of the new digital Moderate. Look for faster

marketplace marketplace can be seen in development of the software-

software as a service, the as-a-service model, more

integration of Internet and development of composite

enterprise search and other applications, and more directly

functionality, the concept of competitive products (e.g.,

"cloud computing," and social network application

competition for ad revenue platforms). Also look for rapid

among Microsoft, Google, and growth of Internet advertising

other vendors. The digital revenue in emerging

marketplace will affect content geographies.

delivery, commerce, datacenter

architectures, advertising,

marketing, telecommunications,

and social interactions. It may

also accelerate the

consumption of ICT in

emerging geographies, where

more and more online

populations reside.

Internet of Things The Internet of Things refers to High. The addition of billions of

the proliferation of client devices to the network edge will

devices and end-user or end- drive the need for more

use devices at the network enterprise systems to deploy,

edge. These other devices manage, and make use of

range from smartphones and these devices. It will also shift

networked entertainment the prevailing traffic from the

devices to automobiles, center of the network outward

building automation systems, to edge inward, which will affect

smart meters and thermostats, computing and communications

medical electronics, and architectures.

industrial controllers, not to

mention RFID tags and

sensors. Communicating client

devices will proliferate at 5–10

times the rate of PCs installed.

Devices will both converge

(smartphones with more

functionality) and diverge

(single-use devices, such as

RFID readers and industry-

specific devices).

©2015 IDC #257492 15TABLE 6

Key Forecast Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Specific market

trends

Converged Conferencing and messaging Moderate. Convergence will

modality are becoming more of a drive new competitive

multimodal experience and are dynamics, offer new

being built into social workflow applications and functions to

to meet the needs of the new customers. Applications that

enterprise workspace. have the embedded video

capability enable users to do

different tasks within the same

application.

Enterprise decision The need to support ad hoc Moderate. Collaboration and

making decisions becomes increasingly personal productivity are rapidly

critical. Companies will look to changing, and new features are

native collaboration being defined and incorporated

applications and other to meet emerging business

lightweight SaaS-based and needs.

mobile collaboration tools to

support other business

decisions.

User centricity Consumerization of the High. Initiatives from vendors

enterprise continues with to launch social workflow

consumer devices and Web features as a complement to

applications brought into the existing collaboration

workplace as well as vendors applications and business

positioning products/solutions workflow will continue. For

to increasingly suit user needs, instance, content repositories

not IT. and enterprise social networks

will become accessible from

inside other applications. A

number of enterprise social

software vendors have

launched mobile OS SDKs in

support of this trend.

©2015 IDC #257492 16TABLE 6

Key Forecast Assumptions for the Worldwide Enterprise Social Networks and

Online Communities Market, 2015–2019

Accelerator/

Inhibitor/ Certainty of

Market Force IDC Assumption Impact Neutral Assumption

Consumption

Buying sentiment Buying sentiment has High. Buyer sentiment

fluctuated in recent months, in obviously has a major direct

line with stock markets and impact on IT spending.

macroeconomic events/risk Confidence can be volatile from

factors. In the past 12 months, month to month, however, and

CIOs have consistently CIOs have often misjudged

underforecast their own IT their own IT spending. The

spending, reflecting the decentralization of IT budgets

persistent air of caution and risk makes it more difficult to rely on

aversion. If the economy individual polls of buyer intent

remains stable, spending will in order to accurately judge

likely outpace buyer sentiment sentiment. Underlying

polls. If the economy enters sentiment is usually higher than

another downturn, buyer surveys indicate.

confidence could plunge

quickly.

Legend: very low, low, moderate, high, very high

Source: IDC, June 2015

Market Context

A five-year forecast update (2014–2018) was last published for the enterprise social networks market in

Worldwide Enterprise Social Networks 2014–2018 Forecast and 2013 Vendor Shares (IDC #249846,

July 2014). Table 7 compares the forecast published in the previous document with the current

forecast in terms of regional revenue and worldwide annual growth rates. Historical data (2010–2014)

is also included in Table 7 for comparison purposes. Figure 5 displays the same data in graphical form.

IDC expects revenue of standalone enterprise social networks to slow significantly, particularly in the

Americas region, compared with the previous forecast. This is aligned to the social workflow processes

that are enabled by activity streams and the nature of interactions this generates inside organizations.

As the nature of communications in business changes because of the impact of online social

interactions, these new dynamics create an increased level of automation in decision support systems

through ad hoc workflows and increasing urgency from businesses looking to capture market

opportunities created by these new dynamics. This means that the processes inherent in enterprise

social networks, primarily activity streams, messaging, and document repositories, will become

embedded in other applications rather than being provided by standalone applications and move out

into online communities.

©2015 IDC #257492 17TABLE 7

Worldwide Enterprise Social Networks Revenue, 2010–2019: Comparison of

July 2014 and July 2015 Forecasts ($M)

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

July 2015 forecast 569.8 806.8 959.0 1,277.1 1,459.7 1,707.2 2,031.7 2,422.3 2,898.4 3,498.7

Growth (%) NA 41.6 18.9 33.2 14.3 17.0 19.0 19.2 19.7 20.7

July 2014 forecast 569.8 806.8 967.9 1,242.0 1,540.9 1,907.0 2,345.4 2,870.4 3,509.4 NA

Growth (%) 33.7 41.6 20.0 28.3 24.1 23.8 23.0 22.4 22.3 NA

Notes:

See Worldwide Enterprise Social Networks 2014–2018 Forecast and 2013 Vendor Shares (IDC #249846, July 2014) for prior

forecast.

