Suncorp Employee Superannuation Plan - Member Booklet Issued 29 October 2011

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Suncorp Employee Superannuation Plan Member Booklet Issued 29 October 2011

Suncorp Portfolio Services Limited (Trustee) (ABN 61 063 427 958, AFSL 237905, RSE Licence No L0002059), Asteron Life Limited (Insurer) (ABN 64 001 698 228, AFSL 237903), Suncorp Life & Superannuation Limited (SLSL) (ABN 87 073 979 530, AFSL 229880) and Suncorp-Metway Limited (SML) (ABN 66 010 831 722, AFSL 229882), are related bodies corporate of Suncorp Group Limited (Suncorp) (ABN 66 145 290 124). Various products and services are provided by different entities of the Suncorp Group. The different entities of the Suncorp Group are not responsible for, or liable in respect of, products or services provided by other entities of the Suncorp Group. The obligations of the Trustee and the Insurer aren’t guaranteed by any other company within the Suncorp Group. Except as otherwise stated, Suncorp and its subsidiaries don’t guarantee the repayment of capital invested in or the investment performance of this product. This product is not a bank deposit or other liability and is subject to investment risk including possible delays in repayment and loss of the interest and principal invested. The Product Disclosure Statement (PDS) and the Member Booklet were prepared on 15 September 2011. The Trustee is the issuer of the PDS and Member Booklet and takes responsibility for its contents. Investment option information is provided by the investment managers which includes their objectives, strategies, asset allocations, fees and buy/sell spreads. The investment managers have consented to the publication of this information in the Member Booklet and haven’t withdrawn their consent at the time of its preparation. They take no responsibility for any other information in the PDS and Member Booklet. The Suncorp Employee Superannuation Plan is part of Suncorp WealthSmart Business Super. Suncorp WealthSmart Business Super (SPIN RSA0003AU) is part of the Suncorp Master Trust (Fund) (ABN 98 350 952 022, RSE Fund Registration No. R1056655). Applications can only be accepted from persons receiving this PDS (including electronically) within Australia. If you print an electronic copy, please ensure you print all pages of this PDS and the Member Booklet. If you would like a printed version, free of charge, just call us on 1800 652 489 or email us at staff.super@suncorp.com.au. Administration services are provided to the Suncorp Employee Superannuation Plan by Suncorp Portfolio Services Limited (ABN 61 063 427 958), a wholly owned subsidiary of the Suncorp Group. We reserve the right to refuse or reject an application for membership or insurance. Insurance cover offered through the Suncorp Employee Superannuation Plan is provided by the Insurer in a policy issued to us. This policy is a non-participating policy. Subject to confirmation from the Federal Court, from 1 January 2012, insurance cover offered through the Suncorp Employee Superannuation Plan provided by Asteron Life will be provided by SLSL and all references to ‘Asteron Life’ and ‘Asteron Life Limited’ should be replaced by SLSL. Throughout this PDS and the Member Booklet, unless otherwise specified, references to: • ‘we’, ‘us’, ‘our’ and ‘Trustee’ mean Suncorp Portfolio Services Limited • ‘adviser’ means a qualified financial adviser • ‘Insurer’ and ‘Asteron Life’ mean Asteron Life Limited • ‘bank account’ means an Australian bank, building society or credit union account • ‘business day’ means a Sydney business day other than a Saturday, Sunday or public holiday in Sydney • ‘licensee’ means an organisation that has obtained an Australian Financial Services Licence (AFSL) for the provision of financial services • ‘plan’ means the Suncorp Employee Superannuation Plan • ‘employer’ means the Suncorp Group, which includes GILD Insurance Litigation Pty Ltd (GILD) • ‘associated employer’ means an associated employer of the Suncorp Employee Superannuation Plan • ‘employee’ means an employee of the Suncorp Group, which includes GILD • ‘you’ and ‘member’ means a member of the Suncorp Employee Superannuation Plan.

Contents

Welcome to the Suncorp Employee Superannuation Plan 2

Contributions7

Managing your account 9

Accessing your benefits 11

Investments12

Diversified investment options 21

Single sector investment options 23

Information about the investment managers 39

Insurance45

Fees and costs 57

Taxation information 61

Keeping in touch 62

What happens when you leave the Suncorp Group? 65

Other things you need to know 66

Suncorp Employee Superannuation Plan Member Booklet 1

Welcome to the Suncorp Employee

Superannuation Plan

Welcome to the Suncorp Employee With Suncorp, you’re on the way to a better future for you

and your family.

Superannuation Plan – Super for the

Suncorp Team Additional information

The Suncorp Employee Superannuation Plan is part of This Member Booklet forms part of the Suncorp

Suncorp WealthSmart and your employer, the Suncorp Employee Superannuation Plan Product Disclosure

Group, has chosen Suncorp WealthSmart as your Statement (PDS), issued 29 October 2011. You should

superannuation fund. read both the PDS and this Member Booklet before

Suncorp WealthSmart is a whole of life superannuation making any investment or insurance decisions.

solution, with integrated pension options allowing you to You can get a copy of the PDS and this Member Booklet

continue your account into retirement. from our website, or if you’re a current Suncorp Group

We’d like to welcome you to the plan and invite you to get employee, from the Suncorp Employee Superannuation

to know your super account. After all, your super’s going to Plan page on the Suncorp Intranet. If you would like a

play a big role in your family’s financial security, and even printed version, free of charge, just call us on 1800 652

small decisions now could make a big difference later. 489 or email us at staff.super@suncorp.com.au. We’ll be

happy to help.

What you can expect from us

We take the responsibility for your investment very

Changes to the PDS and Member

seriously. That’s why we’ll do all we can to support you Booklet

and help you make the most of your super account. The information in the PDS, this Member Booklet and its

underlying Trust Deed may change.

