Wealth and Insurance Choices: Evidence from US Households

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Wealth and Insurance Choices: Evidence from US Households*

Michael Gropper Camelia M. Kuhnen

University of North Carolina University of North Carolina & NBER

Abstract

Theoretically, wealthier people should buy less insurance, and should self-insure

through saving instead, as insurance entails monitoring costs. Here, we use adminis-

trative data for 63,000 individuals and, contrary to theory, find that the wealthier have

better life and property insurance coverage. Wealth-related differences in background

risk, legal risk, liquidity constraints, financial literacy, and pricing explain only a small

fraction of the positive wealth-insurance correlation. This puzzling correlation persists

in individual fixed-effects models estimated using 2,500,000 person-month observations.

The fact that the less wealthy have less coverage, though intuitively they benefit more

from insurance, might increase financial health disparities among households.

* We thank seminar participants at the Bank of Italy, the Chinese University of Hong Kong, Nova School

of Business and Economics, the 2021 Quadrant Behavioral Finance Conference, the University of North

Carolina at Chapel Hill, Tinbergen Institute, and Vienna Graduate School of Finance for their comments

and suggestions. All remaining errors are ours. Corresponding author: Camelia M. Kuhnen, University of

North Carolina Kenan-Flagler Business School, 300 Kenan Center Drive, MC #4407, Chapel Hill, NC 27599,

USA, Email: camelia kuhnen@kenan-flagler.unc.edu.

1 Introduction

Insurance products are ubiquitous. One in two US households have life insurance cover-

age, and the vast majority of households have property-related insurance coverage, such as

homeowners or automobile insurance.1 Insurance is an important part of households’ finan-

cial portfolios, yet we do not have much empirical evidence as to how people make these

insurance-related decisions. There exists a substantial body of theoretical work on this topic,

including the classical models of Mossin (1968) and Lewis (1989), or the more recent models

in Gollier (2003) and Koijen, Van Nieuwerburgh, and Yogo (2016). These theories posit

that one of the key factors driving insurance purchases is wealth. Specifically, the prediction

is that wealthier individuals will choose to purchase less insurance, as insurance products

come with a load, that is, monitoring and other fixed costs that make them costlier than

self-insurance through saving.

Empirically, there is scant evidence on what factors drive insurance purchases, and most

of this evidence is survey-based. In this paper, we examine administrative records of 63,000

people during 2015-2019, in a dataset of 2,500,000 person-month observations, to investi-

gate whether actual insurance choices match the theoretical predictions. We document that

the main prediction of standard models, namely, that wealth and insurance coverage are

negatively correlated, is not met in the data. Instead, we observe a very strong positive

relationship between a person’s wealth and the extent of coverage secured through life in-

surance and homeowners and other property-related insurance, controlling for the value of

the insured asset. For example, we estimate that a $1 increase in financial wealth leads to

an increase of 68 cents in a person’s term life insurance coverage limit, and to an increase of

$2.25 in the coverage limit of their homeowners insurance policy.2

1

Estimates of insurance coverage across the US population can be found in the LIMRA Insurance Barom-

eter Survey or the Insurance Information Institute (III) Consumer Insurance Survey. For example, according

to the III, 95% of homeowners have homeowners insurance. According to LIMRA, about half of the people

who have life insurance policies purchase them individually, and the rest are covered by group life insurance,

typically provided by employers.

2

Our analysis of life insurance demand is restricted to term life insurance (as opposed to so-called “whole”

life insurance). Term life insurance is a pure insurance contract which pays out a pre-specified amount (i.e.,

1

We then seek to understand why the data do not match the standard theoretical predic-

tions, to assess which features ought to be included in future models of household insurance

choices to account for the seemingly puzzling positive relationship between wealth and in-

surance coverage. We first show that risk tolerance is higher for wealthier households, based

on their allocation to risky versus riskless financial assets, and thus the assumption of dimin-

ishing risk aversion used in standard theories of insurance purchase is verified in the data.

Hence the positive wealth-coverage correlation is not driven by the existence of risk prefer-

ences different from what standard theory assumes. We also examine insurance premiums

paid per dollar of coverage to assess whether the wealthier households get better prices for

insurance products. We find that if anything, wealthier households pay more in premiums

per dollar of insurance coverage, potentially due to having more states of the world to which

the coverage applies.

We document that wealthier households are exposed to higher consumption, income, and

financial wealth volatility, suggesting that higher insurance coverage by these individuals is

in part a response to facing a different distribution of economic shocks, or background risk,

relative to their less wealthy counterparts. We also investigate whether wealthier households

get higher insurance coverage due to increased litigation risk. We find that the positive rela-

tionship between wealth and property insurance coverage increases in states where expected

payouts from civil lawsuits are higher, a finding akin to the result in Mahoney (2015) that

weaker bankruptcy protection increases the demand for health insurance. We document

that liquidity constraints (e.g., Baker and Yannelis (2017), Parker (2017)), financial literacy

(e.g., Brown, Cookson, and Heimer (2019), Haliassos, Jansson, and Karabulut (2020)), or

employer-provided benefits that may differ by wealth levels can also explain some of the pos-

itive wealth-insurance coverage pattern. That being said, controlling for these other mecha-

nisms, we continue to observe that cross-sectionally, wealthier people are better insured. We

the coverage limit) in the event that the insured dies during the duration (i.e., “term”) of the contract, which

is also specified ex-ante. Unlike whole life insurance, term life insurance is not treated in a tax-preferred

manner (Brown (2001)). Thus, the increasing demand for life insurance among the wealthy in our sample is

not driven by tax considerations.

2

then conduct within-person analyses using individual fixed effects, and find further support

for the positive wealth-insurance correlation we document in cross-sectional analyses.

Overall, the evidence presented here is consistent with a subset of features that appear in

classic models of insurance, such as diminishing risk aversion or, in the case of life insurance,

a bequest motive. At the same time, our analyses suggest certain features to be added in

future models of insurance choice, such as wealth-related differences in the distribution of

shocks, or in market frictions such as access to liquidity or to information about financial

products. A recent theory paper that goes in this direction is Rampini and Viswanathan

(2019), which assumes wealth-related differences in insurance pricing, and as a result predicts

that wealthier individuals are protected by insurance against a broader set of states of the

world.

Our paper contributes to the household finance literature by providing novel evidence,

based on a large administrative dataset, regarding the drivers of insurance-related choices.

