ROYAL LONDON PENSION PROPERTY FUND (RLPPF) - February 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

ROYAL LONDON PENSION PROPERTY FUND (RLPPF)

February 2021

PROPERTY

BENEFITS IN A MULTI ASSET PORTFOLIO

Property provides the potential Property offers a hybrid Property is a

for a high income return investment return risk diversifier

UK commercial property: long-term performance

40

30

20

Rolling 12 month %

10 Yield Impact

0 Rental Value Growth

-10 Income Return

-20 Total Return

-30

-40

'88 '90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20

Multi-asset historic performance

12.0

Property (MSCI UK Monthly)

6.0

UK Gilts (FTSE A All Stocks Gilt)

0.0

Equities (UK FTSE All Share Index TR)

-6.0 Cash (IBA Libor 1w)

-12.0 Commodity (Bloomberg Commodity Index GBP)

1 Year 3 Years 5 Years 10 Years 15 years 20 years

Past performance is not a reliable indicator of future results. The views expressed are the author’s own and do not constitute investment

advice. Portfolio characteristics and holdings are subject to change without notice. This does not constitute an investment

recommendation. For information purposes only.

Source: MSCI Monthly Index as at December 2020. Source: MSCI UK Monthly Index, Bloomberg & ONS

1

PROPERTY

BENEFITS IN A MULTI ASSET PORTFOLIO

Property provides a partial hedge against inflation Property can be a less volatile investment

+/-

Rolling 12 month rates of income growth vs inflation Standard deviation

20

UK Gilts (FTSE A All Stocks Gilt)

5.4

15

10

Equities (UK FTSE All Share Index TR)

5 16.0

0

MSCI UK Monthly Index

-5

'90 '92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20 9.9

Gross Rent Passing Growth Annual rate of CPIH

Property attracts high

Property has a residual value Property is a real asset

transaction costs

The views expressed are the author’s own and do not constitute investment advice. Past performance is not a reliable indicator of future

results. Source: MSCI Monthly Index as at December 2020. Source: MSCI UK Monthly Index, Bloomberg & ONS

2

ATTRACTION OF UK ASSET CLASSES

LONG-TERM PROPERTY OUTPERFORMANCE VS. EQUITIES AND GILTS

UK Pull Factors UK Asset Class Performance, Total Return (Dec 1999 – Dec 2020)

Dec 1999 based to 100

500

450

400

350

Time Zone Legal System Language

300

250

200

150

Regulation Culture Diversity

100

50

0

MSCI UK Monthly Index UK Gilts (FTSE A All Stocks Gilt)

Skilled

Equities (UK FTSE All Share Index TR) Cash (IBA Libor 1W)

Liquidity Workforce Transparency

Commodity (Bloomberg Commodity Index GBP)

Past performance is not a reliable indicator of future results.

Source: MSCI Monthly Index, Bloomberg & ONS as at 31 December 2020

3

THE PROPERTY MARKET

IMPACT OF COVID

MARCH Rates of capital growth

2020 0.5

0.0

Investment -0.5

market -1.0

volumes -1.5

-2.0

-2.5

Material

Uncertainty

Clause Comparison of recent market downturns

0

Cumulative fall in value

-10

Fund -20

Suspensions

(%)

-30

-40

-50

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42

SEPT

2020 Nov 89 - May 93 GFC

Number of months

EU Referendum Nov 18 - Feb 20 COVID

Past performance is not a reliable indicator of future results.

Source: MSCI Monthly Index as at December 2020

4

THE PROPERTY MARKET

IMPACT OF COVID

UK and Eurozone prime office yields

8

7

6

5

4

3

Eurozone UK

UK Investment Volumes - purchaser by region (2020) UK Investment transactions by quarter 2020 (£mil)

Unknown 20,000

8%

15,000

£m

Foreign

10,000

Foreign Local

Local 52%

40% Unknown 5,000

0

Q1 Q2 Q3 Q4

Past performance is not a reliable indicator of future results.

Source: JLL, CBRE as at 31 December 2020

5

THE PROPERTY MARKET

ACCELERATION OF TRENDS

Sector returns over 2020

Retail

Growth in online 15

10

5

0 3.6

Industrial -5 -0.7

-3.9

Growth of -10 -6.3 -6.6

logistics -15 -6.6

-11.7

-20 -14.9

-25 -16.7

Office -30 -22.5

-26.6

Post COVID -35

occupation

Alternative

Lockdown

restrictions

Income Return Rental Value Growth Yield Impact Total Return Capital Growth

The views expressed are the author’s own and do not constitute investment advice. Past performance is not a reliable indicator of future

results.