How will we do this?

Where the change isn’t materially adverse, we may update

• We’ll keep things simple the information on our website at suncorp.com.au, or if

• If you’re unsure about where your super should be you’re a current Suncorp Group employee, from the

invested, we’ll help you with information about how to Suncorp Employee Superannuation Plan page on the

match your attitude to risk with your investment choice Suncorp Intranet.

– we can even set you up with an appointment to talk to We’ll give you a printed version of the updated information,

Standard Pacific, your plan’s financial adviser free of charge, on request.

• We’ll help you protect what’s important with insurance

within your super

• We’ll make it easy for you to manage your account, by

giving you a range of contact options – from online,

telephone, fax or post

2 Suncorp

Product Summary

The following sets out key features of the Suncorp Employee Superannuation Plan. Take a few

moments to get to know your account.

The choice is yours

Where you invest your superannuation is your choice. ‘Super Choice’ is legislation that allows you to choose where you want your

compulsory employer contributions paid, if you’re eligible. If your compulsory employer contributions are currently being paid

into another account and you’d like them to be paid into your Suncorp Employee Superannuation Plan account, fill in a ‘Standard

Choice Form’, available from our website.

Understanding your plan – What type of member are you?

There are a number of different types of members within the plan and it’s important to know which category you fall into.

The following table provides a summary of the different membership categories within the plan:

Category name Who is included in this category?

Employed member Currently employed members of the Suncorp Group, including currently employed members of

GILD Insurance Litigation Pty Ltd (GILD)

Non-employed member A member who has left employment with the Suncorp Group, including members who have left

employment with GILD

Associate employee member Employees of an employer associated with the Suncorp Employee Superannuation Plan, but not

employed by the Suncorp Group

Family account members A family member with a Suncorp Employee Superannuation Plan account linked to an

employed, non-employed or associate employee member

Your plan at a glance

Features

Investment minimums

Initial investment No minimum

Ongoing account balance $1,200

Regular contribution plan No minimum

Investment choice

Diversified investment 6

options

Single sector investment 32

options

Maximum number of You can invest in up to 20 investment options at the one time

investment options

Default investment option Suncorp Traditional Capital Guaranteed Fund

General features

Investment switching You have the flexibility to switch between investment options at any time

Auto-rebalancing You can choose to keep your investments in line with your investment strategy by rebalancing

quarterly, half-yearly or yearly

Family accounts Your family members can enjoy most of the benefits associated with your plan, including

competitive fees, by setting up their own Suncorp Employee Superannuation Plan account

linked to yours

Suncorp Employee Superannuation Plan Member Booklet 3

Welcome to the Suncorp Employee Superannuation

Plan continued

General features

Super consolidation service Consolidating your super accounts could reduce the amount of fees you pay and the amount of

paperwork you receive

We can help you transfer all your super balances into the one account, or, if you’d prefer to do it

yourself, we also have an online super rollover wizard

Lost super service We can help you find your missing super benefits by conducting searches on the Australian

Taxation Office (ATO) databases on your behalf

Non-lapsing death benefit You can have certainty over who’ll receive your death benefit without the hassle of needing to

nomination update your nomination every 3 years

Child pension You can provide your children under age 18 with a tax-effective income stream if you die

Anti detriment payment Your beneficiaries may receive an additional amount representing the contributions tax you paid

as part of your death benefit payment

Contribution methods Making contributions to your Suncorp Employee Superannuation Plan account is easy, and you

can choose from the following methods:

• direct debit

• BPAY® (from savings and credit card)

• cheque

• transfer from another super fund

• deposits at a Suncorp branch

Regular contribution plan Contribute regularly by direct debit when it suits you – monthly, quarterly, half-yearly or yearly

Insurance options The Suncorp Employee Superannuation Plan gives members the option of having the following

types of insurance:

• Death only cover

• Death & Total and Permanent Disability (TPD) cover and

• Income Protection cover

Online access Access your Suncorp Employee Superannuation Plan account at any time by logging on to

Suncorp WealthSmart online at suncorp.com.au

Member education Log on to Suncorp WealthSmart online at suncorp.com.au to access our member education

website, customised for members of the Suncorp Employee Superannuation Plan (provided by

Standard Pacific)

Email communications By providing us with your email address, you can choose to receive many of the more important

communications, such as annual statements, transaction confirmations and confirmations of

changes to your account details via email

If your employer gives us your email address, we’ll use this to communicate with you whenever

possible

Fees and costs for current employees of the Suncorp Group1,2

(If you are an eligible employee, your employer pays for your monthly member fee)

Contribution fee Nil

Administration fee Nil

Investment fee Ranges from 0% to 1.87% pa, depending on the investment option(s) selected3

Investment switching fee Nil

Withdrawal fee $60 for withdrawing your entire account balance

Member fee $5 per month

1 Other fees and costs may apply. Please see the ‘Fees and costs’ section in this Member Booklet for more information.

2 This is subject to change. Please see the ‘Fees and costs’ section in this Member Booklet for more information.

3 An investment fee does not apply to the Suncorp Bank Deposit Fund or the Suncorp Term Deposit Fund.

4 Suncorp

Other features of the Suncorp Employee

Superannuation Plan to suit your

lifestyle

The Suncorp Employee Superannuation Plan also offers

a range of other great benefits, to make managing your

super, simple.

Family ties

Keep it in the family with the Suncorp Employee

Superannuation Plan. Your family members can choose to

open their own super accounts within the plan which are

linked to your account. By opening a family account, not

only can they access most of the same features within the

Suncorp Employee Superannuation Plan, it could also save

them money. That’s because family account members

receive competitive fees – allowing them to reach their

retirement goals faster, just by being related to you!

