Thailand Key Hotel Market Trends & Outlook - November 2021 - Horwath HTL

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Thailand

Key Hotel Market Trends & Outlook

November 2021

Thailand Key Hotel Market Trend & Outlook

Horwath HTL Methodology

Analyze historical performance, demand characteristics, travel Review existing supply and pipeline to

01 and tourism drivers for Thailand relative to global markets

03 identify trends and model supply outlook

Historical Reopening and Historical Historical RNA

ADR Vaccination Progress RNO Source: STR

Source: STR Source: TAT and Our World in Data Source: STR &

Horwath HTL

Estimate Room Additions to Hotel Markets

Forecast hotel performance based on historical statistics, Source: Horwath HTL

02 recovery patterns, demand growth by segment & nationality

Forecast RNO Forecast RNA

04 Use RNO and RNA to calculate market occupancy

Forecast ADR Forecast Occupancy %

05 Check for anomalies and draw conclusion

2022 THAILAND HOTEL MARKET OUTLOOK

Note: RNO = Room Night Occupied, RNA = Room Night Available, ADR = Average Daily Rate

© 2021 Horwath HTL 2

Thailand Reopening & Vaccination Progress

Reopening Plan Update • The Thai authorities expect one million tourist

arrivals from November 2021 to March 2022. For

• The kingdom has reopened its doors to fully the first half of November, a new record of 50,000

vaccinated travellers from 63 countries without a visitors is a big improvement from 100,000 visitors

quarantine requirement since November 1, 2021. through various entry schemes during January-

The list includes a majority of Thailand’s October. The Phuket Sandbox program in

important source markets, such as China, the particular attracted 60,000 visitors from July to

U.S., the UK, and many European countries. October, with the top five markets being the U.S.,

Israel, the UK, Germany, and France.

• Besides full-dose vaccination, the Thailand entry

checklist includes additional screening measures: • However, the travel and tourism industry should

1. A stay in the listed 63 countries for the past 21 be mindful of inconsistency and uncertainty of

consecutive days; restrictions across countries. China and Australia,

2. Negative PCR test result within 72 hours for example, have maintained border closures

before departure; over travel to Thailand. Reciprocal free travel

3. PCR test upon arrival; and between Thailand and any countries depends on

4. Medical insurance with a coverage of USD both the achievement of national vaccination

50,000. coverage and the governments’ sentiment

towards the pandemic.

• Fully vaccinated travellers from countries that are

not on the exemption list will be able to choose Vaccination Progress

from the 17 ‘Blue Zone’ destinations (expanded

coverage from the Sandbox model), including • Thailand has started COVID-19 vaccination since

Bangkok, Phuket, Pattaya and Hua Hin, for a February, 2021. As of October 31, around 11.5

seven-night mandatory stay within the destination million (16 percent) of the Thai population are

before travelling to other parts of the country. partly vaccinated and 30.7 million (44 percent) are

fully vaccinated. The inoculation rate accelerated

• A ten-day quarantine measure remains in place in the second of half of 2021 and, since October,

for unvaccinated travellers. around 600,000 to 800,000 doses are

administrated daily. The vaccines used are mainly

• A night-time curfew (11pm to 3am) was lifted Sinovac/Sinopharm (49 percent) and Astra

nationwide except for 6 high risk provinces, which Zeneca (45 percent). mRNA makes up a small

are not tourism hotspots. Meanwhile, a temporary fraction of 6 percent.

