Polaris Infrastructure - (TSE: PIF)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Polaris Infrastructure (TSE: PIF) Natural Resources Group Analysts: Gabrielle Gregg, Owen Stimpson, Garrick Bracken, Nitin Reddy, Chloe Macklin, Edward Liu Researchers: Krishan Karia, Derek Liu, Sophia Lu, Damien Perera, Amay Shenoy, Nick Woollcombe, Judy Zhang January 20th, 2021

Disclaimer The analyses and conclusions of the Western Investment Club (“WIC") contained in this presentation are based on publicly available information. WIC recognizes that there may be confidential information in the possession of the companies discussed in the presentation that could lead these companies to disagree with WIC’s conclusions. This presentation and the information contained herein is not a recommendation or solicitation to buy or sell any securities. The analyses provided may include certain statements, estimates and projections prepared with respect to, among other things, the historical and anticipated operating performance of the companies, access to capital markets and the values of assets and liabilities. Such statements, estimates, and projections reflect various assumptions by WIC concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrative purposes. No representations, express or implied, are made as to the accuracy or completeness of such statements, estimates or projections or with respect to any other materials herein. Actual results may vary materially from the estimates and projected results contained herein. The sole responsibility for the content of this publication lies with the authors. Its contents do not reflect the opinion of the University Students’ Council of the University of Western Ontario (“USC”). The USC assumes no responsibility or liability for any error, inaccuracy, omission or comment contained in this publication or for any use that may be made of such information by the reader.

Table of Contents I. Introduction to Emerging Markets II. Business Overview III. External Analysis IV. Internal Analysis V. Thesis I VI. Thesis II VII. Thesis III VIII. Valuation IX. Catalysts X. Risks & Mitigations XI. Appendix

I Introduction to Emerging Markets

Emerging Markets Investing

Introduction

What are Emerging Markets? Key Characteristics

▪ Global economies in nations actively pursuing

Emerging Developed

development – share some characteristics with developed

nations, though still not fully developed High income & GDP per capita X

High political uncertainty X

– Eg: country with growing solar infrastructure

Highly developed capital markets X

(advanced technology) while per capita energy usage

is much lower than developed economies High market volatility X

High economic growth rates X

▪ Emerging markets are in various stages of development,

Highly established regulatory regimes X

but tend to experience higher growth rates than developed

countries

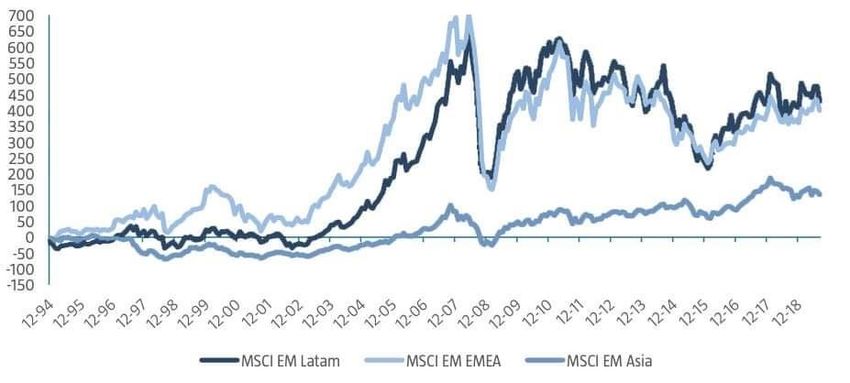

Cumulative EM Performance by Region Map of Emerging Markets

750▪ Need to be recolored with WIC

600

450

300

150

0

-150

Dec-1994 Dec-2006 Dec-2018

MSCI EM LatAm MSCI EM EMEA MSCI EM Asia

Emerging Markets

Sources: RBC, Global Finance Magazine, MSCI

Emerging Markets Investing

Challenges & opportunities

Economic Growth Geopolitical Risk

▪ GDP growth is generally higher in emerging markets due ▪ Developing economies are often accompanied by

to a key focus on economic development while developing political contexts

developed nations focus more on economic stability ▪ Political instability and civil unrest can have significant

▪ The World Bank estimates that 75% of global GDP implications for companies operating in emerging markets

growth from 2008 – 2018 has come from emerging ▪ Foreign policy changes, trade wars, environmental

markets in Asia, Latin America, and Africa issues, regime changes, and military tensions are key

factors that more substantially affect emerging markets

than developed countries

Demographics Volatility

▪ Changing demographics, while important in any economy ▪ Stock price & market volatility is often higher than in

for macroeconomic trend predictions, can have more mature markets due to unpredictability of numerous

substantial impacts in emerging markets factors in these economies

▪ Significant demographic change coupled with economic ▪ Volatility is also driven by heightened perception of

political instability and its impact on the economy

growth can either compound or neutralize projected

growth trends ▪ Reduced government control over economy due to high

dependence on foreign-determined factors such as:

– Trade relations

– Foreign Investment

Sources: RBC

II Business Overview

Business Overview

Polaris Infrastructure operates renewable energy project in Latin America

Business Overview Key Financials

Ticker TSE: PIF

▪ Polaris Infrastructure (TSE: PIF) is a developer, owner, and

operator of renewable energy projects in Latin America Share Price $18.25

▪ Currently operates four projects in Nicaragua and Peru, 52 Week Low – High $8.59 – $19.88

both hydro and geothermal, with two additional projects Enterprise Value $468.7 M

currently under construction in Nicaragua and Panama

Market Capitalization $291.3 M

▪ While smaller than most competitors operating in Latin 2021E EV / EBITDA 6.4x

America, Polaris capitalizes on smaller market

2021E Price / Earnings 19.5x

opportunities, specifically $50M – $150M projects

2021E Net Debt / EBITDA 2.3x

Geographic Power Generation Breakdown 52-Week Stock Performance

$24 800,000

$18 600,000

28%

Nicaragua $12 400,000

Peru

72% $6 200,000

$0 0

16/Jan/20 16/Apr/20 16/Jul/20 16/Oct/20

Business Overview: Assets

Polaris continues to expand assets with focus on geographical & asset-type diversification

Key Assets Asset Diversification

▪ Nicaraguan projects are geothermal assets, while those in

Nicaragua Peru and Panama are Run of River Hydro projects

▪ In past 2-3 years, Polaris has shifted focus towards

San Jacinto – 72MW Binary Plant Addition – 10MW diversification, expanding from a single asset in Nicaragua

– Asset type and geographical diversification

▪ Diversification expected to continue in coming years with

Peru potential new projects and acquisitions

▪ All assets & potential future projects fall under renewables

Canchayllo – 5MW 8 de Agosto – 20MW El Carmen – 8MW umbrella; project size ranges typically from $50M - $150M

Expansion Pipeline

Geography Generation Type Size

Panama

Nicaragua Geothermal 5-10 MW

Panama Hydro 10 MW

Chuspa – 10MW

Peru Hydro 20 MW

Dominican Solar 32 + 20 MW

Management sees opportunities to continue growth into Panama Hydro 14 MW

Panama, and extend further across Latin America with delays in Panama Solar 10 MW

construction stemming from COVID risks

Peru Hydro 80 MW

Several Diversified >100 MW

III External Analysis

External Analysis

Renewable energy projects are becoming increasingly economical

Overview of Renewable Energy Levelized Cost of Electricity by Technology

▪ Renewable Energy – energy derived from natural $0.20

processes that are replenished at a rate that is equal to Fossil Fuel Price Range

or faster than the rate at which they are consumed $0.15

(USD/kWh)

