Wood Mackenzie Downstream Seminar - Moscow, 9th April 2019 - Al-Attiyah Foundation

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Wood Mackenzie Downstream Seminar Moscow, 9th April 2019 Trusted Intelligence woodmac.com

Wood Mackenzie – Moscow Downstream Seminar

Putting together the global downstream puzzle and what it means for Russia

Tuesday 9th April 2019

13:00 – 14:00 Registration and Refreshments

14:00 – 14.10 Welcome Address Elena Borisova

Senior Manager

14:10 – 14:50 Global Oil & Gas Outlook Alan Gelder

VP Refining, Chemicals and Oil Markets

14:50 – 15:30 Global Refining Outlook Alan Gelder

VP Refining, Chemicals and Oil Markets

15:30 – 16:00 Coffee Break

16:00 – 16:45 Global Petrochemical Outlook Patrick Kirby

Principal Analyst, EMEARC Olefins

16:45 – 17:00 Closing Remarks Elena Borisova

Senior Manager

EVENT

DISCLAIMER

These materials, including any updates to them, are published by and remain subject to the copyright of the Wood

Mackenzie group ("Wood Mackenzie"), and are made available to clients of Wood Mackenzie under terms agreed

between Wood Mackenzie and those clients. The use of these materials is governed by the terms and conditions of the

agreement under which they were provided. The content and conclusions contained are confidential and may not be

disclosed to any other person without Wood Mackenzie's prior written permission. Wood Mackenzie makes no warranty

or representation about the accuracy or completeness of the information and data contained in these materials, which

are provided 'as is'. The opinions expressed in these materials are those of Wood Mackenzie, and nothing contained in

them constitutes an offer to buy or to sell securities, or investment advice. Wood Mackenzie's products do not provide a

comprehensive analysis of the financial position or prospects of any company or entity and nothing in any such product

should be taken as comment regarding the value of the securities of any entity. If, notwithstanding the foregoing, you or

any other person relies upon these materials in any way, Wood Mackenzie does not accept, and hereby disclaims to the

extent permitted by law, all liability for any loss and damage suffered arising in connection with such reliance.

Copyright © 2018, Wood Mackenzie Limited. All rights reserved. Wood Mackenzie is a Verisk business.

woodmac.com

Global Oil & Gas Outlook

Moscow, 9th April 2019

Trusted Intelligence woodmac.com

4

woodmac.com

Global demand reached 100 million b/d in Q4 2018. Growth in 2018

averaged 1.1 million b/d

Recovery in OECD demand has been a key feature since 2015. OECD growth to soften

by 2020.

Global liquids demand Growth in global oil demand

OECD nonOECD OECD nonOECD global

120 3.0

100

2.0

year-on-year change, million b/d

80

1.0

million b/d

60

0.0

40

-1.0

20

0 -2.0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Source: Wood Mackenzie Source: Wood Mackenzie

Source: IEA MODS, EIA, local statistics Forecast: Wood Mackenzie 5

woodmac.com

Global supply growth to slow to 1.1 million b/d in 2019: non-OPEC

growth offset by OPEC declines in Iran and Venezuela

Demand gains for 2019 match those of oil supply making 2019 tighter than expected early this year

and reflecting the impact of geopolitical risk on the supply/demand balance

Global liquids supply Global liquids demand

3.5 106 3.5 China Rest Asia US Europe

Other* Global previous

3.0 104 3.0 * Other includes Middle East,

Africa, Russia/ Caspian, and

Latin America

Year-on-year change (million b/d)

2.5 102 2.5

Global supply (million b/d)

Annual change million b/d

2.0 100 2.0

1.6

1.5 98 1.5

1.1 1.1

1.0 96 1.0

0.5 94 0.5

0.5 2.5 1.1 2.3

0.0 92 0.0

2015 2016 2017 2018 2019 2020

Global supply change Mar-19 Global supply (rhs) -0.5

2015 2016 2017 2018 2019 2020

Source: Wood Mackenzie 6

woodmac.com

Brent forecast to remain broadly stable, with 2020 supported by IMO

Strong global oil demand growth in 2020 adds support to price

Brent price outlook (nominal)

Surge of demand growth in 2020

Strong OPEC+ production adds upward pressure to price.

$90 restraint, and lower supply from

Prices fell as fears ramped up at end 2018

Iran and Venezuela adds price View reflects moderate OPEC+

about weakening global economic growth.

support into Q3 2019 production restraint

$80 Signs of easing in trade tensions between US

and China has helped spark recovery since

early 2019

$70

$60 IMO regulations going into

effect in Jan 2020 boost

refining crude runs sharply

US$ per bbl

$50 for the year

A tight Q3 2019 supply and demand That lifts prices as refiners

$40 balance combined with peak summer seek to meet surge in

demand season in US lifts prices. distillate demand

$30 IMO offsets price impact of

Political risk, in Venezuela especially,

continues to have an upward price potential oversupply in

impact 2020, especially with

$20 political risk continuing

Global demand growth: Global demand growth: Global demand growth: Global demand growth:

$10 1.3 million b/d 1.1 million b/d 1.1 million b/d 1.6 million b/d

$54 $71 $66 $68

$0

Jan-17

Jan-18

Jan-19

Jan-20

Source: Argus, Wood Mackenzie forecast 7

woodmac.com

Longer term, global liquids demand growth rate to slow. Demand to

reach around 110 million b/d in 2040

Excluding biofuels, LPG and ethane, oil demand grows 5 million b/d between now and

2040. Annual growth decelerates steadily through mid-2030s

Global liquids* demand Annual growth in global liquids demand

oil demand LPG

Ethane demand met by biofuels 2,000

Global GDP growth eases from 3.1% in

actual Linear (actual) 2017 to 2.5% by 2021 as China, Europe

120 and US lose momentum. Risk to GDP is

to the downside from US/China trade war

1,500

100 2020 growth includes one-time 100 kbd

increase in total demand caused by

IMO-related shift from marine fuel oil to

1,000 gasoil (when measured in volume terms)

80

000 b/d

million b/d

Oil demand increasingly

displaced by electrified

60 Global liquids demand vehicles and natural gas

grows 11 million b/d to 2040 500 in transport

40

-

20

-500

-

2000 2005 2010 2015 2020 2025 2030 2035 2040

Source: Wood Mackenzie

Source: Wood Mackenzie * liquids includes oil products, NGLs, and biofuels 8

woodmac.com

Growth in gasoline demand loses momentum post-2020 as fuel

efficiency kicks in, followed by rising penetration of EVs

Europe and North America lead the decline in global demand, but growth rate also

slows in Asia

Global demand by main product Global demand by region

Gasoline Diesel/Gasoil Fuel Oil North America Europe Asia Pacific FSU

Jet/Oth Kero Eth/LPG/Nap Other Latin America Mid East Africa

50

35

45 Asian demand growth slows

as China demand peaks;

30 40 India continues to surge

ahead but from low base

35

25

30

million b/d

20

million b/d

25

Europe’s oil demand enters terminal decline by the

15 20 end of this decade, while US demand continues to

grow until the mid 2020s

15

10

10

5

5

0 0

2000 2010 2020 2030 2040 2000 2010 2020 2030 2040

Source: Wood Mackenzie

Source: Wood Mackenzie

Source: IEA Energy Statistics, Local Statistics Forecast: Wood Mackenzie 9

woodmac.com

Global stock of EVs is expected to grow to 290 million passenger

cars by 2040. AEVs reach 3 mil by 2035, 24 mil by 2040.

