MNI RBNZ Review - May 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MNI RBNZ Review – May 2022

Meeting Date: Wednesday, 25 May 2022

Link To Decision: https://www.rbnz.govt.nz/news/2022/05/monetary-conditions-tighten-by-more-and-sooner

Link To MPS: https://www.rbnz.govt.nz/monetary-policy/monetary-policy-statement/mps-may-2022

CONTENTS

• Page 2: MNI POV (Point of View)

• Page 3-5: RBNZ May Monetary Policy Review

• Page 6: RBNZ Key Forecast Variables - May vs. February MPS

• Page 7-10: Sell-Side Analyst Views

• Page 11: MNI Policy Team Insights

1|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB

MNI POV (Point Of View): Hawkish Resolve

The statement from the RBNZ echoed the “stitch in time” narrative from April monetary policy review, albeit its

overall tone grew more combative, as the inflation target becomes somewhat distant. The Committee delivered

another 50bp hike to the OCR while signalling the need to take more heat out of the economy sooner, in order to

ensure that consumer price inflation is brought under control.

The Committee left no doubt that they are placing more focus on fighting runaway inflation, which remains above

the target range across measures of headline and core prices, with near-term inflation expectations also elevated.

Members observed that medium-term inflation expectations are near the mid-point of the target range (“albeit

heightened somewhat”) and it is crucial to keep them that way. They agreed that “stabilising inflation is [their]

priority” and vowed to act “confidently” to that effect.

Compared with previous statements, the labour market received more attention. The Committee noted that

“employment remains above its maximum sustainable level,” generating upside pressure on wages and

constraining the productive capacity of businesses. Although they expected that growing labour supply will help

drive the unemployment rate higher, it seemed that these dynamics may have received some more scrutiny in their

discussions.

Trying to identify the sources of the problem, members judged that the observed strength in inflation and

employment “is broad-based, arising from a range of economic factors,” while the rate of price growth “reflects a

relatively similar contribution of global imported price pressures and domestic price pressures.”

The Reserve Bank signalled awareness of arguments against continued aggressive tightening. It tipped hat to the

strong headwinds provided by “heightened global economic uncertainties and higher inflation,” to the decline in

asset prices and the impact of further rate rises on households’ spending intentions. But concern over inflation

prevailed and policymakers chose to press ahead with their hawkish campaign, comforted by signs of household

balance sheets still being healthy.

Cognisant of risks, the Committee decided that continued powerful tightening is the path of least regrets.

Policymakers reaffirmed their “stitch in time” tactics outlined in April and strengthened the language around it. The

summary record of the meeting noted that “raising the OCR by more and sooner was consistent with avoiding

higher future costs to employment and the economy in general as a result of high inflation.” The preference for

earlier, firmer action to avoid an extended tightening cycle remains.

In order to stress the core idea behind the “stitch in time” logic, the Reserve Bank promised to step back once the

task of constraining consumer price inflation and inflation expectations are completed. The OCR track was altered

to reflect a steeper tightening path with a considerably higher peak (nearly 4%), but easing off towards the end of

the forecast horizon. Accordingly, the Committee said that “once aggregate supply and demand are more in

balance, the OCR can return to a lower, more neutral level.”

While a repeat of the double-barrel (i.e. 50bp) rate rise was widely expected, the magnitude of the revision to the

OCR track took many by surprise. The shift in the expected trajectory of the key interest rate indicated firmer front-

loading intentions of the Reserve Bank, while few expected the Committee to lift the projected peak by such a wide

margin. Markets reacted accordingly as NZ 2-year swaps rose 24bp and the NZD exchange rate topped $0.65.

In fact, the extent of the lift in the terminal level of the OCR was such that it left some sell-side desks in doubt

whether the Reserve Bank will deliver on its own interest-rate forecast. In the months ahead, Governor Orr will

need to carefully calibrate his messaging to maintain the credibility of the OCR track.

The pace of monetary tightening is already historic, as the RBNZ leads the hawkish charge of G10 central banks.

