SONAR Monthly Market Update - A deep dive into the freight markets with unprecedented - FreightWaves

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SONAR Monthly Market Update

A deep dive into the freight markets with unprecedented

charts, analysis and market commentary.

January 2019 Edition

For distribution and use by FreightWaves SONAR seat licensed users only.

sonar.freightwaves.com

1

Table of Contents

1. Economic Outlook…….…………………………….……………………………….……………………………….………………...Page 3-4

2. Manufacturing……………………………..……………………..….……………………………….………………………………….Pages 5-6

3. Retail and Inventories…..………………..…………..……...………………………………….………………………..……….Pages 7-9

4. Labor Markets………………………...……………...……………………..….……………………………….……………..……...Pages 10-11

5. Housing and Construction………..…………………………….…………………….……………….………………..…Pages 12-14

6. International Trade………...…………………………………..…………………………………………………..…………...…Pages 15-17

7. Pricing and Inflation…………………………………….………………………….…….……………..……….………..…….……...Page 18

8. Policy & Risks………………………………….………………………….……………………………….…………………….….….Pages 19-20

9. Freight Market Overview…………………….……………………….……………….………..…….…………….………Pages 21-32

sonar.freightwaves.com

2

Economic Outlook

Source: Survey of Professional Forecasters, FreightWaves Economics

Current Environment: Signs of a slowing economy

Growth in the economy continued to show some signs of slowing down over the past month,

even as performance remains generally above trend to round out 2018. The U.S. economy

enjoyed two of the most impressive back-to-back quarters of growth in the middle of the

year, with GDP growing at a 4.2% and 3.5% annualized pace during the 2nd and 3rd quarters.

During this time, several areas of the economy enjoyed robust performance, with retail sales,

manufacturing production, and goods trade all seeing the fastest growth in years. Aside from

some weakness in housing, the economy has essentially been running on all cylinders for

most of the year. This kind of growth from some of the key drivers of freight demand

contributed to one of the strongest years for surface freight in recent memory, straining

capacity in the industry and fueling rapid rate increases both in contracts and spot prices.

sonar.freightwaves.com

3

Across nearly almost every sector, growth rates have come down from the highs experienced

in the middle of the year. After a steady stream of positive results, signs are emerging across

the economy that suggest that the pace of growth is slowing headed into next year. Growth

in most key economic indicators has come down from recent highs, and the current

environment suggest further slowing as we head into 2019.

Consumer spending remains the primary engine of demand in the economy. U.S.

households have benefitted throughout the year from a strong labor market, and the rapid

pace of hiring and wage growth has fueled income growth in the economy. Going forward,

conditions for U.S. consumers are likely to remain favorable as the tight labor market fuels

additional strength in wage growth. However, U.S. households will not get the same boost in

2019 from a tax cut like they did in 2018, and the implementation of scheduled tariffs next

year will likely hit consumers harder next year. As a result, growth on the consumer side is

likely to be strong, but not as strong going forward.

Tariffs also appear to be taking a bite out of business demand, as concerns over the future of

trade policy have reduced the incentive for firms to invest. In addition, the recent plunge in

oil prices has take the legs out from underneath the U.S. domestic energy sector, which had

been one of the strongest areas of growth. This reduced appetite for investment has caused

manufacturing activity to stumble towards the end of the year, and data on orders for

investment goods suggests that demand will remain subdued in upcoming months.

Housing also continues to face challenges. Construction activity has been the lone consistent

source of weakness throughout 2018. Recent data has been distorted by weather-related

distortions due to the hurricane season, but rising mortgage rates and and challenges with

supply will again hinder housing activity in 2019.

All of this suggests that the U.S. will continue to grow slightly above trend in upcoming

quarters, but will slow significant from the rapid pace seen in the middle of the year. We

expect growth of 2.4% in the fourth quarter, and 2.6% for all of 2019.

sonar.freightwaves.com

4

Manufacturing

In the industrial sector, industrial production (IPROG.USA) growth beat expectations in

November by advancing 0.6% from October’s levels. Year-over-year growth improved to 3.9%,

down from the rapid pace of growth in the 3rd quarter but still strong by historical standards.

However, much of the gain was driven by a surge in utility production during the month,

fueled by particularly cold weather across much of the country. This type of weather-related

surge does not mean much for the fundamentals of the industrial sector, as gains in one

month are typically reversed quickly once weather returns to normal.

Manufacturing industrial

production, which excludes utility

and mining production from the

total, stalled in November.

unchanged from October’s levels.

In addition, results from the

previous two months were revised

downward, leaving behind a more

dismal view of the health of the

manufacturing sector as we near

the end of the year. Year-over-year

growth in manufacturing

production (IPROG.MFTG) has now tumbled all the way to 2.0% after reaching a multi-year

high of 3.8% a couple of months ago.