Europe and the US lead with 60-70% of sales by 2040, while China leads the developing

world at half that level of penetration

EVs as a share of total light vehicle sales Global electric vehicle stock

Europe US China India Global

80% 300 China

EV sales accelerate in Europe and Other Asia

the US post 2035 due to AEVs.

70% AEV share reaches 20% in the US Europe

250

and 17% in Europe by 2040. United States

60% Rest of the world

share of light vehicle sales

200

Million units

50%

40% 150

China EV sales lose momentum

30% as subsidies fade by 2020.

Sales accelerate once 100

technology no longer is a

stumbling block

20%

50

10%

0% 0

2015 2020 2025 2030 2035 2040 2015 2020 2025 2030 2035 2040

Note: ‘Electric vehicles’ include autonomous electric vehicles (AEVs), battery electric vehicles (BEVs), and plug-in hybrid electric vehicles (PHEVs)

Europe defined as OECD Europe plus Albania, Bosnia, Bulgaria, Croatia, Cyprus, Lithuania, Macedonia, Malta, Montenegro, Romania and Serbia

Source: Wood Mackenzie 10woodmac.com

In road transport, electrification and autonomous technology

disrupt oil demand in the long-run

While the shift in car sales to EVs is rapid post-2030, the impact on the car parc is gradual. By 2040,

EVs account for 37% of new car sales and 17% of total cars in operation.

Global passenger car sales by type Global passenger car stock by type

140 2,000

Globally, the share of conventional cars Total EV stock reaches

falls to 50% by 2040. 296 million in 2040.

1,800

120 Post 2035, the rise of AEVs leads to a AEVs reach 4 mil units by 2035 and

decline in global car sales 24 mil units by 2040

1,600

100 1,400

1,200

80

million

million

1,000

60

800

40 600

400

20

200

0 0

2015 2020 2025 2030 2035 2040 2015 2020 2025 2030 2035 2040

Others AEVs EVs/PHEVs HEVs Conventional

Source: Wood Mackenzie

Conventional: Gasoline, Diesel and LPG internal combustion engine vehicles, HEVs: Hybrid Electric Vehicles,

PHEVs: Plug-in Hybrid Electric Vehicles, EVs: Battery Electric Vehicles; AEVs: Autonomous Electric Vehicles 11woodmac.com

Acceleration of EV adoption post-2030 leads to ~5.3 million b/d of oil

demand displaced by 2040

The US, China and Europe, in particular, will see the most oil demand displaced

Global liquids demand displaced by EVs Global liquids demand

6 E-trucks 115

Lost to E-trucks

AEVs

Lost to AEVs

5 ROW

Lost to EVs

China 110

4 Europe Base case

US

Million b/d

Million b/d

3 105

2

100

1

- 95

Source: Wood Mackenzie 12woodmac.com

Non-OPEC countries dominate near term supply increases…

…but OPEC capacity additions strengthen through the mid-to-late 2020s

Year-on-year change in OPEC capacity and non-OPEC production*

3.0 OPEC Capacity

Stronger non-OPEC growth forecast through the near Non-OPEC

term, primarily driven by upgrades to US supply

2.5 OPEC Capacity H1 2018

Non-OPEC H1 2018

2.0

Million b/d change

1.5

1.0 OPEC capacity additions drive increases through mid-

to-late 2020s

OPEC capacity continues to grow through to the end of

the forecast period

0.5

0.0

-0.5

Non-OPEC production turns to decline post-2030

-1.0

Source: Wood Mackenzie *Excludes unconventionals (biofuels, gas-to-liquids and coal-to-liquids) and processing gains 13woodmac.com

US lower 48 crude oil: production coming in higher and faster

The peak occurs in 2025 at 12 million b/d compared to 11.7 million b/d in 2031 in our H1

2018 outlook. This is supported by stronger than expected short-term growth

US Lower 48 crude and condensate production

14 Reserves Growth Bakken Eagle Ford Niobrara

Permian SCOOP-STACK-Cana Other H1 2018

Crude oil and field condensate production (million b/d)

12

10

8

6

4

2

0

Source: Wood Mackenzie 14woodmac.com

The level of supply outages remains highly unpredictable

Iran sanctions and Venezuelan economic and political turmoil help push unplanned supply

losses back to 4 million b/d in 2019

Global unplanned supply outages

5.0 Historical Forecast

Other

4.5

Venezuela

Kuwait

Visible unplanned outages (million b/d)

4.0

Saudi Arabia

3.5 China

Azerbaijan

3.0 Canada Oil Sands

US GoM

2.5

Colombia

UK/Norway

2.0

South Sudan

1.5 Yemen

Iraq

1.0 Syria

Iran

0.5

Libya

Nigeria

0.0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Source: Wood Mackenzie 15woodmac.com

Geopolitical risk remains a critical driver of the supply outlook

Russia: increased brownfield drilling/ continued

Canada: delays in expansion of takeaway development of greenfield projects; despite recent

capacity will hinder investment in oil sands and production increases, an extra ~250 kb/d could be available

conventional heavy crude. through projects like Messoyakhaneftegaz, Severnaya Neft,

Trebs and Titov, or Yurubcheno-Tokhomskoye.

Iraq: upside risk from resumption of Kirkuk volumes in the North, and

strong growth from southern fields, with recent uptick in project FIDs.

Iran: US sanctions have a greater effect on exports

US: alleviation of infrastructure Libya: supply wildcard - upside potential from as waivers expire. Impact on fresh IOC investment

constraints, inventory upgrades, streamlined security improvements and increases in service sector

delays field expansions.

operations, technological innovation and higher oil activity; but threats to infrastructure remain.

prices all provide upside risk.

UAE: new developments and expansions at Upper

Zakum, Satah al-Razboot, Umm al-Lulu and Nasr push

capacity higher, quicker.

Nigeria: as predicted, militant activity has Saudi Arabia/ Kuwait: resumption of Neutral Zone

Venezuela: downside risk if no political been low in the run up to the presidential elections. Stability is production could bring back 0.5 million b/d of

or economic improvement in the early 2020s; production

falls below our base case view of 1 mb/d in 2020 and no

dependant on election results and adopted policy. potential capacity.

medium-term recovery.

Brazil: slower pace of development of pre-salt Santos Basin fields and

higher declines in mature Campos Basin limits production growth.

Global upside: resilience of mature producers (such as China, Mexico, North

Global downside: rising geopolitical tensions pose significant risk to

Sea, Egypt) to period of weaker prices lifts near-term supply above expectations.

the supply outlook beyond the visible horizon.

Source: Wood Mackenzie 16woodmac.com

The oil ‘supply gap’ to 2030 will be met by US crude, OPEC capacity

growth and more expensive conventional production

Over 25 million b/d liquids supply must be met by new drilling by 2030

The 2030 supply gap Filling the ‘supply gap’ to 2030

110

30

The 2030 supply gap

10m

25

100

26m 20

Million b/d

90 15

21m

OPEC Capacity Growth

10

Non-OPEC Other Sources

80 4m

Conventional Pre-FID

5 US Lower 48 Future Drilling

Supply Gap

70 0

2018 Demand Non-OPEC Non-OPEC, Supply gap $90

Demand growth by decline, projects

2030 onstream under dev

fields -5

Source: Wood Mackenzie 17

Non-OPEC other sources includes reserves growth, contingent resources, yet-to-find and unconventionals (biofuels, CTL and GTL)woodmac.com

Fundamentals downward price pressure in the short-term gives way

to higher price pressure as supply-demand balance tightens

Oil demand peaks in the late-2030s but total liquids capacity plateaus from the early

2030s

Global liquids capacity plateaus from 2030. About 6 years later global oil demand

Brent price outlook (real) peaks, implying a tightening supply/ demand balance through the mid-2030s.