The April meeting marked the first 50bp OCR hike since 2014 and there have been no two back-to-back 50bp hikes

since 2004. In the words of Governor Orr, “monetary and financial conditions as a whole are now at least neutral if

not tightening” and need to remain so for some time. Yet, despite bold steps taken to date, the latest MPS

demonstrated the Reserve Bank’s growing assertiveness in fulfilling its monetary policy mandate.

2|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBRBNZ May Monetary Policy Review Announcement

The Monetary Policy Committee today increased the Official Cash Rate (OCR) to 2.0 percent. The Committee

agreed it remains appropriate to continue to tighten monetary conditions at pace to maintain price stability and

support maximum sustainable employment. The Committee is resolute in its commitment to ensure consumer price

inflation returns to within the 1 to 3 percent target range.

Consistent with the economic outlook and risks ahead, monetary conditions need to act as a constraint on demand

until there is a better match with New Zealand’s productive capacity. A larger and earlier increase in the OCR

reduces the risk of inflation becoming persistent, while also providing more policy flexibility ahead in light of the

highly uncertain global economic environment.

The level of global economic activity is generating rising inflation pressures, exacerbated by ongoing supply

disruptions driven by both COVID-19 persistence and the Russian invasion of Ukraine. The latter continues to

cause very high prices for food and energy commodities.

The pace of global economic growth is slowing. The broad-based tightening in global monetary and financial

conditions is acting to slow spending growth, accentuated by the high costs of basic food and energy staples.

European geopolitical uncertainty is also weighing heavily on business confidence and investment intentions

worldwide. Likewise, COVID-19 restrictions in significant regions of China are exacerbating supply chain

disruptions and adding cost and complexity to trade.

In New Zealand, underlying strength remains in the economy, supported by a strong labour market, sound

household balance sheets, continued fiscal support, and a strong terms of trade. The reduction in COVID-19

health-related restrictions is also enabling increased economic activity, including hospitality and tourism.

However, headwinds are strong. Heightened global economic uncertainty and higher inflation are dampening global

and domestic consumer confidence. Asset prices, in particular house prices, have also declined, reflecting in part

higher mortgage interest rates and increased supply of housing.

On balance, a broad range of indicators highlight that productive capacity constraints and ongoing inflation

pressures remain prevalent. Employment remains above its maximum sustainable level, with labour shortages now

the major constraint on production. The Reserve Bank’s core inflation measures are above 3 percent.

The Committee agreed to continue to lift the OCR at pace to a level that will confidently bring consumer price

inflation to within the target range. The Committee viewed the projected path of the OCR as consistent with

achieving its primary inflation and employment objectives without causing unnecessary instability in output, interest

rates and the exchange rate. Once aggregate supply and demand are more in balance, the OCR can then return to

a lower, more neutral, level.

Summary Record of Meeting

The Monetary Policy Committee discussed developments affecting the outlook for inflation and employment in New

Zealand. Members noted that current inflation and employment were above their target and sustainable levels

respectively. Members agreed that while the direction of their monetary policy decision was clear, the extent and

timing of future increases in the Official Cash Rate (OCR) still depends on the economic outlook and avoiding

major risks.

The Committee agreed that global economic activity was slowing more than previously expected, and that further

weakening in global economic growth was likely. Members noted that while international fiscal and monetary policy

actions have partly cushioned the effect of the COVID-19 pandemic on household incomes and employment so far,

significant and ongoing disruption is now being felt.

The recent rise in global inflation pressures has led central banks to raise their policy interest rates and signal

further tightening to come. These measures have been aimed to deliberately slow demand to be more consistent

with the current constrained supply capacity of goods and services.

3|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBThe Committee noted that the disruption caused by the Russian invasion of Ukraine has added to the underlying

global inflation pressures. The cost of living has risen significantly, in particular due to shortages of food and fuel.

This rise in costs is necessitating lower non-essential spending in households globally. High global commodity

prices are likely to persist for some time, creating long-lasting cost pressure for firms and households, even as

general consumer price inflation slows.

Economic activity globally, and especially in China at present, is still being severely disrupted by COVID-19.

