TOURISM SECTOR IN CYPRUS - IMF eLibrary

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CYPRUS

TOURISM SECTOR IN CYPRUS

The global pandemic shock has caused an unprecedented shock to the tourism industry, severely

impacting tourism-dependent economies such as Cyprus. This chapter seeks to examine the recent

developments in the tourism sector in Cyprus. It further examines the outlook for recovery prospects

and outlines some policy priorities given the economic vulnerability to the tourism shock and the need

to minimize scarring and protect the vulnerable workers.

A. Recent Trends in the Tourism Sector

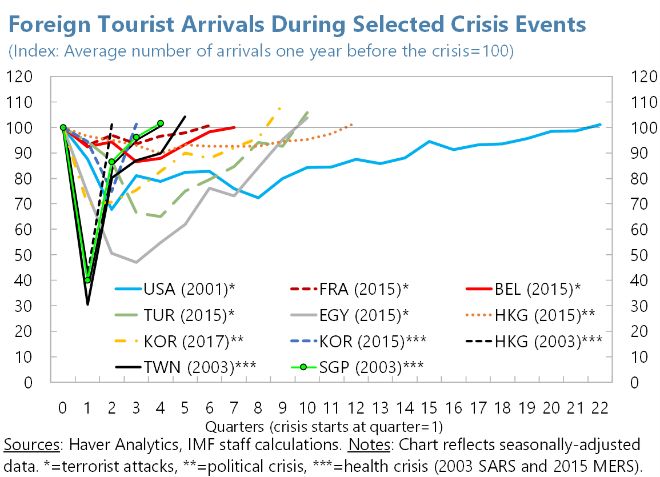

1. Global tourism has suffered the worst year on record in 2020 following the

unprecedented fall in demand and widespread travel restrictions. According to UNWTO (2021),

international arrivals dropped by 74 percent in 2020 (1 billion fewer arrivals) than in 2019. The

collapse in international travel represented an estimated loss of USD 1.3 trillion in export revenues,

more than 11 times the loss recorded during the 2009 global economic crisis. The loss in tourism

translated into an economic loss of USD 2 trillion in direct tourism GDP (more than 2 percent of the

world’s GDP). Europe recorded a 70 percent drop in tourist arrivals in 2020, and the region suffered

the largest drop in absolute terms with over 500 million fewer international tourists. By comparison,

during the 2009 global financial crisis, international tourist arrivals fell by 4 percent in the world and

10 percent in Europe, with a much smaller economic impact and swift recovery afterwards. Based on

a simple event analysis, tourism slumps associated with major terrorist attacks, epidemics, and

political crises, showed, on average, 20 to 30 percent declines in tourist arrivals (Salas, et. al, 2020).

For instance, tourist arrivals dropped by 5 to 31 percent after terrorist attacks (USA, France, Belgium,

Turkey, Egypt) and recovered in one to five years. Tourist arrivals dropped, on average, by above

30 percent and recovered in one year or less in the SARS and MERS epidemics (Hong Kong, Taiwan,

Singapore, South Korea).

International Tourist Arrivals

(Percent Change)

Source: UNWTO.

* Provisional Data.

2 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for Redistribution

CYPRUS

2. Tourism in Cyprus has been hard hit by the Covid-19 shock, among the most severe in

Europe. Tourist arrivals experienced an unprecedented collapse since the pandemic. In 2020, tourist

arrivals decreased by 84 percent, while tourism revenue decreased by 85 percent, compared to

2019. Travel restrictions led to a significant decrease in tourist demand from the major markets such

as the United Kingdom (UK) and Russia. While travel restrictions were lifted in early June for arrivals

from a limited number of countries, Cyprus still experienced the most severe decline of tourist

arrivals for the year when compared with other European countries.

Cyprus: Tourist Arrivals Cyprus: Tourism Revenue

(Thousand persons) (Millions of euro)

600 600 500 500

2014 2014 2015

450 450

2015 2016 2017

500 500

400 400

2016 2018 2019

2017 350 350

400 400 2020

2018 300 300

300 2019 300 250 250

2020

200 200

200 2021 200

150 150

100 100

100 100

50 50

0 0 0 0

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Source: Statistical Service of Cyprus. Source: Statistical Service of Cyprus.

3. Employment has been largely protected in the tourism sector, but hours worked

declined much more severely than during the previous crises. While tourism employment has

declined more than in the rest of the economy, with the temporary employment support measures,

this decline has been contained so far. The number of workers in Trade, Travel & Food Services

decreased by 13 percent in 2020:Q2 and 9 percent in 2020:H2 compared with the previous year. This

trend also held for self-employed workers. Nonetheless, hours of work in Trade, Travel & Food

Services decreased more significantly in the second, third and fourth quarters of 2020 by 20 percent,

15 percent, and 18 percent, respectively, compared to the previous year.

