Investor Update April 2021 - Kāinga Ora

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor Update

April 2021

1

CONTENTS

SECTION 01

SECTION 02

Construction

Overview and urban

development

SECTION 03

Financing and

financials

2

SECTION 01

Overview

Photo: Weymouth Road, Manurewa,

Auckland

3

New Zealand’s largest residential landlord and developer

We own or manage

189,000+ 5,180

People live in our houses Families placed into homes 66,253

Which is 4% of New Zealand’s 5.0m population

last financial year Properties

Over 98%

Occupancy rate

Value of group assets

$30.8 billion

4

COVID-19: heading in, and the recovery COVID-19 - lessons learned

• Stable and secure rents and income - over 90% of

income directly or indirectly from the Crown Customer welfare

• $871 million of cash and financial assets available to the Improvements to

business - as at 31 March 2021 customer

programme on

• Construction work quickly recommenced - following one welfare calls and

month of a stringent national lockdown in April 2020 check ins

Supporting the

• Tenant debt largely unchanged - lower risk given most sector

tenants receive a benefit ($9 million of $1,465 million

total annual revenue) Immediate

payment terms for

• Continue to work closely with our stakeholders - making all build partners

sure contingencies are in place should infections escalate and suppliers as

• Supporting the sector as a key economic driver - more BAU

than 100 build partners and contractors supporting the

national recovery from the impacts of COVID-19

5

Kāinga Ora – established October 2019

The creation of Kāinga Ora brings a more cohesive, joined-up approach to supporting the Government’s priorities

for housing and urban development.

Kāinga Ora supports people across New Zealand to have good quality, affordable homes, and live in strong,

healthy communities.

Two key roles

Being a world-class public housing landlord Partnering to lead and facilitate urban

development projects of all sizes

6

Kāinga Ora

On 1 October 2019 the people, capabilities and resources of Housing New Zealand Corporation, KiwiBuild and

HLC (a subsidiary of Housing New Zealand) came together as Kāinga Ora – Homes and Communities.

Past Present

Crown Crown

(controlling entity) (controlling entity)

Housing New Zealand Corporation Kāinga Ora (incorporating HNZC, HLC and KiwiBuild)

KiwiBuild

Housing Housing (A department of the

HLC (2017) Ministry of Housing Housing New Zealand Housing New Zealand

New Zealand New Zealand

Ltd and Urban Limited Build Ltd

Limited Build Ltd Development -

Planning)

7

Our outcomes

• Public housing customers - Our public housing customers live well in their homes with

dignity, stability, and the greatest degree of independence possible

• Māori interest - Partnering with Māori ensures Māori interests are protected and their

needs and aspirations are met and allows Kāinga Ora to fulfil its obligations in respect of Te

Tiriti o Waitangi

• Housing access - We provide good quality, affordable housing choices that meet diverse

needs

• Communities - We create sustainable, inclusive and thriving communities: supporting

good access to jobs, amenities and services

• Environment - Environmental wellbeing is enhanced and preserved for future

generations

• System transformation - System transformation is catalysed and delivered

8

Overview of funding and financing

Ministry of Social Minister of Housing

Development Minister of Finance

Budget

appropriations

Governance NZD $500 million

Independent Crown loans

Board

Housing NZ Build Ltd.

~68% of rent (income-related rent subsidy)

~22% of rent (benefits, pensions, deducted at source) NZD $1,500 million

~10% (other income) Bonds, Commercial Paper

Tenant Capital

Markets

Source: Moody’s Investors Service

9

Sustainability Financing Framework includes focus on Wellbeing

C

B Wellbeing

UN Sustainable

Development Human capital

Goals

A B • Social connections

• Knowledge and skills

NZ Living • Time use

Standards

Framework Social capital

A • Cultural identity

• Civic engagement and

ICMA principles governance

and guidelines • Jobs and earnings

Financial/Physical capital

C • Housing

• Income and

Kāinga Ora consumption

• Subjective wellbeing

Sustainability

Financing Natural capital

Framework

• Environment

• Health

• Safety

10Impact attributed to Wellbeing Bonds

In FY20 we raised $2,321 million, allocated as follows: Eligible projects ICMA

(Social / Green)