Members agreed that China’s regional health-related economic restrictions are having a direct impact on global

growth, supply chain efficiency, and New Zealand’s trade outlook. New Zealand’s trade performance is strongly

linked to China’s economy.

The recent rise in central banks’ policy interest rates, and forward guidance for more increases, has led to a

significant fall in global equity prices, albeit from high levels. The Committee noted that a rise in official rates

creates a higher hurdle for investment decisions.

Members discussed developments in the New Zealand economy. It was noted that rising global interest rates have

narrowed interest rate differentials with New Zealand, adding to downward pressure on the New Zealand dollar

exchange rate. The Committee noted that the lower New Zealand dollar raises import prices – exacerbating the

effect of elevated global prices.

The Committee agreed that both high food and energy costs, and rising mortgage interest rates for those with debt,

will affect household budget decisions and lead to less discretionary spending. Members noted that over the past

year or so, wage growth has been less than consumer price inflation, adding further pressure on discretionary

spending.

Recent and expected increases in mortgage interest rates are likely to contribute to falls in house prices, further

reducing households’ willingness to spend. It was agreed that household consumption was likely to be relatively

subdued in coming quarters. The Committee noted that house prices are now headed toward a more sustainable

level.

The Committee noted the Government’s Budget announcements. It was agreed that fiscal policy is currently

supporting economic activity, but that this stimulus is expected to reduce in coming years. The current level of fiscal

spending is contributing to a modest increase in demand. This is expected to diminish over time as a result of the

end to the large, broad based, fiscal support packages the Government delivered during the initial phase of the

COVID-19 economic response.

The Committee noted that measures of core consumer price inflation are above their target range. Surveyed

measures of near-term inflation expectations are also high, in line with actual consumer price inflation. It was noted,

however, that the medium-term measures of inflation expectations have remained near the centre of the target

range, albeit heightened somewhat. The Committee agreed that it was critical for these medium-term inflation

expectations to remain around 2 per cent.

Members also noted the factors responsible for the current elevated consumer price inflation. New Zealand’s

inflation rate reflects a relatively similar contribution of global imported price pressures and domestic price

pressures. They observed that a key factor contributing to domestic inflation pressure is housing – including both

the cost of construction and the operating costs of dwellings in general.

On the costs of construction, members noted that the growing delay in accessing key building materials is

significantly slowing activity, and increasing the financial risks associated with construction. The Committee

observed that these delays, cost pressures, and associated uncertainty could limit the conversion of building

permits into dwellings, exacerbating the pressure on housing supply.

Members agreed that employment is above its maximum sustainable level, as highlighted by a suite of indicators.

They agreed that rising wage pressures are an expected outcome, with access to labour the key constraint on

firms’ productive capacity. With the global labour market tight, people are also more willing and able to take up new

roles for higher wages.

4|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBThe Committee noted that the reopening of the border should see a return to a net inflow of migrants into New

Zealand over the next two years. Over time, this net immigration will help to ease New Zealand’s labour shortages.

More immediately there is an outflow of New Zealanders creating supply capacity constraints. With the international

border reopening, more immigrants will also bolster demand ahead of supply capacity as they settle. It was agreed

that these patterns of migration will have an uncertain net effect on inflation pressure, as they will affect both supply

and demand in the economy. As a result, these dynamics do not play a key role in determining monetary policy at

present.

The Committee noted the weaker outlook for employment growth in New Zealand, which is likely to be outpaced by

labour force growth. As a result of the increase in labour supply, measured unemployment is expected to rise to

around levels more consistent with maximum sustainable employment.

The Committee discussed the future path of the OCR based on the outlook for inflation and employment pressures.

Members noted that both inflation and employment are currently higher than previously expected, and that this

strength is broad-based, arising from a range of economic factors.

Members agreed that a higher level of the OCR is necessary to ensure annual consumer price inflation returns to

within its target range over the next two years. They agreed this was also consistent with ensuring employment

remained near its maximum sustainable level.