Source: MSCI Monthly Index as at 31 December 2020

6

INVESTMENT

PHILOSOPHY

STRATEGY ASSET SELECTION

Rent £200m

c.£5.38bn

Value

ERV £252m

Stock selection to drive

outperformance

Invest with a Manage and

long-term horizon maximise income

136 Reversion

Investments of £52m

Focus on prime Actively identify asset 1043 +26% of

assets management opportunities

Tenants Current rent

Timing acquisitions /

Focus on larger disposals

assets

Projected

6.9 yrs

5 Year

WAULT

Returns

to expiry

ESG 7%

Portfolio characteristics and holdings are subject to change without notice. This does not constitute an investment recommendation.

For information purposes only, methodology available on request. Capital invested in the funds is at risk and there is no guarantee that

forecast returns or targets will be achieved over the 12 months rolling periods, or any other time period.

Source: RLAM as at 31 December 2020

Our investment strategy of focusing on prime assets for the long term is key to driving

outperformance

7

SCALE ENABLES OUTPERFORMANCE

LARGEST FUND IN THE ABI / MSCI MONTHLY INDEX

Rework into 4 tiles with icons

and move sub bullets into

smaller text

Lower concentration

Increased Lot Size

risk ratios

Active development Geographical focus

Portfolio characteristics and holdings are subject to change without notice. This does not constitute an investment recommendation. For

information purposes only.

Source: RLAM and MSCI as at 31 December 2020.

8

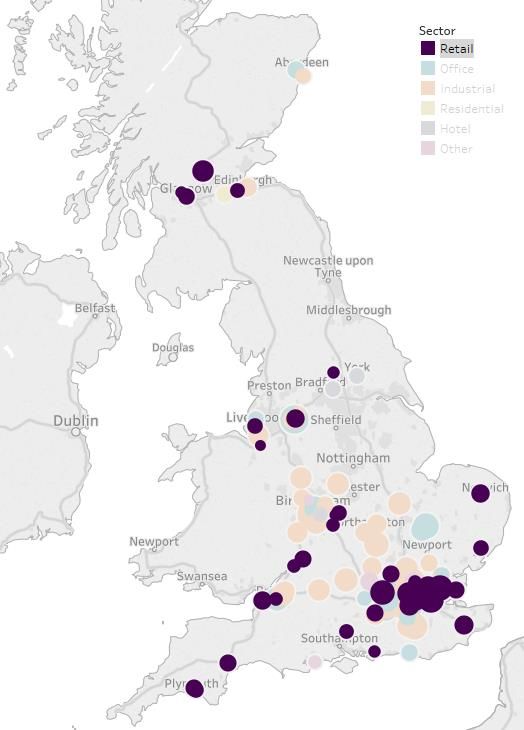

REGIONAL BREAKDOWN

PORTFOLIO

CV £4.5bn Central London

No. Assets 136 CV £1.0bn

Avg. Lot Size £33m CV % of Total 22%

No. Assets 18

Avg. Lot Size £55m

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: RLAM as at 31 December 2020

9REGIONAL BREAKDOWN

RETAIL ASSETS

CV £0.9bn

CV % of Total 20%

No. Assets 37

Avg. Lot Size £23m

Former Homebase, Weston Super Mare

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: RLAM as at 31 December 2020

10REGIONAL BREAKDOWN

OFFICE ASSETS

CV £1.4bn

CV % of Total 31.0%

No. Assets 35

Avg. Lot Size £40m

South East & Eastern

25 Soho Square

3 Hardman Square,

Manchester

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: RLAM as at 31 December 2020

