OPEN SESSION TUESDAY January 18, 2022 - SMITHFIELD TOWN COUNCIL MEETING

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

SMITHFIELD TOWN COUNCIL

MEETING

OPEN SESSION

TUESDAY

January 18, 2022

SMITHFIELD TOWN COUNCIL VIRTUAL

MEETING

TUESDAY, JANUARY 18, 2022

6:30 P.M.

Please join the meeting from your computer, tablet or smartphone.

https://www.gotomeet.me/RandyRossi/smithfield-town-council

You can also dial in using your phone.*

United States (Toll Free): 1 877 568 4106

United States: +1 (646) 749-3129

Access Code: 342-830-965

6:30 P.M. EXECUTIVE SESSION

A. Convene into executive session to consider, discuss, and act upon matters

pursuant to Rhode Island General Laws Section 42-46-5(a)(1), Personnel; Town

Manager Annual Review.

7:00 P.M. AGENDA

I. Regular meeting reconvened at 7:00 p.m.

- Announce any executive session votes required to be disclosed pursuant to

Rhode Island General Laws, Sec. 42-46-4.

II. Prayer

III. Salute to the Flag

IV. Presentations: None

V. Minutes: None

VI. Consider, discuss and act upon the following possible appointments and

reappointments:

A. Tree Warden reappointment with a term expiring in December of 2022.

VII. Public Hearings:

A. Schedule a public hearing on February 15, 2022 to consider, discuss, and act

upon amendments to Chapter 19 of the Code of Ordinances entitled “Capital

Improvements” and replacing it with Chapter 19 entitled “Capital Program

and Reserve Funds”.

B. Schedule a public hearing on February 15, 2022 to consider amendments to

Chapter 321 of the Code of Ordinances entitled “Taxation” by adding Article

VI entitled “Exempting or Stabilizing of Taxes on Qualifying Commercial or

Manufacturing Property”.

C. Conduct a public hearing to consider, discuss and act upon approving a new

Class B-Victualler Beverage License for Fresco Ditto, Inc. d/b/a “Fresco”,

181 George Washington Highway to include Outdoor Seating/Bar Service,

with the hours of operation to be Monday through Sunday, 6:00 a.m. to 1:00

a.m., as applied subject to compliance with all State regulations, local

ordinances, a copy of the Retail Sales Permit, final approval from the RI

Department of Health and final inspection from the Smithfield Fire

Department.

D. Conduct a show cause hearing to consider, discuss and act upon the possible

suspension, revocation, or other sanction regarding the listed Liquor Licenses

due to non-renewal or non-compliance with the conditions of renewal:

1. DLA, LLC d/b/a “Parma Ristorante”, 266 Putnam Pike, Unit 1

2. Ichiraku, LLC d/b/a “Ichiraku Ramen and Fusion”, 970 Douglas Pike

3. Lola’s Lounge, LLC d/b/a “Lola’s Lounge”, 55 Douglas Pike

4. Rebel Alliance Group, LLC d/b/a “Bistecca Chop House”, 332 Farnum

Pike

VIII. Licenses:

A. Consider, discuss and act upon approving a new Victualling License for

Fresco Ditto, Inc. d/b/a “Fresco”, 181 George Washington Highway, as

applied, subject to compliance with all State regulations, local ordinances, a

copy of the Retail Sales Permit, final approval from the RI Department of

Health and final inspection from the Smithfield Fire Department.

B. Consider, discuss and act upon approving a new Entertainment License for

Fresco Ditto, Inc. d/b/a “Fresco”, 181 George Washington Highway, as

applied, subject to compliance with all State regulations, local ordinances and

a final inspection from the Smithfield Fire Department.

C. Consider, discuss and act upon approving a new Special Dance License for

Fresco Ditto, Inc. d/b/a “Fresco”, 181 George Washington Highway, subject

to compliance with all State regulations, local ordinances and a final

inspection from the Smithfield Fire Department.

D. Consider, discuss and act upon approving the renewal of three (3) Victualling

Only Licenses, as listed, as applied, subject to compliance with all State

regulations and local ordinances:

1. ALG 33 Enterprises, Inc. d/b/a “Piezoni’s”, 259 Putnam Pike

2. Target Corporation d/b/a “Target Store T-1404”, 371 Putnam Pike

3. Vibe Nutrition RI, LLC d/b/a “Vibe Nutrition, LLC”, 285 George

Washington Highway

E. Consider, discuss and act upon approving the renewal of one (1) Mobile Food

Truck License, as applied, subject to compliance with all State regulations and

local ordinances.

1. Rhode Island Kona, LLC d/b/a “Rhode Island Kona”, to sell only frozen

ice from a truck with RI Reg. number 21700, 4 Cider Lane.

IX. Old Business: None.

X. New Business:

A. Consider, discuss, and act upon the acceptance of the Audit Report for Fiscal

Year Ending June 30, 2021 prepared by Hague, Sahady & Co., P.C.