ban on night entertainment has been extended to

mid January. • The government aims for 100 million doses or 50

million fully vaccinated people, a 70 percent target

© 2021 Horwath HTL for national immunity, by the end of 2021. 3

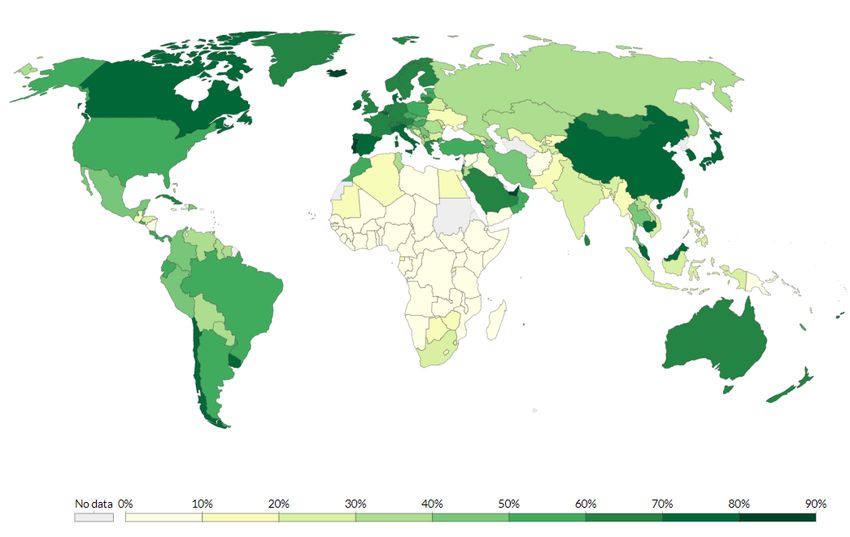

Global Pandemic Situation at a Glance

As of October 31, 2021

Europe

Vaccination Rate: 55%

Total Cases (millions): 65.38

Cases per Million People: 87,292

Death Rate%: 2.0%

North America

Vaccination Rate: 52%

Total Cases (millions): 55.28

Cases per Million People: 92,666

Death Rate%: 2.0% Asia

Vaccination Rate: 43%

Total Cases (millions): 79.37

Cases per Million People: 16,964

Death Rate%: 1.5%

South America

Vaccination Rate: 52% Africa

Total Cases (millions): 38.37 Vaccination Rate: 6%

Total Cases (millions): 8.50 Oceania

Cases per Million People: 88,369

Cases per Million People: 6,188 Vaccination Rate: 48%

Death Rate%: 3.0%

Death Rate%: 2.6% Total Cases: 260,526

Cases per Million People: 6,028

Death Rate%: 1.1%

Vaccination Rate

© 2021 Horwath HTL Source: OurWorldindata.org 4

Pandemic Situation in Thailand vs. Key Source Markets

As of October 31, 2021

China 75% 10% 85% 97,320 67 4.8%

Total Cases Cases per Mil People Death Rate

United Kingdom 67% 6% 73% 9.1 M 133,424 1.6%

Total Cases Cases per Mil People Death Rate

United States 57% 9% 66% 46.01 M 138,195 1.6%

Total Cases Cases per Mil People Death Rate

Thailand 44% 16% 60% 1.91 M 27,334 1.0%

Total Cases Cases per Mil People Death Rate

Europe 55% 5% 59% 65.38 M 87,292 2.0%

Total Cases Cases per Mil People Death Rate

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Share of people fully vaccinated Share of people only partly vaccinated

© 2021 Horwath HTL Source: OurWorldindata.org 5

Pandemic Situation in Thailand vs. Key Source Markets

Vaccinations vs. Deaths – January 1, 2021 to October 31, 2021

20

Daily new COVID-19 deaths per million people

15

10

5

0

0 40 80 120 160

January 1, 2021 Total vaccination doses administered per 100 people October 31, 2021

UK China US Thailand Europe

© 2021 Horwath HTL Source: OurWorldindata.org 6Thailand Hotel Performance Trends

Occupancy ADR

• As in many tourism-dependent countries, • The nationwide ADR in Baht dropped by 9

Thailand’s hotel market has been hit hard by the percent in 2020. Phuket’s unusually high ADR

COVID-19 pandemic. In 2020, hotel occupancy was led by a peak season in Q1 before COVID-

dropped sharply by 44 percentage points 19 hit the world. With strong domestic support,

nationwide. Pattaya and Hua Hin benefitted from Hua Hin maintained its ADR level. Meanwhile,

strong domestic demand and were able to volume driven markets like Bangkok and Pattaya

achieve relatively higher occupancies compared continued to register rates below the nationwide

to Bangkok and Phuket. These two world-famous average. Bangkok’s ADR took the most severe

destinations are vulnerable to international hit as its shortfall was more significant than in any

demand volatility. of the three markets.