Members discussed their ‘least regrets’ framework which in the current context amounted to the risk of tightening

policy ‘too little, too late’ versus ‘too much, too soon’. The Committee agreed that at present, with persistent cost

pressures and rising inflation, the risk of moving too slowly and not far enough remained the most costly option.

On the risk of doing too much too soon, the Committee acknowledged that raising the OCR steeply puts pressure

on some households’ spending decisions, especially those that are highly indebted.

However, members noted that, on average, household balance sheets are healthy. Banks have been testing

mortgage lending for higher interest rate possibilities – consistent with current projected levels – before recent

home loans were made. They also noted that house prices are expected to remain above their pre-pandemic level.

The Committee also noted that while higher interest rates will increase firms’ hurdle to investing, recent business

surveys suggest labour shortages are the main constraint preventing an increase in production.

The Committee agreed that stabilising inflation is its priority. Members agreed that raising the OCR by more and

sooner was consistent with avoiding higher future costs to employment and the economy in general as a result of

high inflation. Stable inflation expectations will be a key indicator that the current monetary policy strategy is

working.

The Committee agreed to maintain its approach of briskly lifting the OCR until convinced that monetary conditions

were sufficient to constrain inflation expectations and bring consumer price inflation to within the target range. Once

aggregate supply and demand are more in balance, the OCR can then return to a lower, more neutral, level. The

Committee viewed the projected path of the OCR as consistent with achieving their primary inflation and

employment objectives without causing unnecessary instability in output, interest rates and the exchange rate.

On Wednesday 25 May, the Committee reached a consensus to increase the OCR to 2.0 percent.

5|Page

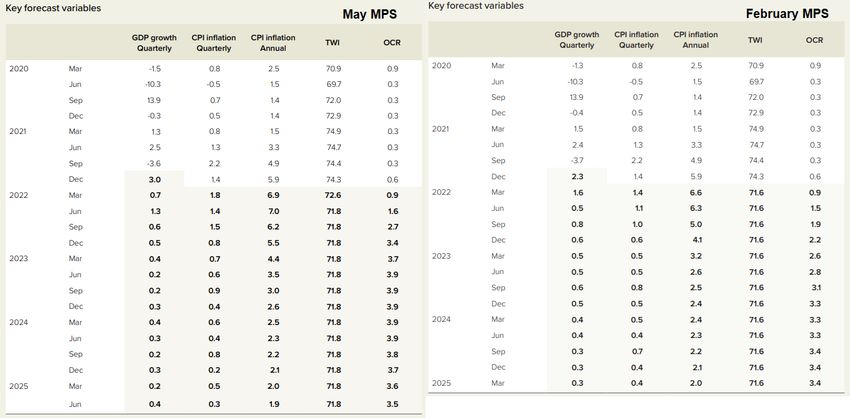

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBRBNZ Key Forecast Variables - May vs. February MPS

Source: RBNZ

6|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBSell-Side Analyst Views

ANZ

• As was all but universally expected, the RBNZ today raised the Official Cash Rate (OCR) by 50bps to

2.0%, and indicated plenty more tightening to come. The MPS forecast track was more aggressive than

expected: it sees the OCR reaching just shy of 4% by the second half of 2023, 65bp higher than in the

February Monetary Policy Statement (MPS), before declining back to around 3.5% by mid-2025.

• The overall tone of the Policy Assessment was hawkish. The RBNZ has its eyes firmly on the medium-term

inflation outlook, rather than on near-term growth risks, while acknowledging these. The RBNZ simply can’t

treat those risks symmetrically, with inflation where it is. The RBNZ stated: “The Committee agreed that at

present, with persistent cost pressures and rising inflation, the risk of moving too slowly and not far enough

remained the most costly option.” And to underline the point further: “The Committee agreed that stabilising

inflation is its priority.”

• The track is also consistent with more 50bp hikes to come. In our view, domestic growth momentum is

cooling rapidly, and this is likely to be more evident by July. However, the RBNZ doesn’t think it’s done with

50s yet, and was happy to signal that clearly today. Accordingly, we have changed our OCR forecast to

include one more 50bp hike in July before the RBNZ reverts to a more normal pace of hiking. We maintain

our OCR peak forecast of 3.5%.