Historical market values presented here are as published in prior IDC documents based on the market taxonomies and current

U.S. dollar exchange rates existing at the time the data was originally published. For more details, see the Methodology in the

Learn More section.

Source: IDC, June 2015

FIGURE 5

Worldwide Enterprise Social Networks Revenue, 2010–2019: Comparison of

July 2014 and July 2015 Forecasts

Source: IDC, June 2015

©2015 IDC #257492 18ESSENTIAL GUIDANCE

IDC expects the deployment of standalone enterprise social networks to continue to slow. However,

the uptake in online communities is encouraging. Over time, enterprise social networks will become

part of the business platform, and vendors like salesforce.com already work in this way. Toward the

end of the forecast period, there will be increasing focus on self-service interactions where

communities become a powerful business tool to support existing business interactions with

customers, employees, partners, and suppliers. In addition:

Online communities will become a place of interaction as well as transaction. As businesses

look beyond customer support as a way to engage users in the community, there are many

opportunities in delivering a comprehensive business platform that can connect to other

business functions. By connecting components of the business and supplier network that may

collaborate through disconnected but shared processes, organizations can start to build an

experience that transcends existing business relationships.

Capturing influence, relevance, and expertise across a business or community remains a

complex challenge. As organizations look to target future potential touch points of customers

and partners, it will be essential to deliver context to these touch points with quick reference to

relevant expertise across all business stakeholders.

To enable the core features of enterprise social networks to be surfaced inside enterprise

workflow, open APIs need to be provided to enable information assets to become productized,

syndicated, and distributed as callable IP assets via an API. Streamlined user interface

connectivity also needs to be included to deliver seamless user connectivity between apps.

LEARN MORE

Related Research

Worldwide Collaborative Applications Market Shares, 2014: Year of the Empowered Worker

(IDC #256775, June 2015)

Worldwide Collaborative Applications Forecast, 2015–2019 (IDC #256756, June 2015)

Lithium LiNC '15: Moving Toward IPO (IDC #lcUS25713215, June 2015)

Microsoft Office 365 — In Full Force (IDC #lcUS25635315, May 2015)

Salesforce in 2020 (IDC #254171, February 2015)

Worldwide Enterprise Social Networks 2014–2018 Forecast and 2013 Vendor Shares (IDC

#249846, July 2014)

Methodology

Historical Market Values and Exchange Rates

Historical market values presented here are as published in prior IDC documents based on the market

taxonomies and current U.S. dollar exchange rates existing at the time the data was originally

published. For markets other than the United States, these as-published values are therefore based on

a different exchange rate each year.

Because many individual countries contribute to regional totals, it is difficult to give precise differences

between current and constant currency values in this document. However, the scale of the difference

can be understood from the movement of the U.S. dollar against major regional currencies. Customers

©2015 IDC #257492 19should consider multiplying regional historical market values for each year by the change in value of

the U.S. dollar against representative currencies in the region as shown in Table 8. This will provide a

better approximation of local market growth. For example, to restate 2012 eurozone values into 2014

dollars, one would adjust the 2012 value upward by 3% (because the dollar weakened slightly against

the euro between 2012 and 2014).

Please refer to IDC's regional research studies containing historical forecasts for multiple countries for

more accurate regional growth in local currencies. Note that this discussion applies only to historical

values prior to 2014. 2014 and all future years are forecast at a constant exchange rate.

TABLE 8

Exchange Rates, 2006–2014 (%)

2006 2007 2008 2009 2010 2011 2012 2013 2014

Euro 106 97 91 95 100 95 103 100 100

Pound 89 82 90 106 107 103 104 105 100

Yen 110 111 98 88 83 75 75 92 100

Canadian dollar 103 97 97 103 93 90 91 93 100

Mexico peso 82 82 84 102 95 94 99 96 100

Brazilian real 93 83 78 85 75 71 83 92 100

Note: To restate prior-year U.S. dollars, multiply historical market values by the percentage indicated in the table.

Source: IDC, January 2015

Synopsis

This IDC study examines vendor revenue performance in the enterprise social networks market for

2012–2014 and presents a forecast of the market for 2015–2019. It also includes vendor revenue share

and forecast data in the same periods for the online communities segment of the enterprise social

networks market.

"The nature of business interactions is moving toward ongoing communication and building

relationships and away from prescriptive and responsive interactions," says Vanessa Thompson,

research director for IDC's Enterprise Social Networks and Collaborative Technologies. "Organizations

will focus on driving brand awareness as well as having ongoing conversations with customers. This is

particularly suited to online communities where brands can quickly build a trust relationship with

customers, employees, partners, and suppliers."

©2015 IDC #257492 20About IDC International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications and consumer technology markets. IDC helps IT professionals, business executives, and the investment community make fact- based decisions on technology purchases and business strategy. More than 1,100 IDC analysts provide global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries worldwide. For 50 years, IDC has provided strategic insights to help our clients achieve their key business objectives. IDC is a subsidiary of IDG, the world's leading technology media, research, and events company. Global Headquarters 5 Speen Street Framingham, MA 01701 USA 508.872.8200 Twitter: @IDC idc-insights-community.com www.idc.com Copyright Notice This IDC research document was published as part of an IDC continuous intelligence service, providing written research, analyst interactions, telebriefings, and conferences. Visit www.idc.com to learn more about IDC subscription and consulting services. To view a list of IDC offices worldwide, visit www.idc.com/offices. Please contact the IDC Hotline at 800.343.4952, ext. 7988 (or +1.508.988.7988) or sales@idc.com for information on applying the price of this document toward the purchase of an IDC service or for information on additional copies or Web rights. Copyright 2015 IDC. Reproduction is forbidden unless authorized. All rights reserved.

You can also read