Marin Sales Meeting, August 24, 2021 Selected Angles on the Market

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Marin Sales Meeting, August 24, 2021

Selected Angles on the Market

Presented by Patrick Carlisle

Compass Chief Market Analyst, Bay Area

1989 2021: agent, sales manager, designated broker, director of training, VP of

business development, chief market analyst Pacific Union, Paragon, Compass

1st Half, Dollar-Volume Home Sales House, condo, co-op, townhouse, TIC,

halfplex sales reported to NorCal Regional

Marin County, Sales Reported to MLS since 2015* MLS, January 1 through June 30 of each year.

In the first 6 months of 2021, almost

$3.5 billion in home sales were

Of Bay Area Counties, Marin County reported to MLS in Marin County, 65%

saw the highest percentage increase in above the previous peak in 2018.

2021 over its previous peak in sales.

Covid hits in

Spring 2020

$1,876,400,000 $1,899,000,000 $1,973,000,000 $2,123,100,000 $2,014,500,000 $1,593,900,000 $3,493,500,000

1st Half 2015 1st Half 2016 1st Half 2017 1st Half 2018 1st Half 2019 1st Half 2020 1st Half 2021

* As reported to NorCal Regional MLS. Data from sources deemed reliable but may contain errors and

subject to revision. All numbers are approximate and rounded. We estimate, very approximately, that

10% - 12% of sales are not reported to MLS and thus not reflected in this analysis.