ASB

• We thought the RBNZ would come out swinging, but today’s Statement was even more hawkish than we

and financial markets were expecting. The OCR was lifted 50bps as expected by all and sundry. However,

and as we’d flagged in our preview, most of the attention was on what the RBNZ’s updated projections

would imply for the pace of further tightening. Here, the Bank doubled down on the ‘stitch in time’ approach

adopted in April. OCR projections were raised substantially, and front- loaded, to imply a roughly 3.5%

OCR by year-end (compare this to 2.4% in the February MPS) and a peak of 3.95% (3.35% in Feb). Taken

at face value, this implies two of the remaining four meetings of the year will be 50bps hikes. Unless, of

course, something comes along to throw the RBNZ off course.

• To remove any doubt about whether the Bank is trying to guide market pricing to do its tightening work for

it, the Statement was littered with fighting talk. The MPC was noted as “resolute” in its commitment to

“confidently” bring elevated consumer price inflation down to within the target range. This is the talk of a

central bank worried about the updrift in inflation expectations and keen to stamp its authority all over the

task at hand.

• The only way it can do this, while acknowledging the inflationary consequences of supply disruptions, is to

squash demand. The Bank’s intention to (aggressively) use the OCR to bring aggregate supply and

demand into alignment couldn’t be clearer.

• On this basis, we have adjusted our OCR forecasts to incorporate two further 50bps hikes in July and

August (taking the OCR to 3.0%). A further two 25bps hikes in the final two meetings of the year are

expected to take the OCR to a peak of 3.5%.

Barclays

• The RBNZ increased the OCR by 50bp as expected and maintained its commitment to do more to slow

demand and bring it closer to supply levels. Still, we read the statement as being less hawkish than in

previous meetings. We now expect another three 25bp hikes this year, up from two.

• We still expect more hikes from the RBNZ, but see the balance of risks as tilted towards 25bp increments,

as we think the bank will likely be slower in deciding the path beyond its neutral estimates. We see the

bank lifting the OCR three more times this year, in July, August and October, taking the OCR to 2.75%.

While we note the risk of a 50bp hike in July, this is not our base case.

• If our forecast of the OCR ending this year at 2.75% is correct, this would mean that the RBNZ delivers

250bp of hikes from the pandemic-lows, which is more and faster hiking than the previous record during

2003-05.

• In the press conference, Governor Orr said that monetary and financial conditions are now at least neutral,

if not tightening, with actual interest rates much higher than the OCR. Indeed, we note that residential

standard mortgage rates are already close to double levels of early 2021. We think likely tighter financial

conditions (after three more hikes and a hawkish forward guidance) suggest that the bank will likely not

have to raise rates by much more than we forecast.

7|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBBNZ

• What a difference a month makes. From an April statement that affirmed the OCR peak of February’s

Monetary Policy Statement (MPS), the RBNZ has today lifted that peak 60 basis points, to 3.95%. The

Bank has clearly gotten nervous, all of a sudden, about achieving its inflation mandate, while seeing, more

clearly, the necessity of higher unemployment to bring this about.

• The Bank’s determination is reflected in the fact its new track on the OCR involves more front-loading

rather than an extended cycle. This involves a 3.40% average for Q4 2022, which infers a 3.50% level by

the very end of the year and, by implication, 50-point hikes at each of the July and August meetings. And a

decent chance of another +50bps in October.

• The Bank’s sense of aggression was also, arguably, manifest in what, at first blush, would appear to be a

dovish element of its forecasts. Rate cuts, which come into play during 2024, and with an end-page level of

3.5% (and falling). Ultimately though, this shapes a strong cycle in the OCR, knowing the Bank has today

not changed its view on the “neutral” level of the cash, still in the vicinity of 2.00%.

