STATE OF TRANSPORTATION ENERGY AND VEHICLE ELECTRIFICATION - WHITE PAPER AUGUST 2 020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

WHITE PAPER STATE OF TRANSPORTATION ENERGY AND VEHICLE ELECTRIFICATION A U G U S T 2 02 0

©2020 Fuels Institute Disclaimer: The opinions and views expressed herein do not necessarily state or reflect those of the individuals on the Fuels Institute Board of Directors and the Fuels Institute Board of Advisors, or any contributing organization to the Fuels Institute. The Fuels Institute makes no warranty, express or implied, nor does it assume any legal liability or responsibility for the use of the report or any product or process described in these materials.

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N Contents INTRODUCTION ............................................................................................................................................................... 02 THE FLEET IS BECOMING MORE EFFICIENT .................................................................................... 03 I C E S W I L L S U RV I V E F O R D E C A D E S .......................................................................................................... 10 T H E S TAT E O F V E H I C L E E L E C T R I F I C AT I O N ....................................................................................... 14 CONCLUSION .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 A B O U T T H I S W H I T E PA P E R This report was written by the Fuels Institute, combining public and proprietary data as well as industry insights gained from members and other industry relationships. ©2020 Fuels Institute

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

Introduction

The transportation market is Rather, a more measured pace of transition is

likely to occur with a broad mix of powertrains

transitioning to lower-carbon-intense

moving people from one place to another. This is

sources of energy and more efficient not to say that disruption cannot occur — it most

use of existing energy resources, but certainly can, and there are a number of market

the transition is proceeding at an areas in which a more rapid restructuring of market

fundamentals could take place — but as of now,

evolutionary pace. While many are

there does not appear to be the impetus for such

advocating a rapid transition to an dramatic change and consumers do not seem

electrified transportation market, the poised to force a revolution. An objective look

realities of market fundamentals and at the numbers as they stood at the end of 2019

provides a solid foundation upon which to evaluate

the nature of consumer choice stand in

the future of the market’s evolution.

the way of radical reform.

2

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

The Fleet Is Becoming

More Efficient

It is no illusion that the vehicle fleet is performance of every class of vehicle has improved.

becoming more efficient and that the According to the U.S. Environmental Protection

Agency (EPA), carbon dioxide (CO2) emissions and

impact on overall liquid-fuel demand

MPG for pickups, minivans, sport utility vehicles,

will be pronounced. crossover utility vehicles, and sedans improved

According to the U.S. Bureau of Transportation significantly between 2004 and 2018.

Statistics, the average fuel economy of new light What is impressive about these achievements is the

duty vehicles improved by more than 35% between technologies used by the automotive manufacturing

2000 and 2017.1 As a result, the environmental industry to achieve them. Through 2018 the use of

1 “Average Fuel Efficiency of U.S. Light Duty Vehicles,” U.S. Department of Transportation, accessed June 3, 2020, https://www.bts.dot.gov/content/average-fuel-

efficiency-us-light-duty-vehicles.

26.6 29.2 32.8 35.8 39.4 41.4 39.9 41.2 41.3

Low Medium High Variation

F I G U R E 1 : AV E R A G E F U E L E C O N O M Y O F N E W V E H I C L E S

Passenger Cars Light Trucks

40

39

35

30

MPG

29

25

20

1980 1990 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2015 2017

Source: U.S. Bureau of Transportation Statistics

3

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

FIGURE 1. CHANGE IN CO2 EMISSIONS AND MILES PER GALLON (2004–2018)

CO2 MPG

PICKUP

M I N I VA N / VA N

TRUCK SUV

CAR SUV

S E D A N / WA G O N

-40% -35% -30% -25% -20% -15% -10% -5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

Source: U.S. Environmental Protection Agency

electrified powertrains was very limited. Engineers • Stop start, which shuts off the engine when idling

leveraged a variety of other strategies to achieve to save fuel and then automatically restarts, first

improved efficiency, reduced emissions, and appeared in 2012 and in 2018 was found in 28%

enhanced performance (a vehicle characteristic of the market

many consumers were most aggressively seeking).

10%Equally impressive is how engineers leveraged

According to the EPA, some of the emerging

transmission technology. Anyone who has

technologies brought to market to deliver these

Percentage of ever

Creditsridden

Generateda bicycle knows that the more gear

improvements have been adopted at rapid rates:2

selections you have at your disposal, the easier

• Multi-valve cylinders

2 0 11

debuted

2012

in 1986

2 0 13

and in2 0 14 it2 0is1 5to climb hills, go 2faster,

2016 017

and2 0travel

19

further

2 0 11 - 2 0 1 8

2018 represented 92% of new engines without exhaustion. By increasing the number of

Fossil Natural Gas Biomethane Electricity gearsBiodieselavailable in a vehicle,

Renewable automotive

Diesel engineers

Ethanol

• Turbo boosting was a relatively niche product

are able to get the most performance from their

until the mid-1990s and are now available in 31%

engines. By 2018, vehicles equipped with seven

of new vehicles Lorem ipsum or more gears, including continuously variable

• Variable valve timing debuted in 2000 and within transmissions, accounted for 58% of new vehicles.

