Retail Sourcing Report - Facts & Insights - Q4 2020 - Newswire

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Q4

2020

Retail Sourcing Report

Facts & Insights

Sponsored By

1

FORWARD

RETAIL SOURCING REPORT

CBX Software’s Retail Sourcing Report provides

research and analysis aimed at informing global

sourcing and buying decisions for retailers, brands

and other sourcing and supply chain professionals.

Each issue includes a snapshot of key information and

trends impacting global sourcing, such as economic

conditions in sourcing countries, container shipping

trends, currency exchange and commodity rates. We

also cover hot topics ourselves and include insight

from analysts and other experts.

If you like this content, please share: The Number 1 Collaborative Sourcing

LinkedIn App for Retailers and Suppliers!

Americas +1.858.264.1133 www.tradebeyond.com

Asia +852.2378.6300

EMEA +49.89.9040.5110

www.cbxsoftware.com

Statement of Indemnity: CBX Software recommends that any information provided in this report be

weighed against other sources and experts on the individual topics covered. As such, CBX Software

bears no legal or fiscal responsibility for any potential harm or outcome which may result directly or

indirectly from information provided in this report.

2

CONTENT

RETAIL SOURCING REPORT 0

FORWARD 1

MANUFACTURING OUTLOOK (PMI) 3

LOW COST COUNTRY SOURCING (LCCS) HIGHLIGHTS 4

SOUTH EAST ASIA 4

SOUTH AND WEST ASIA 5

CHINA MINIMUM WAGE TRENDS 6

LOW-COST COUNTRY SOURCING WAGE TRENDS 7

CONTAINER FREIGHT RATES & TRENDS 8

TRADE CURRENCY RATES & TRENDS 9

GLOBAL COMMODITY RATES & TRENDS 10

CRUDE OIL 10

RUBBER 10

METALS 10

COTTON 11

PLASTICS AND SYNTHETIC FIBERS 11

QUALITY CONTROL INDICATORS 12

FOCUS TOPICS 13

COVID-19, E-COMMERCE ACCELERATOR 13

THE OUTLOOK FOR GLOBAL TRADE IN Q4 AND BEYOND 14

ABOUT CBX SOFTWARE & TRADEBEYOND 15

3 Purchasing Manager’s Index (PMI)

To help understand industry and economic conditions in a country, the PMI Index tracks variables such as

output, new orders, stock levels, employment and prices across private companies in the manufacturing,

construction, retail and service sectors. Over 30 countries and regions participate in various PMI surveys.

4

Manufacturing Outlook (PMI)

A reading below 50 indicates contraction from the previous month, while a reading above 50 indicates growth.

This update looks at a selection of emerging economies and key sourcing countries, providing indicators for

recent months based on data provided by IHS Markit, NIKKEI, CAIXIN and other sources.

To help understand industry and economic conditions in a country, the Purchasing Manager’s Index (PMI)

tracks variables such as output, new orders, stock levels, employment, and prices across private companies

in the manufacturing, construction, retail, and service sectors. A reading below 50 indicates contraction

from the previous month, while a reading above 50 indicates growth. While over 40 countries and economic

Q4 2020 News

regions and Analysis:

participate in various PMI surveys, this update looks at a short-list of emerging economies and key

sourcing countries to provide indicative trends. (Data Source: IHS Markit)

As businesses reopened and consumer demand picked-up following lockdowns and closures due to the

pandemic,

Q4 global manufacturing

2020 Summary: rebounded

As businesses throughand

reopened Q3consumer

and into Q4 as output,

demand exports

picked-up and new

following orders expanded

lockdowns and

to one of the highest levels since 2018. The upcoming Christmas season also pushed trade flow and stretched

closures due to the pandemic, global manufacturing rebounded through Q3 and into Q4 as output, exports

global supply chains still recovering from the impact of Covid-19. While input costs have reached record levels,

and new orders expanded to one of the highest levels since 2018. The upcoming Christmas season also

businesses felt more confident about the coming year. Overall the global trend was recovery and growth, with

pushed trade

some exceptions flowasand

such stretched

Mexico, global supply

Indonesia, chains

Malaysia andstill recovering

Myanmar, from economies

whose the impact of Covid-19.to

continued While

contract

under the impact of the pandemic. The economic picture for 2021 is still unclear, given the potentialthe

input costs have reached record levels, businesses felt more confident about the coming year. Overall of new

global

outbreaks trend

across was recovery

Europe and NorthandAmerica.

growth, with some exceptions such as Mexico, Indonesia, Malaysia and

Myanmar, whose economies continued to contract under the impact of the pandemic. The economic picture

for 2021 is still unclear, given the potential of new outbreaks across Europe and North America.

Jul Aug Sep

Country Summary of Indicators

2020 2020 2020

Brazilian manufacturing continued to recover at pace, supported by a weaker local

Brazil 58.2 64.7 64.9

currency; new orders, production and exports saw record growth, despite higher costs.

Chinese manufacturers maintained their robust growth momentum through Q3, with

China 52.8 53.1 53.0

new business growing at the fastest rate since 2011.

Columbia’s manufacturing economy continued to improve in Q3, despite easing off in

Columbia 54.2 51.2 50.4

September as quarantines eased, resulting in output growth and optimism for 2021.

Czech Manufacturing in Czechoslovakia continued to improve through Q3 as domestic and

47.0 49.1 50.7

Republic export orders and production increased, while competition pushed input costs lower.

India’s economy rebounded strongly through Q3, as factories ramped up production

India 46.0 52.0 56.8

and increased headcount to fill new orders, following 6 months of contraction.

Indonesia’s manufacturing had a setback in September following new outbreaks of

Indonesia 46.9 50.8 47.2

Covid-19, with new lockdowns limiting production, employment and purchasing.

Malaysia saw some pullback in manufacturing activity in late Q3 following an initial

Malaysia 50.0 49.3 49.0

rebound from the pandemic effect, with businesses confident for a stronger 2021.

Mexico’s manufacturing continued to feel the impact of Covid-19 through Q3 and into

Mexico 40.4 41.3 42.1

Q4 as many businesses remained closed, yet businesses confidence remains high.

Manufacturing came to a standstill in September after new lockdowns measures were

Myanmar 51.7 53.2 35.9

enforced, reducing output and headcount, making for an uncertain end to the year.

Despite easing off in Aug/Sept, Polish manufacturing improved marginally though Q3

Poland 52.8 50.6 50.8

reflecting growth in employment, despite weakness in output and new orders.

In line with other economies that saw a rebound in Q3, then a drop-off in September,

Russia 48.4 51.1 48.9

Russia’s production sector lost momentum into Q4 with uncertainty for the new year.

