The U.S. Economic Outlook: Welcome to Boomtown - Kevin L. Kliesen Business Economist and Research Officer Federal Reserve Bank of St. Louis

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

The U.S. Economic Outlook:

Welcome to Boomtown

Kevin L. Kliesen

Business Economist and Research Officer

Federal Reserve Bank of St. Louis

FRB St. Louis Louisville Branch Regional Economic Briefing (webinar)

March 23, 2021

1

Disclaimer

The views I will express today are my

own and do not necessarily reflect the

positions of the Federal Reserve Bank

of St. Louis or the Federal Reserve

System.

2

The Big Picture

• My baseline forecast is for very strong U.S. GDP

growth this year and next. Vaccine dynamics!

• Strong growth will generate large monthly job gains

and a rapid decline in the unemployment rate.

• The big question: Will an inflationary impulse follow

on the heels of this jet-fueled growth? Markets say, yes.

• The marked rise in federal debt: There are no free

lunches.

3

THE BIG PICTURE IN

PICTURES

4

Real GDP Continues to Recover

Growth of Real GDP, 2019-20:

Annual Quarterly

Rate Rate

2019:Q4 2.4% 0.6%

2020:Q1 - 5.0% -1.3%

2020:Q2 -31.4% -9.0%

2020:Q3 33.4% 7.5%

2020:Q4 4.1% 1.0%

2021:Q1(F) 6.0% to 7%

Percent below peak: 2.4%

5

Employment Growth is Rebounding

Monthly Changes in U.S.

Nonfarm Payroll Employment:

Sept. 2020 716,000

Oct. 2020 680,000

Nov. 2020 264,000

Dec. 2020 -306,000

Jan. 2021 166,000

Feb. 2021 379,000

Mar. 2021 500,000 (F)

Employment is still 9.5 million

below the peak.

6A Falling U.S. Unemployment Rate

Unemployed as a Percent of

the U.S. Labor Force:

April 2020 14.8%

June 2020 11.1%

Nov. 2020 6.7%

Dec. 2020 6.7%

Jan. 2021 6.3%

Feb. 2021 6.2%

Mar. 2021 6.1% (F)

7Temp Unemployment Surges, Falls

Unemployed: Those on Temporary and Not Temporary Layoff

Percent of labor force

14

12

Temp. UR Not Temp. UR

10

8

6

4

2

0

2005 2007 2009 2011 2013 2015 2017 2019 2021

SOURCE: BLS and Haver Analytics Data through Feb. 2021

8A Most Unusual Recession

Personal After-Tax Incomes and Expenditures, 2018 to the Present

Billions of $2012

18,000

After-Tax Real Income

17,000

16,000

Real Personal Consumption Expenditures

The passage of the

15,000 ARP Act will

14,000 Personal Saving increase after-tax

13,000 income and saving

12,000 even more!

11,000

10,000

Jan.2018 Jul.2018 Jan.2019 Jul.2019 Jan.2020 Jul.2020 Jan.2021

SOURCE: BEA and Haver Analytics

9Federal Finances Deteriorate

U.S. Federal Tax Receipts, Outlays, and Surplus/Deficit

$Billions, 12-month rolling sums (through Feb. 2021)

8,000

7,044 Total Legislative Response to

6,000

COVID thus far: $6 trillion.1

4,000

3,490

CBO Feb. Budget Projections:

2,000

• Deficit

0 ‒ FY 2020: $3.1 trillion

‒ FY 2021: $2.3 trillion

-2,000

-4,000

(3,554) • Debt/GDP (%)

‒ FY 2020: 100.1% (A)

-6,000

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

‒ FY 2021: 102.3% (P)

Outlays Receipts Surplus/Deficit 1covidmoneytracker.org

10Fed on Hold at the “Zero-Lower Bound”

The FOMC's Nominal Federal Funds Target: Actual and Projected

Percent

6

5

NOTE: FOMC

Actual FFTR projections are

4

Mar. 2021 SEP Projection based on each

(Median)

3 person’s view of

2 “appropriate”

1

policy for the

projection period.