18 years was installed in 96% of new vehicles The number of vehicles equipped with four- or

five-speed transmissions, which were once the

• Gasoline direct injection was first introduced

dominant transmissions in the market, became

in 2008 and by 2018 was found in 51% of

virtually non-existent by 2015.

new vehicles

2 U.S. Environmental Protection Agency, 2018 Automotive Trends Report, March 2019, https://www.epa.gov/automotive-trends/download-2018-automotive-trends-report-

previous-year.

4

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

F I G U R E 3 . M A N U FA C T U R E R S ’ U S E O F E M E R G I N G T E C H N O L O G I E S ( M O D E L Y E A R 2 018 )

TURBO 31%

GASOLINE DIRECT INJECTION 51%

C O N T I N U O U S VA R I A B L E

TRANSMISSION 22%

7+ GEARS 36%

26.6I O N 29.2 32.8 35.8 39.4 41.4 39.9 41.2 41.3

C Y L I N D E R D E A C T I VAT 12%

S T O P S TA R T

28% More than 25 years 11 to 15 years

HYBRID 4% 21 to 25 years 6 to 10 years

P H E V / E V / FFE

C VDE R AL TAX CR E DIT 16 to 20 years 0 to 5 years

3%

0 10 20 30 40 50 60

$57,067 $54,200 $60,390

Source: U.S. EPA, “The 2018 EPA Automotive Trend Report”

FIGURE 4. SHARE OF TRANSMISSIONS BY NUMBER OF GEARS

4 or less 5 Gears 6 Gears 7 Gears 8 Gears 9+ Gears CVT

100%

80%

60%

40%

Percentage of Credits Generated

20%

0% 2 0 11 2012 2 0 13 2 0 14 2015 2016 2017 2019 2 0 11 - 2 0 1 8

1974 1980 1985 1990 1995 2000 2005 2010 2015

Source: U.S. Environmental Protection Agency

Fossil Natural Gas Electricity Biodiesel Renewable Diesel Ethanol

Biomethane

Lorem ipsum

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

The fact is that automotive

$52,500 engineers

$54,568 have boosted fuel economy and reduced emissions by improving upon

$69,262

technologies within the internal combustion engine (ICE). An executive for a major global automaker was quoted

in the July/August 2019 issue of Automotive Engineering saying, “The way things are being covered right now, you

would think we had just stopped everything, and everything is electric, and that certainly is not the way things

are going to develop …. In the end you want to provide what the customers want: fuel economy, performance,

quality, reliability …. We are doubling the number of resources that we have on [battery electric vehicles], but we

still have a tremendous amount of work to do on ICEs.”3

3 Paul Seredynski, “GM’S Ken Morris Lives the Pace of the Powertrain Revolution,” Automotive Engineering, July/August 2019, 26, https://www.nxtbook.com/nxtbooks/

sae/19AUTP08/index.php?lre=1%3A3532383635454233363938363332434244393037393833333637314646424144#/0

5

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

The EIA forecast for

light-duty vehicle (LDV)

fuel economy remains

relatively bullish

and results in a 47%

improvement in fleet fuel

economy by 2040.

Despite recent progress, there remains room today. Even so, their forecast for light-duty vehicle

to improve, and the federal Corporate Average (LDV) fuel economy remains relatively bullishand

Fuel Economy (CAFE) standards require such results in a 47% improvement in fleet fuel

improvements be achieved by 2025. In its Annual economy by 2040 with total passenger cars on the

Energy Outlook 2020,4 the U.S. Energy Information road delivering 42 MPG and light trucks delivering

Administration (EIA) forecast new vehicle and fleet 30 MPG. New vehicles are projected to deliver

fuel economy through 2050. In framing its forecast, greater fuel economy, but the impact on the fleet

the agency assumed the CAFE program that existed is determined by new vehicles sales and overall

at the end of 2019 would remain in place and that fleet turnover, which takes a significant period of

no further required efficiency improvements will time. The diesel freight fleet is likewise projected

be enacted. Some change in the CAFE program to become much more efficient, delivering

beyond 2025 is likely, but with no policy guidance approximately 30% more MPG across the market

to inform its model, EIA used what standards exist by 2040.

4 U.S. Energy Information Administration, Annual Energy Outlook 2020, January 29, 2020, https://www.eia.gov/outlooks/aeo/.