South Easing of South Africa’s lockdowns in Q3 resulted in growth in output, new orders,

44.9 45.3 49.4

Africa employment and purchasing, as companies attempted to recoup pandemic losses.

South Manufacturing in South Korea stabilized through Q3 as businesses reopened and

46.9 48.5 49.8

Korea output grew; ongoing recovery will depend on both domestic and foreign demand.

Turkey’s manufacturing sector saw a sustained recovery through Q3, with further

Turkey 56.9 54.3 52.8

gains in output and new orders, along with job creation and optimism for 2021.

Vietnam’s manufacturing economy picked up in September from the effects of

Vietnam 47.6 45.7 52.2

lockdowns in Q3, with output growth and stronger business confidence for 2021.

© 1995-2020 Copyright by CBX Software. All rights reserved.

Q4 2020 Retail Sourcing Report

Low Cost Country Sourcing (LCCS) Highlights 4

This section looks at selected issues impacting sourcing from key LCCS destinations based on data available at the

time of printing the report, alongside official import/export numbers highlighting global sourcing trends.

Summary: Asian economies continue to be heavily impacted by pandemic lockdowns, given they rely on trade with

each other as much as they do on consumer product exports to Western countries. Garment producing countries such

as Bangladesh and Cambodia continue to be hard hit by cancelled orders and factory shutdowns which have resulted

in mass unemployment and social unrest. The only Asian countries who are seeing growth, now and into 2020, are

China and Vietnam.

South-East Asia

Cambodia – Cambodia’s garment workers turned to the streets to protest the sudden loss of income due to Covid-19

factory related closures. Over 200 factories have closed, thousands of workers receiving dismissal notices and no

severance pay – in violation of labor laws. The garment sector in Cambodia employs over 800,000 people, mostly

women at an average wage of US$ 190/month ($1.30 an hour).

Indonesia – Indonesia is another country hit hard by the pandemic, with over 400,000 cases, leading to shutdowns and

mass unemployment. The Indonesian government passed a new law in October opening the door to labor intensive

manufacturing and foreign investment, aimed at creating jobs. Labor-intensive industry makes up less than 2% of

Indonesia’s GDP, much lower than other Asian countries.

Philippines – The Philippines continues to experience a severe fallout from the pandemic with the International

Monetary Fund (IMF) predicting a GDP contraction of 8.3% in 2020. To put it in context, Asian economies together are

projected to contract by 2.2%. This is the sharpest projected contraction among South-East Asian countries. As of mid-

October, the Philippines had almost 350,000 COVID-19 cases.

Thailand – In mid-October, Thailand’s new central bank governor predicted that the country’s economic recovery is

expected to take at least 2 years to reach pre-pandemic levels. He warned that Thailand, South-East Asia’s second

largest economy, could contract by a record 7.8% in 2020, partly due to the heavy impact of tourism. Anti-government

protests are also reportedly limiting consumption and business confidence

Vietnam – Aside from China, Vietnam is one of the only Asian economies to report economic growth in Q3 and into the

busy Christmas and 2021 pre-Chinese New Year season. Vietnam’s GDP rose by 2.62% in Q3, with exports increasing

11%, partly due effective management of the pandemic through strict lockdowns allowing for rapid business

reopening. Vietnam also continues to benefit as manufacturers shift from China.

Q4 2020 Retail Sourcing Report

5

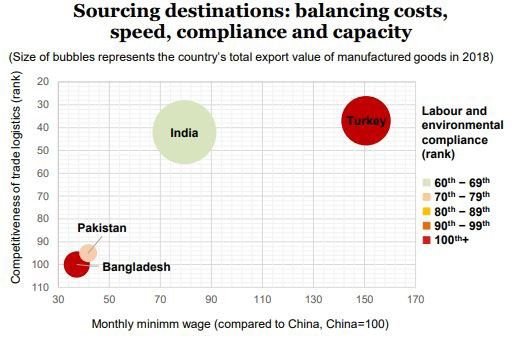

South and West Asia

Bangladesh – Manufacturing in Bangladesh continues to bear the impact of the pandemic, with order

cancellations and factory closures resulting in layoffs and tough times for garment workers living on already

sub-standard wages. According to the Bangladesh Garment Manufacturer’s and Exporters Association

(BGMEA), 1,150 factories have been impacted, with $3.18 billion in pandemic related order cancellations.

India – India continues to be hit hard by the pandemic with around 8 million cases and over 100,000 deaths

by mid-October. While average daily numbers are on the decline, India is still the worst affected country

after the US. Given the substantial number of potential cases in a population of 1.3 billion, the government

has enforced lockdowns to some extent, but is also trying to balance the economic fallout of halting the

economy.

Pakistan – Despite a relatively low-number of Covid-19 related deaths, Pakistan’s economy is still set to

contract through 2020. To stimulate their economy and create jobs, the Pakistani government is pushing

hard for the $6.8 billion, 2.655 ML-1 railway project, part of the China-Pakistan Economic Corridor that will

connect Karachi in the South to Peshawar in the North. This project will be 90% funded by Chinese loans.

Turkey – Turkey’s COVID-19 death toll reached 10,000 in mid-October with almost 370,000 cases, with new

lockdowns in place as the country fights off a second wave. While Turkish President Erdogan focused on

pushing a political agenda across the Muslim world, the Turkish economy went into a free-fall, with the lira

falling to record lows against the USD, inflation at 11.7% in Q3 and economic growth reached a 10-year low.

Sources: News Reports, Statistical Bureaus, Li & Fung Group (charts)

© 1995-2020 Copyright by CBX Software. All rights reserved.

China Minimum Wage Trends 6

Q4 2020 News & Analysis:

It is almost redundant to still look at individual Chinese provinces and regions for the purpose of finding an edge

in labor cost. For more than a decade the Chinese central government has pushed their economy away from

labor intensive industry towards higher value production and focused on growing domestic consumption versus

7 exports. Despite this policy exports grew strongly in Q3 and should continue to grow through Q2, 2022 assuming

the pandemic recovery trend continues.

China Minimum Wage Trends

Since 2005, the Chinese economy has grown from $2.3 trillion in GDP to $14.4 trillion in 2019, with average

annual income increasing by at a similar ratio from $1750 to over $10,000. As China’s leaders sit down for

Q4 2020 News & Analysis: It is almost redundant to still look at individual Chinese provinces and regions for the purpose of finding

their

an edge next

in laborfive-year plan,

cost. For more than we canthe

a decade beChinese

sure central

that government

similar policies

has pushed oftheir

managing growth

economy away will

from labor mean steadily increasing

intensive

minimum

industry towardswages across

higher value China’s

production provinces

and focused anddomestic

on growing regions. consumption versus exports. Despite this policy exports

grew strongly in Q3 and should continue to grow through Q2, 2022 assuming the pandemic recovery trend continues.