$0.12

▪ While historically costly, renewable energy technology is $0.10 $0.07 $0.07

key to combatting climate change by producing electricity $0.05

$0.05

with reduced emissions and without air pollution $0.05

▪ Renewables have seen drastic cost reductions increasing

their feasibility and popularity, making it a very $0.00

Geothermal Hydro Solar Offshore Onshore

attractive source of energy Wind Wind

Global Renewable Electricity Generation Breakdown

8,000,000

Biofuels & Waste Hydro Solar Wind Other sources

7,000,000

6,000,000

5,000,000

(GWh)

4,000,000

3,000,000

2,000,000

1,000,000

0

1990 1995 2000 2005 2010 2015 2018

Source: IEA, IRENAExternal Analysis

Several key factors driving renewables growth in Latin America

Latin America Energy Targets Latin America Electricity Generation

▪ A coalition of Latin American and Caribbean countries 1,500

pledged a target of 70% renewable energy use by 2030 1,250

1,000

– ~33% is currently non-renewable 59%

(TWh)

67%

750 66%

– Overall grid growth is the main driver for 70%

500 72%

renewable energy generation growth 75%

75%

250

▪ Small power stations are more likely to be constructed than 0

larger ones for rural areas to gain access to electricity 1990 1995 2000 2005 2010 2015 2018

Fossil Fuels Renewable

Selected Renewable Energy Policies in Latin America

60

Import/Export Fiscal Benefits Auctions

Number of Countries Opted

50

Pre-investment Support

Net Metering

40 Direct Funding

Tax Exemptions

30 Fuel Mandates

Currency Hedging

20 Eligible Funds

10 Others Others

Others

0

Fiscal Incentives Regulatory Instruments Financial Mechanisms

Source: Reuters, IEA, IRENAExternal Analysis

Polaris’ key target geographies are focused on increasing renewable energy usage

Nicaragua Peru

▪ 42% of electricity supply is oil, with 58% renewable (mix of ▪ Electricity mix is 54% renewable energy and 46%

solar, biofuel, wind, geothermal, hydro) conventional energy

– Venezuelan oil dependency is a key driver for renewable ▪ Target mix is 60% renewable and 40% gas by 2025

electricity growth – Main driver: reduce imports of fossil fuel products

– Aims to generate 91% of electricity from renewables by ▪ Project focus is small-scale renewable energy plants (such as

2027 small hydro or solar) for rural communities to achieve

“nationwide electrification” by 2021)

▪ National energy consumption has increased over 200% since 1990

– Historical 20-year generation growth of ~5.5% CAGR

– Main drivers: Both grid growth and conversion from fossil

– Peru has an electrification rate of roughly 84%

fuels are drivers for renewable growth in Nicaragua

Panama Dominican

▪ Panama National Energy Plan 2015-2050 suggests that 77% of ▪ Current electricity generation mix is 14% renewable

the country’s power supply could be renewable in the next

35 years – Target mix is 25% electricity generated by renewable

energy sources by 2025

– ~33% is currently produced using fossil fuel

generation (coal, oil and natural gas) ▪ Signed the Paris Agreement within the UN

▪ Signed the Paris Agreement within the UN ▪ As with the other countries, regulatory and incentive policy has

been implemented to encourage this change

▪ Main driver: While some conversion is needed, overall grid

growth will grow renewable energy generation ▪ Main drivers: Both grid growth and conversion from fossil

– Historical 20-year generation growth of ~3.8% CAGR fuels are drivers for renewable growth in Dominican

▪ Historical 20-year generation growth of ~2.6% CAGR

Source: Investor Presentation, Company Filings, Oxford business groupExternal Analysis

Nicaraguan Geopolitical Risk

Political Context Nicaraguan GDP per Capita

▪ President Daniel Ortega has been in power since 2007, and $2,500

is the leader of the Sandinista National Liberation

$2,000

Front party

$1,500

– SNLF party – party with Socialist beliefs

▪ Various pro-democracy, anti-socialism protests have taken $1,000

place since 2018 yielding conflict between civilians & $500

government

$0

▪ Dictatorship also yields numerous potential risks related to

checks & balances in government

Key Considerations Latin America – Risk Factor Breakdown

▪ Dictatorship, while not favorable or optimal in any Corruption

way, is not a prominent risk to foreign business operations 7%

13% Excessive Bureaucracy

▪ Significant portion of geopolitical risk in Latin America

comes from Political Instability 41%

Violence

– Of this, a majority is derived from regime change 15%

due to changes in law and goals of new party Political Instability

▪ Opposition to Ortega’s leadership has largely been

24% Macroeconomic &

promotion of democracy which would be have positive Policy Turbulence

implications for all stakeholders in Nicaragua

Source: Geoffrey Jones, Harvard UniversityIV Internal Analysis

Internal Analysis

Polaris owns & operates four key projects across Latin America with upcoming potential expansions

San Jacinto PPA Contract Renewal Project Overview

▪ Term of contract extended to January 2039 (from 2029)

– This increases Polaris’ weighted average contract

length for their projects to 18.1 years

– Indicates codependence with government and

stability of future cash flows

▪ Polaris can build a new binary unit in San Jacinto to

increase capacity by up to 10MW

– Projected to generate $6M in cash flow and cost

$20M to get online by 2023; 3.3 year payback period

▪ Removal of price escalator and a lower price of US$110

per MWh from US$130 per MWh

– Equates to US$12M reduction in annual cash flow San Jacinto

(72 MW)

▪ Income tax holiday extension from 2023 to 2025

▪ Series of changes provides opportunity to refinance 8 de Agosto

(20 MW)

existing project loan with more favourable terms

– Time frame matching of asset life, contract length, El Carmen

and debt length can have significant implications on (8 MW)

ability to pursue growth opportunities

Canchayllo

▪ Management believes that new contract is net positive to (5 MW)

previous contract on NPV basis

Source: Investor Presentation, Annual ReportInternal Analysis

Polaris’ balance sheet has improved drastically since restructuring in 2015

Restructuring & Current Balance Sheet Strength Credit Statistics

▪ In 2015 Polaris completed a capital structure Polaris Peer Average

restructuring by converting debentures into common

shares and amending credit agreements with existing Interest Coverage 3.5x 3.2x

lenders

Net Debt /

– The financial distress was caused by high leverage 2.0x 3.2x

EBITDA 2021E

and poor cash management by the previous

management team at the San Jacinto Power Plant Quick Ratio 2.3x 0.8x

▪ The San Jacinto Power Plant was stabilized in 2016 and

Polaris has used the stable cash flows from this asset

to pay down existing debt obligations Debt Obligations

▪ Polaris boasts a strong balance sheet and ample liquidity 38 38

40 35

to fund future developments throughout Latin America

35 31 31

Debt Obligations

▪ The amended PPA agreement for the San Jacinto facility 30 27

24 24

($ Millions)

should enable the company to refinance existing debt 25 21 19

obligations at a much lower cost 20

15

– Refinancing the debt is expected to result in up to a 10

$15 million reduction in debt servicing costs, 5

increasing cash flows which can then be used to 0

2021E 2022E 2023E 2024E 2025E

fund growth opportunities

Current Debt Obligations Refinancing Debt Obligations

Source: CapIQInternal Analysis

Polaris’ strategy and location provides a long runway for dividend growth and project expansion