6

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

F I G U R E 5 : P R O J E C T E D L I G H T- D U T Y V E H I C L E F U E L E C O N O M Y

80

Passenger Cars Light Trucks Car Fleet Trucks Fleet

70

60

50

MPG

40 42

30 30

28

20 20

10

2019 2020 2021 2022 2023 2024 2025 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

26.6 29.2 32.8 35.8 39.4 41.4 39.9 41.2 41.3

Source: U.S. Energy Information Administration AEO2020

Low Medium

2019 High Variation

F I G U R E 6 : P R O J E C T E D AV E R A G E D I E S E L F U E L E C O N O M Y O F N E W A N D S T O C K V E H I C L E S

New Light Medium New Medium New Heavy Stock Light Medium Stock Medium Stock Heavy

20

17.9

15

14.3

MPG

12.2

10

8.9

7.6

6.1

5

2019 2020 2021 2022 2023 2024 2025 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Source: U.S. Energy Information Administration AEO2020

The market effect of these projected gains in efficiency could be significant. Although EIA projects overall

2019

vehicle miles traveled to increase between 7% and 20% (depending on the oil price scenario evaluated) and

the number of licensed drivers to increase 12%, the efficiency gains are still projected to reduce gasoline

consumption between 13% and 26% and diesel fuel consumption between 3% and 15%, with the ranges

reflecting the difference between the high oil price and low oil price scenarios.

7

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

F I G U R E 7 : P R O J E C T E D L D V M I L E S T R AV E L E D P E R Y E A R

4000

VMT VMT High and Low Range

3500

Billion Miles

3000

2500

2019 2020 2021 2022 2023 2024 2025 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Source: U.S. Energy Information Administration AEO2020

26.6 29.2 32.8 35.8 39.4 41.4 39.9 41.2 41.3

FIGURE 8: LIQUID FUEL DEMAND

Low Medium High Variation

Gasoline Diesel Ethanol Biodiesel Other Biomass

10

1980 1990 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 -13%

20 1 1 2to

0 1 5-26%

2017

8

Million Barrels per Day

6 17.9%

4 -3% to -15%

12.2%

2

0

2019 2020 2021 2022 2023 2024 2025 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Source: U.S. Energy Information Administration AEO2020

2019

8F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

Achievements in fuel efficiency are likely to into markets that are governed by some sort of

continue despite domestic policy decisions. In April efficiency/emissions program. Consequently, while

2020, the EPA finalized the SAFE Vehicles Rule that U.S. policy has a major influence on the market, the

reduces annual efficiency improvements from 5.0% demands of the global market are likely to compel

to 1.5% per year. The original proposal and the the industry to continue delivering more efficient

final rule raise questions about the impact it might vehicles, perhaps at a rate greater than mandated

have on overall vehicle efficiency improvements. by the U.S. In addition, automakers have made it

It is important to remember that the automobile a practice to market their vehicles’ fuel efficiency

manufacturing industry is producing vehicles relative to competing models, seeking to capitalize

for more than just the U.S., and soon more than on consumer’s interest in purchasing more fuel

90% of the vehicles sold globally will be sold efficient vehicles.

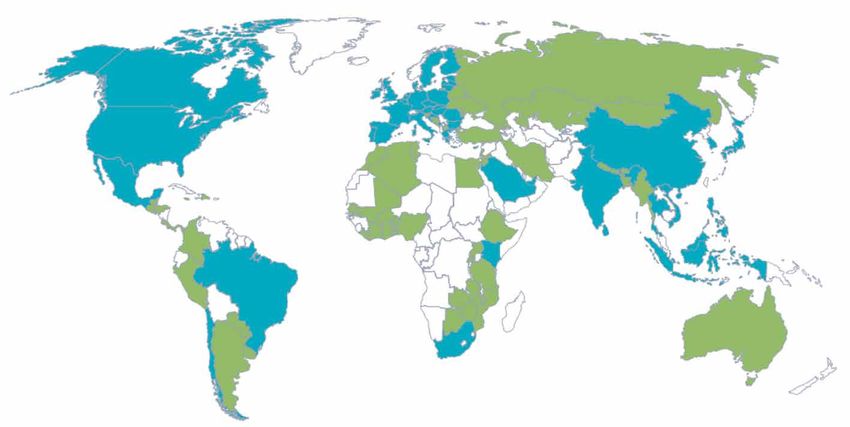

F I G U R E 9 : G L O B A L F U E L E C O N O M Y E F F I E N C Y S TA N D A R D S

Has Set Standards In the Planning Process to Set Standards

LDV=Passenger Cars, Light Trucks and Sport Utility Vehicles (SUVs)

IEA World Energy

Outlook 2018:

“By 2040, there

are no cars sold

that have an

efficiency worse

than 6.5 liters/100 km

(approximately 36 mpg).”