Since 2005, the Chinese economy has grown from $2.3 trillion in GDP to $14.4 trillion in 2019, with average annual income increasing

by at a similar ratio from $1750 to over $10,000. As China’s leaders sit down for their next five-year plan, we can be sure that similar

Note:ofThese

policies managing are official

growth wage

will mean guidelines

steadily mandated

increasing minimum by each

wages across China’sprovince

provinces andorregions.

region based on information publicly

available as of Oct 1, 2020. As such these numbers serve as an indicator. Actual wages

Note: These are official wage guidelines mandated by each province or region based on information publicly available as of Oct 1,

may include benefits,

food,

2020. Ashousing etc. Minimum

such these numbers serve as anwage isActual

indicator. typically

wages40-60%

may includeofbenefits,

average food,total wage.

housing etc. Minimum wage is typically

40-60% of average total wage.

2020 Minimum Wage Updates (official)

Monthly Min Avg Wage

City/Region/Province Increase % Official Update

(RMB)

Anhui 1,550 20.6% Nov 1, 2019

Beijing 2,200 3.8% Jul 1, 2019

Fujian 1,800 7.4% Jan 1, 2020

Chongqing 1,800 20.0% Jan 1, 2019

Gansu 1,620 10.2% Jun 1, 2019

Guangxi 1,680 16.7% Jan 1, 2020

Guangdong 2,200 12.3% Jul 1, 2019

Guizhou 1,790 6.6% Dec 1, 2019

Hainan 1,670 12.6% Feb 1, 2019

Heilongjiang 1,680 15.4% Oct 1, 2019

Henan 1,900 8.2% Oct 1, 2018

Hebei 1,900 14.8% Nov 1, 2019

Hubei 1,750 13.1% Nov 1, 2019

Hunan 1,700 13.6% Oct 1, 2019

Inner Mongolia 1,760 8.0% Aug 1, 2019

Jiangsu 2,020 8.1% Aug 1, 2018

Jiangxi 1,680 15.1% Jan 1, 2019

Jilin 1,780 22.5% Oct 1, 2019

Liaoning 1,810 7.6% Nov 1, 2019

Ningxia 1,660 12.4% Jan 1, 2019

Qinghai 1,700 15.2% Jan 1, 2020

Shaanxi 1,800 7.0% May 1, 2019

Shandong 1,910 6.7% Jun 1, 2018

Shanghai 2,480 2.5% Apr 1, 2019

Shenzhen 2,200 4.9% Jul 1, 2018

Sichuan 1,780 7.1% Jul 1, 2019

Tianjin 2,050 5.1% Jul 1, 2019

Tibet 1,650 17.8% Jan 1, 2019

Xinjiang Uyghur 1,820 12.9% Jan 1, 2019

Yunnan 1,670 10.6% May 1, 2019

Zhejiang 2,010 8.4% Jan 1, 2019

Q4 2020 Retail Sourcing Report

© 1995-2020 Copyright by CBX Software. All rights reserved.

7 Low-Cost Country Sourcing Wage Trends

Below is a snapshot of minimum wages in selected Asian sourcing locations, with the addition of Egypt,

Ethiopia, and Turkey to give a comparative view. Wages vary by region or province and indicate either

an estimated or actual/official rate. In cases with a distinct variance, we provide an average.8 Currency

fluctuations mean that these figures are approximate at the time of finalizing this report.

Low-Cost Country Sourcing Wage Trends

Below is a snapshot of minimum wages in selected Asian sourcing locations, with the addition of Egypt,

Q4 2020 News & Analysis:

Ethiopia, and Turkey to give a comparative view. Wages vary by region or province and indicate either an

estimated or actual/official rate. In cases with a distinct variance, we provide an average. Currency

With no clear horizon for the end of COVID-19, there is little cause for optimism on the labor front in low cost

fluctuations mean that these figures are approximate at the time of finalizing this report.

sourcing countries, in some cases the gains in compliance and the movement towards a living wage might

be going backwards. While Bangladesh approved a wage increase for leather goods and footwear workers,

Q4 2020 News & Analysis: With no clear horizon for the end of COVID-19, there is little cause for optimism

the first for them since 2013, Indonesia is pushing ahead with a controversial Omnibus Bill aimed at relaxing

on the labor front in low cost sourcing countries, in some cases the gains in compliance and the movement

business, labor, and environmental laws to encourage foreign investment and create more labor-intensive jobs

towards a living wage might be going backwards. While Bangladesh approved a wage increase for leather

with minimum wages set by regional governors. Similarly, workers in low-cost countries such as Cambodia and

goods and footwear workers, the first for them since 2013, Indonesia is pushing ahead with a controversial

Myanmar face an uncertain future until the pandemic ends.

Omnibus Bill aimed at relaxing business, labor, and environmental laws to encourage foreign investment and

create more labor-intensive jobs with minimum wages set by regional governors. Similarly, workers in low-

cost countries such as Cambodia and Myanmar face an uncertain future until the pandemic ends.

Note: Figures are provided in USD/month based on currency exchange as of Oct 1, 2020. Minimum wage

Note: Figures are provided in USD/month based on currency exchange as of Oct 1, 2020. Minimum wage

policies are updated as per data available at the time of finalizing this report and are based primarily on

policies

unskilledarewages.

updatedConsult

as per data available

sources suchatastheFair

timeWage

of finalizing

Guide this report and are based

or Wageindicator.org toprimarily

assess onand calculate

unskilled wages. Consult sources such as Fair Wage Guide or Wageindicator.org

benchmarks for wages in particular countries and regions not covered here. to assess and calculate

benchmarks for wages in particular countries and regions not covered here.

BANGLADESH CAMBODIA CHINA EGYPT ETHIOPIA

$95 (Sep 2020) $190 (Jan 1, 2020) $163-$359 (Jan 2020) $116 (April 2019) $26 (Jan 2015)

As of September 2020, Cambodia announced Minimum wages in Egypt raised their Ethiopia is still

the Bangladesh an increase to their China are set by local minimum age to 2000 working on a system

Ministry of Labor and minimum wage from governments and have Egyptian pounds ($116) to determine a

Employment approved US$182, to $190 a varying wage formulas from 1200 pounds, minimum wage for the

a 94% minimum wage 4.4% increase, to take (with housing, food, applying to all workers, private sector. Entry

increase for leather effect from January 1, overtime etc.) with higher increases level wages in the

goods and footwear 2020. Political and Actual 2020 wages for going to the private textile sector range

workers from 3,652 labor tension manufacturing jobs in sector. This increase from $35 to $40. The

taka (2013) to 7,100 continues as China are much higher came ahead of a June base minimum wage

taka (US $85). opposition push for at US$870/month 30, 3029 target date. is officially

more rights and pay. $18/month.