In doing so, we document an unexpected fact, in light of prior theory: namely, we find that

insurance coverage is better for wealthier people. Another novel aspect of our paper is that

our data allows us to examine several mechanisms which may explain this puzzling wealth-

insurance correlation. Existing empirical evidence on the relationship between households’

wealth or income and insurance demand in the US is often limited to aggregate data or large-

scale surveys. Showers and Shotick (1994) analyze households’ expenditures on insurance

premiums (aggregating across products) using data from the 1987 Consumer Expenditure

Survey. They show that households with larger incomes spend more on insurance premi-

ums. A similar relationship between incomes and premiums is documented in the context

of life insurance by Fortune (1973) using aggregate US data from 1964 to 1971. Using data

from the 1992 wave of the Health and Retirement Survey (“HRS”), Eisenhauer and Halek

(1999) provide evidence that wealthier households purchase more life insurance coverage

than poorer households. However, the authors restrict their sample to households purchas-

ing life insurance and therefore only consider demand on the intensive margin. Fang and

3

Kung (2012) likewise use data from the HRS to analyze life insurance purchase and lapsa-

tion decisions. They find that individuals with higher incomes are more likely to purchase

life insurance. Their findings also suggest that negative income shocks may play a role in

individuals’ choosing whether to continue or lapse on existing life insurance policies.

A particularly important contribution to this literature is Armantier, Foncel, and Treich

(2018), who examine the effect of wealth on insurance choices using survey data from ap-

proximately 1,800 participants in the Survey of Consumer Expectations, and focus on auto

insurance coverage. The authors supplement the survey data from the US with administra-

tive data on auto insurance coverage from clients of a French bank. We complement this

paper by examining a larger sample of households (60,000) and by relying on administrative

data regarding several types of insurance contracts (life, homeowners, other property-related

insurance), which include information about the dollar value of coverage limits – a dimension

of insurance choice not examined in extant work due to lack of data.

Other notable papers that empirically examine insurance choices in the United States are

Sydnor (2010), Barseghyan, Prince, and Teitelbaum (2011), Koijen, Van Nieuwerburgh, and

Yogo (2016), and Jaspersen, Ragin, and Sydnor (2019). Sydnor (2010) examines households’

choice of deductible for homeowners insurance. Barseghyan, Prince, and Teitelbaum (2011)

likewise examine households’ simultaneous choice of deductibles across both home and auto

insurance and find that households’ exhibit inconsistent risk preferences across their choice of

deductibles, exhibiting greater risk aversion when choosing homeowners insurance relative to

auto insurance policies. Jaspersen, Ragin, and Sydnor (2019) conduct a experiment and show

that many structural models have poor predictive ability when it comes to explaining par-

ticipants’ insurance decisions over laboratory stakes. Similarly, Koijen, Van Nieuwerburgh,

and Yogo (2016) use data from the HRS to document another insurance-related “puzzle” in

the United States: households fail to rebalance their portfolios away from life insurance and

toward annuities as they age. Their finding is consistent with the notion that “inertia” may

play a role in households’ insurance decisions (Sydnor (2010)). This suggests that insurance

4purchase decisions do not appear to be optimal for all households. The review in Cutler

and Zeckhauser (2004) also indicates that at least in the context of life insurance, some

households may make mistakes. Working-age individuals appear to underpurchase insur-

ance, while older individuals appear to be overinsured, for example, by having life insurance

in the absence of any dependents.

A different strand of the literature has examined the effects of having certain types of

insurance on households’ economic behavior. Using data from rural China, Cai (2016) finds

that crop insurance increases households’ crop production and borrowing. Also using data

from rural China, Liu (2016) finds that access to health insurance increases households’ in-

vestments in childhood education, but does not affect consumption. Autor, Kostøl, Mogstad,

and Setzler (2019) finds that the receipt of disability insurance benefits reduces households’

labor supply. There also exists a significant literature related to health insurance and its

consequences. We do not study health insurance in this paper, as we do not have data about

this type of coverage.

2 Data

We examine households’ demand for insurance using administrative data provided by a

financial services firm. The financial services firm offers both insurance and banking services

to its customers. The data begin in September 2015, end in March 2019, and cover a sample

of approximately 63,000 individuals with 2,500,000 person-month observations. For most of

the analysis we will work with data aggregated at the person level, but we use monthly data

when assessing within-person variables, such as the volatility of an individual’s consumption

or income. We also estimate regressions including individual-level fixed effects using the data

at the person-month level.

The individuals in our sample were randomly selected from the universe of clients of

this financial institution who maintained a checking or savings account at the financial

5services firm throughout the time period. For all individuals we have information about

the monthly flows in and out of these accounts as well as the account balances. A third

party firm employed by the financial institution categorizes transactions from the checking

and savings accounts into various monthly payment types, such as credit card payments,

mortgage payments, as well as auto or other loan payments. The dataset also includes the

identity of each person’s employer if that person is working. If an individual receives income

from Social Security then that amount is labeled as such and is tabulated separately from

labor income.

We also observe the balances of investment accounts for the subset of these individu-

als who use the wealth management arm of this financial services company. Our data do

not contain the level of debts so we are unable to calculate net worth. We can however,

observe whether or not the individual has a mortgage and some other types of debt (e.g.,

automobile or other installment loans) based on their monthly payments. The types of ac-

counts for which we have balance information include checking accounts, savings accounts,

certificates of deposit, tax-qualified and non-tax-qualified brokerage accounts, individual re-

tirement accounts, mutual fund investments, and savings and annuity investments. We also

have a measure of financial assets held by the individual that is calculated by the third party

firm employed by this financial institution to provide supplementary information about the

institution’s clients; we use this measure of financial assets because it is available for all in-

dividuals regardless of whether or not they use the wealth management arm of the financial

institution.

We observe individuals’ insurance behaviors from two data sources: one source is the

monthly information on income and insurance-related expenditures (based on observing

transactions in these individuals’ checking accounts at the financial institution providing

the data), and the other contains information on financial assets and insurance coverage

limits (based on information from the insurance arm of this institution). The expenditure

data contain information on premium payments for life insurance and separately for “bun-

6dled” insurance, which we interpret as combined expenditures on property insurance such

as homeowners or automobile policies.

The data on coverage limits separate six different insurance products: life (whole and

term), homeowners, renters, automobile, valuable personal property (“VPP”), and fire in-

surance. We do not observe insurance deductibles nor do we observe the term length for

life insurance policies. We observe premiums paid to a number of different insurers based

on transactions via the checking and savings accounts; however, we only observe coverage

limits for policies issued by the financial services provider. That is, if an individual pur-

chases an insurance policy from an insurer other than the provider of our data, we observe

the premiums paid but not the coverage limit for that policy.

In practice, insurance contracts can include various provisions that allow households’

to purchase more insurance by means other than increasing coverage limits. For example,

automobile insurance contracts can include “rental car coverage,” which grants insureds the

use of a rental car in the event of a loss while the insured vehicle is being repaired or replaced.

This additional insurance coverage is reflected in higher premiums but not in an increased

coverage limit. Unfortunately, we do not observe such contract features in our data.