Operating Cash Flow Generation Annual Dividend Per Share

Peru Asset Development

▪ Polaris focuses on acquiring and developing assets that $0.70

generate less than 25MW in power $0.60

$0.50

– There is limited competition for these projects as

$0.40

they are too small for most major utility companies

$0.30 $0.53 $0.60 $0.60 $0.60

which drives down the prices Polaris pays

$0.20

▪ Polaris also focuses on utility markets that are $0.31

$0.10

“undersupplied” allowing the company to negotiate PPA $0.00

pricing that is much higher than developed markets in 2016 2017 2018 2019 2020

Europe and North America

▪ These factors enable the company to achieve profitability Comparable Valuations

despite being smaller than competitors Dividend as

Market Enterprise Dividend % of Operating

– Polaris spends a much smaller portion of operating Capitalization Value Yield Cash Flow

cash flow on dividends compared to peers, allowing Algonquin Power 12,798 19,141 3.68% 50.0%

Boralex 5,451 8,434 1.22% 18.0%

the company more flexibility with it’s operating Innergex Renewable 5,250 10,034 2.40% 48.3%

cash flow Etrion Corporation 172 218 N/A N/A

Ormat Technologies 6,289 715 0.41% 8.0%

Transalata Renewables 5,863 6,684 4.32% 75.0%

Mean 5,970 7,538 2.4% 39.9%

Median 5,657 7,559 2.4% 48.3%

Polaris Infrastructure 291 469 4.3% 21.8%V Thesis I

Thesis I: Polaris Well-Positioned For Growth

Strong external environment in Latin America presents numerous opportunities

Low Competition in High Growth Environment Select Regional Electricity Demand Growth (%)

▪ Other major renewable project developers are much larger in size and 50%

typically do not prioritize lower capacity assets (Thesis I: Polaris Well-Positioned For Growth

Management is focused on growing company operations

Overview of Management View Management Expansion Targets (Geography)

▪ Management attitude towards growth is key

consideration

▪ Primary research demonstrates management’s plan to

expand operations beyond current geographies and asset

type is core to their business

– MOU to be signed in Panama has been delayed due

to COVID-19 complications, but management is

confident hat it has not materially changed the

growth prospect

▪ Plan to continue acquisitions/new developments reduces Current Nicaragua

the expected generation share of the Nicaraguan Plants (70 MW)

asset to less than 33% of the overall asset mix by Current Peru Plants

approximately 2024, from 90%+ in 2019 (33 MW)

– Management demonstrated clear intent to diversify, New Panama Plants (34 MW)

addressing concerns of single asset risk New Peru Plants (100 MW)

– Can result in multiple re-rating due to reduced risk New Dominican Plant

(52 MW)

Target Acquisitions vs Investible Cash FlowThesis I: Polaris Well-Positioned For Growth

Polaris’ growth plan indicates strong asset diversification, which will drive multiple re-rate

Growth Strategy (MW Capacity)

300

250

200

150

100

50 93% 68% 49% 32% 32% 24%

0

2019 2020 2021 2022 2023 2024/25

Nicaragua Peru Panama Other

Capital

Geography Generation Type Size Stage Required Estimated IRR

Nicaragua Geothermal 5-10 MW Construction $15 - $20 M +20%

Panama Hydro 10 MW Construction $15 - $20 M 15%

Peru Hydro 20 MW Operating $15 M 8 – 10%

Progress

Panama Solar 10 MW Greenfield $10M 12%

Dominican Solar 32 + 20 MW Operating + Expansion $15 - $20 M –

Panama Hydro 14 MW Operating $10 M 8 – 10%

Peru Hydro 80 MW Greenfield N/A 15%

Several Others Diversified >100 MW Operating + Expansion N/A 10 - 12%

Source: Investor PresentationThesis I: Polaris Well-Positioned For Growth

Polaris’ strong balance sheet and stable cash flows suggest feasibility of extensive growth

Strong Balance Sheet and Predictable Cash Flow Debt-EBITDA vs Comps

10.0x 9.4x

▪ Given the nature of the long-term energy PPAs, Polaris

benefits from a stable revenue stream that depends very 7.6x

8.0x

little on external factors 6.3x

6.0x 5.2x

▪ Predictable revenue leads to predictable cash flows, 4.1x

which Polaris has leveraged to maintain a strong cash 4.0x

2.3x

position and consistent paydowns on debt 2.0x

▪ Lower debt figures relative to competitors also enables 0.0x

stronger growth capabilities PIF BLX ETX AQN ORA INE

Polaris Cash Sources vs Uses for Growth-Projects

180 M

Other

150 M

Dominican

120 M

Panama

90 M Peru

60 M Nicaragua 2021

30 M 5-year FCF

M Cash

Polaris Growth Initiatives

Target Acquisitions vs Investible Cash FlowVI Thesis II

Thesis II: Stability Amid Geopolitical Risk

Financial history indicates stability and limited political sensitivity

Cash Receipts vs. Debt Service

$ 25 M

$ 20 M

$ 15 M

$ 10 M

$5M

$ M

Q1 2016 Q1 2017 Q1 2018 Q1 2019 Q1 2020

Cash Receipts Debt Service

Dividend History

$0.16

$0.12

$0.08

$0.04

$0.00

Q1 2016 Q1 2017 Q1 2018 Q1 2019 Q1 2020

Dividends Paid

Source: Investor PresentationThesis II: Stability Amid Geopolitical Risk

Financial history indicates stability and limited political sensitivity

Immaterial Impact of Political Turmoil

$ 25 M

$ 20 M

$ 15 M

$ 10 M

$5M

$ M

Q1 2016 Q1 2017 Q1 2018 Q1 2019 Q1 2020

Cash Receipts Debt Service

Dividend History

$0.16

$0.12

$0.08

$0.04

$0.00

Q1 2016 Q1 2017 Q1 2018 Q1 2019 Q1 2020

Dividends Paid

Source: Investor PresentationThesis II: Stability Amid Geopolitical Risk

Domestic use & necessity of energy hedge against geopolitical risk

Electricity as Essential Service Domestic vs. Export

▪ Regardless of political context, energy is essential to ▪ Traditional geopolitical conflicts arise more frequently in

both the people and the government the context of corporations exporting products to Western

▪ Impossible for government to have public support without nations

reliable electricity for civilians ▪ Reliance of local communities on Polaris electricity

▪ For the rest of an economy to operate, energy needs to be yields different relationship with company & government

available as compared to traditional foreign exporters

– Unreliability in energy sector does not help any ▪ Companies exporting output are potential levers for

political party; even in times of political instability, governments to pull in times of foreign political conflict

energy sector remains priority

Crucial for Development Correlated GDP and Energy Use per Capita

180

▪ Requirement of energy as basic input for most production

Energy Use per Capita (MWh)

& consumption activities makes energy key to further 150

economic development 120

▪ Energy use in Latin America per capita is roughly 10 – 20% 90

of that in North America

60

– Consistent growth of energy consumption per

capita in recent years across Latin America 30

▪ As countries across Latin America continue to develop, -

- 20 40 60 80

energy demand continues to grow with renewables being

GDP per Capita ($Thousands)

the key area of energy growth

_ Nicaragua Peru Panama

Sources: Investor Presentation, Our World in Data (Oxford)Thesis II: Stability Amid Geopolitical Risk