In addition, data on new orders suggests that manufacturing activity may remain subdued in

upcoming months.

Manufacturers’ new orders for

durable goods (ORDR.DG)

increased just 0.8% in November

from October’s levels, on the

heels of a 4.3% decline in the

previous month. The fluctuations

over the past couple of months

have been caused by swings in

the volatile transportation

equipment component, which

often experiences non-seasonal

surges in aircraft orders.

Excluding transportation equipment, durable goods orders actually declined by 0.3% as

year-over-year growth stayed below 5%. Core capital orders, which are a proxy for investment

sonar.freightwaves.com

5

Manufacturing (cont.)

spending on equipment, fell by 0.6% during the month. Durable goods orders serve as a

useful leading indicator of future durable goods shipments (SHIP.DG), typically leading

shipments in the economy by 1-2 months. Orders excluding aircraft have now declined in 2

out of the last 3 months, heightening concerns over the future strength of manufacturing

activity. Durable goods manufacturing has been one of the standout areas in terms of

industrial output throughout

the year, and a slowdown in

durable goods production

would further restrain output.

Oddly enough, the hard data

on output and orders is

telling quite a different story

than survey results from the

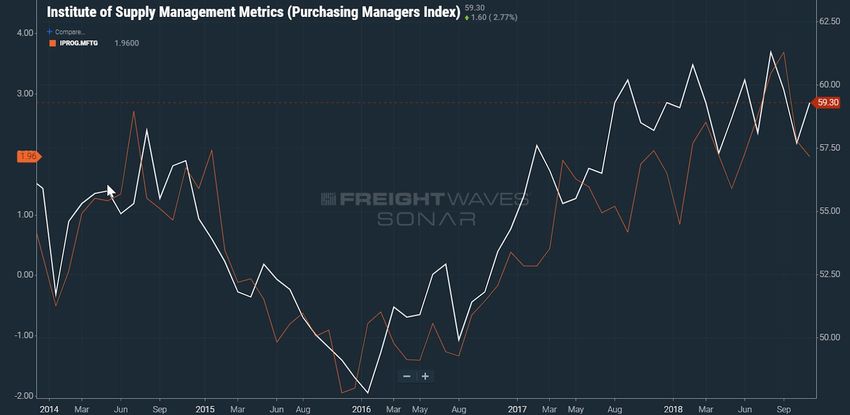

manufacturing sector. The

Institute of Supply

Management’s

manufacturing purchasing

managers’ index (PMI) continues to signal robust growth in the manufacturing sector.

Results from PMI data represent the percentage of survey respondents that report that

activity is expanding, so numbers above 50 signal expansion in the manufacturing sector.

PMI data historically has a tight correlation with year-over-year growth in manufacturing

production, with readings above 55 signaling above average growth in manufacturing.

Because of this, it is a bit surprising to see the recent results from the manufacturing PMI

data (ISM.PMI), which has hovered between 55 and 60 throughout most of the year. PMI data

has come down slightly from the 14-year high of 61.3 set in August of this year, but still

remained elevated at 59.3 even as manufacturing production growth slowed considerably.

Moreover, survey responses related to new orders have also been exceptionally strong,

diverging from the hard data on new orders in the economy.

These type of disconnects in the data happen from time to time and are usually resolved

quickly, either through one of the series shifting to meet the other going forward or revisions

to previous data showing that the disconnect never existed. Some of the regional surveys of

manufacturing activity have also declined recently, which would suggest that the national

PMI data will soon come down to match the actual output data.

sonar.freightwaves.com

6

Retail and Inventories

As mentioned earlier, after a brief lull in spending to start the year, consumer spending has

been one of the real highlights in the economy throughout 2018. This trend in retail spending

largely continued in November, though total sales in the sector rose just 0.2% from October’s

levels. Year-over-year growth (RESLG.USA) moderated to 4.2%, which is well below the 6+%

highs seen earlier this year

but still strong by historical

standards.

In addition, the gain in

November came despite a

sizeable decline in gasoline

sales . Retail sales figures are

nominal measures, and the

collapse in gas prices

throughout the month

depressed sales figures at gas

stations. Core retail sales,

which exclude motor vehicles and gas, rose 0.5% in November and are now up 4.6% from this

point last year.

Gains during the month were generally broad-based with every other major industry

category except for building materials, apparel, and restaurants expanding during the

month. Electronics stores, furniture stores, and nonstore (mostly online) retailers led the way,

with each industry seeing stronger than 1% monthly growth.

November’s retail result give the first official

glimpse at sales performance during the

holiday season, and the strength of core

spending during the month points to an

impressive peak season for retailers.

Anecdotal reports and data from private

companies such as Mastercard and Adobe

Analytics further underscore this strength,

indicating that holiday growth in 2018 was

one of the strongest in recent years.