Improved fuel efficiency curbs growth in oil demand, while EVs and natural gas

Prices fall through 2020 as supply growth, driven by the US, outpaces

penetration into bunkering and trucking cause oil demand destruction of almost 8

$140 demand growth. Since H1 2018 we have revised US supply growth higher,

million b/d by 2040. The full impact of this is partially offset by growing petchem

and global demand growth lower to 2020. But OPEC and Russia will step in

feedstock demand, softening the pace of global oil demand decline after the peak.

and restrain production to keep prices above $70/ bbl.

$120 Prices come under downward pressure as conventional

US$ per bbl, constant 2018 prices

production sanctioned during the run up in prices to

2023 enters the market. OPEC spare capacity also

increases, with growth in Iraq, the UAE and Kuwait.

Meanwhile, oil demand growth decelerates markedly as $100

$100 the impact of fuel efficiency mandates take effect.

$80

$80 $74 $76

While prices come off

around the peak in oil

Prices rise as higher cost supply is required to meet

demand, industry reduces

continued growth in demand and replace significant

$60 conventional and increasingly unconventional declines.

its exposure to long-lead

projects in advance of the

peak in oil demand, and

US onshore producers move to marginal acreage and

global supply growth is

work hard to maintain production as core tight oil

$40 slowing. Together this

inventory is drilled out.

prevents a crash in prices.

Brent prices reach $80/ bbl in 2023 as: For conventional non-OPEC supply, attention is

(i) onshore US breakevens increase due to service cost inflation and stalling switching to reserves growth and yet-to-find, as

$20 well productivity growth as drilling moves away from the core of the core; pipeline of new field developments diminishes. OPEC

(ii) Iranian sanctions remain in place; and spare capacity begins to drop off post-2030.

(iii) more expensive conventional production is required to fill the supply gap,

exacerbated by rising declines from US tight oil wells

$0

2010 2015 2020 2025 2030 2035 2040

H1 2018 H2 2018

Source: Wood Mackenzie 18woodmac.com

Asian LNG demand growth will start to slow next decade and pace

of future growth is uncertain

Asian LNG demand growth to 2030 • Increased domestic production

and pipe import competition in

China

400

• Coal and nuclear competition in

350

South Korea and Japan

300

• Renewable developments

250

• Economic slowdown

mmtpa

CAGR 0%

200

150

100

• Increased concern about

50 pollution and backlash against

coal

0

• Infrastructure and demand

creation in emerging markets

Japan Other Asia South Korea

• LNG prices remain competitive

Taiwan India Sub Cont South East Asia against oil

China

Source: Wood Mackenzie 19woodmac.com

…however resilient demand and declining indigenous production

are making Europe increasingly import dependent

Europe will require 70 bcm of additional imports by 2025

European Supply-Demand Gap Europe Import Dependency from Russia or LNG

350 70

600

bcm

300

500

Import Dependency

from Russia or LNG

60

Russia and LNG

supplies required to bcm

bcm (@40 MJ/m³)

bcm (@40 MJ/m³)

400 meet growing gap 250

300 200

200 150

100

100

-

50

Europe North Africa Southern Corridor -

Russia LNG Demand

Source: Wood Mackenzie European Energy Service 20woodmac.com

Europe will be a “sink” for the global LNG market in the short-term but

it will need to compete post-2020 as the global market tightens

We now see market tightening in 2023, a year earlier than our previous update

Russia pipe and LNG imports into Europe TTF price

250 10.00

Pipe/LNG Europe in need of

Softening of Prices trade in

competiti 200 bcm of Russian 9.00 prices excess of oil

on gas despite LNG

towards indexed

imports >100bcm 8.00

US$/mmBtu, Real (2018)

US$5/mmbtu contracts

200

7.00

bcm(@40MJ/M3)

6.00

150 -20 bcm +30 bcm 5.00

4.00

3.00

100

2.00

+40 bcm

1.00

50 0.00

2015 2016 2017 2018 2019 2020 2021 2022 2023

2015 2016 2017 2018 2019 2020 2021 2022 2023

Russia Pipe LNG Europe Indigenous supply TTF Europe Proxy Oil Indexed Contract

Source: Argus Media, NYMEX, Wood Mackenzie

Source: Wood Mackenzie 21woodmac.com

2019 is set to be a record year for new LNG project sanctions….

FID taken in 2019 Expected FID in 2019 Wildcard FID in 2019 Targeted FID in 2020

WM

Golden Pass: Arctic LNG-2: Busy signing Forecast

Announced FID on 05- Woodfibre LNG: engineering contracts early in

70

Feb on 16.0 mmtpa, Has HoAs for most of the capacity ; 2019. Significant global interest

Capacity Sanctioned (mmtpa)

$10 billion project. needs to finalise EPC costs and with more partner announcements

SPAs expected soon 60

Partners expect start up

in 2024

50

40

Tortue Phase 2 & 3:

Partners pushing to take 30

FID on additional

phase(s) in 2020,

supported by cost 20

Calcasieu Pass:

Venture Global has efficiencies from Phase

line of sight on FID in 1 10

2019 after successful

marketing campaign in 0

2018 and obtaining

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

FERC approval.

Financing the final NLNG 7: Partners

hurdle pushing for FID

but financing, Rest of World Qatar Australia

marketing and

country elections Qatar Megatrains: Partner USA West Canada Mozambique

could hamper announcements expected Russia

progress mid 2019 with FID

planned for late

Sabine Pass T6: Cheniere 2019/early 2020

state FID is imminent on

PNG LNG Train 3 /

sixth train (4.5 mmtpa)

Papua LNG: Partners in

both projects signed MOU

with government at end of

2018 defining key terms of

Gas Agreement. Working

on Gas Agreement,

Other North America: engineering and offtake

Many projects moving agreements in 2019

through legislative, Mozambique LNG

(Area 1): Signed Pluto Expansion:

environmental, marketing and Rovuma LNG (Area 4): Woodside selected Bechtel as

financing milestones. numerous SPAs at

Partners announced offtake agreements end EPC contractor. FID target of

Driftwood, Costa Azul and the start of 2019

of 2018. Targeting FID mid 2019 but H1 2020, but looking to farm

Freeport Train 4 all targeting sufficient to secure

requires progress on government approval down in upstream asset

FID before end of 2019. financing. FID target

and clarity on financing to make FID this (Scarborough)

is H1 2019.

year

22woodmac.com

woodmac.com

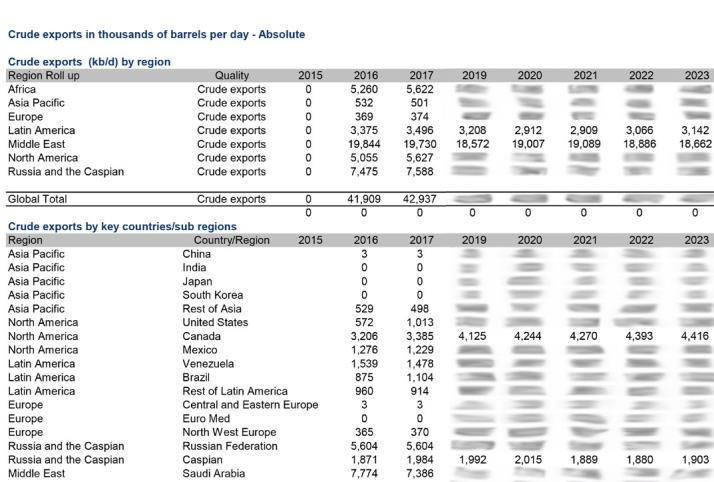

Crude Trade

Oil Supply Tool Macro Oils Product Market

Service Global oil supply

forecast by grade

Benchmark crude

price forecast

Service/Refinery

Evaluation Model

offers a

Refinery investments

and crude runs,

Crude price

historical crude slate

holistic view

of global

crude trade Crude supply Crude demand

Crude Trade Service

Crude trade flows

and crude price

differentials by

quality 6

23woodmac.com

woodmac.com

Why will global crude trade see significant changes?