For the purposes of family account linking, ‘family

member’ means your:

• spouse (including legal, de facto, and interdependency

relationship)

• child (including biological, step-child, adopted or in-laws)

• parents (including biological, adopted or in-laws) and

• siblings (including biological, adopted or in-laws)

Going part time?

Have you reached the age when you can retire but Anti-detriment benefit

aren’t quite ready to leave the workforce? The transition

The Suncorp Employee Superannuation Plan provides

to retirement feature within our Suncorp WealthSmart

an anti-detriment benefit if you die. This means your

Pension product allows you to access your super benefits

beneficiaries may get a refund representing the amount of

as a retirement income stream (if you are preservation

contributions tax you paid. This benefit is limited to your

age or older) while still continuing to work. It’s particularly

spouse (legal or de facto) and children and is only payable

beneficial for those aged 60 or over.

on lump sum benefits.

And when you’re ready to retire? Continued flexibility, even when you leave

You can feel confident knowing that the change will be employment with the Suncorp Group

simple and hassle-free. You may be able to transfer to

If you leave the Suncorp Group, you can still keep your

a Suncorp WealthSmart Pension without altering your

super account in the Suncorp Employee Superannuation

investments at all. The Suncorp WealthSmart Pension

Plan. We’ll also provide you with the information you need

provides regular income to fund your retirement needs,

so that your new employer can contribute to your Suncorp

while continuing to grow your savings in a tax-effective

Employee Superannuation Plan account on your behalf.

way.

For more information on what happens when you leave

For more information on the Suncorp WealthSmart

the Suncorp Group, please see page 65 of this Member

Pension, please see the Suncorp WealthSmart Personal

Booklet.

Super & Pension PDS which is available from our website,

or speak to your adviser.

Suncorp Employee Superannuation Plan Member Booklet 5

Welcome to the Suncorp Employee Superannuation

Plan continued

Important information about the Suncorp Employee Superannuation Plan for

associate employee members

If you’re an associate employee member you still get all of the great features of the Suncorp Employee Superannuation

Plan, however, some parts of the PDS and this Member Booklet do not apply to you.

For more information about what is different for you, please see the below table:

Section How is it different? Where can I get more information?

Fees and Costs Your employer does not pay for your ‘Fees and costs’ on page 57 of this Member Booklet

monthly member fee

Insurance Cover Your employer does not pay for your ’Insurance’ on page 45 of this Member Booklet

insurance premium

Access to a member only As you are an employee of an

web page and educational associated employer, you may only

tools access the member only web page

by logging into your super account

via Suncorp WealthSmart online

6 SuncorpContributions

Get off to a super start The Government’s co-contribution amount decreases for

those on higher incomes, but you can still benefit from the

Your super is your key to a life of financial independence. co-contribution scheme if you earn less than $61,920 pa

But it’s easy to forget about your super – you probably don’t (in the 2011-12 financial year).

see the money going in, and for most people there’s no way

of getting it out. Until you retire that is. Spouse contributions

The fact is that your super is likely to be the second largest Having your spouse contribute to your super is a great

asset you build in your lifetime, after the family home. The way to work towards your retirement goals. By making a

Suncorp Employee Superannuation Plan can help you reach contribution on your behalf, your spouse may be entitled

your financial goals and achieve the retirement lifestyle you to a tax offset of up to $540 which can be claimed through

want. By taking advantage of the tax-effective nature of the their personal tax return. The offset is equal to 18% of a

superannuation environment and investing regularly in your maximum contribution of $3,000 pa (in this case, $540).

Suncorp Employee Superannuation Plan account now, you

can make saving for your retirement easier. Contribution splitting

You can direct up to 85% of any concessional

How much is your employer contributing contributions made in the previous financial year, from

for you? your account to your spouse’s account. Your spouse must

Did you know that unless you are an exempt employee, be under age 65, but if they are between preservation age

your employer must make superannuation guarantee (SG) (currently age 55) and age 60, they must not be retired.

contributions to your account on a quarterly basis?

Self-employed?

As a Suncorp Group employee, the SG amount paid to

As a self-employed person, you can’t rely on SG

your account is equal to 9% of your salary (unless you

contributions to help you save for your retirement. The

have a specific agreement in place where Suncorp pays

good news is if you’re self-employed or substantially self-

more). To find out how much is being contributed to your

employed, you may be able to claim a tax deduction for

super account on your behalf, check your payslip on

personal contributions if you’re under age 75. All the more

‘Our People Space’ (on the Suncorp Intranet), or call HR

reason to contribute extra to your super!

Central on 1800 188 833.

You can claim a tax deduction on all contributions you

Super strategies to boost your savings make. To be eligible for this deduction, less than 10% of

your assessable income, plus reportable fringe benefits

for your retirement and reportable employer super contributions can come

The 9% of your salary contributed to your super account by from an employer.

Suncorp is a great start, but the truth is it probably won’t If you’ve made personal contributions into your account

be enough to provide you with the lifestyle you want in and haven’t subsequently withdrawn them, we’ll send you

retirement. To help you boost your savings for retirement, a notice at the end of the financial year. This is known as

the Government has put in place a number of initiatives to a s290-170 notice of intent to claim a tax deduction. If you

encourage you to save more for your retirement. wish to claim a tax deduction, simply complete the notice

The following snapshots give you a flavour of these super and send it back to us. We’ll take care of the rest and

boosting strategies. For more information on how these will let you know what information you’ll need to claim a

strategies can work for you, speak to your adviser, or call tax deduction.

us on 1800 652 489.

Who can contribute?

Salary sacrifice

Personal circumstances, such as your age and

Putting a portion of your pre-tax salary into your super is employment status, determine who can open an account

one of the most powerful and tax-efficient ways to boost and contribute to super.

your Suncorp Employee Superannuation Plan account.

