Municipal Bond Market Monitor - Q1 2022 - Eaton Vance

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Q1 2022 Municipal Bond Market Monitor MUNICIPAL BOND GROUP

2 Municipal Bond Market Monitor | Q1 2022

Q1 2022 Municipal Market Overview

Volatility was the theme for markets as investors balanced inflationary pressures, the war in Ukraine and policy statements from the

Federal Reserve.

The Fed raised rates 25bps in March and Chair Powell’s comment that “the labor market is tight to an unhealthy level” makes a

50bps hike in May and June highly likely.

High quality muni returns were deeply negative across the curve and the Bloomberg Municipal Bond Index experienced its worst

quarterly performance since Q3 1981.

Following record muni mutual fund inflows in 2021, the market experienced 12 consecutive weeks of outflows.

After trading rich throughout 2021, Muni/treasury ratios cheapened significantly across the curve.

Municipal upgrades have outpaced downgrades as overall credit quality has been bolstered by significant federal support, strong

GDP growth and a replenishment of State rainy day funds.

Past performance is no guarantee of future results. It is not possible to invest directly in an index. See end of report for important additional information. This commentary may contain statements that are not historical facts,

referred to as "forward looking statements". Actual future results may differ significantly from those stated in any forward-looking statement, depending on factors such as changes in securities or financial markets or general

economic conditions.

3 Municipal Bond Market Monitor | Q1 2022

Municipal Yield Changes

Major Asset Class Returns

Volatility was the theme for markets as investors balanced 30%

28.7% Q1 2022 2021

inflationary pressures, the war in Ukraine and policy statements

20%

from the Federal Reserve.

10%

5.4% 5.2%

1.5%

The Fed raised the fed funds rate 25bps in March and Chairman

0%

-0.1%

Powell indicated a willingness to raise the rate 50bps in both May -1.0% -2.3%

-4.5% -6.2% -5.6%

-10% -4.6% -7.7%

and June.

S&P 500 High Yield Bank Loan Municipal Corporate Treasury

In March, 2-year treasury yields jumped 86bps, while 30-year

yields increased 27bps. Year-to-date, treasury yields have risen AAA Municipal Yields (%)

56-156bps across the curve. 3%

12/31/21 3/312022 2.53%

2.32%

2.18%

2.04%

In Q1, the municipal market displayed similar volatility with yields 2%

1.97%

1.76%

up 104-152bps across the curve. 1.49%

1.15%

1.03%

1% 0.87%

0.59%

0.24%

0%

2 yr 5 yr 7 yr 10 yr 15 yr 30 yr

Source: Bloomberg and Thomson Reuters as of 3/31/22. Past performance is no guarantee of future results. It is not possible to invest directly in an index. See end of report for important additional information. *Basis points

(BPS) is a unit that is equal to 1/100th of 1% and is used to denote the change in a financial instrument.

4 Municipal Bond Market Monitor | Q1 2022

Index Returns

Index Returns

10% Q1 2022 2021

High quality muni returns were deeply negative across the curve. The 7.8%

8%

-6.23% return for the Bloomberg Municipal Bond Index marked the 6%

4% 3.2% 1.5%

worst quarterly performance since Q3 1981 (-9.69%). 2% 1.0%

0.3%

0%

-2%

As expected, lower quality BBB’s and high yield municipals -4%

-6%

underperformed, down -7.13% and -6.53%, respectively. -5.1% -6.2% -6.2% -6.5%

-8%

-10% -8.7%

5 yr 10 yr 22+ yr Bloomberg Bloomberg

Municipal Bond Municipal HY

Index Index

High Yield Index vs AAA Index Yield to Worst Spread

Despite the persistent volatility and municipal outflow pressures, high 8.00

yield spreads did not widen meaningfully during the quarter – a 7.00

reflection of the strong state of municipal credit quality. 6.00

Percent (%)

5.00

4.00

Average

While spreads remain tight from a historical perspective, with the

3.00

significant sell-off in the first quarter, absolute yields are much more 2.00

attractive than the start the year. 1.00

0.00

Source: Bloomberg, MMA and Morningstar Direct as of 3/31/22. Past performance is no guarantee of future results. Performance less than one year is cumulative. It is not possible to invest directly in an index. See end of

report for important additional information.5 Municipal Bond Market Monitor | Q1 2022

Flows and Issuance

Muni Mutual Fund Flows

6% 15

Total Flows AAA GO 30 yr

5% 10

After record inflows in 2021, the market experienced 12

4% 5

Flows (Billions)

consecutive weeks of outflows or -$21.9 billion cumulatively

Yield (%)

3% 0

according to Lipper.