Although, growth in US light crude exports is the single biggest reason, there are several other

important reasons that will change global crude trade flows

North America Europe Russia

• Rising US crude exports: where will it • Lower European crude runs, increased • Lower Urals, higher ESPO supply: how

go and why? US light crude imports: how will will Russia balance between Europe

• Canadian oil sands exports to Asia: European crude market balance? and Asia crude exports?

when and how much?

• Sharp declines in Mexico’s production:

what is the impact on exports?

Latin America Middle East/Africa Asia Pacific

• Sharp declines in Latin America heavy • Large grassroots condensate splitters • Rising crude demand, declining

crude production: what does it mean and refineries coming online: what is domestic production: how will Asia

for US and Asian heavy crude refiners? the impact on exports? meet its crude import demand?

• Heavy crude supply growth in Iran • Will Asia meet its heavy crude

and Iraq: will it be enough to offset requirements?

declines elsewhere?

• What is the impact of US sanctions on

Iran crude exports?

24

24Medium crude trade changes due to competition from US grades

woodmac.com

US and Europe cut back Africa and Middle East imports. Asia pulls in these barrels to

meet rising crude demand

Key changes to medium crude trade (2025 minus 2017), kb/d

Russia cuts back Urals

exports to Europe due to

Europe cuts Africa and the declining production. ESPO

Middle East imports with exports to China rises with

rising US light crude amid expanded pipelines

falling crude runs

Russia and

Caspian -750

Europe

US cuts back US

Middle

medium crude

+80 East

imports from the Asia

Middle East and

Africa with rising Asia pulls in large volumes

domestic crude -2110 of Africa and Brazil crudes

processing Africa to meet its rising import

Latin demand

America -95

Trade increase

Trade decrease +1100

Exports Exports

increase, decrease,

500 kb/d 500 kb/d

Exports = domestic supply – domestic demand

25

Source: Wood Mackenziewoodmac.com

woodmac.com

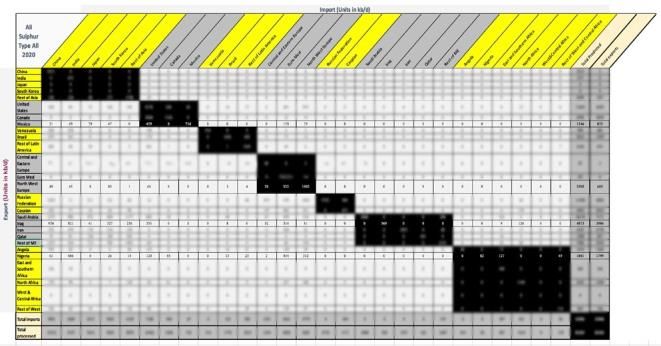

Crude Trade Service deliverables

Excel data and PowerPoint updated

Data tables

six-monthly

Global crude supply (2016 to 2025 – annual)

Trade flows

• By country/region matrices

• By quality (Condensates/Light/Medium/Heavy)

Crude oil demand for refining

(2016 to 2025 – annual)

• Refinery investments

• Crude capacity

• Crude intake by region/country

• Crude intake by quality

• Crude imports/exports/domestic

Trade flows matrices (2016 to 2025 – annual)

• Condensates/Light/Medium/Heavy PowerPoint

slides

Crude price forecasts for 90+ benchmark and key

crude grades

PowerPoint slides to explain the key messages

2626woodmac.com

Global Refining Outlook

Moscow, 9th April 2019

Trusted Intelligence woodmac.com

27woodmac.com

Refinery capacity additions accelerate in 2019 and 2020, with 2020

capacity additions outpacing oil demand growth

Spare capacity increases in 2020 but IMO distillate demand growth limits the downside for

utilisation

Global CDU capacity changes Refining capacity and products demand

Major refined products demand

Capacity and demand (million b/d)

2.5 108 95

Annual CDU change (million b/d)

Asia Middle East

2.0 Russia & Caspian Europe 103 90

Africa North America

Latin America

1.5 98 85

1.0 93 80

0.5 88 75

0.0 83 70

Jan-18 Sep-18 May-19 Jan-20 Sep-20

-0.5 CDU capacity LHS

2016 2017 2018 2019 2020 Total demand LHS

Naphtha thru fuel oil demand RHS

Source: Wood Mackenzie 28woodmac.com

IMO is getting closer - there are now over 2,000 confirmed orders for

scrubbers as the uptake from shippers starts to accelerate

The volume of scrubbed HSFO is expected to grow steadily after 2020, rising to

around 1.3 million b/d by 2025

Outlook for scrubber installations Scrubbed HSFO outlook by vessel type

30% 7,000

1.4 Containers

Number of vessels

Crude tankers

6,000

25% % of marine fuels 1.2 Cruise and passenger ferries

Dry bulk vessels

Number of vessels

5,000

% of marine fuels

20% 1.0

Product tankers

million b/d

4,000

0.8

15%

3,000 0.6

10%

2,000 0.4

5%

1,000 0.2

0% 0 0.0 2020

2021

2022

2023

2024

2025

2019

2020

2021

2022

2023

2024

2025

Source: Wood Mackenzie Product Markets Service 29woodmac.com

Improving crude and stream segregation at refineries, combined

with VGO blending, should support increasing VLSFO production

VLSFO supply reaches 1.7 million b/d by 2024

Global VLSFO supply forecast, kb/d Global VLSFO supply forecast by region, kb/d

VGO diversion Asia Pacific Greater Europe

Latin America Middle East

Low sulphur resid components - existing and from North America Russia & Caspian

2,000 investment Sub-Saharan Africa

2,000

1,800 1,800

1,600 1,600

1,400 1,400

1,200 1,200

1,000 1,000

800 800

600 600

400 400

200 200

0 -

2020 2021 2022 2023 2024 2025 2020 2021 2022 2023 2024 2025

Source: Wood Mackenzie 30woodmac.com

VLSFO component availability varies by region

This may present shippers with fuel compatibility challenges when refuelling in different

regions

Regional VLSFO component “blends”*

Vac Resid - Cracked Vac Resid - Straight Run Slurry Oil Hydrocracker Bottoms Atmospheric Resid

Light Cycle Oil Vacuum Gasoil Distillates Potential Supply, kb/d

100% 500

90% 450

potential supply, kb/d

80% 400

70% 350

component %

60% 300

50% 250

40% 200

30% 150

20% 100

10% 50

0% -

North America Latin America North West Med Europe Russia & Sub-Saharan Middle East India North Asia SE Asia

Europe Caspian Africa

Source: Wood Mackenzie Refinery Evaluation Model/PetroPlan

*availability of components from refineries deemed likely to supply to the marine fuels market. Based on 2017 output 31woodmac.com

Refiners cannot make enough VLSFO to meet demand so gasoil

will have to make up the gap of low S fuels

There are some concerns about quality but we assume most shippers will buy the

cheapest compliant fuel while refiners will look to get best value for their residues