INTERNATIONAL MONETARY FUND 3

©International Monetary Fund. Not for Redistribution

CYPRUS

Number of Workers: Cyprus Hours Worked: Cyprus

(Year on year growth, percent) (Year on year growth, percent)

15 15 20 20

Employees: Total economy

10 10 15 Self-Employed: Total economy 15

5 5 Employees: Trade, Travel & Food Services

10 10

Self-Employed: Trade, Travel & Food Services

0 0 5 5

-5 -5 0 0

-10 -10 -5 -5

-15 -15 -10 -10

-20 Employees: Total economy -20 -15 -15

Self-Employed: Total economy

-25 Employees: Trade, Travel & Food Services -25 -20 -20

Self-Employed: Trade, Travel & Food Services

-30 -30 -25 -25

2001Q1 2005Q1 2009Q1 2013Q1 2017Q1 2020Q4 2001Q1 2005Q1 2009Q1 2013Q1 2017Q1 2020Q4

Sources: Eurostat, Haver Analytics, and IMF staff calculations. Sources: Eurostat, Haver Analytics, and IMF staff calculations.

4. The pandemic shock has had a The Impact of Covid-19 Pandemic on Tourism

significant impact on exports of services and GDP

10

and on GDP growth. The adverse impact on Export in services growth, 2020 (yoy)

y = 3.0268x - 3.5126

R² = 0.4847 IRL

0

the economy was large since tourism is a key BEL POL

LUX

-10

MLT

sector for Cyprus. Services exports decreased

NLD LTU

CYP DNK

ROMSWE

DEU

EA CZE

AUT

-20

FIN

by around 27 percent in the second and third

FRA

SVN

LVA EST

quarters of 2020 compared to the same

HUN

-30 ITA BGR

periods of 2019, mainly reflecting the fall in

PRT

-40

ESP GRC

demand for tourism. The overall economy also

HRV

-50

showed a deep recession in 2020, with real -15 -10 -5 0 5

GDP growth, 2020 (yoy)

GDP declining by around 8 percent in the Source: Eurostat.

Note: Bubble size corresponds to share of services exports in GDP (percent).

second and third quarters of 2020.

B. Vulnerability of the Cypriot Economy to the Tourism Sector

5. The Cypriot economy has a high dependence on tourism, which makes it more

vulnerable to the impact of the Covid-19 shock. Tourism receipts accounted for more than

18 percent of Cyprus’s total exports in 2019. Tourism expenditure balance (inbound minus

outbound) reached around 8 percent of GDP in 2019. Tourism also has large spillover effects to

related industries outside of hotels (food services, retail, transport, construction, other services).

Cyprus’s economy has a very high dependence on tourism related industries, with the total of direct

and indirect contribution accounting for nearly 14 percent of GDP in 2019, which was higher than in

many other European countries. 1 Tourism and related services also provided a large contribution

(around 13 percent) to total employment.

1

Based on the World Travel and Tourism (WWTC) database, the direct contribution of travel & tourism to GDP is

calculated to be consistent with the output of tourism-characteristic sectors such as hotels, airlines, airports, travel

agents, and leisure & recreation services that deal directly with tourists. The total contribution of travel & tourism

includes its wider impacts on the economy (i.e. the indirect and induced impacts), in addition to the direct impacts.

4 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for RedistributionCYPRUS

Travel Service Exports Contribution of Tourism Related Industries, 2019

(Percent of Total Exports) (Percent of GDP)

40 40 35

2019 Direct Indirect

35 2013 35 30

2008

30 30 25

25 25

20

20 20

15

15 15

10

10 10

5

5 5

0

0 0

ISL

MNE

GRC

PRT

ESP

ITA

EST

HUN

CYP

AUT

TUR

LUX

BGR

SVN

BIH

RUS

IRL

HRV

DEU

GBR

FRA

SWE

LVA

MKD

MDA

BLR

SVK

ROU

UKR

NLD

ISR

BEL

ALB

MLT

NOR

CHE

FIN

DNK

CZE

LTU

POL

SRB

ISL

CYP

BEL

AUT

DEU

TUR

HUN

MLT

FRA

HRV

LTU

SVN

SWE

LVA

SVK

GRC

PRT

POL

NLD

CZE

NOR

LUX

ESP

EST

FIN

BGR

ITA

GBR

ROU

DNK

Sources: Eurostat, Haver Analytics, and IMF Staff Calculations. Sources: World Travel and Tourism Council and IMF staff calculations.

