OUTLOOK 2023 INVESTMENT STRATEGY GROUP - JANNEY MONTGOMERY SCOTT LLC Published: December 15, 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INVESTMENT STRATEGY GROUP

OUTLOOK 2023

JANNEY MONTGOMERY SCOTT LLC

Published: December 15, 2022

TWO-WAY RISK The economy continues to move in a positive fashion even as its cadence stutters at times. The strength of the labor market and the abundant level of savings still held by households provide an impulse for spending—a key driver of domestic activity. However, high inflation and the Federal Reserve’s efforts to thwart its harmful impact have significantly raised the probability of a recession occurring in the coming year. There is the possibility of things going much better than expected, or much worse. In our outlook for 2023, we present the challenges and opportunities that come with this two-way risk.

I N V E S T M E N T S T R AT E G Y G R O U P

OUTLOOK 2023

OVERVIEW

Outlook 2023 offers the Janney Investment Strategy Group’s baseline forecasts for the economy and equity and fixed income

markets in the coming year.

Economy & Equity Markets............................................................................................................................................... Page: 4

• The economy slips into a shallow recession around midyear. While the unemployment rate rises, the labor market

remains sufficiently strong to support consumption.

• Corporate profits may decline marginally year-over-year, which will keep stock prices from advancing in a sustainable

manner until later in the year.

• Commodities, particularly oil and industrial metals, could rise given that tight supplies will underpin prices. The prospects

improve exponentially if China relaxes its stringent COVID measures.

• Evolving geopolitical tensions emanating from relations with Iran and the war in Ukraine, while not an imminent threat,

can emerge as fissures that impart exogenous volatility at any time.

Fixed Income & Interest Rates........................................................................................................................................ Page: 10

• Inflation should decelerate in 2023, but it will likely remain too high for policymakers to quickly cut interest rates as they

have in past downturns.

• For bond markets, the probable outcome is a deeply inverted yield curve with short-term interest rates holding well

above long-term rates, despite economic slowing.

• Although it is tempting to buy shorter-term bonds at higher yields, we see better value in the range of maturities from

five to 10 years—an area where investors can lock in yields for longer.

• Credit fundamentals are unusually solid at this point in the cycle, but we believe an up-in-quality bias will perform better

in the face of a probable economic contraction.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 3 OF 13

ECONOMY & EQUITY MARKETS

The U.S. economy may flirt with, or encounter, a recession in 2023. The evolution of that

development will likely keep markets volatile until data offer certainty. The signals from

many leading indicators that have been prescient in forecasting a measured economic

contraction portray a gestalt that a downturn is developing.

The lack of excesses in private sector Chart 1: US GDP

leverage, or indebtedness, that typically

precede more severe or protracted recessions

MARK LUSCHINI, CMT gives us reason to believe that if a recession

Chief Investment Strategist

is encountered, it should be relatively mild

President and Chief and brief. If that is the case, financial market

Investment Officer, Janney participants’ fears will be eased.

Capital Management

Mark Luschini serves as

If a recession is avoided because inflation

Janney’s Chief Investment dissipates soon, thereby allowing the

Strategist and leads the Federal Reserve to curb its need to deeply

Investment Strategy Group, tighten policy and restrict economic activity,

which sets the firm’s view on markets would likely inflect bullishly. On (Source: Janney ISG, US Bureau of Economic Analysis)

macroeconomics, as well as

the other hand, if the pace of inflation fails

the equity and fixed income

markets. In addition, Mark to moderate, which further emboldens the the National Bureau of Economic Research

is the President and Chief Fed’s resolve to slay it, the recession that (NBER). They define a recession more

Investment Officer of Janney could ensue may be deeper and lengthier qualitatively and include measures of job

Capital Management (JCM), in nature. In that scenario, financial markets growth, income, and business activity. By that

the asset management may suffer a significant de-rating from measure, a recession has yet to occur (not

subsidiary of Janney

Montgomery Scott. Under current levels. at least since the historically brief one that

his leadership, JCM has lasted two months in 2020) and for as much

delivered competitive results

Investors should be aware of the potential as advertised by pundits and the media,

across its suite of investment conditions that could stem from these one need not be inevitable. Much depends

strategies and grown its different scenarios. on the evolution of inflation and the Fed’s

assets under management

to more than $3.5 billion.

response to it. While perhaps low odds, a

U.S. recession could be avoided if the fever pitch

Mark has spent more than

of inflation breaks hard and quickly.

thirty years in the investment The economy is ending 2022 with a rate

industry. He draws on that of growth that is accelerating from the more Indeed, the economy continues to post

experience to speak on topics tepid pace seen during the year’s first half.

related to macroeconomics

activity that remains quite healthy even as

and the financial markets at After posting two consecutive quarters of there are fissures starting to emerge that

seminars, client events and negative growth (defined by the quarterly foreshadow a slowdown or worse in 2023.

conferences. He is frequently report of the annualized pace of the gross While the monthly report on employment is

quoted in publications domestic product, or GDP), the economy a lagging indicator, it does offer some insight

ranging from the Wall Street expanded at almost a 3% pace in the third into the economy’s momentum. The most

Journal and Barron’s to

the New York Times and

quarter and real-time data for the fourth recent release from the U.S. Bureau of Labor

USA Today. In addition, he quarter indicate a nearly similar tempo. Statistics (BLS) showed job gains in excess

regularly appears in various of 250,000 in the month of November,

media outlets including While the blunt definition of a recession

and that was sufficient to maintain the

CNBC, Fox Business News, being two consecutive quarters of negative

unemployment rate at 3.7%—near its

and Bloomberg Television economic activity was met earlier in 2022,

and Radio. He has an historic low. It is estimated that there needs

that was somewhat misleading as it had

undergraduate degree in to be about 100,000 new jobs created

more to do with trade flows and inventory

Psychology and an MBA each month in order to account for those

in Finance from Gannon destocking than it did with the underlying

entering the workforce for the first time, so

University and holds the and all-important support that comes from

the recent pace of job creation has been

Chartered Market Technician consumer spending. Examining those first

more than enough to absorb new entrants

(CMT) designation from two quarters’ figures, private consumption

the Market Technicians to the workforce, as well as those who are

was positive throughout and remains so. The

Association. marginally attached.