We expect the official holiday sales

numbers, which exclude auto, gasoline, and

building material sales, to come in at 4.5%

higher than they were in 2017.

sonar.freightwaves.com

7

Retail and Inventories (cont.)

This would place it slightly below the 5.3% pace seen in 2017, but still makes 2018 one of the

strongest years for holiday retail in the past decade. As has been the case all year,

e-commerce likely grew in above 15% during the holiday season, continuing to gain

significant share in the retail space.

It is also worth remembering that e-commerce during the holiday season works a bit

differently than it does during the rest of the year. Because so many of the purchases are

gifts for others, there is typically a surge in return volume in the weeks following Christmas.

This typically keeps parcel demand high through the early part of January, and for LTL

carriers may require some deliveries from a residential location to a warehouse or retailer.

However, there are signs emerging that retail growth may begin to slow down going

forward. Consumers are likely to still find themselves in a generally favorable environment in

upcoming months, with solid job growth and rising wages providing the fundamentals for

retail spending. However, consumers will not another boost to disposable income in 2019 as

they did in 2018 with the passage of the Tax Cuts and Jobs Act. As a result, disposable income

growth should remain healthy, but not as strong as it was throughout 2018.

Secondly, the next wave of tariffs on imports from China will target more consumer goods if

they are implemented as planned in 2019. This means that the prices of things that

households typically purchase may experience a level shift as retailers are forced to

accommodate the higher cost of imported goods. This would further restrain consumer

spending in the economy and lead to weaker retail performance in 2019.

Lastly, equity markets have plunged over the past couple of months. The S&P 500 has

declined nearly 15% since peaking on October, with nearly 10% of that decline coming in

December alone. This reduces the amount of household wealth in the economy, which

negatively affects consumer spending. There are also signs that suggest that this recent drop

in the stock market is starting to affect consumer confidence. The Conference Board’s

consumer confidence index experienced the largest monthly drop in over three years in

December, with a severe decline in consumer expectations about the future health of the

economy. Confidence is still generally high even after the dip in December, but if the collapse

in stock markets deepens and confidence falls further, consumers may not be willing to go

out and spend even if they have the ability to go and purchase products.

sonar.freightwaves.com

8

Retail and Inventories (cont.)

On the inventory side, levels have climbed steadily over the past couple of months after

falling in the 2nd quarter of the year. Due to tariff concerns much of this inventory build has

been driven by US businesses importing more goods than they traditionally would. This has

caused inventory/sales ratios to creep up from the lows seen earlier in the year. The total

business inventory-sales ratio

(TBIS.USA) reached 1.35 in

October after hitting a

multi-year low of 1.33 in the

middle of the year.

This trend is likely to continue

for the remainder of the year,

which should ease some

time-sensitive pressure on

carriers that were previously

held to just-in-time inventory

movements.

In addition, if businesses are indeed bringing goods into the ports earlier than normal and

storing them in inventory, then once tariffs hit there should be a shift away from port

volumes and a rise in shipments from warehouses to retailers or manufacturers. When this

happens, inventory/sales ratios should continue to drift downward, resuming the trend seen

earlier this year.

sonar.freightwaves.com

9

Labor Markets

Of course, any strength that emerges from the retail sector hinges on continued support

from job and income growth. The impressive pace of hiring and accelerating path of wage

growth boost consumer sentiment in the economy provide critical support for spending

behavior.

Job growth slowed down as the the economy added 155,000 workers to payrolls during the

month, down from a downwardly-revised gain of 237,000 in the previous month. This fell well

short of consensus estimates of a 198,000 gain, but is still a solid number on the heels of last

month’s impressive result. Job growth has now been positive for a record 8 years and two

months in a row, and has averaged over 200,000 per month since the start of 2018.

Other measures of labor

market health suggest that

hiring conditions remain

generally tight in the

economy. The unemployment

rate (UEMP.USA) held steady

at 3.7%, matching the lowest

rate in the economy since

1969. Wage growth also

continued to advance at a

solid pace in this morning’s

report, as average hourly

earnings rose 0.3% from October’s levels. Yearly earnings growth exceeded 3% last month

and remained unchanged at 3.1% in November. This would suggest that the shrinking pool of

available workers is leading businesses in the economy to raise wages in an effort to attract

and retain employees.

Going forward, the combination of a lack of qualified available labor and higher wage rates

will likely cause the pace of hiring to slow from the current pace. The 155,000 jobs added

result seen in November is likely to become the norm for the labor market. The economy is

beginning to transition from a high job growth, modest wage growth environment to one

with more modest job gains but better wage growth. As long as economic growth in the

economy remains at or above trend, labor market conditions will remain tight and this shift

should continue in upcoming quarters.