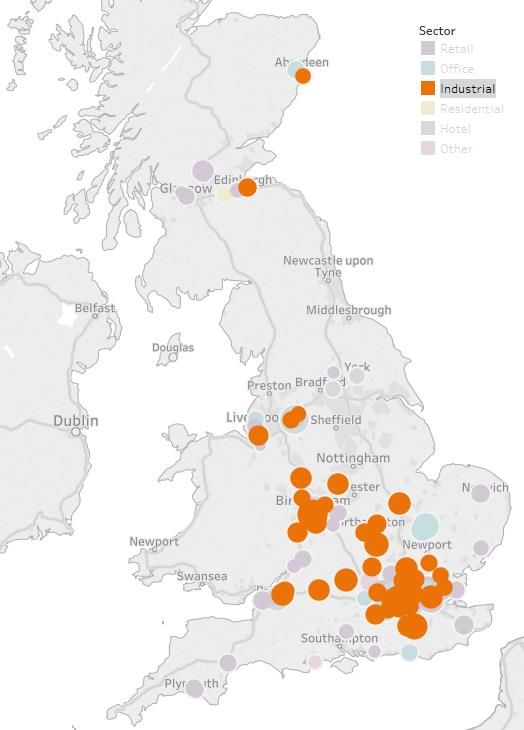

11REGIONAL BREAKDOWN

INDUSTRIAL ASSETS

CV £1.7bn

CV % of Total 39.3%

No. Assets 48

Avg. Lot Size £35.3m

Greater London

Kings Norton

Business Centre

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: RLAM as at 31 December 2020

12REGIONAL BREAKDOWN

ALTERNATIVE ASSETS

CV £0.4bn

CV % of Total 9.9%

No. Assets 13

Avg. Lot Size £32m

Capital Way, Colindale, London

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: RLAM as at 31 December 2020

13SECTOR BREAKDOWN

PROPERTY LEVEL

Sector weights MSCI Monthly Index Capital Growth by Sector

8.0%

20.0%

Retail

23.2%

3.0%

30.8% -2.0%

Office

30.7%

-7.0%

39.3%

Industrial

36.2% -12.0%

9.9% -17.0%

Other

9.9%

-22.0%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 1 Year 3 Years (p.a.) 5 Years (p.a.) 10 Years (p.a.)

CV

RLPPF MSCI UK Monthly Index Retail Office Industrial Other

Portfolio characteristics and holdings are subject to change without notice. This does not constitute an investment recommendation. For

information purposes only.

Source: RLAM and MSCI as at 31 December

The Fund is positioned to produce more resilient returns being overweight to Industrial

and underweight to Retail

14INCOME

QUALITY & MIX

Concentration of rent to tenants Top 20 tenants

Contracted Contracted

Tenant Name Rent £ Rent %

Kingfisher Plc (B&Q / Screwfix) 10,015,758 5.0%

Top 5 Top 10 Top 20 Rest J Sainsbury Plc 8,922,005 4.5%

16.8% 24.0% 33.8% 63.1% Whitbread Group Plc 6,692,301 3.3%

H&M Hennes Mauritz Ltd 4,661,146 2.3%

Gartner UK Limited 3,435,186 1.7%

Tesco Stores Ltd 3,243,154 1.6%

Industrial Property Investment Fund 2,976,742 1.5%

Iceland Foods Limited 2,723,893 1.4%

Portfolio is well let to tenants and tenant industries that Studio Retail Group Plc 2,678,420 1.3%

have fared well through COVID United Biscuits (UK) Limited 2,652,470 1.3%

MSCI Jaguar Land Rover Limited 2,402,400 1.2%

Credit Risk Portfolio Monthly Relative Risk Band Percentile DFS Furniture Ltd 2,229,713 1.1%

Index

Co-Operative Group (CWS) Ltd 2,115,007 1.1%

Weighted Credit Lower to Premier Oil UK 2,047,290 1.0%

71.74 68.6 3.1 82

Risk Score* Lowest Risk Next Group Plc 1,932,873 1.0%

Regatta Limited 1,898,538 0.9%

% Income in Lower to

10.1 13.8 -3.7 25 Wren Kitchens Limited 1,838,729 0.9%

High Risk Tenants Lowest Risk

Rochpion Properties Ltd 1,802,931 0.9%

% Income in Lower to Allies and Morrison LLP 1,739,539 0.9%

59.4 54.1 5.4 80

Low Risk Tenants* Lowest Risk The First Secretary of State 1,735,358 0.9%

Total 67,743,453 33.8%

* For this measure a higher percentile means a lower risk

Portfolio characteristics and holdings are subject to change without notice. This does not constitute an investment recommendation. For

information purposes only.