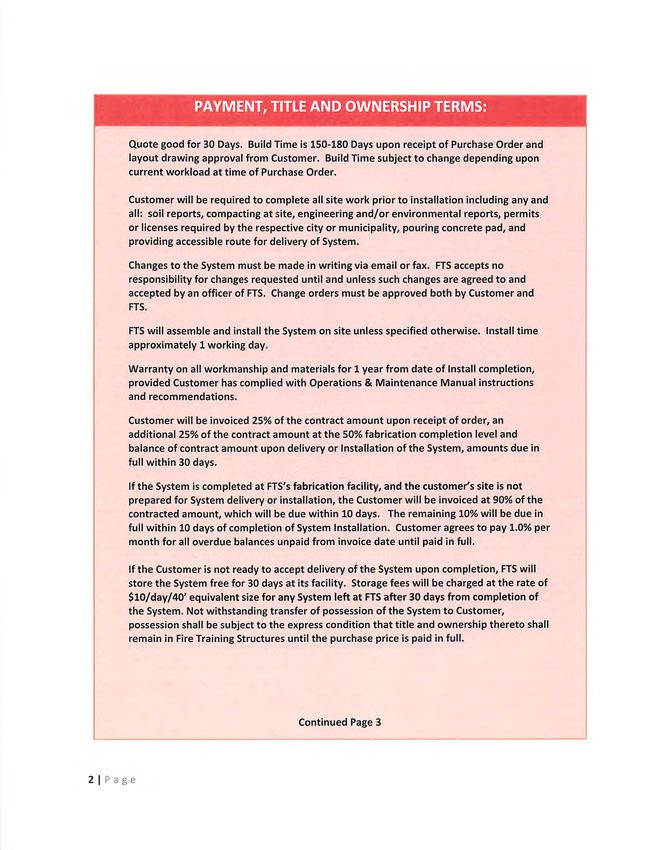

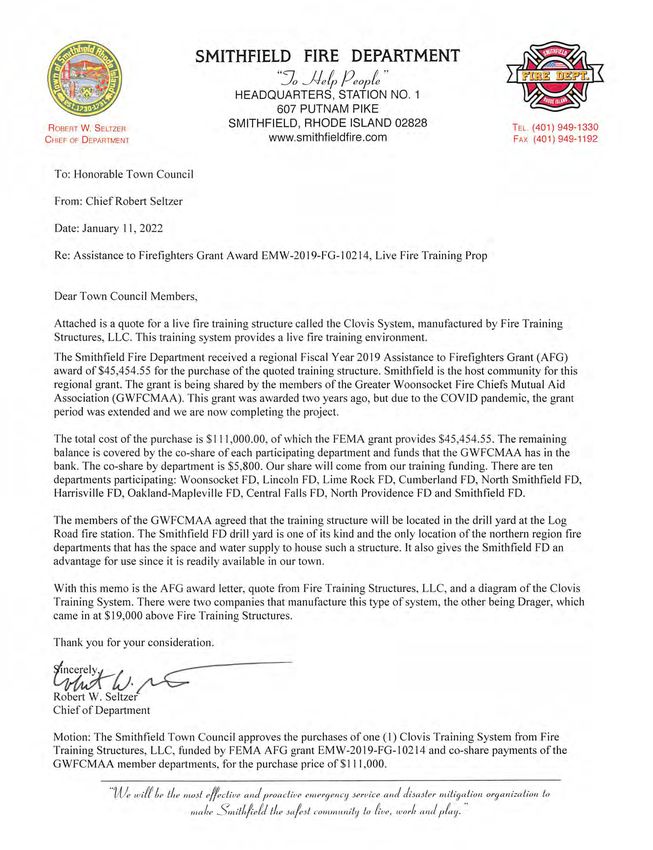

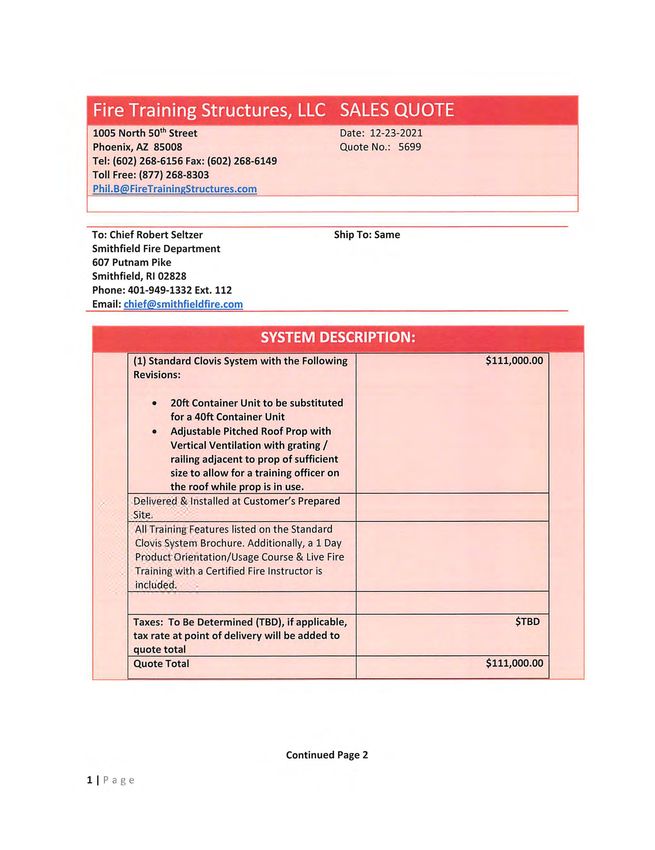

B. Consider, discuss, and act upon approving the purchase of one (1) Clovis

Training System for Fire Training Structures, LLC, in the amount of one

hundred and eleven thousand dollars ($111,000.00) to be funded by FEMA

Assistance to Firefighters Grant EMW-2019-FG-10214 and co-share

payments from the Greater Woonsocket Fire Chiefs Mutual Aid Association.

C. Consider, discuss, and act upon authorizing the purchase of one (1)

rescue/ambulance, one (1) engine/pumper truck, and one (1) tower ladder

truck from Greenwood Emergency Vehicles of North Attleboro, MA, through

the Houston-Galveston Area Council contract, for an amount not to exceed

two million, one hundred and fifty-five thousand, nine hundred and fifty-three

dollars ($2,155,953.00) to be funded by the EMS billing account.

D. Consider, discuss, and act upon approving tax abatements in the amount of

five hundred, fifty-nine dollars and fifty-seven cents ($559.57).

XI. Public Comment

XIV. Adjournment.

AGENDA POSTED: THURSDAY, JANUARY 13, 2022*

*It is advised that you download the GoToMeeting app from gotomeeting.com in advance of the

meeting.

**If you are participating in the virtual meeting from your phone, please hit “*6” to mute and unmute

yourself.

***Documentation relating to agenda items can be found on the Town of Smithfield website at

https://www.smithfieldri.com/2021-meeting-agendas/.

The public is welcome to any meeting of the Town Council or its sub-committees. If communication assistance

(readers/interpreters/captions) or any other accommodation to ensure equal participation is needed, please contact

the Smithfield Town Manager’s office at 401-233-1010 at least forty-eight (48) hours prior to the meeting.

Recommended Motion: That the Smithfield Town Council hereby schedules a public hearing on February 15, 2022 to consider and act upon amendments to Chapter 19 of the Code of Ordinances entitled “Capital Improvements” and replacing it with Chapter 19 entitled “Capital Program and Reserve Funds”.

It is hereby ordained by the Town of Smithfield as follows:

Section 1. Part One(1) of the Smithfield Code of Ordinances entitled “ General

Legislation” is hereby amended by repealing Chapter 19, entitled “Capital Improvements”

and replacing it with Chapter 19 entitled “Capital Program and Reserve Funds” which

shall read as follows :

Chapter 19. Capital Program and Reserve Funds

Article I. Definitions

§ 19-1. Definitions.

The following terms, when used in this chapter, shall have the meanings ascribed to them

in this section, except where the context clearly indicates a different meaning:

CAPITAL IMPROVEMENT PROJECT

Shall include the following:

(a) The acquisition of land;

(b) The lease of land or buildings;

(c) The acquisition or construction of buildings or facilities, including preconstruction,

survey and engineering costs;

(d) The improvement, expansion or reconstruction of existing buildings or facilities in

excess of normal maintenance work; and

(e) The purchase of items of equipment which have a useful life in excess of five years

and which have a cost in excess of $10,000.

PUBLIC FACILITIES

(a) Water supply production, treatment, storage and distribution facilities;

(b) Wastewater and solid waste collection , treatment and disposal facilities;

(c) Roads, streets, bridges, including rights-of-way , traffic signals , landscaping and

local improvements of state and federal highways;

(d) Stormwater collection, retention, detention, treatment and disposal facilities, flood

control facilities, flood control facilities, bank and shore projections and enhancement

improvements;

(e) Parks, open space areas and recreational facilities;

(f) Police, emergency medical, rescue and fire protection facilities;

(g) Public schools and libraries; and

(h) Other public facilities consistent with the Smithfield Capital Improvement Plan or

Comprehensive Community Plan; including but not limited to historic preservation or

restoration projects.

Article II. Capital Program

§19-2. Capital Committee.

