OPEN ENROLLMENT 2019 BENEFITS INFORMATION SESSION - Open Enrollment: November 1 - November 21, 2018

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

OPEN ENROLLMENT 2019

BENEFITS

INFORMATION SESSION

Open Enrollment:

November 1 – November 21, 2018

AGENDA

Welcome and Overview Vision

• Highlights for 2019

• Wellness Incentive Accident and Critical Illness

• Spousal/LDA Premium

• Tobacco Premium Hyatt Legal

• “Alex” – Online Benefits Counselor KinderCare

Medical and Prescription Drug

• NEW *PPO 3 HSA* How to Enroll

Health Savings Account (HSA) Paid Time Off Changes

• Paid Parental Leave

Flexible Spending Accounts (FSAs) • Revised Vacation Policy

• Payout Details

Dental

Open Q&A

OPEN ENROLLMENT HIGHLIGHTS

• Open Enrollment will be held from November 1 to November 21, 2018

• All benefit changes and enrollments will be effective January 1, 2019

• All benefit elections are made through Employee Self Service (ESS): https://lawson.luc.edu

Benefit Carrier/Administrator

Medical BlueCross BlueShield of Illinois

Prescription Drug CVS/Caremark

Health Savings Account – NEW IN 2019 BenefitWallet

Flexible Spending Account BenefitExpress

Dental – PPO Delta Dental of Illinois

Dental –DHMO Guardian/First Commonwealth

Vision VSP

Life/AD&D Reliance Standard

Disability Reliance Standard / Matrix

FMLA Matrix

Accident Reliance Standard

Critical Illness Reliance Standard

Pre Paid Legal Hyatt Legal

Pet Insurance Nationwide

Child Care Tuition Benefit– NEW IN 2019 KinderCare

HIGHLIGHTS FOR 2019

• New Medical Plan Option PPO 3 HSA • Vision Insurance

• Lower monthly premiums per pay period • Frame allowance increasing from $150 to $180

• Loyola will contribute money to your Health

Savings Account (HSA) • Hyatt Legal

• $600 for You, Or • Includes Identity Management Services

• $1,200 for You + 1 or More

• Combined medical and prescription out of

• Limited Flexible Spending Account (LFSA)

pocket maximum

• Dental and vision expenses

• $10,000 Critical Illness Benefit

• Accident Benefit

• KinderCare Child Care Tuition Benefit

• Health Savings Account (HSA) • Tuition savings

• Available for PPO 3 HSA participants

• Save tax-free for medical expenses now or in

retirement • Paid Time Off Policy Changes

• Receive Loyola contribution in January 2019 • Paid Parental Leave

• Use funds tax-free for qualified expenses

• Invest or save for future expenses

ENROLLING IN BENEFITS

• Annual Enrollment: Thursday, November 1 – Wednesday, November 21

• Use Employee Self-Service (ESS): https://lawson.luc.edu

• Must be connected to Loyola’s secure network

• Troubles? Contact the ITS Help Desk

• helpdesk@luc.edu or 773-508-4487

• What You Need to Do During Open Enrollment:

• If you don’t enroll, you will miss out on the opportunity to enroll in PPO 3

HSA, and have an HSA in 2019 with contributions from Loyola

• Must re-enroll for FSA (PPO 1 and PPO 2 only) through ESS

• Must complete Tobacco Premium and Spousal Premium Certifications

• Verify your dependents/beneficiaries

Reminder: Both medical plan participants and their covered spouse/LDAs must

complete the respective Spousal/LDA and wellness incentive by December 7, 2018 in

order to receive the $50 monthly premium discount in 2019.