unofficial arbiter of declaring a recession is

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 4 OF 13

Chart 2: US Unemployment Rate Chart 4: JOLTS

(Source: Janney ISG, Bloomberg) (Source: Janney ISG, US Bureau of Labor Statistics)

The pace of job creation also helps contain the rise in the Occam’s Razor is the problem-solving principle of distilling

U.S. Department of Labor’s weekly jobless claims, a leading complex or multiple theories into fewer or simpler

indicator for the state of labor conditions. Unemployment explanations. The U.S. economy is complex and dynamic.

insurance claims have been creeping higher lately, as an However, its growth is driven by consumer spending

increasing number of companies—including those in the that accounts for almost 70% of its ongoing impulse. To

tech and mortgage industries—have announced layoffs oversimplify, get the consumer right and you will get the

due to overly rapid hiring or the impact of the dramatic economy right. The litmus test taken of the consumer, in our

decline in housing activity. Still, those insurance claims as a view, suggests consumers in aggregate are in quite good

percentage of the total U.S. labor force continues to plumb shape. Along with jobs, income growth has been robust,

all-time lows. Also, continuing claims—a count of those who with the latter showing gains of around 5% on average

have been receiving benefits for weeks—are rising but weekly earnings reported from the U.S. Bureau of Economic

slowly implying that jobs are being found and taken fairly Analysis (BEA). Even better, the Atlanta Federal Reserve’s

quickly by displaced workers. Wage Growth Tracker, which is the median percent change

Chart 3: US Initial Jobless Claims in the hourly wage of individuals observed 12 months apart,

is annualizing near a multidecade high north of 6%.

Chart 5: US Personal Income

(Source: Janney ISG, US Department of Labor)

Another indication of the strength of the labor market can (Source: Janney ISG, US Bureau of Economic Analysis)

be surveyed via the monthly JOLTS (Job Openings and

Labor Turnover Survey) report issued by the BLS. Among In addition, consumer bank accounts remain well stocked.

other things, probably the most-watched component is The abundance of savings that accumulated during the

the number of job openings available, especially as it pandemic because of deferred spending and/or fiscal

compares to the number of those unemployed. Today, transfer payments, stands north of $1 trillion. Of course, this

there are more than 10 million unfilled jobs and given the accrued to all income cohorts, but it is those with incomes

total of unemployment at roughly a level of 6 million, the that are amongst the lowest quintile of earners that have

job-openings-to-unemployed ratio is approximately 1.7, near largely used those savings for any number of reasons,

its record high. Once again, this a good sign for job stability including combating the deleterious effects of rampant

and all that comes with it including its residual impact on inflation on their discretionary income.

consumer confidence and consumption.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 5 OF 13

Yet, roughly 90% of spending comes from those in the top activity, and the National Association of Home Builders

four quintiles, so there remains a considerable amount (NAHB) index reflects the collective sentiment of

of horsepower available to drive consumption, and thus homebuilders as they see activity such as completed

economic activity. Together, jobs and income, as well homes selling and the traffic touring their showrooms.

as a healthy consumer balance sheet, form a formidable Together, these offer insight into prospects for the

foundation upon which consumer-driven activity can housing industry, which is sensitive to interest rates

produce a positive impulse to propel growth going forward. and thus a de-facto proxy for financial conditions.

However, not all is well. The housing market has been The Conference Board’s monthly Leading Economic

on its heels for months. The sharp spike in mortgage Index (LEI) is a widely followed gauge consisting of

rates, basically doubling from the low of around 3.5% 10 components that are viewed as forward-looking

on a standard 30-year note of a year ago until falling indicators of economic activity. Among them are

back below 7% more recently, caused massive sticker credit conditions, the stock market, new orders for

shock for homebuyers. Housing is important because no manufacturing, and consumer expectations. Its utility for

other industry has a similar multiplier effect. The activity signaling the state of the economy in the future is robust.

associated with housing, from residential construction Over the last 50 years, if the LEI went negative on a year-

to labor and materials from suppliers, financial services, over-year basis, a recession usually followed within 12

furnishings, and so on, radiates throughout the economy. months on average. The first negative print occurred in

July 2022 and subsequent months have seen the number

Chart 6: US Housing - Building Permits

deepen further.

The LEI is not infallible—it has had a false positive

in the past. However, the index and other variables,

including the Fed’s current exercise to tighten monetary

policy to help slay inflation, serve as signposts for a

looming recession.

Although monetary officials could swiftly adopt a softer

policy stance if they deemed inflation tamed, and try

to manipulate rates to avoid a recession, their dubious

record under previous regimes suggests the odds

are exceedingly low. In fact, not dissimilar to the LEI’s

predictive value, historically once the Fed raises its

overnight interest rate, a.k.a. the federal funds rate, to a

(Source: Janney ISG, US Census Bureau)

level that is considered tight and slows economic activity,

a recession often ensues in about 12 months. By the

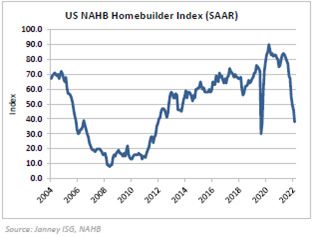

Leading indicators from the housing market are often a Fed’s own measures, interest rates have been restrictive

tell on the broader economy. Two preferred measures for growth since September.

are building permits and homebuilder sentiment. Both Chart 8: US Leading Economic Index (LEI)

have had the propensity to turn in advance of broader

economic activity that follows. Building permits are useful

because they are an indication of future construction

Chart 7: US NAHB Homebuilder Index (SAAR)

(Source: Janney ISG, Conference Board)

It is likely inflation will dissipate over the next year.

