TUNISIA ECONOMIC MONITOR - Navigating Out of the Crisis Spring 2021 - World Bank Documents

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Navigating Out

Middle East and North Africa Region

Spring 2021

of the Crisis

MONITOR

TUNISIA ECONOMIC

Tunisia

Economic Monitor

Navigating Out of the Crisis

Spring 2021

Middle East and North Africa Region

© 2021 International Bank for Reconstruction and Development / The World Bank 1818 H Street NW Washington DC 20433 Telephone: 202-473-1000 Internet: www.worldbank.org This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy, completeness, or currency of the data included in this work and does not assume responsibility for any errors, omissions, or discrepancies in the information, or liability with respect to the use of or failure to use the information, methods, processes, or conclusions set forth. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. Nothing herein shall constitute or be construed or considered to be a limitation upon or waiver of the privileges and immunities of The World Bank, all of which are specifically reserved. Rights and Permissions The material in this work is subject to copyright. Because The World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given. Any queries on rights and licenses, including subsidiary rights, should be addressed to World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: pubrights@worldbank.org. Cover photos used with the permission of ShutterStock.com. Publication design and layout by The Word Express, Inc.

TABLE OF CONTENTS

Abbreviations and Acronyms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

Acknowledgements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .vii

Addendum to the Tunisia Economic Monitor – Spring 2021 . . . . . . . . . . . . . . . . . . . . . . . . . . . . viii

Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ix

Résumé Exécutif . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xi

الملخص التنفيذي. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xv

1. Recent Economic Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Growth and Employment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

The Socioeconomic Impact of COVID-19 on Household Welfare . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

The External Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Fiscal Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10

Monetary Policy and Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

2. Outlook and Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Special Focus: Assessment of the Digital Transition in Tunisia . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Why Digitization? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19

Tunisia’s Digital Strengths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Tunisia’s Missed Opportunities and Areas of Improvement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

Recommendations to Accelerate the Digital Transformation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

List of Figures

Figure 1 Impact of COVID-19 Was Higher than Neighboring Peers… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Figure 2 …while Policy Stringency Was More Relaxed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Figure 3 Nearly All Sectors Contracted in 2020… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Figure 4 …with Sharper Declines than Regional Peers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

iiiFigure 5 International Flights Recovered Only Temporarily . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Figure 6 Energy and Mining Sectors Still Far Below Potential . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Figure 7 Household Reported Worsening in Living Standards… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Figure 8 …Particularly among the Lowest Income Groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Figure 9 Varying Reasons for the Decline in Business Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

Figure 10 The Deterioration of Welfare Felt among Everyone . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Figure 11 Net Exports Shrinks, Moderating the Trade Deficit... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

Figure 12 ...Mainly Caused by Savings on Energy Imports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Figure 13 Current Account Deficit Still Wider than Peers... . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 14 …yet Borrowing Still Largest Source of Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Figure 15 A Narrow Current Account Appreciates the Dinar . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 16 Less Pressure on CA Boosts FX Reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Figure 17 Fiscal Deficit Balloons Public Debt to Record Levels… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Figure 18 …while Subsidies Continue to put Pressure on Budget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Figure 19 Despite Rising Concern, Public Wage Bill Grows… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 20 …with Interior and Defense Shares Doubling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Figure 21 Lower Inflation Provides Space for Rate Cuts… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Figure 22 …yet Most Credit is Soaked Up by the Public Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .13

Figure 23 Output Will Not Recover Before 2024… . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

Figure 24 …due to the Sharper Contraction in 2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16

Figure 25 Maturity of the Pillars of the Digital Economy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

List of Boxes

Box 1 Building a Green, Resilient, and Inclusive Agro-Food Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Box 2 How Did COVID-19 Affect Regional Growth? Monitoring Economic Activity

Using Night-Time Lights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .5

iv TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISISABBREVIATIONS AND

ACRONYMS

AMG2 Assistance Médicale à tarif réduit M3 Broad Money

CBT Banque Centrale de Tunisie (Central Bank MNO Mobile Network Operators

of Tunisia) MVNO Mobile Virtual Network Operator

EFF Extended Fund Facility NPL(s) Non-performing loan(s)

GDP Gross Domestic Product OIT Tunisian Order of Engineers

GIPAC Groupement Interprofessionel des Produit ONAGRI Observatoire National de l’Agriculture

Avicoles et Cunicoles ONH Office National de l’Huile

GIVLAIT Groupement Interprofessionel des Viandes PNAFN Programme national d’aide aux familles

rouges et du Lait nécessiteuses

IFAD International Fund for Agricultural Q-o-Q Quarter over Quarter

Development RFI Rapid Financing Instrument

IMF International Monetary Fund SOE(s) State-owned Enterprise(s)

INS Institut National des Statistaiques STEM Science, Technology, Engineering, and

IRESA Institut de la Recherche et de Math

l’Enseignement Supérieur Agricoles STIR Société Tunisienne Des Industries de

ISP Internet Service Provider Raffinage

LMICs Low- and Middle-Income Countries US$ United States Dollars

vACKNOWLEDGEMENTS

T

he Tunisia Economic Monitor (TEM) presents Professional, HMNHN), Yosra Bouaziz (ET Consultant,

timely and concise assessments of current SMNAG), and Mehdi Barouni (Senior Economist,

economic trends in Tunisia in light of the HMNSP).

country’s broader development challenges. Each It was prepared under the direction of Jesko

edition includes a section on recent economic Hentschel (Country Director, MNC01), Eric Le Borgne

developments and a discussion of the economic (Practice Manager, MTI) and Tony Verheijen (Country

outlook, followed by a special focus section drawing on Manager, MNTCN). The team is grateful to Muna Salim

recent World Bank analytics on Tunisia. The report is (Senior Program Assistant, MTI) and Olfa Limam

intended for a wide audience, including policy makers, (Program Assistant, MNCTN) for their administrative

business leaders, financial market participants, and support.

the community of analysts and professionals engaged The findings, interpretations, and conclusions

in Tunisia. The Tunisia Economic Monitor is a product expressed in this Monitor are those of World Bank

of the Middle East and North Africa (MENA) unit in the staff and do not necessarily reflect the views of the

Macroeconomics, Trade & Investment (MTI) Global Executive Board of the World Bank or the governments

Practice in the World Bank Group. they represent.

The report was prepared by Ali Ibrahim For information about the World Bank and its

Almelhem (ET Consultant, MTI), Mohamed Habib activities in Tunisia, please visit www.worldbank. org/

Zitouna (ST Consultant, MTI) and Shireen Mahdi en/country/Tunisia (English) or www.albankaldawli.

(Senior Economist, MTI). The team included Olivier org/ar/country/tunisia (Arabic).