2% -5

1% -10

After a record $23 billion of fund flows into muni high yield funds in

0% -15

2021, a total of $5.2 billion left high yield muni funds.

-1% -20

Municipal Bond Issuance: New vs. Refunding

Municipal issuance finished the quarter at $98.3 billion compared

500 Refunding

to $113 billion in Q1 2021. New money issuance was up ~3% 450 New

while refunding deals were down 44%. 400

350

Issuance (Billions) 300

Taxable municipal issuance fell 42% and finished the quarter at

250

$15.8 billion. This large decline is due to the drop-off in advance 200

refunding deals as rates moved significantly higher. 150

100

50

0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Source: Sifma, BofA Merrill Lynch Global Research, Thomson Reuters Municipal Market Data. Date Range: March 2007 – March 2021.

Flow data provided by ICI. Municipal Bond Issuance data from SIFMA, Bloomberg Barclays Research. Private placement issuance counted as new capital.6 Municipal Bond Market Monitor | Q1 2022

Muni-to-Treasury Yield Ratios

AAA Muni-to-Treasury Yield Ratios (%)

350%

Muni/treasury ratios cheapened significantly across the curve 300%

5Y 10Y 30Y

during the quarter. 250%

200%

150%

For the quarter, the 5 year muni/treasury ratio cheapened from 103%

100% 94%

47% to 81%, the 10 year ratio cheapened from 68% to 94% and 81%

50%

the 30 year ratio jumped to 103% from 79%.

0%

How Attractive Are Muni/Treasury Ratios vs. 10 Year History

Ratios have been Higher Ratios have been Lower

100%

Over the last 10 years, the 5-year, 10-year and 30-year

90%

muni/Treasury ratios have been higher (cheaper) approximately 80%

36%, 39% and 28% of the time, respectively. 70%

60% 64% 61%

72%

50%

This indicates that AAA-rated municipals across the curve ended 40%

30% 36% 39% 28%

the quarter cheap relative to treasuries.

20%

10%

0%

5Y 10Y 30Y

Source: Thomson Reuters as of 3/31/22.

Past performance is no guarantee of future results. It is not possible to invest directly in an index. See end of report for important additional information.7 Municipal Bond Market Monitor | Q1 2022

Municipal Yield Curve

2-Year / 30-Year Curve

500

The municipal yield curve bear flattened 48bps as 2-year yields

jumped 152bps while 30-year yields increased 104bps. 400 2-30

300

The treasury curve experienced a more significant flattening as the 200

2-year yield increased 156bps while the 30-year yield increased

100

56bps.

0

We would expect this trend to continue as the Fed has committed

to additional rate hikes in the coming months.

5-Year / 15-Year Curve

250

The five-to-fifteen year portion of the muni curve also flattened as 5-

5-15

200

year yields increased 138bps while 15-year yields increased 117bps.

150

At the end of the quarter, an investor picks up 78% of the yield

100

available by going out 5 years and 92% by going out 15 years.

50

-

Source: Thomson Reuters as of 3/31/22. Past performance is no guarantee of future results. It is not possible to invest directly in an index. See end of report for important additional information.8 Municipal Bond Market Monitor | Q1 2022

Municipal Yield Curve

Percentage of Entire Municipal Yield Curve

Captured by 2-year Municipal Bond

Following its 25bps hike at the March meeting, the Fed's "dot plot"

70%

anticipates 7 additional rate hikes in ’22. 61% 59%

50%

40%

In our view, Chair Powell’s comment following the March FOMC

decision that “the labor market is tight to an unhealthy level” makes 26%

19%

16%

a 50bps hike in May and June a near certainty. 9% 11% 8% 11% 8% 11%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 Q1

2022

SIFMA, LIBOR and Fed Funds Yield (%)

The SIFMA* Index increased 40bps and ended Q1 at 0.51%.