INDIA INDONESIA LAO PDR MALAYSIA MYANMAR

$94-$236 (Oct 2020) $120-$298 (Oct 2020) $124 (May 2018) $270-$295 (Jan 2019) $80 (Mar 2018)

The Indian Parliament As of Q4 2020, The Lao Government Malaysia implemented Myanmar revised its

is in the process of Indonesia is working to approved an increase a nationwide minimum minimum wage from

reforming labor finalize a controversial in minimum wage from wage of RM 1,100 as of K600 ($2.70) per day

policies. By September Omnibus Bill focused Kip 900,000 (US$107) January 2019. Wages to K4,800 (3.60) or

of 2020 3 of 4 labor on creating jobs in to Kip 1,100,000 vary by region and are K600/ hour for an

bills passed through labor heavy industries, (US$142)) in key supposed to be eight-hour workday in

and await final to create jobs and provinces which took reviewed every 2 years. 2018. This is increase

approval from the incentivize foreign effect in May 2018. The new directive is of 33%, mostly affects

Indian President. investors. being enforced widely. garment workers.

PHILLIPPINES SRI LANKA THAILAND TURKEY VIETNAM

$132-$190 (Jan 18) $67 (Mar 2016) $248-$265 (Apr 1/18) $482 (Jan 2020) $132-190 (Jan 1/19)

Wages in the Sri Lanka adopted two Thailand is in the To combat inflation of Vietnam announced

Philippines vary by laws on minimum process of updating close to 12%, Turkey they will increase their

region, skill level and wages as of early their minimum wage announced a minimum minimum wage by

wage classification. 2016, mandating a from a current wage increase of 15%, 5.3% in 2019. This

Negotiations are still minimum wage of Rs minimum of 308 – 330 effective Jan 1, 2020 to increase was relatively

underway, but Manila 10,000 (+/- $67) and Baht per day to a 2,324 liras/month lower than the 2018

for example saw a 21 an increase of Rs proposed 400 Baht per (US$381) net. This increase of 6.5%.

Peso ($0.42) increase 2,500 (+/-f$17) for day. Most businesses brings the gross Wages range from

in their daily wage to workers earning less are opposed to this minimum wage (before $125-$180 / month

491 Pesos ($9.82) in than Rs 40,000 per higher wage as being deductions) to 2,943 across 4 key regions

Q4 2017. month (+/- $270) too high. liras/month (US$482). in Vietnam.

Sources: WageIndicator.org, SAFSA, Local News Reports

Q4 2020 Retail Sourcing Report

© 1995-2020 Copyright by CBX Software. All rights reserved.

Container Freight Rates & Trends 8

Q4 2020 News and Analysis:

While spot rates on major East-West shipping routes have climbed higher through Q2 and Q3, carrier service

levels and on-time arrivals of container ships has plummeted. Through late Q3, carrier reliability was below 50%

on shipments from Asia to US East and West Coasts and down 69% for Asia-North Europe. Container ships were

on average five days late in September, according to Sea-Intelligence Maritime Analysis. Carriers have continued

to reduce capacity through the pandemic, which has kept prices high but left importers frustrated. Importers are

also dealing with port congestion and unpredictability in inventory forecasting and replenishment. With concern

over a second wave of Covid-19 and economic and political uncertainty in the US and Europe, container shipping

rates and service are unlikely to improve until well into 2021, if at all.

Asia - North Europe Trade Lanes

Asia-North Europe container shipping rates have

continued to increase through 2020, based on limited

capacity and strong demand, especially following

pandemic shut-downs and approaching the busy

Christmas and pre-Chinese New Year season.

Container shipping rates are expected to remain high

given that carriers are carefully managing capacity

below the level of demand to protect their interests.

According to Sea-Intelligence, shipping volumes on

Asia – North Europe routes were up 2% year-on-year in

July to 1.5 million TEU.

Asia – North America Trade Lanes

Both East and West coast US spot container shipping

rates reached annual highs in Q3 and continue to climb

into Q4. Similar to Asia-North Europe lanes, carriers

cut capacity by blanking sailings from Asia to North

America during the first half of 2020 (the pandemic),

but as demand increased, they have not reintroduced

sufficient capacity.

Heading into the peak Chr istm as seaso n and

subsequent peak pre-Chinese New Year period, the

current trend in shipping rates/capacity is most likely to

continue. Reports show that consumer goods spending

is up dramatically, driven by e-commerce growth and by

consumer’s shifting spend from services to goods such

as furniture, home office, exercise and other products

which should continue to drive demand for shipping.

Sources: IHS Markit, Joc.com, Alphaliner, SeaIntel

Q4 2020 Retail Sourcing Report

9 Trading Currency Rates & Trends

Following are exchange rates and indicators for major currencies commonly factored into global sourcing

costing estimations. The fallout from Covid-19 has extended to foreign exchange with many investors selling

currencies in countries that are hard hit with the virus and placing their assets in safe-haven currencies

– especially the US dollar. The dollar is likely to hold11 strong since there are few alternatives, given the

Euro’s limited role as a reserve currency and the fact that the Chinese Renminbi is still tightly controlled.

11

11Trading Currency Rates & Trends

Currency volatility continues to impact purchasing, resulted in higher costs and threatening margins. Other

factors driving volatility are the upcoming US election, uncertainty over future stimulus packages, the Brexit

Tradingongoing

negotiation, Currency Rates

uncertainty & Trends

with US/China trade andFollowing

the potential resurgence of Covid-19

indicatorsthis Winter.