6. High exposure of the Cypriot banking system to the tourism sector also increases the

risk of a macro-financial feedback loop. Loans to accommodation and food services was

46 percent of tier 1 capital, one of the highest in the euro area (IMFa, 2020) 2. The sectors of trade,

hotel, restaurant, and transportation accounted for the largest shares of total loans and non-

performing loans in Cyprus. These sectors were hit harder by the pandemic with more negative

growth rates of gross value added than other sectors. However, the moratorium on loan repayments

have helped alleviate the negative impact of the pandemic on the financial sector. The take-up rate

of the loan repayment moratorium, at over 90 percent, was particularly high for non-financial

corporations involved in tourism related activities, including accommodation and food, arts,

entertainment and recreation, and construction. But with the expiry of the moratorium, there are

risks of loan distress as the repayments become due. A heatmap table capturing these economic

and financial sector exposures placed Cyprus among the highest quintile of countries vulnerable to

the tourism sector in the EU 3.

The indirect contribution includes the GDP and jobs supported by: travel & tourism investment spending;

government 'collective' spending which helps travel & tourism activity; and domestic (non-imported) supply chain

purchases of goods and services by the sectors dealing directly with tourists. The induced contribution measures the

GDP and jobs supported by the spending of those who are directly and indirectly employed by the travel & tourism

sector (WTTC/Oxford Economics 2020).

2

Based on IMF (forthcoming), “The Impact of COVID19 on European Banks,” EUR Departmental Paper.

3

Based on Salas, et. al. (2020), “Tourism in Europe After the COVID-19 Shock: Impact, Prospects, and Policies.”

Unpublished slides, European Department, International Monetary Fund.

INTERNATIONAL MONETARY FUND 5

©International Monetary Fund. Not for RedistributionCYPRUS

Loans to Highly Affected Sectors Macroeconomic Indicators

(Percent of Tier 1 capital) Share of Bank

tourism Share of Private Lending to

Real Estate Activities

Transport & Storage

Share of

(direct and travel consumptio Accommod

Wholesale & Retail

Accommodation &

Arts & Entertainm

tourism Average

indirect) in services n WEO ation &

in total quintile

total in total forecast Food

Other Services

output

Food Services

employme exports (2020-2021) Services

Construction

nt Sector

Austria 4.2

Trade

Belgium 2.2

Bulgaria 3.4

Croatia 4.3

AT 29 56 18 16 116 2 4 Cyprus 4.0

Czechia 2.5

BE 26 40 15 4 41 3 4 Denmark 2.0

Estonia

CY 39 59 17 46 44 2 3

3.0

Finland 1.8

DE 10 42 28 4 177 2 11 France 3.2

Germany 2.8

EE 14 59 24 4 86 3 7 Greece 4.8

ES 29 70 24 18 48 3 24 Hungary 2.8

Iceland 4.5

FI 20 30 30 4 167 3 10 Ireland 2.8

FR 18 53 25 9 90 2 28 Italy

Latvia

4.4

3.2

GR 40 91 51 40 29 6 10 Lithuania 1.0

Luxembourg 2.4

IE 6 25 13 21 60 4 8 Malta 4.0

IT 47 77 24 16 66 3 28 Netherlands 3.4

Norway 2.8

LU 9 3 2 3 22 0 5 Poland 1.8

LV 12 33 33 14 72 1 5 Portugal 4.8

Romania 2.0

MT 16 24 10 12 32 4 1 Slovakia 1.3

NL 15 68 33 7 88 2 21 Slovenia

Spain

3.4

5.0

PT 34 41 19 18 38 3 19 Sweden 2.6

Switzerland 2.7

SI 16 52 39 6 11 1 4 Turkey 3.0

EA SSM 22 47 23 15 90 3 11 United Kingdom 3.6

Sources: IMF (2020a) based on data from EBA Transparency Sources: Eurostat; WTTC; and IMF WEO.

Exercises and IMF staff calculations.