Source: Compiled by Future Fuel Strategies citing numerous sources including “Global Fuel Economy An update for COP23,” Global Fuel

Economy Initiative; September 2018

9F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

ICEs Will Survive

for Decades

The registered improvements in vehicle It is clear that electrified powertrains will be entering

efficiency to date have been achieved the market and will play a significant role in the

transportation sector, but even if the government

with improved ICEs. Engineers have

were to mandate a 100% transition, the impact

successfully delivered more miles from would not be immediate.

each drop of fuel through better engine

For example, assume every single vehicle sold

design and application of technologies, beginning January 1, 2018, included some new

and that is not slowing down. Such technology. Given projected sales and scrappage

continued improvement is critical rates at the time, it would take nine years before

50% of the vehicles on the road were equipped with

because ICEs will be a significant part

the new technology. This assumes that the new

of the market for the foreseeable technology did not increase the price of vehicles to

future. This is because the LDV market such a level that sales would suffer and that the new

is substantial, and any change will take technology did not dissuade consumers from buying

new vehicles at the expected pace.

time to have a tangible impact.

1026.6 29.2 32.8 35.8 39.4 41.4 39.9 41.2 41.3

Low Medium High Variation

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

F I G U R E 10 : N E W V E H I C L E S A S S H A R E O F F L E E T O N T H E R O A D

Data and Assumptions:

U.S. EIA LDV Fleet Size - 243.8 million in 2018

U.S. EIA LDV Sales Forcast - 16.1 million/year average

80%

39

70%

60%

At least 9 years for New Vehicles to Amass 50%

50%

40%

29

30%

20%

10%

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

Source: U.S. EIA Annual Energy Outlook 2018

Since ICEs are expected to be around for decades to The ability of higher octane to enable improved

come, the pursuit

2 0 1 8 2of

0 1lower

9 2020carbon

2 0 2 1 emissions

2 0 2 2 2 0 2 3may

2 0 2 engine

5 2 0 2 6 efficiency

2024 2 0 2 7 2 0 2is

8 supported

2 0 2 9 2 0 3 0by2sound

0 3 1 2 0science.

32

require changes to the fuel being consumed—by The U.S. Department of Energy’s Co-Optimization of

both legacy and future engines. Already, the market Fuels and Engines Initiative research estimates that

is witnessing policies, regulations, and incentives higher octane fuels, with a greater spread between

encouraging the use of alternative fuels such as E15, the RON and MON (known as sensitivity), can enable

B20, and renewable diesel. But other blends have the design of engines with high compression ratios

captured the attention of engine manufacturers and and turbo boosting that can increase efficiency by up

some refining interests. to 7.5%. Although the policy pursued last Congress

was unsuccessful for a variety of reasons, automotive

During the 115th Congress, a coalition of automobile

engineers are still looking for ways to fuel new

manufacturers and refiners sought legislation to

engines with a higher octane fuel to deliver greater

raise the bar on fuel octane to 95 RON (research

performance and efficiency with lower emissions.

octane number), which would be essentially

The question remains how (or when) to get there.6

equivalent to today’s 91 pump octane.5

5 This is expressed as the antiknock index and calculated by averaging the fuel’s measured RON with its measured motor octane number, or MON.

6 Fuels Institute, Analysis of the Potential for Increasing Octane in the U.S. Fuel Supply, March 21, 2019, https://www.fuelsinstitute.org/Research/Analysis-of-the-Potential-

for-Increasing-Octane-in.

11F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

F I G U R E 11 : P O S S I B L E E F F I C I E N C Y G A I N S A S S O C I AT E D W I T H O C TA N E R AT I N

8% 7.5%

Efficiency Improvement

7%

6%

5% 4.1% 4.4%

4%

3% 2.5%

2%

1%

91 RON, S=8 95 RON, S=8 95 RON, S=10 98 RON, S=8 98 RON, S=12

BASELINE

Source: U.S. EIA Annual Energy Outlook 2018

Meanwhile, as the effort to reduce carbon emissions continues, one tool that states and regions have

considered are programs that require the industry to deliver to the market fuels with lower carbon intensity.

The California Low Carbon Fuel Standard (LCFS) is the first fully implemented program of its type in the

nation and is viewed by many as a model for success. Consequently, many other states and regions are

working to develop similar programs. Specifically, Oregon has done so, Washington has made a valiant

attempt to do so, a collection of midwestern governors have signed a memorandum of understanding (MOU)

to explore a regional regulation, and the Transportation and Climate Initiative in the Northeast seems to be a

combination of a low-carbon program and a carbon tax.

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

F I G U R E 1 2 : U . S . P R O G R A M S T H AT R E Q U I R E M A R K E T F U E L S W I T H L O W E R C A R B O N I N T E N S I T Y

Carbon tax measure

failed in Maine last year

LCFS Policy in Place

LCFS Legislation Failed in 2019

Midwest LCFS– Maybe?