Rather than paying income tax which can be up to 46.5%, You can open a Suncorp Employee Superannuation Plan

you’ll generally only pay 15% tax on these contributions. account if you’re:

And because these contributions aren’t considered salary • receiving SG or certain Award employer contributions

for tax purposes, salary sacrificing can potentially reduce at any age

your overall taxable income. You can make contributions into your Suncorp Employee

Superannuation Plan account if you’re:

Government co-contributions

If you are eligible to receive the co-contribution, earn less • under age 65 or

than $31,920 pa (in the 2011-12 financial year) and you • age 65 to 74 and have worked at least 40 hours

make a $1,000 after tax contribution, the Government will in a consecutive 30-day period within the current

contribute the maximum $1,000 to your retirement savings. financial year

Suncorp Employee Superannuation Plan Member Booklet 7Contributions continued

What types of contributions are accepted?

Contributions made to your super account fit into one of two categories, known as:

• Concessional contributions or

• Non-concessional contributions

Both of these contribution categories are subject to caps on the amount you may contribute in a financial year (from 1 July

to 30 June). The table below shows what category each type of contribution made into your super account falls into and the

contributions caps for the 2011-2012 financial year:

Concessional contributions Non-concessional contributions

Types accepted • Compulsory employer (SG and • Spouse

Award) • Personal (after tax)

• Personal (deductible)

• Salary sacrifice

• Voluntary employer

Contribution caps for the $25,000 $150,000

2011-2012 financial year

$50,000 if you’re age 50 or older If you’re under age 65, you can contribute up to three

(until 30 June 2012 only)1 times the cap in a single year by combining some future

years’ caps

What happens if your Depending on the circumstances, you may pay additional tax or the contributions will be rejected

contributions exceed

the caps?

1 The Federal Government has announced that the higher concessional contribution limit will remain for individuals aged 50 or older if their super balance

is less than $500,000 (from 1 July 2012).

Contribution methods

It’s easy to contribute to your super account, with a range of flexible methods.

Direct debit Contribution type Biller code

You, your spouse and your employer can conveniently

Personal contribution 787275

contribute to your Suncorp Employee Superannuation Plan

account on a regular basis by setting up a direct debit Spouse contribution 787283

facility.

Employer salary sacrifice 787317

Deductions from the nominated bank account are made on

or around the 1st of the relevant month. You can change or Employer SG and Award 787309

cancel this arrangement at any time and we must receive

your request on or before the 25th of the month for it to be Employer voluntary 787291

effective for the next scheduled direct debit.

Cheque

BPAY® Please make cheques payable to ‘Suncorp Portfolio

BPAY® allows you to contribute from your savings or Services Limited – ’ and send it with

credit card account by phone or internet. You’ll need an Additional Investment form to us at:

your Suncorp Employee Superannuation Plan Customer Suncorp Employee Superannuation Plan

Reference Number (CRN) and the BPAY® code for the type

GPO Box 2585 (IPC: LS004)

of contribution you wish to make. Your CRN is included in

the welcome letter you’ll receive after joining the Suncorp Brisbane QLD 4001

Employee Superannuation Plan or you can find it anytime

by logging into your account online. Visit a Suncorp branch

If your employer or spouse is contributing to your account Pop into a Suncorp branch, where we accept

by BPAY®, you’ll need to provide them with the relevant cheques, cash deposits or transfers from your other

biller code and your CRN. Suncorp accounts. Simply fill out a Suncorp Employee

Superannuation Plan deposit slip which is available from

our website.

8 SuncorpManaging your account

It’s easy to manage your Suncorp Employee Superannuation Plan account via the

following transaction options

The table below answers some questions you may have and helps you identify the choice of options available for each

transaction. All forms are available from our website.

How do you? What form do you Transaction options

need to use?

Apply for insurance cover Insurance application form 3 3 – – –

Change your investment Investment change form

options 3 – – 3 3

Add or amend the auto- Investment change form

rebalancing service 3 – – 3 3

Set up a new regular Direct debit request form

contribution plan 3 3 – – –

Change your regular Change of details form

contribution plan amount or 3 – – 3 –

payment frequency

Change your address Change of details form 3 – 3 3 3

Change your name Change of details form 3 3 – – –

Change your bank account Direct debit request form

details 3 3 – – –

Transfer funds from another Super Rollover form

super provider 3 3 – – 3

Make a withdrawal Withdrawal form 3 – – 3 –

Nominate or change your Non-lapsing death benefit

death beneficiary nomination form 3 3 – – –

Provide your TFN Change of details form 3 – 3 3 3

Appoint an authorised Authorised representative

representative form 3 – – 3 –

Cancel a request No form – Simply write to us

with your request 3 – – 3 –

by mail Suncorp Employee Superannuation Plan

GPO Box 2585 (IPC: LS004)

Brisbane QLD 4001

by phone 1800 652 489

by fax 07 3002 3259

online Log on to Suncorp WealthSmart online at suncorp.com.au

Original

signature

required We must receive an original ink signature

Suncorp Employee Superannuation Plan Member Booklet 9Managing your account continued

Our service standards Auto-rebalancing

We’re committed to delivering consistent, superior Keeping track of movements in your investment options

service. Our service standards apply from when we can be a time consuming task. By selecting the auto-

receive your complete instructions. If we receive a rebalancing feature, you can ensure that your investments

complete investment transaction request from you by are automatically adjusted in line with your future

12pm (Sydney time) on a business day, you’ll receive the investment strategy at quarterly, half-yearly or yearly

unit price effective for the investment option for that day. intervals.