(a) There shall be one Capital Committee for the entire Town, including the Smithfield

Public Schools (Smithfield School Department) and all other Departments of the Town of

Smithfield. The Capital Committee will be an advisory board to the Smithfield Town

Council and shall consist of eleven (11) members: Three(3) members of the School

Department (One member of the School Committee, the School Superintendent, and the

School Facilities Director) , Two (2) members of the Budget and Financial Review

Board, One(1) member of the Asset Management Commission , The Town Finance

Director , The Town Planner, Two (2) Town Council members who shall be selected by

the Town Council President and the Town Manager.

(b) Submission to Town Council.

The Capital Committee shall meet quarterly and prepare and submit to the Town Council,

three (3) months before the operating budget submission date, a twenty (20) year Capital

Program consisting of four(4) increments having a duration of five (5) years each . On or

before November 1st, of each year all Town Departments and agencies shall submit

requests for capital improvement projects to the Capital Committee in accordance with

the procedures outlined in the “Capital Budget Manual of Procedure” published by the

Smithfield Planning Board. The Town Council by resolution shall approve the Capital

Program with or without amendment after the public hearing and on or before the third

(3rd) Thursday of February of the current fiscal year.

(c) Contents. The Capital Program shall include:

1) A clear general summary of its contents; including but not limited to capital revenues,

debt service, and what capital needs require bonding, etc.;

2) A list of capital improvements and other capital expenditures which are proposed to

be undertaken during the five (5) ensuing fiscal years, with appropriate information as

to the necessity of each item;

3) Cost estimates and recommended time schedules for each improvement or other

capital expenditure;

4) Confirmation with the Town Treasurer to ascertain the availability of the Town funds

and method of financing to support the project;

5) The estimated annual cost of operating and maintain the facilities to be constructed or

acquired;

6) The Capital Program shall be revised every year with regard to capital improvements

that are still pending or in the process of construction or acquisition;

7) A Town Council resolution shall be required on all capital items in excess of ten

thousand dollars ($10,000).

(d) Life of Assets.

If the Town finances a capital project through the issuance of bonds the useful life of the

asset shall be at least equal to the term of the bond.

§ 19-3. Priority rating of projects.

In formulating the program for capital improvements the Capital Committee shall

establish a priority list of proposed projects. Such a priority list shall be based on the

general needs of the community with due regard for:

A. Protection of life and public health;

B. Protection of property;

C. Protection and proper exploitation of natural resources;

D. Provision of essential public services;

E. Replacement of obsolete facilities;

F. Improvement of operating efficiency; and

G. Improvement of social and cultural values.

§ 19-4. Town Council Action on Capital Program.

(a) Notice of Hearing.

The Town Council shall publish in one (1) or more newspapers of general circulation in

the Town a general summary of the Capital Program and a notice stating:

1. The times and places where copies of the Capital Program are available for inspection

by the public and;

2. The time and place, not less than two weeks after such publication, for a public

hearing on the Capital Program.

(b) Adoption.

The Town Council by Resolution shall adopt the Capital Program with or without

amendments.

Article III. Reserve Funds

§ 19-5. School Capital Reserve Fund.

(a) The Town of Smithfield hereby establishes the School Capital Reserve fund that will

adhere to the applicable Rhode Island General laws governing School Department

autonomy. The purpose of the fund is to augment the Smithfield Public School’s capital

budget that is approved through the Town’s annual budget process and ensure that the

Smithfield School Department complies with the minimum threshold for capital

maintenance requirements for approved projects under Rhode Island General Law 16-7-

23.

(b) The Town Manager’s annual budget that is submitted to the Budget and Financial

Review Board shall include an appropriate amount to be deposited into the School

Capital Reserve Fund.

(c) The School Capital Reserve Fund shall be used for funding school facility capital

improvement expenditures in excess of $50,000 with a useful life of 10 years or more. A

Town Council resolution shall be required for any expenditure from this fund.

(d) The Town’s twenty-year Capital Program will serve as a basis for capital expenditures

from this fund.

(e) All Rhode Island Department of Education reimbursements received due to expenditures

from this fund shall be deposited into this fund.

§ 19-6. Capital Reserve Fund and Land Trust Reserve Funds.

The Capital Reserve Fund and Land Trust Reserve Fund will be used for the

accumulation of funds prescribed in Article V, Financial Procedures, §C-5.08 Reserve

Funds, of the Smithfield Town Charter as amended in November, 2020. The Capital

Reserve Fund shall be available to the Town as necessary for expenditures relating to

certain capital expenditures pursuant to local ordinance. The Land Trust Reserve Fund

shall be used exclusively by the Smithfield Land Trust for the acquisition and

preservation of real property pursuant to the legislative charter of said land trust.

Expenditures from the Capital Reserve Fund and Disbursements from the Land Trust

Reserve Fund shall be shall be authorized by a Town Council Resolution.

§ 19-7. Capital Reserve Fund Purpose.

The Capital Reserve Fund shall be used for funding capital improvement expenditures in

excess of $50,000 with a useful life of 10 years or more. This policy does not preclude

the funding of any additional capital assets from the general fund or other sources. The

Town’s twenty-year Capital Improvement Plan or Comprehensive Community Plan will

serve as a basis for annual capital appropriations.

§19-8. Disbursement of Funds.

A. By the first of March each year, the Town Manager shall submit to the Budget and

Financial Review Board a Budget for the ensuing fiscal year. This budget may include

capital improvement expenditures funded from the Capital Reserve Fund.

B. Any subsequent increases or decreases to the expenditures from the Capital Reserve Fund

proposed by the Town Council will follow the procedure outlined in the Town Charter

for increases or decreases in the budget. Moreover, all expenditures from the Capital

Reserve Fund must be approved by a specific resolution at the Town Council public

budget hearing.

C. In no event shall the sum of funds appropriated under this article exceed the total funds

available in the Capital Reserve Fund at the time of appropriation.

D. The Smithfield Town Council shall oversee the expenditure of all funds disbursed under

this article.

E. Should an “emergency” situation arise, under Section C-5.10(a) of the Town Charter an

emergency appropriation [following budget adoption] could be implemented.

§ 19-9. Reporting

The Town’s Finance Director shall maintain all records of the reserve funds in

accordance with general accepted accounting principles and practices. A report of the

fund balances as well as collections to and disbursements from the funds shall be made

annually in the annual audit report as well as a report in the annual budget presentation.

Section II. This ordinance shall take effect thirty (30) days after its adoption.memorandum

DATE: January 10, 2022

TO: Smithfield Town Council

FROM: Christopher Celeste, Tax Assessor

RE: Proposed amendment Code of Ordinances, Chapter 321, Sections 17 through 26

A tax stabilization agreement is a highly useful tool to facilitate economic development. The proposed

amendment allows the Town of Smithfield to enter into an agreement for purposes of stabilizing taxes

on businesses expanding their facilities in, or relocating to, the Town of Smithfield. The ordinance sets

a minimum investment threshold, as well as requires that all taxes and fees remain current before and

during the term of an agreement. The ordinance also stipulates that any business subject to an

agreement, when adding or replacing employees must give deference to Smithfield residents. Terms

of an agreement under this ordinance would be limited to a maximum of ten years.

The proposed ordinance has been recently updated to more specifically define the application process.

Additionally, a new section has been added which requires annual review of compliance with terms of

the agreement and this ordinance. Along with non-payment of taxes; non-payment of any fees and/or

any violations of local code have been included as grounds for nullification of the agreement, thus

causing all relief given to be due and payable back to the Town. The minimum investment threshold

to qualify has also been increased.