Evidence is mounting that supply-chain distortions are

clearing, which accounted for some of the stiff price

(Source: Janney ISG, National Association of Home Builders)

increases that have occurred. Surveys across many

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 6 OF 13industries show shrinking delivery times and the prices INTERNATIONAL

paid for feedstock have fallen precipitously. That should

help shrivel the pass-through to the consumer. Per usual, our primary focus on non-U.S. activity is China.

As the second-largest economy on earth, China’s yearly

Goods prices, which represent less than a third of the growth impulse accounts for more than a fifth of the world’s

Consumer Price Index (CPI), have been deflating for annual GDP. Slowing global growth has weighed heavily

months, relieving a pressure point for overall pricing. on China, which is to be expected given its exports are

The goods category includes items such as computer now close to contracting. Meanwhile, Chinese imports—

equipment, TVs, and furniture. On the other hand, services, a reflection of the country’s fragile property market and

which represent more than two-thirds of the CPI calculation, inhibited consumer—have collapsed. Chinese officials have

have moderated some but are still rising. A contributing instituted myriad, albeit so far timid, stimulus measures this

factor to that is cost of shelter. While price gains in the year and had a marginal impact on stabilizing growth so far,

housing and rental market have begun to ebb, the feed falling short of President Xi’s target of 5.5%.

into the CPI formula operates with a lag of about one year.

Therefore, it will take some time for lower shelter costs to As such, we do not believe that an economic recovery

contribute to lowering inflation readings. in China is likely within the next few months. Certainly,

we expect Chinese policymakers to ease policies further

The risk is that services inflation, which beyond shelter in 2023 to support the economy, but it remains unclear

includes wages across industries such as travel, leisure, whether these policies will merely firm economic activity

and entertainment, remains sticky. After all, one only at middling levels or whether they will cause a significant

has to drive down a commercialized street to see an acceleration in growth. Speculation about China’s

abundance of “Now Hiring” signs posted outside of any relaxation of its dynamic zero-COVID policy is rampant, but

number of enterprises. this will not likely unfold in a meaningful way until the spring

despite ongoing protests in China. Improved vaccination

If services inflation fails to abate, this will likely reinforce the efforts are necessary to ease COVID restrictions. When

resolve of monetary officials to raise rates and hold them at these efforts are successful, the growth prospects for

a sufficiently restrictive level for long enough to stamp out China should rise and the feedback loop to Europe and

inflation and quell consumer expectations of it. The price other developing countries could be pronounced.

to be paid, however, is likely to be a recession perhaps

midyear 2023. While it may not be as severe as those of Chart 9: Chinese GDP

other Fed-induced contractions, unemployment is likely to

rise, nonetheless. Historically, once unemployment rises

by more than 0.5% it usually doesn’t stop there. Indeed,

the Fed’s own forecast calls for the unemployment rate

to reach the mid-4% level next year. That is certainly not

welcome news, and it could cause consumers to retrench

if sentiment erodes. Watching retail sales activity, which has

been remarkably vigorous, will be critical to ascertain if any

negative feedback from rising unemployment is infiltrating

consumer behavior.

A further support for the labor market, even if the

economy slows and businesses adopt a margin-saving

posture, is the scarcity of labor. Businesses could be

reluctant to shed many jobs during a recession because (Source: Janney ISG, National Bureau of Statistics of China)

of fear that the eventual re-hiring effort might be too

costly. The best case would be for the labor markets to Even then, by all accounts President Xi is shifting China toward

loosen, thus softening demand, by reducing the unfilled a more nationalistic state. In his speeches to the Communist

job openings (shown in JOLTS) that exist without trampling Party Congress, Xi’s comments about national security

on the ranks of the employed. That again is plausible, eclipsed those about the economy, market, and reforms,

but unlikely. Having said that, given the current strength underscoring that Chinese policy continues to gravitate

of the labor market, the lack of excess leverage in the toward self-reliance. This could raise tensions in the coming

private sector, the well-endowed state of the consumer, years among allies and adversaries as to where allegiances

and prospects that we could be nearer to the nadir of lie regarding trade, financial support via China’s Belt and

the weakening global backdrop (barring an unforeseen Road Initiative, and military cooperation. A more positive

spark of geopolitical agitation from Eastern Europe, view towards the Chinese economy may be warranted when

Iran, or China), we expect better economic conditions to the second half of 2023 approaches, but only in response

ultimately prevail once past the relatively mild and brief to tangible evidence of a growth catalyst. For now, we urge

downturn we envision for next year. a cautious stance towards China-related investments.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 7 OF 13The European economy is facing stronger near-term financial market volatility it can unpredictably induce, is a

headwinds than the U.S. economy. The manufacturing and constant threat. While the conflicts mentioned do not as

services sectors are slowing, beset by a massive decline of yet have clear resolutions, there are paths to reduce

in European real wages and a substantial terms-of-trade tensions depending on how they evolve. From a geopolitical

shock precipitated by high energy prices. The decline in risk perspective, it’s a challenge to design an actionable step

real wages means that consumption in the euro area will to be taken except to raise awareness that these “known

likely be weak, and the profitability impact of a sharp rise in unknowns,” as coined by the late Donald Rumsfeld, lurk in

euro-area energy costs will also likely hamper employment the macroeconomic sphere of risks.

growth. In the chart that follows, the Organisation for

Economic Co-operation and Development’s (OECD) INVESTMENT IMPLICATIONS

leading economic indicator for the euro area is falling,

suggesting an uptick in the prospects for growth has yet The following outline demonstrates how we would express

to materialize. our central thesis that the U.S. economy will experience a

recession, but one that is neither severe nor protracted,

Chart 10: OECD Euro Area Composite Leading Indicators

yet nonetheless causes demand to slip as unemployment

rises and inflation to subside. We also assume the Fed’s

narrative will move toward lowering rates, but not actually

do so until late into the year or into 2024. In our opinion, this

suggests that even as growth recovers, it will be slow before

accelerating when monetary officials begin to taper rates.