If we receive a completed investment transaction request For more information on how this feature works, please see

after 12pm on a business day, we’ll process the request ‘Auto-rebalancing’ in the ‘Investments’ section on page 15

using the investment option unit prices for the following of this Member Booklet.

business day.

The 12pm cut-off applies to all contributions, switches Nominating your beneficiaries

and withdrawal requests. Have certainty over who will receive your death benefits by

Generally, we aim to process requests within four nominating a dependant.

business days.

Who is a dependant?

We strive to consistently meet our service standards,

however the unit price used to process your transactions You can only nominate your estate or your dependants to

may differ from the effective unit price for that day or receive your death benefits. A dependant under super law

processing your transactions may be delayed in some includes:

circumstances including: • spouse (legal and de facto)

• incomplete or incorrect information from you • child (any age)

• a delay in confirmation or payment from an external • person in an interdependency relationship with you and

investment manager

• financial dependant

• carrying out the transaction may materially impact

other members Non-lapsing nomination

• us receiving a direction from a lawful authority to A non-lapsing death benefit nomination allows you to

suspend or amend the transaction nominate your dependants and/or your estate to receive

• the investment manager suspending redemptions part or all of your death benefit (including any insurance

from your underlying investment benefit). We must pay the benefit to your beneficiaries when

you die (provided your nomination is valid at the time).

• the proximity to the end of the financial year and

For your nomination to be valid:

• any other delays in redeeming assets

• each beneficiary must be a dependant and/or your legal

We may from time to time review our service standards.

representative at the time of your death

Please also refer to ‘Unit pricing delays’ on page 15 of

• if there is more than one beneficiary, the apportionment

this Member Booklet.

of your benefit must be clear and add up to 100% and

Terms and conditions for accepting faxes • two adult witnesses who aren’t beneficiaries must

witness and sign the nomination

We’ll accept faxed instructions on our relevant forms.

While your nomination is non-lapsing, it’s still a good

Before using this option, there are a few things you need

idea to keep it up to date. We recommend you review

to know, like:

your nomination whenever you experience a change in

• we’re not responsible to you for any loss resulting circumstances such as marriage, divorce, birth of a child or

from any fraudulently completed request when a beneficiary ceases to be a dependant.

• we’re not responsible to you for any loss suffered

by you because we process a fax that has been Child pension nomination

corrupted during transmission The child pension is an extension of the non-lapsing death

• we won’t compensate you for any losses arising from benefit nomination. You can nominate your child under age

the use of this facility and 18 to receive an income stream paid from your benefits

when you die. You can restrict your child from accessing

• we’ll be released and indemnified by you against

their account until a pre-determined age. However the

any liabilities as a result of acting on any faxed

pension must be paid out as a lump sum when the child

communication received in relation to your account

reaches age 25, unless they’re disabled.

10 SuncorpAccessing your benefits

When can you withdraw from your Suncorp Employee Superannuation Plan account?

Super is a long-term investment designed to help you save for your retirement and government legislation defines when you

can access your super benefits. While you can only access your super benefits before your preservation age under certain

circumstances, you can transfer to another complying super fund at any time.

What can you access?

Preserved benefits These benefits can only be accessed once you have satisfied a condition of

release.

Restricted non-preserved benefits These benefits can be accessed under the same conditions of release as your

preserved benefits, but can also be paid to you when you leave the employer who

made the contributions for you. Generally, restricted non-preserved benefits arise

from personal contributions made to an employer fund from 1 July 1983 up to 30

June 1999, and for which you couldn’t claim a tax deduction.

Unrestricted non-preserved benefits These benefits are fully accessible at any time.

When have you met a condition of release?

You’ll be able to access your preserved benefits if you satisfy one of the following conditions of release in the below table:

Condition of release What you can access

Permanent retirement from the workforce All

(after reaching your preservation age)

Leaving your employer after turning age 60 All

Reaching age 65 All

Permanent incapacity All

Severe financial hardship You may be limited to one lump sum payment between $1,000 and $10,000 within a

12-month period depending on your circumstances.

Compassionate grounds You’ll need to make an application to the Australian Prudential Regulatory Authority (APRA)

to have your benefits released. The amount you receive is determined by APRA.

Temporary residents departing Australia All

Termination of your employment with the You can access all your restricted non-preserved benefits. You can access your

employer who contributed for you preserved benefits as a non-commutable life pension, or as a lump sum if the amount is

less than $200.

Lost member who is found and have less than All

$200 in your account

Reaching preservation age and using your You’ll need to commence a non-commutable income stream that is limited to a maximum

benefits to start a non-commutable pension pension payment of 10% of the account balance.

(transition to retirement)

Terminal illness All

Temporary incapacity You can access an amount as long as it doesn’t exceed your income level before

becoming temporarily incapacitated. You can only receive the payments as a non-

commutable income stream.

Death All

Your preservation age Date of birth Preservation age

Your preservation age is based on when you were born

Before 1 July 1960 55

and determines when you can access some of your

benefits. Once you have reached age 60 and retired, 1 July 1960 – 30 June 1961 56