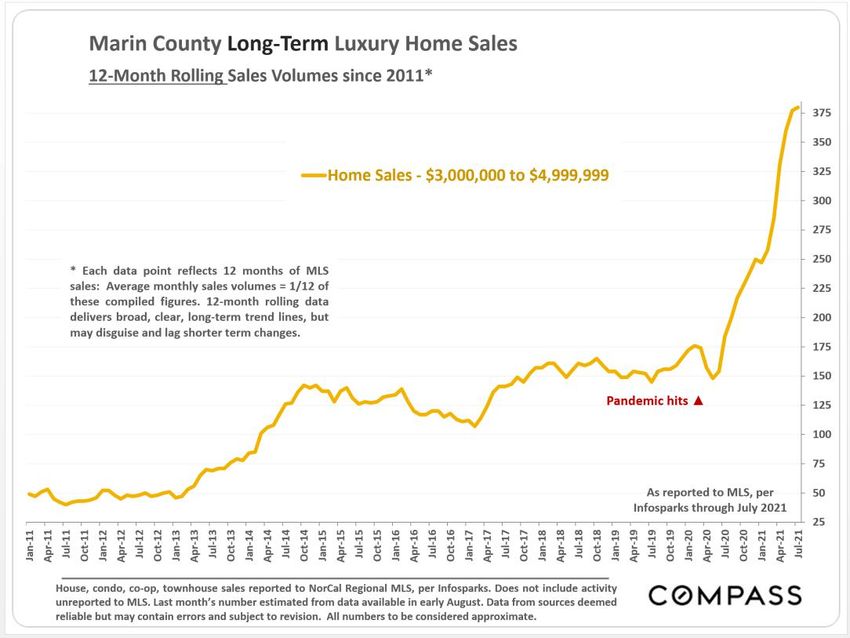

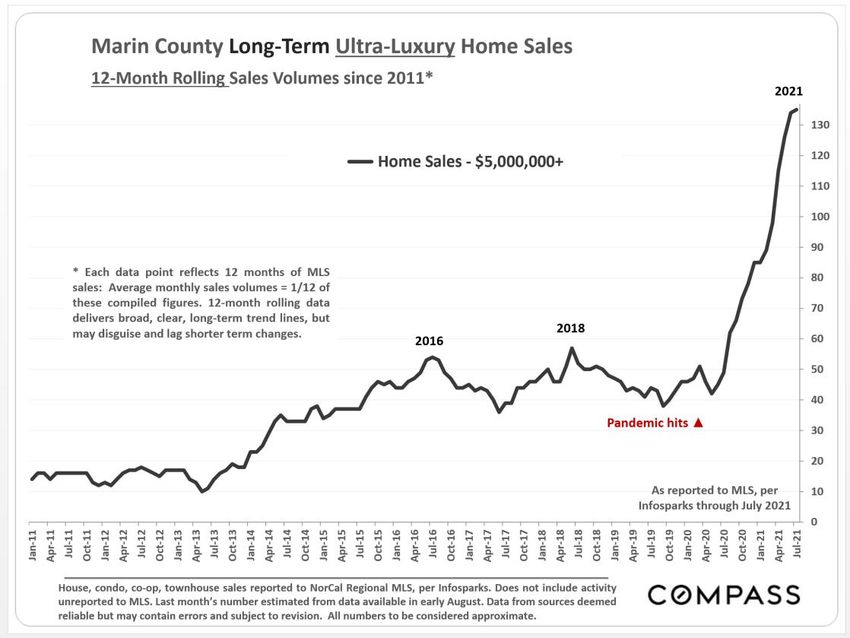

New Listing & Sales Volumes, Longer-Term Trends since 2005

Marin County, 12-Month Rolling Data*

Updated through July 2021

5,000

4,500

12-month rolling data delivers Highest 12-Month New Listing Volume since 2010

broad, clear, long-term trend

lines, but may disguise and Highest 12-Month Sales Volume since 2005

4,000 lag shorter term changes.

3,500

12-Month-Rolling New Listing Volume

12-Month-Rolling Sales Volume

3,000

2,500

▲ Market recovery begins Pandemic strikes ▲

2,000

Financial markets crash ▲

The smaller the gap between new listings and sales, the tighter

the supply of homes for sale as compared to buyer demand.

1,500

Jul-17

Jul-05

Jul-06

Jul-07

Jul-08

Jul-09

Jul-10

Jul-11

Jul-12

Jul-13

Jan-14

Jul-14

Jul-15

Jul-16

Jul-18

Jul-19

Jul-20

Jul-21

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Jan-21

* Each data point reflects the total of 12 months of activity for houses, condos, co-ops and townhouses.

1/12 of these numbers = an average month within the 12 month period. Sales reported to MLS, per NorCal

Regional MLS, per Infosparks. Last month data estimated from data available in early August. Data from

sources deemed reliable, but may contain errors and subject to revision. Numbers are approximate.

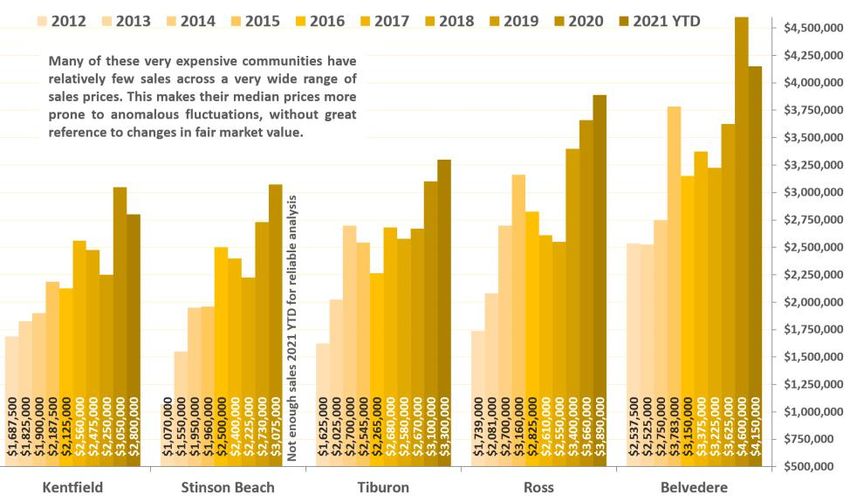

Marin County Home Price Trends since 2005

Monthly Median House Sales Prices, 3-Month Rolling

2021 $1,800,000

$1,700,000

Median sales price is that price at which half the

$1,600,000

sales occurred for more and half for less. It is a

very general statistic, often affected by other

factors besides changes in fair market value. $1,500,000

2018

Monthly and seasonal fluctuations are common. $1,400,000

Longer-term trends are more meaningful than

short-term changes. $1,300,000

$1,200,000

Pandemic hits ▲

$1,100,000

$1,000,000

$900,000

2009 - 2012

$800,000

$700,000

Financial Market Crash ▲

$600,000

Jul-12

Jul-05

Jul-06

Jul-07

Jul-08

Jul-09

Jul-10

Jul-11

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jul-20

Jul-21

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Jan-21

3-month rolling sales reported to NorCal Regional MLS, per Infosparks. Analysis

may contain errors and subject to revision. All numbers are approximate.