• With a series of major outbreaks and lockdowns • As of YTD August 2021, ADR weakened further

in 2021, Pattaya and Hua Hin could not sustain across all four markets, to a larger extent for

Bangkok their occupancy levels. A downfall was more Phuket and Bangkok. Phuket’s rate fell by 46

apparent in Pattaya while Hua Hin was better at percent YOY as its focus switched to the

Pattaya containing the spread. As of YTD August, domestic market. Bangkok’s rate slid by 33

Pattaya and Phuket’s occupancy levels were percent YOY and was ranked at the bottom due

below the nationwide average. Despite the mass to low-rate quarantine business.

Hua Hin vaccination coverage and the launch of Phuket

Sandbox model by July, complicated travel

measure and low season weather deterred RevPAR

holidaymakers from spending time in Phuket. On

the other hand, Bangkok and Hua Hin recorded • The nationwide RevPAR declined significantly

superior occupancy levels, attributed to from THB 2,329 in 2019 to THB 848 in 2020, by

quarantine and domestic vacation demand 64 percent.

respectively.

Phuket • As of YTD August 2021, a further decline to THB

391 was recorded. In comparison to 2019 level,

RevPAR was down by 83 percent.

© 2021 Horwath HTL Source: Google Images 7Thailand Hotel Performance Trends

Performance Snapshot, 4 Key Markets, 2019 to 2021 YTD August

THB 4,500

THB 4,000

Phuket Hua Hin

Hua Hin

THB 3,500 Phuket

Hua Hin

ADR

THB 3,000 Bangkok

Pattaya Pattaya

THB 2,500 Bangkok

Phuket

THB 2,000

Pattaya

Bangkok

THB 1,500

0% 10% 20% 30% 40% 50% 60% 70% 80%

Occupancy

YTD 2021 2020 2019

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 8Thailand Hotel Performance Trends

Occupancy & Recovery Index Comparison, 4 Key Markets, 2019 to 2021 YTD August

Occupancy Recovery Index Against 2019 Level

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 9Thailand Hotel Performance Trends

ADR & Recovery Index Comparison, 4 Key Markets, 2019 to 2021 YTD August

ADR Recovery Index Against 2019 Level

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 10Thailand Hotel Performance Trends

RevPAR & Recovery Index Comparison, 4 Key Markets, 2019 to 2021 YTD August

RevPAR Recovery Index Against 2019 Level

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 11Thailand vs. Global Comparison

• Several factors come into play for the healing of Latest news showed the widespread emergence of

the travel and tourism industry, which could turn Delta variant in China and sudden outbursts in many

into a gradual and lengthy process. Looking at the parts of Europe such as the UK, Germany and

global hotel market, a recovery journey is Austria. The uncertainty raised a public concern over

contingent on not only vaccination progress, but vaccine efficacy against new variants and the

also the relaxation of movement control and border readiness of health care system in handling a new

restriction. Air connectivity and travel procedures, normal of living with COVID-19.

such as the EU Digital COVID-19 certificate, play

important roles in influencing a return of travellers. ADR

• Demand in the early stage of the world’s reopening Overall, rate recovery appears to be weak to mild

is mainly from domestic and short-haul regional across most hotel markets while they are rebuilding

travels. China benefited from keeping opulent occupancy. Without high yielding international

tourism demand within the country. Singapore rode demand, Thailand and Singapore saw ADR plunging

out the pandemic with quarantine and staycation through 2021.

bookings on the back of its relatively small market.

Specifically for the U.S. and Europe, a strong The only exception, Maldives drove 2020 and 2021

summer travel season signalled a market rebound. YTD ADRs up from the pre-pandemic level mainly

due to high season performance in Q1.

