TCFD UPDATE 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE - Deloitte

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

TCFD UPDATE 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 10 Novembre 2021

Our Deloitte speakers

Laurence Rivat

Catherine Saire

Deloitte Partner

Deloitte Sustainability Partner

EU Corporate Reporting Policy Leader

TCFD Member

lrivat@deloitte.fr

csaire@deloitte.fr

Olivier Jan

Olivier Sautel

Deloitte Sustainability Partner

Deloitte Economic Advisory Partner

Climate & Energy Leader

osautel@deloitte.fr

ojan@deloitte.fr

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 2

Agenda

01

Introduction

02

TCFD Status Report

- Progress in implementing TCFD recommendations

- Sharing of good practices per TCFD pillar

- From theory to practice: Risk impact modelling- Example of tax carbon

03

Metrics TargeTs and Transition Plan

- TCFD climate metrics as per TCFD revised guidance

- Targets & Transition plan

- From theory to practice – Decarbonisation pathway and roadmap

- Financial impacts & Alignment with AMF / ESMA recommandations

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 3

Introduction

4

Overview of key TCFD Reports and Guidance © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 5

Core elements of the TCFD recommendation

Governance Strategy Risk Management Metrics and Targets

Disclose the organization’s governance Disclose the actual and potential Disclose how the organization Disclose the metrics and targets used

around climate-related risks and impacts of climate-related risks and identifies, assesses, and manages to assess and manage relevant climate-

opportunities. opportunities on the organization’s climate-related risks. related risks and opportunities where

businesses, strategy, and financial such information is material.

planning where such information is

material.

Recommended Disclosures Recommended Disclosures Recommended Disclosures Recommended Disclosures

a) Describe the board’s oversight of a) Describe the climate-related risks a) Describe the organization’s a) Disclose the metrics used by the

climate-related risks and and opportunities the organization processes for identifying and organization to assess climate-

opportunities. has identified over the short, assessing climate-related risks. related risks and opportunities in

medium, and long term. line with its strategy and risk

management process.

b) Describe management’s role in b) Describe the impact of climate- b) Describe the organization’s b) Disclose Scope 1, Scope 2, and, if

assessing and managing climate- related risks and opportunities on processes for managing climate- appropriate, Scope 3 greenhouse

related risks and opportunities. the organization’s businesses, related risks. gas (GHG) emissions, and the

strategy, and financial planning. related risks.

c) Describe the resilience of the c) Describe how processes for c) Describe the targets used by the

organization’s strategy, taking into identifying, assessing, and organization to manage climate-

consideration different climate- managing climate-related risks are related risks and opportunities and

related scenarios, including a 2°C or integrated into the organization’s performance against targets.

lower scenario. overall risk management.

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 6

2021 Status Report (Link here)

The TCFD Momentum

• Disclosure increased more last year than in any previous year

2600+ 50+ • Progress is still needed- only 50% of companies aligned with at least 3 recommended

disclosures

TCFD Supporters Central

globally Banks

(+73% in 1 year)

• More disclosure on climate-related risks and opportunities (over half of the companies)

USD25tn • Scenario disclosure still the least reported recommended disclosure but encouragingly increase

Combined company market from 5% in 2018 to 13% in 2020

capitalisation

(+92% in 1 year)

• Progress needed on the governance disclosure- recommended regardless of materiality

89

Countries and jurisdictions

represented • Materials and building companies now leading on dislosure

Top 5 : Japon, UK, US, Australia and France

8 • Significant progress in the insurance industry- leading disclosure on risk management processes

TCFD aligned officials

reporting requirements

(Brésil, HK, Japon, Singapore, Suisse, • Europe still the leading region for disclosure (16 percentage points more than the next closest

NZ, UE, UK)

region)

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 8

TCFD Aligned reporting © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 9

TCFD Disclosure example Climate governance (1/2) Source: Legal and General Group Plc, TCFD Report, 2020, p.10 © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 10