Durand (Senior Agriculture Economist, SMNAG), Eric For questions and comments on the content of

Raoul Philippe Dunand (Senior Digital Development this publication, please contact Ali Ibrahim Almelhem

Specialist, IDD02), Carlo Maria Rossotto (Digital (aalmelhem@worldbank.org), Massimiliano Cali (mcali@

Development Senior Specialist, BM), Sadok Ayari worldbank.org) or Eric Le Borgne (eleborgne@worldbank.

(External Affairs Associate, ECRMN), and Federica org).

Alfani (ET Consultant, EMNPV). Helpful comments The cutoff date for this edition of the TEM was

were received from Denizhan Duran (Young June 1st, 2021.

viiADDENDUM TO THE

TUNISIA ECONOMIC

MONITOR – SPRING 2021

This issue of the TEM covers political and economic on July 26th. The fall in bond prices is in line with the

developments until June 2021. As such it does not market perception of higher short-term uncertainty on

include the decision, and its potential impact, of public debt sustainability. Hard-currency bonds issued

the Tunisian President Kais Saied to dismiss the by Tunisia’s central bank dropped by record amounts

Prime Minister Hichem Mechichi on July 25th. This on Monday, the 2027 and 2024 dollar-denominated

emergency measure has been the prelude to a bonds both fell more than 5 cents to their lowest in

number of other measures, including the dismissal more than a year. Five-year credit default swaps for

of the minister of defense and the minister of justice, Tunisia’s central bank reached 751 basis points, up

the suspension of parliamentary activities and the one point from Friday’s close. The level has almost

removal of the immunity of members of Parliament. doubled from a year ago.

President Saied also declared a curfew from July Countering this uncertainty is the perception

26th through Friday August 27th, between 7p.m. and by the markets that these measures may help break

6 a.m. At the time of writing the President has yet to the long-standing political impasse on the policy

nominate the new Prime Minister. reform agenda and address the corrupt practices that

These measures are likely to impact the had grown to unprecedented levels in the last few

economy and the reform agenda as well. However, years. Consistent with this view, exchange rates and

it is too early for the TEM to identify such impacts, the stock markets have fluctuated within the normal

which will be covered in the next issue of the TEM. bands in the week of July 26th.

These will include the revised economic projections Much of the outcome could depend on who will

and outlook, with the analysis in this report providing be named as a Prime Minister, and how the President

a baseline prior to the emergency measures. will frame his actions and plans going forward.

The reactions of the markets have been mixed.

Tunisian Government bonds have fallen substantially

viiiEXECUTIVE SUMMARY

Recent Developments percent of GDP (from 8.5 percent a year before),

as a 34 percent drop in the trade deficit reduced

Due to disruptions in international trade and pressure on external balances. The reduction in

tourism triggered by the COVID-19 pandemic, the the trade deficit was led mainly by import demand

Tunisian economy contracted by unprecedented falling faster than exports, and higher energy savings

levels during 2020. Fortunately, recent data caused by lower commodity prices. The narrowing of

indicates that the economy stabilized during the first the current account helped reduce pressure on the

quarter of 2021, with quarter-over-quarter (q-o-q) exchange rate and boost foreign exchange reserves,

growth no longer in negative territory. In comparison which climbed from 112 at the end of 2019 to 158

with regional peers, Tunisia experienced a sharper days of import cover at the end of 2020.

contraction than others, having entered the crisis Although the government has made recent

while already experiencing slow growth, limited fiscal gains in balancing the budget, lower tax revenues

space, and rising debt levels. While the government and higher health-related spending widened the

managed the first phase of the pandemic well from fiscal deficit to 10.4 percent of GDP. Losses in tax

a health standpoint, this early success waned as revenue after the economic fallout of the pandemic

controls were relaxed later in 2020. A record 13.3 was the largest contributor to the widening deficit,

decline in the tradable services sector and a 11.7 followed by an increasingly growing consumer

percent drop in exports contributed towards the subsidy program and transfers to public employees

8.8 percent economic contraction, as weak global and state-owned enterprises (SOEs). Higher health-

demand depressed industrial and tourism exports related expenditures certainly contributed to the large

throughout 2020. As a result, unemployment rose deficit, but will moderate going forward, as some of the

from 14.9 to 17.4 percent, contributing to the wave coronavirus-related stimulus will wane. To finance the

of protests breaking out around the country on the budget, the government quickly mobilized to secure

10-year anniversary of the Arab Spring. Some of the US$6 billion from external lenders, pushing public

recent gains made in poverty reduction will be lost debt levels to 88 percent of GDP. This led credit rating

because the share of the population vulnerable to agencies to downgrade the sovereign credit rating

falling into poverty increased during 2020 due to the of Tunisia, although the risk of debt default “remains

impact of COVID-19 on the economy. highly unlikely.”

Despite this low growth environment, the A declining inflation rate provided much

current account deficit has narrowed to 6.8 needed space for looser monetary policy, as the

ixCentral Bank of Tunisia (CBT) cut rates twice, of the pandemic’s impact on the economy. The

in March and September of 2020. The CBT also financing of the public sector will be particularly

played an active role outside of standard monetary challenging in 2021, with an expected fiscal deficit of

policy by enacting pro-active measures to support the 8.6 percent of GDP, as the authorities deal with the

economy during the pandemic. Without the strong pandemic and maintain support to households, but

fiscal and monetary response from the government with depleted fiscal buffers. In particular, meeting

and the central bank, the impact of the crisis would the 2021 budget’s external financing needs will be

have been far more severe. challenging given the deterioration of the fiscal setting

and the recent sovereign credit rating downgrade.

Structural reforms are on the horizon but

Outlook and Risks will be difficult to implement in a fragile socio-

political environment. In April 2021, the Prime

Output is not projected to return to pre-pandemic

Minister and the Minister of Economy, Finance and

levels until 2024, due to pre-existing structural

Investment announced the government’s broad

weaknesses, a gradual global recovery, and a

economic reform priorities. The main elements were

slow path towards complete vaccination. The real

transitioning from generalized subsidies to targeted

economy is projected to grow by 4 percent in 2021

social assistance, controlling the public sector wage

before quick moderation back to historical growth

bill, SOE governance reforms and restructuring,

rates of 2.2–2.6 percent.1 The magnitude of the

modernization of monetary and financial policies,

recovery will depend on the evolution of the pandemic

digitization (see special focus section) and increasing

in major trading countries and normalization of supply

energy independence through investments in

chains, providing a revival in exports and services.

renewable energy. Such reforms have been on the

The current account deficit is expected to

agenda of every government since the revolution,

widen to 9.2 percent of GDP in 2021 as imports

but have not been implemented because of a lack

begin to recover and commodity prices rise.

of consensus between major stakeholders and an

As the pandemic wanes and trade flows recover,

unstable political and social environment. These issues

manufactured exports and tourism arrivals are

have grown in importance during the pandemic, as

expected to pick-up gradually, supporting a gradual

the government has struggled to convince voters that

reduction in the current account deficit to 8.9 percent

it has a viable plan to create jobs and restore growth.