• On the contrary, Maldives’ success story hinged on

its first mover advantage to consolidate beach

vacation demand while access to tropical islands RevPAR

around the world remained tightly controlled. Its

promotion of winter escapes strongly appealed to Maldives is one of the pioneers to successfully open

the European market, particularly Russian- up for foreign travellers even when it had not

speaking countries. The number of visitors from achieved herd immunity. Its focus on tranquil getaway

this region in 2021 exceeded a pre-covid level. experience is compatible with social distancing norms

and isolation requirements.

• However, during a transition period, several

frontrunning countries on the national vaccination The U.S. and China were able to curb the virus

coverage experienced a subsequent surge in new spread and stabilize domestic activities for the most

cases after the easing of travel precautions. They part of 2021, resulting in a quick RevPAR turnaround.

went back into another lockdown, which became a

setback for the hotel market. Examples include In contrast, Thailand was ambushed by the Delta

The UK, UAE and Maldives. variant and entered another long lockdown while

ramping up inoculations, hurting 2021 RevPAR.

© 2021 Horwath HTL Source: Google Images 12Thailand vs. Global Destinations

5 Select Markets, Occupancy & Recovery Index Comparison, 2019 to 2021 YTD August

Occupancy Recovery Index Against 2019 Level

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 13Thailand vs. Global Destinations

5 Select Markets, ADR & Recovery Index Comparison, 2019 to 2021 YTD August

ADR Recovery Index Against 2019 Level

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 14Thailand vs. Global Destinations

5 Select Markets, RevPAR & Recovery Index Comparison, 2019 to 2021 YTD August

RevPAR Recovery Index Against 2019 Level

© 2021 Horwath HTL Source: STR and Horwath HTL Analysis 15Thailand Demand and Supply Factors

Demand and supply trends in Thailand and a broader However, some headwinds listed below are inevitable.

global context are taken into consideration to determine

where the Thailand hotel market is heading in 2022. • Gradual return of international demand has been

evident from the Phuket Sandbox Model on the

The following positive movements in Thailand and its back of tedious and unclear travel procedures as

key source markets will stimulate demand growth. well as additional travel costs from testing and

insurance requirements;

• Thailand’s reopening to fully vaccinated travellers

from countries on the quarantine exemption list. • China, the largest single source market for

Such a bold move is expected to induce demand Thailand, is likely to keep its border closed until

from key source markets that have scaled back the National Congress in October 2022. Another

border restrictions such as the U.S., the UK and major demand source for Thailand beach resorts,

Europe; Russia is not on the quarantine exemption list in

the meantime due to low vaccination rate;

• Pent-up demand and the upcoming high season.

Several industries and affluent business people • Vaccine efficacy against new variants, uncertainty

are not affected by the COVID-19 situation and of vaccine immunity period and risk of subsequent

have a high propensity to spend; outbreaks as evident across the world;

• Thailand’s full-dose vaccination rate is expected to • Competition from destinations that have recently

reach 70 percent by end-2021 and higher levels in followed Thailand’s restriction easing; and

main tourism spots;

• Supply pressure on occupancy and ADR growth

• Domestic corporate and leisure demand boosted from newly constructed hotels, alternative

by travel stimulus packages (so-called in Thai accommodations (e.g. condotels and room

“Rao Tiew Duay Gan”); rentals) and reopening of hotels that were closed

during the pandemic.

• Further improvement of immunization coverage

globally and green shoots evident in the U.S. and Going forward, it is expected that transient demand,

Europe; and particularly among leisure travellers, will enjoy the

most significant recovery in 2022. Meanwhile, group

• Appreciation of major currencies against Baht. demand will likely be sourced from the domestic

corporate market. International corporate and leisure

groups from China, South Korea, Japan and India

show no sign of immediate return.