• Having seen today’s MPS we have taken the Bank’s full steam ahead signal on board and now expect a

50-point hike at the July Monetary Policy Review, to 2.50%. August seems a line ball call between 25/50,

with a clear risk that, by the time this arrives, there will be enough to convince the Bank to slow down to 25-

point increments. However, given the Bank wants to be “convinced” of getting inflation under control, we

are calling +50bps for the August MPS, as a base case. From there, however, we forecast just two more

successive 25-point increases, which would take the OCR to a peak of 3.50% at the November 2022 MPS.

Citi

• The outcome of the RBNZ meeting was more hawkish than we expected. The NZ central bank decided to

increase the OCR by 50bp to 2%, which was in line with our thought, and the OCR projection in the

updated Monetary Policy Statement (MPS) released today was raised further, following the significant

upward revision in the February MPS. Importantly, such revisions in the economic projection implicates the

RBNZ is now feeling the necessity to tighten its policy more quickly and decisively and sacrifice growth to

anchor inflation expectations.

• The economic outlook the RBNZ showed today was more conservative than that the Bank suggested at

the last meeting in early April. The Bank said “headwinds are strong” in the statement today, pointing the

risk that the supply chain constrain and the increased inflation erode the production and real income and

consumption. Given this, we think another upward revision for the OCR projection in the August MPS or

later is becoming unlikely. Considering the local rate market has already priced in the rate hikes to 4.3%

over the next year, exceeding the terminal rate level (3.95%) suggested in today’s MPS, the tailwind for the

NZD blowing from the increasing interest rates is likely to wane from here over time (unless oil and

commodity prices escalate further).

Goldman Sachs

• The RBNZ lifted the Official Cash Rate (OCR) by 50bp to 2.0%, as widely expected. The forward guidance

was markedly more hawkish than expected, featuring an upgrade to the OCR projections to a c.4% peak

by mid-2023 (previously: 3.3% peak by early 2024). The Committee also stressed that it is appropriate to

continue to tighten monetary conditions "at pace" and that it "is resolute in its commitment" to return

inflation to the target range. The RBNZ’s hawkish pivot was framed against the backdrop of rising global

inflationary pressures/expectations and capacity constraints in New Zealand.

• Looking ahead, the RBNZ's clear hawkish bias suggests policy will tighten "at pace" over the coming

months. We now expect two 50bp hikes in July and August (previously: 25bp hikes in each), and

subsequent 25bp increases to take the OCR to a 3.5% peak by year-end (vs 3% previously). Our terminal

rate forecast is somewhat less aggressive than RBNZ guidance and market pricing as we expect material

headwinds to growth and the housing market to emerge by year-end, alongside clearer signs of easing

global inflationary pressure.

J.P. Morgan

• The RBNZ hiked 50bp for a second consecutive meeting to 2.0% (JPM: +25bp, consensus: +50bp), which

is in line with the RBNZ’s measure of neutral. Remarkably, the staff’s OCR path was steepened further,

with a higher terminal rate (3.9%, from 3.4%) which has also been brought forward, with easing added in

the back of the projections. The normalization back toward (but still nowhere close to) neutral levels is

presumed to occur “once aggregate supply and demand are more in balance” in 2024. In the near term

8|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBthough, this means the hiking cycle accelerates in its second half, even though activity is already

weakening.

• The statement doesn’t convey any good news, for example any positives that have accrued on growth to

explain the step-shift from April’s statement. Rather, the constraint of very high spot inflation seems to be

overriding all else: “monetary conditions need to act as a constraint on demand until there is a better match

with NZ’s productive capacity”, even though on the activity outlook, “headwinds are strong”.

• The best explanation we have for such an overt push to even more hawkishness in the absence of data

catalysts since April is that the leadership is unhappy with the substantial rally in front-end rates of late

(1Yx1Y IRS having dropped 60bp from the yield highs), and Governor Orr does not yet want to give back

any leash to mortgage conditions. An above-average size cohort of mortgagees is due for reset/repricing

this quarter, for example, which the central bank may want to see locked away into materially higher rates.

There is also probably some unease that NZD/USD is weaker than it would usually be in a hiking cycle

(adding to imported inflation), but delivering an even more stagflationary-induced hawkish stance is unlikely

to have a different effect than seen so far, where the exchange rate has been more sensitive to curve

shape and growth prospects than outright policy differentials in 2021/22.