This ordinance is intended to be a general framework which will be used for a specific agreement based

on individual components of each application. All agreements will need to be created as a contract

between the Town and the taxpayer under the terms of this proposed ordinance.

It is our request that the Town Council schedule a public hearing on February 15, 2022 to consider

the proposed amendment.

MOTION:

That the Smithfield Town Council hereby schedules a public hearing on February 15, 2022

to consider amendments to Chapter 321 of the Code of Ordinances entitled “Taxation” by

adding Article VI entitled “Exempting or Stabilizing of Taxes on Qualifying Commercial

or Manufacturing Property”.SECTION 1. CHAPTER 321 OF THE SMITHFIELD CODE OF ORDINANCES ENTITLED

“TAXATION” IS HEREBY AMENDED BY ADDING THERETO THE FOLLOWING

SECTION ARTICLE VI ENTITLED “EXEMPTING OR STABILIZING OF TAXES ON

QUALIFYING COMMERCIAL OR MANUFACTURING PROPERTY”

ARTICLE VI

EXEMPTING OR STABILIZING OF TAXES ON QUALIFYING COMMERCIAL OR

MANUFACTURING PROPERTY

321-17 Purpose. This chapter is adopted pursuant to the authority in R.I. Gen. Laws § 44-3-9.11

for the purpose of establishing requirements and procedures by which the Town Council may enter

into agreements with property owners to exempt or stabilize taxes on real or personal property

used for manufacturing or commercial purposes, in order to encourage economic development,

expansion, redevelopment and/or rehabilitation of existing manufacturing, industrial and

commercial buildings as well as the new development of manufacturing, industrial and commercial

buildings or structures on appropriately zoned land.

321-18 Definitions. As used in this chapter, the following words or phrases shall have the

following meaning:

A. “Commercial property” means any structure or facility, or other real or personal

property, used primarily for offices or commercial enterprises.

B. “Manufacturing property” means any structure or facility, or other real or personal

property, used in the process of working raw materials into wares suitable for use or

that gives new shapes, new quality or new combinations to matter that already has gone

through some artificial process by the use of machinery, tools, appliances, and other

similar equipment, and any structure or facility used for distribution, warehousing, or

storage of goods.

321-19 Authority. Upon application, and after advertisement and public hearing, the Town

Council may enter into an agreement with the owner of commercial or manufacturing property

located in the Town, or proposed to be located in the Town, to exempt from payment of municipal

property tax, in whole or part, or to determine a stabilized amount of taxes on, commercial or

manufacturing property for a period not to exceed ten (10) years, subject to the requirements of

this Chapter.

321-20 Application Procedure for stabilization. The application procedure shall proceed as

follows:

A. Owners of commercial or manufacturing property eligible for tax exemption or

stabilization under this Chapter shall file an application for tax relief with the Town

Clerk, on a form provided for that purpose and which shall include:1. The nature of the building, alterations and/or improvements to be made;

2. The nature and extent of any proposed job creation; and

3. A certification by the applicant that the application meets the eligibility

requirements of this Chapter.

B. The application shall be submitted to the Town Council at its next regularly

scheduled meeting. The Town Council shall then refer said application to the

Budget and Financial Review Board for an advisory recommendation. Upon

receipt of the Budget and Financial Review Board’s recommendation the Town

Council shall vote to advertise the application fourteen (14) days before the date of

the scheduled public hearing. The advertisement shall state that the application has

been received, the name and address of the applicant, the date, time and location of

the public hearing, and that a copy of the application may be reviewed at the Town

Clerk's office during regular business hours.

321-21 Findings required. The Town Council shall enter into an agreement to exempt property

from taxation in whole or part, or to stabilize taxes on property, only if it finds that:

A. Granting of the exemption or stabilization will inure to the benefit of the Town by

reason of:

1. the willingness of the manufacturer or commercial firm or concern to locate in

the Town; or

2. the willingness of a manufacturing or commercial firm or concern to expand

facilities with an increase in employment or the willingness of a commercial or

manufacturing firm or concern to retain or expand its facility in the Town and

not reduce its work force in the Town.

B. Granting of the exemption or stabilization of taxes will inure to the benefit of the Town

by reason of the willingness of a manufacturing or commercial firm or concern or

property owner to construct new or to replace, reconstruct, expand, retain, or remodel

existing buildings, facilities, fixtures, machinery, or equipment with modern buildings,

facilities, fixtures, machinery, or equipment, resulting in an increase in plant or

commercial building investment by the firm or concern in the town of not less than two

million dollars ($2,000,000.) in real property and/or tangible improvements, excluding

the purchase price of any real property.

321-22 Effect of agreement. Except as provided in section 321-23, property for which taxes have

been exempted in whole or part or stabilized pursuant to this chapter shall not, during the period

for which taxes have been exempted or stabilized, be further liable to taxation by the Town so long

as the property is used for the manufacturing or commercial purpose for which the exemption or

stabilization was granted. Additionally:

A. Any applicant for tax agreement pursuant to this article must be current on all tax, userfees and any other payments owed to the Town and otherwise be in good standing to

operate as a business in the State of Rhode Island at the time the application for a tax

agreement is filed with the Town Clerk.

B. Any agreement made under the provisions of this chapter shall be considered null and

void, and of no further force and effect, and shall cause any and all taxes exempted

under the agreement to become immediately due and payable, due to:

1. A change in use, such that the property is no longer used solely for the

manufacturing or commercial purpose for which the exemption or stabilization

was granted;

2. Nonpayment or late-payment of taxes due under this article if such non-

payment or late payment is not cured within sixty (60) days of any such

delinquency; provided however, that the taxpayer may petition the Town

Council to maintain the tax agreement one time during the term of the

agreement as a result of any non-payment or late payment. In addition, all

authority granted to the Town in the General Laws to sell property at tax sale

shall remain in full force and effect during the period of any tax agreement;

3. Nonpayment or late-payment of any municipal fees if such non-payment or late

payment is not cured within sixty (60) days of any such delinquency; provided

however, that the taxpayer may petition the Town Council to maintain the tax

agreement one time during the term of the agreement as a result of any non-

payment or late payment; or

4. Violations of any local building code and/or zoning ordinance during or after

construction and/or relocation that is not cured within sixty (60) days of notice

of violation; provided however, that the taxpayer may petition the Town

Council to maintain the tax agreement one time during the term of the

agreement as a result of any local violations.

C. The benefits of a tax agreement obtained pursuant to this article, upon Town Council

approval, shall be transferable to property owners and tenants, as long as the property

is used solely for the manufacturing or commercial purpose for which the agreement

was granted; however, the duration of the agreement period shall not be extended.