C. Characteristics of the Tourism Sector Affecting the Recovery Prospects

7. The tourism sector in Cyprus is highly reliant on foreign/inbound tourism, which puts

Cyprus in a less favorable position regarding the prospects for a near-term recovery. Foreign

tourist arrivals reached around 5 times of domestic tourist arrivals in 2019, and the tourism

expenditure balance (inbound minus outbound tourism expenditure) was around 8 percent of GDP

in 2019, higher than most other European countries. The European Travel Commission (2021)

estimated that European international travel declined by 69 percent in 2020, compared to a

35 percent decline for domestic travel. The high reliance of Cyprus’s tourism on international arrivals

indicates a slower near-term recovery prospect as international travel restrictions will be eased at a

slower pace than domestic tourism, and the smaller share of domestic tourism also reflects its

relatively minor contribution from its rebound to offset the drop in international arrivals. In addition,

the full dependence on air travel also makes it highly susceptible to travel restrictions.

6 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for RedistributionCYPRUS

Tourism Expenditure Balance

(Percent of GDP)

25 25

2019

2013

20 20

2007

15 15

10 10

5 5

0 0

-5 -5

CYP

ISL

CHE

BEL

MNE

AUT

IRL

DEU

MLT

TUR

HUN

ALB

FRA

HRV

SVN

LVA

SVK

LTU

SWE

GRC

PRT

POL

CZE

RUS

NOR

ESP

EST

FIN

BGR

ITA

GBR

ROU

DNK

Source: UNWTO.

8. High reliance on hotel accommodation makes Cyprus more vulnerable to the Covid-19

shock, while concentration of stays away from cities presents a more favorable outlook. Given

the fall in attractiveness of hotels with the pandemic shock, there is potential for non-hotel

accommodations to attract tourists, which benefits countries that can provide a greater variety of

accommodations. However, in the case of Cyprus, almost all tourists stay in hotels and similar

accommodations. On the other hand, the location of overnight stays in Cyprus is more diverse, with

more stays in towns and suburbs and rural areas and relatively low ratio of stays in cities. The

relatively large size of non-urban tourism is helpful for Cyprus to cope with the pandemic, as rural

tourism is likely to increase and could partly offset the decline in urban tourism.

Overnight Stays by Degree of Urbanization, 2019

Tourist Arrivals by Type of Accomodation, 2019 (Percent)

(Percent) Cities Towns and suburbs Rural areas

100 100

Camping grounds, recreational vehicle parks and trailer parks

Holiday and other short-stay accommodation 90 90

Hotels and similar accommodation

100 100 80 80

90 90

70 70

80 80

60 60

70 70

50 50

60 60

50 50 40 40

40 40 30 30

30 30 20 20

20 20 10 10

10 10 0 0

0 0

LVA

CZE

FIN

LTU

NLD

BEL

FRA

SVK

AUT

DEU

BGR

EST

MLT

PRT

ROU

HUN

SWE

LUX

ESP

DNK

POL

EU27

MKD

ITA

CYP

HRV

AUT

CZE

SVK

NLD

BGR

FIN

LVA

DEU

EU27

FRA

LTU

BEL

CYP

MKD

MLT

EST

HUN

ESP

GRC

ROU

PRT

LUX

POL

ITA

SWE

DNK

HRV

Sources: Eurostat and IMF staff calculations.

Sources: Eurostat and IMF staff calculations.

9. Cyprus’s lower dependency on business travel and good progress on vaccination in

source countries are more favorable for recovery prospects. When evaluating travel exports by

type, Cyprus has a very high ratio of personal travel and low reliance on business travel. This trend

could suggest a quicker rebound of tourism since business tourism may be more severely affected

post-Covid-19. In addition, the major tourist market countries of Cyprus have made good progress

INTERNATIONAL MONETARY FUND 7

©International Monetary Fund. Not for RedistributionCYPRUS

on vaccinations. Two of the top three source countries (UK and Israel) are advanced in vaccinating

their population, with around 60 percent and 110 percent of population having completed

vaccinations by mid-April. Another positive factor is that two of the top three markets (Russia and

Israel) are expecting a faster recovery to pre-pandemic growth rates in 2021. The concentration of

tourist sources from Europe also increases the likelihood of travel as travel restrictions ease within

Europe and travelers prefer short-haul flights.

Cyprus: Sanitary and Recovery Indicators of

Tourism-Source Countries 1/

Total

Historical Vaccinations per 2021 real GDP

arrivals (% of Total cases per hundred of growth relative

Country of origin total) million population to 2019

United Kingdom 33.7 64716 60.4 -5.1

Russian Federation 19.9 31615 10.2 0.6

Israel 5.9 96654 111.7 2.5

Germany 4.8 36823 23.1 -1.5

Greece 4.7 29184 21.8 -4.8

Sweden 3.9 87668 21.0 0.2

Poland 2.3 69256 21.0 0.6

Switzerland 1.9 72559 21.0 0.4

Ukraine 1.8 44357 1.0 -0.3

Romania 1.7 52836 19.9 1.9

Sources: UNWTO; Bloomberg; and IMF WEO.