your money can be taken out of your super tax free as a

pension or a lump sum. 1 July 1961 – 30 June 1962 57

1 July 1962 – 30 June 1963 58

1 July 1963 – 30 June 1964 59

After 30 June 1964 60

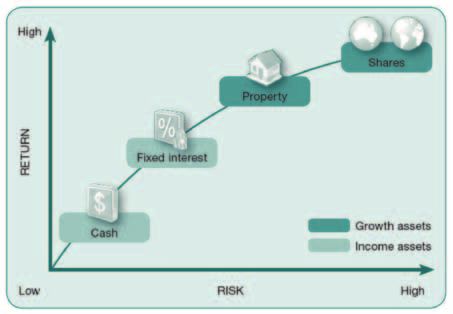

Suncorp Employee Superannuation Plan Member Booklet 11Investments Make the right investment choice. A few small decisions now could make a big difference to where you’ll end up. Our investment menu The Suncorp Employee Superannuation Plan investment menu makes it simpler for you to choose an investment option that’s right for you. As a member of the Suncorp Employee Superannuation Plan, you have a choice of 38 investment options, including six diversified investment options that are designed to suit a broad range of investors. • Suncorp Traditional Capital Guaranteed Fund • Suncorp Balanced Portfolio • Suncorp Secure Portfolio • Suncorp Growth Portfolio • Suncorp Conservative Portfolio • Suncorp High Growth Portfolio Default investment strategy If you don’t make a choice, your super will be invested in the plan’s default investment option, the Suncorp Traditional Capital Guaranteed Fund. This could be a perfectly reasonable investment option for you. But no single investment option suits everyone. And the risk you take is that the default investment option won’t deliver what you want, or need, from your investments. Matching your investments to your risk profile, and to your long-term lifestyle goals, is a good start to achieving your retirement goals. With so much choice there’s sure to be an investment option, or a combination of investment options, to suit you. It’s just a matter of finding out what they are and discussing with your adviser the investment strategy that’s right for you. Check out the Suncorp Employee Superannuation Plan investment menu starting on page 19 for details on each investment option. Investment risks As with all investment products, there are risks associated with investing in the Suncorp Employee Superannuation Plan. And because we all have different attitudes towards risk, it’s a good idea to talk to your adviser about the risks relevant to your own financial situation and objectives. The relationship between risk and return As a general rule, investments with a higher level of risk will provide a higher potential return. In other words, you can’t have one without the other. By the same token, the smaller the risk an investment poses, the smaller the potential return it will provide. This is shown below: 12 Suncorp

Balancing this relationship can be tricky. That’s why it’s important to speak to your adviser before making any investment

decisions. Your adviser can recommend an investment option or a combination of investment options that suits your own

risk tolerance level.

What are the risks?

Like any investment, super is subject to risks. The biggest risk is that you won’t have enough money to meet your retirement

needs. This can happen where an investment decreases in value but also where monies are invested conservatively in

investment options which provide more stable but lower long-term returns. For most people super is a long-term investment

– be sure you speak with your adviser to see what’s right for you.

Some of the risks that may affect your investments in the Suncorp Employee Superannuation Plan are set out below. We

regularly monitor these risks for their impact on the investment menu as a whole, but it’s a good idea for you and your

adviser to consider what they might mean for you.

Risk type What is it?

Market risk This can arise due to changes in government or economic policy, interest rates and exchange

rates, market sentiment, global events, technological change, environmental conditions or

changes in legislation.

Investment options risk Investment professionals or teams and the strategies they adopt may change, which may not

be in line with your expectations when you first invested. It’s also possible an investment option

may be terminated.

Liquidity risk This arises where an investment can’t be easily converted into cash or disposed of at market

value, at a time when it’s needed.

Credit risk This is where someone doesn’t meet their obligations to, or relating to, the investment option.

For example, it includes the risk that we or an underlying investment manager are unable to

make payments.

Inflation risk If inflation exceeds an investment’s return, it’ll reduce the purchasing power of the assets.

Inflation risk is more common in low risk investments, which generally fluctuate less, but

potentially provide lower long-term returns.

Currency risk International investments can be affected by changes in the value of the Australian dollar

relative to other currencies that the investment option is invested in. Their value can rise and

fall, depending on the value of the Australian dollar. Generally, a fall in the value of the Australian

dollar will lead to an increase in the value of an unhedged international investment and vice

versa. Hedging can be used by investment managers to either minimise losses or maximise

returns on these currency fluctuations. They can do this by investing in financial instruments

such as futures, swaps and other derivatives.

Derivatives risk Derivatives are securities that derive their value from another security. Commonly known

derivatives include futures and options. Derivatives can be used to manage risks in a portfolio

or to leverage a portfolio in the hope of generating greater returns. The risks of using derivatives

include that they may be costly or difficult to reverse and their value may not move in line with

that of the underlying security.

Gearing risk Gearing involves borrowing money to invest in an asset. Geared investment options are

internally geared, meaning the investment option borrows the money, rather than you. The cost

of borrowing, including interest rates, and the level of gearing influence returns on a geared

investment. Geared investment options experience larger fluctuations in their investment returns

when compared to non-geared investment options, and they have the corresponding potential

to suffer greater losses if there is a market downturn.

Changes in law Changes in super and tax legislation may occur. This may affect when you can access your

benefits and how they’ll be treated upon withdrawal. We’ll inform you of any changes we think

are likely to affect your investment. Generally, we do this through the annual report.

Suncorp Employee Superannuation Plan Member Booklet 13Investments continued

How can you reduce risk?

The most common way to reduce your risk is by diversification, or ‘not putting all your eggs in the one basket’.

The Suncorp Employee Superannuation Plan can help you diversify your investments:

• A

cross asset classes

You can invest in a range of asset classes, including domestic and international shares, domestic and international fixed

interest, domestic and international property, cash and alternative assets

• W

ithin an asset class

You can invest in different markets, different sectors or different investment styles, within the one asset class

• A

cross investment managers

With a choice of quality investment managers to select from, you can invest with different investment managers of

differing investment styles

Understanding the asset classes

Each investment option is invested into what are called ‘underlying assets’. These underlying assets have different

characteristics and may be either income assets or growth assets or a combination of both.

• Income assets include such things as cash and fixed interest, which provide income returns in the form of interest

• G

rowth assets include property, shares and alternative assets, which provide for investment returns comprising both

capital growth (increase in value of the investment) and income

Asset Risk Potential What is it?

class level return

Low Low Cash is the most secure of all the asset classes. Returns are stable with a low potential for capital

loss.