Notable differences between Polaris and traditional Natural Resource foreign companies

Comparison of Common Foreign-Held Companies to Polaris

Mining & Oil Polaris

Low – output is exported & not High – domestic reliance on Polaris

Importance to Locals used domestically for electricity, necessity for daily life

High – fluctuations in prices greatly Low – minimal price variation &

Profitability Variability affect profit; expropriation becomes highly contracted revenue reduce

more attractive & tensions rise variability

American Dollars – extremely Local – makes business no more

Currency valuable to government increasing attractive to expropriation than any

attractiveness of expropriation other local company

Sources: The Economist, Mabel Azcui,, Norton Rose Fulbright, Project FinanceThesis II: Stability Amid Geopolitical Risk

Historical expropriation examples

▪ Asian economic collapse of 1997 caused largely by Thai foreign debt and currency value concerns

was self-fulfilling prophecy across Asia ⟶ this is worst case scenario in which entire continent

sees economic collapse

Indonesian ▪ 27 foreign-owned PPA contracts were in place, Indonesian government could not pay, shuts down

Expropriation of CalEnergy Assets; company sues winning $570M

CalEnergy utilities,

1998 ▪ 20 other PPAs in Indonesia are renegotiated

▪ Key implications: expropriation does not indicate loss of full investment; expropriation is also not

only potential outcome (renegotiation is a mutually beneficial alternative)

▪ While volatility is somewhat common, volatility ≠ risk; risk = permanent impairment of capital

▪ Oil & Gas assets result in depletion of limited high-value resources; Venezuela’s key export

– Depletion of fixed-quantity key resource by foreign multinational companies leads to

immense conflict between company & government

Venezuelan ▪ Government expropriates Conoco assets; company compensated with 45% of book value, and 2.5x

Expropriation of earnings

Conoco Assets, 2007

▪ Key differences & implications: second example showing how expropriations don’t result in

complete loss of investment; Oil & Gas was exported while Polaris electricity is used & sold

domestically; Polaris is a renewables company, meaning there is no depletion of country’s

natural resource

Non-depletion resource and lack of political focus & action on expropriation further indicate reduced risk for Polaris

Sources: The Economist, Mabel Azcui,, Norton Rose Fulbright, Project FinanceVII Thesis III

Thesis III: Valuation Discount to Peers

Polaris trades at a 59% discount to peers when other Latin America companies trade at a 30% discount

Summary of Historical Multiples Compared to Peers

100x

80x

60x

40x

20x

x

Algonquin Boralex Innergex Etrion Ormat Transalta Mean 25% Discount Polaris

Power Renewable Corporation Technologies Renewables Infrastructure

EV/EBITDA LTM EV/EBITDA 2021 P/E LTM P/E 2021

Global EV / EBITDA Valuation Gap

▪ Polaris currently trades at a 59% discount to peers and a 56% discount

EV / EBITDA Discount

to the average Canadian company vs other natural resource companies

Canada & US 14.6x –

that trade at a discount of approximately 33% relative to peers

Latin America 9.7x 33.6%

Polaris 6.4x 56.0% – Current discount is due to investor concern regarding Nicaragua

▪ Polaris continues to diversify away from Nicaragua, the discount

relative to North American peers should narrow and this multiple

expansion should result in share price appreciationThesis III: Valuation Discount to Peers

Case study: Parex Resources trades at approximately 74% of peers

Implied Valuation Implications

EV / EBITDA Production ▪ Parex Resources, a TSE listed oil & gas producer

Company LTM 2021E boe/d % Liquids

in Colombia trades at ~74% of peers on an EV /

Enerplus Corporation 3.2x 3.7x 85,800 78%

EBITDA basis

Paramount Resources 4.7x 5.4x 70,600 70%

Tamarack Valley 3.8x 4.6x 21,100 86% ▪ Polaris currently trades at ~ 41% of peers on an EV /

Baytex Energy 4.4x 5.1x 72,100 92% EBITDA basis, and will experience significant value

appreciation if the gap between peers narrows

Mean 4.0x 4.7x 62,400 82%

– Valuation gap to peers should narrow as Polaris

Median 4.1x 4.9x 71,350 82%

diversifies assets and risk from the San Jacinto

Parex Resources Inc. 4.0x 3.6x 46,400 100% asset decreases

▪ Polaris should trade at less of a discount to peers

% of EV / EBITDA LTM 2021E than non-renewable resource companies as utilities are

Median 97.6% 73.9% more insulated against nationalization danger

EV / EBITDA 2021E ▪ CEO explicitly stated that one of his goals for this

Peer Median PIF Implied Implied year is to increase Polaris' multiple, reducing its

Multiple Multiple Share Price Upside discount to peers

15.6x 11.5x $37.90 107.7%

% Discount to EV / EBITDA 2021E Median

41% 46% 51% 56%

PIF Implied

0% 11.2% 27.1% 43.0%

UpsideThesis III: Valuation Discount to Peers

Asset diversification and debt refinancing are expected to lead to multiple expansion

Multiple Expansion Valuation Summary

▪ Polaris current EV / EBITDA valuation of 15.6x

18.0x $53.80

6.4x is substantially lower than the peer

195%

average of 15.6x 16.0x

▪ There are many catalysts that will enable PIF 11.5x

to achieve multiple expansion and share price 14.0x $37.90

appreciation 107%

12.0x 8.4x

EV / EBITDA 2021E

– Refinancing debt obligations is $25.88

7.4x

expected to increase cash flow by ~ 10.0x $22.00 42%

$15 million annually 6.4x

$18.25 18%

– Diversification into less risky 8.0x 0%

jurisdiction such as Panama will lower

risk associated with San Jacinto 6.0x

▪ Asset diversification and additional cash

4.0x

flows from refinancing will be the key

drivers of multiple expansion for Polaris

2.0x

0.0x

PIF Refinancing Panama Parex Peer Median

Expansion (Implied)VIII Valuation

Valuation: Comps

Polaris’ 59% discount to peers is unjustified given favorable leverage and dividend metrics

Net Debt / Dividend as

Market Enterprise EV/ EBITDA P/E EBITDA Dividend % of Operating

Capitalization Value LTM 2021E LTM 2021E 2021E Yield Cash Flow

Algonquin Power 12,798 19,141 22.0x 13.9x 19.9x 22.9x 3.3x 3.68% 50.0%

Boralex 5,451 8,434 19.1x 16.9x NM 75.5x 5.3x 1.22% 18.0%

Innergex Renewable 5,250 10,034 19.7x 19.6x NM 188.8x 8.6x 2.40% 48.3%

Etrion Corporation 172 218 20.8x 13.0x NM NM 2.2x N/A N/A

Ormat Technologies 6,289 715 20.6x 17.9x 72.0x 69.6x 3.1x 0.41% 8.0%

Transalata Renewables 5,863 6,684 25.5x 14.3x 66.3x 31.6x 1.6x 4.32% 75.0%

Mean 5,970 7,538 21.3x 15.9x 52.7x 77.7x 4.0x 2.4% 39.9%

Median 5,657 7,559 20.7x 15.6x 66.3x 69.6x 3.2x 2.4% 48.3%

Polaris Infrastructure 291 469 6.0x 6.4x 11.2x 19.5x 2.3x 4.3% 21.8%

EV / EBITDA Discount to CA/US EV / EBITDA Discount to Peers

Canada & US 14.6x – Parex Resources 3.6x 26.1%

Latin America 9.7x 33.6% Polaris Infrastructure 6.4x 58.9%

Polaris Infrastructure 6.4x 56.0%

Polaris should trade at a discount to peers given Latin American exposure, however a 60% discount is

unjustified given that other Latin American companies trade at a 33% discount on averageValuation: Discounted Cash Flow