of GDP by 2023. But risks to the external outlook

A fragmented parliament has made policymaking

remain high, including a sluggish recovery in exports,

cumbersome, complicating the coronavirus response

given the heavy impact of the pandemic on firm

and undermining the effectiveness of the government.

capacity and the pace of recovery amongst Tunisia’s

main trading partners

Financing needs are projected to remain

elevated in the medium term given the extent 1

World Bank April 2021 Forecast (Spring Meetings).

x TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISISRÉSUMÉ EXÉCUTIF

Derniers Développements Il est attendu que les quelques progrès réalisés en

matière de réduction de la pauvreté soient, eux aussi,

En 2020, l’économie tunisienne s’est contractée perdus : en 2020, la part de la population susceptible

à des niveaux sans précédents suite aux pertur- de tomber dans la pauvreté a augmenté en raison

bations que la pandémie de COVID-19 a causées des répercussions de la pandémie de COVID-19 sur

aux échanges internationaux et au tourisme. Fort l’économie.

heureusement, les dernières évolutions indiquent En dépit de ce contexte de faible croissance,

que l’économie s’est stabilisée au cours du premier le déficit du compte courant s’est resserré pour

trimestre de 2021, la croissance en glissement se situer à 6,8 % du PIB (contre 8,5 % une année

trimestriel n’étant plus négative. La Tunisie a connu auparavant), au moment même où la diminution

une contraction plus forte que celle enregistrée du déficit commercial a allégé la pression exer-

par les autres pays pairs de la région, le pays ayant cée sur la balance des paiements. La diminution

affronté la crise alors qu’il pâtissait déjà des effets du déficit commercial s’explique essentiellement par

d’une croissance lente, d’un espace budgétaire limité la rapidité de la diminution des importations compa-

et d’un endettement en hausse. Le gouvernement, qui rativement à celle des exportations. Le resserrement

avait pourtant réussi à gérer la première phase de la du compte courant a permis d’alléger la pression

pandémie d’un point de vue sanitaire, a vu cet acquis exercée sur le taux de change et aidé à renflouer les

s’estomper à mesure que les contrôles commen- réserves en devises qui sont passées de 112 jours

çaient à se relâcher plus tard en 2020. La contraction d’importation fin 2019 à 158 jours d’importations fin

économique, estimée à 8,8 %, a essentiellement été 2020.

provoquée par une baisse record de 13,3 % enregis- En dépit des gains récemment réalisés en

trée au niveau du secteur des services échangeables matière d’équilibre budgétaire, la baisse des re-

et le repli de 11,7 % des exportations, le recul de la cettes fiscales et l’augmentation des dépenses de

demande mondiale ayant réduit les exportations santé ont davantage creusé le déficit budgétaire,

industrielles et touristiques tout au long de 2020. Par le portant à 10,4 % du PIB. Le repli des recettes

conséquent, le taux de chômage est passé de 14,9 % fiscales des suites de l’impact économique causé par

à 17,4 %, alimentant ainsi les vagues de protestations la pandémie de COVID-19 a été le principal respon-

qui ont éclaté un peu partout dans le pays à l’occa- sable du creusement du déficit, suivi du programme

sion du dixième anniversaire du printemps arabe. de subventions aux consommateurs et de transferts

xiaux entreprise publiques. L’augmentation des dé- que les exportations de produits manufacturés et les

penses de santé a, elle aussi, contribué à l’ampleur arrivées de touristes reprennent progressivement,

du déficit, même si l’on s’attend à ce qu’elle s’atténue induisant ainsi une réduction graduelle du déficit de

avec le temps, à mesure que la menace pandémique la balance des paiements à 8,9 % du PIB en 2023.

s’estompe. Pour financer le budget, le gouvernement Toutefois, les risques qui pèsent sur les perspectives

s’est rapidement mobilisé pour obtenir 6 milliards de extérieures restent élevés, notamment eu égard à la

dollars auprès de divers bailleurs extérieurs, ce qui a lenteur de la reprise des exportations, compte tenu

porté le niveau de la dette publique à 88 % du PIB. du lourd impact de la pandémie sur les capacités

Cela a conduit les agences de notation à revoir à la des entreprises et du rythme de la reprise chez les

baisse la note de crédit souverain de la Tunisie, bien principaux partenaires commerciaux de la Tunisie.

que le risque de défaut de paiement “reste hautement On s’attend également à ce que les besoins

improbable”. en financement continuent de grimper sur le

La baisse du taux d’inflation a permis de moyen terme, au vu de l’ampleur de l’impact de

dégager l’espace nécessaire à l’assouplissement la pandémie sur l’économie. Pour 2021, on table

de la politique monétaire, la Banque Centrale de sur des finances publiques en difficulté et un déficit

Tunisie (BCT) ayant réduit ses taux à deux reprises, budgétaire de l’ordre de 8,6 % du PIB. Dans le même

d’abord en mars puis en septembre 2020. La temps, les autorités continuent de lutter contre la

BCT a également joué un rôle actif en se démarquant pandémie et de venir en aide aux ménages dans

de sa politique monétaire conventionnelle et en le besoin, en dépit de l’épuisement des réserves

décrétant un paquet de mesures proactives visant à budgétaires du pays. Il sera particulièrement difficile

soutenir l’économie pendant l’épisode pandémique. de répondre aux besoins de financement extérieur

Sans la forte réponse budgétaire et monétaire du du budget de l’année 2021, au vu de la détérioration

gouvernement et de la BCT, l’impact de la crise aurait du cadre budgétaire et de la récente décote du crédit

été bien plus grave. souverain.

Les réformes structurelles sont difficiles

Perspectives et Risques à mettre en œuvre au vu de la fragilité du

contexte socio-politique. En avril 2021, le chef

Il n’est pas attendu que la production reprenne du gouvernement et le ministre de l’économie, des

ses niveaux pré-pandémiques avant 2024, en finances et de l’investissement ont annoncé les

raison de l’existence de faiblesses structurelles, grandes priorités du gouvernement en matière de

du caractère progressif de la reprise mondiale et réforme économique. Les principales composantes

de la lenteur de la progression de la campagne de de ces réformes ont porté sur : (i) l’abandon

vaccination. Il est prévu que l’économie réelle croisse des subventions universelles en faveur d’une

de 4 % en 2021, avant de revenir rapidement aux taux aide sociale ciblée, (ii) le contrôle de la masse

de croissance habituels de 2,2 %–2,6 %. L’ampleur de salariale du secteur public, (iii) la réforme et la

la reprise va dépendre de l’évolution de la pandémie restructuration de la gouvernance des entreprises

dans les principaux pays qui commercent avec la publiques, (iv) la modernisation des politiques