Source: Source: Top 20 tenants from RLAM as at 31 December 2020. Credit Risk scores from MSCI as at 30 September 2020

15INCOME SECURITY

PROPERTY LEVEL

Risk Eye

Fund quartiles from safest

(purple) to riskiest (orange)

71.7 6.9 yrs

v v Top

68.6 7.2 yrs Upper

Lower

Fund

Weighted Bottom

V Unexp’d

10.1% risk lease term 48.7%

Benchmark companies

v incl. v

Breaks Rent

13.8% 58.2%

High risk expiring

companies

CovenantINCOME

EXPIRY PROFILE & CURRENT VOID

RLPPF MSCI UK Monthly Index

9.1% 9.0% Vacancy Rate

6.9 yrs 7.2 yrs WAULT

(including breaks)

54.9% 58.2% Rent Expiry

(INCOME

REVERSIONARY POTENTIAL

MSCI Monthly

RLPPF

Index

3.6% 2.8% Development

Exposure

Potential

5.5% 7.8% Gain/Loss to lease

(net under/over

renting %)

-6.5% -7.8% % Overrent

Space, Woking

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: MSCI as at 30 September 2020.

18DEVELOPMENT EXAMPLES

Amazon Distribution Unit,

Redditch

• 360,873 sq. ft. distribution unit

• 15 years let to Amazon

Statesman House,

Maidenhead

• New 114,000sq ft. office

• Elizabeth Line

Past performance is not a reliable indicator of future results. Portfolio characteristics and holdings are subject to change without notice.

This does not constitute an investment recommendation. For information purposes only.

Source: MSCI as at 31 December 2020.

19IMPACT OF COVID

INCOME

99%

Vacancy rate - Standing Investments

12.0

Average collection rate

9.1

10.0

82% 8.0

8.7

COVID average

collection rate

6.0

4.0

2.0

0.0

3%

Proportion of CVAs/Administration/liquidation

The views expressed are the author’s own and do not constitute investment advice. Past performance is not a reliable indicator of future

results.

Source: RLAM as at 31 December 2020

20PORTFOLIO

PERFORMANCE

Periods to 31 December 2020

8.0%

6.0% 5.4%

4.0%

4.0%

Total return (%)

2.3%

2.0% 1.1% 1.2%

0.0%

-0.4%

-2.0%

-2.8%

-4.0%

-4.4%

-6.0%

1 Year 3 Years (p.a.) 5 Years (p.a.) 10 Years (p.a.)

RLPPF ABI UK - UK Direct Property-Pen

Past performance is not a reliable indicator of future results. The impact of fees or other charges including tax, where applicable, can be

material on the performance of your investment. The impact of fees reduces your return. The value of investments and the income from

them is not guaranteed and may go down as well as up and investors may not get back the amount originally invested.

Source: RLAM, ABI as at 31 December 2020.

Over all timescales the Fund has outperformed against the ABI Peer group.

21THE OUTLOOK

FUND STRATEGY

Industrials

Maintain Industrial weighting

Central London Offices

South East Offices

Increase weighting to Central London Offices

Rest of UK Offices

Reduce weighting to High Street Retail

Retail Warehouses

High Street Shops

Continue to actively asset manage and develop

Shopping Centres

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

RLPPF fund allocations (Percent of total portfolio)

Our market expectations (5 year annualised total return)

1RLAM forecasts - Winter 2020

2As at December 2020. RLPPF also has 9.7% of its overall portfolio allocated to the Alternative sector (Hotels, car showrooms, leisure and residential)

The views expressed are the author’s own and do not constitute investment advice. Past performance is not a reliable indicator of future

results.

22RESPONSIBLE PROPERTY INVESTMENT

HIGHLIGHTS

RPI Strategy

The funds have undertaken a major review of its RPI

strategy with the completion of a strategic framework and

action plan now at an advanced stage.

Net Zero Carbon pathway

The funds are nearing the completion of developing its net

zero carbon pathway. The delivery of this ambition will

require a number of targets and actions to be met, placing

greater emphasis on the ownership and operation of

energy efficient buildings, the adoption of renewable

energy technology, reducing the embodied carbon within

our developments, and offsetting.

Development

In 2020 a thorough review was undertaken of our

Development Sustainability Standards which has led to the

creation of a fresh set of targets which we consider are

both aspirational and market leading.

Source: MSCI as at 31 December 2020.

23RESPONSIBLE PROPERTY INVESTMENT

KEY ACHIEVEMENTS

Global Real Estate Sustainability United Nations Principles for Environmental Management System

Benchmark (GRESB) Responsible Investment (UNPRI) (EMS)

• RLPPF achieved a three star rating which is an • As a signatory to the UNPRI we have committed • The funds have achieved EMS 14001 which covers

improvement on last year’s rating of two stars, to reporting on our responsible investment the largest and highest impact commercial assets.

achieving 16th place of 59 within its peer group. activity year on year across all our asset classes. This helps to ensure compliance with relevant

• In 2020 the funds received an ‘A’ against a median environmental legislation and other

score of ‘B’. requirements.