MEDICAL & PRESCRIPTION DRUG (RX)

MEDICAL PLAN COMPARISONS

Medical PPO 1 PPO 2 PPO 3

$500 (You)/ $1,200 (You)/

Annual Deductible

$1,000 (You + 1 or More) $2,400 (You + 1 or More)

$3,000 (You)/ $4,000 (You)/

Out of Pocket Max

$6,000 (You + 1 or More) $8,000 (You + 1 or More)

90% Home Hospital 90% Home Hospital

Coinsurance

80% In Network 80% In Network

Office Visit Deductible & Coinsurance Deductible & Coinsurance

Wellness Visit Covered at 100% Covered at 100%

Hospital Inpatient –

$100 Copay then 90% Coinsurance $100 Copay then 90% Coinsurance

Home Hospital

$250 Copay + Deductible & $250 Copay + Deductible &

Hospital Inpatient

Coinsurance Coinsurance

Hospital Outpatient Deductible & Coinsurance Deductible & Coinsurance

Pharmacy PPO 1 PPO 2 PPO 3

Deductible $100 (You)/ $200 (You + 1 or More) $100 (You)/ $200 (You + 1 or More)

Does not apply to mail order Does not apply to mail order

Out of Pocket Max $3,000 (You)/ $3,000 (You)/

$6,000 (You + 1 or More) $6,000 (You + 1 or More)

Generic 15% up to $200/script 15% up to $200/script

Preferred Brand 30% up to $200/script 30% up to $200/script

Non-Preferred Brand 45% up to $400/script 45% up to $400/script

Mail Order 5% / 15% / 25% 5% / 15% / 25%

MEDICAL PLAN COMPARISONS

Medical PPO 1 PPO 2 PPO 3

$500 (You)/ $1,200 (You)/ $2,800 (You)/

Annual Deductible

$1,000 (You + 1 or More) $2,400 (You + 1 or More) $5,600 (You + 1 or More)

$5,000 (You)/

$3,000 (You)/ $4,000 (You)/

Out of Pocket Max $10,000 (You + 1 or More)

$6,000 (You + 1 or More) $8,000 (You + 1 or More)

*Includes Rx

90% Home Hospital 90% Home Hospital 90% Home Hospital

Coinsurance

80% In Network 80% In Network 80% In Network

Office Visit Deductible & Coinsurance Deductible & Coinsurance Deductible & Coinsurance

Wellness Visit Covered at 100% Covered at 100% Covered at 100%

Hospital Inpatient –

$100 Copay then 90% Coinsurance $100 Copay then 90% Coinsurance Deductible & Coinsurance

Home Hospital

$250 Copay + Deductible & $250 Copay + Deductible &

Hospital Inpatient Deductible & Coinsurance

Coinsurance Coinsurance

Hospital Outpatient Deductible & Coinsurance Deductible & Coinsurance Deductible & Coinsurance

Pharmacy PPO 1 PPO 2 PPO 3

Deductible $100 (You)/ $200 (You + 1 or More) $100 (You)/ $200 (You + 1 or More)

Included in Medical

Does not apply to mail order Does not apply to mail order

Out of Pocket Max $3,000 (You)/ $3,000 (You)/

Included in Medical

$6,000 (You + 1 or More) $6,000 (You + 1 or More)

Generic 15% up to $200/script 15% up to $200/script Deductible & Coinsurance

Preferred Brand 30% up to $200/script 30% up to $200/script Deductible & Coinsurance

Non-Preferred Brand 45% up to $400/script 45% up to $400/script Deductible & Coinsurance

Mail Order 5% / 15% / 25% 5% / 15% / 25% Deductible & Coinsurance

ADVANTAGES OF PPO 3 HSA

Family Deductible is Embedded – No single individual on a plan with employee and a spouse/LDA

and/or child(ren) will have to pay a deductible higher than the individual deductible amount

Out of Pocket Maximum – Includes Deductible, Coinsurance and Prescription Drug Expenses

• PPO 1 & PPO 2 have a separate medical and RX out of pocket maximum, the total of both in

either plan option is greater than that of PPO 3 HSA’s combined out of pocket maximum

Health Savings Account (HSA) Compatible – Includes an HSA to use for eligible medical expenses

• Loyola contributes $600 (You) or $1,200 (You + 1 or More)

• You can contribute on a pre-tax basis, too!