0

2003 2004 2006 2008 2010 2011 2013 2015 2017 2018 2020 2022

SOURCE: Federal Reserve and Haver Analytics

11The Fed’s Balance Sheet is Still Growing

The FOMC is

purchasing “at

least” $80 billion

per month in

Treasury securities

and $40 billion per

month in

mortgage-backed

securities.

12Moving Up: Long-Term Interest Rates

13Financial Conditions Still Look Good

Values below zero

imply below average

levels of financial

stress, which point to

improving economic

conditions.

14THE U.S. ECONOMIC

OUTLOOK

NARRATIVE

15Uncertainty is Falling—That’s Good!

Businesses don’t like

uncertainty! Falling

levels of uncertainty,

coupled with faster

growth, should trigger a

healthy rebound in

business investment.

The Blue Chip

Consensus forecast is for

7.25% growth in 2021.

NOTE: An index value of 100 is defined to be “average.”

16Housing Likely to Remain Strong

New and Existing Single-Family Homes for Sale Housing Affordability Index

Thousands of Units, End of Period Values in Excess of 100 Indicate Housing is More Affordable

4,500 250

4,000 225

3,500 200

3,000 175

2,500 150

2,000 125

1,500 100

1,000 75

Jan.2001 Jan.2005 Jan.2009 Jan.2013 Jan.2017 Jan.2021 1991 1994 1997 2000 2003 2006 2009 2012 2015 2018 2021

Index = 100 when median family income qualifies for an 80% mortgage on a median priced existing single-family home.

SOURCE: Census, NAR, and Haver Analytics. Last observation is January 2021. SOURCE: National Association of Realtors and Haver Analytics

17PCE Services Spending Still Lags

Real Consumer Spending and its Major Components

Index, Jan. 2020 = 100

120

115

110

105

Expenditures on

100 services comprise

95

61% of the average

90

85

person’s consumption

80 basket and 44% of

75

70

GDP before the

Jan.2020 Mar.2020 May.2020 Jul.2020 Sep.2020 Nov.2020 Jan.2021

pandemic.

Total PCE Durables Nondurables Services

18A Lot of Fuel for the Fire

Real Personal Saving: Actual and Hypothetical No Pandemic Scenario

Billions of $2012

7,000

The passage of the

ARP Act will

increase saving

6,000

Actual

even more.

5,000

Hypothetical

3,930

4,000

3,000

Key question: How

$2.7 Trillion

2,000

much of this extra

1,000

1,168 saving is

0

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

precautionary?

NOTE: Last observation is January 2021.

19PCE-Services: Jet Fuel

PCE Services: Actual and Hypothetical No Pandemic Scenario

Billions of $2012

9,500

Actual Currently, PCE Goods

9,000

expenditures are 10% above it

Hypothetical

8,500

pre-pandemic peak.

$764 Billion

8,000

If real PCE services exceeds its

pre-pandemic peak by 10% in

7,500 Dec. 2021, this will increase

real GDP by about 6.5%

7,000 above its 2020:Q4 level.

6,500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

SOURCE: BEA, Haver Analytics, and author's calculations.

20Have Vaccine, Will Eat Out . . . Will Travel

Open Table Seated Diners at Restaurants: United States US Airline Passenger Traffic Since February 1, 2020

Percent change from a year earlier

Total Passengers

10 2,500,000

0 Actual Current 7-Day Mov. Avg.

-10

7-Day Moving Avg.

2,000,000

-20

-30

1,500,000

-40

-50

1,000,000

-60

-70

-80 500,000

-90

-100 0

20200218 20200518 20200818 20201118 20210218 1-Feb 1-Apr 1-Jun 1-Aug 1-Oct 1-Dec 1-Feb

SOURCE: Open Table and Haver Analytics Data through Mar. 19, 2021 SOURCE: TSA Data through March 22, 2021

As of March 22, a little less than 80 million U.S. persons have received at least one dose. This

number represents about 30% of the population age 16 and older.

21Inflation Remains Below 2%

2% is the Fed’s

inflation target.

Data through January 2021.