However, like many of the other indicators in the economy, there are some concerns that

hiring in the economy may slow faster than expected. Survey data has increasingly reported

that businesses in the economy are concerned about all of the uncertainty surrounding trade

sonar.freightwaves.com

10Labor Markets (cont.)

policy. The U.S. recently agreed to a cease-fire in the ongoing trade dispute with China, but

has yet to reach a concrete resolution. What this means is that the air of uncertainty

surrounding tariffs is likely to remain at least through the early parts of 2019, and businesses

may be more reluctant to hire new workers.

Our view is that a prolonged trade dispute will eventually have a negative impact on hiring

trends in the economy. However, most of the job growth in the economy comes from the

service sector, which is less affected by tariffs and trade policy. As a result, job growth is likely

to remain strong enough to keep the labor market tight in upcoming quarters.Despite the

sowing pace of job growth in the overall economy, hiring within the transportation and

logistics industry remained strong as employment grew by 25,400 during the month. As was

the case in October, much of the gain was driven by parcel companies, which saw the largest

monthly job gain in nearly two years with 9,900 workers added to payrolls. Warehousing and

storage also enjoyed strong employment growth, adding 6,200 jobs in November

The trucking industry also saw

solid hiring during the month,

adding 4,500 workers during

the month on a seasonally

adjusted basis (EMPS.TRUK).

This was offset by downward

revisions to previous data,

which revealed a slight

decline in trucking hires in

October. Still, trends within

the industry continue on a

general climb, and

employment within for-hire trucking is now 2.5% higher than at this point last year.

To put this in perspective, consider that employment in the economy overall is growing at a

1.7% pace. This would suggest that the trucking industry is gaining some ground as it

attempts to address the capacity crunch. Hiring in the industry is not occurring as quickly as

it among parcel companies and warehouses, which benefit from exceptionally strong growth

in e-commerce demand. Trucking employment is growing faster than other modes of

surface transportation however, and is even outpacing manufacturing hiring in the economy.

sonar.freightwaves.com

11Housing and Construction

As mentioned earlier, housing and construction has been a consistent source of weakness for

freight demand and the economy overall. Housing continues to be plagued by problems on

both the supply and demand side of the market, restaining the amount of activity that most

expected at the start of this year

On the construction side, housing starts(HOUS.USA) jumped in November, rising to a 1.256

million annualized pace from

a 1.217 pace in the previous

month. The gain in November

was entirely driven by a rise in

the volatile multifamily

component of housing starts.

Single family home starts fell

4.6% in November and are

now 3.6% lower than at this

point last year.

As was the case in September

and October, data on

November housing starts was distorted by weather events. While results in previous months

were restrained by hurricanes hitting the South region, November data on single-family

home starts was held back by the recent wildfires in California. Single-family starts in the

West region (HOUS.URWT) fell

by a whopping 24.4% in

November, helping to bring

down the overall housing

numbers. This decline was

partially offset by a 6.8% gain

in the South, likely boosted by

rebuilding activity after the

hurricane season.

All of these weather-related

fluctuations have made it

difficult to interpret the

underlying trends in recent months. On one hand, the results from the single-family

construction sector were not as bad as the numbers might suggest, because the downturn

in the West is only temporary. In fact,

sonar.freightwaves.com

12Housing and Construction (cont.)

the weakness in November should lead to additional construction in upcoming months, as

residents look to either rebuild or replace their damaged homes.

On the other hand, there was already some rebuilding activity helping to boost single family

construction during the month. In addition, the West wasn’t the only region to experience a

decline during the month. Every other region except for the rebuilding-aided South saw

declines in single family home construction during the month, suggesting that the softness

in the sector is much broader than just a temporary weather problem.

The fact is that housing had already been a disappointment before any of these major events

occurred, and once all of the rebuilding happens, the construction industry will still be faced

with some key concerns. The construction industry continues to struggle with finding skilled

workers to build homes. In addition, home builders have struggled with a lack of developed

lots for building. This shortage of available lots for construction means that prospective home

builders have to pay more for the limited supply available. This adds to the costs of building

new homes, and further contributes to the disappointing building activity in 2018. Headed

into next year, there are no easy solutions for these problems, and we expect housing starts

to continue to struggle once all of the weather effects fade.

Unfortunately, it may be quite a while before we get a clear picture of construction trends.

Even without major weather events like hurricanes and wildfires, housing data can be

difficult to interpret during the winter months. Abnormally cold or warm weather in

December, January, and February can cause unusual jumps or declines in building activity.

Add to that all of the pent up building activity caused by damages from recent events, and it

is likely that housing construction data will be quite volatile through the early part of next

year.

On the demand side, sales have also been a disappointment throughout the course of the

year. However, recent signs suggest that the pace of sales may be picking up as we near the

end of the years. Purchases of previously-owned homes rose for the second straight month,

rising to a 5.32 million annualized pace in November from a 5.22 million pace in October.