Limited FSA – You can contribute up to $2,650 pre-tax to use for eligible 2019 dental and vision expenses

Preventive Drug List– Some preventive prescriptions require you to only pay coinsurance, even without

meeting the deductible yet

Lower Premiums – PPO 1 and PPO 2 rates are increasing for 2019

• PPO 3 HSA monthly premiums are considerably lower than the existing plan options

Like the PPO 1 & PPO 2, you can still take advantage of:

• Preventive Exams and Certain Preventive Prescriptions covered at 100%

• National PPO Network – Utilizes the large national BCBS PPO Network; Coinsurance is 90%

when you use Home Hospitals

• Includes Virtual Visits, Benefits Value Advisor, Blue365 Deals and more

HEALTH SAVINGS ACCOUNT

(HSA)WHAT IS A HEALTH SAVINGS ACCOUNT

(HSA)?

An HSA is a bank account that allows you to save and pay for your share of everyday qualified

health care expenses tax-free.

You can pay for qualified expenses, for you, your spouse, and any tax dependent (including LDAs)

with your HSA– even if they are not covered by your health plan.

Loyola will make a contribution into your HSA account on January 1, 2019

Employee Only Employee + 1 or More

$600 $1,200

You can contribute up to the following amounts tax free (less Loyola's contribution) in 2019:

$3,500 total = $600 Loyola + up to $2,900 (you)

$7,000 total = $1,200 Loyola + up to $5,800 (you + 1 or more)

If you are 55 or older, you can contribute an additional $1,000 in catch-up contributions, too.HEALTH SAVINGS ACCOUNT (HSA)

Access the BenefitWallet member portal at

www.mybenefitwallet.com. Complete your

set up and you will be mailed a Visa® HSA

debit card.

www.mybenefitwalletsite.com/luc

Loyola will fund your HSA on January 1. You

can also contribute via payroll deduction on

a pre-tax basis.

• You can only access the funds that are

currently in your account.

• Choose to spend it on today’s health care

expenses or save for future expenses

• Never pay taxes when using your HSA for

qualified health care expenses.HEALTH SAVINGS ACCOUNT (HSA) Q&A

www.mybenefitwalletsite.com/luc

How do I qualify for an HSA?

You must be enrolled in an HSA qualified health plan option (PPO 3 HSA). If addition, you cannot be covered by another

health plan (including Medicare or Tricare) or be claimed as a dependent on another person’s tax return.

How do I make deposits to my HSA?

You can contribute to your account with payroll deductions, online by making deposits from your checking account, or

by mailing a personal check. Loyola will deposit the University’s contribution in January 2019.

What expenses qualify for payment from an HSA?

Funds in your HSA can be used to pay for any eligible medical, dental, or vision expenses – doctor’s visits, prescriptions,

lab tests, and hospitalizations. See IRS Publication 502 for a complete list of qualified expenses.

Do HSA funds expire?

Your HSA funds never expire. Any funds you don’t spend roll over year after year and can be saved and invested for

retirement. There is an annual limit for contributions, but the total balance of your account has no limit.

What happens if I change jobs or health plans?

You own your HSA. If you change jobs or health plans, you continue to own your account. If you enroll in another HSA-

qualified health plan, you can continue to contribute to your HSA. If you choose another type of health plan, you are still

eligible to spend the funds in your HSA on qualified medical expenses — for you, your spouse, and your tax dependents.

What are the fees for having this account?

The monthly maintenance fee is employer paid by Loyola. $1.90 per employee per month if the monthly average balance

is $3,000 or less. No fee if the monthly average balance is $3,000 or higher.EXAMPLES OF HOW EACH MEMBER COULD BENEFIT FROM AN HSA

Meet Mike. Age 23. Salary < $40,000

• Mike has limited resources because he is paying off student loans.

• He’s young and healthy, so he doesn’t have many health-related expenses.

• He enrolls in the PPO 3 plan because the per pay period premiums are less than PPO 1 & PPO 2.

o His annual premiums will be $600 and Loyola contributes $600 to his HSA.