DCF valuation for Polaris indicates a 37.21% upside in the base case

Cash Flow Projection 2021E 2022E 2023E 2024E 2025E Cost of Equity

Net Income 21,813 22,679 34,881 35,735 36,458 Risk Free Rate 1.03%

Add: D&A 25,924 26,424 26,424 26,424 26,424 Equity Risk Premium 7.50%

Less: Cap Ex 30,062 16,312 1,437 1,437 1,437 Levered Beta 0.65

Less: Changes in WC (1,347) (2,069) 775 (2,073) (2,362) Cost of Equity 5.92%

Less: Mandatory Debt Repayments 20,592 14,813 15,759 13,349 12,272

Levered Free Cash Flow (1,570) 20,047 43,334 49,446 51,536 COE 5.92%

PV Levered Free Cash Flow (1,491) 17,160 33,441 34,400 32,323 South America Risk 3.00%

Size Premium 2.00%

Adjusted COE 10.92%

Sensitivity Analysis Equity Value

Adjusted Cost of Equity Final Year EBITDA 36,458

$0.37 8.92% 9.92% 10.92% 11.92% 12.92% Exit Multiple 12.0x

10.0x 30.47% 25.69% 21.13% 16.79% 12.64% Terminal Value 437,502

Exit Multiple

11.0x 39.19% 34.06% 29.17% 24.51% 20.06% PV Terminal Value 274,399

12.0x 47.92% 42.44% 37.21% 32.23% 27.48% Total PV of Projection Period 115,833

13.0x 56.64% 50.81% 45.25% 39.95% 34.90% Equity Value 390,232

14.0x 65.37% 59.19% 53.29% 47.67% 42.31%

Fully Diluted Shares Outstanding 19,000

Share Price $US $20.54

Share Price $C $26.08

Implied Upside 37.21%Valuation: Range

52-Week Low52 -W

– High $8.59 $19.88

Parex Implied Valuation $36.90 $38.90

EV / EBITDA 2021E $36.48 $58.59

P/E NTM $20.88 $68.80

DCF $16.40 $35.33

Current: $19.01 Target: $26.09

$0 $10 $20 $30 $40 $50 $60 $70 $80IX Catalysts

Catalysts

A number of trends and events could drive value appreciation for Polaris

Short-Term

▪ Polaris is expected to refinance existing debt with a more favorable debt package

Debt Refinancing ▪ Refinancing will decrease interest expense and annual amortization dramatically

▪ The refinancing is expected to add ~$15 million to annual cash flow (~10 MW)

▪ Panama acquisition would further diversify operations from Nicaraguan asset reliance

Mid-Term

▪ Previous MOU to acquire Panama assets was extended until June 30, 2021 from

Panama Expansion December 31, 2020

▪ Construction is expected to commence later in the year once Covid-19 cases in

Panama fall

▪ As Polaris continues to scale and increase power generation capacity, it may become an

attractive takeover candidate for large utilities looking to expand into Latin America

Long-Term

Acquisition Target due to its profitability and valuation

▪ Polaris has an existing relationship with Brookfield Renewable Partners

▪ Atlantic Power recently acquired at a 48% premium to market priceCatalysts: Boralex Inc. Case Study

Polaris is in a similar position to Boralex when the company experienced significant multiple expansion

Boralex EV / EBITDA 2012 - 2016

20.0x 20%

EV / EBITDA NTM

15%

% Thermal

16.0x

10%

12.0x

5%

8.0x 0%

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

EV / EBITDA NTM % Thermal

Multiple Expansion

▪ Boralex used to trade below other renewable peers on an EV / EBITDA basis because investors were wary of their thermal assets

▪ Boralex’s multiple increased substantially between 2013-2015 as their thermal assets became a smaller portion of the company’s power

generation capacity

▪ Polaris’ Nicaragua asset currently makes up ~72% of power generation but this is expected to decrease to ~33% by 2025

– Although Polaris is still expected to trade at a discount to peers, decreasing Nicaraguan exposure should result in multiple expansion

▪ In 2013, Boralex had a market capitalization of ~$400 million and was also in the process of refinancing debt for more favorable terms

– Polaris is similar in size to Boralex in 2013, is expecting similar catalysts in the near future and has a much longer track record

with dividend payments than Boralex had in 2013X Risks & Mitigations

Risks & Mitigations

Environmental regulation relaxation and leverage concerns could hamper growth

Risk Mitigation

▪ San Jacinto being the main operating asset ▪ Addition of 5-10 MW Binary unit along with

poses potential expropriation risk by remaining aspects of new PPA contract

Nicaraguan government renewal positions Polaris well with

Nicaraguan government

Single-Asset Risk ▪ Reliance on the San Jacinto plant may also

▪ Geographic expansion across Peru,

increases Polaris’ risk profile with

Panama, and Dominican has, and will

potential unforeseen impacts to the plant continue to, diversify assets

(eg. maintenance, natural disaster)

Risk Mitigation

▪ Potential refinancing can reduce annual debt ▪ Management strongly believes their

servicing costs by up to $15M annually, strength in recent years of meeting credit

allocated towards funding further expansion obligations will translate to an attractive

Inability to refinancing structure

Refinance ▪ The inability to refinance existing debt at

▪ CEO has extensive experience in finance

attractive rates could limit potential future

and led the company through the 2015

growth refinancing

Risk Mitigation

▪ Political instability and autocracy result in ▪ Necessity of electricity regardless of

potential conflict for Polaris across Latin political context indicated margin of safety

America ▪ Utilization of non-depletion resource is

Geopolitical Risks ▪ Expropriation, changing policies and key expropriation mitigation

regulations, political uprising, and regime ▪ Domestic use of Polaris-generated

change are notable potential risks associated electricity indicates codependence

with Latin American operations ▪ Direct investment in local communitiesRecommendation

Buy Polaris (TSE: PIF) at $19.01

Implied Upside: 37.21%XI Appendix

Appendix: Bull Case

DCF valuation for Polaris indicates an 85.86% upside in the bull case

Cash Flow Projection 2021E 2022E 2023E 2024E 2025E Cost of Equity

Net Income 27,217 25,939 38,349 42,358 43,081 Risk Free Rate 1.03%

Add: D&A 25,924 26,674 26,924 26,924 26,924 Equity Risk Premium 7.50%

Less: Cap Ex 30,062 23,812 8,937 1,437 1,437 Levered Beta 0.65

Less: Changes in WC (509) (2,210) 733 (1,033) (3,025) Cost of Equity 5.92%

Less: Mandatory Debt Repayments 20,592 14,813 15,759 13,349 12,272

Levered Free Cash Flow 2,997 16,198 39,843 55,529 59,322 COE 5.92%

PV Levered Free Cash Flow 2,845 13,866 30,747 38,632 37,206 South America Risk 3.00%