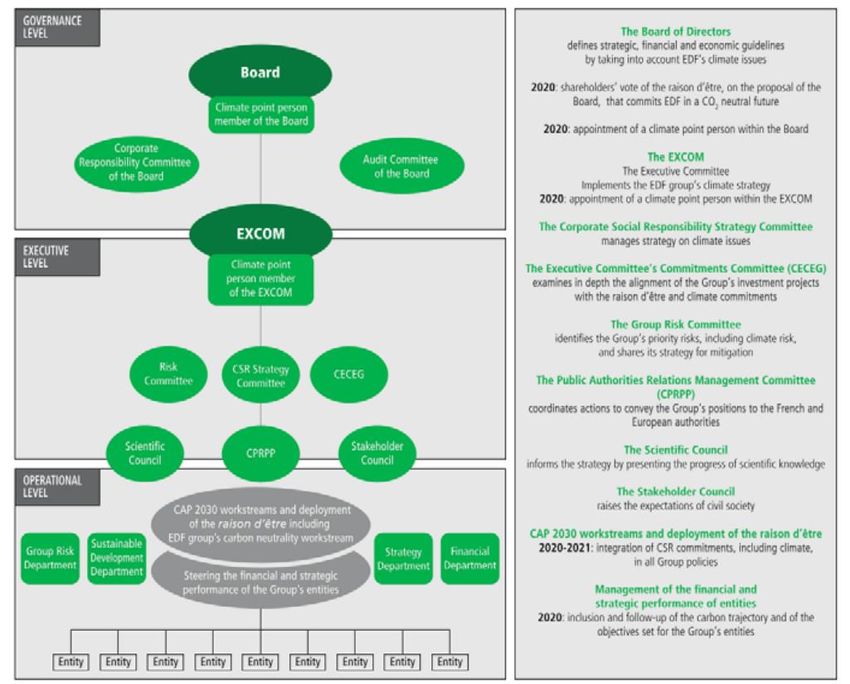

TCFD Disclosure example Climate governance (2/2) Source: EDF, Registration Document, 2021, p.141 © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 11

TCFD Disclosure example Scenario analysis (1/2) Source: Allianz Group, Sustainability Report, 2020, p. 86 © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 12

TCFD Disclosure example Scenario analysis (2/2) Source: Lendlease Annual Report 2021, p. 53 © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 13

TCFD Disclosure example

Risk Analysis (1/3)

Source: Orbia, TCFD Report, 2020, p. 2–3

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 14TCFD Disclosure example Risk Analysis (2/3) Source: Meridian Energy, Climate Change Disclosures Meridian Energy Limited FY20, p. 11 © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 15

TCFD Disclosure example Risk Analysis (3/3) Source: Meridian Energy, Climate Change Disclosures Meridian Energy Limited FY20, p. 11 © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 16

Moving from theory to practice

Risks impact modeling

Example of tax carbon

By Olivier Sautel

Deloitte Economic Advisory Partner

17Tarification du carbone

Quels enjeux ?

Illustration des mécanismes de

répercussion d’un surcoût carbone

De multiples dispositifs et des incertitudes sur les modalités

d’application, mais un consensus sur la nécessité d’internaliser le

coût social du carbone par une tarification de la tonne de CO2 Secteur D

Nécessité de passer à des estimations quantifiées appuyées sur Secteur A

des données opposables, sur un sujet qui concerne

nécessairement toutes les entreprises

Demande

Secteur B Secteur C

finale

Importance potentielle des comportements de répercussion le

long des chaînes de valeurs, au-delà des impacts directs pour

les secteurs émetteurs

Secteur E

Impact direct (taxe)

Difficulté pour une entreprise donnée d’appréhender Impact indirect négatif (répercussion subie)

l’ensemble de sa chaîne de valeur amont

Impact indirect positif (répercussion appliquée)

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 18Tarification du carbone

Proposition de méthodologie

Méthodologie de type Input-Output appuyée Développement par nos équipes d’un module

sur les matrices de relations sectorielles de simulation de surcoût et de sa répercussion

fournies par les données publiques

Outil de simulation des effets tout au long des

chaînes de valeurs, en fonction du

World Input-Output Database secteur/niveau de taxe/taux de répercussion

• Multisectoriel (54 secteurs), multi pays (Pays de la

zone ETS, USA, Chine, agrégat « reste du monde »)

Données d’émissions 2018 • Approche à technologie fixe, sans substitution

produit

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 19Tarification du carbone

Enjeux et défi d’application

Output de l’outil

▪ Estimation d’exposition au risque, en pourcentage du chiffre d’affaires

/ Ebitda, assortie de tests de sensibilité

▪ Travail en cours sur la traduction en termes de valorisation

d’entreprises

Personnalisation/

adaptation ▪ Calibration des émissions et du niveau de taxe directe

▪ Données d’achats et prise en compte de la spécificité de la spécificité

des consommations de l’entreprise par rapport à la moyenne sectorielle

▪ Ajustement du scope géographique

Approfondissement

▪ Prise en compte des plans de décarbonation sectorielle

▪ Approfondissement des comportements de réponse/substitution pour

les produits les plus affectés

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 202021 MTT Guidance (Link here)