D. A business receiving tax relief under this section that replaces or adds employees

working at the property which is subject to an agreement, agrees that among applicants

it deems, in its sole discretion, to be equally qualified, it will give hiring preference to

residents of the town of Smithfield.321-23 Extent of exemption or stabilization. Notwithstanding any vote of, or findings by the Town Council, the property shall be assessed for and shall pay that portion of the tax, if any, assessed by the Town for the purpose of paying the indebtedness of the Town and the indebtedness of the State or any political subdivision to the extent assessed upon or apportioned to the Town, and the interest thereon, and for appropriation to any sinking fund of the Town, which portion of the tax shall be paid in full, and the taxes so assessed and collected shall be kept in a separate account and used only for that purpose. 321-24 Effective date of agreement. Construction shall be complete and the business shall be fully operational as of December 31 to qualify for relief on the subsequent tax bill. Application is due to the Assessor no later than January 31 following the December 31 on which the business begins operation and the agreement has been approved by the Town Council. An agreement for exemption or stabilization of taxes made pursuant to this Chapter shall take effect on the first tax bill following the approval of the application. 321-25 Annual Certification. The Tax Assessor shall on annual basis perform a review of all existing tax stabilization agreements to ensure compliance with the terms and conditions of the agreement as well as the provisions of this ordinance and file an annual report with the Town Council regarding the same. 321-26 Severability. If any one section of this article is found to be unenforceable, then the other provisions herein shall continue to have the same force and effect as if the unenforceable provision were not passed as part of this article. Section 2. This ordinance shall take effect thirty (30) days after its adoption. REFERENCE R.I. Gen. Laws § 44-3-9.11

ANALYSIS OF TAX STABILIZATION ORDINANCES FOR SIMILAR TOWNS IN RHODE ISLAND

Ordinance Application Must Be Current On Anti‐

Notes Term Minimum Investment Strict Schedule Transferrable Delinquency Employment Other

Section(s) Fee Taxes, Fees Etc. Cannibalization

Smithfield 321‐21 to 321‐26 SUBJECT / work in progress 10 years no $2 Million yes no yes, with council 60 days, one council make effort to hire not addressed

approval request for relief local

Cranston 3.64 to 3.100 multiple ordinances based on varies, 5 ‐ 20 no varies, based on type yes, and for three yes, based on type no, and claw back and only for "technology some must retain or yes City liens property for claw

property type and use years, based and use of property years except by and use of property penalty applies if original property", exemption is increase over three back purposes

on type and approval of council owner vacates within forfeited, but can be years, some must

use of term of agreement reinstated the following increase # of

property fiscal year employees

Johnston NONE Nothing in local ordinance n/a n/a n/a n/a n/a n/a n/a n/a n/a NO LOCAL ORDINANCE

Lincoln 228‐21 to 228‐23 States explicitly that terms and 20 years no no not addressed no not addressed not addressed not addressed yes

conditions are to be negotiated by

town administrator (elected

position in Lincoln)

North Providence 32‐171 to 32‐182 only one agreement for 10 years n/a specific not addressed (was for Yes, only for one yes, for transfer for not addressed make effort to hire not addressed "Buy North Providence" ‐ make

"CharterCARE" is codified, no specific entity) property, calls out other than foreclosure local effort to buy goods and

general stabilization ordinance actual tax payment services locally

for RP, hybrid

payment and

assessment

reduction on PP

North Smithfield 6‐3.11 10 years no no not addressed Yes, based on yes not addressed not addressed not addressed

assessment

Scituate NONE Nothing in local ordinance n/a n/a n/a n/a n/a n/a n/a n/a n/a NO LOCAL ORDINANCE

South Kingston 17‐50 to 17‐58 10 years no no not addressed no council must review council must review not addressed not addressed

Warren 7‐31 only applies to increase of real 5 year no no not addressed yes not without council stabilization ceases must increase yes

property value approval, and claw back immediately upon default proportionate to size

applies if original owner (no specifics as to extent of increase

vacates within eight delinquency)

years from granting of

agreement

Warwick 74‐147 to 74‐152 only allowed in certain zones 15 years $3500, non‐ $5 Million yes, and in good yes, based on base yes 60 days, one council not addressed yes ‐ must start construction within

refundable standing with RI SOS value first 5 years, request for relief 12 months and finish within 36

new assessment for months of application

years 6‐15 ‐ sunsets in 2027 (10 years from

adoption of ordinance)

Westerly 229‐12 to 229‐15 5 or 10 years, no 20% of current value yes, and must have no Yes, based on not addressed not addressed not addressed not addressed

based on use or 100,000, whichever violations of building assessment, varies

and type is less code based on use and

typeMemorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

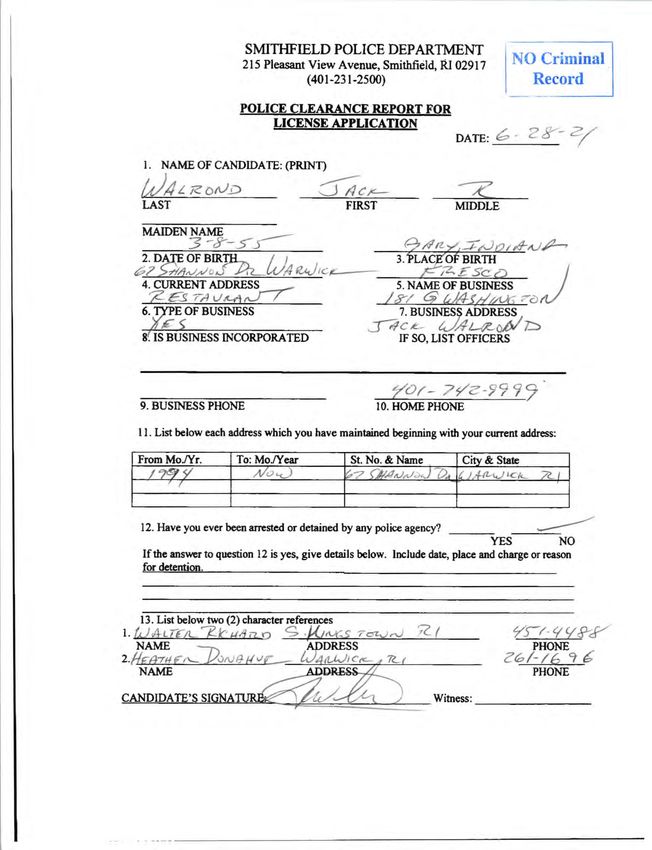

SUBJECT: Public Hearing for a new Class B-Victualler Beverage License for Fresco Ditto, Inc.,

d/b/a “Fresco” to include Outdoor Seating/Bar Service for the January 18 th Town

Council Meeting

BACKGROUND:

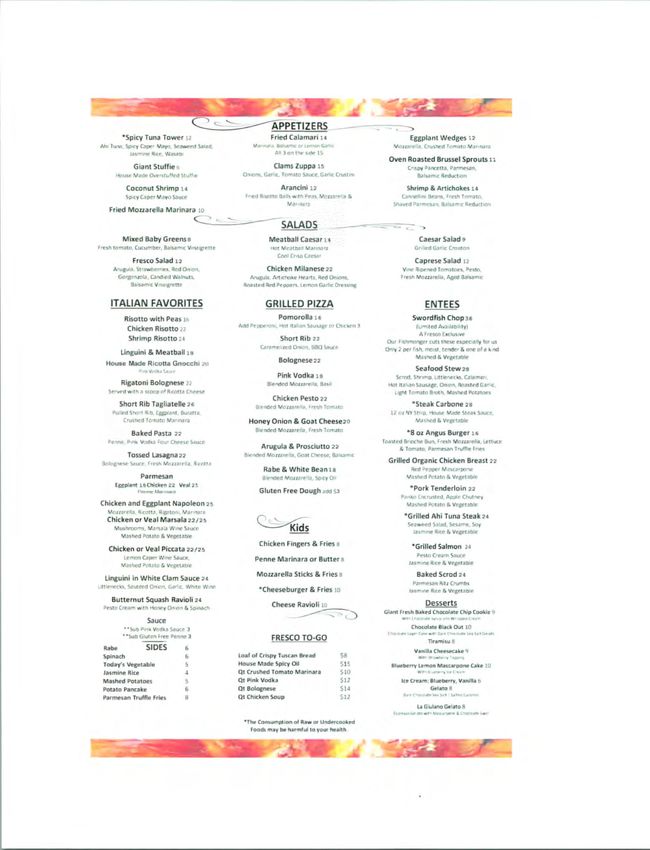

Conduct a Public Hearing to act upon approving a new Class B-Victualler Beverage License for Fresco

Ditto, Inc., d/b/a “Fresco”, located at 181 George Washington Highway to include Outdoor Seating/Bar

Service.