22Firms are Reporting Price Pressures

ISM Manufacturing and Nonmanufacturing Prices Indexes

Index, 50+ = More respondents reporting higher than lower prices

90

Manufacturing

80

Nonmanufacturing

70

60

50

40

30

Jan.2013 Jan.2015 Jan.2017 Jan.2019 Jan.2021

Last actual observation is February 2021

23Rising Fuel Prices

Retail Gasoline and Diesel Prices: Actual and March 2021 EIA Forecast

Dollars per barrel

$3.50

Diesel

$3.00

$2.50

Gasoline

$2.00

Gasoline Forecast Diesel Forecast

$1.50

$1.00

Jan.2019 Jul.2019 Jan.2020 Jul.2020 Jan.2021 Jul.2021 Jan.2022 Jul.2022

SOURCE: U.S. Energy Information Administration. NOTE: Last actual observation is week ending, March 15, 2021

24And Inflation Expectations Are Rising

Breakeven Inflation Rates: 0-5 Years and 5Y5Y Forward

Percent

3.0

FOMC, March 17

2.5

2.0

1.5

1.0

5Y5Y 5Y

0.5

0.0

Dec.2017 Aug.2018 Apr.2019 Dec.2019 Aug.2020 Apr.2021

NOTE: Last actual observation is March 19, 2021

25Forecasters Expect Interest Rates to

Remain Low Over the Next Year

What Are Forecasters Predicting for 3-Month and

10-Year Interest Rates?

Percent, at annual rates

4.0

10-Year Yield Forecast But the 10-Year

3.0

(2021:Q1 to

2022:Q1)

Treasury is already

2.0 yielding about

1.75%.

1.0

3-Month Yield

0.0

2018:Q1 2018:Q4 2019:Q3 2020:Q2 2021:Q1 2021:Q4

SOURCE: Survey of Professional Forecasters, Feb. 2021.

26Inflation is Currently Low But Maybe

Not for Very Long.

• The probability of an inflationary impulse seems high.

All the ingredients are there.

‒ Price declines caused by the pandemic should reverse as

the economy strengthens.

‒ Rising input prices (e.g., commodities), exacerbated by

supply chain issues in some industries.

‒ Record money growth, rising debt and deficits, and a Fed

actively striving to run a “hot” economy.

27The FOMC’s Economic Outlook

March 2021 FOMC Economic Projections

Percent

10.0

2020 (A) 2021

8.0

6.5 6.8 2022 Longer run

6.0

4.5

4.0 3.9 4.0

3.3

2.4 2.0 2.0

2.0 1.8

1.2

0.0

-2.0

-2.4

-4.0

Real GDP Unemployment Rate PCEPI Inflation

NOTE: FOMC Projections are the median estimates of FOMC participants. The unemployment

rate is the average of the fourth-quarter for the year indicated.

28Risks to the Outlook

• So, what are some potential potholes?

• Problems might arise with the new vaccines; or, a new virus

strain that is totally or partially immune to the new vaccines.

• Strong growth and huge deficits could cause a spike in

interest rates and inflation expectations. Overheating!

• Rising interest rates and an inflation spike could trigger

financial market distress and a possible sell-off in stocks.

• Something not on our radar.

29QUESTIONS?

30REGIONAL

ECONOMIC BRIEFING Louisville Regional

Economic Outlook

Charles S. Gascon

March 23, 2021

The views I will express are my own and do not necessarily reflect the

positions of the Federal Reserve Bank of St. Louis or the Federal Reserve

System.Was the pandemic shock

localized?

Two pictures of the recovery

Outline

Short-run outlook

Long-run outlook

1We have all seen maps like this

Share of population with a reported COVID-19 case: Range 1:40 to 1:8

Source: New York Times, Accessed 3/22/2021

2Or even maps like this

Unemployment Rate by State: January 2021

3Or even maps like this

Unemployment Rate by State: January 2021

But maps like these are

designed to highlight differences

4Regional impact is more the same than different

Total

-5.6%

-6.5%

Hospitality: -22.5%

5Where you work matters more than where you are

Summary of employment changes Summary of employment changes

across 350 US MSAs across US major sectors (2-digit NAICS)

Feb. to Apr. Apr. to Dec. Feb. to Apr. Apr. to Dec.