1/ Data on COVID cases and vaccinations is up to April 15.

10. Furthermore, the relatively good health conditions of Cyprus would help to attract

tourists once travel restrictions are lifted. Cyprus has so far ranked relatively well in terms of

health conditions. When compared with other European countries, Cyprus has relatively fewer

reported cases of Covid-19 per million people, suggesting the relatively high degree of safety of

sanitary situation in Cyprus. Cyprus has also conducted more Covid-19 tests per million people than

most of the other European countries which could help contain the pandemic. Nonetheless, the

health situation remains highly uncertain given the ongoing wave of infections.

11. Based on a Heatmap Analysis of the overall tourism characteristics and sanitary

situation, Cyprus is placed in the fourth and third quintile of EU countries in terms of the risks

to the prospect of tourism recovery. As shown in the text table, Cyprus has a score of 3.4 using

the tourism indicators 4, mainly reflecting the large dependence on foreign tourism and air travel.

Cyprus fares relatively well in terms of sanitary/health indicators, placing it in the middle quintile

with a score of 2.8. This reflects the lower number of cases and high testing rates which is partly

offset by the high stringency score on mobility restrictions that deter the attractiveness for travel.

4 The Heatmap Analysis based on indicators include: relative size of urban (vs. rural) tourism, relative size of foreign

(vs. domestic) tourism, inbound (vs. outbound) tourism spending, share of business (vs. personal) travel, share of

hotel stays (vs. other accommodations) and share of tourism by air (vs. other modes). Each indicator is scored in a

range between 1–5 with a higher score indicating a higher vulnerability (Salas, et. al., 2020). The relative ranking

should however be treated with caution given the missing values in some variables. A similar heatmap for the

health/sanitary indicators uses number of COVID-19 cases, vaccination rate, number of COVID-19 tests and

stringency of the mobility restrictions (see IMF (forthcoming) ,” Tourism in Southern Europe: Development and

Prospects under the COVID-19 Pandemic,” EUR Departmental Paper).

8 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for RedistributionCYPRUS

Tourism Indicators Sanitary Indicators

Relative Relative

Relative

Relative Relative size of size of Inbound Share of

size of

size of size of inbound tourism (vs. hotel stays

tourism Average COVID-19 COVID-19 COVID-19 Stringency Average

urban (vs. foreign (vs. tourism exports on outbound) (vs. other

by air (vs. quintile cases vaccines tests Index quintile

rural) domestic) from RoW business tourism accommo

other

tourism tourism (vs. from (vs. spending dations)

modes)

Europe) personal)

Austria 3.0 3.8

Belgium 2.5 3.0

Bulgaria 2.5 3.3

Croatia 2.2 3.5

Cyprus 3.4 2.8

Czechia 3.7 3.8

Denmark 2.6 1.8

Estonia 3.8 2.0

Finland 4.0 2.0

France 2.7 3.0

Germany 3.7 3.0

Greece 2.5 3.0

Hungary 2.7 3.5

Iceland 4.0 1.0

Ireland 3.8 2.8

Italy 2.1 3.3

Latvia 2.9 2.8

Lithuania 3.0 3.0

Luxembourg 3.5 3.3

Malta 4.0 1.3

Netherlands 3.2 4.3

Norway 2.0 2.0

Poland 2.3 3.5

Portugal 3.6 3.8

Romania 2.4 3.0

Slovakia 2.5 3.3

Slovenia 2.8 3.5

Spain 3.0 2.8

Sweden 3.2 3.5

Switzerland 4.0 3.0

Turkey 4.3 3.3

United Kingdom 3.3 2.8

12. Looking ahead, Cyprus fares relatively well in terms of prospects for recovery given

the tourism characteristics, sanitary indicators, and recovery in the main source countries.

Using the quantile distribution of countries (combining indicators in the heatmaps), with 1 indicating

the least vulnerable and 5 being the most vulnerable, we estimate the speed of recovery for

countries assuming each broad category has the same weight. Based on the results, Cyprus should

have a relatively faster recovery rate.