TOWN REVENUE:

Fee for Liquor License is $600.00 per year

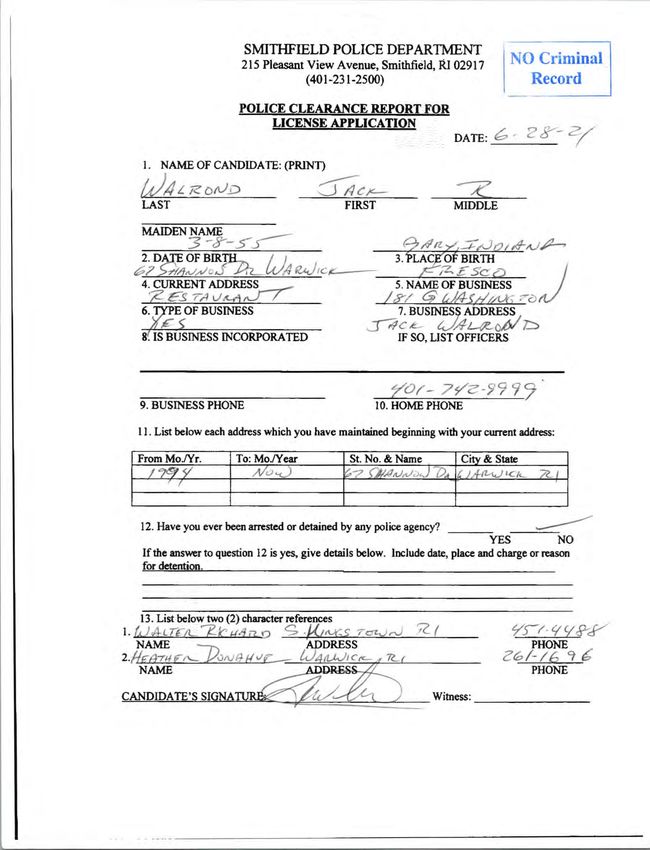

SUPPORTING DOCUMENTS:

Copy of application

Copy of BCI – No Record

Copy of Notice to abutters

Copy of radius map and abutters list

TIP Cards

Notice of Public Hearing that appeared in the Valley Breeze (run dates were January 6, 2022 and January

13, 2022)

Copy of menu

Drawing of outdoor seating/bar service area

Certificate of Good StandingRECOMMENDED MOTION: Move that the Smithfield Town Council approve a new Class B-Victualler Beverage License for Fresco Ditto, Inc., d/b/a “Fresco”, located at 181 George Washington Highway, to include Outdoor Seating/Bar Service, with the hours of operation to be Monday through Sunday 6:00 a.m. to 1:00 a.m., as applied, subject to compliance with all State regulations, local ordinances, a copy of their Retail Sales Permit, final approval from the RI Department of Health and a final inspection from the Fire Department.

If-.";

im On Premise

Issued: 6/11/2020 Expires: 5/31/2021^

ll#^347469 •

STEPHEN M BURGESS

2931 W Shore Rd .%

Warwick, Rl 02886-5448 ""1 J'

For service visit us online at www.gettips.po^^^^^

TIPS Trainer: Dawn Kidd, 41(^4

i

I

yfi" W

'I

i '. ^T ,1

■■ .-*•-■• I-".' '■"•1*.*.

rt Pike

02825

t> j

k *"4 #• ♦ fc

.t:--. Tr te: 11/15/2022

3 *•—

I, -i *«-.» ■• -f •

4 m k—»•!-!»•Memorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

SUBJECT: Show Cause Hearing for the January 18th Town Council Meeting

RECOMMENDED MOTION:

Conduct a Show Cause Hearing to consider the possible suspension, revocation or other sanction

regarding Liquor Licenses due to non-renewal or non-compliance with the conditions of renewal:

1. DLA, LLC d/b/a “Parma Ristorante”, 266 Putnam Pike, Unit 1 (Failure to produce a Certificate of

Good Standing and copy of TIP Cards)

2. Ichiraku, LLC d/b/a “Ichiraku Ramen and Fusion”, 970 Douglas Pike (Failure to obtain a

Certificate of Good Standing)

3. Lola’s Lounge, LLC d/b/a “Lola’s Lounge”, 55 Douglas Pike (Failure to pay outstanding tangible

taxes and failure to have a fire inspection done)

4. Rebel Alliance Group, LLC d/b/a “Bistecca Chop House”, 332 Farnum Pike (Failure to obtain a

Certificate of Good Standing and outstanding tangible taxes)Memorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

SUBJECT: New Victualling License for Fresco Ditto, Inc. d/b/a “Fresco”, for the January 18 th Town

Council Meeting

BACKGROUND:

Fresco Ditto, Inc., d/b/a “Fresco”, has applied for a new Victualling License for their business located at

181 George Washington Highway.

TOWN REVENUE:

Fee for a Victualling License is $50 per year

SUPPORTING DOCUMENTS:

Copy of application

Copy of BCI – No Record

RECOMMENDED MOTION:

Move that the Smithfield Town Council approve a new Victualling License for Fresco Ditto, Inc. d/b/a

“Fresco”, 181 George Washington Highway, as applied, subject to compliance with all State regulations,

local ordinances, final approval from the RI Department of Health and a copy of the Retail Sales Permit.Memorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

SUBJECT: New Entertainment License for Fresco Ditto, Inc. d/b/a “Fresco” for the January 18th

Town Council Meeting

BACKGROUND:

Fresco Ditto, Inc. d/b/a “Fresco”, has applied for a new Entertainment License for their business located

at 181 George Washington Highway.

TOWN REVENUE:

The cost for a new Entertainment License is $100.00 plus a one-time initial application fee of $15.00

SUPPORTING DOCUMENTS:

Copy of License Application

Copy of BCI – No Record

RECOMMENDED MOTION:

Move that the Smithfield Town Council approve a new Entertainment License for Fresco Ditto, Inc. d/b/a

“Fresco”, for their business located at 181 George Washington Highway, as applied, subject to

compliance with all State regulations and local ordinances.Memorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

SUBJECT: New Special Dance License for Fresco Ditto, Inc. d/b/a “Fresco” for the January 18 th

Town Council Meeting

BACKGROUND:

Fresco Ditto, Inc. d/b/a “Fresco”, has applied for a new Special Dance License for their business located

at 181 George Washington Highway.