• In accelerating the tightening until inflation starts falling, the RBNZ sets up a precarious situation for the

back half of the year. Our best guess is that introducing a hump-shaped OCR track will in the end prove to

be an intermediate step before a sudden stop that means lopping off the remainder of the up/down rate

projections, once evidence of traction becomes hard to ignore. For now, the prerogative to keep tightening

is very overt and so we add a 50bp hike for the next meeting (July), and another 25bp in August, taking the

OCR to 2.75%. The next meeting after that is October, which feels a very long way away given how the

local data and global outlook are evolving. The further out one looks, it seems very likely that the RBNZ

undershoots, and we remain of the view that market rates have peaked for the cycle. As of writing, forward

spreads are meaningfully inverting and 2Yx1Y for example is lower on the day.

Kiwibank

• The RBNZ hiked the cash rate 50bps to 2%. Policy is now neutral – or close to. But the RBNZ wants policy

to be tight, very tight. The RBNZ predicts a 4% cash rate next year. That’s high. And we think it’s too high.

• Importantly, the rapid-fire 50bp hikes have not come to an end. It appears the RBNZ want to deliver a

series of 50bp hikes – with more to come. The BIG surprise in today’s statement was the extent of work the

RBNZ is prepared to do to drive down demand to rein in the inflation beast.

• We have ramped up our forecast for RBNZ tightening. We expect a 50bp move in July and August (to 3%),

followed by two 25bp move to 3.5% by November. We’ve effectively added another 50bps to our forecasts.

And then enough is enough. We don’t buy into the need to go to 4% (yet).

• The 3.95% end point of the OCR track surprised us, and the market. We had expected a mild lift to 3.5%. It

appears the bank wants to squash demand in order to meet its mandate. We’d argue they are getting

plenty of bang for buck already. We’d argue current mortgage rates are already tight. Mortgage rates have

risen swiftly. And rates are soon to be above 6% with the delivery of expected hikes to come. Nevertheless,

the RBNZ is setting consumers up for much higher lending rates.

RBC

• The RBNZ delivered a strong message, hiking by 50bp to 2.00%, lifting the OCR track to a peak of 3.95%

(from 3.35% in Feb) and affirming that getting inflation down remains its primary focus. Under the bank’s

“least regrets” framework, the RBNZ would rather risk over-tightening than allowing inflation to run out of

control. This even more hawkish stance comes despite acknowledgement of rising headwinds including

slowing global growth, fresh Chinese supply-chain & growth concerns, heightened uncertainty and the

negative impacts of higher inflation itself.

• Interestingly, the MPS OCR track now inverts from a peak of 3.95% in late-23/early-24 to an average of

3.50% in the Jun-25 quarter. This fits with a desire to act more quickly, capturing the revised RBZN view

that ”once aggregate supply and demand are more in balance, the OCR can then return to a lower, more

neutral, level”. Like some Fed speakers, the RBNZ is now explicitly countenancing an overshoot of neutral,

followed by rate cuts once inflation is reined in. And like many other central banks counterparts, the RBNZ

is also keenly focused on ensuring inflationary expectations don’t become too embedded, stating the

“critical” needs to keep medium-term expectations around the 2% mark. Orr stated that the RBNZ’s range

of neutral rate estimate was between 2-3%.

• We are doubtful the RBNZ will realise its OCR track, and expect them to cease hikes later this year as the

risks which they themselves highlight begin to demand a reassessment of the tightening cycle. We see the

9|Page

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBbank pausing after taking rates to 2.75% by October of this year. By comparison, the published OCR track

suggests the bank is expecting to hike in two more 50bp increments in the July and August meetings.

Given the conviction on hiking currently on display from the RBNZ, the risk to our profile is that cash does

indeed move above 3%, but still well short of the OCR track.

Westpac

• After increasing the Official Cash Rate by 50 basis points at its April policy review, it was clear that the

Reserve Bank was open to more of the same. Consequently, today’s decision to raise it by a further 50

basis points to 2% was widely anticipated, and the real interest was always going to be in what the RBNZ

signalled for the path ahead.