Considering Carbon Tax on Fuel

TCI States – Cap

and Trade on Fuels

Source: Future Fuel Strategies

12F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

The lessons learned from analyzing the

California LCFS program provide some

insight into what might result should such

programs spread to other regions. California

has found that the greatest contributor

to reducing the carbon intensity of its

fuel supply has been through increased

use of biofuels. The latest projection

estimates that 80% of the required carbon

reduction in 2020 would be satisfied by

using ethanol, biodiesel, and renewable

diesel. If the California LCFS program serves

as the foundation for other programs, it

is likely that biofuels will assume a much

more significant role in the overall U.S.

transportation market in the coming years.7

7 Fuels Institute, Market Reactions to Low Carbon Fuel Standard

Programs, February 22, 2019, https://www.fuelsinstitute.org/

26.6 29.2 32.8

Research/Market-Reactions-to-Low-Carbon-Fuel-Standard-Progr. 35.8 39.4 41.4 39.9 41.2 41.3

More than 25 years 11 to 15 years

21 to 25 years 6 to 10 years

FE DE R AL TAX CR E DIT 16 to 20 years 0 to 5 years

F I G U R E 1 3 : C A L I F O R N I A’ S E V O LV I N G P R O$57,067

J E C T E D$54,200 $60,390

LCFS CREDIT POOLS FOR 2020 COMPLIANCE

100%

57.3%

80%

Renewable Diesel

Biodiesel

Natural Gas

60%

Renewable Gasoline

Percentage

Hydrogen

Electricity

40%

Low-CI Ethanol

Sugar Ethanol

Starch Ethanol

20%

20.0 %

0.0

2009 2 0 11 2015 2018 LD/High ZEV

Source: Fuels Institute Report by Trinity Consulting and Stillwater Associates

13F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

The State Of Vehicle

Electrification 26.6 29.2 32.8 35.8 39.4

The momentum of public opinion, FEDERAL TAX CREDI T

FIGURE 14. PLUG-IN ELECTRIC VEHICLES SOLD

government policy, and the leaders $57,067 $54,200

of the automobile industry indicate BEV PHEV Highlighted numbers

that the future for electric vehicles will

are year over year

changes in sales

be bright. The technology that will 350000

74.7% -0.6%

enable electric vehicles to satisfy a

300,000

growing segment of the transportation

market is developing rapidly, and soon 250,000

consumers will have a competitive 200,000 26%

Total Sales

economic choice between similarly

29.7%

equipped vehicles powered by 150,000

traditional or electrified powertrains. 100,000

As the market grapples with reducing carbon

50,000

emissions and the transportation industry seeks

sustainable solutions, it is essential to understand

0

the fundamentals of the market and to make

business decisions based upon facts and realistic 2015 2016 2017 2018 2019

expectations for the future. This requires taking Source: Wards Intelligence

a fresh look at the data. There are many exciting

developments in this space, and electric vehicles are

2008 2009 2010 2011 2012 2013

becoming more capable, affordable, and convenient

Plug-in vehicle sales

$52,500 in 2018$54,568

beat 2017 by 75%, and

(e.g., charge times are coming down), but they are $69,262

many assumed this rate of growth would continue

still in the early stages of market growth.

— this optimism was supported by rapid technology

Even with the expansion of sales of plug-in vehicles advancements and the introduction of more models

over the past five years, there has been inconsistency to the market. By June 2019, sales of BEVs were up

in market penetration. The year-over-year change in 96% over the previous year, and it seemed indeed

sales of plug-in hybrid electric vehicles (PHEV) and like 2019 was going to be an exceptional year. But

battery electric vehicles (BEVs) since 2015 shows the then everything slowed down, and overall plug-in

challenges of penetrating the vast LDV market. sales for the year ended lower than in 2018.

1426.6 29.2 32.8 35.8 39.4 41.4 26.6 39.9 29.2 41.2 32.8 41.3 35.8 39.4 41.4

F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

More than 25 years 11 to 15 years

There are a variety of potential

21 to 25 explanations

years for 6 to 10 years

FIGURE 15. SHARE OF SALES BY POWERTRAIN

this, but one that should 16

betoconsidered

20 years

is the 0 to 5 years

100% expiration of the federal tax credit for electrified

models offered by Tesla and General Motors (GM).8

It is uncertain how this policy affected sales, what

other factors may have contributed to the decline

in plug-in vehicle sales, or how trends may continue

in coming years. One interesting fact to note about

2019, however, is that BEVs ended the year up 17.1%

over 2018 while PHEVs dragged down the sector by

80%

dropping 30.6%.

A fact that is often missing from the discussions

about transitioning to an electrified future is that

gasoline-powered ICEs remain dominant. Since

2015, sales of vehicles equipped to run exclusively

on gasoline-powered ICEs have yielded just 1.6%

of market share and continue to represent 92.4%

60%

of total LDV sales. Reflecting on how long it will

take to transition the market to a new technology

assuming 100% immediate conversion of all new

Total Sales

vehicles, the dominance of the gasoline engine

94% 92.4%

further demonstrates the challenge of transitioning

the market to something new.