San Francisco Bay Area Real Estate Market Cycles

Home Price Increases & Declines, by Percentage, 1984 2021*

https://www.spglobal.com/spdji/en/indices/indicators/sp-corelogic-case-shiller-san-francisco-home-price-nsa-index/#overview

Updated through

Market Peaks & Bottoms April 2021

Approximate Percentage Changes

A simplified, smoothed-out graph*

Financial

markets crash 2012 4/2021

Per CoreLogic S&P Case-Shiller + 143%

Aggregate Index for Bay Area Houses

Seasonally adjusted. Not adjusted for inflation.

2002 2006/07

+ 72%

2007 2011

1995 2001 High-tech boom,

- 40% then pandemic

1989 SF + 100% Dotcom

earthquake Pop/ 9-11 Subprime

- 5% bubble

1984 1990 Approximate % value changes based upon S&P Case-

Dotcom

+ 100% 1991 1994 Shiller Home-Price Index for 5-county metro area

boom

- 11% (aggregate sales index, seasonally adjusted). Different

Junk bond price segments were affected very differently in the

boom scale of their subprime bubbles and resulting crashes.

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

* The years between market peaks and bottoms are not accurately represented, but entered as straight

lines between high and low points to illustrate percentage changes over time. Shorter-term fluctuations

are not reflected on this chart. All numbers are very approximate and subject to revision.

Percentage of Off-MLS Sales by Price Segment House, condo, townhouse, sales

reported to NorCal Regional

Marin County, Sales Reported to MLS, 2021 YTD MLS, 1/1/21 8/10/21

40%

11% of Marin County home sales reported

to MLS were marketed off-MLS. As the sales 35%

price increased, the percentage of sales

occurring off-MLS soared.

30%

Of off-MLS sales of $5 million & above, 43%

were listed by Compass agents.

25%

20%

15%

10%

5%

8% 15% 18% 32% 42%

0%

Under $2,000,000 $2,000,000 - $3,000,000 - $5,000,000 - $8,000,000+

$2,999,999 $4,999,999 $7,999,999

* As reported to NorCal Regional MLS. Data from sources deemed reliable but may

contain errors and subject to revision. Not all off-MLS sales are reported to MLS.

New Listings Coming on Market

Marin County Market Dynamics & Seasonality by Month

May Oct.

2018 2020

May Sept. June

2019 2019 June 2021

350 2020

300

Feb.

250

2020

Mid-

200 Mid- Summer

Summer

150

The ebb and flow of new listings coming on

market is deeply affected by market seasonality.

100 Pandemic

Hits

December

50

December

December

0

Nov-20

Feb-18

Apr-18

Jul-18

Nov-18

Jul-19

Jul-20

Apr-21

Jul-21

Jun-18

Sep-18

Feb-19

Apr-19

Sep-19

Nov-19

Feb-20

Apr-20

Oct-18

Jun-19

Oct-19

Jun-20

Sep-20

Feb-21

Oct-20

Jun-21

May-18

May-21

Jan-18

Dec-18

May-19

Jan-19

Dec-19

May-20

Jan-20

Dec-20

Jan-21

Mar-18

Aug-18

Mar-19

Aug-19

Mar-20

Aug-20

Mar-21

Per Realtor.com Research: https://www.realtor.com/research/data/, listings posted on site. Data from sources

deemed reliable, but may contain errors and subject to revision. All numbers should be considered approximate.

Active Listings on Market

Marin County Real Estate Market Dynamics & Seasonality

For houses and condos

June

2019

Oct. 600

2018

June

May 2018 June Oct. 500

2017

2020 2020

Pandemic hits

400

July

2021

300

200

This is a snapshot measure of how many active listings can be

expected on any given day of the specified month. This number 100

is affected by 2 major dynamics: 1) how many new listings come

on market, and 2) how quickly buyers snap them up.

0

Jul-17

Jul-18

Jul-19

Jul-20

Jul-21

Sep-17

Nov-17

Sep-18

Nov-18

Sep-19

Nov-19

Sep-20

Nov-20

Jan-21

May-19

Mar-20

May-20

Jan-17

Mar-17

May-17

Jan-18

Mar-18

May-18

Jan-19

Mar-19

Jan-20

Mar-21

May-21

Per Realtor.com Research: https://www.realtor.com/research/data/, listings posted on site. Data from sources

deemed reliable, but may contain errors and subject to revision. All numbers should be considered approximate.