Size Premium 2.00%

Adjusted COE 10.92%

Sensitivity Analysis Equity Value

Adjusted Cost of Equity Final Year EBITDA 43,081

$0.86 8.92% 9.92% 10.92% 11.92% 12.92% Exit Multiple 15.0x

13.0x 80.06% 73.30% 66.86% 60.73% 54.88% Terminal Value 646,222

Exit Multiple

14.0x 90.37% 83.20% 76.36% 69.85% 63.64% PV Terminal Value 405,306

15.0x 100.68% 93.09% 85.86% 78.98% 72.41% Total PV of Projection Period 123,296

16.0x 110.99% 102.99% 95.37% 88.10% 81.18% Equity Value 528,602

17.0x 121.30% 112.88% 104.87% 97.23% 89.94%

Fully Diluted Shares Outstanding 19,000

Share Price $US $27.82

Share Price $C $35.33

Implied Upside 85.86%Appendix: Bear Case

DCF valuation for Polaris indicates a 10.15% downside in the bear case

Cash Flow Projection 2021E 2022E 2023E 2024E 2025E Cost of Equity

Net Income 13,642 14,462 22,468 23,322 24,046 Risk Free Rate 1.03%

Add: D&A 25,924 26,424 26,424 26,424 26,424 Equity Risk Premium 7.50%

Less: Cap Ex 30,062 16,312 1,437 1,437 1,437 Levered Beta 0.65

Less: Changes in WC (3,291) (1,762) (215) (1,352) (1,581) Cost of Equity 5.92%

Less: Mandatory Debt Repayments 20,592 14,813 15,759 13,349 12,272

Levered Free Cash Flow (7,796) 11,523 31,912 36,313 38,342 COE 5.92%

PV Levered Free Cash Flow (7,403) 9,863 24,626 25,263 24,048 South America Risk 3.00%

Size Premium 2.00%

Adjusted COE 10.92%

Sensitivity Analysis Equity Value

Adjusted Cost of Equity Final Year EBITDA 24,046

### 8.92% 9.92% 10.92% 11.92% 12.92% Exit Multiple 11.2x

9.2x -18.41% -21.45% -24.35% -27.12% -29.76% Terminal Value 269,312

Exit Multiple

10.2x -12.65% -15.93% -19.05% -22.03% -24.87% PV Terminal Value 168,911

11.2x -6.90% -10.40% -13.75% -16.93% -19.97% Total PV of Projection Period 76,398

12.2x -1.14% -4.88% -8.44% -11.84% -15.08% Equity Value 245,309

13.2x 4.61% 0.64% -3.14% -6.75% -10.19%

Fully Diluted Shares Outstanding 19,000

Share Price $US $12.91

Share Price $C $16.40

Implied Upside -13.75%2020 Debt Refinancing

Strong credit fundamentals and a recent refinancing have reduced risk significantly

Details from Refinancing Historical Debt Highlights

▪ On June 5th 2020, Andean Power Generation, a wholly owned ▪ Using proceeds from the refinancing, PIF repaid the

subsidiary of PIF, obtained debt financing of $27 M from Canchayllo credit facility

Brookfield Asset Management in order to refinance the

Canchayllo credit facility, an existing term loan – The company now no longer holds debt maturing

– The original loan, maturing in March 2025, carried an before 2024

interest rate ranging from 5.38% to 8.65%; The new loan

carries an 8.75% interest rate and matures in June 2028 ▪ PIF’s Debt/EBITDA is in line with peers and has

fluctuated between 3.0x and 4.0x since 2016

– The terms of the loan give Brookfield a 1st priority lien on

PIF’s Canchayllo project and a 2nd priority lien on the El ▪ Low interest rates may improve funds from operations

Carmen and 8 de Agosto projects (FFO) further by encouraging refinancing in the future

FFO/Debt Steadily Increasing Asset Coverage Remains High Post-Restructuring

30% 300%

25% 233% 241% 238% 238% 236%

250%

20%

200%

15%

150%

10%

5% 100%

0% 50%

2016 2017 2018 2019

0%

PIF Industry Average 2016 2017 2018 2019 2020

Source: S&P Global2015 Restructuring

Prior to 2015 the company was known as Ram Power until bankruptcy forced them to restructure as Polaris

Infrastructure

Details from Restructuring Underlying Cause and Future Mitigation

▪ In Q2 of 2015, Ram Power filed for bankruptcy and

▪ The reason they were distressed is because initial drilling

restructured as Polaris Infrastructure due to overwhelming

did not go well and they were unable to produce the

debt

needed cash flow to service interest payments, but that

– They engaged in a private placement, raising $74M, should not be a problem now that the Nicaragua asset is

and converted senior secured debentures into $53M stable

of shares

– The company has since grown significantly and has

– Adjusted terms on outstanding credit to pay down other cash producing assets

debt on better terms - Senior loans with rates of

▪ Polaris's debt coverage is now 23.3% of operating income

6.5% were reduced to 1.5% and maturity dates have

which poses a significantly lower liquidity risk

been extended

Interest Expense/EBIT Through Restructuring Debt Maturity Schedule

600% 5 Years

200% 48%

100%

0%

2013 2014 2015 2016 2017 2018 2019 3-5 Years

28%

Source: Polaris Investor RelationsOwnership Structure

Insider ownership by CEO aligns incentives with shareholders

Shareholder Overview Ownership Summary

% of Shares Market Value

Outstanding (CAD mm) Institutions

18.4%

Insiders

Murnaghan, Marc (CEO & Director) 2.4% 7.1 Individuals/Insiders

Lawless, James (Independent Director) – 0.1 2.4% 15.7 mm

Total Insiders 2.4% 7.2 Shares

Traditional Investment Managers Outstanding

Dimensional Fund Advisors L.P. 4.2% 12.3

AGF Management Limited (TSX:AGF.B) 2.4% 7.0 Public and Other

PenderFund Capital Management Ltd. 1.7% 5.0 79.2%

Jarislowsky, Fraser Limited 1.4% 4.2

Erste Asset Management GmbH 1.4% 4.0

CIBC Asset Management Inc. 1.1% 3.1 Commentary

1832 Asset Management L.P. 0.9% 2.7

QS Investors LLC 0.7% 1.9

Other Traditional Investment Managers 3.6% 10.8 ▪ While insiders only own 2.4% of shares outstanding, the

Total Traditional Investment Managers 17.8% 52.0 lean organizational structure aligns management incentives

Hedge Fund Managers with common stockholders

Hillsdale Investment Management Inc. 0.4% 1.1 ▪ Sizeable investments from institutional owners instills

Goodwood Inc. 0.1% 0.3

confidence that PIF is a strong business

Arrow Capital Management Inc. 0.1% 0.3

Total Hedge Fund Managers 0.6% 1.7 ▪ Diversified shareholder base ensures that large investors

Other Investors will not be able to engage in undesirable behavior at the

Starlight Investments Capital LP (REIT) 0.6% 1.7 expense of minority owners

Retail & Other Investors 78.6% 228.9

Total Other Investors 79.2% 230.6

Sources: CapitalIQOwnership Structure

PIF is similar in structure to other renewable energy companies on the TSX

Short Interest (% of Shares Outstanding)