TOWN REVENUE:

The cost for a new Special Dance License is $1.00

SUPPORTING DOCUMENTS:

Copy of License Application

Copy of BCI – No Record

RECOMMENDED MOTION:

Move that the Smithfield Town Council approve a new Special Dance License for Fresco Ditto, Inc. d/b/a

“Fresco”, for their business located at 181 George Washington Highway, as applied, subject to

compliance with all State regulations and local ordinances.Memorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

SUBJECT: Annual renewal of three (3) Victualling Only Licenses for the January 18 th Town Council

Meeting

BACKGROUND:

Victualling Licenses are due for renewal the first week in December. The businesses listed below have

filed their applications for renewal.

TOWN REVENUE:

The cost to renew the Victualling Only License is $50.00 per year.

APPROVAL STATUS:

Applications are complete for approval by the Town Council.

RECOMMENDED MOTION:

Move that the Smithfield Town Council approve the annual renewal of three (3) Victualling Only

Licenses, as listed, as applied, subject to compliance with all State regulations and local ordinances.

1. ALG 33 Enterprises, Inc. d/b/a “Piezoni’s”, 259 Putnam Pike

2. Target Corporation d/b/a “Target Store T-1404”, 371 Putnam Pike

3. Vibe Nutrition RI, LLC d/b/a “Vibe Nutrition, LLC”, 285 George Washington HighwayMemorandum

DATE: January 12, 2022

TO: Smithfield Town Council

FROM: Carol Banville – License Coordinator

SUBJECT: Mobile Food Truck License Renewal for the January 18th Town Council Meeting

BACKGROUND:

The business listed below has filed their application for renewal.

TOWN REVENUE:

The cost for a Mobile Food Truck License is $75.00 per year, however, if the Mobile Food Truck

applicant has an existing restaurant then the fee would be $50.00 per year.

APPROVAL STATUS:

Application is complete for approval by the Town Council.

RECOMMENDED MOTION:

Move that the Smithfield Town Council approve the renewal of one (1) Mobile Food Truck License, as

applied, subject to compliance with all State regulations and local ordinances.

1. Rhode Island Kona, LLC d/b/a “Rhode Island Kona Ice”, to sell only frozen ice from a truck with

RI Reg. number 21700, 4 Cider Lane.Town of Smithfield

OFFICE OF FINANCE DIRECTOR/TAX COLLECTOR

64 FARNUM PIKE

SMITHFIELD, RHODE ISLAND 02917

TELEPHONE: (401) 233-1072 FACSIMILE: (401) 233-1060

EMAIL: BSILVIA@SMITHFIELDRI.COM

BRIAN SILVIA

FINANCE DIRECTOR

DATE: January 3, 2022

TO: The Honorable Smithfield Town Council

Cc: Randy Rossi, Town Manager

FROM: Brian Silvia, Finance Director

RE: Audited Financials for the Fiscal Year Ended June 30, 2021

Background:

The audit document is a compilation of the Town’s financial results for the Fiscal Year Ended June 30,

2021, reviewed and presented by a certified public accounting firm according to generally accepted

accounting principles.

Financial Impact:

The Town Council’s acceptance of this document will enable the Town to forward copies of the document to

rating agencies, financial institutions and appropriate state agencies.

Filing this document on a timely basis will enable and enhance the Town’s strength when the Town is ready

to issue bonds in the future for the fire station or any other financing opportunities as they may arise.

MOTION:

That the Smithfield Town Council accepts the audited financial statements for the Fiscal Year Ended June

30, 2021 from the audit firm of Hague, Sahady & Co., P.C.

townofsmithfield SMITHFIELDRI.COM @SmithfieldRITown of Smithfield, Rhode Island

Presentation Summary

Fiscal Year Ended June 30, 2021

▪ Independent Auditor’s Report

▪ Independent Auditor’s Report will include an Unmodified Opinion, which indicates that the

Statements are presented fairly in all material respects.

▪ Auditor’s Report provides an opinion on the Governmental Activities, Business-Type Activities,

Each Major Fund, and the Aggregate Remaining Fund Information.

▪ A Fund is considered a Major Fund if the:

▪ Total assets and deferred outflows, or liabilities and deferred inflows, or revenues, or

expenditures/expenses of that individual fund are at least 10% of the corresponding total

for that fund category. AND

▪ Total asset and deferred outflows, or liabilities and deferred inflows, or revenues, or

expenditures/expenses of that individual fund type are at least 5% of the corresponding

total for that all governmental and enterprise funds combined.

▪ Major funds in FY2021 include General Fund, School Unrestricted and School Renovations Bond.

▪ Management’s Discussion and Analysis (MD&A)

▪ Serves as a narrative overview and analysis of the Town’s Financial Activities for the Fiscal Year

ending June 30, 2021.

▪ Presents financial highlights in the Government-Wide Financials and the Fund Financials.

▪ Government-Wide Financial Statements (pages 18-21)

▪ Utilize the full accrual basis of accounting.

▪ Statement of Net Position

▪ Reports all assets, deferred outflows, liabilities, deferred inflows with the net amount being

reported as net position.

▪ Presentation of the aggregate amount of assets, liabilities and outflows for the

governmental activities and business-type activities.

▪ Unrestricted Net Position – cumulative deficit of $87,023,814 for the Governmental

Activities. Deficit position is primarily the result of the Town’s unfunded pension and

OPEB liabilities.

▪ Statement of Activities

▪ Reports the results of activities for fiscal year ending June 30, 2021.

▪ Governmental Activities reported a surplus of $49,243,983 while Business-Type Activities

reported a surplus of $372,499.

▪ The large change in the governmental activities was due to the proceeds of $40,000,000

Bond Anticipation Note.

▪ The information presented in the Statement of Activities does not utilize the same accounting

recognition methods that the Town uses to prepare the budget. The Fund Level Statements will

present the results in a manner consistent with the Town’s budget practices.▪ Governmental Funds Exhibits (pages 22 -25)

▪ These exhibits focus on the current financial resources (modified accrual basis of accounting) and

therefore include only current assets, deferred outflows of resources, liabilities, deferred inflows of

resources, and fund balance.

▪ Major Fund are broken out separately while the aggregate remaining funds are combined in one

column, “Non-Major Governmental Funds.” The details of the Non-Major governmental funds can

be found in supplementary information, currently pages 156 to 173.

▪ The Balance Sheet on page 22 presents a snapshot of the financial position of the Town of Smithfield

at June 30, 2021.

▪ Investments are valued at fair value (market value) while receivables are presented net of an

estimated allowance for doubtful accounts.

▪ Allowance is an estimate prepared by management. Allowance is normally based on past

experience and future expectation. An allowance is recorded for past due tax receivables,

EMS rescue fees, CDBG loans, etc.

▪ Unavailable tax and fee revenue represents the amount of receivables at year end which are not

considered available and therefore not recognized as revenue at June 30, 2021. Taxes are considered

available and recognized as revenue if they are collected within 60 days of the end of the fiscal year.