Marin County Short-Term Market Dynamics & Seasonality

Listings Accepting Offers (Going into Contract) by Month Houses, condos, co-ops,

townhouses as listed in MLS

Typically, market activity ebbs and flows by season, though the pandemic

upended normal trends in 2020. In summer 2021, activity began to decline July

(a little) from spring peaks, an apparent reversion to seasonal norms 2020 Spring

October

400 though activity remained much higher than in pre-pandemic summers. 2020 2021

May

350 May 2019

2018

June-

300 October Fires July

2019 2021

250

Summer

Summer 2019

200

December

- January

150

100 December

December

- January Pandemic

- January

hits

50

0

Nov-19

Feb-18

Feb-19

Feb-20

Feb-21

Apr-18

Jul-18

Oct-18

Apr-19

Jul-19

Oct-19

Apr-20

Jul-20

Oct-20

Jun-18

Sep-18

Nov-18

Jun-19

Sep-19

May-20

Nov-20

Apr-21

Jul-21

Jun-20

Sep-20

Jun-21

May-18

Jan-18

Dec-18

May-19

Jan-19

Dec-19

Jan-20

Dec-20

May-21

Jan-21

Mar-18

Aug-18

Mar-19

Aug-19

Mar-20

Aug-20

Mar-21

As reported to NorCal Regional MLS, per Infosparks. Does not include activity unreported to MLS. Last month’s

number estimated from data available in early August. Data from sources deemed reliable but may contain errors

and subject to revision. All numbers to be considered approximate.Months Supply of Inventory (MSI)

Marin County Real Estate Market since 2011 Based upon accepted-offer activity for

Marin houses, condos and townhouses

reported to Bareis MLS per Broker Metrics

5

4.5 MSI = the number of months it would take

to sell the existing inventory of homes for

sale at current rates of market activity.

4

Fluctuations occur due to market

Market recovery begins in conditions (demand vs. supply) and typical

3.5 market seasonality. Pandemic

hits

3

2.5

2

1.5

1

Spring

2018

0.5 Spring

2021

0

Jul-21

Jul-12

Jul-13

Jul-14

Jul-15

Jul-16

Jul-17

Jul-18

Jul-19

Jul-20

Oct-11

Apr-12

Oct-12

Apr-13

Oct-13

Apr-14

Oct-14

Apr-15

Oct-15

Apr-16

Oct-16

Apr-17

Oct-17

Apr-18

Oct-18

Apr-19

Oct-19

Apr-20

Oct-20

Jan-21

Apr-21

Jan-12

Jan-13

Jan-14

Jan-15

Jan-16

Jan-17

Jan-18

Jan-19

Jan-20

Data from sources deemed reliable, but may contain errors and subject to revision.

All numbers approximate. Late reported activity may alter last month’s reading.Price Reductions on Active Listings

Marin County Real Estate Market Dynamics

For houses and condos

Sept.

Oct. 2019

2018 250

June

The number of price reductions

2019

remains far below seasonal norms, 225

another indication of a market

characterized by extremely high 200

demand.

175

Sept.

2017 June

2018 Oct. 150

June 2020

2017 June

2020 125

Pandemic hits

100

May-July

2021

75

50

25

0

Jul-17

Jul-18

Jul-19

Jul-20

Jul-21

Sep-17

Nov-17

Sep-18

Nov-18

Sep-19

Nov-19

Sep-20

Nov-20

Jan-21

May-17

May-18

May-19

Mar-20

May-20

Jan-17

Mar-17

Jan-18

Mar-18

Jan-19

Mar-19

Jan-20

Mar-21

May-21

Per Realtor.com Research: https://www.realtor.com/research/data/, activity on website. Data from sources

deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.Luxury Homes Listings Accepting Offers by Month

Marin County: Homes Priced $3,000,000+ Going into Contract

Residential listings posted in

MLS, per Infosparks

Short-Term Trends By Month May

2021

Typically, luxury market activity ebbs and flows by July-Aug.

season, peaking in spring, hitting its nadir in mid-winter, 2020

though the pandemic upended normal trends in 2020. In 50

summer 2021, activity declined from spring peaks, an Oct.