Tunisie, ainsi que de la normalisation des chaînes monétaires et financières, (v) la numérisation (Se

d’approvisionnement, relançant ainsi les exportations référer à la section dédiée) et (vi) l’amélioration de

et les services. l’indépendance énergétique par l’intensification des

Le déficit de la balance des paiements est investissements dans les énergies renouvelables.

voué à se creuser davantage pour atteindre 9,2% Ces réformes, inscrites à l’ordre du jour de tous les

du PIB en 2021, conséquemment à la reprise des gouvernements depuis la révolution, n’ont jamais

importations et à la hausse des prix des produits été mises en œuvre en raison de l’absence de

de base. A mesure que la pandémie s’estompe et consensus entre les principales parties prenantes et

que les flux commerciaux se rétablissent, on prévoit de l’instabilité de l’environnement politique et social.

xii TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISISCes questions ont pris plus d’importance pendant la Le caractère fragmenté de l’ARP a entravé la mise

pandémie et le gouvernement a des difficultés pour au point de politiques adéquates, compliqué la

convaincre les citoyens qu’il détenait un plan viable réponse à la pandémie et sapé l’efficacité du travail

pour créer des emplois et restaurer la croissance. gouvernemental.

Résumé Exécutif xiiiالملخص التنفيذي

األسعار .وساعد تقلص عجز الحساب الجاري عىل تحفيف الضغط عىل آخر التطورات

سعر الرصف وتعزيز احتياطيات العملة الصعبة التي قفزت من 112

يو ًما من التوريد يف نهاية عام 2019إىل 158يو ًما يف نهاية عام .2020 نتيجة لالضطرابات التي شهدتها التجارة الدولية و قطاع السياحة الناجمة

عن جائحة الكوفيد ،-19سجل االقتصاد التونيس انكامشا مبستويات غري

و عىل الرغم من أن الحكومة قد حققت مكاسب يف اآلونة األخرية عىل مسبوقة خالل عام .2020و لحسن الحظ ،تشري املعطيات األخرية إىل أن

مستوى توازنات امليزانية ،إال أن انخفاض اإليرادات الرضيبية وزيادة االقتصاد يشهد استقرار خالل الثاليث األول من عام ،2021حيث متكنت

اإلنفاق املرتبط بالقطاع الصحي أدى إىل توسيع عجز املالية العامة ليبلغ معدالت النمو من ثاليث إىل آخر ( )q-o-qمن تجاوز املستويات السلبية.

10.4يف املائة من الناتج املحيل اإلجاميل .و ت ُعترب الخسائر يف اإليرادات و باملقارنة مع نظرائها يف املنطقة ،شهدت تونس انكامشً ا أكرث حدة من

غريها من البلدان ،حيث دخلت األزمة بينام كانت تعاين أصال من بطء

الرضيبية بعد التداعيات االقتصادية للجائحة أكرب مساهم يف اتساع

يف نسق النمو ،ومحدودية الحيز املايل ،وارتفاع مستويات الديون .و بينام

العجز ،يليها كل من برنامج دعم املستهلك ،الذي يشهد زيادة مطردة،

متكنت الحكومة من إدارة املوجة األوىل للجائحة بشكل جيد من وجهة

والتحويالت لفائدة املوظفني العموميني والرشكات اململوكة للدولة .و من نظر صحية ،فقد تراجع هذا النجاح املبكر تزامنا مع تخفيف اإلجراءات

املؤكد أن النفقات املرتفعة املرتبطة بالصحة قد ساهمت يف اتساع العجز، االحرتازية يف وقت الحق من عام .2020وساهم الرتاجع القيايس املسجل

لكنها ستصبح معتدلة يف املستقبل ،حيث ستختفي بعض العوامل املرتبطة يف قطاع الخدمات القابلة للتداول التجاري بنسبة 13.3٪وانخفاض

بفريوس كورونا .و لتمويل امليزانية ،قامت الحكومة بتعبئة املوارد بشكل الصادرات بنسبة 11.7٪يف انكامش اقتصادي بنسبة ،8.8٪حيث أدى

رسيع لتأمني 6مليار دوالر من قبل املانحني الدوليني ،مام رفع مستويات ضعف الطلب العاملي إىل تراجع الصادرات الصناعية والسياحية طوال

الدين العام إىل 88يف املائة من الناتج املحيل اإلجاميل .وقد أدى ذلك عام .2020ونتيجة لذلك ،ارتفعت معدالت البطالة من 14.9٪إىل

إىل قيام وكاالت التصنيف االئتامين بخفض التصنيف االئتامين السيادي ،17.4٪مام ساهم يف اندالع موجة من االحتجاجات يف جميع أنحاء البالد

(الرتقيم السيادي) لتونس ،عىل الرغم من أن مخاطر التخلف عن سداد مبناسبة الذكرى العارشة للربيع العريب .باالضافة إىل ذاك ستخرس تونس

الديون «ال تزال غري مرجحة إىل حد كبري». بعض املكاسب األخرية التي تحققت يف مجال الحد من الفقر ألن نسبة

السكان املعرضني للوقوع يف براثن الفقر ارتفعت خالل عام 2020بسبب

و أدى انخفاض نسبة التضخم إىل توفري مساحة رضورية من أجل تداعيات جائحة الكوفيد-19عىل االقتصاد.

سياسة نقدية أكرث مرونة ،حيث قام البنك املركزي التونيس بخفض

و رغم هذه البيئة التي تتسم بانخفاض معدالت النمو ،فقد تقلص

أسعار الفائدة مرتني ،يف مارس وسبتمرب من عام .2020لعب البنك عجز الحساب الجاري إىل 6.8٪من إجاميل الناتج املحيل (من 8.5٪

املركزي التونيس أيضً ا دو ًرا نشطًا خارج السياسة النقدية التقليدية يف العام السابق) ،حيث أدى انخفاض العجز التجاري بنسبة 34٪إىل

من خالل وضع تدابري استباقية لدعم االقتصاد أثناء الجائحة .و لوال تخفيف الضغط عىل التوازنات الخارجية .و كان االنخفاض يف العجز

االستجابة املالية والنقدية القوية من الحكومة والبنك املركزي ،لكان التجاري مدفو ًعا بشكل أسايس بانخفاض الطلب عىل الواردات بوترية

تأثري األزمة أكرث حدة. أرسع من الصادرات ،مدخرات عيل تكاليف الطاقة بسبب انخفاض

xvالعمومي تحديًا خاصا يف عام ،2021يف ظل عجز مايل متوقع بنسبة 8.6 اآلفاق واملخاطر

يف املائة من إجاميل الناتج املحيل ،حيث ستواصل السلطات التعاطي مع

الجائحة و دعم األرس ،ولكن مع استنفاد االحتياطيات الوقائية .و عىل ليس من املتوقع أن يعود الناتج إىل مستويات ما قبل الجائحة قبل حلول

وجه الخصوص ،ستمثل تلبية احتياجات التمويل الخارجي مليزانية 2021 عام ،2024و يعود ذلك إىل نقاط الضعف الهيكلية املوجودة من قبل ،و

تحديا كبريا نظ ًرا لتدهور الوضع املايل وخفض التصنيف االئتامين السيادي النسق التدريجي لالنتعاش العاملي ،و النسق البطيء لعملية التطعيم.