Overseas, the growth driver will be hinged off China’s

successful application of COVID vaccinations and

treatments, which would allow its economy to reopen

more fully. If, and as that happens, many European and

emerging-market countries will benefit from the increased

trade flow they depend on with China. This could lead to a

shift in equity capital toward international equities, where

valuations are far more compelling than in the U.S., and

(Source: Janney ISG, Organisation for Economic Co-operation and Development) the potential returns are greater should risk premiums in

foreign markets fall as global uncertainty recedes. It should

That said, Europe may have scope to outperform the also reboot the rally in commodity prices that has been

grim prognosis many pundits offer for it. A stabilization underway since fall 2020, but stalled recently as worries

of the European energy market is essential for euro- about global demand propagated markets.

area consumption to improve and news on that front is

• G

lobal Equity Markets – U.S. equities may struggle early

encouraging. European economies are switching their

in the year, as slowing nominal growth and rising costs

mix away from natural gas toward less-costly forms of

weigh on profit margins. As the economy pushes through

energy. France’s nuclear electricity generation should

the downturn, the earnings picture should brighten and

improve next year, subsidizing the need for fossil fuels,

foster a better foundation for stocks to advance. Many

and the fiscal policy backdrop is also supportive by way

foreign markets are more cyclical in nature and have

of the various programs implemented across Europe

fared worse than U.S. stocks. As global activity stabilizes,

to contend with the energy situation. This does not

boosted by a stimulus-induced improvement in China’s

completely offset the encroachment of energy costs to

economy, too-cheap-to-ignore valuations overseas

consumers and businesses, but it goes a long way toward

should draw interest. We look for non-U.S. stocks,

mitigating its impact.

particularly those in emerging markets, to present a

In our judgment, without any further impact from the compelling opportunity later in the year.

Russian-Ukrainian war on Europe’s energy market, the

• Sectors – We find Energy and Metals to be attractive

fate of China’s economy remains the primary driver for

as investable themes around inventory depletion and

European economic activity. European exports to China are

de-carbonization. Also of interest is the housing and

sizable, especially for Germany, Europe’s largest economy.

related industries that have performed poorly given the

Therefore, a growth boost in China from policy-induced

spike in mortgage rates, yet the long-cycle thesis of an

sources or relief from stringent COVID mitigation protocols

undersupplied market remains intact. Biopharma also

would reflect well for Europe’s economic lot.

offers potential as large drug companies face patent cliffs

and have sizeable war chests to replenish their product

OTHER GEOPOLITICAL RISKS stream via acquisition. Technology should be attractive

Russia’s invasion of Ukraine, the possibility of another as decelerating growth tends to favor those companies

Taiwan Strait Crisis, and Iran’s nuclear breakout greatly that are capital-lite and have more predictable cash

reinforce the notion that rising geopolitical risk, and the flows. Additionally, we favor small-company stocks where

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 8 OF 13valuations relative to their larger-company counterparts

Scenario 2: Soft(ish) Landing

are uncommonly low, therefore offering the prospect for

appealing returns. The economy succumbs to the slowdown engineered

by the Fed’s effort to dampen demand and stave off

• Commodities – Ongoing global demand and years of

inflation. While a recession occurs perhaps around

underinvestment are drivers for commodity prices to rise.

midyear, it is neither deep nor lengthy. Later in the year, as

The seemingly continuous risk that a disruption in the

unemployment rises modestly and consumers pull back

tight supply of oil could cause a price spike, let alone

on their spending, the underlying strength in the labor

the strict supply management conducted by OPEC+,

market is sufficient to sustain purchasing power, allowing a

suggests prices offer asymmetrical risk to the upside.

recovery to ensue concurrent with inflation subsiding and

Industrial metals, especially copper for its ubiquitous

the Fed on pause. Stocks typically move higher in advance

usage as an electrical conductor, should benefit from fiscal

of the end of the recession, so weak prices in the first

expenditures on infrastructure both here and abroad, as

half of the year in anticipation of a recession give way to

well as the manufacturing of electric vehicles (EVs) and

strength in the second half. As corporate earnings fall into

alternative fuel sources. Used as a hedge in a diversified

the recession before recovering as prospects brighten in

portfolio, precious metals, namely gold and its higher-beta

the year’s latter half, stocks oscillate within a range before

brethren silver, may be used in part to address the risk of a

ultimately resolving higher. Commodities, particularly oil

geopolitical or inflationary shock.

and industrial metals, advance as years of underinvestment

tighten balances as demand slowly begins to improve. The

VARIOUS ECONOMIC SCENARIOS S&P 500 struggles to surpass 4,300.

AND PROBABLE OUTCOMES

Probability: 55% (our Base Case)

Our prognostication for the U.S. stock market’s path

forward includes three potential outcomes that emanate

from various economic scenarios that could unfold, Scenario 3: What Could Go Wrong Did

assigning a probability to each. In preview, we see a path

for a bullish view to be validated over the course of the Inflation moderates but remains well above the Fed’s

year, even as we may encounter some downside in equity target of 2%. At the same time, consumer expectations

prices early in the forecast window. Our confidence interval related to inflation’s prospects risk coming unmoored. The

between the bull and bear case is wide, given the myriad Fed tightens policy by raising rates well above neutral and

and fluid variables that are shifting rapidly today and will holds them there through the year in a concerted effort to

likely continue to throughout 2023. quell inflation. Even as inflation moderates, falling below

the Fed’s interest-rate setting, the Fed remains resolved

to ensure it does not reignite should policymakers loosen

Scenario 1: The Needle is Threaded prematurely. Financial conditions tighten meaningfully;

businesses devoted to protecting margins shed workers

Inflation plunges, mostly due to clearing supply-chain

in earnest; and consumers retrench to weather unstable

distortions and not crippling demand. As a result, the

labor conditions. Economic activity contracts as is typical

Fed shifts its rhetoric toward a more dovish tone. While

in a Fed-induced recession, and corporate earnings fall

the rate setting may not be reduced until late in the

double digits. With inflation high, economic activity weak,

year, the fundamental support for the economy, namely

and unemployment rising, the definition of stagflation is

consumer spending, stays firm as job stability with

fulfilled. Bonds and cash returns prevail. The stock market

steady and improved real incomes induce higher levels

falls below its recent low in October 2022 and nears

of confidence about the future. The economy averts a

3,200 before rebounding to 3,800.