40%

FIGURE 16. SHARE OF SALES OF NON-GASOLINE

POWERTRAINS

8%

7%

6%

Non-Gasoline Powertrain Sales

5%

0.7% 0.5%

20%

1.2% 1.4%

4%

Fuel Cell

3%

Hybrid

PHEV 2%

Electric

Diesel 1%

Gasoline

0.0 0.00

92.4%

2015 2016 2017 2018 2019 2015 2016 2017 2018 2019

Source: Wards Intelligence

8 Once a manufacturer sells 200,000 qualified electrified vehicles, the federal tax credit phases out for additional vehicles sold by that manufacturer. The tax credit is still

available to other manufacturers until they reach the 200,000-unit threshold.

15F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

When analyzing the market for non-gasoline-powered vehicles, slight shifts in consumer purchasing behavior

become apparent. In the electrified sector, BEVs did gain some market share, but at the expenses of PHEVs.

Combined, they still represented only 1.9% of sales — the same market share they commanded in 2018. This

is not to say that electrified vehicles do not have a promising future — they certainly do, especially considering

interest from both automakers and policymakers and the number of new models expected to be introduced

in the coming years. But as for right now, they are still struggling to gain market share.

Even if PHEVs and BEVs were to continue recording strong year-over-year sales, it would take many years

before they would significantly impact the overall LDV fleet. Figure 17 presents three scenarios (Low, Mid

and High) in which PHEV and BEV sales would increase by 10%, 15% or 20%, respectively, every year from

2020 through 2040. (No assumptions were made in creating this chart other than as stated that sales would

increase by a consistent percentage every year.) In these scenarios, electric vehicle sales could capture

between 16.6% and 94.5% of LDV sales. However, given fleet turnover rates, the number of plug-in electrified

vehicles on the road would represent between 7.4% and 26.6% of the fleet. As mentioned before, the LDV

market is large and currently dominated by gasoline-powered ICEs, and it will take many years of sales

expansion to change the dynamics of the market.

F I G U R E 17 : P O T E N T I A L G R O W T H O F B AT T E RY E L E C T R I C A N D P L U G - I N H Y B R I D V E H I C L E S

Assumptions: High Growth % Sales High Growth % Stocks

U.S. EIA Annual Energy Outlook 2020 LDV Fleet Size and Sales

Mid Growth % Sales Mid Growth % Stocks

Annual of Sales Growth for BEV & PHEV:

High Growth: 20% increase in sales each year Low Growth % Sales Low Growth % Stocks

100% Mid Growth: 15% increase in sales each year

Low Growth: 10% increase in sales each year

Scrappage Rates: LDV 5.5%, PEV 5%

80%

39

60%

40%

29

20%

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

Source: Fuels Institute

16F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

ELECTRIFIED VEHICLES ARE

OVERCOMING CONSUMER CONCERNS

Despite the slow start and the challenges facing

electric vehicles (EVs) in their quest to penetrate

the LDV market, there is tremendous cause for

optimism about their future. Research indicates that

consumers who are not yet ready to purchase an

electric vehicle primarily are concerned with range,

recharge time, and purchase price. The EV market

has responded. Vehicles are consistently delivering

more than 200 miles per charge, with GM most

recently announcing a battery system for its BEVs

that will deliver 400 miles per charge. In addition,

batteries are becoming more durable, and fast

charging is much more of a viable option. Tesla has

announced that their new V3 Supercharging system

will be able to deliver up to 75 miles of range in five

minutes of charge 26.6

time. 29.2 32.8 35.8

39.4

41.4 39.9 41.2 41.3

F I G U R E 18 : 2 4 B E V S AVA I L A B L E I N 2 0 2 0

150,000

Taycan Turbo

120,000 Model X

Performance Model S

MSRP After Incentives (Virgiinia)

Performance

90,000 Model X

Long Range

e-tron Plus Model S

I-Pace Long Range

Mach E Premium Mach E Model 3 Performance AWD

60,000 First Edition Plus

Mach E Select Mach E GT

Model 3 Long

Cooper S E i3 Bolt Range AWD

Hardtop 2

30,000 Door Electric Kona Electric

Leaf

Ioniq Electric Mach E California Rt. 1

e-Golf Leaf Plus Model 3 Standard Range Plus

Niro EV

0

100 150 200 250 300 350 400

RANGE IN MILES

Source: Plug-In America (PlugStar.com)

17

7.5%F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

Despite these advancements, purchase price to decline as batteries become more affordable.

remains a challenge. The majority of vehicles Since 2014, the price per kilowatt-hour of BEV

available in 2020 that offer 200 miles or more batteries has come down 73%.

of range are also priced $40,000 or higher and

Within a few years, consumers will have the option

average $44,272 (excluding

26.6 the three 32.8

29.2 vehicles 35.8 39.4 41.4 39.9 41.2 41.3

to purchase a BEV that is priced competitively with

with MSRPs of $100,000 or more). This purchase

a comparable ICE vehicle, has a range of 250 miles

price may be outside the realm of affordability for

or more, and can substantially recharge within 15

most families to achieve a scale of mass adoption.