However, even with improvement in recent months, existing home sales are still 7.1% lower

than they were at this point last year.

The lack of available inventory for purchase remains a key issue for existing home sales.

Home building activity has been weak, so potential buyers are having a hard time finding

homes for purchase. This, in turn, has pushed up prices in the economy throughout the

course of the year and further affected demand.

Rising mortgage rates may also be curbing activity. The pace of home price appreciation has

eased in recent months but the 30-year mortgage rate has increased by 60 basis points

sonar.freightwaves.com

13Housing and Construction (cont.)

throughout the course of the year. This has further affected the ability of potential consumers

to purchase a home.

Lastly, the recent change in the tax code contained some provisions that were unfavorable to

homeowners. Specifically, the limits placed on the amount of property taxes that can be

deducted from taxable income have removed some of the incentives for purchasing

higher-end homes, particularly in high property tax states in the Northeast. As with

construction, these issues are not disappearing any time soon, so expect home purchasing

behavior to advance at a slow pace in upcoming quarters.

The softness in home buying has begun to affect some of the connected industries in retail.

Home buying typically drives remodeling and renovation spending, as well as additional

spending on home furniture and household appliances. Retail spending on building

materials and appliances have seen growth in 2018, but have lagged behind overall retail

spending in the economy. It is through these channel that home sales affects freight

demand in the trucking industry, and weakness on the home sales front combined with

softness in home building has negative implications going forward.

sonar.freightwaves.com

14International Trade

In the trade sector, all eyes have been focused on goods import and export numbers for signs

that the recent implementation of tariffs on many imported goods is beginning to affect

global trade patterns. To this point, tariffs have certainly introduced some volatility into usual

trade behavior, but overall trade volumes remain generally strong as we round out the year.

On the export side, much of the volatility has been driven by agricultural exports. China

implemented tariffs on US

exports of agricultural

products such as soybeans

and sorghum in July of this

year in retaliation for some

tariffs that the Trump

administration placed on

imports from China. This led

to a surge in agricultural

exports during the 2nd

quarter in advance of the

tariffs, and pushed overall

goods export growth

(GOEXG.USA) to a multi-year high above 13% in May.

China followed up the tariff hike with an outright ban on soybean imports from the U.S. As a

result, exports of agricultural products have struggled in recent months, dropping 6.8% in

October after an 8.0% decline in September. This has weighed down overall export growth,

which has fallen below 9% in the most recent data. China has recently agreed to lift the ban

on soybean imports, which should help export performance in upcoming months

Not everything here is tariff related however. Global growth among some of the U.S.’ key

trading partners is beginning to show signs of slowing down, most notably the UK and the

rest of the European Union. This makes for a tough export environment, and will likely

continue to be an issue in upcoming quarters even if tariffs are not increased any further. In

addition, the U.S. Dollar has appreciated over 5% in real terms since the start of the year. This

makes U.S. made goods comparatively more expensive and further hampers export

performance

On the import side, the U.S. has already implemented 10% tariffs on a number of Chinese

imports, in addition to earlier tariffs on imports of steel and aluminum. Up until recently, the

sonar.freightwaves.com

15International Trade (cont.)

U.S. appeared set to raise the tariffs on Chinese-made goods to 25% at the start of 2019, which

led many businesses to begin bringing in imported goods ahead of schedule to avoid the

potential tariff hike. As a

result, goods imports

(GOIMG.USA) have surged in

recent months, with growth

reaching as high as 11.5%

before moderating in

October. Like exports, there

will likely be some payback

on the import side in

upcoming months. Even if

tariff increases never

materialize, businesses

already find themselves with

higher than normal

inventories of imported goods, and will likely scale back import behavior while these

inventories get drawn down. This may disrupt some of the normal seasonal patterns,

particularly those are Chinese New Year which takes place early next year.

Also like exports, there are some fundamentals at play in the recent import results. The

strength in the domestic U.S. and general tightness in capacity for U.S. businesses

encourages imports of goods from the rest of the world. In, addition, the gain in the value of

the U.S. dollar makes foreign goods comparatively cheaper and further encourages import

volume.

What this means is that the trade deficit may rise even with the U.S. placing or increasing

tariffs on goods from the rest of the world. There are likely to be some wild swings in import

and export performance as the U.S. and other countries hash out their plans for trade policy,

but the deficit should tend to generally widen in upcoming quarters

A widening trade deficit is not necessarily bad news for freight demand, however. Both

import and export movements are good for ocean, air, and surface freight demand, so as

long as overall trade is growing, it is generally good news for carriers. October’s results were a

bit of a disappointment in this regard, as the decline in goods exports outweighed the gain in

imports. Still, year-over-year growth in to the total value of traded goods (exports plus

imports) is growing at al healthy clip despite all of the global concerns over U.S. trade policy.