Average -13 9 Average -13 9

Min -33 -1 Min -53 -4

Max -5 29 Max -1 51

+/-1 Std. Dev. -17 to -9 5 to 13 +/-1 Std. Dev. -27 to 1 -5 to 23

6Low-income workers have been more severely impacted

Employment Level relative to January 2020

10.0

5.0 4.1%

0.0

-5.0 -5.3%

-10.0 -10.1%

-15.0 -15.5%

-20.0

-25.0

-30.0

-35.0

-40.0

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21

US LOI-High Income LOI-Low Income LOI

Source: Payechex, Ernin, Intuit, and Kronos via Opportunity Insights

7Two pictures of the recovery

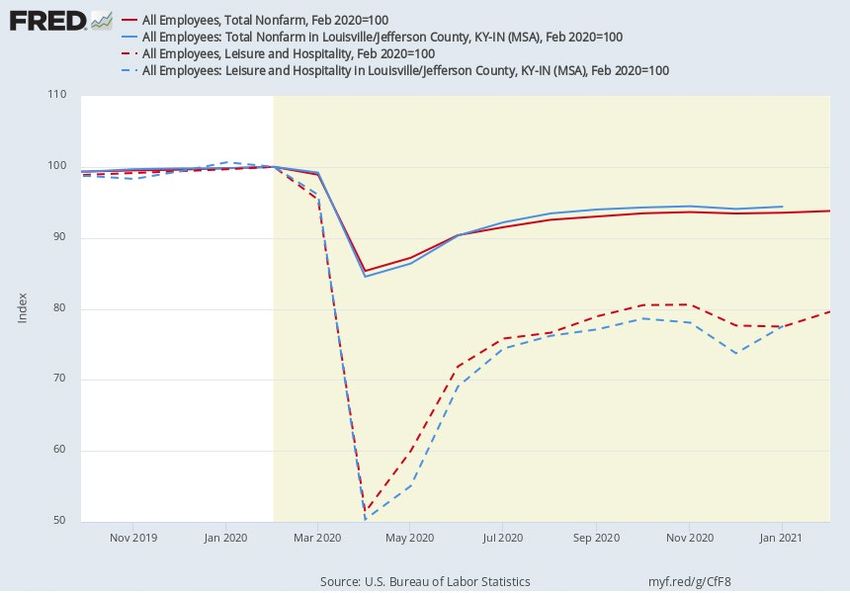

8A quick rebound: look at the unemployment rate!

Jan 2021

6.3

4.7

9A long way to go: look at total employment!

-38,100 jobs

-42,300 jobs

10How to reconcile these two pictures?

Labor Force Nonfarm Employment Unemployed Unemployment

Payrolls Rate

Feb 2020 679,000 680,000 655,000 24,000 3.5%

Jan 2021 659,000 641,900 627,000 31,300 4.7%

Diff -20,000 -38,100 -27,200 7,300 1.2%

¼ are out of

¾ are out of labor force unemployed

• Does this mean unemployment rate is really 7.6%? No

• Changes in the unemployment rate will depend on if, and how, people re-enter

labor force.

11Where is the economy headed?

Forecasts for 2021

US US Kentucky Louisville

(FOMC*)

Real GDP Growth (Q4/Q4) 6.5 5.9 5.2 6.0

Unemployment Rate (Q4) 4.5 4.9 5.0 4.9

Forecasts for 2022

US US Kentucky Louisville

(FOMC*)

Real GDP Growth (Q4/Q4) 3.3 2.9 3.3 3.5

Unemployment Rate (Q4) 3.9 3.8 4.5 4.2

Source: IHS/Markit; *Federal Reserve Board of Governors, March 2021 Summary of Economic Projections

12Where is the economy headed in the next 5 years?

• Future of telework, what does it mean for cities?

• Look to trends and not the cycle

• Slow growth on the horizon?