• Mike also has the Accident and Critical Illness benefits that are also paid for by Loyola.

Why should he save in an HSA right now?

Mike can use his HSA

Once his HSA balance By starting now,

funds for qualified

reaches $1,000, Mike will build

health care expenses,

he can start investing an important safety net

such as office visits,

with his HSA – yet still for future health care

prescriptions,

access the funds expenses –or even

dental or

any time. retirement.

vision care.Meet Max and Emma. Age: Late 30s. Salary $40k - $120k

• A young family on a budget, with third child on the way.

• Emma knows she will satisfy her deductible.

• They have a high-deductible health plan with a $5,600 family deductible.

• Money is tight and they have very little disposable income.

PPO 2 PPO 3 HSA

Emma’s Deductible $1,200 $2,800

Coinsurance $2,800 $2,200

Maximum Medical Out of Pocket for Emma $4,000 $5,000

Maximum Prescription Out of Pocket for Emma $3,000 Included in Medical

Maximum Medical and RX Out of Pocket Maximum $7,000 -

Loyola HSA Contribution $0 ($1,200)

Annual Wellness Premium $7,025 $5,646

Estimated Annual Cost for Emma in 2019 $14,025 $9,446

Annual Difference between PPO 2 & PPO 3 HSA $4,579

Emma can take the premium and maximum out of pocket differential of $4,579 and

contribute that into her HSA.Meet Max and Emma. Age: Late 30s. Salary $40k - $120k

• Emma knows she will incur a medical expense so she can save in her HSA.

• Emma can use the funds as they accumulate or reimburse herself once they accumulate.

How can an HSA help them maximize their health care dollars?

Save on taxes

• When spending $1,000 on health care expenses through

their pre-tax HSA, they can save $350 in taxes.

Spend less on medical costs

• By using their pre-tax HSA to pay for health care, they will

spend up to 35% less on today’s health care costs.

Assumes 35% savings, 25% federal, 3% state, and 7% payroll tax savings. Payroll tax savings apply when

contributions are made through payroll only. Your savings may vary. Consult a tax advisor for more information.Joe & Julie Smith. Age: Early 50s.

• Joe and Julie Smith’s last child has just completed college and moved out of their family home.

• Now empty nesters, they are committed to retiring in the next 5-8 years .

• They have a good start on saving, but their biggest concern is the cost of health care in

retirement.

How can an HSA help them?

The average

couple needs

$370,000*

for medical

To get ready, expenses Once the HSA

they are in retirement. owner reaches age

maxing out 55, they can

their HSA contribute an extra

contributions $1,000 to the HSA

each year. each year.

*HealthView Services, 2016 Retirement Health Care Costs Data ReportJoe & Julie Smith. Age: Early 50s.

The Smiths still worry though. Will contributing to their HSAs help

pave the way to their golden years, even if they face health issues?

• They have over $1,000 in their HSA, so they are eligible to invest that money in a

variety of mutual funds available through BenefitWallet.

• Investment gains in HSAs are not taxed; this will preserve the Smiths’ savings for

future expenses.

• The chart below shows how investing your HSA funds can help you build your

health care savings nest egg.

$397,000 Assumes $3,000 contribution to

$400,000

investment account yearly, earning

8% annual return. All returns and

$300,000

principal remain invested each

$162,000 year.

$200,000

$53,000 BenefitWallet is not recommending any

$100,000

$23,000 investment, nor can it assure you of a

profit or protect you against any loss on

$0

any investment made under the

5 years 10 years 20 years 30 years BenefitWallet investment platform.Meet Andy and Alicia. Age: Early 60s.

• Andy and Alicia are planning to retire in the next couple of years. They have each diligently

saved in their 403(b) plans.

• Now, they would like to contribute up to the maximum in an HSA to help prepare for

retirement – whether for medical expenses or for everyday bills.

How can an HSA help them?

No minimum

After age 65,

required

HSA funds can be

distributions gives

used for any

flexibility to your

expense at all,

withdrawal strategy

just like a 403(b).

during retirement.