Growth has hovered near double digits since the end of 2017, and has yet to show any real

signs of slowing.

sonar.freightwaves.com

16International Trade (cont.)

The bigger concern from a trade perspective isn’t whether or not tariffs will increase to cost

of trading with other countries, it’s the state of global growth. With signs in the U.S. economy

pointing towards a less impressive year of growth in 2019 and growth among major trading

partners also beginning to slow, overall trade volume growth will likely moderate from the

rapid pace seen in 2018.

sonar.freightwaves.com

17Prices and Inflation

Overall, signs from nearly every areas of freight demand point to softening growth headed

into next year. In addition, hiring trends within the industry suggest that trucking has been

adding capacity at a decent clip. As a result, trucking will likely feel less capacity-constrained

in 2019 than it did in 2018.

As a result, rate increases should calm somewhat within trucking. Year-over-year rate

inflation in the trucking industry is facing increasingly tough comparisons to last year, which

is going to put downward pressure on yearly gains going forward. Freight rates began their

surge last in August in the aftermath of Hurricane Harvey, and continued through the

impressive holiday season of 2017 and the ELD mandate. As a result, the tough comparisons

should lead moderating yearly

rate growth even if rates

continue to climb.

This phenomenon is already

playing out in the Producer

Price Index (PPI) data released

by the Census Bureau, which

measures the prices that

businesses receive for the

goods and services they

provide.. Year-over-year

growth in the PPI for the

trucking industry (PPIG.GFTK) has come down from the record high of 9.8% set in July of this

year, settling in at 8.3% in November. However, rates are still making solid advances in the

industry, with the PPI for trucking making an impressive 1.2% monthly gain in November

after a solid 0.5% increase in the previous month.

Gains during the month were largely driven by long-distance truckload services, which

posted a second consecutive monthly gain above 1% with a 1.3% gain in November. Both

truckload and LTL services enjoyed healthy gains during the month, with rates rising 1.2% and

1.6%, respectively. Local trucking rates also experienced a respectable 0.5% increase during

the month, and are now 10.1% higher than at this point last year.

This would suggest that carriers still retain some pricing power in this environment of

moderating demand,and have been able to extract higher rates across many different types

of freight. Year-over-year rate inflation probably will not reach the highs seen in July for quite

some time, but the pace of rate increases is still well above average as we head into next year.

sonar.freightwaves.com

18Policy and Risks

Much of this outlook for above-average but moderating growth going forward hinges on the

policy environment as we head into next year. Drastic changes to fiscal, monetary, and trade

policy could have significant implication for the performance of the economy in upcoming

quarters, and there are a number of issues that remain unresolved at the end of 2018.

Trade policy has been at the forefront of the policy arena throughout much of the year,

beginning all the way back in February when President Trump announced the first tariffs on

steel and aluminum imports from the rest of the world. Much of the attention has been

focused on the U.S. trade relationship with China, which has turned into an escalating

dispute over what the U.S claims are unfair trading policies regarding U.S. intellectual

property.

The U.S. was initially scheduled to increase existing tariffs on goods imported from China to

25% at the start of the year. In addition, the Trump administration threatened to broaden the

scope of the tariffs to potentially include all goods imported from China. However, President

Trump and President Xi Jinping of China met during the G-20 summit in Argentina at the

end of November and agreed to halt any escalation in the trade dispute until March while the

two sides try to come to an agreement on trade policies going forward.

The good news is that this gives the economy a bit more time before some of the more

painful tariffs kick in. As mentioned earlier, a broadening in scope of tariffs combined with

higher tariff rates would have a bigger impact on U.S. consumer and could damage

consumer confidence and cause a level shift in prices in 2019. Unfortunately, the agreement

reached during the G-20 did little in the way of actually solving any of the existing issues.

What this means is that the cloud of uncertainty that has lingered over the economy

throughout 2018 is going to remain an issue in 2019 as well. Businesses already appear to be

reluctant to make any big investment plans given the unresolved status of trade disputes,

and this trend will continue until some of these issues reach a conclusion.

In the fiscal arena, the partial shutdown of the government has thrown a surprising wrinkle

into the mix. President Trump and Congress were unable to reach an agreement to fully fund

the government by the December 21 deadline, leaving several key areas of government such

as the Department of Homeland Security and the Department of Transportation without

money at the end of the year.

Historically, government shutdowns are fairly short-lived. The government had already shut

down twice in 2018, with each shutdown lasting only a few days. The last significant

shutdown came in October of 2013, when President Obama and Congress argued over

funding for Obamacare. and shuttered the government for two weeks. GDP growth during

sonar.freightwaves.com

19Policy and Risks (cont.)

that quarter was noticeably impacted, with the shutdown subtracting approximately 25 basis

points from quarterly growth.