© 2021 Horwath HTL 16Demand Characteristics

Business Mix (LHS) & Nationality Mix (RHS), 2019

Business Mix Nationality Mix

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Bangkok Pattaya Hua Hin Phuket

Transient Group Others

© 2021 Horwath HTL 17Supply Pipeline

By Opening Year (LHS) & By Positioning (RHS)

New Hotel Rooms by Opening Year 2022 New Supply by Positioning

5,000

Luxury

4,500

4,000

Upper

Midscale & Upper Upper

3,500 Below Upper Midscale & Upscale &

Upscale & Below Upscale

3,000 Upscale

2,500

2,000

Bangkok Pattaya

1,500

1,000 Luxury

500

0

Upper

Bangkok Pattaya Hua Hin Phuket Upper Upper Upscale &

Midscale & Luxury Midscale & Upscale

2019 2020 2021 2022 Below Below

© 2021 Horwath HTL Hua Hin Phuket 18Supply Movements

Total Room Nights Available, YOY Change, 2018 to 2022

40%

Bangkok Pattaya Hua Hin Phuket

30%

20%

10%

0%

-10%

-20%

-30%

-40%

2018 2019 2020 2021 2022

© 2021 Horwath HTL 192022 Thailand Hotel Market Outlook

Thailand’s continued efforts in achieving herd Despite a strong domestic support and a relatively

immunity and reopening for a much needed moderate supply increase, Pattaya is expected to

international support, on top of optimism in major pick up even more slowly, due to its heavy reliance

advanced economies, show a glimpse of hope that on Asian markets and group demand. According to

the country is coming out of the pandemic. In our the International Air Transport Association (IATA),

opinion, the overall hotel market is also expected to Asia’s regional travel is anticipated to be relatively

bottom out, but its initial recovery is known to be sluggish due to the modest easing of border controls.

slow and unsteady. The market performance is Uncertainty looms over outbound travels from China

unlikely to return to a pre-COVID level in 2022. and India, which have proven to be a strong base for

Pattaya in normal days.

Hua Hin is expected to lead the performance in

both occupancy and ADR in 2022, driven by the The recovery of Hua Hin and Pattaya will drive

first wave of returning Europeans on the back of its growth in Bangkok, the gateway to Thailand.

strong reputation among locals. The domestic However, it will inevitably face supply challenges

market makes up at least one-third of total demand. similar to Phuket i.e. a massive supply pipeline and a

Additionally, the commercialization of the Hua Hin full resumption of existing hotels’ operation. Like

International Airport will make Hua Hin “open to the Pattaya, the capital will endure a slow recovery in

world” and thus attract more foreign visitors who Asian markets, particularly group demand. The two

prefer relaxed and peaceful holidays with local negative causes will exert an enormous pressure on

lifestyles. Bangkok’s occupancy and ADR growth.

As the very first Asian resort destination to open up,

Phuket should witness a relatively strong

international demand rebound in the high season,

especially with the reopening of Phi Phi islands

after a two-year rehabilitation. However, it is

anticipated that Phuket’s recovery pace will be

slower than Hua Hin’s due to a rapid increase of

new supply, the reopening of existing hotels that

previously suspended operation, and limited

demand from two major source markets, China and

Russia.

© 2021 Horwath HTL 20Thailand Hotel Market Outlook Forecast vs. Historical Performance, 4 Key Markets, 2019 to 2022 © 2021 Horwath HTL Source: STR and Horwath HTL Analysis 21

Thailand Hotel Market Outlook

Occupancy Forecast, 2022

2019 2022 Forecast

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Bangkok Pattaya Hua Hin Phuket

© 2021 Horwath HTL 22Thailand Hotel Market Outlook

ADR Forecast, 2022

2019 2022 Forecast

THB 4,000

85-95%

Recovered

THB 3,200 80-90%

Recovered

75-85% 80-90%

THB 2,400 Recovered Recovered

THB 1,600

THB 800

THB 0

Bangkok Pattaya Hua Hin Phuket

Exchange Rate: EUR/THB=36.9715

© 2021 Horwath HTL 23Thailand Hotel Market Outlook

RevPAR Forecast, 2022

2019 2022 Forecast

THB 2,500

THB 2,000

THB 1,500

45-60%

Recovered

THB 1,000

30-45%

25-40% Recovered

Recovered 25-40%

Recovered

THB 500

THB 0

Bangkok Pattaya Hua Hin Phuket

Exchange Rate: EUR/THB=36.9715

© 2021 Horwath HTL 24Authors

Nikhom Jensiriratanakorn (aka Nick) is a Director Vicky Jian is a Project Director of Horwath HTL, based in

of Horwarth HTL. Nikhom has advised both local the Singapore office. She joined Horwath HTL in 2014

and international investors in the Thailand after graduating from the School of Hotel Administration

hospitality sector and extends oversight to the at Cornell University. Since then, she has worked on