Speed of Recovery: Country Rankings Speed of Recovery: Country Rankings

(Quintile) (Quintile)

5 5

Tourism Indicators Sanitary Indicators Source Country Recovery Indicators Tourism Indicators Sanitary Indicators

4 4

Slower Faster Faster

Slower

3

3

2

2

1

1

0

TUR HRV IRL LTU PRT FRA CYP ITA ESP MLT GRC 0

DEU

CHE

FIN

LTU

POL

FRA

SWE

TUR

AUT

LUX

LVA

EST

IRL

MLT

DNK

NOR

PRT

CYP

HUN

ESP

ISL

HRV

BEL

NLD

CZE

ITA

GBR

SVN

SVK

BGR

ROU

GRC

Sources: Eurostat; UNWTO; IMF WEO; Bloomberg; and IMF staff calculations.

INTERNATIONAL MONETARY FUND 9

©International Monetary Fund. Not for RedistributionCYPRUS

D. Outlook for Tourism

13. The decline in tourism is expected to be partially reversed in 2021 with a full recovery

to pre-pandemic levels expected only in the medium term. Eurocontrol forecasts (Nov 2020)

shows that air traffic in Europe would only return to 2019 levels by 2024 in the most optimistic

scenario, assuming vaccine is made widely available for travelers by summer 2021, while air traffic in

2024 would be at 92 percent of the 2019 level in their second scenario (vaccine widely available in

2022) and 75 percent in their third scenario (vaccine not effective). According to the UNWTO (2021),

the recovery outlook for 2021 remains subdued amid high uncertainty, with half of the respondents

expecting a rebound in 2021 and the other half only in 2022. The extended UNWTO scenarios for

2021–2024 indicate that it could take between 2½ and 4 years (mid-2023 – end 2024) for

international tourism to return to 2019 levels. Based on European Travel Commission (2021), which

conducts global tourism forecast using the Global Travel Service model, inbound visitor growth rates

of Southern and Mediterranean Europe are projected to be -72 percent in 2020, 132 percent in

2021, 34 percent in 2022, and 16 percent in 2023.

Cyprus: Eurocontrol's Forecast on Instrument Flight International Tourist Arrivals: Recovery to Return to

Rules (IFR) Movements 2019 Levels, Scenarios for 2021–2024

(Thousands) (Millions)

500

450 Projections

400

350

300

250

Scenario 1 - Vaccine widely made

200

available for travelers by Summer 2021

150 Scenario 2 - Vaccine widely made

100 available for travelers by Summer 2022

Scenario 3 - Vaccine not effective

50

0

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Source: UNWTO World Tourism Barometer, January 2021.

Source: Eurocontrol.

14. The slow recovery is also consistent with recent high frequency indicators. Decline in

flights to Cyprus was among the highest in Europe. Flights continue to decline in early 2021, which

does not bode well for Cyprus’s tourism given its full reliance on air travel. Based on anecdotal

evidence, hotel occupancy remains low at around 10 to 15 percent compared to the 50 to

55 percent in 2019, consistent with Southern European peers such as Portugal and Greece. EU

business confidence surveys also show continued underperformance of tourism industries although

forward-looking expectations have improved slightly since July 2020.

10 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for RedistributionCYPRUS

Total Number of Flights: Europe Europe: Hotel Rooms Occupancy Rate

(Percent change, weekly relative to 2019 baseline) (Occupied rooms as percent of total available rooms)

20 100

0

80

-20

60

2021: week 15 2020: week 15 2019: week 15

-40

40 2020 w15: AE 2020 w15: EE 2019 w15: AE

-60 2019 w15: EE

20

-80

Week ending April 5 Week ending March 29

0

Weekly average in March 2020

-100

RUS

TUR

ESP

LUX

ITA

IRL

ROU

FRA

PRT

GBR

AUT

GRC

UKR

BEL

NLD

CHE

HRV

DEU

POL

HUN

EST

LVA

IRL

CYP

PRT

ESP

ITA

ISR

TUR

SWE

GRC

ISL

FIN

UK

ROU

LUX

MKD

NLD

BGR

AUT

BEL

FRA

MDA

BIH

SVN

BLR

DNK

MLT

POL

MNE

LTU

DEU

UKR

SVK

RUS

NOR

HRV

CHE

SRB

CZE

ALB

KOS

Sources: Smith Travel Research (STR); and IMF staff calculations.

Note: AE refers to Advanced Europe, and EE refers to Emerging Europe.

Sources: FlightRadar24; and IMF staff calculations.

Sources: Smith Travel Research (STR); FlightRadar24; and IMF staff calculations.

15. The recovery of tourism will be determined by the pace of the vaccination rollout, the

coordination among countries on travel procedures and the economic situation. New infection

waves and protracted containment measures could further delay the recovery of tourism sector. On

the other hand, vaccine developments help to shift the balance of risks and elevate the upside

potential. For Cyprus, based on the current pace of vaccine rollout in the country as well as the main

source countries, staff has projected that a recovery of 30 percent, on average, of the 2019 level is

expected in 2021 with full recovery taking place by 2024.