Our data contain monthly snapshots of demographic information for each person in the

sample, such as the zip code of residence, home ownership status, sex, age, marital status,

and whether there are children in the household. The locations of the individuals in the

sample span 50 states and the District of Columbia, for a total of 2,323 counties and 14,547

zip codes in the USA. Figure 1 illustrates the geographical dispersion of the people we

study.3 Summary statistics regarding the individuals in the sample are presented in Table

1. To eliminate the influence of extreme outliers, we exclude from our regression analyses

any individuals falling below the first percentile or above the 99th percentile in terms of

dollar-denominated covariates (e.g. financial wealth or credit card spending).

3

For 70% of individuals, we observe the complete set of 43 months (i.e. there are no gaps). We observe at

least 42 out of 43 months for 90% of individuals in our data. Gaps are treated as missing data and are not

otherwise accounted for. Some of these gaps occur due to individuals moving outside of the United States

for a period of time. We exclude observations where the individual is living outside of the United States.

7We merge in other demographic variables related to the personal and geographic charac-

teristics for individuals in our sample. Namely, we obtain information on house prices and

the legal environment based on individuals’ zip code of residence. We use the Zillow home

value index (“ZHVI”) for each month/zip code combination as our proxy for an individual’s

housing wealth, conditional on them being a homeowner. We use the Database of State Tort

Law Reforms (Avraham (2019)) to examine legal standards across different states that may

affect insurance demand. We discuss this database in additional detail below. For our anal-

yses regarding life insurance, we obtain estimates for individuals’ probability of death based

on their sex and age from the National Vital Statistic System at the Centers for Disease

Control and Prevention. Insurers are licensed and regulated at the state level, hence we use

state fixed effects in our analyses to capture regulatory and other time-invariant differences

across states.

To assess the representativeness of our sample, we compare it to the 2016 Survey of

Consumer Finances (“SCF”).4 Compared to SCF respondents, individuals in our sample are

more likely to be married, have children, and own a home. This is expected, as our sample

by construction consists of individuals who actively use banking services of a major financial

institution.

As shown in Table 2, the distribution of total income of individuals in our sample looks

similar to that of the SCF; 54% of individuals in our sample lie within the 25th and 75th

percentiles of total income in the SCF, although the highest income percentiles in our sam-

ple are smaller than those of the SCF – likely due to the SCF’s oversampling of wealthy

individuals. However, in terms of earned income and financial wealth, individuals in our

sample tend to resemble the middle of the SCF distribution. 70% of individuals have earned

income within the middle 50% of the SCF earned income distribution and 95% of individuals

have a financial wealth between the 25th and 75th percentiles of the SCF financial wealth

4

We download the public release summary extract data available at https://www.federalreserve.gov/

econres/scf_2016.htm. Dollar-denominated values in the 2016 SCF are inflation-adjusted to 2019 dollars.

We use all five implicates for each household along with the supplied survey weights to calculate summary

statistics.

8distribution.

The insurance products studied here may also cover the same assets up to a particu-

lar limit. For example, homeowners and renters policies cover losses on certain durable

goods such as furniture or electronic equipment. Individuals wishing to purchase additional

coverage for these goods would purchase VPP policies.

3 Results

3.1 Insurance coverage choices

3.1.1 Life insurance

In Table 3 we investigate the factors that influence individuals’ decision to have life in-

surance. We focus on term life insurance policies, as they constitute the vast majority

(92%) of life insurance policies we observe in the data. Moreover, while whole life insurance

comes with investment related, tax-optimization features which make it difficult to study

the insurance-related aspect of that product, term life insurance does not have these con-

founding features (Brown (2001)).5 Thus, we exclude individuals with whole life insurance

from all life insurance-related analyses. In some countries (e.g. Portugal), mortgage lenders

may require borrowers to obtain life insurance. However, mortgage lenders in the United

States typically require that borrowers obtain homeowners insurance but do not require life

insurance.

The dependent variable in Table 3 is an indicator for whether at any time during our

sample the individual had a life insurance policy. We use Lewis (1989) as our theoretical

framework for modeling life insurance demand. According to that model, the demand for life

5

Insurance and financial advice websites (e.g. https://www.policygenius.com/life-insurance/

whole-life-insurance/ and https://www.ramseysolutions.com/insurance/whole-life-insurance)

note the poor investment properties of whole life insurance and describe whole life policies as appro-

priate for higher income earners for tax purposes. Anagol, Cole, and Sakar (2017) provide evidence

from India that whole life insurance policies are dominated by a combination of term life contracts and

traditional savings accounts. Term life insurance is not given any tax-preferential treatment (see, e.g.

https://www.policygenius.com/life-insurance/is-life-insurance-taxable/).

9insurance depends on the level of consumption needed by the individuals benefiting from the

policy, for example, spouses and children. In the Lewis (1989) framework, this consumption

is the expected value of spending by these beneficiaries over the years left until the time

when the children have sufficient income of their own. Life insurance is therefore used to

guarantee that if the income of the individual is lost due to death, the same spending by

beneficiaries would occur as in the case when the individual stayed alive and earned their

income.

In our analysis, we assume that beneficiaries become financially independent when the

insured person reaches age 65, but other age thresholds lead to similar results. We calculate

the net present value of the dependents or beneficiaries as the discounted value of a stream of

annual credit card spending equal to that observed in the individual’s financial records during

our sample, over the number of years left until the person reaches 65. In this calculation

we use a discount rate r equal to 1%, but the choice of r does not qualitatively change

the results. Since consumption by beneficiaries also includes payments to creditors if the

household has a mortgage or other consumer loans, we include among explanatory variables

in Table 3 indicators for whether the household has such liabilities.

As shown in Table 3, the canonical predictions regarding the effect of the future expected

spending of dependents on whether the person has life insurance are met in the data. A higher

expected spending need of spouses or children leads to a significantly higher probability that

an individual has life insurance, whether or not that expected spending captures the credit

card expenditures we observe for this person on average in the years of the sample, or

whether it captures mortgage payments or payments on other loans that the individual has

during the sample, which most likely will need to continue to be paid in the event this

individual dies. The estimated effects are both statistically significant and economically

meaningful. Increasing the expected credit card expenditures by $100,000 (i.e. increasing

the value of the consumption stream to be insured) is associated with between a 0.43 to

0.72 percentage point increase in the probability of having life insurance depending on the

10specification. Simultaneously having a mortgage and a dependent is associated with an

increased likelihood of having life insurance by between 13 and 14 percentage points. Having

a dependent and non-mortgage loan (e.g. an automobile or installment loan) increases the

likelihood of owning life insurance by between 2 and 4 percentage points. These effects are

economically sizeable, given that the unconditional probability for a person in our sample

to have term life insurance is 36% (see Table 1).