4.0%

3.2%

2.4%

1.6%

0.8%

0.0%

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20 Jan-21

Comparable Ownership Structure Commentary

100.0% ▪ Investors have lately been shorting PIF at increasing levels,

which is typically a bearish sign, though interest as % of

80.0%

Insiders shares outstanding remains low

60.0% Corporations ▪ The past two years did not see much insider trading activity

40.0% Institutions ▪ Other renewable companies on the TSX also have low

20.0% Public insider ownership levels indicating immaterial concern

0.0%

PIF NPI INE BLX TA

Sources: CapitalIQ, ShortDataInstitutional Investors Dividend Payments

Largely Institutionally Held Small and Micro Cap P&U Stocks (>50% Institutional)

140 129 132 129

Consecutive Dividend Payments 120

104

100

80

60

40

25

20 15

0

0

• Sources: Finwiz, Yahoo Finance

• *Atlantic Power Corporation has dividend history previous to 2015, however has not paid dividends sinceExecutive Team

Polaris Infrastructure is supported by an experience management team

• 20 years of experience within senior investment banking roles where he ran the Power and

Mark Muraghan Alternative Energy groups

• Helped raise capital for companies in the solar, wind, hydro, geothermal, biomass, power

Chief Executive Officer electronics, battery technologies, and fuel cell sectors

• 25 years of experience within equity investments, project finance, project development,

and commercial contract negotiations, and company operations

Jaime Guillen • Experiences within energy, transportation, and natural resource industries

Chairman of the Board • Currently serves on the the investment and asset management committees of the various

energy and infrastructure funds in Latin America managed by Polaris’ affiliates

James V. Lawless • 30 years of experience within the geology and geothermal industry

• Holds previous experience with company’s San Jacinto power product through oversight

Director of drilling activities

Alexis Osorno • Previously a Finance Manager at Puma Energy Nicaragua for a period of 3 years before

joining Polaris Energy Nicaragua, S.A (PENSA)

Regional Manager • Supervises the businesses in both the Peruvian subsidiary, Polaris Energy Peru; as well as

(Nicaragua) the operations of the Nicaraguan subsidiary, PENSA

Source: Capital IQCall with Polaris CEO Marc Murnaghan

Annotated Stock Chart

PIF’s stock has grown 405% over the past five years while proving resilient to the COVID-19 pandemic

$25 2,500K

$20 2,000K

5

$15 2 1,500K

4

3

$10 1,000K

1

$5 500K

0 0

Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18 Jan-19 Jul-19 Jan-20 Jul-20 Jan-21

1 Board of directors declares the first quarterly dividend of $0.10 USD per common share outstanding

2 Protests against reforms decreed by President Ortega that increased taxes and decreased benefits sparked a regional sell-off

3 PIF completes acquisition of Union Energy Group, a developer of three run-of-river hydroelectricity projects located in Peru

4 Private placement offering of $25,000,000 7% senior unsecured convertible debentures announced

5 Global market correction from the COVID-19 pandemic as countries enter lockdown

Sources: CapitalIQ, BloombergCurrent Project Overview

PIF currently operates a Geothermal Plant in Nicaragua and three Hydroelectric Run-of-River (ROR) Power Plants in Peru

San Jacinto-Tizate Geothermal Plant Canchayllo Hydroelectric Power Plant

▪ Operating since 2013 in San Jacinto, Nicaragua. ▪ Operating since 2015 in Canchayllo, Peru.

▪ Second largest geothermal energy generator in Nicaragua. ▪ Installed capacity 5MW Run-of-River hydro facility.

▪ Current steam can result in power capacity of ▪ 20-Year Power Purchase Agreement approved by

approximately 68-72 MW. government – US $47.40 / Mwhr.

▪ Generation license signed in 2013, allowing for the ▪ Transmission line is connected to the existing transmission

generation of 62MW net of the project for a period of 30 line of Oroya Nueva-Chumpe.

years.

8 de Agosto Hydroelectric Power Plant El Carmen Hydroelectric Power Plant

▪ Operating since December 2019 in Aucantagua, Peru. ▪ Operating since November 2019 in Maravillas, Peru.

▪ Installed capacity 20MW Run-of-River hydro facility. ▪ Installed capacity 8MW Run-of-River hydro facility.

▪ 20-Year Power Purchase Agreement - US $53.90 / Mwhr. ▪ 20-Year Power Purchase Agreement – US $55.70 / Mwhr.

▪ Substation receives the interconnection lines from 8 de ▪ Substation receives the interconnection lines from El

Agosto and the outgoing 138 kV transmission lines to the Carmen and the outgoing 138 kV transmission lines to the

Tingo Maria substation. Tingo Maria substation.

▪ Connected to the national grid. ▪ Connected to the national grid.

Sources: Polaris Infrastructure, Polaris Energy Nicaragua, Corporate PresentationGrowth Strategy Overview

Diversification Strategy (MW Capacity)

300

250

200

150

100

50

0

2019 2020 2021 2022 2023 2024

Nicaragua Peru Panama Other

Geography Generation Type Size Stage Capital Required Estimated IRR

Nicaragua Geothermal 5-10 MW Construction $15 - $20 M +20%

Panama Hydro 10 MW Construction $15 - $20 M 15%

Peru Hydro 20 MW Operating $15 M 8 – 10%

Dominican Solar 32 + 20 MW Operating + Expansion $15 - $20 M –

Panama Hydro 14 MW Operating $10 M 8 – 10%

Panama Solar 10 MW Greenfield $10M 12%

Peru Hydro 80 MW Greenfield NA 15%

Several Diversified >100 MW Operating + Expansion 10 - 12%

Source: Investor PesentationWorld Bank Commitment

Nicaragua’s dependence on World Bank financing further deters expropriation against Polaris

World Bank Commitments to Nicaragua

250

195

200

$US Millions

145

150

100

50 20

0 0

0

2017 2018 2019 2020 2021E

World Bank Mitigation

▪ World Bank funding to Nicaragua was cut off in 2018 in response to President Ortega’s actions against civilians in Nicaragua

▪ The World Bank has pledged $20 million to Nicaragua to help fight the Covid-19 pandemic

▪ Reliance on funding from the World Bank should deter President Ortega from any hostile actions such as expropriation that may

jeopardize the loan or any other future financial commitments

Source: World BankEnergy Processes: Geothermal

Geothermal Energy Process

Injection Wells Heat Extraction Energy Conversion Generator Conversion

Hot high-pressure brine Steam passes through a Generator converts this

Injection wells drilled into solution travels up the well turbine causing it to spin, mechanical energy into

earth at depths with hot to the surface, where it converting steam to electrical energy, and now

temperature, hot brine heats a different solution mechanical energy which cooled brine is returned

injected through wells quickly creating high- travels to a generator via a below earth’s surface via

pressure steam shaft injection wells

Injection Wells Brine Solution Heat Energy Spins Mechanical to

Drilled Extracts Heat Turbine Electrical ConversionEnergy Processes: Hydroelectric