Cyprus: Expected Demand Over Next Three Months Cyprus: Estimated Recovery of Tourist Arrivals

(Percent Balance) (Share of total tourist arrivals)

40 40

100

20 90

20

0 80

0 70

-20

60

-40 -20 50 Share

-60 40

-40

30

-80 CYP reaches total

Overall Services -60 20

vaccination doses over

-100 Air Transport 10 120% population

Accommodation -80

-120 0

Food & Beverage

May-21

Jul-21

May-22

Nov-21

Jan-22

Jul-22

Nov-22

Jan-23

May-23

Jul-23

Nov-23

Mar-21

Sep-21

Mar-22

Sep-22

Mar-23

Sep-23

Travel/Tour Operator

-140 -100

Jan-19 Jun-19 Nov-19 Apr-20 Sep-20 Feb-21

Sources: Eurostat and Haver Analytics. Sources: UNWTO; Bloomberg; and IMF Staff Calculations.

E. Policy Priorities

16. Cyprus has adopted various measures to support the economy and tourism sector.

Main policy measures 5 include: 1) Income tax measures and VAT reductions; 2) support for bank

lending; 3) a Suspended Operations Plan for businesses that decided to suspend their operations or

5

Based on UNWTO compilation of country policy measures to support travel and tourism.

INTERNATIONAL MONETARY FUND 11

©International Monetary Fund. Not for RedistributionCYPRUS

suffered high losses and unemployment allowance; 4) Small Business Support Plan to provide funds

and subsidy of employee salaries; 5) Granting of “sickness benefit” and residence allowance for

students abroad. More targeted measures for the tourism sector include: 6) a co-promotional

program of EUR10 million with tourist agents for the projection of Cyprus as a safe destination for

tourists, and additional appropriations of EUR 11 million to support tourism between June and

September 2020, in cooperation with airlines and travel operators, as well as actions to boost tourist

attraction during the period from October 2020 to March 2021; 7) covering the health cost of

travelers who test positive while in Cyprus; 8) allowing vaccinated travelers to avoid quarantine and

negative coronavirus test restrictions from March 2021; 9) “Extraordinary Plan for the Support of

Domestic Tourism” which offers hotel discounts to permanent residents to support local businesses.

17. Continued targeted support

measures to the tourism sector are Euro Area: Increase in the Share of Insolvent Firms

(Percentage points from pre-pandemic levels; simple averages)

warranted in the short term given their 50

systemic importance to the economy. 40

Measures will need to consider solvency 30

20

support given the high risk of insolvency 10

among tourism sector firms as shown by 0

simulations of corporates in the Euro Area

Transportation

Professional activities

Electricity, Gas, Steam,

Water Supply

Construction

& Communication

Accomodation &

Public Administration

Wholesale and

Manufacturing

Mining & Quarrying

Real Estate

and Air Conditioning

Retail Trade

Food Services

& Storage

Information

(IMF, 2020b) 6. Liquidity-type support, such as

activities

guaranteed loans or lending rate subsidies,

etc. could be considered. These measures

Source: “Corporate Liquidity and Solvency in Europe during the Covid-19

would allow public support to benefit from a Pandemic: The Role of Policies”, Chapter 3 of the October 2020 Regional Economic

Outlook for Europe.

viability assessment by banks. Since many

tourism-related businesses would fall under SMEs, increased access to SME restructuring tools

would help avoid costly bankruptcies. For larger, strategic businesses, equity-type support—with

potential upside for the government down the road as the economy recovers—could also be

considered. Since the tourism sector is more likely to suffer for an extended period, these measures

could mitigate long-term scarring while ensuring scarce public resources are extended to viable

businesses. The length of the support, if fiscal space allows, could last until the end of the crisis, and

should reduce as tourism picks up. Other targeted polices such as promoting marketing for tourism,

could also boost tourism revenues.

18. Policy design measures should also take into account that tourism sector workforce is

among the most vulnerable. Workers in the hotel industry tend to fall disproportionately in the

lowest income quintile compared with other industry groups. Given low teleworkability of this

industry, these workers are more susceptible to unemployment and income loss. Policies should

thus ensure continued income replacement or wage subsidies to maintain employment ties.