All else equal, the model in Lewis (1989) also predicts that having life insurance is

more likely for a higher probability of death and a higher relative risk aversion coefficient.6

The first of these predictions can be verified in our data, as we are able to merge in for

each individual in the sample the probability of death in the subsequent year, based on

the person’s age and gender. These probabilities are estimated by the CDC and represent

averages across populations in the US that fall into each gender and age subcategories. These

estimates, however, are not tailored based on the specific health status, for instance, of the

particular individuals in our sample. As the theory predicts, we find a strong and positive

correlation between the indicator variable for whether the person has life insurance and their

probability of death in the next year (or, equivalently, a negative correlation between having

life insurance and the person’s expected remaining life span).

The result that does not conform to the Lewis (1989) theory is the positive and significant

effect of the person’s financial wealth on the probability that they have life insurance. In-

creasing the financial wealth of a household by $100,000 is associated with approximately a 12

percentage point increase in their probability of owning life insurance. Housing wealth sim-

ilarly is positively correlated with having life insurance (controlling for having a mortgage),

with an increase of $100,000 in the value of the home corresponding to a 0.93 percentage point

increase in the probability of having term life insurance. The fact that wealth is a positive

predictor of insurance coverage is a clear violation of the prediction in models of insurance

6

A higher load also lowers the probability of having life insurance (Lewis (1989)). Here we assume that

the load (i.e., the extent of monitoring costs) is similar across individuals, in the absence of any evidence to

the contrary. To the extent that load values might be different for people residing in different parts of the

US, the inclusion of state fixed effects in the analysis will control for these differences.

11choice, with the exception of Rampini and Viswanathan (2019). We will later investigate

whether the pattern we document is driven by the assumptions in that model, specifically,

the assumption that wealthier individuals face more favorable pricing of insurance and thus

purchase more insurance than poorer individuals.

In Table 4 we examine the factors driving the life insurance coverage limit for individuals

in our sample. The dependent variable is equal to the coverage limit for term life insurance

policies held by each of these individuals. For those without such policies during the sample

period, the dependent variable is equal to zero. We investigate the factors that have been

proposed theoretically to drive the extent of life insurance in models such as Lewis (1989).

We find that for most of these factors, the data line up with the theory. An $1 increase

in the insured consumption stream is associated with a $0.04 increase in the magnitude of

life insurance coverage. Simultaneously having a dependent and mortgage is associated with

increased life insurance holdings of $32,000. The coefficient on the dependent/non-mortgage

loan interaction is no longer significant, potentially indicating that non-mortgage loans drive

the extensive margin of life insurance demand but not the intensive margin. Analogously,

the sign on the coefficient estimate for an individual’s probability of death switches from

positive to negative. This reflects that life insurance ownership is more likely among older

individuals but the magnitude of coverage decreases as individuals get older.7

However, we observe that wealth has the opposite effect on life insurance coverage limits

relative to the theoretical predictions. Wealth, whether financial or housing-related, is a

significant and positive predictor of the extent of life insurance coverage. In the entire

sample (those who have no term life insurance and thus have a coverage limit of zero dollars,

and those who have this product, for whom we know the coverage limit), we estimate that

an increase of $1 in their financial wealth corresponds to an increase of $0.68 in the life

7

We do not explicitly examine life cycle effects in the ownership of life insurance. But in unreported

analyses, we use a series of age bin indicator variables and observe a “hump-shaped” pattern in terms of

predicted life insurance coverage over the life cycle. See Koijen, Van Nieuwerburgh, and Yogo (2016) and

Heimer, Myrseth, and Schoenle (2019) for examples of life cycle effects in households’ insurance and savings

decisions.

12insurance coverage limit. For housing wealth, a $1 increase leads to an increase of $0.07 in

the coverage limit. Restricting the sample to just those people who have term life insurance

(see the last column of Table 4, the effects of a $1 increase in wealth on the coverage limit

are $1.51 in the case of financial wealth, and $0.20 in the case of housing wealth.

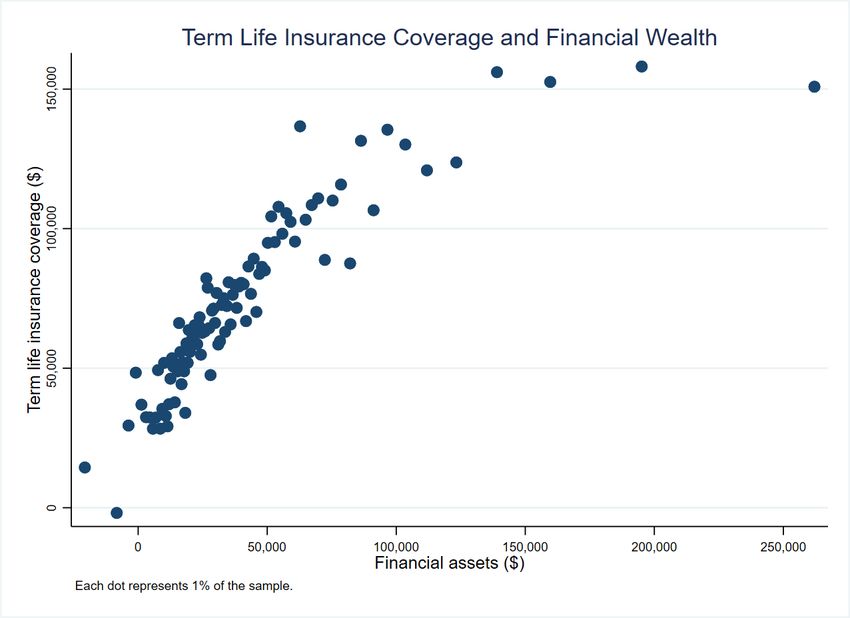

Figure 2 shows that the positive correlation between financial wealth and the extent of

term life insurance coverage is present for all levels of financial wealth. Figure 2 is a binned

scatter plot. Binned scatter plots are a convenient way to visualize regression results; they

plot the residuals from two multivariate regressions to visualize the two-dimensional relation-

ship between the dependent variable and independent variable of interest in a multivariate

regression. In this figure, the residuals from a regression of term life insurance coverage on

all explanatory variables except for financial wealth are plotted against the residuals from a

regression of financial wealth on all other explanatory variables. The data are then grouped

into one hundred bins and the mean of the residualized values are plotted against each other.8

The slope of a hypothetical least squares line plotted through Figure 2 is identical to the

coefficient estimate on financial wealth in the multivariate regression results in the fourth

column of Table 4. For an example of binned scatter plots used in a similar manner, see

Chetty, Friedman, and Rockoff (2014).

In the analysis presented in that figure, just as in Table 4, we control for the insured

dependents’ expected spending, the insured person’s own probability of death in the subse-

quent year, their housing wealth, and state fixed effects. We see that the correlation between

life insurance coverage and financial wealth becomes smaller for higher levels of wealth, but

it remains positive.