recession. Inflation fails to reignite as rates remain high

enough to act as a governor on demand but allows Probability: 30%

growth to expand at a moderate pace. After a volatile

and somewhat directionless first half, the S&P 500

begins to discount improving prospects for corporate BOTTOM LINE: ENSEMBLE FORECAST

earnings and a sustained rally develops. Cyclical sectors

lead the rally and commodities rise on better domestic Considering the probabilities around three different but

and global prospects. The market appreciates as rising plausible scenarios, we look for an S&P 500 Index level

earnings estimates accompanied by multiple expansion at 4,195. Our confidence around this outcome is almost a

drive the price to 4,600. coin toss, therefore we are prepared to adjust accordingly

as new information is collected in the coming months.

Probability: 15% Stay tuned.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 9 OF 13FIXED INCOME & INTEREST RATES

Fixed income markets faced many challenges in 2022, as interest rates increased across

maturities and credit spreads widened. 2023 is poised to offer better outcomes for fixed

income investments.

In reviewing 2022 bond markets, it is Chart 12:

Chart 12: Interest

Interest Rates

Rates Increased

Increased Across

Across Maturities

in Two Separate

Maturities in TwoWaves

Separate Waves

difficult to avoid superlatives. Through mid-

December, return from the U.S. Aggregate 5.00%

5.00%

-11.3%, easily

Bond Index measured -12.6%, easilythe

the 4.50%

4.50%

GUY LEBAS, CFA® worst since the invention of bond indices 4.00%

4.00%

Chief Fixed Income Strategist

in the 1970s. While data are sketchy going 3.50%

3.50%

Director of Custom Fixed back further, some studies point to the worst 3.00%

3.00%

Income Solutions, Janney performance since the 1920s (Morningstar),

2.50%

2.50%

Capital Management 2.00%

2.00%

the 1840s (Prof. Ed McQuarrie), or even 1.50%

1.50%

Guy LeBas is responsible the Washington Administration (Vanguard). 1.00%

1.00%

for providing direction to Whether its 40, 140, or 240 years, suffice it to 0.50%

0.50%

the firm’s clients on the say that bond markets have been particularly 0.00%

0.00%

Oct-21 Jan-22 Mar-22 Jun-22 Sep-22 Dec-22

macroeconomic, interest Oct-21 Jan-22 Mar-22 Jun-22 Sep-22 Dec-22

rate, and bond market troubled in 2022.

(Source: Janney

(Source: Janney ISG,

ISG, Bloomberg)

Bloomberg)

investing climate.

Chart 11: 2022

2022 US

US Bond

Bond Market

Market Total

Total Returns

Returns

Guy authors bond Among Worst Ever fundamentals

strong credit this this risk

year, investor year,aversion

investor

market periodicals which risk aversion

(evident (evident

in equities) in equities)

meant meant a

a sizeable

provide relative value sizeable underperformance

underperformance in corporate

in corporate and otherand

recommendations across 30%

30%

other “risky”

“risky” bonds.bonds. Investment-grade

Investment-grade credit credit

the fixed income spectrum.

Bloomberg named him the 20%

20% spreads rose from a fairly tight +0.92% at

most-accurate forecaster of the beginning of the year to about 1.30%

10%

the Treasuries market in 2015

10%

as of mid-December, leading risky bonds to

and previously recognized underperform and compounding the effects

0%

0%

him as a “Bloomberg Best”

for his work in bond market of higher interest rates. A similar theme

applies for different reasons to mortgage-

-10%

-10% Dec 5,

Dec 5,

Dec 2022:

15,2022:

2022:

forecasting. -12.1%

-11.3%

-12.1%

Prior to joining Janney in -20%

-20%

backed securities, which performed very

2006, Guy served as Interest

Jan

Jan Feb

Feb Mar

Mar Apr

Apr May

May Jun

Jun Jul

Jul Aug

Aug Sep

Sep Oct

Oct Nov

Nov Dec

Dec

poorly and which comprise about 20% of the

Rate Risk Manager for U.S. (Source:

(Source: Janney

Janney ISG,

ISG, Bloomberg

Bloomberg Indices

Indices (((FKA

FKA Barclays

FKA Barclays Indices

Indices &&

Barclays Indices Lehman

& Lehman Indices))

Lehman Indices))

Indices)) Aggregate Index.

Trust’s bank asset and liability

portfolios, a role in which he Chart 13: Credit

Credit Spreads

Spreads Moved

Moved Steadily

Steadily Wider

Wider

oversaw risk and return on

The reasons for negative

negative returns

returnsare

aretwofold:

twofold. Alongside the Spring and Fall Equity Market Selloffs

an $11 billion balance sheet. First, interest rates across maturities are

First, interesthigher,

significantly rates across

largelymaturities

a functionareof 175bps

175bps 650bps

650bps

He received his education

from Swarthmore College significantly

Federal higher,

Reserve largely

rate hikesathat

function of

brought 165bps

165bps 600bps

600bps

and is a CFA Charterholder. Federal Reserve

overnight interestrate hikes

rates fromthat brought

zero to

155bps

155bps 550bps

550bps

overnight interest rates from zero to 4.50% 145bps IG Credit

IG Credit Spreads

Spreads

145bps 500bps

4.50% at year end. As of mid-December, HY

HY Credit

Credit Spreads

Spreads 500bps

135bps

at year end. As of mid-December, 10-year

135bps

450bps

benchmark 10-year Treasury yields were

450bps

125bps

125bps

bond yields were trading about 3.50% 400bps

trading about 3.60% after a +2.10% increase,

400bps

115bps

115bps

after a +2.0% increase, while 2-year yields 350bps

350bps

while 2-year Treasury yields were trading

105bps

105bps

were

at abouttrading

4.30% about

after 4.20%

a +3.55% after a +3.5%

increase—

95bps

95bps

300bps

300bps

increase—one

one of the largest of the

moves largest moves Fed

on record. on 85bps

85bps

250bps

250bps

record. Fed tightening is, in turn, a function

75bps

75bps 200bps

200bps

tightening is, in turn, a function of stubborn

Oct-21

Oct-21 Jan-22

Jan-22 Mar-22

Mar-22 Jun-22

Jun-22 Sep-22

Sep-22 Dec-22

Dec-22

of stubborn core inflation, which will end the

core inflation, which will end the year (Source: Janney

(Source: Janney ISG,

ISG, Bloomberg)

Bloomberg)

year slightly above 6% year-over-year (YoY).

slightly above 6% year-over-year (YoY). In

In the Outlook 2022 fixed income article, we

the Outlook 2022 fixed income article, we If bond markets were a function of Fed

highlighted good odds of significantly higher

highlighted good odds of significantly higher tightening in 2022 and Fed tightening was

interest rates

interest rates in

in 2022,

2022, butbut the

the degree

degree ofof the

the

moves far exceeded even our bearish case. a function of inflation, it stands to reason

moves far exceeded even our bearish case. that the most significant economic variable

Second, credit spreads on corporate bonds in 2023 will also be inflation. While core

Second, credit spreads on corporate bonds

are significantly wider in 2022. Despite inflation has remained elevated through

are significantly wider in 2022. Despite

© JANNEY

© JANNEY MONTGOMERY

MONTGOMERY SCOTT

SCOTT LLC

LLC •• MEMBER:

MEMBER: NYSE,

NYSE, FINRA,

FINRA, SIPC

SIPC •• JANNEY

JANNEY OUTLOOK

OUTLOOK 2023

2023 •• REF:

REF: 889807-1222

889807-1222 •• PAGE

PAGE 10

10 OF

OF 13

13October 2022, there are signs that many components Table 1: U.S. Interest Rate Forecasts

are easing. For example, healthcare costs in the CPI were

steeply positive in 2022, but will flip to somewhat negative Date

Date FedFunds

Fed Funds 2yrUST

2yr UST 5yr

5yrUST

UST 10yr UST

10yr 30yr30yr

UST 2s10s 5s30s

5s30s

in 2023, peeling 0.05% each month from consumer prices. Target

Target UST UST

Private indices of rental rates are showing deceleration. 12/30/2022

12/30/2022 4.25

4.25- -4.50

4.50 4.30

4.25 3.85

3.70 3.80

3.60 3.85

3.60 -0.50

-0.65 0.00

-0.10

Moreover, leading indicators of core inflation, such as 3/31/2023

3/31/2023 4.50

4.50- -4.75

4.75 4.15

3.95 3.75

3.55 3.60

3.30 3.70

3.50 -0.55

-0.65 -0.05

commodities prices, are outright declining.

6/30/2023

6/30/2023 4.50

4.50- -4.75

4.75 3.95

3.65 3.65

3.45 3.55

3.15 3.70

3.50 -0.40

-0.50 0.05

Chart 14:

Chart 14: Inflation

Inflation Markets

Markets are

are Pricing

Pricing CPI

CPI (All

(All Items)

Items) to Decline to 3% 9/30/2023

9/30/2023 4.50

4.50- -4.75

4.75 3.75

3.45 3.55

3.35 3.45

3.10 3.70

3.50 -0.30

-0.35 0.15

YoY

to in 2023

Decline to 3% YoY in 2023

10.00%

10.00% 12/31/2023

12/31/2023 4.25

4.25- -4.50

4.50 3.55

3.25 3.50

3.30 3.40

3.00 3.70

3.50 -0.15

-0.25 0.20

9.00%

9.00% 12/31/2024

12/31/2024 3.25

3.25- -3.50

3.50 3.05

2.85 3.35

3.15 3.25

3.05 3.70

3.50 0.20

0.20 0.35

0.35

8.00%

8.00%

(Source:

(Source: Janney

(Source: Janney ISG)

Janney ISG)

ISG)

7.00%

7.00%

6.00%

6.00% which in many ways makes the current inversion stranger.

5.00%

5.00% Stranger still, we anticipate the inversion could last through

4.00%

4.00%

the end of 2023. The last time the curve was this inverted,

it returned to positive slope in just three months!

3.00%

3.00%

2.00%

2.00% Reported

Reported CPI

CPI Inflation

Inflation Implied

Implied by

by Inflation

Inflation Swap

Swap Fixings

Fixings

With short-term yields significantly above long-term yields,

1.00%

1.00%

the temptation to buy shorter-term bonds with less interest

Sep-21

Sep-21 Dec-21

Dec-21 Mar-22

Mar-22 Jun-22

Jun-22 Sep-22

Sep-22 Dec-22

Dec-22 Mar-23

Mar-23 Jun-23

Jun-23 Sep-23

Sep-23 Dec-23

Dec-23 Buffett-ism,yield

rate risk is high. But, to twist a Buffet-ism, yieldisiswhat

whatyou

you

(Source:

(Source: Janney

(Source: Janney ISG,

Janney ISG, Bureau

ISG, Bureau of

of Labor

US Bureau Labor Statistics,

Statistics,

of Labor Bloomberg)

Bloomberg)

Statistics, Bloomberg)

buy, value is what you get. In today’s market environment,

the biggest risk in our view is no longer interest-rate risk,

These indicators make it likely that the CPI will decelerate, but rather reinvestment risk. In 2023 (or 2024 or 2025),

even as economic growth wanes. On the topic of growth, interest rates will likely be lower than they are today, and

interest-rate-sensitive sectors of the economy such as investors who buy short-term bonds today will be faced

housing and auto sales are already flagging. While the with reinvesting at lower yields when those bonds mature.