6

Based on simulations using firm-level data (ORBIS database) in 13 euro area countries and October 2020 WEO

projections and announced policies, the authors find that the share of firms deemed insolvent would rise by

8 percentage points, on average, given high leverage levels and limited scope for equity financing among SMEs. See

IMF (2020b), “Corporate Liquidity and Solvency in Europe During the COVID-19 Pandemic: The Role of Policies,”

Chapter 3, Regional Economic Outlook (October) for further details.

12 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for RedistributionCYPRUS

Workers in this sector appear to be more gender balanced, although women are represented more

than in other sectors. At the same time, this sector has a higher reliance on foreign workers in

Cyprus. Support measures should appropriately target these populations in terms of safety net

support and to facilitate easier transition back into the workforce as the recovery takes hold.

Likelihood of Being in the Top and Bottom Income Quintile by

Industry's Teleworkability

Bottom fifth Top fifth

Hotels

Agriculture

Retail

Construction

Health

Transport

Manufacturing

Art

Mining

Utilities Share of jobs

OtherServ that can be

Adminsupport done remotely

PublicAdmin

Realestate

Wholesale

Education

ICT

Finance

Professional

0.0 0.1 0.2 0.3 0.4

Sources: European Social Survey, 2018; and IMF Staff Calculations.

19. The longer-term policy challenge is to steer the sector from mass tourism to

sustainable tourism, given the impact of the pandemic and environmental concerns. Mass

tourism tries to maximize revenues through demand anticipation and capacity management,

notably in airlines, hotels, and rental cars. Risks of future pandemics, overcrowding, and

environmental policies may have long-term impacts on international travel and make mass-tourism

business model less viable. Sustainable tourism could be a potential alternative which focuses on

smaller-scale, regionally more diverse, and higher-end tourism; more strongly based on

environmental sustainability, quality of services, and non-price competitiveness. Based on the Travel

and Tourism Competitiveness Index by World Economic Forum (WEF), Cyprus has similar

competitiveness scores as the average of Euro Area countries. Cyprus also ranks among the most

improved (from 55th to 42nd); nevertheless, further improvements will need to focus on

environmental sustainability and diversification to different types of markets such as cultural

resources. Cyprus has made progress in diversifying the source markets of tourism, although the

share of its top three markets (UK, Russia, Israel) remains very high, making it vulnerable to

developments in these countries. More diversification of tourist market would help Cyprus to cope

with shocks.

INTERNATIONAL MONETARY FUND 13

©International Monetary Fund. Not for RedistributionCYPRUS

Travel and Tourism Competitiveness Index Tourism Arrivals

(Score, 1-7 (best)) (Percent, Share of arrivals from the top 3 market)

Business environment Cyprus 80

Cultural resources and 7

Safety and security EA19

business travel 6 70

5

Natural resources Health and hygiene

4 60

3

Tourist service 2 Human resources and 50

infrastructure 1 labour market

0 40

Ground and port

ICT readiness 30

infrastructure

20

Air transport Prioritization of Travel

infrastructure & Tourism 10

Environmental

International Openness

sustainability 0

Price competitiveness

IRL UKR CYP ESP MLT ITA MNE LTU PRT ISR GRC TUR HRV FRA

Sources: World Economic Forum; and IMF staff calculations. Source: UNWTO.

F. Conclusion

20. Global tourism has suffered the worst year on record in 2020. The impact on tourism in

Cyprus has been among the most severe in Europe, which in turn had a significant impact on

exports of services and on GDP growth. Nevertheless, employment has been largely protected in the

tourism sector, due to large support packages that were rolled out.

21. Looking ahead, near-term challenges to the tourism sector remain significant. The

decline in tourism is expected to be only partially reversed in 2021 with a full recovery to pre-

pandemic levels only expected in the medium term, raising risks of scarring. The Cypriot economy

remains vulnerable to the COVID-19 shock given its high dependence on tourism. High exposure of

the Cypriot banking system to the tourism sector also increases risks of a macro-financial feedback

loop. At the same time, Cyprus fares relatively well in terms of prospects for recovery, given its

tourism characteristics, sanitary indicators and recovery in the main source countries, once travel

restrictions are eased. While uncertainty remains high, the recovery of tourism will be determined by

the pace of the vaccination rollout, the coordination among countries on travel procedures and the

economic situation.

22. In this context, continued targeted support measures to the tourism sector are

warranted in the short term given their systemic importance to the economy. Policy design

measures should also take into account that the tourism sector workforce is among the most

vulnerable. The longer-term policy challenge is to steer the sector towards sustainable tourism,

given the impact of the pandemic and environmental concerns.

14 INTERNATIONAL MONETARY FUND

©International Monetary Fund. Not for RedistributionYou can also read