Green Apple Awards Industry Working Groups and

Memberships

• In 2020 we received 8 Green Apple Awards for the • We are now active members participating and

two funds for a variety of biodiversity initiatives contributing to the Better Buildings Partnership

including the planting of wildflower areas, the (BBP), the UK Green Building Council (UK GBC),

installation of bug hotels and bee hives. the British Property Federation (BPF) and the

Investment Property Forum (IPF)

Sustainability Interest Group.

Source: MSCI as at 31 December 2020.

24RISK WARNING

IMPORTANT INFORMATION

For professional clients only. This document may not be distributed to any unauthorised persons and is not suitable for retail clients. The views expressed are the author’s own

and do not constitute investment advice.

This document is a financial promotion. It does not provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations.

Past performance is not a reliable indicator of future results. The value of investments and the income from them is not guaranteed and may go down as well as up and investors

may not get back the amount originally invested.

EPM Techniques: The Fund may engage in EPM techniques including holdings of derivative instruments. Whilst intended to reduce risk, the use of these instruments may

expose the Fund to increased price volatility.

Counterparty Risk: The insolvency of any institutions providing services such as safekeeping of assets or acting as counterparty to derivatives or other instruments, may expose

the Fund to financial loss.

Property Risk: The Fund invests in real property, the value of which is a matter of an independent valuer’s opinion and may not reflect the actual value realised upon its sale.

Investments in property are highly illiquid compared to equities or bonds and may be difficult to sell in a timely manner or at a reasonable price. Poor market conditions or times

of high investor redemptions may lead to difficulty dealing in the units of the Fund.

Investment Risk: The value of investments and any income from them may go down as well as up and is not guaranteed. Investors may not get back the amount invested.

For more information on the fund or the risks of investing, please refer to the fund factsheet, Prospectus or Key Investor Information Document (KIID), available via the Fund

Information page on www.rlam.co.uk

All confidential information relating to any Royal London Group company must be treated by you in the strictest confidence. It may only be used for the purposes of assessing

the proposal to engage Royal London Asset Management Limited (RLAM). Confidential information should not be disclosed to any third party and should only be disclosed to

those of your employees and professional advisers who are required to see such information for the purpose set out above. You should ensure that these persons are made

aware of the confidential nature of such information and treat it accordingly. You agree to return and/ or destroy all confidential information on receipt of our written request to

do so.

Issued by Royal London Asset Management Limited, 55 Gracechurch Street, London, EC3V 0RL Registration Number 141665 which is authorised and regulated by the

Financial Conduct Authority.

25For any queries or questions please contact:

Include key contacts here from

the Stephanie Hacking

UpSlide shape library

Fund Manager - Property

Royal London Asset Management Limited

55 Gracechurch Street

London

EC3V 0RL

T +44 (0) 20 3272 5098

stephanie.hacking@rlam.co.uk

All information is correct at January 2021 unless otherwise stated. Telephone calls may be recorded.

Issued by Royal London Asset Management Limited, Firm Registration Number: 141665, registered in England and Wales number 2244297; Royal London Unit Trust Managers Limited, Firm

Registration Number: 144037, registered in England and Wales number 2372439; RLUM Limited, Firm Registration Number: 144032, registered in England and Wales number 2369965. All of

these companies are authorised and regulated by the Financial Conduct Authority. Royal London Asset Management Bond Funds Plc, an umbrella company with segregated liability between

sub-funds, authorised and regulated by the Central Bank of Ireland,Insert disclaimer

registered fromRegistered office: 70 Sir John Rogerson’s Quay, Dublin 2, Ireland.

text364259.

in Ireland number

theSociety

All of these companies are subsidiaries of The Royal London Mutual Insurance UpSlide shape

Limited, library

registered in England and Wales number 99064. Registered Office: 55 Gracechurch Street,

London, EC3V 0RL. The Royal London Mutual Insurance Society Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the

Prudential Regulation Authority. The Royal London Mutual Insurance Society Limited is on the Financial Services Register, registration number 117672. Registered in England and Wales

number 99064.

Our ref: PR RLAM WNAR 0049 - 01/2021 - SB

ASSET MANAGEMENTYou can also read