Trading Currency Rates & Trends

are exchange rates and for major currencies comm

costing estimations. The fallout from Covid-19 has extended to foreign ex

Following are exchange rates and indicators for major currencies commonly factored into global sourcing

currencies in countries that are hard hit with the virus and placing their

costing estimations. The fallout from Covid-19 has extended to foreign exchange

Following areUS with manyrates

exchange investors

and isselling

indicators for major currencies comm

especially the dollar. The dollar likely to hold strong since there are

CBX Software

currencies helps

in countries that you

are hard hit stay

with theup toand

virus date with

placing theirchanging

costing

limited

assets

estimations.

role as a reserve trading

in safe-haven currencies

Thecurrency

fallout from –

and Covid-19 has the

the fact that extended

Chineseto foreign

Renminb e

especially the US dollar. The dollar is likely to hold strong since there are fewinalternatives,

currencies countries given

that arethe

hardEuro’s

hit Learn

with More

the virus and placing thei

policies

limited role as and new

a reserve tariffs

currency andrule with

the fact our

that the AI sourcing

Chinese Renminbi solution.

volatility

especially

continues to impact purchasing, resulted in higher costs and t

is still

the UStightly controlled.

dollar. Currency

driving volatility are the The dollar

upcoming isUS likely to holduncertainty

election, strong since there

over a

futu

volatility continues to impact purchasing, resulted in higher costslimited

and threatening

role as a margins.

reserve Other and

currency factors the fact that

negotiation, ongoing uncertainty with US/China tradethe Chinese

and Renminb

the potential re

driving volatility are the upcoming US election, uncertainty over futurecontinues

volatility stimulus to packages, the Brexit resulted in higher costs and

impact purchasing,

negotiation, ongoing uncertainty with US/China trade and the potential drivingresurgence

volatility of

areCovid-19 this Winter.

EUR / USD (Oct 2019 –the

Octupcoming

2020) US election, uncertainty over fut

negotiation, ongoing uncertainty with US/China trade and the potential r

EUR / USD (Oct 2019 – Oct 2020) EUR/USD Low High

EUR / USD (Oct 2019 – Oct 2020)

2 year 1.06 1.94

1 year 1.06 1.19

1 month 1.16 1.87

T

U

The Euro appreciated against the th

USD through Q3 on optimism over wT

the European economy but flattened wU

with fears of a second COVID-19 et

wave. The EUR/USD pair is 1w

expected to trade in the range of thw

1.17 until 2021. Assuming stability in the

the US and Covid-19 containment, 1

EUR

The/ Chinese

CNY (Julycould

the Euro 2019reach

Yuan – July

made 2020)

1.20 nextagainst

gains year. the Euro t

EUR / CNY (July 2019 – July 2020) through Q3, weakening into Q4. Chinese government t

EUR/CNY

CNY (July 2019 – Low

July 2020) High

officials have warned of risks of CNY fluctuation in

EUR /

both directions

2 year through 2021. Most

7.49 8.31predictions are

that the Chinese currency

1 year 7.55 will continue

8.31 to appreciate

against both the Euro7.83

1 month and the USD.

8.01

T

a

The Chinese Yuan made gains w

against the Euro through Q3, gT

weakening into Q4. Chinese ria

government officials have warned of dw

risks of CNY fluctuation in both pg

directions through 2021. Most cur

predictions are that the Chinese ad

USD / currency

CNY (Julywill

2019continue to appreciate

– July 2020) p

against both the Euro and the USD. c

USD / CNY (July 2019 – July 2020) a

The Chinese Yuan appreciated against the USD USD / CNY (July 2019 –Low

USD/CNY July 2020) High

through Q3 to 2018 levels, after plunging to

2008 lows in Q1 early this year. Drivers for Yuan 2 year 6.64 7.17

appreciation are a fast recovery in the domestic 1 year 6.64 7.16

economy and ongoing strength in exports. Volatility 1 month 6.64 6.82 T

is expected to continue through Q4 and into 2020 The Chinese Yuan appreciated

a

based on the US election outcome and COVID-19 le

against the USD through Q3 to 2018 QT

containment. levels, after plunging to 2008 lows in aa

Q1 early this year. Drivers for Yuan dl

appreciation are a fast recovery in the stQ

domestic economy and ongoing ea

strength in exports. Volatility is ind

Sources: XE.com, News/Analyst Reports

expected to continue through Q4 and os

Sources: XE.com, News/Analyst Reports into 2020 based on the US election e

outcome

© 1995-2020

Sources: and COVID-19

Copyright

XE.com, containment.

by CBX Software.

News/Analyst All rights reserved.

Reports i

© 1995-2020 Copyright by CBX Software. All rights reserved. Sources: XE.com, News/Analyst Reports o

© 1995-2020 Copyright by CBX Software. All rights reserved.

© 1995-2020 Copyright by CBX Software. All rights reserved.Global Commodity Rates & Trends 10

12

Global Commodity Rates & Trends

Q4 2020 News and Analysis:

Q4 2020 News & Analysis: Almost all commodity prices recovered in the third quarter of 2020 following

Almost all commodity prices recovered in the third quarter of 2020 following steep declines earlier in the

steep declines earlier in the year due to the COVID-19 pandemic. Following a strong summer rebound, as

year due to the COVID-19 pandemic. Following a strong summer rebound, as lockdowns lifted, momentum in

lockdowns

commodity lifted,prices

momentum in commodity

has stalled in recentprices

weekshasasstalled

second in recent

wavesweeks

of theas second waves

pandemic of the

and economic uncertainty

pandemic and economic uncertainty continued. A levelling off in demand is coinciding with limited supply

continued. A levelling off in demand is coinciding with limited supply suggesting that commodity prices face

suggesting

an uphillthat commodity

battle. prices

Oil prices, facetend

which an uphill battle.

to lead mostOil prices, which prices

commodity tend toin

lead mostdirection,

either commodity areprices

likely to have a slow

in either direction, are likely to have a slow recovery into 2021. The forecast for

recovery into 2021. The forecast for commodities depends on geopolitical factors such as thecommodities depends on outcome of the

geopolitical

US election, the ongoing Brexit scenario and how long it takes for a COVID-19 vaccine to roll-out.it

factors such as the outcome of the US election, the ongoing Brexit scenario and how long

takes for a COVID-19 vaccine to roll-out.

Crude Oil

Crude Oil Crude oil prices have doubled

since their April low, supported

70

70 Oil US$ per barrel Crude oil prices have doubled since their

65 Dated by sharp supply cuts by OPEC.

65 Dated April low, supported by sharp supply cuts

60

60 Brent,light

Brent,light However, prices remain a third

55

55

blend 38

blend 38 by OPEC. than

lower However, prices remain a third

pre-pandemic

API

50 API

lower

50

45

45

levels.than pre-pandemic

Oil prices levels. Oil prices

are expected

40

40

Dubai,mediu

Dubai,mediu

m, fob

fob

are expected

to increase to increase

gradually gradually

in 2021 as in

m,

35

35 Dubai Fateh

Dubai Fateh demand

2021 is matched

as demand by an

is matched by an easing

30

30

25

25

32 API

32 API easing

of supply. of supply. The

20

20 West Texas

West Texas pandemic could have lasting

15

15 Intermedia

Intermedia effects on oil demand though

10

10 40 API,

API, The pandemic could have lasting effects

40 as changes in consumer

Midland

Midland on oil demand though as changes in

Texas

Texas behavior influence demand.

consumer behavior influence demand.