Indochina region. more than 50 hotel related assignments in 8 countries

across the Asia Pacific region, including Maldives,

He has brought with him comprehensive skills in Indonesia, Malaysia, Vietnam, Thailand, China,

feasibility analysis, investment underwriting and Philippines, and Singapore. She has strong experience in

asset management, as well as years of conducting feasibility studies, valuations, repositioning/

experience with hotel management companies, renovation studies, and destination master planning.

investment funds and consulting firms, namely

Pan Pacific Hotels Group, Jumeirah Group, Host Vicky’s expertise is in market and financial feasibility and

Hotels and Resorts and PricewaterhouseCooper valuation for resort destinations, which involves market

Thailand respectively. research, site inspection, competitor analysis, best-use

Nikhom Jensiriratanakorn Vicky Jian facility recommendations and financial projections. She

Director Project Director also manages the Horwath HTL Annual Benchmarking

Horwath HTL Thailand Horwath HTL Singapore Studies, which cover 15 Asian markets with a total of

nikhom@horwathhtl.com vjian@horwathhtl.com approximately 2,500 hotels and serviced apartments

participating every year.

© 2021 Horwath HTL 25Horwath HTL

At Horwath HTL, our focus is one hundred percent Our Expertise: Horwath HTL Thailand

on hotel, tourism and leisure consulting. Our services The Great Room,

cover every aspect of hotel real estate, tourism and • Hotel Planning & Development Gaysorn Tower Level 25-26,

leisure development. • Hotel Asset Management 127 Ratchadamri Road,

We are a global brand with 52 offices in 40 countries, • Hotel Valuation Lumpini, Pathumwan,

who have successfully carried out over 30,000 Bangkok, Thailand

• Health & Wellness +66 62 891 9478

assignments for private and public clients.

• Transactional Advisory

We are part of Crowe Global, a top 10 accounting Horwath HTL Singapore

and financial services network. We are the number • Expert Witness & Litigation

15 Scotts Road, #08-10/11,

one choice for companies and financial institutions • Tourism & Leisure Thong Teck Building,

looking to invest and develop in the industry. Singapore

• Hospitality Crisis Management

We are Horwath HTL, the global leader in hotel, +65 6735 1886

tourism and leisure consulting.

www.horwathhtl.asia

© 2021 Horwath HTL 26Thank You

Africa

Rwanda

South Africa

Asia Pacific

Australia

China – Beijing

Europe

Andorra

Austria

The Netherlands

Poland

Latin America

Argentina

Brazil

North America

Atlanta, GA

Denver, CO

China – Hong Kong Croatia Portugal Chile Los Angeles, CA

China – Shanghai Cyprus Russia Dominican Miami, FL

China – Shenzhen Germany Serbia Republic New York, NY

India Greece Spain Mexico Norfolk, VA

Indonesia Hungary Switzerland Orlando, FL

Japan Ireland Turkey Canada – Montréal

Malaysia Italy United Kingdom Canada – Toronto

Middle East

New Zealand

Singapore UAE and Oman

Thailand

Horwath HTL is a member of Crowe Global, a Swiss verein. Each member firm of Crowe Global is a separate and independent legal entity. Horwath HTL and its affiliates are not responsible or liable for any acts or omissions of Crowe Global or any other member of Crowe Global. Crowe Global does not

render any professional services and does not have an ownership or partnership interest in Horwath HTL.

© 2021 Horwath HTLYou can also read