يف اآلونة األخرية. من املتوقع أن ينمو االقتصاد الحقيقي بنسبة 4يف املائة يف عام 2021قبل

أن يرتاجع برسعة إىل معدالت النمو التقليدية البالغة 2.2إىل 2.6يف املائة.

رغم التخطيط للقيام باإلصالحات الهيكلية سيكون من الصعب تنفيذها و سيعتمد حجم االنتعاش عىل مدى تطور الجائحة يف البلدان التجارية

يف بيئة اجتامعية وسياسية هشة .يف أبريل ،2021أعلن رئيس الحكومة الكربى و عودة سالسل التوريد إىل وضعها الطبيعي ،مام يوفر انتعاشً ا يف

ووزير االقتصاد واملالية و دعم االستثامر عن الخطوط العريضة ألولويات الصادرات والخدمات.

اإلصالح االقتصادي للحكومة .و متثلت العنارص الرئيسية يف :االنتقال من

الدعم الشامل إىل املساعدات االجتامعية املوجهة ،والتحكم يف كتلة أجور من املتوقع أن يتسع عجز الحساب الجاري ليبلغ 9.2٪من إجاميل

القطاع العمومي وإصالحات حوكمة الرشكات العمومية وإعادة هيكلتها، الناتج املحيل يف عام 2021تزامنا مع بدء انتعاش الواردات وارتفاع

وتحديث السياسات النقدية واملالية ،والرقمنة (انظر قسم الرتكيز الخاص) أسعار السلع األساسية .حيث أنه بانحسار الجائحة و انتعاش التدفقات

و دعم االستقالل الطاقي من خالل االستثامرات يف الطاقات املتجددة. التجارية ،من املتوقع أن تنتعش الصادرات الصناعية و يرتفع عدد السياح

و املالحظ هو أن هذه اإلصالحات كانت دامئا مضمنة يف برنامج كل الوافدين تدريجياً ،مام يساعد عىل التخفيض التدريجي لعجز الحساب

الحكومات املتعاقبة منذ الثورة ،لكنها مل تُنفذ بسبب عدم التوصل إىل اتفاق الجاري ليبلغ 8.9يف املائة من الناتج املحيل اإلجاميل بحلول عام .2023

بني األطراف الفاعلة و بسبب عدم استقرار البيئة السياسية واالجتامعية .و لكن املخاطر عىل التوقعات الخارجية ال تزال مرتفعة ،مبا يف ذلك انتعاش

ازدادت أهمية هذه القضايا خالل الجائحة ،حيث بذلت الحكومة مجهودا بطيء يف الصادرات ،بالنظر إىل التأثري الكبري للجائحة عىل قدرات الرشكات

من أجل إقناع الناخبني بأن لديها خطة قابلة للتطبيق ستساهم يف خلق ووترية التعايف لدى الرشكاء التجاريني الرئيسيني لتونس.

فرص العمل واستعادة معدالت النمو .و باإلضافة إىل ذلك ،فقد جعل عدم

فاعلية العمل الربملاين جعلت عملية صنع السياسات مرهقة ،مام يعقد من املتوقع أن تظل احتياجات التمويل مرتفعة عىل املدى املتوسط

االستجابة لجائحة الكوفيد -19ويقوض فعالية العمل الحكومي. بالنظر إىل مدى تأثري الجائحة عىل االقتصاد .و سيمثل متويل القطاع

xvi TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISIS1

RECENT ECONOMIC

DEVELOPMENTS

Growth and Employment and reduce pressure on hospital and medical staff.

As policy measures were relaxed over the Summer of

By mid-2021, the Tunisian economy began to 2020, new cases emerged (Figures 1 & 2). Managing

stabilize after a difficult year of managing the this second wave of the virus was complicated by the

pandemic. The impact of the pandemic has been political uncertainties created by the government’s

more strongly felt than in neighboring countries resignation in July 2020. In September, a new

and will require careful planning to pull the government was formed with the daunting task of

economy out of the recession. managing increasingly difficult health, economic,

The road to Tunisia’s recovery is long. and social conditions. Containment measures were

The initial containment measures imposed during imposed throughout the rest of 2020 including

March 2020 helped control the spread of the virus curfews, restrictions on movement between regions,

FIGURE 1 • Impact of COVID-19 Was Higher than FIGURE 2 • …while Policy Stringency Was More

Neighboring Peers… Relaxed

COVID-19 new cases and deaths COVID-19 policy stringency index

25,000 800 100

700 90

20,000 80

Stringency index

600 70

500 60

15,000 50

400 40

10,000 300 30

20

200 10

5,000

100 0

Jan-20

Feb-20

Mar-20

Apr-20

May-20

Jun-20

Jul-20

Aug-20

Sep-20

Oct-20

Nov-20

Dec-20

Jan-21

Feb-21

0 0

Tunisia Morocco Egypt Algeria

Cases (per million) Deaths (per million) Tunisia Algeria Morocco Egypt

Source: MENA Crisis Tracker, World Bank. Source: Johns Hopkins Coronavirus Resource Center.

1FIGURE 3 • Nearly All Sectors Contracted in FIGURE 4 • …with Sharper Declines than Regional

2020… Peers

100% 4 Regional comparison of GDP growth

80% 8

2

Growth (%) by sector (YoY)

GDP growth (%) YoY

60% 6

40% 0

Real GDP growth (percent)

4

20% –2

0% 2

–20% –4 0

–40% –6 –2

–60%

–8 –4

–80%

–100% –10 –6

2015 2016 2017 2018 2019 2020 2021 –8

(Q1)

–10

Agriculture Manufacturing industries 2019 2020 2021 2022

Non-manufacturing industries Tradable services

Non-tradable services GDP growth Jordan Egypt Morocco Tunisia

National Institute of Statistics (INS). World Bank, MENA Economic update, April 2021.

alternating work in the public sector, and limiting Lower domestic and public sector demand are also

capacity in the hospitality sector. These policy affecting output as private consumption contracted

responses helped reduce pressure on a health by 3 percent while public consumption fell by 11.4

system with limited capacity and reduced the negative percent owing to lower revenues. Some of the recent

repercussions on both lives and livelihoods. Despite gains made in poverty reduction will be lost as the

these measures, a third wave of cases began to rise share of the population vulnerable to falling into pov-

toward the end of the year, highlighting the difficulty of erty increased because the share of the population

managing the pandemic. vulnerable to falling into poverty increased during

The real economy contracted by unprece- 2020 (See Box 3).