Global marine bunker demand by fuel Nearly 2.1 million b/d of HSFO is

displaced by low sulphur fuels in 2020

4.0 2019 2020

MGO sales rise by nearly 1.1 million b/d

3.5 in 2020

3.0 VLSFO displaces the remaining LSFO

market by 2020, as well as a sizable

Million b/d

2.5 amount of HSFO, amounting to total sales

of ~1.4 million b/d in 2020

2.0

LNG use rises by over 70% between

1.5 2019 and 2020, but this only displaces a

further 40 kb/d of marine fuels, as LNG

1.0

bunker infrastructure is still in its infancy

0.5

0.0

HSFO LSFO VLSFO Distillate LNG*

Source: Wood Mackenzie 32woodmac.com

There is spare capacity in upgrading units to process additional

volumes of feedstock

And refiners are investing in more resid upgrading capacity

Global resid upgrading unit capacity and Global supply of vac res from crude production

average utilisation, 2017 versus capacity to upgrade it

9.0 82% 1.6

8.0 1.4

80%

7.0 1.2

million b/d

78%

million b/d

6.0

1.0

5.0 76%

0.8

4.0 74%

0.6

3.0

72%

0.4

2.0

70% 0.2

1.0

0.0 68% 0.0

Coker RHT/RFCC RHCU SDA VSB 2019 2020 2021 2022 2023 2024 2025

Cumulative vac res supply potential

Capacity Average Utilisation Cumulative upgrading capacity (COK + 50% RCC)

* in refineries with CDU capacity above 50 kb/d

Source: Wood Mackenzie 33woodmac.com

Gasoline cracks remain under pressure in 2019 but there is a new

floor in 2020

Gasoil cracks to get a boost in Q4 2019 and average $20/bbl in 2020

NWE gasoline crack vs Brent NWE gasoil 0.1%S crack vs Brent

25 25

20 20

15 15

$/bbl

$/bbl

10 10

5 5

0 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5-yr range 2018 5-yr range 2018

2019 2020 5-yr avg 2019 2020 5-yr avg

Source: History Argus, Forecast Wood Mackenzie 34woodmac.com

HSFO has to lose its recent strength as demand collapses

VLSFO price is midway between diesel and LSFO and so could price higher than shown

NWE HSFO 3.5%S crack vs Brent NWE VLSFO 0.5%S crack vs Brent

0 12

10

-5

8

-10

6

$/bbl

$/bbl

-15 4

2

-20

0

-25

-2

-30 -4

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

5-yr range 2018 5-yr range 2018

2019 2020 5-yr avg 2019 2020 5-yr avg

Source: History Argus, Forecast Wood Mackenzie 35woodmac.com

Increased use of distillate bunker fuel will support gasoil crack

spreads over the medium term

Product crack spread profile, 2001-2025 Refineries will have to increase crude throughputs in

order to produce sufficient distillate fuel for the bunker

sector

Gasoline 95R Gasoil

40 0.5%S VLSFO 3.5 wt%S HSFO There is limited flexibility for refiners to shift yields

between products meaning that there will be excess

30 production of other products

Crack spread vs Brent $/bbl

Gasoline crack spreads are expected to weaken in

20

2020 as production increases beyond demand.

10 The reduction in demand for HSFO means that it will

need to price lower relative to crude to encourage

0 increased upgrading and to compete in other markets

As HSFO cracks get much weaker in 2020, gasoil

-10 cracks have to strengthen in order to provide a strong

enough margin for refiners to increase runs and meet

-20 the extra demand for gasoil

VLSFO pricing methodology is assessed as the floor

-30

price to make the assumed VLSFO volumes available.

-40 LSFO crack spreads are likely to get some support

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

from demand for blending into VLSFO

Source: Product Markets Service 36woodmac.com

The biggest windfall in 2020 is for deep conversion refineries with a

distillate orientation

Gross refinery margins for selected reference Stronger crack spreads for middle distillates and

assets weaker HSFO cracks will result in a steep increase in

USGC Maya Coking margins for complex refiners

Singapore Dubai Hydrocracking/coking Coking refineries will see the biggest advantage as

NWE Brent Cracking they will be able to process widely discounted crudes

25

Gross refining margin $/bbl

while not producing loss-making fuel oil

Refineries based on the US Gulf Coast are particularly

20 advantaged, due to their residue import capabilities

There is an incentive for refiners with high

naphtha/gasoline/fuel oil yields to maximise the switch

15

to distillates

The impact is much more muted for more simple FCC

10 refineries focused on producing gasoline, and a

sizeable proportion of fuel oil

The overall increase in margins in 2020 should be

5

sufficient to incentivise refiners to increase crude

throughputs enough to meet the extra distillate

demand

0

2020

2015

2016

2017

2018

2019

2021

2022

2023

2024

2025

Source: Wood Mackenzie Product Markets Service 37woodmac.com

Heavier sour crudes will fall in value relative to lighter sweeter

crudes and the relative value of very sweet crudes will rise

Crude differentials to Brent, 2015-2025

Crack spreads for middle distillates are expected to

Urals NWE Bonny Light strengthen while high sulphur fuel oil cracks are

forecast to weaken

4

As a result, refiners will make more profit from crudes

Price differential to Dated Brent $/bbl .

3 with high middle distillate yields and the value of these

2 crudes is expected to strengthen relative to crudes

with a high gasoline yield

1

0

A weaker HSFO crack would result in heavier sour

crudes becoming less attractive to refiners and falling

-1 in value relative to light sweet crudes

-2

Less complex refiners, in particular, will seek out light

-3 sweet crudes in order to reduce their HSFO yields and

-4 maximise middle distillate output

-5 More complex refiners, with coking and hydrocracking

facilities, will enjoy wide discounts for their target

-6

crudes

-7

Medium/heavy sweet crudes could be in strong

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

demand to produce VLSFO

Source: Wood Mackenzie Product Markets Service 38woodmac.com

China, the Middle East and other developing Asia to build more than

70% of the new grassroots capacity additions by 2025

Kuwait: China:

Al-Zour,

615kbd, 2020 Hengli refinery,

400kbd, 2020

Zhoushan

Nigeria: (Zhejiang)

Dangote refinery, 400kbd,

refinery, 2020

Global net CDU additions (kbd) 650kbd, 2022

Caojing refinery,

300kbd, 2023

Rest of the Zhanjiang

World 2019 2020 refinery, 200kbd,

2021 2022 2020

2023 2024

Middle East Saudi Arabia: Iran:

2025 Jazan, 400 kbd, Persian Gulf, Vietnam:

2019 360kbd, 2017- Nghi Son

Asia Pacific

2019 refinery,

200kbd, 2018

Oman:

World Duqm refinery, Malaysia:

230 kbd, 2023 RAPID project,

300kbd, 2019

0 5000 10000

Source: Wood Mackenzie – Product Markets Long Term Outlook 39woodmac.com

Global refining capacity additions start to outpace global demand

growth

Average global utilisation is forecast to fall

Global refining capacity versus demand

Capacity & non-refinery supply Demand Average utilisation (right-hand axis)

3.5 83%

Forecast

3.0 82%

2.5 81%

2.0 80%

1.5 79%

million b/d

1.0 78%

0.5 77%

0.0 76%

-0.5 75%

-1.0 74%

-1.5 73%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Source: Wood Mackenzie 40woodmac.com

Refining margins are forecast to fall from 2020, particularly in

Europe

Margins return to closure threat levels by 2024

NWE reference gross refining margins (US$/bbl)