2020

apparent reversion to seasonal norms though activity

was much higher than in typical summers (2018, 2019)

40

June-

May July

Fires

May 2019 2021

2018 30

Sept.

2018 Oct.

2019

20

January

Summer July 10

Winter

▲ Pandemic hits

Winter

0

Jul-18

Mar-18

Apr-18

Oct-18

Mar-19

Mar-20

Mar-21

Aug-18

Nov-18

Jul-19

Oct-19

Aug-19

Nov-19

Jul-20

Oct-20

Aug-20

Nov-20

Jul-21

Feb-18

Dec-18

Feb-19

Apr-19

Dec-19

Feb-20

Apr-20

Dec-20

Feb-21

Apr-21

Jan-18

May-18

Jun-18

Sep-18

Jan-19

May-19

Jun-19

Sep-19

Jan-20

May-20

Jun-20

Sep-20

Jan-21

May-21

Jun-21

House, condo, co-op, townhouse activity reported to NorCal Regional MLS, per Infosparks. Does not include

activity unreported to MLS. Last month’s number estimated from data available in early August. Data from

sources deemed reliable but may contain errors and subject to revision. All numbers are approximate.Year-over-Year Median House Sales Price Increases

by Bay Area County, Q2 2021 vs. Q2 2020 Per CAR Housing Affordability

Index calculations

San Mateo $2,117,500

$1,700,000

San Francisco $1,900,000

$1,710,000

Santa Clara $1,699,500

$1,380,000

Marin $1,650,000

$1,460,000

SF Bay Area $1,345,000

$989,000

Alameda $1,300,000 Q2 2021

$990,000

Santa Cruz $1,250,000 Q2 2020

$905,000

Contra Costa $1,000,000

$725,000

Napa $905,000

$720,000

$860,000 Median price is that price at which half the sales

Monterey $680,000 occurred for more and half for less. It is a very general

$817,950 statistic that typically disguises an enormous range of

California $611,000 sales prices in the individual underlying sales. It may

$795,000 fluctuate for reasons other than changes in fair market

Sonoma $680,000 value, and should not be considered an exact

$570,000 measurement of changes in fair market value. Seasonal

Solano $485,000 fluctuations in median sales prices are very common.

United States $357,900

$291,300

Data per California Association of Realtors: “C.A.R.'s Traditional Housing Affordability Index (HAI). Methodology

can be found on www.CAR.org, Market Data section. “SF Bay Area includes 9 counties, Napa to Santa Clara.Percentage of Households Able to Afford Median Priced House

by San Francisco Bay Area County, Q2 2020 to Q2 2021 Per CAR Housing

Affordability Index

This statistic is calculated using Q2 median house sales 46%

prices, county household income figures, the prevailing

fixed 30-year interest rate, assuming a 20% Q2 2020 Q2 2021

downpayment, and including tax and insurance costs. 40%

37%

According to the CAR Index, the 4 most expensive

counties on the left side of the chart saw no or very 33% 33%

small changes in affordability percentages, while more 31%

affordable counties saw large or very large declines.*

26% 26%

25% 25%

23% 23% 23%

22% 22%

21% 21%

19% 19%19%

18% 18%

17%

15%

San SF Santa Marin Santa Monterey Alameda Napa CA Sonoma Contra Solano

Mateo Clara Cruz Costa

Calculation per California Association of Realtors: C.A.R.'s Traditional Housing Affordability

Index (HAI). Methodology can be found on www.CAR.org, Market Data section.Estimated Migration of Bay Area Households in 2020

Bay Area County # Households # Households Change in # Total # of % Change in

Moving In (2020) Moving Out (2020) Households Households Households

Alameda 50,000 67,000 - 17,000 577,177 - 2.9%

Contra Costa 35,000 32,000 + 3,000 394,769 + .8%

Marin 9,050 7,000 + 2,050 105,432 + 1.9%

Monterey 5,400 5,050 + 350 127,155 + .3%

Napa 3,300 2,550 + 750 48,705 + 1.5%

San Francisco 27,500 68,000 - 40,500 362,354 - 11%

San Mateo 24,000 34,000 - 10,000 263,543 - 3.8%

Santa Clara 42,000 67,000 - 25,000 640,215 - 3.9%

Santa Cruz 6,050 6,000 + 50 95,818 -

Solano 12,000 10,650 + 1,350 149,865 + .9%

Sonoma 10,900 8,800 + 2,100 189,374 + 1.1%

Household numbers are estimates extrapolated from The Wall Street Journal article, “Americans Up & Moved During