This current shutdown will likely be less painful on a week-to-week basis, because most

agencies have already secured funding through previous agreements. However, most signs

point to this shutdown being considerably longer than average. Congress is out of session

until January 3, and has made no plans to hold emergency sessions to resolve the shutdown.

In addition, the Trump administration has drawn a hard negotiating line over funding for the

border wall along the Mexico border, and will soon have to deal with an incoming House

where Republicans no longer hold the majority. If this shutdown drags on, the economic

impact could be much larger even if only part of the government is not operating.

In addition, questions have emerged over the future pace of monetary policy. The federal

Reserve increased interest rates for the fourth time this year in December The prevailing

feeling from the Federal Reserve for most of the year has been that there would be an

additional 3-4 hikes in the key federal funds interest rate next year, matching the pace seen

throughout 2018. However, the Federal Reserve has recently changed its tone, suggesting

that there will be a pause in rate increases next year. With inflation low, unemployment near

historical lows, and signs emerging that growth is slowing, the Fed may decide to hold off on

rate increases entirely.

It is worth noting that there is a considerable lag between when monetary policy is enacted

and when it actually takes hold on economic activity in the economy. What this means is that

the economy next year will be affected by the rate increases that were put into place

throughout 2018, particularly for the housing and automotive sectors. Even if there are not

further increases from this point, much of the impact on 2019 growth have already been put

into place.

sonar.freightwaves.com

20Freight Market Update

The November freight market recovered slightly after bottoming near the end of October.

Tender rejection rates increased slowly through the first couple of weeks before spiking near

the Thanksgiving holiday. Volume was a factor as the national tender volume index

(OTVI.USA) averaged approximately 1.5% higher than October during the month. There was

not a lot of volatility aside from the typical holiday disruption. As with October there was no

noticeable event that lead to national disruption.

sonar.freightwaves.com

21Even with volume increasing slightly over October, there was not enough to destabilize the

market like we saw in 2017. Last year the market was still reeling from the hurricanes and was

entering one of the biggest retail shipping seasons in the past five years. Even though total

volume was higher in 2018 there were numerous issues with imbalance as trucks had moved

to the gulf coast region for the recovery efforts.

The big story this year has been the tariffs and their impact to the economy and

subsequently freight market. Maritime shippers have been able to capitalize on increased

volume as the international shippers scrambled to pull inventory into the U.S. in order to buy

time to reorganize their supply chains. This activity has put increasing pressure on ports and

drayage carriers. A lot of the volume hits the largest port in the country in Los Angeles, but it

has overflowed to some of the eastern ports like Savannah.

November saw rates continue to increase for most of the month, but then took their first

significant downward turn in November for the first time since the summer. The volume

spilled into the freight market in November, fueling the L.A. markets with outbound freight.

sonar.freightwaves.com

22The Cass Freight Expenditure Index – an index that measures total freight spend including

intermodal and rail – fell for the second consecutive month, returning to a more normal

pattern after increasing during this time in 2017. After hitting record highs from May to

September, the index has dropped from a value of $2.99 to $2.85 in November. The drop is

another indication demand is weakening in relation to supply, and volatility is lower.

Along with signs of freight market slowing there is indication the capital expenditure side is

slowing as used truck prices for 3 (UT3.USA)and 4 year (UT4.USA) models contracted together

for the first time this year. The stimulus from the tax breaks and booming freight market

sonar.freightwaves.com

23revenue may be running low as orders are filled and signs of a slowing economy are visible.

There are still reports of backlogs from OEMs as there is about a 6-9 month cycle from order

to delivery, but it looks as though demand on the used truck end may have peaked.

The big story of the month was the continued volume coming out of Southern California.

After having a record month, both the port of Los Angeles and Long Beach cooled down –

L.A. loaded inbound volume down 8.8% and Long Beach up 0.2% YoY. This did not translate

to the outbound freight due to the delay of getting freight off the ship to a facility to prepare

for inland shipping. Some of the freight does get put straight onto the rail but a lot of it will

be brought to a transloading facility or stored until needed.

sonar.freightwaves.com

24Related to the inbound container volume, intermodal containers shipped on rail have been

steadily increasing since 2017 and hit the second highest weekly volume of all time the last

week of November – 271,198 containers. The biggest volume week occurred in late

September of this year at 272,955 containers.

With L.A. and intermodal dominating the freight market in November, tender rejection rates

increased 416 bps in the first two weeks. They hit the top on November 23rd, the day after

Thanksgiving, at 14.67% before starting to fall and ending the month at 8.54%. The

rollercoaster ride was the result of carriers moving off and on the coast as there was little

freight moving back into the market.