$/bbl

14

12

10

8

6

4

2

0

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

NWE Brent Cracking $/bbl (Real) NWE Urals Cracking $/bbl (Real) NWE Urals Hydrocracking $/bbl (Real)

Source: Wood Mackenzie

41woodmac.com

Crude-to-chemicals projects in China are gaining momentum, as a

means to add value to light distillate streams

China’s new “crude to chemicals” projects are delivering materially higher

petrochemicals integration – at ~40 – 50wt% yield

Panjin (300, NORINCO, unclear)

LIAONING

Yingkou (70, CNOOC, 2019)

Caofeidian (300, Risun, unclear) Dalian (400, Hengli, 2020)

HEBEI Huabei (100, Sinopec, 2018)

SHANDONG Dongying (70, CNOOC, 2019)

Senchi (100, Zibo Senchi, 2019)

HENAN

"Firm" crude-to-chemicals Luoyang (200, Sinopec, 2020) Lianyungang (320, Shenghong, unclear)

Mb/d

Proposed crude-to-chemicals

Jingmen (80, Sinopec, 2020)

2.5 "Firm" grassroots refineries HUBEI Caojing (300, Sinopec, 2022)

"Firm" Expansions ZHEJIANG Zhejiang (400, Rong Sheng, 2020)

2.0 Zhejiang - 2 (400, Rong Sheng, unclear)

1.5

GUANGDONG Quanzhou (60, Sinochem, 2019)

1.0 Zhanjiang (200, Sinopec/KPI/Total, 2020)

Zhuhai Baota (100, Ningxia Baota, 2021)

HAINAN

0.5 Hainan (100, Sinopec, 2022)

0.0

“Firm” mega grassroots crude-to-chemicals

-0.5 sites

2018 2019 2020 2021 2022 2023 2024+ Proposed grassroots crude-to-chemicals sites

“Firm” grassroots refineries

“Firm” Expansions

42

Source: Wood Mackenzie Product Markets Service Numbers in the brackets represents CDU capacity in kb/dwoodmac.com

Value-add from petrochemical integration can be significant

China’s new “crude to chemicals” projects are delivering materially higher

petrochemicals integration and value addition

Hengli margins and value build-up (2020), Hengli integrated site net margins, US$/bbl

US$ for every barrel of crude

Hengli margins design crudes

Chemicals uplift

100 Refinery Hengli margins non design crudes

25

12.7

80

8.1

55.6 20

60 40.4 40.4

92.4

40 77.2 15

58.2

20 36.8 36.8

10

0

Chemical margin

Site crude cost

Refinery margin

OPEX

Fuels value split

Fuels+Chemicals

Fuels revenue

Incremental OPEX

Site product revenue

Fuels to chemicals

Design feed Non design feed*

5 API ~27.8 API ~31.5

revenue

S = 2.8 wt% S = 1 wt%

0

2016 2017 2018 2019 2020 2021 2022 2023

Crude-to-chemicals

• Margin loss because of sub-optimal feed varies from

• Location will be a key driver in overall project economics $2/bbl to $4/bbl, based on market environment

• Relative fuels/chemicals pricing, utility fuel costs, relative

crude freight, will all impact relative project economics in

various locations of these mega projects

* Non design feed assumed at similar levels to average

Source: Wood Mackenzie Product Markets Service, PetroPlan 43

Sinopec/Petrochinawoodmac.com

Weaker refiners will struggle to compete when over-capacity returns to

the sector, as first quartile sites achieve high utilisation

A key challenge is that slowing global demand growth reduces the capability to absorb

world-scale refineries, which are getting larger and more competitive

2017 Regional Net Cash Margin profile for North America, Asia, Russia, Middle East and Europe

30

Crude to chemical projects are large

25 and will occupy a first quartile

position

20

NCM 2017, US$/bbl

15

10

5

0

-5

-10

North America Latin America Europe FSU Africa Middle East Asia Pacific

Source: Wood Mackenzie

Source: Wood Mackenzie Refinery Evaluation Model

44woodmac.com

Longer-term gasoline demand trends will challenge refiners in the

US and Europe

Gasoline & naphtha

Cumulative change in regional demand Middle distillates

0.0 2.5

-0.5 2.0

-1.0 1.5

-1.5 1.0

-2.0 0.5

-2.5 0.0

2024 2026 2028 2030 2032 2034 2024 2026 2028 2030 2032 2034

2.5

West of Suez 2.5 East of Suez

2.0

2.0

1.5

1.5

1.0

1.0

0.5

0.0 0.5

-0.5 0.0

2024 2026 2028 2030 2032 2034 2024 2026 2028 2030 2032 2034

45woodmac.com/chemical

woodmac.com

s

OPEC+ has a supply dilemma for at least the next 2 years

Longer term, OPEC’s role grows in the medium term as US tight

oil growth slows

The Energy Transition slows demand growth, but the Upstream

sector is less impacted than refining

IMO remains uncertain, but it supports refining margins in 2020

Over-capacity is returning to the refining sector, so lowering

utilisation and margins. Threat of closure returns to Europe

Exports of crude and products to Europe will become more

challenging

Refinery/petrochemical integration is a key theme to develop

structurally sustainable refining assets

Alan Gelder

VP Refining, Chemicals and Oil Markets

Refining Global Content Lead

46woodmac.com

Global Petrochemicals Outlook

Moscow, 9th April 2019

Trusted Intelligence woodmac.com

47The petrochemical industryacross the entire energy to

woodmac.com/chemicals

woodmac.com

petrochemical value chain

Coal Syngas Ethylene Ethylene Ethylene EODs Recyclate

Oxide Glycol

Coal

Gasification Propylene Phthalic Plasticizer

Butanol O-xylene

Anhydride Alcohols

Ethane

Steam

Cracker Butadiene Polyethylene PVC All Films

Propane

Natural Polypropylene HMD All Fibres

Gas

Butane

Gas Derivative

Processing & Benzene Styrene Adiponitrile Polyamide

Conversion

Fractionation

Condensate

Cumene PBT PET

Toluene Caprolactam

Phenol

Reformer &

LPG Aromatics Xylene m-Xylene Paraxylene PTA Polyester

Extraction

Crude Oil

Naphtha

Oil Refinery

48

48woodmac.com

Agenda

1 Global petrochemical trends

What is driving the focus on chemicals?

2 Ethylene market outlook

Latest forecast for the biggest petrochemical market

3 Ethylene economics

What is next for costs and margins

49woodmac.com

Global petrochemicals

50woodmac.com

Megatrend 1 – small part of the barrel, but increasing focus

Liquid hydrocarbon use

Hydrocarbon liquids used in chemical production 2019 Global oil demand by key segments

Million tons

per year

Others

500 LPG Naphtha 13%

Distillates Others/NGL

400 Industry

13%

Estimated 4.2

300 billion tons Transport

RCA 55%

10%

200

chemicals

9%

100

0

2005 2010 2013 2015 2020

51woodmac.com

Megatrend 2 – emerging and growing plastics concern

Although chemicals are integral to every day life

Polyethylene Polystyrene / ABS

PVC PET / Polyester

Polypropylene Methyl Methacrylate

Synthetic Rubber Fertilizer

52woodmac.com

Global commodities outlook – focus on ethylene

The growth of ethylene is expected to continue to be significant through the long-term forecast

Global commodities outlook – demand growth relative to 2005 base

2.5

2.2

1.9

1.6

1.3

1.0

2005 2010 2015 2020 2025 2030 2035

Oil Steel Ethylene GDP

Source: Wood Mackenzie

53woodmac.com

Global base chemical demand outlook

Global market for base chemicals is expected to grow by over 50% through to 2035

Global base chemical demand outlook

Million tons

600

500

400

300

200

100

-

2008 2011 2014 2017 2020 2023 2026 2029 2032 2035

Paraxylene Benzene Butadiene Propylene Ethylene

Source: Wood Mackenzie Chemicals

54woodmac.com

Ethylene market outlook

55woodmac.com

Global ethylene demand by major derivative

Polyethylene is the engine of long-term ethylene volume growth. Growth is present across all

derivative chains, with ethylene oxide showing strong growth driven by MEG/polyester chain.