Transfers to the spouse

Spend your HSA on upon account holder’s

qualified medical death, with no tax

expenses in retirement, implications.

including Medicare

premiums (Parts A, B Not married? The

and D) – all tax free! HSAs for account will become

part of your estate.

retirementMeet Andy and Alicia. Age: Early 60s.

Regarding HSAs and Medicare, Andy and Alicia will want to

pay attention to these notable points.

• Becoming eligible for Medicare does not impact their ability to make

contributions or withdrawals from the HSA, assuming they remain

HSA eligible.

• If Alicia enrolls in Medicare, Andy (the HSA account holder) can still

contribute to the HSA as long as he is covered by an HSA-qualified

health plan.

• Once they are both enrolled in Medicare, they can no longer

contribute to the HSA, but they can use it to pay for qualified expenses.

Learn more about HSAs and Medicare on the HSA

education site: www.mybenefitwalletsite.com/lucACCIDENT & CRITICAL ILLNESS

BENEFIT PLANSACCIDENT PLAN This coverage is provided at

no cost to employees who

enroll in PPO 3 HSA

• Pays benefits, based on a schedule of services, when you

(coverage for other

seek treatment for injuries sustained in an accident dependents may be

purchased voluntarily).

• All benefits are paid directly to you, regardless of other

benefits you may receive

• You use the benefit as you see fit

• 24-hour coverage

• Guaranteed issue – no health questions

• No waiting periods

• No limit to the number of times you and your family can

use the plan

• Annual Wellness Benefit - $75CRITICAL ILLNESS

$10,000 CI coverage is

provided at no cost to

employees who enroll in

• CI pays a Lump sum benefit directly to you upon PPO 3 HSA (coverage for

diagnosis of a covered critical illness: other dependents may be

• Employee & Spouse: choose $10,000 or $20,000 purchased voluntarily).

• Spousal amount cannot exceed employee amount

• Additional costs due to a critical illness contribute to pressure you are already

under at the worst possible time

• Out-of-pocket medical expenses like co-pays, deductibles, and

coinsurance

• Durable Medical Equipment

• Lost income

• Home modification

• Dependent Child(ren): If elected, coverage will be equal to 25% of employee’s

approved amountCRITICAL ILLNESS

Category 1 Category 2 Category 3

• Life threatening • Heart Attack • Blindness

Cancer • Ruptured Cerebral, • Coma

Carotid or Aortic • Kidney (Renal)

Aneurysm Failure

• Stroke • Paralysis

• Severe Brain

Damage

This benefit includes a wellness benefit – if you receive a health

screening you will receive $50.FLEXIBLE SPENDING ACCOUNTS

FLEXIBLE SPENDING ACCOUNT (FSA)

• Tax free dollars to be used for qualified medical, dental, and vision expenses for you and your

tax qualified dependents as determined in the IRS Publication 502.

• FSA cards are loaded with the entire amount of your Health Care FSA annual election for full

use as of January 1, 2019.

• Use it or lose it. Consider signing-up via Employee Self-Service before November 21, 2018.

• Cannot have both an FSA and an HSA, if you are enrolled in the PPO 3 and receive the LUC

HSA contribution you cannot enroll in the FSA.

2019 Plan Year

Annual Max

$2,650

ContributionNEW JANUARY 1, 2019

LIMITED FLEXIBLE SPENDING ACCOUNT

(LFSA)

• The Limited FSA (LFSA) is similar to a Health Care FSA, however the LFSA only

reimburses for eligible dental and vision expenses.

• This account will be available if you are enrolled in PPO 3 HSA.

2019 Plan Year

Annual Max

$2,650

ContributionDEPENDENT CARE (DCFSA)

If you have eligible child or adult day care expenses while

working, then a Dependent Care FSA can help you pay your

expenses with tax-free money.

– Consider using tax-free dollars for Qualified Dependent Care expenses!

– Sign up through Employee Self-Service before November 21, 2018.