6.00%

As a result of the Fed’s more hawkish stance, the SIFMA* Index 5.00% SIFMA

will continue to move higher making VRDNs and Muni Floating 4.00%

1-Month LIBOR

Yield (%)

Rate Notes increasingly attractive as 2022 progresses. Fed Funds Rate

3.00%

2.00%

1.00%

0.00%

Source: Thomson Reuters, Federal Reserve as of 3/31/22.

*SIFMA is a seven-day high grade money market index comprised of tax-exempt variable rate demand obligations.9 Municipal Bond Market Monitor | Q1 2022

Overview of legislation and municipal related spending in relief bills

Below is a high level summary of the fiscal support for municipals through the most recent pieces of legislation passed by Congress.

In aggregate, over $1.7 trillion of capital has been allocated to various parts of the municipal bond market.

2021 Infrastructure American Rescue Dec. Federal

CARES Act

Bill Plan Stimulus

Total Muni Market Support $550 $650 $157 $347

States $136 $408 $30 $169

Locals -- $182 $30 $164

Community based orgs. -- -- -- $1

Not for Profits -- $0.8 $15 --

Healthcare -- $13 $4 $108

Primary/Sec Education -- $137 $58 $25

Higher education -- $40 $26 $17

Airports/Ports $42 $11 $2 $10

Surface transit $110 -- $10 --

Mass transit $39 $30 $14 $25

Other Transportation $78 $2 $2 --

Housing -- $39 $25 --

Utilities $143 -- -- --

Source: US Congress, J.P Morgan. Note: Sum of individual sector amounts may not add up to aggregate total due to double counting, as much of the capital is shared across sectors10 Municipal Bond Market Monitor | Q1 2022

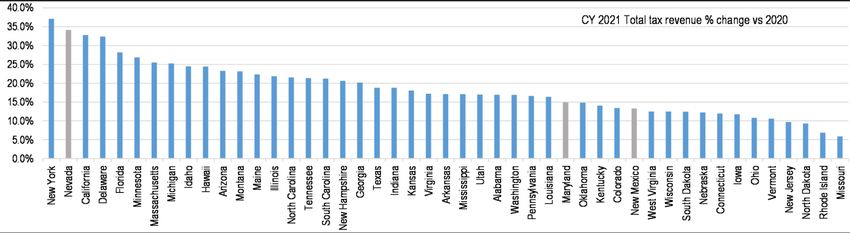

State Revenues Surged in Calendar Year 2021

Calendar year 2021 tax receipts are up on average 18.6% vs 2020 and 16.6% vs 2019

Source: Individual state monthly tax reports, J.P. Morgan. Note: Oregon, Wyoming, and Alaska do not provide monthly tax data. Bars in gray

indicate December data is not yet available and YTD period has been adjusted11 Municipal Bond Market Monitor | Q1 2022