impact of slowing sales takes some time to be felt (e.g., Table 2:

Table 2: Rolling

Rolling Short-Term

Short-Term Bonds

Bonds Creates

Create Reinvestment

ReinvestmentRisk

Riskifif

construction industries have yet to shed any jobs), there is Rates Fall

Rates Fall

a very high probability of a significant contraction in these

sectors that could expand into the broader economy. Dec-22 (Act) Dec-23 (Proj) Dec-24 (Proj) 3yr Avg. Yield

We can envision a scenario in which industry-specific 1yr T-Bill 4.70% 3.60% 2.60% 3.63%

contraction does not lead to a recession, but that scenario

is the exception, not the rule. Ultimately, by raising interest

rates rapidly, the Fed has engineered a recession in order (Source:

(Source: Janney

(Source: Janney ISG)

Janney ISG)

ISG)

to control inflation.

As inflation fades, growth slows, and rates reach their The simple way to reduce reinvestment risk is to avoid

highest levels in 15 years, the question for bond markets short-term maturities, despite their headline appeal. We

becomes: What will the Fed do about it? Nothing, probably. prefer the 5-to-10-year portion of the yield curve, which is far

Fed Chairman Jerome Powell has repeatedly highlighted enough out to avoid the most problematic reinvestment risk,

what he views as the error of the 1970s, namely that the but short enough to avoid the swings in market value from

Fed declared high inflation “over” and then eased too very long-duration bonds in a still-volatile climate. Finally,

quickly, exacerbating long-term inflation risks. While we the 5-to-10-year part of the curve provides significant carry,

think the February rate hike will be the last in this cycle, it regardless of which way interest rates move in the coming

is premature to expect cuts. Given Powell’s perception, we 12 months. Our outlook for economic growth is cautious,

instead expect the Fed will remain on hold for most if not and historically that outlook has also proven challenging

all of 2023, bearing

barring aa surprisingly

surprisingly deep

deep downturn.

downturn. ItIt might

might for leveraged credits. Accordingly, we prefer higher-quality

take a year of persistently near or below 2% core inflation investment-grade issues, a preference that generally holds

before Powell is willing to pull the trigger on cuts. across corporate and municipal sectors.

For the level of term interest rates, a not-ready-to-cut CORPORATE CREDIT

Fed is likely to create an unusually deeply inverted yield

curve that progresses forward without de-inverting. With On a fundamental basis, leverage across investment-grade

the spread between the 2-year and 10-year Treasury yield and high-yield credit sectors is still relatively low. Moreover,

(-0.75%), we are already at that point, but we see a chance the high-yield sector has a lot of liquidity runway as there

of a deeper -1.00% 2s/10s inversion early in the new year. are virtually no maturities among index-eligible high-yield

The last time the curve was this inverted, in the early 1980s, names in 2023 or 2024. Historically, however, lower

the absolute level of interest rates was far higher (11%+), credits have struggled in terms of investor perception in

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 11 OF 132012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2021 2022

(Source: Janney ISG, Bloomberg)

MUNICIPAL CREDIT

One area of the markets that fared poorly in the spring but

weak

has held economic environments

up surprisingly well inlike

the the

fall one we will

of 2022 haslikely

been Going forward, we expect muni ratios to have limited room

face in 2023. With current spreads at +1.30%

the high-grade municipal markets. Muni/Treasury ratios (investment- for further improvement, but the lack of supply should also

grade)

startedand the +4.50%

year well(high-yield)

lower thanabove Treasuries,

historical averages onand prevent any sharp widening—barring another round of

top of andup

rocketed slightly

abovetighter

100% than

in thethe long-term

10-year averages

maturity range. more severe risk-off activity in overall financial markets. Our

respectively,

Ratios have sincethereretreated

remains scope

as muni forissuance

wideningdived,

and credit preference in munis is like that in investment-grade credit:

underperformance.

creating a favorableHolding higher-quality

supply dynamic namesthe

that helped willsector Avoid reinvestment risk from maturities in 2023-2025

help reduceinthe

outperform theimpact of further

subsequent six spread

months.widening—and

At present, muni with higher-grade 5-to-10-year holdings as a way to take

itrelative

doesn’tvaluations

hurt that income generation

are in the even but

neutral range, amongtherehigh-

are no advantage of greater carry.

grade

obvious bonds is near

negative decade highs.

catalysts.

Chart 15:

SUMMARY

16: Historically, Credit Spreads Continue to Widen through the

First Halfthe

through of an Economic

First Downturn

Half of an Economic Downturn In brief, after an extremely tough 2022 for fixed income

1500bps

investors, we anticipate smoother sailing with respect

to interest rates in the coming year. The period of rapid

1300bps

Recession

Fed rate hikes is coming to an end, which should reduce

1100bps

6m Change IG Credit Spreads volatility. Even though we believe cuts are further in the

future than the market is pricing, the odds fall in the favor

900bps 6m Change HY Credit Spreads

700bps

of lower, not higher, interest rates in 2023. Still, given the

500bps probability of a recession or near-recession, we hold an

300bps up-in-quality bias across sectors and anticipate that higher-

100bps grade credits and municipals will broadly outperform lower-

-100bps grade ones in the coming year.