Rubber

Rubber Natural rubber prices have

soared through the pandemic

Rubber, No. 3 Smoked Sheet (RSS3), Singapore Natural

partly onrubber

strong prices

demand have soared

for PPE

Exchange through

such as the pandemic

protective partlyOn

gloves. on strong

2.0

2.0 Price in US cents per kilogram demand

the supplyfor PPE suchpandemic

side, as protective

related On

gloves. labor shortages

the supply side, and

pandemic

1.8

1.8 weatherlabor

issues in Thailand

1.6

related shortages andandweather

1.6 Vietnamin (key producers) have (key

issues Thailand and Vietnam

1.4

1.4 resulted in reductions in rubber

producers) havefactors

production. Key resulted in reductions in

in rubber

1.2

1.2 rubber

price volatility into 2021 include in rubber

production. Key factors

1.0

1.0 price volatility into 2021

COVID-19 recovery, US include

China COVID-19

recovery, US China

trade tension and the trade tension and the

American

13 American election outcome.

election outcome.

Metals

Metal

Despite the steepest global

Metals US$ per metric ton economic

Despite contraction

the steepest in recent

global economic

20000

history,

contraction base metal

in recent prices

history, have

base metal

18000

16000 3000 pricessurged well well

have surged above

abovetheir

their pre-

pre-

14000 pandemic

pandemic levels.levels. Key drivers

Key drivers are

are Chinese

12000 2442 Chinese stimulus measures

stimulus measures and the pandemic and

2000

10000 thewhich

recovery pandemic recovery

has fueled which

an industrial

8000 1873

6000 and manufacturing rebound. Going and

has fueled an industrial

1000 manufacturing rebound. Going

4000 forward, waning stimulus measures and

2000 124

forward, waning stimulus

the potential of over-supply might impact

0 0 measures and the potential of

pricing. Metals are expected to see a

over-supply might impact pricing.

modest gain in prices in the range of 2%

Metals are expected to see a

for 2021.

Tin Aluminum Copper Nickel

modest gain in prices in the

Zinc Lead Iron range of 2% for 2021.

Q4 2020 Retail Sourcing Report

Cotton

Q4 2020 Retail

Latest reports indicate a decrease in global cotton production Sourcing

(-934,000 bales toReport

116.3 million) along

with an increase in global mill-use (+1.5 million bales to 114.2 million) through Q3/Q4. This has led to

2.7 million bale reduction for 2020/2021 forecasts, which still leaves stockpiles at the one of the highest12000 20002000 Chineselevels.

pandemic

Chinese stimulus

stimulus Key measures

drivers

measures are and

and

10000 12000

10000

14000

10000

2442

2000

2000

the pandemic

the

the pandemic

pandemic recovery

recovery

recovery whichwhich

which

10000

12000

80008000 18732442

1873 Chinese

has the

hasfueled stimulus

pandemic

fueled an an measures

recovery

industrial

industrial and

which

and and

8000 1873

2000 has fueled an an industrial

industrial and

10000

8000

60006000 1873

10001000 the

has pandemic

fueled recovery whichand

6000

8000

6000

40004000 1000

1873 manufacturing

manufacturing

manufacturing rebound.

rebound.

rebound. GoingGoing

Going

4000 1000 has fueled an industrial

manufacturing rebound. and

Going

6000

4000

20002000 1241000

forward,

forward, waning

forward, waning

waning stimulus

stimulus

stimulus

2000 124

124 manufacturing

forward, rebound. Going

waning stimulus

4000

0 2000

0 0 0 0 124 measures

measures

measures and and

andthe the potential

the potential

potential of of

ofof

Cotton

0 forward,

measuresmight waning

and theimpactstimulus

potential

11 2000

0

0 0

0

124

over-supply

over-supply

over-supply

measures

over-supply and might

mightimpact

the

might

pricing.

impact

potential

impact

pricing.

pricing.

of

pricing.

Metals

Metalsareare

Metals expected

are expected

expected to pricing.

see

to see a aa

over-supply

Metals

modest are

gain

might impact

inexpected

prices toto see

see a

Tin TinTin Aluminum

Aluminum Copper

Copper Nickel

Nickel

modest

Metals

modest

modest

gain

aregain

expected

gain in

inin pricesto in

prices

prices see the

in

in

the

inathethe

Aluminum Copper Nickel

Tin

Zinc Zinc

Zinc

Aluminum

LeadLead

Lead

Copper

Iron Iron

Iron

Nickel range

modestof

range

rangeof2%

of for

2%

gain

of2%2%in 2021.

for 2021.

prices

2021. in the

for2021.

Tin

Zinc Aluminum

Lead Copper

Iron Nickel range for

Zinc Lead Iron range of 2% for 2021.

Cotton Latest reports indicate a decrease in global cotton production (-934,000 bales to 116.3 million) along with

Cotton

Cotton

Cotton

Cotton

an increase in global mill-use (+1.5 million bales to 114.2 million) through Q3/Q4. This has led to 2.7 million

Latest reports

Latest

bale

Latest reportsindicate

reduction

reports indicate

reports indicate

a for

decrease

a adecrease

a2020/2021

in global

decrease cotton

ininglobal

forecasts,

global production

cotton

cotton production

which

production (-934,000

(-934,000

still bales

leaves

(-934,000

(-934,000

balesto 116.3

toto116.3

stockpiles

bales

bales 116.3million)

million)

at the

million) alongalong

onealong of the highest on record.

Latest

withwith

anLatest

with an reports

increase

an increase in

increase

indicate

indicate

global

ininglobal

global

decrease in

a decrease

mill-use

mill-use

mill-use in

(+1.5

global

global

million

(+1.5

(+1.5

cotton

cotton

bales

million

million

production

production

to

bales

bales 114.2

to to114.2 (-934,000

million)

114.2 million) bales

through

million) toto

through

through

116.3

116.3

Q3/Q4Q3/Q4

Q3/Q4.

million)

million)

This

. . has

This

This

along

along

led

has

has to

led to

ledtoto

2.7 2.7

Both

with

with

million

an China

bale

million

increase

an increase and

reduction

bale

in

reduction

India

global

in global

for for

reported

mill-use

mill-use

2020/2021

2020/2021 (+1.5higher

(+1.5 million

million

forecasts,

forecasts,

than

bales

bales

which

predicted

to

tostill

still

which

114.2

114.2

leaves

mill-use

million)

million)

stockpiles

through

through and

at the Q3/Q4 China

Q3/Q4

one

.