This pattern in Figure 2 sheds light on an alternative hypothesis for why those with

lower wealth buy less life insurance – namely, that low wealth or low income individuals

have access to certain types of social insurance (i.e., government-provided health insurance,

8

We use the user-written Stata package binscatter2 to automate the binned scatter plot procedure. Note

that values of values of financial wealth on the horizontal axis may be negative when individuals have lower

financial wealth than would be predicted (i.e. the residualized financial wealth values from the regression

are negative), given their values of the other covariates in the fourth column of Table 4.

13food stamps, etc., that may help one’s dependents to fare well if the bread winner in the

family dies). If that were true, then these individuals would have less of a need to buy

life insurance privately. This hypothesis, however, would imply that in Figure 2 we would

observe a kink in the coverage-wealth relationship. Coverage should be zero or close to zero

for the lowest levels of wealth, and increase steeply after some wealth level for which those

social insurance benefits no longer are accessible. As the figure shows, however, there is no

such kink in the functional form of life insurance coverage as a function of wealth.

3.1.2 Property insurance

We examine the drivers of participation in property-related insurance markets in Table 5. To

a large extent, participation is determined by the legal environment. In the US, automobile

owners must have car insurance.9 Home owners with a mortgage must have homeowners

insurance. Other types of property-related insurance policies are available to consumers, but

their uptake is not required by law. These include, for example, renters insurance, valuable

personal property, boat, or fire insurance. For all property-related policies, the extent of

coverage is determined by the consumer, even though the participation (e.g., whether one

has homeowners insurance) is automatically decided by the legal environment. Hence, the

variable of most interest is the coverage limit, rather than the decision to have coverage at

all.

We first examine whether the individuals in our sample have any of these types of

property-related policies, and then focus on homeowners insurance, as it is related to the

asset that makes up the largest amount of net wealth of most US households. We later on

examine the coverage limits for these policies. We limit our data to homeowners when es-

timating regressions that examine the coverage limit of homeowners insurance policies (i.e.,

in those regressions we exclude renters, as those policies do not apply to renters).

9

There are two states with exceptions to this rule: New Hampshire and Virginia. In both of these states,

automobile owners may forego insurance by paying a fee to the state government. We find that individuals

in our sample residing in these states are not less likely to own auto insurance than residents of other states.

14In Table 6 we investigate whether the extent of coverage through homeowners insurance

policies varies with wealth as in theoretical predictions. Prior models (see Schlesinger (2013)

for a review) deliver clear predictions for the dollar value of coverage purchased. Specifically,

all else equal, more insurance in absolute terms will be purchased by individuals faced with a

higher probability of loss, higher risk aversion, and lower wealth (Schlesinger (1981)). More-

over, Mossin (1968) predicts that the fraction of the value of the home insured decreases with

the ratio of non-housing related wealth to the value of the home. That is, if the insured asset

does not represent much of the value of the overall wealth of the person, then it should be

covered less through insurance. As the results in the table show, these empirical predictions

are contradicted in the data. We find that individuals with higher financial wealth, and

those with higher housing wealth, that is, people owning more expensive homes, will have

higher coverage limits in their homeowners insurance policies. A $1 increase in financial

wealth is associated with a $2.25 increase in the homeowners insurance coverage limit and

a $1 increase in the value of the home is associated with a $0.37 increase in homeowners

insurance coverage. Moreover, we find that people for whom their financial wealth is more

substantial relative to their housing wealth have homeowners insurance policies that cover

a higher fraction of the value of the home, which is opposite to the prediction coming from

standard insurance models. Specifically, we find that a one percentage point increase in the

ratio of financial wealth to housing wealth corresponds to an increase of 3.25 percentage

points in the ratio of homeowners insurance coverage limit to the value of the home.

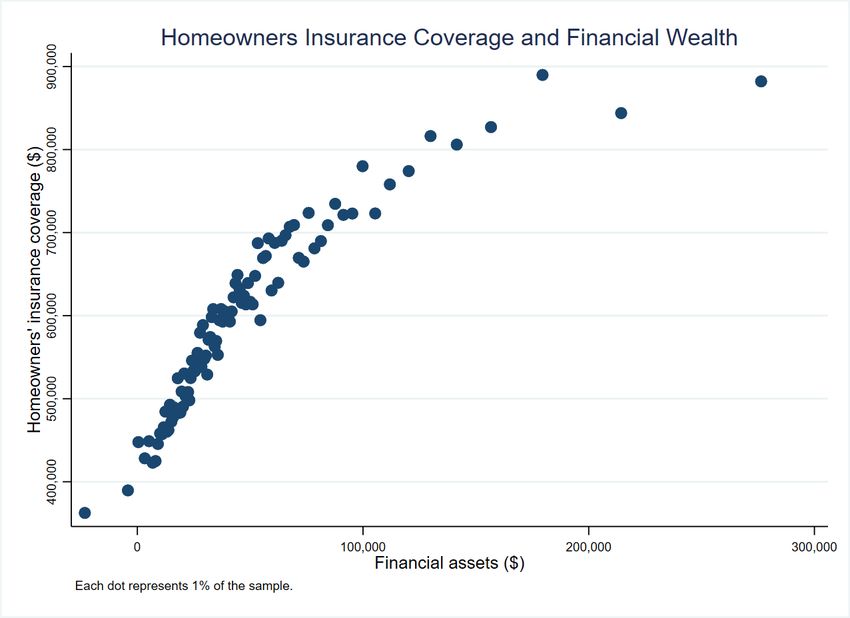

Figure 3 shows that the positive correlation between financial wealth and the extent of

homeowners insurance coverage, controlling for the value of the home insured, is present for

all levels of financial wealth. The correlation becomes smaller for higher levels of wealth,

but it remains significantly greater than zero. As in the case of life insurance, the lack of

a kink in the relationship between coverage and wealth suggests that the existence of social

insurance benefits is not the driver of the positive correlation between these two variables.

