Portfolio Management Diary - Dec 2020 Kotak Pharma & Healthcare Investment Approach - Kotak Mutual Fund

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Portfolio Management Diary – Dec 2020

Kotak Pharma & Healthcare Investment

Approach

1

2

Focus On Key Themes In Portfolio - Domestic pharma growth India is becoming ready for its mega vaccine rollout after saying goodbye to a 2020, a year everyone would like to forget. If there was ever and unanticipated, high impact event, which shook the world, it was the Covid pandemic which had its origins in Wuhan, China. This Black Swan event shook global markets with lockdowns becoming the norm across the globe. In response to the pandemic, Central Banks undertook Monetary and Fiscal measures to pump liquidity into the system and support ailing households and businesses. On the medical front a concerted & joint effort was put in place to develop a vaccine. As the year ended there are at least 6 vaccines which are believed to be efficacious. The roll out of these vaccines would give some succor to the global markets regarding a pickup in demand in CY21. In order to play the Growth opportunities in Pharma & Healthcare, we are focusing on the following themes in our portfolio. Growth in Domestic Pharma demand With the economic activity normalizing at a fairly brisk pace across the country, the Q3 growth trends should further improve going forward. For 9MFY21, IPM has grown at 2.9% yoy and industry estimates ~4.6% growth for FY21 – a reasonably positive outcome given the slow start to FY21. Overall, for Q3FY21, IPM has recorded a reasonably healthy growth of 8.4% with Dec growing at +12%YoY partially driven by strong uptick in COVID treatment options like Remdesivir / Favipiravir. We estimate that excluding contribution from COVID drugs, IPM growth for Q3FY21 has been 6.8%. • ERIS Lifesciences targeting growth in Chronic therapies ie Cardiac, Neuro and Anti-diabeties • Cipla, Cadila focused on strong uptick in COVID treatment options like Remdesivir • Glaxo Pharma, Alkem Lab, IPCA having strong presence in Acute therapies, pain mgmt with strong brands growing in double digits • Fortis Healthcare plays on recovery theme in hospitals and steady growth in diagnostic/pathology services . Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned in the note does not guarantee future performance/return. Source: The Hindu Business Line 3

Covid related supply opportunities in India & global markets

COVID drugs (ie Remdesivir) have been the fastest growing segment with 200%+ yoy growth during December to Rs2.5bn; Remdesivir has

continued to gain ground through the last few months and clocked Rs1.4bn sales in Dec vs Rs1.66bn in Nov’20. For YTD FY21, Remdesivir sales

have been ~Rs6bn – making it one of the largest molecules in IPM for FY21. The portfolio is well positioned with following holdings.

4

Source: ICMR, Compay

China + 1 supply chain beneficiary The US-trade tension along with Covid disruption has catalyzed diversification of supply chains away from China. The objective of such a diversification is to supplement current supply lines from China. The Indian government is mindful of this global trend and has put in place multiple incentives to attract businesses toward India. For instance, implementation of far reaching reforms like GST, IBC, Cut in Corporate tax rates (17% for setting up new manufacturing facilities) & recent Production Linked Incentive schemes for APIs, key starting material (KSM) manufacturing in Pharma are expected to make India an attractive investment destination. Company’s in APIs, Contract Development & Manufacturing Outsourcing (CDMO) are witnessing enhanced enquiries and order inflows. Companies are gearing up to take advantage of this prospective order inflow by adding to capacities and R&D Capabilities. For instance Divis Laboratories (Divis), a portfolio company is one of the largest generic API manufacturers globally and has a successful track record of executing custom synthesis business for innovator customers. Recent and planned capex of ~Rs22bn for expanding capacities provide very high business growth visibility. Key moats of the company have been continuous process innovation, low cost production, talent retention and long-standing relationships with customers.. The management is targeting additional revenue of ~Rs40bn from this new capex over the next few years. Similarly Suven Pharmaceuticals and Hikal Ltd are other portfolio companies; which are in process to invest Rs1,000cr and Rs300cr respectively in building capacities and renew its R&D facilities with latest technologies to capture future growth opportunities. These initiatives are likely to result in strong operating efficiencies, better margins with additions of new products for driving growth ahead. Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned in the note does not guarantee future performance/return. 5 Source: ICMR, Compay

US Gx – tailwinds: Improved pricing, approvals, shortages

Portfolio companies

could leverage the US

generic growth

opportunities are

Indoco Remedies,

Aurobindo Pharma

and JB Chemicals –

recent qtrs revenue

growth trajectory

from the US for these

companies

underscores these

trends.

Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned

in the note does not guarantee future performance/return. 6

Significant R&D has led to substantial pipeline Indian BIG Pharma players have invested heavily over the last 5-years in R&D – this has provided them with a strong pipeline of products which could be launched over the next few years. However our large holding in Sun Pharma which is focused on Speciality Pharma – could see sizeable growth opportunities ahead as its key speciality products ‘Illumya’ and ‘Cequa’ see increased market acceptance and grow market share in US and other developed markets. Note: The names mentioned in this note are for reference only, actual portfolio may differ as per fund manager’s discretion and the underlying stocks mentioned in the note does not guarantee future performance/return. 7

Global Economy

7

Global Economy Has Rebounded Strongly

Citi Economic Surprise Index* (global)

*The CESI compares economic data against economists expectation , rising when the exceeds consensus estimates and falling when the data are below estimates

Source: Refinitv 9

Record Money Printing By Central Banks

Source: Goldman Sachs Global Investment Research

10Excess Liquidity Supports Global Equities Source: Refinitiv, Credit Suisseresearch 11

Record Debt Now Trades At Negative Yield

12Low Interest Rates Support Equity Valuations

Equity valuations will remain a big part of the

market narrative in 1H21. However, history

indicates today’s valuation are supported by

historically low interest rates

Source: Market Desk Research, Yale / Robert Shiler 13 12Global Valuations At Elevated Levels After A Sharp Rerating

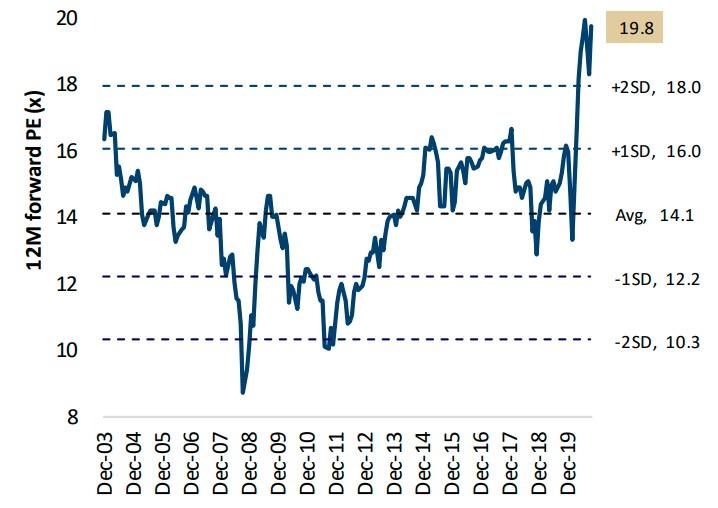

MSCI AC World – 12-month forward PE band

Source: Jefferies, FactSet, As on Nov 2020 14Big Becoming Bigger Source: Bloomberg 15

lndian Economy

15Activity Tracker: India :Supply Side Indicators Also Showing Improving Trends Source: CMIE, RBI, GSTN, Vahan, UBS 17

Economy Back In Green Red- Negative, Amber-Watch, Blue-Neutral, Green-Positive; Source: Nirmal Bang Institutional Equities Research, Google-mobility report, CMIE, Reserve Bank of India, Government of India, CEIC,Bloomberg. 18

Economic Normalisation Continues Apace Source: Google, Apple, CMIE, Bloomberg and Nomura Global Economics 19

Record High GST Collections Source: Ministry of Finance, moneycontrol.com 20

Manufacturing PMI Shows Momentum Holding Up

Manufacturing momentum stabilizes in Dec

Services could show sequential improvement

Source: CEIC, Bloomberg, Markit

21PLI Schemes Can Add 1.6% To FY27 GDP Source: RAVE, Credit Suisseestimates 22

Vaccination Will Begun In 1 Q CY 21

23Equity Markets

32Rising Ownership Of FII’s In Indian Equities Source: CMIE, Bloomberg, UBS India 25

$1 Trillion Could Flow Into The Stock Market In 2021

Change in flows per year in $bn.