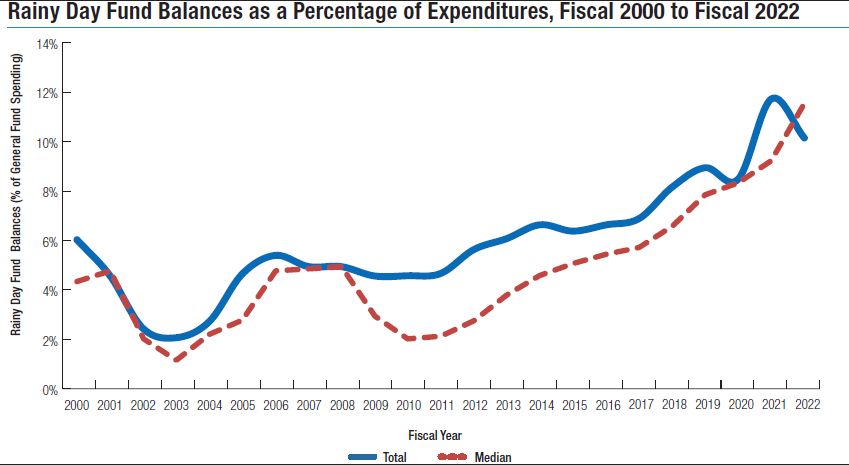

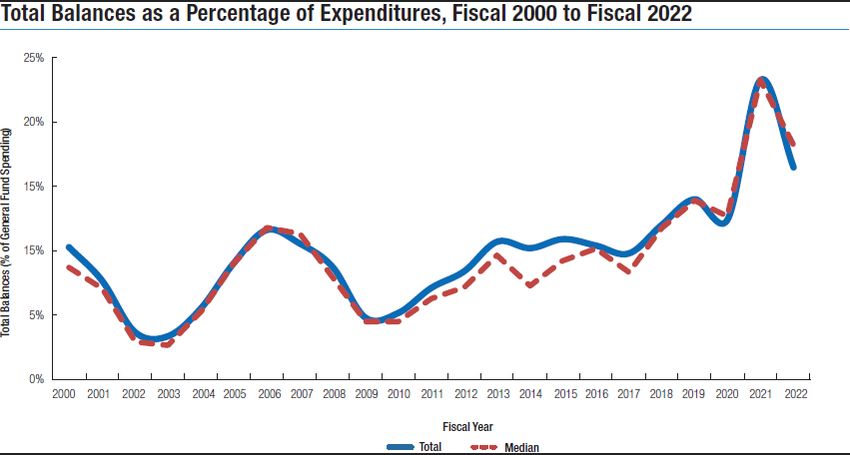

States Prudently Building Reserves and Liquidity

Rainy day fund balances are expected to represent 10.4% of general fund expenditure in 2022 while total fund balances

are expected to be 16.5% of expenditures.

Source: National Association of State Budget

Officers12 Municipal Bond Market Monitor | Q1 2022

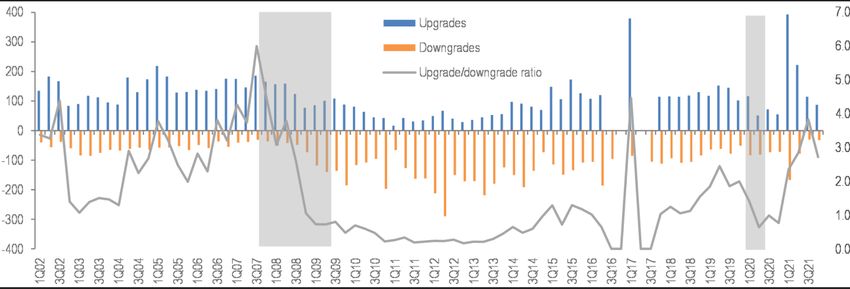

Increase in Upgrades Due to Strong Credit Environment

Upgrades have outpaced downgrades as overall credit quality has been bolstered by significant federal support, an

improving vaccination rate and strong GDP growth.

Source: Moody’s Investors Service, J.P. Morgan. Gray shaded area indicates recessionary period (data not available prior to 1Q02)13 Municipal Bond Market Monitor | Q1 2022

Municipal Default Overview

Number of Unique Annual Defaults Number of Unique Annual Defaults

100 Decreased by 26%

160

90

140 80

Number of unique defaults

Number of unique defaults

120 70

100 Puerto Rico US - ex PR 60

80 50

60 40

40 30

20

20

10

0

0

201020112012201320142015201620172018201920202021 YTD

2020 2021

2022

Dollar Value of Annual Defaults ($Billions)

Dollar Value of Annual Defaults ($Billions) decreased by 51%

40 8

Dollar value of defaults (Billions)

Dollar value of defaults (Billions)

35 7

30 Puerto Rico US -ex PR 6

25

5

20

15 4

10 3

5 2

0

1

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 YTD

2022 0

2020 2021

Source: MMA. Default data as of 3/31/202214 Municipal Bond Market Monitor | Q1 2022

Taxable Equivalent Yields

Taxes are not heading lower. Assuming the highest tax bracket on federal income, municipal taxable-equivalent yields remain attractive

relative to other fixed income asset classes.

4.81256

Taxable Equivalent Yields

9%

8% Tax-Equivalent Yield Nominal Yield 7.77%

7%

6%

5% 4.39%

4%

3%

4.60%

2%

3.60%

2.92% 2.60%

1%

0%

Bloomberg US Aggregate Index Bloomberg US IG Corporate Bloomberg Municipal Bond Index Bloomberg HY Muni Bond Index

