Is 2021 going to be the year of a value rotation? - VALEUR INTRINSEQUE FOCUS - Fourpoints IM

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Is 2021 going to be the year of a value rotation?

VALEUR INTRINSEQUE FOCUS

For professional investors only March 2021

FOURPOINTS IM

I - ANALYSIS - A DECADE OF BULL MARKETS BOOSTED BY CENTRAL BANKS

FED balance sheet Source : Bloomberg

The stock markets were supported by the big central banks (Fed, BoJ, ECB…) which bought trillions of assets, supporting the price of

financial assets. These central banks now hold the equivalent of 30% of global GDP.

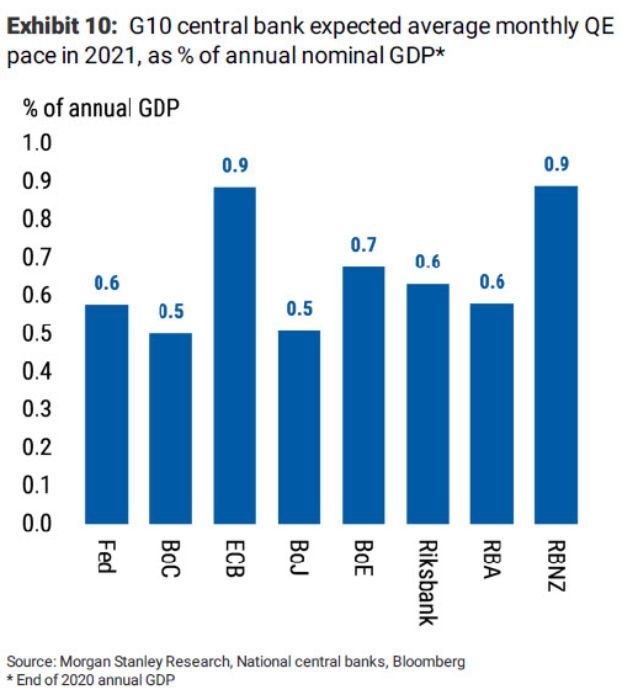

In 2021, there should be no major changes in the monetary policies of the major central banks.

FOURPOINTS IM

II- 2021 : MONETARY AND BUDGETARY SUPPORT

M2 (in $ Billions) in USA

21000

19000

17000

15000

13000

+24% in2020

11000

9000

7000

5000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Source : Fred

In Europe a recovery plan of nearly 750 billion was voted, while

in the United States a recovery plan of 1 900 billion was voted

(of a magnitude three times greater than the fall of the

activity), including 1 000 billion in direct aid to households.

In 2021, the expansionary monetary policy will continue. Above

are the monthly injections from the major central banks as a%

of nominal GDP.

FOURPOINTS IM

II - STIMULUS PACKAGES - THE IMPACT ON THE AMERICAN CONSUMER

Despite a record level of indebtedness, the weight of

debt within households continues to decrease thanks

to the fall in interest rates and the increase in

income.

The behavior of American consumers will be crucial given

the current average savings rate, which stands at around 13

percentage points of GDP compared to a usual level of 3

percentage points.

This global saving should logically fuel consumption and

therefore the economic recovery in the coming quarters.FOURPOINTS IM

III – CRISIS RECOVERY AND ITS PRESSURE ON PRICES

90

Price of containers 40

China and US quarterly growth +33,4

85 30

20

80

10

75 0

-10

70

-20

65 -30

-40 -31,4

60

août-15

août-16

août-17

août-18

août-19

août-20

avr.-15

avr.-16

avr.-17

avr.-18

avr.-19

avr.-20

déc.-14

déc.-15

déc.-16

déc.-17

déc.-18

déc.-19

déc.-20

Chine Etats-Unis

3000

SOX Semiconductor Index

2500

The economic recovery, particularly in China, inventories

effect, strict health precautions are all factors favoring a

2000 bottleneck in the production chain.