the Pandemic, based on “permanent, change-of-address filings in 2020. The term “household can signify one or

many persons. The general dynamic in the Bay Area was net out-migration from more urban regions, and net in-

migration into more suburban/rural areas. Of counties seeing negative changes, relocating tenants (paying very high

rents) the newly unemployed, office employees changed to work-from-home, or students at closed universities

were almost certainly the dominant component in out-migration. Trends may change with the opening of offices,

universities, urban amenities. Even in non-pandemic years, significant population movements are normal.

All numbers are approximate. WSJ article published 5/11/21: Methodology/data not validated by Compass.

Other sources have published different conclusions on migration. Total household data per U.S. Census 2019 ACS

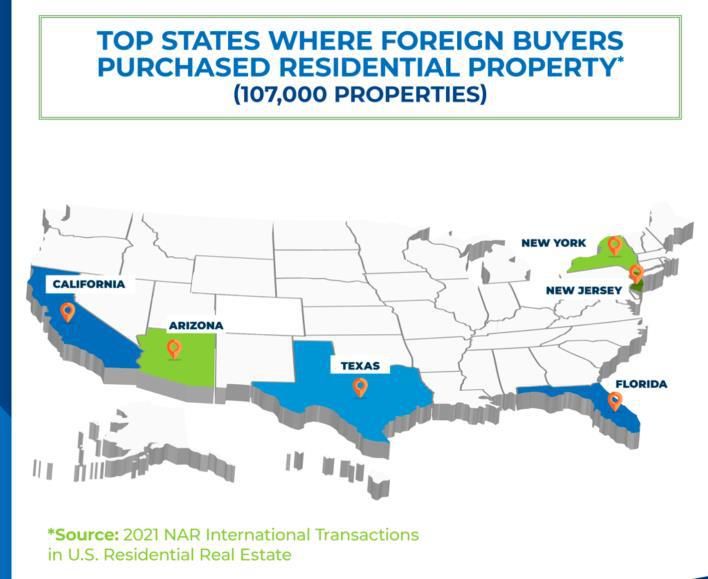

survey estimates. Compiled in good faith, but may contain errors, and subject to revision.Steep U.S. Decline in Foreign National Homebuyers

Estimated Dollar Volume Sales in Billions, Top 5 Countries National Association

of Realtors estimates

International Homebuyer Purchases in Billions of Dollars

30

2013 2014 2015 2016 2017 2018 2019 2020 2021

Years designated reflect estimated sales 25

from April of the previous year through

March of the year specified: Purchases by

resident and non-resident foreign nationals.

20

Billions of Dollars

15

10

| 86% decline, | 78% decline,

2017 - 2021 | 2017 - 2021 | | 60% decline, | 69% decline, | 72% decline,

2017 - 2021 | 2017 - 2021 | 2017 - 2021 | 5

$12.8

$28.1

$27.3

$31.7

$30.4

$13.4

$11.5

$11.8

$13.8

$11.4

$10.5

$4.5

$8.9

$9.5

$4.2

$3.9

$5.8

$7.9

$6.1

$7.8

$7.2

$6.9

$5.4

$3.1

$3.6

$4.5

$4.9

$4.8

$9.3

$4.2

$2.3

$5.8

$2.9

$4.2

$5.8

$3.9

$5.5

$9.6

$7.3

$3.8

$1.4

$2.7

$22

$19

$8

0

China Canada India Mexico United Kingdom

Estimates from the “2021 Profile of International Transactions in U.S. Residential Real Estate published by the National

Association of Realtors in July 2021, based upon a survey of Realtors. Data from sources deemed reliable, but may contain

errors and subject to revision. All numbers to be considered approximate, good-faith estimates. China includes the People’s

Republic, Hong Kong and Taiwan.Mortgage Interest Rate Trends, November 2018 Present

30-Year & 15-Year Conforming Fixed Rate Loans, Weekly Average Readings Rates published

by the FHLMC

4.75%

4.50% 30-Year Fixed Rate Per Freddie Mac, on August 5, 2021, the

weekly average interest rate for a 30-year

4.25% 15-Year Fixed Rate fixed-rate mortgage was 2.77%, slightly

above its nadir in January (2.65%), and the

4.00% 15-year rate was at a historic low at 2.1%.