Aside from the abundance of port volume, reefer demand also played a big role in keeping

L.A. heated most of November. Reefer rejection rates hit summertime levels around

Thanksgiving as holiday demand fueled a lot of food product movement. Reefer rejection

rates topped 35% in late November – a level higher than all of May and most of June when

produce season in normally in full swing. With the main production areas for lettuce and

other Mediterranean crops moving south these rates subsided quickly by the end of the

month.

sonar.freightwaves.com

25Further up the coast in the Northwest tender rejection rates hit annual highs as the apple

harvest and Christmas trees moved out of the region. Oregon is the number one producer of

Christmas trees in the country and the week of Thanksgiving is the heaviest week on

average. The Outbound Tender Rejection Index for the Northwest region (OTRI.URNW)

reflected this with the index peaking at 27.96% after Thanksgiving.

The Northwest markets typically have more inbound than outbound loads -backhaul- but

trended the other direction this month. The Portland Headhaul Index (HAUL.PDX) hit its

highest value of the year of -10.52, an indication that outbound volume had increased

sonar.freightwaves.com

26significantly in relation to inbound volume. This is the time of year carriers can go into the

region and have a good chance at landing a load without deadheading long distances.

The rural Pendleton, OR (OTRI.PDT) and Twin Falls, ID (OTRI.TWF) markets hit their highest

rejection rate levels of the year in late November after trending up from August through

October. As mentioned, the late fall harvests had an impact on capacity, but this was

probably exacerbated by the rush of freight coming out of L.A. as trucks were occupied

deeper into the 4th quarter than usual.

sonar.freightwaves.com

27The extended port season had little impact on the rest of the U.S. as volume was relatively

low in other major markets. The Dallas market which is heavily tied to activity on the West

Coast did experience a boost of volume after declining steadily since the end of June.

Subsequently rates coming from L.A. to Dallas increased and topped their summer peak

level, hitting the annual high of $2.52/mile the day after Thanksgiving. This did not last long as

the rates swiftly recovered after peak demand to around $2.00/mile a week later.

The rates from L.A. to Seattle increased but not to the same extent as that had in relation to

the summer peak in years past. Thanksgiving rates are typically 13-17% lower than summer

peak levels. 2017 was an anomaly as the Thanksgiving rates were only 1.6% lower than the

sonar.freightwaves.com

28summer peak. This year we saw rates 22% lower than the late June peak. This is a function of

June being the hottest month for freight in over a decade and the general market cooling.

Rates were still up approximately 7.7% year-over-year.

The market remained relatively quiet on the east coast. Chicago was flat with a little hitch in

volume occurring around Thanksgiving. Volume took a quick dip in the Joliet market, where

several railheads are located, prior to the holiday and then jumped after the break as the L.A.

freight hit the market for the holiday rush. Capacity was plentiful as tender rejection rates fell

throughout the month, however.

sonar.freightwaves.com

29Further east Harrisburg, PA experienced declining volume but decreased capacity, save for

the days immediately preceding Thanksgiving. With carriers supplying the west coast this

left the northeastern corridors exposed to reduced capacity even as volume declined.

Volume dropped approximately 13% the first 16 days of the month then spiked 13% before

dropping 21% to finish the month well below where it started. Tender rejections also

recovered after the break.

Atlanta was relatively quiet in November along with most of the Southeast. Volume was

relatively falt but did take a few turns during the month. Capacity was not as available as it

had been leading into the holiday but moderated to close the month.

sonar.freightwaves.com

30The major port in the southeast is the port of Savannah. As the west coast ports were clogged

with freight, maritime shippers discounted rates to the east coast to help relieve some

pressure. This did not hold for long as rates and volume increased after the first week of

November. Outbound volume surged after Thanksgiving as well as freight was moved from

the port to regional distribution centers and cross dock facilities. Many major shippers like

Home Depot and Amazon have facilities nearby.

sonar.freightwaves.com

31Heading into the colder months weather becomes an increasing factor on day to day

movement. Unlike tropical storms the winter events tend to be short lived disruptors versus

the months it can take to recover from a hurricane. Aside from a few bigger systems that

moved across the upper Midwest and into the Northeast there was little major impact from

any significant weather event. The days leading up to Thanksgiving were very quiet in terms

of precipitation across the country.

Looking Ahead

Moving into December we have not observed too many large disruptions. November was a

far cry from the November of 2017 and so far, December is proving to be much different as

well. Is it a return to normal or just a brief respite? Economic conditions are smoothing, but

freight volume is higher than it was a year ago. The biggest difference seems to be the lack of

large disrupting event that throws the market out of balance. The heavy port volume may

have been a bit of a pulling forward of volume which may leave the winter months with less

to move. Although there is a surplus of freight sitting in warehouses that will move

eventually. It is just a matter of how much is needed and when.

sonar.freightwaves.com

32You can also read