minutes. Add the fact that maintenance for a BEV

Adding to this challenge is the fact that the federal

is significantly less expensive than for an ICE and

tax credit of $7,500 is limited to the first 200,000

the option of an electric vehicle could be attractive

units sold by a manufacturer and already has

for many customers. This reality leads to many

expired for Tesla and GM. That being said, prices

optimistic forecasts for the future of the EV market.

are coming down and are expected to continue

F I G U R E 19 : P R I C E O F E L E C T R I C V E H I C L E B AT T E R I E S ( $ / K W H )

$1,160

$1,200

$1,000 $899

$4,800 $707 $650 $577

$600

$373

$400 $288 $214 $176 $156

$200

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: CarGurus, Bloomberg NEF, Statista

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

18F U E L S I N S T I T U T E | S26.6 29.2

TAT E O F T R A N S P O RTAT I32.8

O N E N E R G35.8

Y A N D V E H I39.4

C L E E L E C T R41.4

I F I C AT I O N 39.9 41.2 41.3

F I G U R E 2 0 : M U LT I - S TAT E Z E V TA S K F O R C E S H A R E O F U . S . N E W V E H I C L E R E G I S T R AT I O N S —

2 0 1 8

11.7%

10%

Percentage of U.S. New-Vehicle Registrations

8%

6%

6%

4% 3.50%

2% 2.10%

2% 1.60%

1% 1%

0.40% 0.30% 0.30%

CA C0 CT ME MD MA NJ NY OR RI VT

Source: NADA.org

In addition to these market forces creating Ten other states have signed an MOU with California

opportunities for electrified vehicles, government establishing the Multi-State ZEV Task Force,10

policies also provide momentum. California’s committing to have at least 3.3 million ZEVs

Zero-Emission Vehicle (ZEV) Program requires operating on their roadways by 2025. Signatories

most automobile manufactures to ensure a certain to the MOU include Colorado, Connecticut, Maine,

percentage of their sales into the state are ZEV.9 Maryland, Massachusetts, New Jersey, New York,

Qualified vehicles generate credits based upon Oregon, Rhode Island, and Vermont. According to

their electric driving range. California increases the National Automobile Dealers Association,11 in

the credits required each year from 4.5% in 2018 these states combined to represent 30% of

2018 to 22% in 2025. California estimates that new registered vehicles in the U.S., creating a strong

compliance with the 2025 requirement will equate incentive for vehicle manufacturers to increase

to about 8% of new vehicles sold being ZEVs and production and delivery of electrified vehicles into

plug-in hybrids. these markets.

9 “Zero-Emission Vehicle Program,” California Air Resources Board, accessed June 3, 2020, https://ww2.arb.ca.gov/our-work/programs/zero-emission-vehicle-program.

10 Multi-State ZEV Task Force (website), accessed June 3, 2020, https://www.zevstates.us/.

11 “Auto Retailing: State by State,” National Automobile Dealers Association, accessed June 3, 2020, https://www.nada.org/statedata/.

19F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

Within a few years, there

will be a competitively

priced BEV with a range

of 250 miles or more that

can substantially recharge

within 15 minutes. Add lower

maintenance costs and the

option of an electric vehicle

could be attractive for

many customers.

20F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

I M PA C T O F R E TA I L G A S O L I N E P R I C E S

Fuels Institute research has demonstrated that consumers are most focused on alternative-fueled vehicles

when retail gasoline

26.6

prices are

29.2

high. For

32.8

example,

35.8

during a39.4consumer survey in39.92014, when

41.4 41.2

gasoline

41.3

was $3.64

per gallon, 84% of consumers said they would consider a hybrid electric vehicle (HEV) for their next purchase.

Low Medium High Variation

However, during a survey in 2016, when gasoline was $1.74, only 44% of consumers said they would consider

an HEV. Likewise, HEVs garnered their greatest share (3.2%) of the LDV sales market in 2013 when the average

price of gasoline was $3.49, but that share dropped to 1.9% in 2016 when gasoline prices averaged $2.13.12

FIGURE 21: INTEREST IN HYBRID ELECTRIC VEHICLES AND GAS PRICES

Gasoline Price Consider HEV

100%

$3.50

80%

$3.00

$2.50

% Consider HEV

60%

Gas Price

$2.00

$1.50 40%

$1.00

20%

26.6 29.2 32.8 35.8 39.4 41.4 39.9 41.2 41.3

$0.50

Low Medium High Variation

2013 2014 2015 2016 2017

Source: Fuels Institute, PSB, OPIS

FIGURE 22: SALES OF HYBRID ELECTRIC VEHICLES AND GAS PRICES

10.36%

Average Gas Price Hybrid Sales

$4.00 42.94% 4.0%

$3.50 3.5%

$3.00 3.0%

$2.50 2.5%

% of Fleet Sales

Gas Price

$2.00 2.0%

$1.50 1.5%

$1.00 1.0%

$0.50 0.5%

2013 2014 2015 2016 2017 2018 2019

Source: OPIS, Wards Intelligence

12 Fuels Institute, Consumers and Alternative Fuels 2017, December 08, 2017, https://www.fuelsinstitute.org/Research/Consumers-and-Alternative-Fuels-2017.