Sources: Barclays Live as of 3/31/22, Tax Policy Center. This table is for illustrative purposes only and uses the highest current applicable federal tax rates plus 3.8% health care tax. Past performance is no guarantee of future

results. It is not possible to invest directly in an index. See end of report for important additional information.15 Municipal Bond Market Monitor | Q1 2022 Municipal Market Outlook Treasury and municipal volatility is likely to persist, with markets adapting to changes in global central bank policy, evolving geopolitical tensions and emerging economic data. However, as rates have increased to levels not seen in years and valuations have cheapened; we believe that today’s environment could prove worthwhile for adding to municipal exposure particularly for long-term focused investors. Though high yield municipal spreads remain tight from a historical perspective, absolute yields are significantly higher than where they started the year and we are beginning to see some value and opportunities in this part of the market. With the Fed expected to increase rates 100bps in Q2 and with the ability to capture almost 80% of the yield curve by going out 5 years, short and ultra-short duration strategies are particularly attractive for defensive minded investors. The municipal bond market is strong from a credit standpoint, as state liquidity and tax revenue reached an all-time high last year. From both a total dollar value and unique number perspective, we expect municipal defaults to remain low in 2022.

Appendix

17 Municipal Bond Market Monitor | Q1 2022 Investing with a Leader in Municipal Bonds Eaton Vance is a premier municipal bond manager Among the largest and deepest municipal investment teams in the U.S. Consistent, bottom-up investment process and proven track record One of the broadest selections of muni solutions Mutual funds, closed-end funds and separate accounts Customizable solutions engineered for special investment situations Legacy of managing for tax-exempt income and total return

18 Municipal Bond Market Monitor | Q1 2022

Eaton Vance Municipal Investment Process

Team-oriented, research-based process with qualitative and quantitative overlays

The The

Opportunity Process

Credit

1100 Loans Research The Result

$3.8 Trillion Relative

Broad

Municipal

Municipal Value

Investing

Product

Offerings

Market

Market Surveillance Bottom-up Analysis and Selection

Internal risk rating Issuer relative ranking Market valuation Collaborative decision making Risk management Portfolio

Investment Issuer specific Relative industry valuations Portfolio managers Product specific Credit names

universe fundamental analysis Technical analysis Credit analysts guidelines

Relative value Determine liquidity and Traders Best portfolio within

rankings within price trends guidelines

industries

Fundamental trends

Bottom-up industry review19 Municipal Bond Market Monitor | Q1 2022

Important information and disclosure

Additional information

Debt, Pension and OPEB Liabilities as a % of GDP INDEX DEFINITIONS:

Debt is net tax supported debt from Moody’s May 2014. Unfunded pension Bloomberg Municipal Bond Index is an unmanaged index of municipal

liabilities from State CAFRs as of June 30, 2013. States’ share of estimated bonds traded in the U.S.

pension liabilities are based upon the states’ share of the total state and local

Bloomberg U.S. Aggregate Index is an unmanaged index of domestic

liabilities as per Moody’s “US State Pension Medians Increase in Fiscal 2012”

investment-grade bonds, including corporate, government and mortgage-

(January 2014) and Eaton Vance assumptions. GDP from the Bureau of

backed securities.

Economic Analysis 2013 advanced estimates. State’s pension plan discount

rates from 2013 State CAFRs. Eaton Vance then applied a 5.5% discount rate Bloomberg U.S. Corporate High Yield Index measures USD-denominated,

to pension liabilities, based on Moody’s Adjustments to US State and Local non-investment grade corporate securities.

Government Reported Pension Data, July 2, 2012, where for each 1%

difference between 5.5% and a plan’s discount rate, the actuarial accrued Bloomberg U.S. Corporate Index is an unmanaged index that measures the

liability increased by 13%. OPEB liabilities from State CAFRs. Importantly, the performance of investment-grade corporate securities within the Barclays

states’ unfunded OPEB liability has not been adjusted for the states’ share of Capital U.S. Aggregate Index.

the total state and local OPEB liability, which could result in the states’ OPEB S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional

liability being overstated. leveraged loan market.

Terms

Municipal-to-Treasury Yield Ratios are relative value indicators that measure

the richness or cheapness of Municipal bond yields to comparable maturity

Treasury bond yields.