153.2 Why are wealth and insurance coverage correlated?

3.2.1 Risk preferences

Standard models of insurance or portfolio choice are built on the assumption of decreasing

(absolute) risk aversion. While unlikely, it might be that in our data the wealthier are more

risk averse, which would lead to empirical patterns of insurance choice opposed to what

these models predict. We can test this explanation by examining the extent to which the

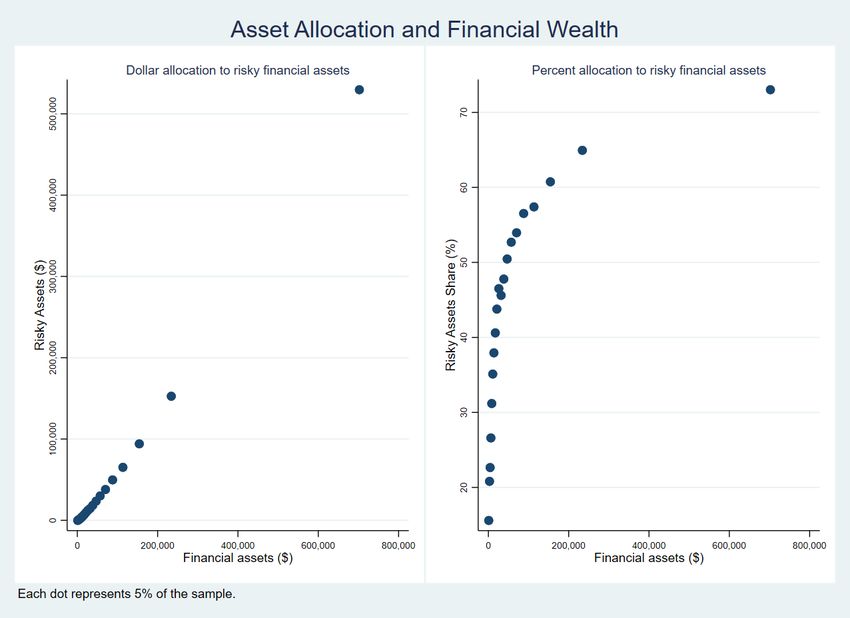

individuals in our sample allocate their wealth to risky financial assets. We calculate the

dollar amount of funds allocated by each individual to risk-free accounts, including savings,

checking, and certificates of deposit. We also calculate the dollar amount of funds allocated

by the same person to risky assets, through investment accounts offered by the financial

institution providing the data. These accounts include regular brokerage accounts as well

as tax-advantaged investment accounts, and contain investments in mutual funds, stocks,

and bonds. We plot in Figure 4 the dollar amount (left panel) as well as the share (right

panel) allocated to risky assets as a function of the total amount invested with this financial

institution across safe and risky financial assets. It is clear from the figure that risk tolerance

increases with wealth, as typically assumed by the theory, and documented by prior papers

using survey or administrative data on portfolio allocations (see Guiso and Sodini (2013) for

an overview of that literature).

Theoretically it has been shown that increased ambiguity aversion generally increases the

demand for insurance (Alary, Gollier, and Treich (2013)), which is intuitive, as increases in

ambiguity aversion have effects similar to increased pessimism. For ambiguity aversion to

explain the positive wealth-insurance correlation we document in the data, it must be that

ambiguity aversion increases with wealth. Baillon and Placido (2019) conduct an experiment

investigating the wealth-ambiguity preferences relationship. They find no clear patterns in

terms of increasing, decreasing, or constant ambiguity aversion attitudes toward wealth.

While we do not have proxies in our data that measure ambiguity-related preferences, we

16rely on this prior work to argue that most likely our results are not driven by the wealthy

being more ambiguity-averse than the less well off.

3.2.2 Prices

The model in Rampini and Viswanathan (2019) predicts that households’ insurance expendi-

tures decrease with income, because an increase in households’ income under their assumed

income process lowers the chance of occurrence of low income realizations in the future. It is

important to keep in mind that wealth and income are the same concept in that model, where

households use income in a period to consume or to buy insurance through Arrow-Debreu

claims. In that setting, buying insurance is the only means to save for the future.

While the model is stark, it does rely on an assumption that seems reasonable: insurance

for less likely future states should be cheaper. Since higher income individuals are assumed

to have a lower chance of having a bad income shock in the future, getting insurance against

those bad states should be cheaper for them than for people who are currently in a lower

income state. In practice, this implies that insurers re-price insurance contracts in response

to changes in insureds’ income. So far there is no documented evidence in the literature that

insurers take individuals’ income into account when pricing life insurance policies, or other

insurance products. Our data allows us to study whether prices for coverage in fact vary

across people based on their income or wealth.

We investigate this pricing channel in the analysis in Table 7 and Table 8, for life and

property insurance, respectively. The dependent variables in the OLS regressions in these

tables are the prices (premiums) paid per dollar of coverage for life insurance, and for property

insurance. The coefficient estimates on the coverage limits in Tables 7 and 8 are negative

and significant. This is unsurprising, as part of the premiums paid by insureds are to cover

monitoring and other fixed costs paid by the insurer, implying the potential for economies

of scale with respect to coverage on individuals.

We find that, controlling for the amount and probability of loss insured, individuals

17with higher financial wealth pay higher prices for life insurance. A similar effect appears

if instead of financial wealth we use the person’s average annual income during the sample

period: higher income individuals pay higher premiums for a certain level of life insurance

coverage. This is opposite to the theoretical mechanism in Rampini and Viswanathan (2019).

A possible reason could be that wealthier individuals choose term life insurance policies

that have longer term, that is, offer protection (for a given level of coverage limit) over more

years than the policies secured by less well-off individuals. This would mechanically lead

to the wealthier paying higher premiums per dollar of coverage. This scenario, however,

is also one where the wealthier get more coverage, in the sense of the time frame covered,

aside from the dollar limit of coverage. Hence, the data indicate one of two things: either

the wealthy secure better coverage in terms of term, or they face higher prices compared

to others. Neither one of these implications conforms to the classic theoretical models of

insurance, but the mechanism in Rampini and Viswanathan (2019) might still be valid, if

indeed the wealthy are insured for longer terms.10

3.2.3 Volatility of consumption, income, or wealth processes

Another possible reason why wealthier people get higher insurance coverage is that they

might face more background risk. Perhaps the shocks to future consumption, income, or

wealth faced by the wealthier households come from a wider distribution, compared to the

shocks facing less wealthy households. As shown theoretically by Fischer (1973) and Rampini

and Viswanathan (2019), increasing income volatility can increase the demand for insurance,

whether it is life- or property-related. Similarly, consumption volatility may be higher for the

wealthier, and hence insurance may be more important for these individuals. More generally,

an independent, uninsurable background risk causes individuals to increase their demand for

10

Analogously, wealthier individuals might purchase property and casualty insurance products with addi-

tional contract features such as rental car coverage while holding the coverage limit constant (and thus pay

a higher premium). Again, this would suggest that the wealthier are better insured than the less wealthy,

which is the puzzle we focus on in this paper.

18insurance (see e.g., Gollier and Pratt (1996)).11 The effects of non-independent background

risk on households’ demand for insurance naturally depends on the combination of pref-

erences and the relationship between the insurable and background risks. See Schlesinger

(2013) for further discussion on the effects of both independent and non-independent back-

ground risk on insurance demand.