1500

These tensions have created an imbalance between supply

1000 and demand leading to an increase in prices of raw

materials, certain products such as semiconductors or even

500 sea freight, which in Asia, for lack of available containers,

sees its prices take off.

0

juin-15

sept-15

juin-16

Dec 2015

sept-16

juin-17

juin-19

juin-20

Dec 2016

sept-17

juin-18

Dec 2017

sept-18

Dec 2018

sept-19

Dec 2019

sept-20

Dec 2020

mars-15

mars-16

mars-17

mars-18

mars-19

mars-20

Source : BloombergFOURPOINTS IM

III – CRISIS RECOVERY AND ITS PRESSURE ON PRICES

120 12000

Bloomberg Commodities Index Price of Copper

110 10000

100 8000

90

6000

80

4000

70 +61% in1 year

2000

60

0

50

déc.-14 déc.-15 déc.-16 déc.-17 déc.-18 déc.-19 déc.-20

Source : Bloomberg

Copper and Nickel are at an all time high since 2011. Copper, considered as a leading indicator of the

Lumber is at an all time high. Sugar hit a 4 year high. economy, is at its highest for 10 years. The rise in

commodity prices and the change in the economic

model of China (which has long exported disinflation)

raise the risk of hike in inflation in the United States.FOURPOINTS IM

IV – PRESSURE ON INTEREST RATES IN 2021

The US 10 years and 30 years have been on an 3

upward trend for over 6 months now. In Europe, 2,5

the movement is more recent and less violent.

2

The market is now anticipating a first rate hike in 1,5

March 2023. 1

0,5

0

-0,5

Inflation swap forward 5y5y

3

-1

2,5 déc.-19 mars-20 juin-20 sept.-20 déc.-20

2

10 years Treasury yield 30 year Treasury yield OAT 10 ans

1,5

1

The sharp rise in the expected inflation rate from its low at the

end of last March, to 2.2% today, attests to the risk of a return

0,5

of inflation in the United States.

0

2015 2016 2017 2018 2019 2020 2021

Etats-Unis Europe

Nonetheless, we believe that inflation should materialize more

USA

in an increase in goods and services (with monetary creation

resulting from "helicopter money"), rather than in an increase

Source : Bloomberg

in financial assets as in the last decade.FOURPOINTS IM

V – 2021, THE RETURN OF VALUE QUALITY / CYCLICAL STOCKS?

115

From February 12 to March 17

110

7,6%

105

1,5%

100

-5,2%

95

90

85

80

-20,8%

75

12-févr. 19-févr. 26-févr. 5-mars 12-mars

Nasdaq Chinext S&P 500 S&P Cyclicals

Since the beginning of the year, a sector rotation has started, from "growth" sectors such as technology and "proxy bonds" to

cyclical sectors (Banks, energy, auto, industrial).FOURPOINTS IM

V – 2021, THE RETURN OF VALUE QUALITY / CYCLICAL STOCKS?

6

2,3

2,1 5

in % (en %)

1,9

4

Growth/Value

américain

1,7

3

1,5

yield

10 years10USans

1,3 2

1,1

1

0,9

0,7 0

Source : Bloomberg

Russell 1000 Growth / Russell 1000 Value 1010ans

years

US US yield

Inflation and economic recoveries are generally favorable environments for discounted companies.

In our opinion, this movement should continue in the coming months.

The gap between growth stocks and discounted stocks is closing sharply (blue curve).

There is a significant correlation (0.84) between the rise of the 10-year US dollar and the outperformance of value stocks compared

to growth stocks.VA L E U R I N T R I N S E Q U E F O C U S

VALEUR INTRINSEQUE

A SIGNIFICANT REBOUND SINCE NOVEMBER 2020 TO MARCH 12TH

140

139

Valeur Intrinseque evolution

135

130 The vast majority of the portfolio drove the performance of the

125

portfolio.