Source: J.P. Morgan 26EM Equities Are The Most Preferred Asset Class Source: BofA Securities fund managers survey 27

India Is Attractive Destination For FPI Flows

30.0 12 Months FPI Flows (Dec’ 19 to Dec’ 20) USD Bn

25.0 23.0

20.0

15.0

10.0

5.0

0.0

-5.0 India Philippines Indonesia Malaysia South Thailand Brazil Taiwan South

-2.5 -3.2 Africa Korea

-10.0 -5.8

-7.4 -8.3 -8.5

-15.0

-16.2

-20.0

-20.1

-25.0

Source: Axis Capital 28Sept 20 Results Were Above Expectations

Source: Bloomberg

29Earnings Growth Likely To Rebound Strongly

`

Source: Bloomberg estimates, Bernstein analysis 30Nifty Trading Rich Relative To Its Own History But Not Relative

To EM Peers

Nifty trading at rich valuations on 12m fwd PE: India's premium to EM at 5 year mean

Source: Datastream, Bloomberg, UBS 31Performance Across Sectors – Pharma has

outperformed thus far

Sectoral Performance CY20 YTD (%)

61%

55%

22% 21%

15% 16%

13% 12%

11%

6% 5% 4%

-3% -3%

-9%

Secvices

Bank

Financials

IT Services

Metals

Private Banks

Smallcap 100

Auto

Energy

FMCG

Realty

NIFTY 50

Pharma

Media

Midcap 100

Source: Bloomberg, Axis Capital. As on 31st Dec 2020. Past Performance may or may not sustain in the future 32Corrections Are Part Of Market Cycle – trend seems positive

Nifty -10% correction from 6 month highs

Source: Bloomberg As on Dec 2020 33Market Cap-to-GDP Ratio – Above Long Term Average

Market cap-to-GDP ratio: Market rebound brings ratio above long term average

103 Average of 75% for the period

95 98

88

82 83 83

81 79 79

71

66 69

64

55 56

52

FY20

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY21E

OW Equities =Ratio Below Historical Lows Neutral Equities = Ratio at Historical Average

Source: Motilal Oswal 34Disclaimer

Investments in securities are subject to market risk and there is no assurance or guarantee of the objectives of the Portfolio being achieved or

safety of corpus. Past performance does not guarantee future performance. The performance related information in the presentation is not

verified by SEBI. Investors must keep in mind that the aforementioned statements/presentation cannot disclose all the risks and

characteristics. Investors are requested to read and understand the investment strategy, and take into consideration all the risk factors

including their financial condition, suitability to risk return profile, and the like and take professional advice before investing. Opinions

expressed are our current opinions as of the date appearing on this material only.

These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local

law or regulation. The distribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons

who come into possession of this document are required to inform themselves about, and to observe, any such restrictions

We have reviewed the document though its accuracy or completeness cannot be guaranteed. Neither the company, nor any person connected

with it, accepts any liability arising from the use of this document. The recipients of this material should rely on their own investigations and

take their own independent professional advice. While we endeavor to update on a reasonable basis the information discussed in this

material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Investors and others are cautioned that any

forward - looking statements are not predictions and may be subject to change without notice.

Statutory Details: Portfolio Manager: Kotak Mahindra Asset Management Company Ltd. SEBI Reg No: INP000000837- Registered Office: 27

BKC, C-27, G Block, Bandra Kurla Complex, Bandra (E), Mumbai - 400 051, Principal Place of Business: 2nd Floor, 12 BKC, Plot No. C-12, ‘G’

Block, Bandra Kurla Complex, Bandra East, Mumbai – 400 051,India. Address of correspondence:6th Floor Kotak Towers, Building No 21

Infinity Park, Off W. E. Highway, Gen A K. Vaidya Marg, Malad (E), Mumbai 400097. - Contact details:02266056825

35You can also read