Yield to Worst is a measure which reflects the lowest potential yield earned on

a bond without the issuer defaulting. The yield to worst is calculated by making

worst-case scenario assumptions by calculating the returns that would be

received if provisions, including prepayment, call or sinking fund, are used by

the issuer.20 Municipal Bond Market Monitor | Q1 2022 Important information and disclosure ABOUT ASSET CLASS COMPARISONS: Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested. The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum. Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision. Credit ratings that may be referenced are based on Moody's, S&P or Fitch, as applicable. Credit ratings are based largely on the rating agency's investment analysis at the time of rating and the rating assigned to any particular security is not necessarily a reflection of the issuer's current financial condition. The rating assigned to a security by a rating agency does not necessarily reflect its assessment of the volatility of a security's market value or of the liquidity of an investment in the security. Ratings of BBB or higher by Standard and Poor's or Fitch (Baa or higher by Moody's) are considered to be investment grade quality. About Risk An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of non-payment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss. Debt securities are subject to risks that the issuer will not meet its payment obligations. Low rated or equivalent unrated debt securities of the type in which a strategy will invest generally offer a higher return than higher rated debt securities, but also are subject to greater risks that the issuer will default. Unrated bonds are generally regarded as being speculative.

21 Municipal Bond Market Monitor | Q1 2022

Important information and disclosure

Source of all data: Eaton Vance, as at 9/30/2021, unless otherwise specified. This material is only intended for and will only be distributed to persons

resident in jurisdictions where such distribution or availability would not be

This material is presented for informational and illustrative purposes only. This contrary to local laws or regulations.

material should not be construed as investment advice, a recommendation to EVMI/MSIM FMIL markets the services of the following strategic affiliates:

purchase or sell specific securities, or to adopt any particular investment Eaton Vance Management ("EVM"), Eaton Vance Advisers International Ltd

strategy; it has been prepared on the basis of publicly available information, (“EVAIL”), Parametric Portfolio Associates® LLC ("PPA"), Calvert Research

internally developed data and other third-party sources believed to be reliable. and Management (“CRM”), and Atlanta Capital Management Company LLC

However, no assurances are provided regarding the reliability of such ("Atlanta "). EVM, EVAIL, PPA, CRM and Atlanta are SEC registered

information and Eaton Vance has not sought to independently verify investment advisor and are part of Morgan Stanley Investment Management,

information taken from public and third-party sources. Investment views, the asset management division of Morgan Stanley.

opinions, and/or analysis expressed constitute judgments as of the date of this This material is for Professional Clients/Accredited Investors only.

material and are subject to change at any time without notice. Different views This material does not constitute an offer to sell or the solicitation of an offer to

may be expressed based on different investment styles, objectives, opinions or buy any services referred to expressly or impliedly in the material in the

philosophies. This material may contain statements that are not historical facts, People's Republic of China (excluding Hong Kong, Macau and Taiwan, the

referred to as forward-looking statements. Future results may differ significantly "PRC") to any person to whom it is unlawful to make the offer or solicitation in

from those stated in forward-looking statements, depending on factors such as the PRC.

changes in securities or financial markets or general economic conditions. The material may not be provided, sold, distributed or delivered, or provided or

This material is for the benefit of persons whom Eaton Vance reasonably sold or distributed or delivered to any person for forwarding or resale or

believes it is permitted to communicate to and should not be forwarded to any redelivery, in any such case directly or indirectly, in the People's Republic of

other person without the consent of Eaton Vance. It is not addressed to any China (the PRC, excluding Hong Kong, Macau and Taiwan) in contravention of

other person and may not be used by them for any purpose whatsoever. It any applicable laws.

expresses no views as to the suitability of the investments described herein to

the individual circumstances of any recipient or otherwise. It is the responsibility

of every person reading this document to satisfy himself as to the full

observance of the laws of any relevant country, including obtaining any

governmental or other consent which may be required or observing any other

formality which needs to be observed in that country. Unless otherwise stated,

returns and market values contained herein are presented in US Dollars.

In the EU this material is issued by MSIM Fund Management (Ireland) Limited

(“MSIM FMIL”) registered in the Republic of Ireland with Registered Office at 7-

11 Sir John Rogerson's Quay, Dublin 2, D02 VC42, Ireland. MSIM FMIL is

regulated by the Central Bank of Ireland with Company Number: 616661.

Outside of the US and EU, this material is issued by Eaton Vance Management

(International) Limited (“EVMI”) 125 Old Broad Street, London, EC2N 1AR, UK,

and is which is authorised and regulated in the United Kingdom by the

Financial Conduct Authority.22 Municipal Bond Market Monitor | Q1 2022

Important information and disclosure

Source of all data: Eaton Vance, as at 9/30/2021, unless otherwise specified. Morgan Stanley Investment Management, the asset management division of

Morgan Stanley.