Seven categories of metrics intended to support comparability

1. The Task Force believes all organizations should disclose absolute Scope 1 and Scope 2 GHG

emissions independent of a materiality assessment. The disclosure of Scope 3 GHG emissions is

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 subject to a materiality assessment; however, the Task Force encourages organizations to TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 22

disclose such emissionsThe importance of interim target © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 23

The transition plan © 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 24

Moving from theory to practice

Decarbonisation pathway and roadmap

By Olivier Jan

Deloitte Sustainability Partner

25Financial impacts & Alignment

with AMF / ESMA

recommandations

26Disclosure of financial impacts

TCFD RECOMMENDATIONS AMF & ESMA RECOMMENDATIONS

Impact on financial performance

• Increases in revenue from new products or services from

climate opportunities; Link here

• Increases in cost due to carbon prices, business

interruption, contingency, or repairs;

• Changes to operating cash flow from changes in upstream

costs;

• Impairment charges due to assets exposed to transition

risks; and

• Changes to total expected losses due to physical risks.

Impact on financial position Link here

• Changes to the carrying amount of assets due to exposure

to physical and transition risks;

• Changes to the expected portfolio value given climate

related risks and opportunities; and

• Changes in liability and equity due to increases or

decreases in assets (e.g., due to low-carbon capital

investments or to sale or write-offs of stranded assets).

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 27Enforcement priorities de l’ESMA 2021 – Eléments relatifs au reporting extra-financier

Informations liées au changement climatique

• Transparence des émetteurs sur leurs politiques liées aux enjeux climatiques (risques physiques et risque de transition) et les

résultats de ces politiques

‒ Mesures en place pour identifier les risques et/ou opportunités climatiques et leurs impacts

‒ Principaux risques et opportunités identifiés ayant un impact matériel sur les activités, leur gestion et les actions prises en

conséquence

• Suivi des risques

‒ Publication des indicateurs de suivis et analyse de ceux-ci par rapport aux objectifs fixés. Indicateurs à un niveau de

segmentation pertinent

exemple : indicateur de suivi de l’évolution des émissions de gaz à effet de serre (GES) par pays/région ou business

‒ Expliquer dans quelle mesure les trajectoires d’émissions sont alignées sur les objectifs de l’Accord de Paris (qualitativement et

quantitativement)

‒ Ces indicateurs comprennent les informations de scope 1, 2 et (si données fiables disponibles) de scope 3

‒ Expliquer qualitativement et quantitativement la progression de l’entreprise vers ces objectifs

• Contextualisation de la communication de l’entreprise sur les enjeux climatiques

‒ Intégration des enjeux climatiques dans la stratégie générale de l’activité, présentation des plans d’intégration des mesures

climatiques et objectifs liés

‒ Ne pas se limiter à des données historiques, présenter une information prospective

• Présenter les enjeux climatiques (stratégie, performance, objectifs, etc) dans la communication extra-financière ET dans les états

financiers avec cohérence. Si ces informations sont omises, expliquer pourquoi

© 2021 Deloitte SAS - Confidential Document – 10 Novembre 2021 TCFD UPDATE: 2021 STATUS REPORT AND METRICS, TARGETS AND TRANSITION PLANS GUIDANCE 28Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities. DTTL (also referred to as “Deloitte Global”) and each of its member firms are legally separate and independent entities. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more. In France, Deloitte SAS is the member firm of Deloitte Touche Tohmatsu Limited, and professional services are rendered by its subsidiaries and affiliates Deloitte is a leading global provider of audit & assurance, consulting, financial advisory, risk advisory and tax & legal services. With 312,000 professionals in 150 countries, Deloitte has gained the trust of its clients through its service quality for over 150 years, setting it apart from its competitors. Deloitte serves four out of five Fortune Global 500® companies. Deloitte France brings together diverse expertise to meet the challenges of clients of all sizes from all industries. Backed by the skills of its 6,900 employees and partners and a multidisciplinary offering, Deloitte France is a leading player. Committed to making an impact that matters on our society, Deloitte has set up an ambitious sustainable development and civic commitment action plan. © Deloitte SAS. Membre de Deloitte Touche Tohmatsu Limited

You can also read