Global ethylene demand by major derivative

Million Tons

300

250

200

150

100

50

0

2005 2010 2015 2020 2025 2030 2035

Polyethylene Ethylene Dichloride Ethylene Oxide Styrene All Others

Source: Wood Mackenzie Chemicals

56woodmac.com

Global ethylene supply by feedstock

Naphtha and ethane remain the workhorses of long-term ethylene supply. Ethane overtook naphtha in

2018 and maintains a higher share through the forecast period.

Global ethylene supply by feedstock

Million Tons

300

250

200

150

100

50

0

2005 2010 2015 2020 2025 2030 2035

Refinery Ethylene Ethane Propane Butane

Light Naphtha Full Range Naphtha Gas Oil Condensate

Hydrowax Coal Methanol Renewables

Source: Wood Mackenzie Chemicals

57woodmac.com Ethylene “gold rush” underway – strong profitability attracted many Ethylene investments planned from upstream through refiners to pure chemical players Source: Wood Mackenzie 58

woodmac.com

Global ethylene capacity developments

The world needs to continue to invest in ethylene capacity in order to meet future demand. The

rate of capacity additions relative to demand is key to setting industry cycle and profitability.

Global ethylene capacity developments

Million Tons

300

250

200

150

100

50

0

2005 2010 2015 2020 2025

Existing Capacity Firm Projects Likely Projects Hypothetical Projects

Source: Wood Mackenzie Chemicals

59woodmac.com

Global ethylene capacity additions by major region

Global ethylene capacity additions surge by 50% in 2020-2025 outlook. China and the Middle East

drive forward largest regional growth. North America sustained but lower than 2015 – 2020 period.

Global ethylene capacity additions by Global ethylene capacity additions by

major region (2015 – 2020) major region (2020 – 2025)

Million tons Million tons

55 55 51

45 45

34

35 35

25 25 21

15 13 15

9 10 8 8

6

5 3 3 3

-1 5 1

-5 -5

China

North America

Rest of world

Europe

Global

Middle East

Asia ex-China

China

North America

Middle East

Rest of world

Global

Europe

Asia ex-China

Source: Wood Mackenzie Chemicals

Source: Wood Mackenzie Chemicals

60woodmac.com

Global ethylene capacity additions by major region

Asia accounts for over 50% of ethylene project capacity in the forecast, with China over 40% alone.

Supply driven investments in North America and the Middle East account for most other projects.

Global ethylene capacity additions versus global ethylene demand by year

Million tons

16

14

12

10

8

6

4

2

0

-2

2010 2013 2016 2019 2022 2025

Rest of world Europe Middle East North America

Asia ex-China China Global demand

Source: Wood Mackenzie Chemicals

61woodmac.com

Global ethylene supply/demand balance

Global ethylene industry is entering a supply driven downturn, driven by good margins and an

increasing trend of oil/refining players further focussing on petrochemicals.

Global ethylene supply/demand balance

Million Tons Nameplate Op. Rate

300 94%

92%

250

90%

200

88%

150 86%

84%

100

82%

50

80%

0 78%

2005 2010 2015 2020 2025 2030

Capacity Production Op Rate

Source: Wood Mackenzie Chemicals

62woodmac.com

Global / regional ethylene operating rates

Global operating rates to pass below 85% in 2023 – 2025 period driven by large and sustained

ethylene capacity additions in this period following a prior easing in the global ethylene balance.

Global / regional ethylene operating rates

Nameplate Op. Rate

100%

95%

90%

85%

80%

75%

70%

2005 2010 2015 2020 2025

Global op rate Europe op rate Asia op rate US op rate

Source: Wood Mackenzie Chemicals

63woodmac.com

Ethylene economics

64woodmac.com

Chemical Feedstocks – NGLs

Integrated flow into a steam cracker for ethylene production

Ethylene

Ethane

Propylene

Steam

NGLs Fractionation Propane

Cracker

C4s

Butane

Pygas

Naphtha

Benzene

Reformer

Condensates &

Oil Refinery Reformate Toluene

Crude Oil Aromatic

Extraction

Xylenes

65woodmac.com

Oil and ethane price outlook comparison

Oil price rises more quickly than US ethane price, widening gas-based advantage for North America.

United States ethane price (Mont Belvieu)

Brent crude oil price outlook ($US/bbl)

and Henry Hub Gas Price

$/bbl $ per ton

120 700

100 600

80 500

400

60

300

40

200

20

100

- 0

2005 2010 2015 2020 2025 2005 2010 2015 2020 2025

United States Ethane (Mont Belvieu)

Brent Crude Oil Price (Nominal $/bbl) Henry Hub Gas Price

Source: Wood Mackenzie Source: Wood Mackenzie

66woodmac.com

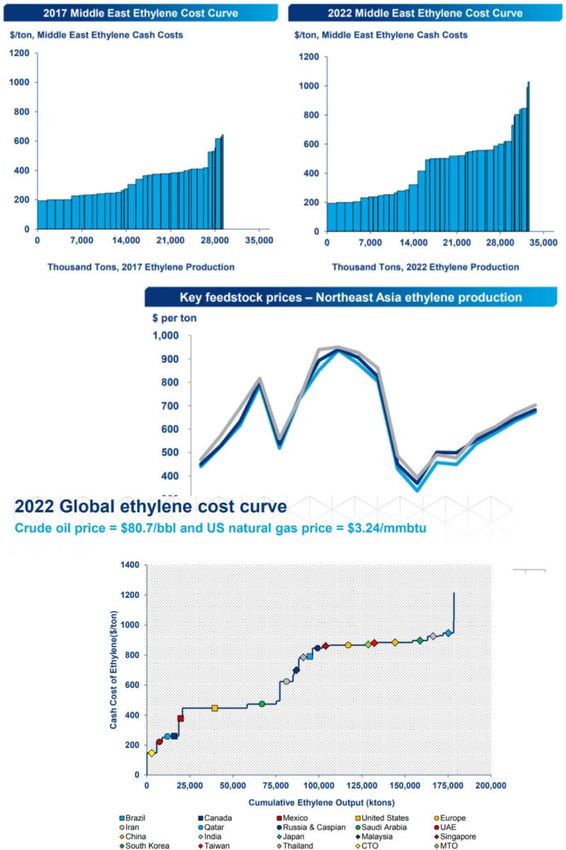

Global ethylene cost curve (2018 / 2023)

Ethylene production cost curve widens with new supply and overall cost structure (shape) is set to

steepen with increasing crude oil price (2018 = $71/bbl, 2023 = $89/bbl).

2018 Global Ethylene Cost Curve 2023 Global Ethylene Cost Curve

$/ton, Global Ethylene Cash Cost $/ton, Global Ethylene Cash Cost

1,800 1,800

1,600 1,600

1,400 1,400

1,200 1,200

1,000 1,000

800 800

600 600

400 400

200 200

0 0

0 40,000 80,000 120,000 160,000 200,000 0 40,000 80,000 120,000 160,000 200,000

Thousand Tons, 2018 Ethylene Production Thousand Tons, 2023 Ethylene Production

Source: Wood Mackenzie Chemicals Ethylene Asset Cost Tool (December 2018). Values in Nominal Dollars. 67woodmac.com

Ethylene pricing outlook

Weakness in United States ethylene prices expected for several years, as regional overcapacity situation

persists. Global ethylene prices in long-term forecast to be set by Asian polyethylene economics.