-300bps

-500bps

1995 1998 2000 2003 2006 2009 2011 2014 2017 2020 2022

(Source:

(Source: Janney

Janney ISG,

ISG, Bloomberg)

Bloomberg)

MUNICIPAL CREDIT

One area of the markets that fared poorly in the spring

but

weak held up surprisingly

economic well

environments

© inMONTGOMERY

JANNEY the fall

like the of one

SCOTT2022LLC • is

we will the

likely

MEMBER:

Going forward, we expect muni ratios to have limited room

NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 12 OF 13

high-grade municipal markets. Muni/Treasury

face in 2023. With current spreads at +1.30% (investment- ratios for further improvement, but the lack of supply should also

started

grade) andthe year

+4.50% well(high-yield)

lower thanabove historical averages

Treasuries, onand prevent any sharp widening—barring another round of

rocketed

top of andupslightly

abovetighter

100% in thethe

than 10-year

long-term maturity range.

averages more severe risk-off activity in overall financial markets. Our

Ratios have since

respectively, thereretreated as muni

remains scope forissuance

widening dived,

and credit preference in munis is like that in investment-grade credit:

creating a favorableHolding

underperformance. supply dynamic

higher-qualitythat helped namesthe willsector Avoid reinvestment risk from maturities in 2023-2025

outperform

help reduceinthe theimpact

subsequent six months.

of further spread widening—and At present, muni with higher-grade 5-to-10-year holdings as a way to take

relative

it doesn’t valuations

hurt that are

incomein the neutral range,

generation evenbut amongtherehigh-

are no advantage of higher carry.

obvious

grade bonds negative catalysts.

is near decade highs.

In brief, after an extremely tough 2022 for fixed income

Chart 16:

15: 10yr AAA Muni/Treasury Ratios are in the “Neutral” Range, investors, we anticipate smoother sailing with respect

although Absolute Yields are Near the Highest in Years to interest rates in the coming year. The period of rapid

Fed rate hikes is coming to an end, which should reduce

190%

volatility. Even though we believe cuts are further in the

170%

future than the market is pricing, the odds fall in the favor

of lower, not higher, interest rates in 2023. Still, given the

150% probability of a recession or near-recession, we hold an

130%

up-in-quality bias across sectors and anticipate that higher-

grade credits and municipals will broadly outperform lower-

110% 2Q 2017 - 2Q 2019 Avg

4Q 2022 Avg

80% grade ones in the coming year.

83%

90% Historically Cheap

Historically Neutral

70%

Historically Rich

50%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2021 2022

(Source:

(Source: Janney

Janney ISG,

ISG, Bloomberg)

Bloomberg)

MUNICIPAL CREDIT

One area of the markets that fared poorly in the spring but

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 12 OF 13

has held up surprisingly well in the fall of 2022 has beenDisclosures Definition of Ratings

This is for informative purposes only and in no event should be construed Overweight: Janney ISG expects the target asset class or sector to

as a recommendation by us or as an offer to sell, or solicitation of an offer outperform the comparable benchmark (below) in its asset class in terms

to buy, any securities. The information given herein is taken from sources of total return.

that we believe to be reliable, but is not guaranteed by us as to accuracy Marketweight: Janney ISG expects the target asset class or sector to

or completeness. Opinions expressed are subject to change without perform in line with the comparable benchmark (below) in its asset class in

notice and do not take into account the particular investment objectives, terms of total return.

financial situation, or needs of individual investors. Employees of Janney

Montgomery Scott LLC or its affiliates may, at times, release written or oral Underweight: Janney ISG expects the target asset class or sector to

commentary, technical analysis, or trading strategies that differ from the underperform the comparable benchmark (below) in its asset class in

opinions expressed here. terms of total return.

Returns reflect results of various indices based on target allocation

weightings. Weightings are subject to change. Index returns are for Benchmarks

illustrative purposes only and do not represent the performance of any

investment. Index performance returns do not reflect any management Asset Classes: Janney ISG ratings for domestic fixed income asset classes

fees, transaction costs, or expenses. Indexes are unmanaged, and you including Treasuries, Agencies, Mortgages, Investment Grade Credit, High

cannot invest directly in an index. Yield Credit, and Municipals employ the “Barclays U.S. Aggregate Bond

Market Index” as a benchmark.

Performance data quoted represents past performance and is no

guarantee of future results. Current returns may be either higher or lower Treasuries: Janney ISG ratings employ the “Barclays U.S. Treasury Index”

than those shown. as a benchmark.

This report is the intellectual property of Janney Montgomery Scott LLC Agencies: Janney ISG ratings employ the “Barclays U.S. Agency Index” as

(Janney) and may not be reproduced, distributed, or published by any a benchmark.

person for any purpose without Janney’s prior written consent. Mortgages: Janney ISG ratings employ the “Barclays U.S. MBS Index” as a

This presentation has been prepared by Janney Investment Strategy benchmark.

Group (ISG) and is to be used for informational purposes only. In no Investment Grade Credit: Janney ISG ratings employ the “Barclays U.S.

event should it be construed as a solicitation or offer to purchase Credit Index” as a benchmark.

or sell a security. The information presented herein is taken from High Yield Credit: Janney ISG ratings employ the “Barclays U.S. Corporate

sources believed to be reliable, but is not guaranteed by Janney as to High Yield Index” as a benchmark.

accuracy or completeness. Any issue named or rates mentioned are

used for illustrative purposes only and may not represent the specific Municipals: Janney ISG ratings employ the “Barclays Municipal Bond Index”

features or securities available at a given time. Preliminary Official as a benchmark.

Statements, Final Official Statements, or Prospectuses for any new

issues mentioned herein are available upon request. The value of and

income from investments may vary because of changes in interest rates, Analyst Certification

foreign exchange rates, securities prices, and market indices, as well We, Mark Luschini and Guy LeBas, the Primarily Responsible Analysts for

as operational or financial conditions of issuers or other factors. Past this report, hereby certify that all views expressed in this report accurately

performance is not necessarily a guide to future performance. Estimates reflect our personal views about any and all of the subject sectors,

of future performance are based on assumptions that may not be industries, securities, and issuers. No part of our compensation was, is, or

realized. We have no obligation to tell you when opinions or information will be, directly or indirectly, related to the specific recommendations or

contained in Janney ISG presentations or publications change. views expressed in this research report.

© JANNEY MONTGOMERY SCOTT LLC • MEMBER: NYSE, FINRA, SIPC • JANNEY OUTLOOK 2023 • REF: 889807-1222 • PAGE 13 OF 13You can also read