dented levels in 2020 as Tunisia’s high exposure Services and export-oriented sectors were

to Europe weighed negatively on demand. The hit hard amid strong economic headwinds from

Tunisian economy saw an unprecedented 8.8 per- the pandemic. The services sector represents over 60

cent contraction for the entire year (Figure 3). The percent of GDP and was hit by a 13.3 percent decline

majority of the decline was registered during the in the tradable services sector, mostly concentrated in

second quarter (–21 percent y-o-y), during which transportation and hospitality. Although interregional

time that the pandemic’s effect on the economy flights showed some recovery during the summer

strengthened. Recent data shows that economic per- months, they sharply declined towards the end

formance is still affected by the pandemic, although of the year, primarily from the uncertainty caused

at a lower rate, with a 3 percent contraction y-o-y in by the pandemic (Figure 5). These declines were

the first quarter of 2021. The pandemic has under- slightly offset by modest growth in agro-food and

lined Tunisia’s high exposure to economic conditions petroleum refining sectors thanks to a favorable

in Europe in terms of trade, tourism, remittances, and harvest and resumption of activity in the national

investment. Weak demand in Europe, the destina- refining industry (Société Tunisienne des Industries

tion of more than 75 percent of Tunisian exports, will de Raffinage – STIR). Industrial production declined

continue to weigh on domestic growth and the pace 5.2 percent as both the domestic economy and major

of recovery in the near term. In fact, Tunisia’s high trading partners registered negative growth for 2020.

trade openness among MENA countries and heavy Similarly, manufacturing and non-manufacturing

emphasis on services has caused a sharper contrac- industries contracted by 9.3 and 8.8 percent during

tion in comparison with regional peers (Figure 4). 2020. In the first quarter of 2021, exports increased

2 TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISISFIGURE 5 • International Flights Recovered Only FIGURE 6 • Energy and Mining Sectors Still Far

Temporarily Below Potential

Weekly interregional flights Energy and minig industrial production

1.2 120

Interregional flights (index)

1.0 100

0.8 80

0.6 60

0.4 40

0.2 20

0.0 0

May-20

May-11

May-13

May-15

May-17

May-19

Aug-20

Mar-20

Dec-20

Mar-21

Sep-20

Sep-10

Sep-12

Sep-14

Sep-16

Sep-18

Sep-20

Nov-20

Feb-20

Feb-21

Jun-20

Jan-20

Jan-21

Jan-10

Jan-12

Jan-14

Jan-16

Jan-18

Jan-20

Apr-20

Oct-20

Jul-20

Egypt Algeria Morocco Tunisia Mining Energy IPI

World Bank, Global Aviation Dashboard. INS.

by 6.2 percent compared to the first quarter of 2020 had steadily grown over the years, but is now down 21

while imports increased by 1.5 percent over the same percent compared to the beginning of 2020.

period, signaling the beginning of recovery for some Domestic and international containment

sectors. Exports in the mechanical and electrical measures are weighing on the income-generating

sector increased by 12.1 percent and those of the role of the private sector, jeopardizing social and

textile-clothing-leather sector rose by 6.5 percent, while economic stability. A survey of 2,500 private firms in

those of the mining and energy sector decreased by November-December 2020 revealed that 65 percent

18.3 percent and 15.3 percent respectively. Imports of firms risk permanent closure in the next 12 months,

by the agriculture and agro-food sector increased by and only 30 percent were confident they would sur-

20.9 percent and those of the mining sector rose by vive until next year. By the end of the 2020, a total of

13.4 percent. 21.6 percent of companies were either permanently

Protests at energy and mining sites caused or temporarily closed. Over 80 percent of businesses

large swings in production, reducing tax reve- saw a drop in demand, and as a result fired employ-

nues and development opportunities for lagging ees (26 percent) or cut wages (15.7 percent). The risk

regions. The energy and mining sectors play impor- of permanent closure was highest among micro-enter-

tant roles in the regional development—especially for prises (70 percent), SMEs (62 percent), non-exporting

lagging regions—but also provide strong buffers to firms (70 percent), and large companies (48 percent).

external balances and tax revenues at the national Amid strong headwinds from the pandemic, the pri-

level. These sectors saw a sharp decline in produc- vate sector has made little headway in its struggle to

tion (–80 percent) after the 2011 revolution and they improve living standards and incomes, exacerbating

remain well below potential (Figure 6). During 2020, already simmering unrest.

mining production declined 13 percent after oil and Unemployment was high before the pan-

phosphate production was disturbed following social demic and worsened to 17.8 percent in 2021. The

unrest and regular protests in the southern regions. labor force participation rate for women has improved

Most of the energy and mining sites are located in the by 4 percent over the past ten years, offset by an

poorest parts of the country with high unemployment

and are more sensitive to economic swings. Protests 2

For instance, in July, miners in Tataouine closed the

began to appear in May 2020 near older sites in

valves for local distribution as a protest against the failure

Tataouine and Gafsa, but also in the recently started to implement an agreement the government signed on in

Nawara gas field.2 Following the sharp decline imme- November 2019, which provided for thousands of new

diately post-revolution, total phosphate production jobs for the region.

Recent Economic Developments 3BOX 1. BUILDING A GREEN, RESILIENT, AND INCLUSIVE AGRO-FOOD SECTOR

The agro-food sector demonstrated sound resilience during the Economic growth by sector (%)

COVID-19 pandemic, but at the same time lockdown measures 15

again confirmed the limited economic inclusion of smallholder 10

farmers. Unlike tourism and manufacturing sectors, agroculture 5

contributed positively to growth during the pandemic, providing a

0

small boost to food processing industries due to favorable harvest

conditions. At the start of the pandemic, the cereal production –5

campaign was already well advanced, and the olive harvest and –10

oil processing were almost completed. During the lockdown, –15

only the fishery industry was put to a complete halt with a severe 2016 2017 2018 2019 2020

impact on fishermen revenues. Subsectors linked to the tourism Agriculture and fisheries

industry (poultry and meat) suffered from a serious demand Manufacturing industries

reduction. As part of a qualitative survey carried out by the Bank Non-manufacturing industries

in June 2020, 70 agro-industries were interviewed on the impact Market services

of the COVID-19 crisis on their activities. With the exception of the Non-market activities (admin, domestic services, etc.)

fishery and poultry subsectors, agro-industry representatives did

not mention serious disruption in supply or commercialization

as a concern but highlighted their major constraints as staff Sub-sector annual production versus 2010–2020 average