Ethylene market prices by region

Nominal dollars per ton

1,600

1,400

1,200

1,000

800

600

400

200

0

2005 2010 2015 2020 2025

US Gulf Coast - Ethylene Contract Transaction Price, Delivered

West Europe - Ethylene Discounted Contract Price, Delivered

China - Ethylene Spot Price, CFR

Source: Argus Media, PetroChem Wire, Wood Mackenzie Chemicals

68woodmac.com

Ethylene production margins and return on investment

Ethylene margins in Asia Pacific and Europe perform better than United States through to 2021. From

this point, the United States advantage is set to be restored as ethylene prices in the United States

move higher, alongside crude oil prices rising faster than ethane prices.

Integrated Ethylene-HDPE Return on

Ethylene Production Margins, by Region

Investment, by Region

Nominal dollars per ton %

1,000 60

50

800

40

600

30

400

20

200 10

0

0

2005 2010 2015 2020 2025

-10

West Europe - Region 'Leader Plant, Naphtha Feed' 2005 2010 2015 2020 2025

Margin

United States Gulf Coast - US 'World Scale Plant, West Europe, Naphtha to HDPE

Ethane Feed' Margin US Gulf Coast, Ethane to HDPE

China - 'World Scale Plant Size, Naphtha Feed' Margin China, Naphtha to HDPE

Source: Wood Mackenzie Chemicals

Source: Wood Mackenzie Chemicals

69woodmac.com

ZapSibNeftekhim (SIBUR) due online this year – what is potentially

next for ethylene investments?

Methanol-to-

olefins cluster.

Feasibility

studies in

Uzbekistan and

Kazakhstan

Source: Wood Mackenzie Ethylene Global Supply/Demand Analytics Service 70woodmac.com/chemical

woodmac.com

s

Petrochemical industry is gaining increased focus as a long-

term oil demand driver.

The overall industry is moving from top-of-cycle profitability to a

period of lower utilisation and margins – predominantly driven

by large investments exceeding near-term demand.

Ethylene is the biggest petrochemical by volume and value and

is driven by scale and costs. Strong underlying demand still

remains for major ethylene derivatives like polyethylene.

Increasing oil price coupled with lower global utilisation will

change global cost and margin structure. Large pressure will be

felt in some regions towards the middle of next decade.

The Global ethylene industry presents huge opportunities for

Russia. 4-5 world-scale ethylene plants needed on average to

keep pace with long-term demand growth.

Monetisation of both gas-based and refinery-based streams are

a possibility. Advantaged feedstock positon allows Russia to

compete on global stage in terms of product exports.

71woodmac.com/chemicals

woodmac.com

Chemicals, Polymers & Fibres Solutions

Short-term Long-term

Market Market Asset

Services Services Services

• Monthly/Weekly Reports • Semi-Annual Reports • Semi-Annual Reports

• Price/Cost/Margin Database • Price/Cost/Margin Database • Asset Operations

• Capacity/Supply/Demand Database • Capacity/Supply/Demand Database • Asset Economics

• Regular Insights • Regular Insights • Regular Insights

• Analyst Access • Analyst Access • Analyst Access

Multi-Client

Bespoke Topical Conferences

Consulting Studies & Training

• Business and Strategic Planning • N America PE Exports • Polyester: Americas, Europe

• Commercial Advisory • N America Polyester • Nylon: Americas, Europe, Asia

• Transaction Support • China CTO/MTO • Olefins: Americas

• Business Strategy • China Paraxylene • Polymers: Americas

• Litigation & Insurance Supports • Ethylene Oxide Derivatives • Living with Plastics: Europe

• Training & Workshops

72

72woodmac.com/chemicals

woodmac.com

Ethylene

Gain essential insight into supply/demand,

capacity developments and price forecasts to

understand today’s markets and tomorrow’s

trends.

Global supply demand analytics and Americas monthly

market reports

• Long-term capacity and trade data and price forecasts with

comprehensive ethylene production capacities itemized by operator,

location, technology and size

• Listing of all announced projects, including our assessment of the

projects’ timing and likelihood

• Monthly overview of supply/demand, accounting for inventories,

outages and new capacities for 18-36 months

• Price forecasts and cost-margin analysis, compared against forward

curve market expectations and inventory trends for actionable insight

• Complete volumetric and economic analysis for every regional

producing asset

• Detailed commercial analysis for the North American ethylene

outlook

73

73woodmac.com/chemicals

woodmac.com

Ethylene Asset

Cost Tool

Asset-by-asset evaluation of cost and key

production metrics can be viewed for key ethylene

technologies - not available from other providers.

• Dataset covers approximately 350 assets and projects

• Granular data on feedstocks, production volumes, costs and margins

updated twice per year

• Analyse ethylene supply using trusted price forecasts and rigorous data files

• Benchmark performance of competitor assets

• Manage risk of supply chain disruptions by understanding the position of

current and potential suppliers

• Compare your own data against our analysis for project evaluations

• Run scenarios to develop optimum business plans

74

74woodmac.com/chemicals

woodmac.com

Propylene

Use our suite of propylene research to understand

the feedstock trends and build a picture of supply/

demand of propylene’s key derivatives.

Global supply demand analytics and Americas monthly

market report

• Annual capacity, supply by technology and feedstock, demand by end-use,

trade and other key indicators for each producing/consuming country from

2005 – 2040

• Propylene prices, production costs and cash margins for US, Europe and

Asia annually from 2005 – 2040

• Propylene production assets by site, operator, capacity and technology

• Monthly overview of short term supply/demand

• Current issues and trends discussion

• Detailed commercial analysis for North American propylene, including

polypropylene outlook

75

75woodmac.com/chemicals

woodmac.com

Polyethylene

Gain a comprehensive view of global supply

and demand, price forecasts and petrochemical

feedstock trends.

Global supply demand analytics

• Economic and energy outlook

• Price forecasts and production economics

• Global capacity, production, demand and trade outlook

• Key end-use outlook: film, sheet, injection moulding, fibre and other processes

• Existing polyethylene production assets by site, operator, capacity and

technology

• Announced production projects by site, operator, capacity, technology,

anticipated timing and likelihood

• Annual capacity, supply by technology and feedstock, demand by end-use,

trade and other key indicators from 2005 – 2040

• Prices, production costs, cash margins and key assumptions for US,

Europe and Asia annually from 2005 – 2040

76

76woodmac.com/chemicals

woodmac.com

Polypropylene

Confidently forecast and plan ahead with

proprietary data and integrated analysis on the

polypropylene market.

Global supply demand analytics

• Economic and energy outlook

• Price forecasts and production economics

• Global capacity, production, demand and trade outlook

• Key end-use outlook: film, sheet, injection moulding, fibre, raffia and other

processes

• Current production assets by site, operator, capacity and technology

• Announced projects by site, operator, capacity, technology, anticipated

timing and likelihood

• Annual capacity, supply by technology and feedstock, demand by

end-use, trade and other key indicators for each producing/consuming

country from 2005 – 2040

• Polypropylene prices, production costs, cash margins and key

assumptions for the US, Europe and Asia annually from 2005 – 2040

77

77You can also read