3.75% In November 2018, the 30-year rate hit

4.94%, and in 2007, it was 6.3%.

3.50%

3.25%

3.00%

2.75%

2.50%

2.25%

2.00%

Nov. Interest rates may fluctuate suddenly and dramatically, and it is very difficult to predict rate Aug

2018 changes. Data from sources deemed reliable but not guaranteed. Anyone interested in residential 2021

home loans should consult with a qualified mortgage professional and their accountant.Consumer Price Index

12-Month Percentage Change, Past 20 Years

As the economic recovery from the pandemic has

accelerated, the Consumer Price Index, a

measurement of inflation, has seen large increases.

Historically, the standard remedy for surging inflation is to raise interest rates, however there are many opinions as

to whether higher-than-normal inflation rates will persist and become a significant economic issue requiring

response by the Federal Reserve Bank in the near future. Predicting interest rate changes is extremely difficult.

Certainly, this is an economic indicator to watch in coming months.

Chart from U.S. Bureau of Labor Statistics, published mid-August 2021:

https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm.

Data from sources deemed reliable, but may contain errors and subject to revision.S&P 500 Stock Index, 1995 2021 S&P +34%, Feb.

2020 July 2021 ► July 30,

By Month through July 2021 2021

▼

4,250

4,000

3,750

S&P 18% drop, Sept. Dec. 2018

Interest rates +20% in 2018 ► 2018 3,500

peak 3,250

▼

3,000

S&P 12% decline, July 2,750

2015 Feb. 2016 ► 2015

◄ Post dotcom & 9/11 low

peak 2,500

◄ Post-bubble crash low

Pandemic crash ►

▼ 2,250

2000 2007 2,000

peak peak

▼ 1,750

▼ ▲

Mid-2015 Mid-2016 1,500

Chinese stock market 1,250

crash; IPO activity crash;

oil price crash; Brexit 1,000

750

500

250

0

1-Jan-04

1-Jan-15

1-Jan-95

1-Jan-96

1-Jan-97

1-Jan-98

1-Jan-99

1-Jan-00

1-Jan-01

1-Jan-02

1-Jan-03

1-Jan-05

1-Jan-06

1-Jan-07

1-Jan-08

1-Jan-09

1-Jan-10

1-Jan-11

1-Jan-12

1-Jan-13

1-Jan-14

1-Jan-16

1-Jan-17

1-Jan-18

1-Jan-19

1-Jan-20

1-Jan-21

Data from multpl.com and Yahoo! Finance. An approximate illustration only. Data from sources

deemed reliable but may contain errors and subject to revision. Financial markets can be prone to

significant volatility even on a short-term basis. For general illustration purposes only.Editable email newsletters in Marketing Center/

Market Data section

Newsletters in Flippingbook format published

monthly

Newsletter pdfs and jpgs (by month, then region):

https://drive.google.com/drive/folders/1kSMZJP6ZPWnFF2

3ZTrqMMvzzkSjkLjAU?usp=sharing

Market share charts (by region):

https://drive.google.com/drive/folders/1RX6mZKYdQOwB-

AthmA0_ox43MbFo2RIU?usp=sharing

Online: https://www.bayareamarketreports.com/

CAR Mid-Year Forecast:

https://www.car.org/en/marketdata

/marketforecastStatistics are generalities, essentially summaries of widely disparate data generated by dozens or hundreds of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers are approximate. Data from MLS, but not all listings or sales are reported to MLS. Median Sales Price is that price at which half the properties sold for more and half for less. It may be affected by seasonality, n al events, or changes in inventory and buying trends, as well as by changes in fair market value. The median sales price for an area will often conceal an enormous variety of sales prices in the underlying individual sales. Dollar per Square Foot is based upon the home interior living space and does not include garages, unfinished attics and basements, rooms built without permit, patios, decks or yards (though all those can add value to a home). These figures are usually derived from appraisals or tax records, but are sometimes unreliable (especially for older homes) or unreported altogether. The calculation can only be made on those home sales that reported square footage. Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, bon rooms, additional parking, quality of location within the neighborhood, and so forth. How these statistics apply to any particular home is unknown without a specific comparative market analysis. Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

You can also read