100%

reduction and rotation, and the additional costs associated with

80%

sanitary measures. No severe disruption was recorded in food

supply to urban markets and medium and large commercial farms 60%

remained connected to export markets. 40%

Source: Institut National des Statistaiques (INS) and Livret annuel 20%

des statistiques agrocoles 2018 (Direction Générale des études et 0%

de développement agrocole), Observatoire National de l’Agroculture –20%

(ONAGRO), Groupement Interprofessionnel des Viandes rouges et

du Lait (GIVLAIT), Groupement Interprofessionnel des Produits –40%

Avicoles et Cunicoles (GIPAC), Office National de l’Huile (ONH) –60%

2015 2016 2017 2018 2019 2020

However, the crisis has had a higher impact on smallholders and

had once again revealed their recurrent disconnect from input Wheat Olive oil Dates

Fisheries Poultry farming Dairy milk

and output markets, their limited economic inclusion, and their

vulnerability to shocks. During the lockdown, and in the absence

of well-structured producer organizations and cooperatives,

more than 80 percent of small farmers could not access agroculture inputs and commercialize their produce. As part of a field survey,

carried out by L’institution de la Recherche et de l’Enseignement Supérieur Agrocoles (IRESA) and International Fund for Agrocultural

Development (IFAD) in June 2020, 82.5 percent of small producers in the north (Siliana and Jendouba), 79 percent in the center (Kairouan

and Mahdia) and 83.5 percent in the south (Kébili et Médenine) declared that they had to reduce their agrocultural activities because they

could not purchase inputs, especially seeds, fertilizer, and animal feed, and were unable to commercialize their produce, especially dairy

and vegetable productions. Access to temporary agrocultural work in larger farms and other off-farm job opportunities was also a major

concern for small producers. As movement restrictions were eased for agrocultural activities, the situation improved but this experience

confirmed the vulnerability of smallholder farmers, whose contribution to the country’s food security is important.

According to the last agrocultural census (ONAGRO 2005), Tunisian smallholder farmers represent 21.5 percent of the cultivated area

but contribute to a large share of the domestic food production. Of the half million farms in Tunisia, 88 percent are family farms and 75

percent hold less than 10 hectares, but these represent 62 percent of the cereal production. But, only 5 percent of the Tunisian farmers

belong to a producer organization and only 7 percent have access to credit.

Smallholder farmers remain isolated and vulnerable, but digital technologies have a significant potential to strengthen their

resilience, and to ensure their financial and economic inclusion. In this context, characterized by a general defiance from farmers vis-

à-vis cooperatives, digital technologies offer solutions to connect small producers to a wide range of technical and financial services, and

to overcome market failures in the agro-food sector, such as market power, information asymmetries, and transaction costs. Digital tools

can help small farmers remain connected with input suppliers, get up-to-date market information, and access technical information (such

as plant disease identification or vet care advice) in order to become more resource-efficient and climate-resilient. Electronic marketing

platforms have started to offer fresh vegetable produce to urban consumers. Digital technologies such as mobile money, digital credit

(continued on next page)

4 TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISISBOX 1. BUILDING A GREEN, RESILIENT, AND INCLUSIVE AGRO-FOOD SECTOR (continued)

scoring, and remote sensing for insurance design have the potential, in rural areas especially, to reduce high transaction costs for credit

access related to isolation, small scale, and risks. The Tunisian government is providing support to smallholders in the form of investment

subsidies that they may not always be able to access independently due to administrative hurdles and requirements, literacy capacities, and

other reasons. With higher levels of digital inclusion for farmers, these public support programs could become better targeted to the most

vulnerable producers, and thereby be delivered in a more efficient and equitable manner.

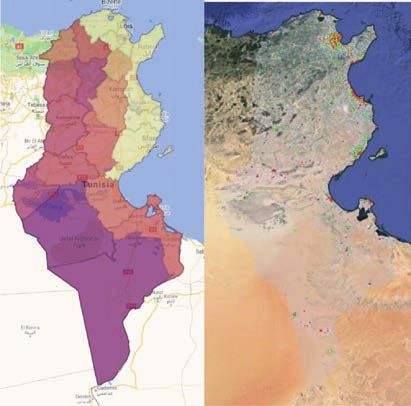

BOX 2. HOW DID COVID-19 AFFECT REGIONAL GROWTH? MONITORING ECONOMIC ACTIVITY USING

NIGHT-TIME LIGHTS

Did COVID–19 affect growth in some regions of Tunisia more

than others? We use satellite data on night–time lights, as a proxy

to GDP growth, to explore the spatial distribution and evolution

of the pandemic’s in Tunisia. The left panel shows the average

luminosity by governate in 2019, while the right panel shows NTL

gains (green) and losses (red) during 2020. Coastal governates

emit the most NTLs given their large manufacturing, trade, and

services sectors, while still developing inland and Southern

governates are less bright. During 2020 however, the brightest

coastal cities exhibited the sharpest declines. The largest

contractions (year–on–year) were concentrated in Tunis (–10.7

percent), Ariana (–8.4 percent), Monastir (–8 percent), Sousse

(–7.2 percent), Ben Arous (–6.5 percent), Nabeul (–4.6 percent),

Manouba (–4.0 percent), Bizerte (–3.7 percent), Medenine (–2.6

percent), Mahdia (–2.5 percent), Gabes (–2.3 percent), Sfax

(–1.1 percent).

equal decline for men. However, the employment rate

percent in the agriculture and fishing sector as of

for men is 60 percent on average while for women

2021. Most of these sectors registered contractions

the rate is only 20 percent. Before the pandemic, the

in 2020, particularly in services and export-oriented

unemployment rate stood at 14.9 percent and initially

industries. The unemployment rate for females is far

spiked to 18 percent in the second quarter of 2020

higher than that for men (24.9 vs. 14.4 percent) and is

in response to the challenges presented by the pan-

disproportionally concentrated in the interior regions

demic. After moderating to 16 percent in October, the

of the country. The unemployment rate for university

rate rose sharply to 17.4 percent by the end of the

graduates continues to be above the national aver-

year. This resulted in a 78,000 increase in the num-

age, highlighting the limited job opportunities for

ber of unemployed persons during the fourth quarter,

high-skilled workers and the structural mismatch in

and an increase of 133,000 for the entire year. This

the labor market.

increase in unemployed definitely contributed to the

wave of protests breaking out around the country and

will continue to weigh heavily on recovery efforts. An The Socioeconomic Impact of

analysis of the distribution of employees shows that COVID-19 on Household Welfare

52.8 percent are in the service sector, 17.9 percent

in the manufacturing industries sector, 16.0 percent Living standards have deteriorated for about half

in the non-manufacturing industries sector, and 13.3 of Tunisian households through the COVID-19

Recent Economic Developments 5FIGURE 7 • Household Reported Worsening in living standards of Tunisian households, particularly

Living Standards… among the most vulnerable (i.e., the bottom 40 per-

cent of the consumption distribution). More than half

Round 5 14.3 31.6 50.0 3.7 0.3 of the households interviewed report a worsening of

Round 4 10.9 32.0 50.4 6.6 0.2

their living standards relative to before the start of

the pandemic in March 2020 (Figure 7). This effect

Round 3 15.4 33.9 46.6 4.1 moderated to 42.9 percent in the second half of the

Round 2 21.7 32.4 42.3 3.5 June (round 4) but rose again to 45.9 percent in the

first half of October (round 5).