We examine this volatility-related mechanism in the analysis in Table 9 and we find that

in general, consumption, income, and wealth are more volatile in absolute terms (i.e., dollar

amounts) for individuals with higher financial or housing wealth. We calculate annualized

volatilities for each individual by taking the standard deviation of the monthly values (across

time) and multiplying by the square root of 12. The estimates in Table 9 show that a $1

increase in financial wealth is associated with a $0.04 increase in the annualized volatility of

consumption. The wealthy also have more volatile income processes as well, a $1.00 increase

in financial wealth is associated with a $0.22 increase in the annualized volatility of income.

Therefore, it is possible that one driver of the positive link we observe between wealth and

insurance coverage is the increased background risk of more affluent households.

To investigate this further, we add these measures of background risk as additional ex-

planatory variables in our prior models where the dependent variable is the extent of life

or homeowners insurance coverage. This analysis is presented in Table 10. As predicted

by theory, the volatility of consumption or income are positive and significant predictors

of insurance coverage limits. That is, people faced with more background risk have more

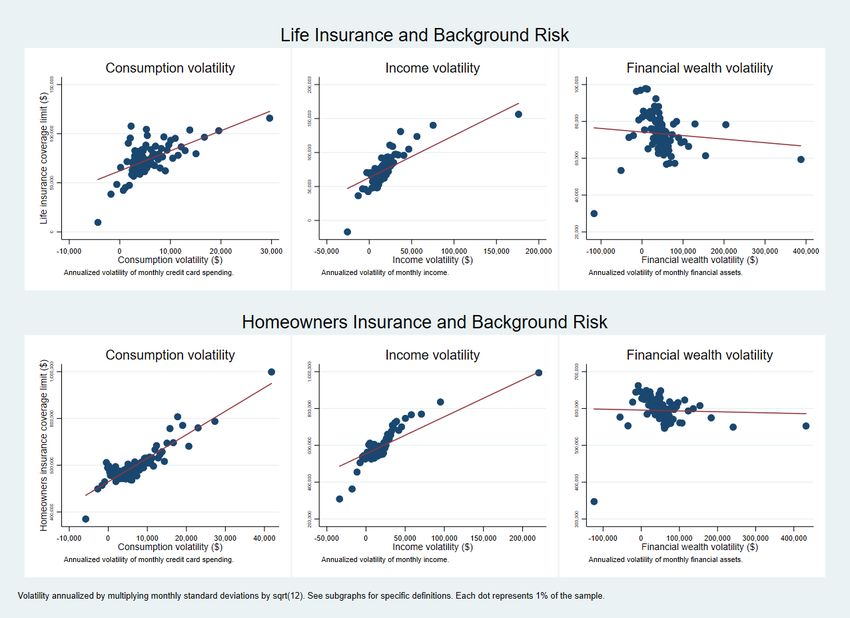

insurance coverage. As shown in Figure 5, these results are obtained throughout the entire

distribution of consumption or income volatility. However, while controlling for background

risk changes slightly the effects of financial or housing wealth on insurance coverage limits

relative to those estimated in our baseline models in Table 4 and Table 6, these effects re-

main positive, statistically and economically significant. Therefore, our evidence indicates

11

Risk aversion is not sufficient for this result. For example, insurance demand with CARA preferences is

unchanged by introduction of an independent background risk. However, a sufficient condition is so-called

“standard risk aversion,” which is related to prudence (the third derivative of the utility function). CRRA

preferences, for example, exhibit “standard risk aversion.”

19that the higher background risk faced by wealthier individuals can not by itself explain why

the wealthier get more insurance coverage.

3.2.4 Legal risk

It is also possible that the probability or extent of loss for any insured asset – be it future

income (through life insurance), or property (through homeowners insurance, for example) –

may be higher for wealthier individuals. In the case of property-related risk, this may be due

to the legal environment. In some U.S. states it is easier than in others for an individual to

be subject a costly lawsuit if somebody gets injured on this person’s property, for example.

This is why many homeowners insurance policies in the U.S. cover not only the cost of the

structure of the home, but also expenses incurred in such lawsuits. Therefore, the wealthy

may have to purchase larger amounts of insurance because they may be liable for payments

commensurate with the value of their total wealth, and not necessarily limited to the value of

the property insured. In other words, the distribution of potential losses depends on wealth.

Note that for life insurance, however, this legal risk channel is unlikely to apply, as the

probability of death is unlikely to increase with the person’s wealth. If anything, as shown

by Chetty, Stepner, Abraham, Lin, Scuderi, Turner, Bergeron, and Cutler (2016), higher-

income individuals have longer life expectancies, which should lower the demand for life

insurance. Hence, we focus on demand for homeowners and other property and casualty

insurance products when we examine the legal risk channel.

While we cannot directly observe the correlation between individuals’ financial wealth

and their propensity to be sued, we can examine the legal risk mechanism by examining

the connection between wealth and insurance demand in different litigation risk regimes. If

legal risk increases with wealth and drives homeowners insurance purchases, the relationship

between wealth and insurance coverage should be stronger in higher risk jurisdictions relative

to lower risk jurisdictions.

To investigate this legal risk channel, we use the Database of State Tort Law Reforms

20(“DSTLR”, Avraham (2019)). The DSTLR was developed for the purpose of examining the

effects of tort law on medical malpractice insurance. The database contains information on

eleven different aspects of tort law for each state in a particular year; we focus on two aspects

that may affect the expected losses due to litigation. The first of these two aspects are rules

governing the maximum amount that can be awarded to a plaintiff in litigation through

caps on damages. The second concerns the percentage of a damages award can be shared

with plaintiffs’ attorneys (a “contingency fees”).12 We combine these two aspects of tort

law with an indicator variable measuring whether or not a particular state has an unlimited

homestead exemption. An unlimited homestead exemption ensures that a defendant’s home

is off-limits in terms of covering the damages award in a lawsuit.13 There are seven such

states in the USA. We then split the states into those that have above-average litigation risk

and those with below-average litigation risk.14 Intuitively, individuals living in states with

more litigation risk should, all else equal, seek higher insurance coverage, especially if they

have higher wealth, which could increase the chance of facing a lawsuit.

In Table 11 we examine the wealth-insurance relationship in a series of regressions where

the dependent variable is the amount of homeowners insurance, or overall property insurance

purchased by individuals. The coefficient estimates in columns 1 and 3 indicate that living

in a state with high litigation risk is associated with a $45,000 increase in homeowners insur-

ance coverage and a $55,000 increase in coverage across all property and casualty insurance

12

Contingency fee rules often take the form of lowering the portion of a damages’ award that can be given

to the attorney at various thresholds. By way of example, the rule governing contingency fees in Illinois

(effective until 2013) specified that contingency fees may not exceed 33% of the first $150,000; 25% of the

next $850,000; and 20% of any amount over $1,000,000. Such contingency fee rules reduce the marginal

returns to effort on the part of plaintiffs’ attorneys and thus may be expected to lower expected payouts by

insurers.