21F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

FIGURE 23: GASOLINE AND DIESEL PRICES FORECAST

Gasoline

$4.00 Diesel Fuel

17%

increase

forcasted

$3.50

Retail Price

$3.00

$2.50

$2.00

2019 2020 2021 2022 2023 2024 2025 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040

Source: U.S. Energy Information Administration

Of course, market dynamics have evolved over the

past several years, and the attraction of electric

vehicles for current customers may not be directly

related to fuel prices. But if EVs are to gain a scale of

mass adoption, consumers will consider the retail

price of fuel as a metric in their search for their next

1980 1990 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2015 2017

vehicle. If the advancements in fuel efficiency result

in a drop in demand for liquid fuels as projected by

the EIA, then the impact on retail pump prices would

likely be to the advantage of consumers. EIA’s Annual

Energy Outlook 2020 projects that gasoline prices

could climb 16.5% and diesel fuel 18.0% by 2040,

putting gasoline at about $3.10 per gallon and diesel

at about $3.59. It is unclear whether these prices

will be sufficiently high to strengthen the appeal of

alternative powertrains like EVs.13

13 U.S. Energy Information Administration, Annual Energy Outlook 2020, January

29, 2020, https://www.eia.gov/outlooks/aeo/.

22F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

Conclusions

The future of transportation energy The pace of that transition, however, could be

accelerated through government policies that

will be a mix of different powertrains

drive adoption of new technologies, market forces

leveraging different sources of energy, that combine to reduce the cost of entry for new

the majority of which presumably technologies (such as fleets purchasing large

will be lower in carbon intensity and quantities of electrified vehicles), or fuel economics

compelling consumers to seek more efficient and

more beneficial to the environment.

lower cost mobility options.

But the transition to new powertrains

At the end of 2019, these accelerating factors were

or energy sources will take time. This

not wielding significant influence over the market,

is not due to opposition to such and the transition to alternatives beyond traditional

technologies or resources but because powertrains and liquid fuels was minimal. However,

the market is substantial, and it will there are signals that some fundamentals may

be evolving to create opportunities for the new

simply take time to transition.

technology to gain greater market share in the

coming years. It is a dynamic worthy of frequent

evaluation to better understand the market forces at

work, the trends affecting consumers and the data

that tells the true story of change.

23F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

About the

Fuels Institute

The Fuels Institute, founded by NACS in 2013, is a 501(c)(4) non-profit

research-oriented think tank dedicated to evaluating the market issues

related to vehicles and the fuels that power them. By bringing together

diverse stakeholders of the transportation and fuels markets, the Institute

helps to identify opportunities and challenges associated with new

technologies and to facilitate industry coordination to help ensure that

consumers derive the greatest benefit.

The Fuels Institute commissions and publishes comprehensive, fact-based

research projects that address the interests of the affected stakeholders.

Such publications will help to inform both business owners considering

long-term investment decisions and policymakers considering legislation

and regulations affecting the market. Research is independent and unbiased,

designed to answer questions, not advocate a specific outcome. Participants

in the Fuels Institute are dedicated to promoting facts and providing decision

makers with the most credible information possible so that the market can

deliver the best in vehicle and fueling options to the consumer.

For more about the Fuels Institute, visit fuelsinstitute.org

F U E L S I N S T I T U T E S TA F F

JOHN EICHBERGER AMANDA APPELBAUM

Executive Director Director, Research

jeichberger@fuelsinstitute.org aappelbaum@fuelsinstitute.org

JEFF HOVE D O N O VA N W O O D S

Vice President Director, Operations

jhove@fuelsinstitute.org dwoods@fuelsinstitute.org

FOR A LIST OF CURRENT FUELS INSTITUTE BOARD MEMBERS AND

FINANCIAL SUPPORTERS, PLEASE VISIT FUELSINSTITUTE.ORG

24F U E L S I N S T I T U T E | S TAT E O F T R A N S P O RTAT I O N E N E R G Y A N D V E H I C L E E L E C T R I F I C AT I O N

The Fuels Institute was founded in 2013 by NACS, the international

association that advances convenience and fuel retailing. Through

recurring financial contributions and daily operational support, NACS

helps the Fuels Institute to invest in and carry out its work to foster

collaboration among the various stakeholders with interests in the

transportation energy market and to promote a comprehensive and

objective evaluation of issues affecting that market and its customers

both today and in the future. NACS was founded August 14, 1961, as the

National Association of Convenience Stores and represents more than

2,100 retail and 1,600 supplier company members.

www.convenience.org

25(703) 518-7970 FUELSINSTITUTE.ORG @FUELSINSTITUTE 1600 DUKE STREET SUITE 700 A L E X A N D R I A , VA 2 2 3 1 4

You can also read