0% 20% 40% 60% 80% 100% Living standards particularly worsened

Percent

among the poor and the bottom 40 percent.

Much worse Worse Same

In May 2020, 66.9 percent of households in the

Better Much better

lowest consumption quintile reported that their living

Source: Alfani et al., 2021. Estimation based on data from the Enquête téléphonique standards had worsened, compared to the situation

auprès des ménages pour étudier et suivre l’impact du COVID19 sur le quotidien des

Tunisiens, Institut national de la statistique (INS) and World Bank. they faced in March (Figure 8). Estimates show that the

probability of declaring a worsening in living standards

is positively correlated with a lower degree of education

level of the household head and with being younger.

pandemic. Between March and October 2020, the Individuals not employed at the time of the survey, the

Institut National de la Statistique (INS), in collabora- self-employed, and contributing family workers have a

tion with the World Bank, implemented five rounds of higher probability of reporting a deterioration of their

high-frequency telephone surveys. This nationally rep-

resentative panel dataset of about 1,000 households 3

Results reported in this section have been extracted

allowed the assessment of the socioeconomic impact

from Alfani F., Dhrif D., Molini V., Pavelesku D., Ranzani

of the COVID-19 over time. The survey results3 indi- M. 2021. “Living Standards of Tunisian Households in

cate that the combined public health and economic the midst of the COVID-19 Pandemic,” World Bank Policy

crises have had a sizeable negative effect on the Research Working Paper, Forthcoming.

FIGURE 8 • …Particularly among the Lowest Income Groups

Round 2 Round 3

0.1 0.1

100% 1.1 0.9 3.4 4.7 6.6 100% 3.2 2.6 6.0 5.2 3.2

80% 32.0 31.2 40.0 80% 32.3 38.5 44.9

48.6 56.2 52.4 60.6

Percent

Percent

60% 60%

32.4 36.8 39.7

40% 32.9 32.9 40% 39.0

27.3 33.6 32.3 26.4

20% 34.5 31.1 20%

23.7 13.8 9.8 24.8 20.0 16.5 10.1 9.7

0% 0%

20% poorest 2 3 4 20% richest 20% poorest 2 3 4 20% richest

Round 4 Round 5

0.9 0.7

100% 4.6 3.3 9.4 8.2 6.9 100% 1.4 4.4 3.9 4.1 4.1

80% 36.9 42.2 80% 37.4 48.6 44.9

49.0 56.8 63.0 55.7 59.4

Percent

Percent

60% 60%

40% 35.4 40% 45.3 26.6

39.9 31.9

20% 33.3 27.9 23.9 20% 30.0 28.3

22.0 14.7 8.3 7.1 5.3 15.9 20.3 18.4 9.5 8.2

0% 0%

20% poorest 2 3 4 20% richest 20% poorest 2 3 4 20% richest

Much worse Worse Same Better Much better

World Bank, MENA Economic update, April 2021

6 TUNISIA ECONOMIC MONITOR – NAVIGATING OUT OF THE CRISISliving standards. Similarly, in the following rounds, Safety net programs mitigated only par-

the percentage of households declaring worsening tially the negative effects of COVID-19 on the

living standards is consistently higher at the bottom poorest and more vulnerable ones. Although

of the consumption distribution than the top. While public transfers, and particularly social protection

waiting for the economy to rebound, most vulnerable systems, usually provide a safety net for those who

households will continue to need income support. lose their job giving them the means to look for new

A lack of demand from clients was the employment, this kind of mitigation measures are

primary contributing factor to a significant labor limited in scope and insufficient to avoid significant

income decline among the self-employed. By increases in poverty. High unemployment and levels

October 2020, incomes had not yet bounced back to of informality has created low coverage rates in the

the level observed before the onset of the COVID-19 country, although Tunisia has a comprehensive

pandemic, with labor income getting worse among social insurance system in place. Shortly after the

the self-employed (Figure 9). The main element COVID-19 outbreak and subsequent lockdown, the

cited by respondents for their fall in income was a government introduced short-term work schemes

lack of customers since the re-opening (from 28.3 which included a wage subsidy of DT 200 per month

percent in May to 47.6 percent in October). On the in April and May 2020 and a one-off cash transfer

other hand, the lockdown and subsequent closure of DT 200 for micro-enterprises (forfaitaire). About

of workplaces was the main reason for the reduction 110,000 micro-enterprises received the transfer,

in income for 49.8 percent of self-employed in while about 140 000 retirees whose monthly pension

early May (round 1) and 53.4 percent in late May is below TND 180 received 100 TND pension top-

(round 2). up. In addition, about 1 million poor and vulnerable

FIGURE 9 • Varying Reasons for the Decline in FIGURE 10 • The Deterioration of Welfare Felt

Business Income among Everyone

Male household head **

Round 5 47.3 16.8 29.0 6.5 **

35–44

45–64 ***

1.7 65+ ***

Round 4 50.4 10.8 37.1 Primary education **

Secondary education **

Tertiary education ***

Round 3 10.1 38.3 5.6 10.8 20.9 14.3 Not employed ***

Private sector employee **

Self employed/employer ***

4.8

Partial salary ***

Round 2 53.4 28.4 8.0 5.4 *

No salary

Lower/No business income ***

1.9 2nd consumption quintile ***

Round 1 49.8 28.3 6.7 13.3 3rd consumption quintile ***

4th consumption quintile ***

0% 20% 40% 60% 80% 100% 5th consumption quintile ***

Percent Round 4 ***

Round 5 ***

Closure of the establishment Lack of customers –0.2 0.0 0.2 0.4 0.6

Lack of raw Inability to

materials/manpower move/transport goods Welfare deterioration

Lack of liquidity Other reasons Note: Probability of declaring a deterioration in living standards, as compared to the

month before the interview. Estimation coefficients of the linear probability model.

Source: Alfani et al., 2021. Estimation based on data from the Enquête téléphonique Reference categories: 15–34; no education; public sector employee; full salary,

auprès des ménages pour étudier et suivre l’impact du COVID19 sur le quotidien des business income as usual or more than usual; Quintile 1; Round 3. Robust standard

Tunisiens, Institut national de la statistique (INS) and World Bank. errors in parentheses. Statistical significance: *** p < 0.01, ** p< 0.05, * p < 0.1.

Recent Economic Developments 7You can also read