▪ Fund Balance is broken down into 4 categories:

▪ General Fund – Non-Spendable Fund Balance of $2,006,020 represents the amount of

prepaid expenditures and amounts of receivables (including interfund receivables) which

are not expected to be collected within one year:

• Salt Barn Fund - $1,010,496

• Greenville Public Library - $161,171

• Capital Lease Fund - $834,352

▪ General Fund – Committed Fund Balance of $6,352,751 represents amounts committed for

specific purposes per Town Council ordinance. At June 30, 2021 the committed fund

balance consisted of:

• Capital expenditure carryover - $2,636,455

• Re-appropriation of balances to 2022 expenditures - $3,116,297

• Amount to supplement fiscal 2022 budget appropriation - $600,000

▪ General Fund – Unassigned Fund Balance – This represents the amount of Fund Balance

that is not committed, restricted, or assigned for other purposes. In accordance with the

Town’s Home Rule Charter, Fund Balance was to be maintained at 8% of the subsequent

year’s budget. In accordance with the Charter, any amount in excess of the applicable

percentage is to be allocated 80% to Capital Reserve Fund and 20% to Land Trust Reserve

Fund.

▪ Statement of Revenues, Expenditures, and Changes in Fund Balances (page 24) presents the results

of operations for the fiscal year ended June 30, 2021.

▪ Net change (income or loss) in Fund Balances or fiscal 2021 in accordance with GAAP:

▪ General Fund – ($414,463), net loss.

▪ School Unrestricted Fund – $687,643, net gain.

▪ School Renovations Fund - $13,853,304, net gain.

▪ Non-Major Governmental Fund – ($1,454,782), net loss.

▪ The details of the net decrease in fund balance for non-major governmental funds can be found on

pages 156 to 173.▪ Budgetary Basis for the Town’s General Fund and School Unrestricted Fund (pages 123-130)

▪ Town’s General Fund

▪ Page 123 – positive revenue variance before other financing sources of $744,666

(represents approximately 1.0% of the 2021 budget). Overall negative revenue and other

financing sources variance of ($130,334).

▪ Page 126 – positive expenditure and other financing uses variance of $132,570. This is

after including RUB carryover balances of $3,116,297 which are available for use in fiscal

2022.

▪ Budgetary Basis surplus fiscal 2021 is $2,236.

▪ Page 127 provides reconciliation from GAAP to budgetary basis.

▪ School’s Unrestricted Fund

▪ Revenue surplus - $8,005

▪ Positive variance in expenditures - $681,863

▪ Budgetary Surplus for fiscal 2021 - $689,868 (2.12% of the budget)

▪ Enterprise Funds (pages 26-29)

▪ Page 26 – Statement of Net Position – reports all assets, deferred outflows, liabilities, deferred

inflows, and net position utilizing full accrual basis of accounting.

▪ Statement of Net Position presents a snapshot of these balances at June 30, 2021.

▪ Restricted cash in Sewer Authority Fund represents the debt service reserve funds maintained by

Wells Fargo in accordance with requirements of bond issuance.

▪ All proprietary funds have positive Net Position at June 30, 2021.

▪ Page 27 – Statement of Revenues, Expenses and Changes in Fund Net Position presents the results

of operations for the fiscal year ended June 30, 2021.

▪ Sewer Authority – Net loss of $295,352 for fiscal 2021 as compared to net loss of $83,670

for fiscal 2020. The change from fiscal 2020 is attributable to the additional $205,725

which was transferred to the General Fund in accordance with the approved budget.

▪ Water Fund – Net income of $531,795 for fiscal 2021 versus $346,768 for fiscal 2020.

The change from fiscal 2020 is attributable to the additional $226,142 which was

transferred to the General Fund in accordance with the approved budget.

▪ Ice Rink – Net loss of $20,101 for fiscal 2021 versus net loss of $22,083

▪ School Lunch Program – Net gain in fiscal 2021 totaling $156,157 versus net income of

$15,944 for fiscal 2020.

▪ Fiduciary Funds (pages 30-31)

▪ Pension Trust Funds, OPEB Trust Fund, and Agency Funds.

▪ Measured utilizing full accrual basis of accounting

▪ Investments are reported at fair value at June 30, 2021.

▪ Police Pension Trust Net Position: $13,702,385

▪ Fire Pension Trust Net Position: $32,429,794

▪ OPEB Trust Fund Net Position: $6,115,083

▪ Change in Net Position for fiscal 2021

▪ Police Pension Trust Fund – increase of $3,219,862

▪ Fire Pension Trust Fund – increase of $6,342,985

▪ OPEB Trust Fund – increase of $1,811,924▪ Required Supplementary Information (pages 123-155)

▪ General Fund Budgetary Comparison (pages 123-127)

▪ School Unrestricted Fund Budgetary Comparison (pages 128-130)

▪ Pension required exhibits – will continue to accumulate to include 10 years’ worth of data. (pages

131-152)

▪ OPEB required exhibits (page 153-155)

▪ Other Supplementary Information and Other Exhibits (pages 156-178)

▪ Non-Major Governmental Funds (pages 156-173)

▪ Custodial Funds (page 174)

▪ Funds that comprise the Town’s General Fund (pages 175-176)

▪ Schedule of Property Taxes Receivable (pages 177-178)

▪ Other Items for Discussion

▪ Auditing Standards define a material weakness of controls as a deficiency, or combination of

deficiencies, in internal control such that there is a reasonable possibility that a material

misstatement of the Town’s financial statements will not be prevented or detected and corrected on

a timely basis. A significant deficiency is defined as a deficiency, or combination of deficiencies, in

internal control that is less severe than a material misstatement, yet important enough to merit

attention by those charged with governance.

▪ At this time there are no reports of any material weaknesses or significant deficiencies.MEMO

Date: January 18, 2022

To: Smithfield Town Council

From: Christopher Celeste, Assessor

Re: Tax Abatements

BACKGROUND:

Abatements are granted by the assessor as a result of assessment appeals on real estate, motor

vehicles, and personal property. Adjustments are also made to motor vehicle tax bills to correct

for erroneous data received from the Rhode Island Division of Motor Vehicles, including incorrect

tax town and registration data. Additionally, the tax collector may request the abatement of taxes

deemed to be uncollectible.

FINANCIAL IMPACT:

Total abatements for this period= $559.57

ATTACHMENT:

Abatement Detail Report

MOTION:

Moved that the Smithfield Town Council approve the tax abatements in the amount of $559.57

The abatements contained herein

are submitted for your approval by:

Christopher Celeste, Assessor

Assessor's Office Christopher Celeste, RICA

64 Farnum Pike (401) 233-1014

Smithfield, RI 02917 www.SmithfieldRI.comABATEMENT DETAIL

January 18, 2022

ACCOUNT # TYPE PROPERTY OWNER YEAR ORIGINAL REVISED REASON ABATEMENT

03-3592-00 RE COTE PAUL AND GAIL 2021 $286,800 $282,600 Appeal $71.95

02-0033-04 RE SHAW JAMES R REVOCABLE TRU 2021 $485,200 $473,300 Appeal $203.85

10-0635-50 PP JUICE BAR AND CO 2021 $44,750 $40,000 Appeal $283.77

Town Council Authorization:

Real Estate Subtotal: $275.80

Motor Vehicle Subtotal: $0.00

Personal Property Subtotal: $283.77

Total Abatements: $559.57You can also read