Cash

Medium Medium Fixed interest is a relatively conservative asset class. It generally refers to investments such as bonds,

debentures and other hybrid securities. Fixed interest investments generally aim to provide returns

higher than that of cash but with a low degree of fluctuations of returns.

Fixed

interest

High High Property is a growth asset with greater risk of fluctuation in returns than cash or fixed interest.

Historically, property has had lower variability of returns than shares.

Property

High High Shares represent a part ownership in a company. Shares are considered to be riskier than cash or

property, as their value tends to fluctuate the most. However, historically over the long term, returns

from shares have outperformed those of other asset classes and are traded both on domestic and

international sharemarkets. Returns from the ownership of shares combine both the income received

(dividends) and growth (capital gains) through the increase in the share price. The value of international

shares may also be affected by fluctuations in the exchange rate.

Shares

Very Very Alternative assets are investments that are not classified or may not be correlated to the traditional

high high asset classes of cash, fixed interest, property or shares. Typically they may involve investments in asset

classes (eg gold, infrastructure or private equity) or investment strategies (eg financial instruments such

Alternative as exchange traded or Over The Counter (OTC) derivatives, or trading techniques) that aren’t liquid and

assets require specialised skills to manage.

Can you change your investment options?

Because your financial needs may change, you have the flexibility to switch between investment options at any time. And

the good news is we won’t charge you a switching fee. However, you may incur a buy/sell spread, which is charged by the

investment manager, depending on the options you select.

For more information, please see ‘Buy/sell spreads’ in the ‘Fees and costs’ section on page 60 of this Member Booklet.

14 SuncorpAuto-rebalancing How are unit prices calculated?

Keeping track of movements in your investment options Unit prices are generally calculated daily and reflect the

can be a time consuming task. Over time, variances in value of the underlying assets of the investment option

investment performance may result in your investment after taking into account income entitlements, investment

options moving away from the percentages nominated in fees, taxes and other expenses and liabilities that are

your original investment selection. considered appropriate. This underlying asset value is

divided by the number of units on issue to arrive at the

By using the auto-rebalancing service, you can choose

price per unit. Buy or sell spreads are then applied to this

to have your investment options rebalanced in line with

price per unit to calculate the entry and the exit prices,

your future investment strategy on a regular basis without

respectively. Like the values of the underlying investments,

having to constantly monitor your account. You can

the price of units can therefore move up and down.

choose to have your account rebalanced each:

The daily unit price for each Suncorp Employee

• quarter (March, June, September, December)

Superannuation Plan investment option (except for the

• half-year (June and December) or Suncorp Bank Deposit Fund and the Suncorp Traditional

• year (June) Capital Guaranteed Fund) is quoted on our website. The

Suncorp Bank Deposit Fund has a fixed unit price of $1

Rebalancing takes effect on or around the 22nd of the month. and the Suncorp Traditional Capital Guaranteed Fund

For example, you invest 50% in Option A and 50% is not unit priced. You can find information about the

in Option B and you want to maintain this investment calculation of performance for these investment options

strategy. Over time, your actual investment allocation on pages 16 and 17 of this Member Booklet.

may change to 40% in Option A and 60% in Option B

as a result of movements in the unit price. Your account Unit pricing delays

will then be automatically rebalanced to your investment We may suspend unit pricing where in our opinion:

strategy (50% in Option A and 50% in Option B) at the

frequency you select. • a significant event or incident occurs that has the

potential to affect investment markets or

Unit prices • an event occurs that has the potential to affect unit

prices or

For all investment options except the Suncorp Traditional

Capital Guaranteed Fund, your account balance is derived • an external investment manager closes the underlying

from the value of a number of underlying units, each of investment to applications and withdrawals or

which represents a part holding in an investment option • the unit prices calculated have the potential to prejudice

and over time moves up or down. specific investors.

Buying units

Investment performance

When you invest in an investment option, units in your

Investment performance lets you see how your investment

chosen investment option are allocated to you. The

is going.

number of units allocated will depend on the entry price of

the units at the time you invest, and the amount of money

you invest.

How is investment performance calculated?

Investment performance is generally calculated net of

Selling units taxes and ongoing fees such as the administration fee,

member fee, performance fee and investment fee. This is in

We may sell units from your investment options to pay for

accordance with industry standards.

taxes, insurance premiums (if applicable) and certain fees

or charges. We also sell units when you request a cash However, when calculating investment performance, we

withdrawal or transfer to another super fund. When we generally don’t take into account contributions tax, entry

sell units in an investment option, the number of units sold fees, exit fees and any discretionary ongoing fees such

depends on the exit price of the units at that time. as insurance premiums and adviser service fees. If we

calculate the investment performance for an investment

Switching between investment options option in a way different from that set out above, we’ll

include an explanation of how investment performance

If you request a switch, we’ll sell units from one investment

is calculated for that investment option in the monthly

option and use the proceeds to buy units in the other

investment performance report which is available from our

investment option. You’ll receive the exit price for any

website.

units that are sold and the entry price for units that are

bought. A buy/sell spread may also be applied to cover

transaction costs.

Suncorp Employee Superannuation Plan Member Booklet 15Investments continued

Please note past performance shouldn’t be taken as an Please note that we don’t take labour standards,

indication of future performance. environmental, social and ethical considerations into

You should be aware that the investment performance account when selecting, retaining or terminating

information for the investment options may differ from the investment options.

performance of the underlying investment managers. This

may be due to: Multi-manager investment options

• holding some assets in cash or short-term securities, A multi-manager approach to investing uses the skills

for liquidity purposes or of more than one investment manager. It’s based on the

view that no single investment manager consistently

• provisions for tax and distribution of tax credits or

outperforms the market in all conditions. Over any given

• the fees and charges that apply or timeframe, it’s difficult to predict which investment

• a lag between when the underlying investment managers or which investment style will outperform the

managers report their performance and when the value market and its peers. Some investment styles will perform

of the underlying investment option is reflected in the well in one stage of the market cycle, while others may

unit prices perform poorly in the same conditions.