120 120

This movement has continued since the beginning of the year

115

110

105

100

oct.-20 nov.-20 déc.-20 janv.-21 févr.-21

MSCI World DNR Valeur Intrinseque

18 1,8

Valeur Intrinsèque and US yield (10 y)

16 1,6

14 1,4

12

1,2

10

1

8

0,8

6

0,6

4

2 0,4

0 0,2

octobre-20 novembre-20 décembre-20 janvier-21 février-21

-2 0

Performance relative de Valeur

Relative performance Intrinseque/MSCI

Valeur World

Intrinseque/MSCI Taux 10 ans US

10 years US yield

World DNRRECENT HISTORY

A transition period between the acquisition of Pastel & Associés by Fourpoints at the end of 2018 and the departure of David

Pastel at the end of 2019.

Started in 2019, the portfolio renewal was accelerated during 2020. Thanks to our active monitoring, we took advantage of

strong market discrepencies caused by the COVID-19 crisis. We focused on companies that were impacted in the short term by

the health crisis but which will eventually emerge stronger.

In 2020: 19 new stocks, 4 disposals and cash ratio down from 30% to 5%.

Following this renewal, the portfolio is now more diversified, with 30 holdings in various sectors and geographies.

Around 50% of the portfolio was invested last year in great companies at very attractive cost prices.

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 12

Les performances passées ne sont pas un indicateur fiable des performances futures.A YEAR OF OPPORTUNITIES

MAIN TRADES IN 2020

NEW POSITIONS DISPOSALS

Titres Secteurs Pays Titres Secteurs Pays

Foot Locker Sporting goods retailer United States Randstad Temporary Staffing Netherlands

MSC Industrial Direct Industrial distribution United States Thermador Groupe Distribution of heating and plumbing products France

Groupe SEB Manufacturing of small household equipment France Mohawk Industries Flooring manufacturer United States

W.W. Grainger Industrial distribution United States Greggs Bakery chain United Kingdom

Pirelli Tire manufacturer Italy

Compass Group Food services United Kingdom

MARR Distribution of food products Italy

Alphabet Technological services Unites States

LafargeHolcim Building materials Switzerland

Carrier Global Air conditioning / Refrigeration United States

Otis Elevator manufacturer United States

Henry Schein Distribution for healthcare professional United States

Photo-me InternationalPhotographic booths and laundries United Kingdom

Autoliv Manufacturing of airbags and seat belts United States

Beneteau Boat Manufacturer France

Greggs Bakery chain United Kingdom

World Fuel Services Fuel Distribution United States

Palfinger Manufacturer of innovative lifting Austria

Mitie Group Facilities Management United Kingdom

STRENGTHENED POSITIONS REDUCED POSITIONS

ISS Facilities management Danemark Covestro AG Industry Germany

Sodexo Food services / Facilities management France Markel Corp Investment company United States

Takkt Business equipment distribution Germany Loews Corp Investment company United States

Berkshire Hathaway Investment company United States

Next Apparel retailer United Kingdom

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 13

Les performances passées ne sont pas un indicateur fiable des performances futures.A MORE DIVERSIFIED PORTFOLIO

P ORTFOLIO EVOLUTION

February 2021

Outsourcing services

Investment companies

Professional distribution

Construction / Renovation

Consumer discretionary

Retail

Oil & Gas services

Industry

Cash

0% 5% 10% 15% 20%

United States

France

UK

Canada

Norway

Italy

Germany

Switzerland

Austria

Denmark

Sweden

Cash

0% 5% 10% 15% 20% 25% 30%

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 14

Les performances passées ne sont pas un indicateur fiable des performances futures.TOP 15 AS OF FEBRUARY 26, 2021