Examples of Reimbursable Expenses:

2019 Plan Year

• Babysitter Expenses

• Before & After School Expenses

• Day Care Center Expenses Annual Max

$5,000

• Preschool Tuition Contribution

• Elder Care (In Home or Day Care)NAVIGATING THE PRE-TAX OPTIONS

Compatibility Chart

Limited FSA

Health Dependent (Dental &

HSA Care FSA Care FSA Vision Only)

Enrolled in PPO 3 HSA

Enrolled in PPO 1 or

PPO 2DENTAL, VISION, HYATT LEGAL, KINDERCARE

DENTAL INSURANCE

Dental insurance options remain the same for 2019:

Delta Dental PPO Guardian/First Commonwealth DHMO

In-network dental care only,

Choose in-network dentists to

Available in Chicagoland and

receive highest level of benefits

Northwest Indiana only

Choose out-of-network providers

No out-of-network coverage

(at higher cost)VISION INSURANCE BENEFIT UPDATE VSP Retail Frame Allowance is increasing from $150 to $180 as of January 1, 2019. • This benefit may be used bi-annually (once every 2 years) VSP members also have access to discounts available at www.vsp.com Non-VSP members with a Loyola medical plan can take advantage of special vision discounts through BCBS. Visit www.blue365deals.com for more information

HYATT LEGAL PLAN ENHANCEMENT

Hyatt Legal Plan premiums remain the same for 2019, but will include Identity

Management Services as of January 1.

LifeStages Identity Management Services from Hyatt Legal Plans keeps pace with

emerging identity threats across all stages of your life, thanks to CyberScout, the

nation’s premier provider of identity services.

This chart shows how employees of all ages may benefit from Hyatt Legal:NEW JANUARY 1, 2019 KINDERCARE CHILD CARE TUITION BENEFIT • Loyola University Chicago has partnered with KinderCare to provide tuition savings on early childhood education programs. • When your child enrolls at a participating KinderCare Learning Center or Champions Before-and After-School Program, you'll save 10% on the cost of tuition as a Loyola University Chicago employee. • Visit www.kindercare.com/luc to find a location close to work or home. • Enroll in a Dependent Care FSA to also take advantage of tax savings on KinderCare services.

OPEN ENROLLMENT REMINDERS

TALK TO ALEX • Need assistance in picking a benefits package? • Alex is your personalized benefits counselor! • ALEX will help you understand medical terminology, and walk you through the basics of how your medical plans work using real life examples. • Answer several questions about your benefit utilization and lifestyle so Alex can help guide you to the best plan option for you. Visit ALEX: www.myalex.com/loyola/2019

ENROLLING IN BENEFITS

• Annual Enrollment: Thursday, November 1 – Wednesday, November 21

• Employee Self-Service (ESS): https://lawson.luc.edu

• Must be connected to Loyola’s secure network

• Troubles? Contact the ITS Help Desk

• helpdesk@luc.edu or 773-508-4487

• What You Need to Do During Open Enrollment:

• If you don’t enroll, you will miss out on the opportunity to enroll in PPO 3

HSA, and have an HSA in 2019 with contributions from Loyola

• Must re-enroll for Health Care FSA (PPO 1 and PPO 2 only), LFSA (PPO 3

only) and/or Dependent Care FSA through ESS

• Must complete Tobacco Premium and Spousal Premium Certifications

• Verify your dependents/beneficiaries

Reminder: Both medical plan participants and their covered spouse/LDAs must

complete the respective Spousal/LDA and wellness incentive by December 7, 2018 in

order to receive the $50 monthly premium discount in 2019.PAID STAFF PARENTAL LEAVE & STAFF VACATION UPDATES

NEW JANUARY 1, 2019

PAID STAFF PARENTAL LEAVE

• Three (3) weeks paid staff parental leave for parents due to birth,

adoption, or placement of a foster child starting January 1, 2019.

• Applicable to benefits-eligible full-time or part-time staff members

after 12 months of employment who

• Have given birth to a child; or

• Are a spouse/partner of a woman who has given birth to a child; or

• Have adopted a child or been placed with a foster child.