Hydroelectric Energy Process

Partial Diversion Turbine Conversion Transportation Generator Conversion

As water flows down the

Partial stream from Generator converts this

pipeline, it passes through a Shaft connected to the

naturally-occurring river is mechanical energy into

turbine causing it to spin, spinning turbine sends this

diverted from traditional electrical energy, and the

converting the flowing mechanical energy up to a

flow through man-made generator water is returned to the

water’s energy into

pipeline river downstream

mechanical energy

Partial Stream is Water Spins Transport to Water returned

Diverted Turbine Generator downstreamEnergy Processes: Solar

Solar Energy Process

Direct Sunlight Energy Capture Initial Conversion Secondary Conversion

Photovoltaic cells absorb The electricity, currently in

Loose electrons are then direct current form, is then

Solar panels constructed sunlight, which consists of

captured by conductive metals

with numerous silicon-alloy photons that knock converted to usable

thus creating a flow of

cells electrons loose within the electrons & electrical current alternating current using an

silicon-alloys of the cell alternator

Solar Panels Collect Cells in Panels Retain Energy Converted to Conversion to Usable

Sunlight Light Energy Electrical Current EnergyPeru – Political & Economic Context

Recent political instability has not hampered economic growth

Peruvian Political Crisis Fewer Peruvians Facing Extreme Poverty

▪ Peru is currently in the midst of a period of political 20%

instability primarily due to corruption

15%

– The country saw six presidents over the course of

the last decade; a general election has been scheduled 10%

for April 2021

5%

▪ Political turmoil has not hindered long-term economic

prosperity significantly as evidenced by a rapidly-growing

0%

middle class 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Current Leadership Gini Coefficient Steadily Falling

▪ Francisco Sagasti and Violeta Bermúdez were appointed 0.46

President and Prime Minister of Peru respectively on

November 17th, 2020 0.45

▪ Although the two elected officials are ineligible for re-

0.44

election, Sagasti has intentions to “leave the next

government with a clear idea…to replace fossil fuels with

0.43

different renewable forms of energy”

▪ Parliament is divided with no party receiving more than 0.42

11% of the vote in 2020 parliamentary election 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: World BankPeru – Renewable Energy Policies

Numerous tax incentives have successfully attracted renewable energy investments in Peru

Renewable Energy Generation Capacity (MW) Accelerated Depreciation Regime

7,000 ▪ Corporate income tax incentive designed to stimulate

6,000 investment

5,000 ▪ Under Legislative Decree No. 1058 passed in June 2008,

4,000 equipment associated with the installation and operation of

renewable energy generation are subject to a 20% maximum

3,000

annual rate of depreciation

2,000

▪ Renewable energy and mining are the only industries with this

1,000 depreciation regime; all other fixed assets are limited to a

0 maximum 10% rate of depreciation

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Benefits Associated With Geothermal Resources Early Recovery of the Input VAT

▪ The import of any goods used to exploit geothermal ▪ Value added tax (VAT) is a monthly tax levied on the sale

resources are exempt from all existing taxes or importation of goods as well as construction contracts

▪ As of 2019, all geothermal concession holders are subject ▪ During the pre-operative stage, renewable energy

to a 26% corporate income tax rate, compared to the companies are entitled to recover the VAT associated with

standard 29.5% tax rate for other Peruvian businesses the import, acquisition or construction of assets

▪ Geothermal concession holders with multiple contracts are ▪ These companies must also receive approval from the

permitted to use losses–if one contract generates tax losses Ministry of Energy and Mines and commit to a minimum

that carry forward–to offset taxes from another contract $5 M USD investment

Source: PwC, KPMGPanama – Political & Economic Context

Panama remains a leader in free trade, a key driving force behind its economic prosperity

Overview Leader In Free Trade

▪ Panama’s service-based economy is expected to contract in ▪ The comparative advantage created by Panama’s

2020, but is projected to rebound quickly geographical location, the Panama Canal and numerous

– Estimates range from 4 – 5% GDP growth in 2021 free trade agreements have made the country a key player

in global trade

– Since 2001, Panama’s GDP has grown at a rate more

than double the regional average ▪ The Panamanian Balboa is pegged at 1:1 to the US Dollar,

▪ Panamanian companies have enjoyed tax-exempt status on providing long-term stability for the country’s economy

foreign income since the mid 20th century; today Panama is ▪ Trade liberalization has viewed favorably by Panamanian

a notable tax haven leadership since 1994

National Income (USD) Per Capita Growth Projected Electricity Consumption Per Capita

16,000 2,600

14,000 2,400

Consumption (kWh)

12,000 2,200

10,000 2,000

8,000 1,800

6,000 1,600

4,000 1,400

2,000 1,200

0 1,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Sources: International Monetary Fund, World BankPanama – Renewable Energy Policies

An optimistic national energy plan is supported by tax exemptions, reverse auctions and other policies

Panama’s National Energy Plan Countless Tax Exemptions

99.3%

100%

85.0% ▪ Renewable energy projects generating up to 0.5 MW

80% 70.0% receive VAT and import tax exemptions

60% ▪ Projects generating up to 20 MW receive exemptions from

transmission and distribution taxes on their first 10 MW

40% 30.0%

20%

15.0% ▪ Wind power generation equipment manufacturers are

0.7% exempt from paying all national taxes for 15 years

0%

2010 2030 2050 ▪ All biomass power generation companies receive full

Renewable Non-renewable income tax exemption

Reverse Auctions For Solar Energy Other Policies

▪ Under Panamanian law, distribution companies must have Ethanol Blending Mandates

100% of their demand contracted for the next two years

▪ The country adopted an E2 mandate in 2013 and steadily

with additional lighter restrictions beyond the second year

increased its ethanol content, ultimately introducing an E10

▪ Solar energy supply is acquired by the government through mandate in 2016

reverse auctions in which developers place bids to secure

up to 20-year power purchase agreements (PPAs) Net Metering

▪ Law 37 of 2013 states that all solar power generation ▪ In June 2012, net metering for all renewable energy

facilities are exempt from all import taxes on equipment systems was established under Resolution 5399

used in the maintenance and installation of plants

Sources: International Energy Agency, International Energy Charter, Global Environment FacilitySelect Geographic Electricity Generation and Demand

% Change

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

1995 2000 2005 2010 2015 2018

Panama Demand Panama Capacity Peru Demand Peru Capacity N.A Demand N.A CapacityPeru Supply and Demand

70

60 57 59

56

49

50

40

30

20

10

0

2018 2021

Peru Demand Peru GenerationCharity Outreach: Polaris Infrastructure

PIF has completed two CSR projects in Telica, León, Nicaragua.

San Jacinto-Tizate Community Water Rehabilitation Project

▪ Provided quality water to the community of Telica, León.

▪ US $1.2 million investment co-financed by Polaris Energy Nicaragua, S.A. (PENSA), the Inter-American Development Bank, the

Development Bank of Austria, and NGO Catholic Relief Services.

▪ Gave priority to water supply, sanitation, hygiene, and community organization.

▪ Increased access to quality water for communities, ensured access to quality water and sanitation for local schools, and improved the

sanitary conditions of the San Jacinto health post.

▪ Beneficiaries for 915 homes, 4,575 people, and 949 students.

“Learning Today, Shining Tomorrow” Program

▪ Beneficiaries for over 800 students in Telica, León.

▪ Partnership with World Vision Nicaragua for educational support in pre-school, primary school, and secondary schools.

▪ Provided accompaniment from for students of the Sara María Parrales School Core and its five satellite schools (El Chorro, San Pío,

El Listón, and Los Salgados)

▪ Equipped schools with technological tools for integral learning.

Sources: PolarisYou can also read