Number of positions : 31 - Invested Portfolio : 94,9%

COMPANIES SECTORS COUNTRIES WEIGHT

Subsea 7 Offshore project management Norway 9.1%

Sodexo Food services / Facilities management France 6.5%

Fairfax Financial Investment companies Canada 6.4%

Takkt Business equipment distribution Germany 4.1%

IPSOS Market research France 3.5%

Compass Group Food services UK 3.4%

Markel Investment companies USA 3.4%

Foot Locker Sporting goods retailer USA 3.3%

Pirelli Tire manufacturer Italy 3.3%

Alleghany Investment companies USA 3.2%

Marr Distribution of food products Italy 3.0%

Palfinger Construction - Renovation Austria 3.0%

LafargeHolcim Building materials Switzerland 3.0%

ISS Facilities management Denmark 2.9%

Next Clothing retailer UK 2.6%

Wei ght of the fi rs t 15 pos i tions 60.6%

Number of hol di ngs 31

Ca s h 4,80%

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 15

Les performances passées ne sont pas un indicateur fiable des performances futures.HISTORIQUE DE PERFORMANCE

AS OF FEBRUARY 26, 2021

300

153,0%

250

145,3%

200

150

100

50

0

Valeur Intrinsèque P MSCI World DNR €

FUND FUND FUND (P

MSCI World MSCI World MSCI World

(P share) (P share) share)

2001* 14.8 -14.9 2008 -38.1 -37.6 2016 31.8 10.7

2002 -22.1 -32.0 2009 57.2 25.9 2017 8.4 7.5

2003 32.9 10.7 2010 19.7 19.5 2018 -18.7 -4.1

2004 16.3 6.5 2011 -17.4 -2.4 2019 1.8 30.0

2005 14.5 26.2 2012 22.6 14.0 2020 3.4 6.3

2006 13.2 7.4 2013 26.8 21.2 2021 7.6 2.4

2007 -11.3 -1.7 2014 -3.1 19.5 Annualized Performance 4.8 4.7

2015 -16.6 10.4 Cumulative Performance 153,0 145.3

Retail share and MSCI World TNR Performance as of February 26th in percentage. I share class performance is available on our website. Past performance

does not guarantee future performance. *Fund's inception on June 6th 2001

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 16

Les performances passées ne sont pas un indicateur fiable des performances futures.VALEUR INTRINSÈQUE FEATURES

INTERNATIONAL EQUITY FUND

All-cap equity fund investing in

companies from North America, Europe

and the UK.

BOTTOM-UP APPROACH LONG TERM HORIZON

Stock picking based on a For company outlook as

purely fundamental analysis well as time for investment

of companies and Private to bear fruit.

Equity valuation methods.

CONCENTRATED PORTFOLIO INDEPENDENCE

Between twenty and thirty

stocks with potentially high We don’t follow investment

weights. fads.

We don’t rely on external

research or advice.

Seeking a reasonable return with low risk by investing in

good companies at a fair price

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 17

Les performances passées ne sont pas un indicateur fiable des performances futures.WHAT IS A GOOD COMPANY FOR US?

A PROVEN AND PROFITABLE • We need to understand the business

BUSINESS MODEL • Resilience of the business in the future

A STRONG COMPETITIVE • Will allow company to preserve or increase profitability

POSITION • Ability to compound growth

• Sustainability of the company in tough times

LOW INDEBTNESS

• Unforeseen negative events will eventually happen

• Reinvestment in the company with a good rate of return

A GOOD CAPITAL ALLOCATION • External growth that makes sense

• Return excess cash to shareholders

AN EXPERIENCED MANAGEMENT • Shows consistency in the strategy

TEAM WITH STOCK OWNERSHIP • Alignment of interests

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 18

Les performances passées ne sont pas un indicateur fiable des performances futures.HOW DO WE SET A FAIR PRICE?

• Idea of seeking economic return on our investment

THINKING LIKE OWNERS

• Time for the investment to bear fruit

SHARE PRICE IS NOT AN • « Mr Market » is only there to serve us

INDICATOR OF VALUE • Price and value tend to converge over time

• In the past: how has the company fared over the past 10 years?

LONG TERM HORIZON

• In the future: what are the company’s prospects in 3-5 years?