• Leave must be taken within 6 months of birth, adoption, or placement of

foster child.

• Leave must be taken continuously:

• Will run concurrently with FMLA.

• Leave will be applied after STD period for birth.REVISED STAFF VACATION POLICY

Effective December 23, 2018

Employee Group Years of Service

Less than 10 years 10 years 20 years

Administrative Directors and above* 4 weeks 4 weeks 5 weeks

All Other Full-time Staff 3 weeks 4 weeks 5 weeks

Part-time Staff (30 to < 40 hrs/week) 12 days 16 days 20 days

Part-time Staff (24 to < 30 hrs/week) 8 days 10 days 15 days

Part-time Staff (20 to < 24 hrs/week) 7 days 7 days 10 days

• As of December 23, 2018, paid vacation time for all staff will accrue bi-weekly

according to the schedule above.

• Newly hired employees will be able to use vacation after 90 days, instead of

waiting 6 months.

• Accrual rate is remaining the same, except for non-exempt staff with less than

5 years of service (increase from 2 weeks to 3 weeks of vacation time annually).REVISED STAFF VACATION POLICY

Effective December 23, 2018

• New maximum vacation accrual allotments will be established at one times

(1X) annual accrual (currently two times (2X) annual accrual).

• Any unused vacation above 1X accrual (plus five pay periods) as of

November 10, 2018 will be paid out in the November 16, 2018 paycheck.

• Payout = the accrued vacation time as of November 10, 2018 above the

new 1X maximum vacation accrual + the equivalent of five pay periods of

vacation accruals.

• This brings the accrual below the maximum, and allows you to continue

accruing vacation during the holidays and closure periods.

• Payout subject to the DCRP 403(b) contributions you currently have on file.PAYOUT DETAILS

Check your vacation hours balance using Employee Self-Service and KRONOS.

To adjust your retirement contributions for the November 16, 2018

paycheck only:

1. Contact Transamerica after October 25, and no later than November 2 to

increase/decrease your deferral percentage amount for the November 16

paycheck.

2. Contact Transamerica again after November 8 and no later than

November 16 to adjust your deferral percentage amount for the following

paycheck on November 30.

3. Contact the Retirement Center administered by Transamerica at

773-508-2770 or visit https://luc.trsretire.com.

Reminder: Adjust your contributions accordingly so that you can continue to

maximize the 5% University match through the last pay date of 2018!OPEN ENROLLMENT QUESTIONS… Feel free to contact benefits@luc.edu with any benefits-related questions.

OPEN Q & A

Thank You

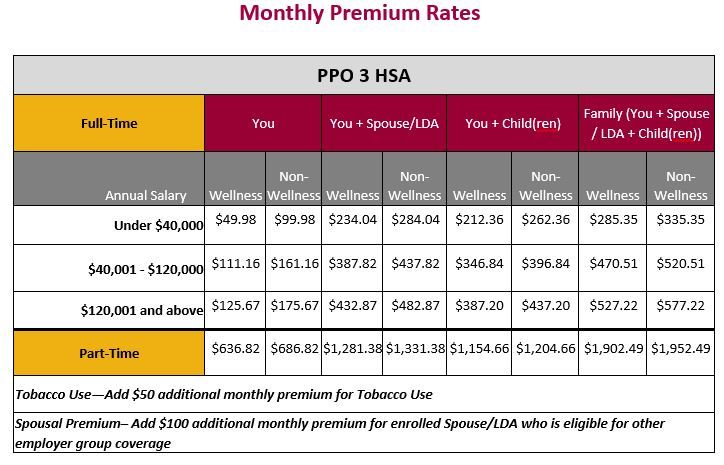

2019 Premium Rates

PPO 1

PPO 2 Monthly Premium Rates

PPO 3 HSA

DENTAL/VISION Monthly Premium Rates

SUPPLEMENTAL LIFE INSURANCE & AD&D

CRITICAL ILLNESS/VOLUNTARY ACCIDENT INSURANCE; HYATT LEGAL

You can also read