The Suncorp Bank Deposit Fund has a fixed unit price The Suncorp Employee Superannuation Plan’s multi-

of $1 and the Suncorp Traditional Capital Guaranteed manager investment options blend a combination

Fund isn’t unit priced. You can find information about the of quality investment management styles to create

calculation of performance for these investment options on investment options aimed at reducing investment risk and

pages 16 and 17 of this Member Booklet. the volatility of returns.

The Suncorp Employee Superannuation Plan offers you

Who manages the Suncorp Employee access to a range of multi-manager investment options via

the Suncorp diversified portfolios.

Superannuation Plan’s investment

options? For more information on these options, please refer to our

investment option profiles.

• Ibbotson Associates (Ibbotson)

• SIM Funds Management Suncorp Traditional Capital Guaranteed

• Tyndall Investment Management Limited and other Fund

external investment managers

Suncorp Life & Superannuation Limited (SLSL) declares

For more information, please see ‘Information about the interest rates in arrears for this investment option at 30

investment managers’ on pages 39 to 44 of this Member June each year. Interest is calculated on the daily account

Booklet. balance and credited to your account on 30 June each year.

An investment in the Suncorp Traditional Capital

About the investment options Guaranteed Fund provides a participating benefit. This

For some investment options, a PDS is issued by the means that the profits arising in respect of this option

underlying investment manager, free of charge. You are allocated 80% to members and 20% to SLSL as

can download copies from our website or ask us for a shareholder.

printed version. SLSL guarantees that the interest credited to your account

Before you select or change your investment selection to at 30 June each year won’t be negative. We use an interim

a new investment option, you should consider the relevant interest rate to calculate interest on full withdrawals made

investment manager’s PDS. before the interest rate is declared (including full switches

to another investment option). The interim rate can be

In general, if there’s a conflict between the terms and

changed by SLSL at any time and will apply from the

conditions shown in an investment manager’s PDS, the

previous 1 July. The final declared rate on 30 June may be

PDS and this Member Booklet, you should refer to the

less than the interim rate that has applied during the past

PDS and this Member Booklet to understand the terms

year.

and conditions applying to your investment.

The declared interest rates are determined based on

If you’d like to find out what the differences are in

several factors, including:

investing into an investment option through the Suncorp

Employee Superannuation Plan as opposed to investing • the investment income received after an allowance for

directly with the underlying investment manager, tax, including both realised and unrealised capital gains

please see ‘Investing through the Suncorp Employee and losses

Superannuation Plan and investing directly’ on page 18 of • transfers to and from reserves in order to smooth

this Member Booklet. returns over time and provide for guarantees

16 Suncorp• administration and investment fees and What happens if an investment option is closed,

• expenses such as brokerage, stamp duty, taxes, and suspended or terminated?

other expenses incurred in managing the assets From time to time, investment options may be closed,

suspended or terminated by an external investment

Suncorp bank deposit options manager or by us. This may happen where:

If you’re looking for secure, simple and easy to • the investment option is no longer offered by the

understand investment options, the Suncorp Employee investment manager or

Superannuation Plan offers the Suncorp Bank Deposit

• the total amount of investor’s money in the investment

Fund and the Suncorp Term Deposit Fund.

option has grown too large for the investment manager

Both investment options offer competitive interest rates. to continue with its current investment strategy or

The Suncorp Bank Deposit Fund pays monthly interest in

• laws change so that some investment types become no

the form of additional units into your Suncorp Employee

longer permissible or

Superannuation Plan account. The Suncorp Term Deposit

Fund is unit priced and investment performance is shown • we determine that it’s in the best interests of the

in the movement of the daily unit price. members or

So if you’re looking for the benefits of a bank account • the investment option may no longer be economically

within your Suncorp Employee Superannuation Plan viable

account, please refer to our investment option profiles for If an investment option is closed, suspended or terminated,

more information. this may cause delays in processing withdrawals and

transfer requests. This delay may be more than 30 days

Suncorp Bank Deposit Fund and the unit price used to process your transaction may

SLSL declares interest rates in arrears for this investment differ from the price applicable on the day you lodged

option on the 15th of each month for the preceding month. your request.

Interest is then calculated on your daily account balance Where an investment option is closed, suspended or

and credited to your account on the 15th of each month terminated, we’ll write to you in advance (where possible)

effective the last day of the previous month. to notify you of this change. You’ll then be able to review

your strategy, with the help of your adviser.

We use an interim interest rate to calculate interest on

full withdrawals made before the interest rate is declared Where we’re unable to tell you in advance, we’ll determine

(including full switches to another investment option). a replacement investment option (one that is comparable

to your investment option) in which to invest your money

The interim rate will be similar to the previous month’s

until you’ve been able to review your investment strategy.

declared rate and can be changed by SLSL at any time.

The declared interest rates are determined based on

several factors, including:

• the interest received from the underlying bank deposit

investments

• expenses such as taxes, and other expenses incurred

in managing the assets and

• interim interest paid to exiting members

Changes to investment options

The Suncorp Employee Superannuation Plan’s investment

menu may change from time to time, including the fees

and charges relating to the investment options. It’s

important to check our website regularly for any changes

to your investment options.

Suncorp Employee Superannuation Plan Member Booklet 17You can also read