13

Mahoney (2015) studies such exemptions in the context of health insurance, finding that the ability to

shield asset values and discharge medical debt in bankruptcy affects insurance decisions, lowering demand

for insurance when agents can shield assets with bankruptcy exemptions.

14

In our sample, the average individual lived in a state with two of the three aspects of litigation risk.

Therefore we split the sample into whether or not a person lives in a state with all three elements of increased

legal risk, or only one or two (all states had at least one “riskier” aspect of tort law or no homestead

exemption). Our conclusions remain the same under alternate definitions of legal risk using other aspects

of the DSTLR such as caps on damages related to pain and suffering or so-called “comparative fault” tort

reforms.

21products in our data. In columns 2 and 4, we find a positive and significant interaction term

between a person’s financial wealth and the high legal risk indicator; an additional $1.00 of

financial wealth is associated with an increase of $2.15 in homeowners insurance in a low-risk

state, versus $2.70 ($2.15 + $0.55) in a high-risk state. The significance of the interaction

term suggests that litigation risk is a driver of individuals’ demand for homeowners or prop-

erty insurance. We interpret this finding as suggestive evidence that legal risk drives some

of the demand for property and casualty insurance, though perhaps only for individuals in

the upper tail of the wealth distribution.

3.2.5 Liquidity constraints

It may be that individuals, particularly those with low income and low financial wealth, are

liquidity constrained and are unable to afford insurance due to other financial commitments.

Generally, the prior literature has found that liquidity constraints reduce household spend-

ing (e.g., Zeldes (1989); Johnson, Parker, and Souleles (2006); Baker and Yannelis (2017)),

particularly for households with low financial sophistication (Parker (2017)).15 Buying in-

surance, however, is not simply spending. Rather, it is a risk-mitigation strategy used for

consumption smoothing. As a result, as shown theoretically in Gollier (2003) and Ericson

and Sydnor (2018), insurance products would be most sought after by individuals who are

most liquidity constrained (particularly products involving the smooth payment of small

premiums over time rather than the payment of one large lump sum premium).

Empirically we find that in fact those who are most liquidity constrained have lower

insurance coverage. We measure liquidity constraints for each individual using two separate

measures. The first measure of liquidity constraints is what we refer to as the credit ratio,

calculated as the monthly expenditures on the credit card provided by the financial insti-

15

While important, liquidity constraints are not the only factor impacting spending responses to income

or other shocks. Prior work has provided evidence that spending decisions are also driven by present bias

(Olafsson and Pagel (2018), Ganong and Noel (2019)), mental accounting, anchoring, or other heuristics

(Baugh, Ben-David, Park, and Parker (2021); Keys and Wang (2019); Baugh and Wang (2018)), as well as

by the lack of financial literacy (Jørring (2020)).

22tution divided by the credit limit on the card.16 The second measure, which we refer to as

the debt-to-income ratio, is calculated as the ratio of short-term debt, which is the sum of

monthly mortgage, auto, and installment loan payments, to total income.

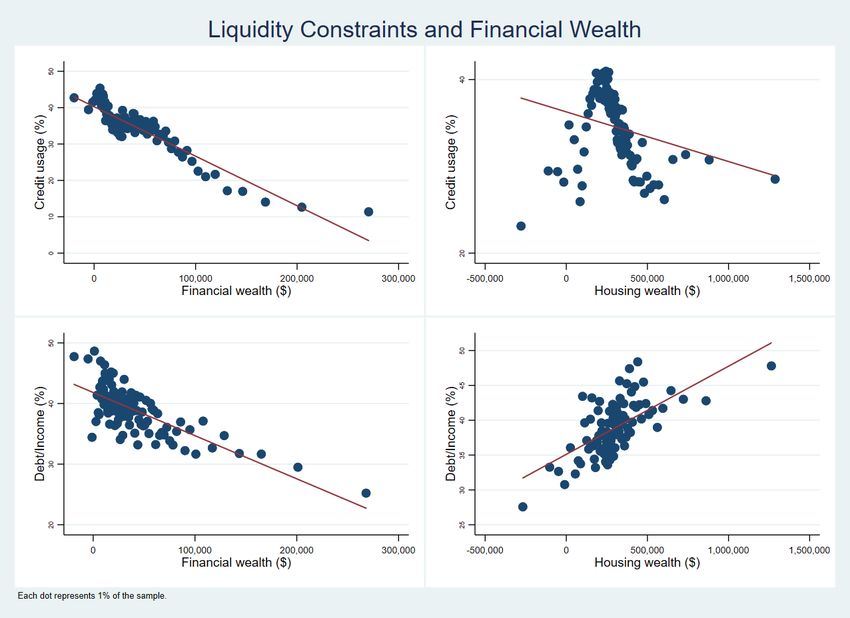

Figure 6, as well as Table 12 show generally that credit usage as well as the debt-to-income

ratio decrease with financial wealth. For housing wealth we observe that for those in the

upper 90% of the distribution of wealth there is generally a decreasing relationship between

housing wealth and credit usage. The debt-to-income ratio increases with housing wealth,

controlling for financial wealth. Since our housing wealth measure for homeowners is the

Zillow home value index, without accounting for the outstanding principal on the mortgage

on the house, this relationship can simply capture the fact that mortgage payments are larger

if, all else equal, the home is worth more. But it may also be the case that leverage is higher

for those with more assets in place. We examined this by looking at the universe of people

who do not have a mortgage on the house, or who are renters, and among those individuals,

we continue to observe a positive and significant correlation between housing wealth and the

debt-to-income ratio (albeit about 50% smaller in magnitude).

While these results show that wealth and liquidity constraints are related, the regression

models in Table 13 indicated that even after controlling for a person’s credit use ratio or

their the debt-to-income ratio, we continue to observe a strong and positive correlation

between wealth (financial or housing-related) and the extent of life insurance and homeowners

insurance coverage. The estimates in Table 13 indicate that after controlling for the credit

usage as a measure of liquidity constraints, a $1.00 increase in financial wealth is associated

with a $0.67 increase in life insurance coverage (as opposed to $0.68 in Table 4, column 4)

and a $2.22 increase in homeowners insurance coverage (as opposed to $2.25 in Table 6,

column 1). In other words, liquidity or the lack thereof, can not explain away the puzzling

16

Over 95% of individuals utilize credit cards issued by the financial institution providing the data at

some point in our sample. The median monthly credit card expenditure is approximately $1,600. We are

unable to observe whether or not an individual carries a balance on the credit card from month-to-month

and therefore cannot distinguish between individuals who rollover credit card debt versus those who simply

spend close to the limit in each month.

23You can also read