In Singapore, Eaton Vance Management International (Asia) Pte. Ltd.

(“EVMIA”) holds a Capital Markets Licence under the Securities and Futures Before investing, investors should consider carefully the investment

Act of Singapore (“SFA”) to conduct, among others, fund management, is an objectives, risks, charges and expenses of a mutual fund. This and other

exempt Financial Adviser pursuant to the Financial Adviser Act Section important information is contained in the prospectus and summary

23(1)(d) and is regulated by the Monetary Authority of Singapore (“MAS”). prospectus, which can be obtained from a financial advisor. Prospective

Eaton Vance Management, Eaton Vance Management (International) Limited investors should read the prospectus carefully before investing.

and Parametric Portfolio Associates® LLC holds an exemption under

Paragraph 9, 3rd Schedule to the SFA in Singapore to conduct fund

management activities under an arrangement with EVMIA and subject to

Investing entails risks and there can be no assurance that Eaton Vance

certain conditions.

will achieve profits or avoid incurring losses. It is not possible to invest

In Australia, EVMI is exempt from the requirement to hold an Australian directly in an index. Past performance is not a reliable indicator of future

financial services license under the Corporations Act in respect of the provision results.

of financial services to wholesale clients as defined in the Corporations Act

2001 (Cth) and as per the ASIC Corporations (Repeal and Transitional)

Instrument 2016/396.

EVMI is registered as a Discretionary Investment Manager in South Korea

pursuant to Article 18 of Financial Investment Services and Capital Markets Act

of South Korea.

Morgan Stanley Investment Management (“MSIM”) (the asset management

division of Morgan Stanley (NYSE: MS)) and its affiliates have arrangements in

place to market each other’s products and services. Each MSIM affiliate is

regulated as appropriate in the jurisdiction it operates. Please refer to the

MSIM ADVs for details of affiliates.

In the United States:

Eaton Vance Management is an SEC –registered investment advisor and part

of Morgan Stanley Investment Management, the asset management division of

Morgan Stanley.

Eaton Vance Distributors, Inc. (“EVD”), Two International Place, Boston, MA

02110, (800) 225-6265. Member of FINRA/ SIPC.

Eaton Vance WaterOak Advisors. Two International Place, Boston, MA 02110.

Eaton Vance WaterOak is an SEC-registered investment advisor and part ofFor more information, please contact:

Eaton Vance

: International Place

Two

Boston, MA 02110

800 225 6265

617 482 8260

eatonvance.com

Eaton Vance Management Eaton Vance Management

(International) Limited International (Asia) Pte. Ltd.

125 Old Broad Street, London, 8 Marina View, 13–01 Asia Square Tower

EC2N 1AR, United Kingdom 1, Singapore 018960

+44 (0)203 207 1900 +65 6713 9241

internationalenquiries@eatonvance.com

eatonvance.co.uk

internationalenquiries@eatonvance.com

eatonvance.sg

For more information or to subscribe

MSIM Fund Management (Ireland) Eaton Vance Management

for updates visit

Limited (International) Limited

7-11 Sir John Rogerson’s Quay,

Dublin 2, D02 VC45, Ireland

Suite 05, Level 25, 259 George Street

Sydney NSW 2000 Australia

eatonvance.com

D04 C7H2, Ireland +61 2 8229 0200

+353 1 799 8700 internationalenquiries@eatonvance.com

eatonvance.com.au

About Eaton Vance

Eaton Vance is part of Morgan Stanley Investment Management, the asset management division of Morgan Stanley. It provides advanced investment strategies and wealth management solutions to

forward-thinking investors around the world. Through its distinct investment brands Eaton Vance Management, Parametric, Atlanta Capital and Calvert, the Company offers a diversity of investment

approaches, encompassing bottom-up fundamental active management, responsible investing, systematic investing and customized implementation of client-specified portfolio exposures. Exemplary

service, timely innovation and attractive returns across market cycles have been hallmarks of Eaton Vance since 1924.

@2021 Eaton Vance Management 15337 4.8.22

NOT FDIC INSURED | OFFER NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY | NOT A DEPOSITYou can also read