• That turned out to be even more assertive than we expected at this stage. The RBNZ projects the cash

rate to reach a peak of close to 4% by the second half of next year, with most of the increase being front-

loaded. That track implies that the OCR will reach 3.5% by the end of this year – and with just four more

review dates this year, some of the upcoming moves will have to be 50-pointers as well.

• Today’s statement fully endorses the forecast track that we published in our Economic Overview last week.

We argued that the need for a firmer response to inflation, and the value of early action, would prompt the

RBNZ to lift the cash rate by 50 basis points four times in a row between April and August, on the way to a

peak of 3.5% by November. Obviously we have no reason to change that view after today’s statement.

• However, what did surprise us was how quickly the RBNZ shifted to this view, in light of what it has said

recently. In the February Monetary Policy Statement the OCR was expected to reach a peak of 3.4% by

the end of 2024. The following policy review in April didn’t include a new set of forecasts, but the RBNZ

indicated verbally that it was comfortable with the peak in that February profile, but would look to get there

sooner. Six weeks later, the Monetary Policy Committee has decided that earlier rate hikes alone won’t cut

it – the OCR will need to reach a higher peak as well.

• So what’s behind the RBNZ’s change of view? The most succinct explanation came from Governor Orr at

the following media conference: behavioural change within the policy committee has been the biggest

factor in the evolution of the RBNZ’s stance over recent months. While we can only guess at the

conversations that would have gone on around the table, we suspect that the RBNZ has come to realise

that it’s fallen behind in its fight against inflation, and is now having to play catch-up.

10 | P a g e

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBMNI Policy Team Insights

MNI STATE OF PLAY: RBNZ Wants 'Least Regrets" On Policy Views

By Lachlan Colquhoun

SYDNEY (MNI) - Reserve Bank of New Zealand Governor Adrian Orr says the central bank does not want "to have

done too little too late" and this "least regrets" policy drove Wednesday's 50 basis point hike in the official cash rate

to 2.0%.

"Inflation expectations are just continuously rising," Orr told a press conference on Wednesday. "And the task of

putting inflation back to within its range becomes incredibly costly. So that is why we have to risk doing too much

too soon, rather than risk too little doing too little too late."

--KIWI GAINS

While the 50 basis point hike was expected by many, the RBNZ surprised in publishing a new track for the OCR in

its updated Monetary Policy Statement which had the rate reaching 3.4% by the end of the year, significantly higher

than the forecast of 2.2% from February's MPS based on higher inflation forecasts.

The news sent the NZ dollar higher, up from 64 cents to 65 cents against the USD.

The OCR track now has rates peaking at 3.9% at the end of 2023 before falling to 3.7% by the end of 2024.

The RBNZ statement noted that global growth was slowing and inflation risks remained high and even though the

NZ economy enjoyed underlying strength, "strong headwinds" remained. Rising global interest rates have also

narrowed interest rate differentials with New Zealand, adding to downward pressure on the New Zealand dollar

exchange rate.

--INFLATION VIEWS

"The Committee noted that the lower New Zealand dollar raises import prices - exacerbating the effect of elevated

global prices," the statement said.

NZ inflation has surged to 6.9% in the first quarter of 2022, and today's MPS forecast it would fall to 5.5% by the

end of the year and to 2.6% by December 2023, back inside the RBNZ target of 1% to 3%.

Helping that along will be a 15% "peak to trough" fall in house prices, which surged around 25% on average in

2021 and helped fuel inflation.

The RBNZ has raised rates at every meeting since October, after cutting the OCR to a record low of 0.25% as it

responded to the pandemic. The central bank is forecasting economic growth at 3.1% this year and 1.1% next year,

both lower than February's forecasts.

The MPS includes forecasts for the NZ Dollar against the TWI, with no fluctuation from 71.8 for the forecast period

out to March 2025 but higher than the previous MPS.

11 | P a g e

Business Address – MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBYou can also read