– Aging population and low rates of immigration

– Loss of human capital from no school and declines in labor

force participation are concerning

– Focus on economic equity and inclusive growth could expand

labor force

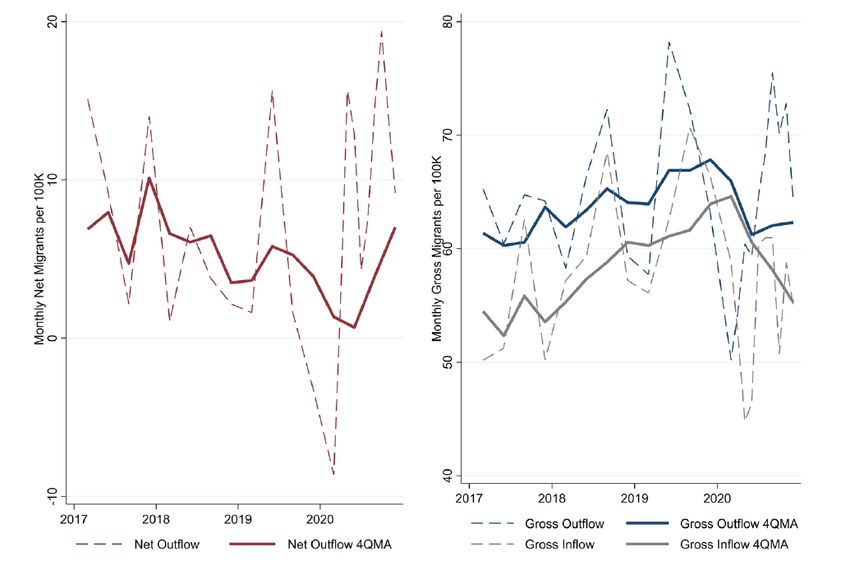

13Are people fleeing urban neighborhoods due to COVID-19?

Average Louisville

Metro

Change in Net Flow 24 21

Change in Outflow 5 1

Change in Inflow -20 -21

Note: Values per 100,000 Residents

Source: Whitaker “Did the COVID-19 Pandemic Cause an Urban Exodus?” March, 2021

14Are people fleeing? Not really.

Estimated Gross and Net Migration into and out of Urban Neighborhoods: Louisville, MSA

Source: Whitaker “Did the COVID-19 Pandemic Cause an Urban Exodus?” March, 2021

15What does telework mean for cities?

• A survey of 22k Americans found 22% of all workdays would be supplied

from home after the pandemic. Up from 5% pre-pandemic.

• Economic models find that when WFH increases, jobs move to the core of

cities and residents move toward the suburbs.

• Housing prices near city center should grow slowly, while suburban

housing prices would grow faster.

• Impact on congestion is unclear:

– Commutes per week decline

– weekly commuting miles may not change

– non-work commuting would likely increase.

16When will Louisville regain all jobs from the pandemic?

Nonfarm Payroll Employment (Actual and Forecast)

Index 2019:Q4=100

105

US LOI

2022:Q3

100

95

90

85

2016 2017 2018 2019 2020 2021 2022 2023 2024 202

Source: IHS/Markit

17Where is the economy headed?

Forecasts for 2025

US FOMC- US Kentucky Louisville

(Longer Run)

Real GDP Growth (Q4/Q4) 1.8 2.3 1.8 1.8

Unemployment Rate (Q4) 4.0 3.6 4.2 3.8

Source: IHS/Markit; *Federal Reserve Board of Governors, March 2021 Summary of Economic Projections

18Don’t lose sight of the trend during the cycle

19Concluding thoughts

• COVID-19 impact

– More similar than different across US Metro areas.

– Recession accelerated trends already occurring, the goal is to move forward, not back.

• The long-term outlook is for slower employment growth due to an aging

population and low rates of in-migration.

• Telework creates a disconnect between location of jobs and households,

particularly at the upper-income.

– Attracting business to stimulate migration becomes more problematic in this environment.

– A renewed focus on households and their decision-making process is important for regional

economic growth post-pandemic.

• Decisions ahead: Regional leaders must balance the desire to promote a quick

recovery and making investments that accelerate trend growth.

20You can also read