VALUATION BASED ON • Use of fundamentals to evaluate intrinsic value of the company

"FREE CASH FLOWS“ • No market consideration in valuation

• Conservative assumptions in our valuation

MARGIN OF SAFETY

• Looking for investments with favorable odds

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 19

Les performances passées ne sont pas un indicateur fiable des performances futures.EXAMPLE : FOOT LOCKER

INVESTMENT INITIATED IN JANUARY 2020

SPORTSWEAR AND FOOTWEAR RETAILER

TURNOVER $ 8MM, MARKET CAP $ 4MM

MORE THAN 3000 STORES AROUND THE WORLD

70% OF TURNOVER IN THE UNITED STATES

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 20

Les performances passées ne sont pas un indicateur fiable des performances futures.EXAMPLE : FOOT LOCKER

A PROVEN AND PROFITABLE BUSINESS MODEL

Average revenue growth of 5% over the past 10 years.

EBIT margin 9-10%.

Average ROE of18%. 9 000 30,0%

8 000

25,0%

7 000

6 000 20,0%

5 000

15,0%

4 000

3 000 10,0%

2 000

5,0%

1 000

0 0,0%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Revenues (in M$) EBIT margin ROE

A STRONG COMPETITIVE POSITION

World largest footwear specialist: economies of scale on procurement, marketing and distribution.

Close relationship with Nike.

Brand awareness.

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 21

Les performances passées ne sont pas un indicateur fiable des performances futures.EXAMPLE : FOOT LOCKER

LOW INDEBTNESS

Historically in a net cash position.

$800M net cash at the time of the initial investment (vs market cap of $4MM).

A GOOD CAPITAL ALLOCATION

Reducing the number of stores in the US while expanding abroad.

Growth of online sales (16% of revenues vs 12% 5 years ago).

Cash return to shareholders through dividend and share buybacks.

180 1,6

160

1,2

140

120

0,8

100

80

0,4

60

40 0

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Outstanding shares (in m) Annual dividend ($)

AN EXPERIENCED MANAGEMENT TEAM WITH STOCK OWNERSHIP

Richard Johnson CEO since 2014, at Foot Locker since 1997.

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 22

Les performances passées ne sont pas un indicateur fiable des performances futures.EXAMPLE : FOOT LOCKER

VALUATION

Net cash representing 25% of the market capitalization.

Average Free cash flow over 5 previous years above $450M.

Upside potential of 50-100% compared to entry level.

Foot Locker Share Price

90

80

70 Initiated

Trimmed

60

50

40

30

Strengthened

20

10

0

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 23

Les performances passées ne sont pas un indicateur fiable des performances futures.CONTACT

Cédric Michel Julien Mathou FOURPOINTS IM

Head of business Development Investor relations 162 boulevard Haussmann

cmichel@fourpointsim.com jmathou@fourpointsim.com

75008 Paris – France

+33 1 86 69 60 65

Phone: +33(1) 86 69 60 65

+33 1 86 69 60 61 www.fourpointsim.com

+ 33 6 80 18 09 53

Disclaimer: This document does not constitute or form part of an offer to issue or sell, or of a solicitation of an offer to subscribe or buy, any securities nor

does it constitute a financial promotion, investment advice or an inducement to participate in any product, offering or investment. The expectations

expressed about the stocks, the market, the economy and other factors represent the opinion of the FOURPOINTS IM and may not be realised in the future.

Performance is presented for a specific period. Performance may be different in the future. Performance for an index is presented. The fund is not

managed to track the benchmark and will likely differ in terms of industry weights, market capitalisation weights and in terms of number of securities held.

Therefore performance for the fund will likely differ from performance of the index in any particular period.

Le contenu du document ne constitue ni une recommandation, ni une offre d'achat, ni une proposition de vente, ni une incitation à

l'investissement. Il ne constitue en aucun cas un élément contractuel. Reproduction interdite. 24

Les performances passées ne sont pas un indicateur fiable des performances futures.You can also read