. This

of the

imported

Thishashasled

highest to more than forecast.

led

2.7

2.7 million

million bale

bale reduction

reduction for

for 2020/2021

2020/2021 forecasts,

forecasts, which

which stillleaves

still leaves

leaves stockpiles

stockpiles

stockpiles at

at

at the one

theone

the one of

of the

ofthe highest

thehighest

highest

Prices

onon2.7

on record. million

record.

on Both

record. have

Bothbale

China

Both increase

reduction

Chinaandand

China India for

andIndia

and steadily

2020/2021

reported

India reported

reported since

higher

higherpandemic

forecasts,

higher than which

predicted

than

than predicted

predicted induced

still leaves

mill-use

mill-use and

mill-use lows

stockpiles

China

and

and inatimported

China

China early

the oneApril

imported

imported

of

morethe and

morehighest

than

more have held steady partly due to

than

than

onrecord.

record. Both

Both China

China and India

India reported

reported higher

higher than

than predicted

predicted mill-use

mill-use andand China

China imported

imported moremore than

than

Hurricane

forecast.

forecast.Prices

forecast.

forecast.

forecast.

Prices

PricesDelta

have

Prices

Prices

have

have

have

have

which

increase

increase

increase impacted

steadily

steadilysince

steadily

increase steadily

increase steadilysince the

pandemic

since

since US

pandemic

pandemic

sincepandemic cotton

induced

induced

pandemicinduced inducedbelt.

lows

inducedlows lowsin

lowsWhile

early

in

in indicators

April

early

early

lowsininearly and

April

April

earlyApril

April have

and

and

and are

haveheld

have

have that

steady

held

held

held cotton

steady

steady

steady prices should continue

partly due

partly

partly

to todue

due

rise

partly dueHurricane

to Hurricane

to

into

to 2021, Delta

Hurricane

Hurricane Deltawhich

Delta

volatility

Delta impacted

which

which

which impacted the

impacted

could

impactedcome US

the

the cotton

theUS UScotton

from

US belt.

cotton

cottonthe While

belt.

belt. While

outcome

belt. indicators

While

While indicators

indicators

of areand

the

indicators that

are

US

are

have

arethatthat

held

cotton

cotton

cotton

election,

that cotton

steady

prices

prices

prices

ongoing

prices US/China (and US/

partly due to Hurricane Delta which impacted the US cotton belt. While indicators are that cotton prices

should

shouldcontinue

should

should continue to rise

continue toto into

rise

rise 2021,

into

into2021,

into volatility

2021, could

volatility

volatility come

could

could comefrom

come from the the

from outcome

the outcome

outcomeof the

of US

ofthe

the election,

USUS election,ongoing

election, ongoing

ongoing

should continue

Vietnam) trade

continue to

to rise

tension

rise into 2021,

and

2021, volatility

how

volatility could

long

could come

recovery

come from

from the

from

the outcome

outcome ofofthe

COVID-19 theUSUStakes. election,

election, ongoing

ongoing

US/China

US/China (and

US/China

US/China US/Vietnam)

(and

(and US/Vietnam)

US/Vietnam) trade tension

trade

trade tension andand

tension how

andhowlonglong

how recovery

long recovery

recovery from COVID-19

from

from COVID-19

COVID-19 takes. takes.

takes.

US/China (and

(and US/Vietnam) trade tension

US/Vietnam) trade tensionand

andhow

howlong

longrecovery

recoveryfrom

fromCOVID-19

COVID-19 takes.

takes.

Speed

Scale

Simplicity

Source: Cotton Inc, News Reports

Source:

Source:

Source: Cotton

Cotton

Source: Inc,

Inc,Inc,

Cotton News News Reports

Reports

News Reports

Sources: Cotton Inc, News Reports

Plastics and Synthetic Fibers

© 1995-2020 Copyright by CBX Software. All rights reserved.

©

© 1995-2020 Q4 2020 Snapshot:

© 1995-2020

1995-2020 Copyright

Copyright by

Copyright

© 1995-2020 by CBX

Copyright

by CBX

by CBX

CBX Software.

Software. All

Software.

All rights

All rights

Software.

rights reserved.

reserved.

reserved.

All rights reserved.

14

Synthetic fiber prices, especially for nylon and polyester fell dramatically through Q3 on lower oil

Plastics and

prices, Synthetic

currency Fibers

devaluations and lower demand for finished goods from Asia, Europe, and the US.

Stability on the supply is also an issue going forward. Synthetic fiber prices in Asia fell by more than

Q4 2020 News: Synthetic fiber prices, especially for nylon and polyester fell dramatically through Q3 on lower

20% year-on-year, mostly due to price drops in polyester, the most widely used fiber.

oil prices, currency devaluations and lower demand for finished goods from Asia, Europe, and the US.

Stability on the supply is also an issue going forward. Synthetic fiber prices in Asia fell by more than 20%

year-on-year, mostly due to price drops in polyester, the most widely used fiber.

Plastics & Fibers, Regrind/ Flakes (Euros/kg)

1.0

0.9

0.8

Nylon

0.7

0.6 Polyester

0.5 ABS

0.4 PVC

0.3

PP

0.2

PS

Sources: IMF data, Plasticker, ICIS

© 1995-2020 Copyright by CBX Software. All rights reserved.12

Quality Control Indicator

This report frequently covers quality control and quality assurance issues. Audit and inspection data which tend to mirror

sourcing activity, provide an indicator of activity and trends in various sourcing regions.

According to data from Quality Inspection provider QIMA, while sourcing and global trade picked up dramatically

through Q3 to meet demand, inspection and audit trends suggest that the recovery scramble has meant a sacrifice on

sustainability and social compliance. Many businesses went into survival mode, cutting costs where they can, adding

pressure on suppliers, in turn putting worker safety and product quality at risk.

Most of the issues around quality we have seen are related to inconsistencies with suppliers and the ability to adapt to

the added demands of the pandemic, both at the buyer and supplier level.

Demand for inspections in China grew at the rate of 11% (year-on-year) overall in Q3, especially from US and European

buyers in the electrical and electronics sectors. Lower demand for inspections (down 15% in Q3) in the Chinese textile

and apparel sector reflected the ongoing shift in apparel production to lower cost countries such as Bangladesh,

Vietnam, and others.

Overall, South-East Asia saw a pick-up in demand for inspections of 10% year-on-year, with growth in Myanmar,

Indonesia, the Philippines, and Vietnam – who all took business from China. South-Asia also saw growing demand for

inspections and audits, led by Bangladesh where inspections grew 86% in September.

Sources: QIMA Data, News Reports

The trend of nearshoring, which was picking up in recent years appears different for US and European buyers. The QIMA

data suggests that US brands were more likely to buy from factories reopening in South Asia than from Latin or South

America, whereas European brands continued to increase their sourcing (and inspections) from countries such as

Morocco, Egypt and Tunisia, which all saw double digit growth.

Sources: QIMA Data, News Reports

Q4 2020 Retail Sourcing Report13 Focus Topic: COVID-19, E-Commerce Accelerator

One of the bright spots that emerged through the COVID-19 pandemic is online retail. Already a growing force

prior to 2020, world-wide implementation of physical-distancing and stay-at-home orders has accelerated the

progression of e-commerce. To put it in perspective, according to Statista (chart below) in 2015 e-commerce

represented 7.4% of total global retail sales, by late 2020 e-commerce’s share of total retail will be above

16.1%. By 2023, online retail should comprise 22% of total retail.

This pandemic driven fundamental shift in consumer behavior will bring lasting effects as consumers shop

more online and retailers improve service levels. The cliché of “adapt or die” applies to retail more than ever.

Online shopping trends we see now provide a sense of where e-commerce is headed.

Lining the Nest

Nearly half of consumers shifted their spending across online verticals such as apparel and electronics, but

categories such as health, fitness, groceries, and DIY did especially well as people spent more time at home.

Online orders in most of these categories grew by two- or three-times times year-on-year, with some retailers

seeing increases of more than 20 times. (e-Marketer).

Retailers that capitalized on consumer trends such as food preparation, online fitness and home offices were

rewarded. Those able to perfect online models such as home delivery (Amazon) thrived through the pandemic

and will continue to do so after.

Platform vs Retailer/Brand

Another evolving trend that grew through the pandemic

is the customer focus on product availability in a

competitive marketplace. Amazon grew exponentially

not because it is cheaper, but because they provide a

platform for competing products, often direct from the

source which are vetted (reviewed) by other consumers.

Other marketplace such as Wayfair and eBay have also

carved out niches, but traditional retailers such as Best

Buy and Walmart are also betting heavily on their own

marketplaces to drive growth.

Re-evaluating Cost-Cutting

The biggest takeaway from the shift in consumer retail behavior, accelerated by the pandemic, is that

conventional forms of cost-cutting are less relevant. For example, historically retailers and brands placed a

heavy focus on the input cost factors we cover in this report – labor costs, material costs, currency exchange,

logistics efficiency and speed to market. Going forward, the biggest area where retailers and brands need

to look at cost-cutting is not through the supply chain, but at the end of it - whether in store or online or a

combination. As an example, companies such as Bed-Bath and Beyond have done well with their Buy-Online-

Pick-up-in-Store (BOPIS) model which has allowed them to cut bricks and mortar locations.

© 1995-2020 Copyright by CBX Software. All rights reserved.The Customer is Always Right 14

No doubt the elements that go into getting products to market quickly and at a reasonable price are still important. But

the biggest long-term factor of success for retailers and brands is the ability to innovate and provide consumers with

the holy grail of what consumers want. This is an ever-moving target but includes the right products (on-trend), meeting

product quality and social standards, pricing/value that makes sense and Amazon level service (question-free returns).

Most importantly though, the pandemic has reinforced some marketing basics – retailers need to ensure customers can

buy WHAT they want, WHEN they want it and WHERE they can get it – which increasingly means online.

The Outlook for Global Trade in Q4 and Beyond

No doubt the pandemic threw us for a loop, but the big question is what things will look like in the next quarter and

next year. Recent reports from the International Monetary Fund (IMF) and the United Nations Conference on Trade and

Development (UNCTAD) suggest that we are on the road to recovery through Q4 and into 2021, but it could be a rocky

road.

Despite what looks like a pandemic recovery, UNCTAD data showed a 5% drop in world trade in Q3 compared to the

same quarter in 2019. This is certainly an improvement over Q2, which saw a 19% drop year-on-year, but overall global

trade is still expected to contract by around 7-9% relative to 2019. While not great news, these numbers reflect a

better than expected outcome, with manufacturing in Asia recovering quicker than expected and demand for products

continuing strong in North America and Europe, possibly as people spent more on goods versus services.

Asia is expected to fare better than the rest of the world, with the IMF forecasting a 2.2% contraction for 2020, based

mostly on the greater impact from COVID-19 through Q3 on India, Malaysia, and the Philippines. China is one exception,

with the IMF predicting growth of 1.9% for 2020 relative to 2019. Chinese exports plummeted in Q1 but picked up

strongly through Q2 and Q3 and should reach year-on-year growth of around 10% (UNCTAD). Chinese imports also grew

strongly through Q3, reaching 13% growth in September. The most dramatic decline in trade was in South and West Asia,

where imports dropped by 23% and exports declined by 29%.

Certain sectors such as energy and automotive were particularly hard hit, while other sectors such a communication

equipment, office machinery, textiles and apparel had robust growth. Exports in medical supplies from China, the

European Union, and the United States grew from an average of US $25 billion to $45 billion per month from January

to May 2020 and 50% per month in subsequent months. The concern revealed by the UNCTAD data is that wealthy

countries have more access to medical supplies, especially non-PPE products – for example, a vaccine. The report

stresses that once a COVID-19 vaccine is created, it is important for developing countries to have equal access to ensure

a faster global recovery.

Q4 2020 Retail Sourcing Report16

About

CBX Software is the world’s leading Total Sourcing TradeBeyond is an exclusive community of retailers,

Management solution provider, from concept, to suppliers, and brands coming together to streamline

delivery – combining people, process and solutions. assortment planning, sourcing, quotations, and

CBX helps retailers and brands streamline product buying. TradeBeyond is not a marketplace; it’s a

development and sourcing, all the way through order & network and an app used by retailers to discover

production. CBX empowers the supply chain network new exclusive products and by suppliers to get

by driving collaboration to over 15,000 retail & supplier discovered and win more business! Visit www.

partners and 30,000 users in more than 50 countries. tradebeyond.com

For more information, visit www.cbxsoftware.com.

Americas +1.858.264.1133

Asia +852.2378.6300

EMEA +49.89.9040.5110

Click below to learn more about

how CBX Software can help!

Request a Callback Request a Demo

© 1995-2020 Copyright by CBX Software. All rights reserved.You can also read