• Social housing for people in the greatest need

• Retrofit existing social housing

• Modifications / accessibility

• Transitional housing

Natural

capital

• Green buildings minimum 6 homestar rating

• Reduction in waste from construction

activities

• Reduced rate of Financial

embodied emissions

and Physical

capital

• Supporting top 5% of most at risk tenants

with high and complex needs

*programme start 1-Jul-19

11Credit ratings of Kāinga Ora and HNZL equalized with New Zealand Sovereign

Agency Domestic currency Foreign currency Last updated

Aaa (stable) Aaa (stable) 04 February 2021

AAA (stable) AA+ (stable) 22 February 2021

Note, there is no explicit government guarantee

“Because of its public policy mandate, Kāinga Ora's “We believe HNZL will continue business as usual as a core

and HNZL's key role in the New Zealand social subsidiary of Kāinga Ora. We also believe there is an

housing sector and government oversight, there almost certain likelihood the New Zealand government

is no meaningful distinction between Kāinga Ora, would provide it with extraordinary support in a stress

HNZL and the Crown from a credit perspective.” scenario, if needed.”

Moody’s, February 2021 S&P Global Ratings, February 2021

12SECTION 02

Construction and

urban development

Photo: 135 Britomart Street, Berhampore,

Wellington

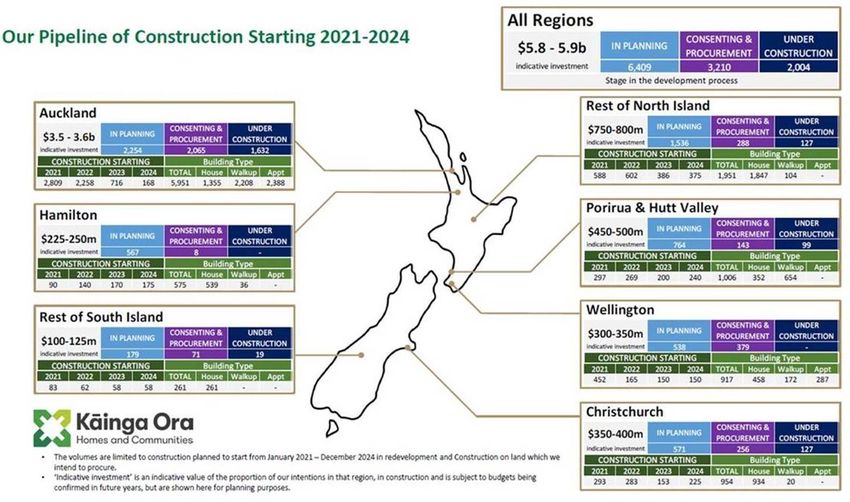

13Build programme overview

• The Government announced plans to deliver an

additional 8,000 new homes as part of May 2020 Budget, Forecast build programmes

made up of 6,000 state houses and 2,000 transitional

houses

• The 2,000 transitional houses are targeted for delivery

over the next two years, with the 6,000 new state houses

targeted in the following two years

• Kāinga Ora will be responsible for around 70% of these

new houses

• The Government announced in March 2021, Kāinga Ora’s

borrowing would increase by $2 billion to enable land

acquisitions (over 10-year period)

• We plan to update the market on our financing

requirements around the time of the Government Budget

(20 May 2021)

• The Borrowing Protocol limit is expected to increase to

accommodate the additional build

14Build programme and capital expenditure has increased in recent years

Newly constructed public and supported homes Gross capital expenditure

• Around 600 homes moved from 2020 to 2021 year • Significant pre-financing for 2021 has already occurred

as a result of disruptions from COVID-19

15The largest build programme in decades has three key drivers

Growth in our public housing Requirement for more affordable Significant renewal and

register housing realignment requirement

• Public housing register has quadrupled • New Zealand housing is among the • Average age of houses is around

in the past four years most unaffordable in the world 45 years – many are cold and damp

• Majority of growth in Priority A • House price to incomes remain very • Over 45,000 homes are due for

category (most at risk) high, particularly in Auckland renewal in the next 20 years

Source: Kāinga Ora Source: Interest.co.nz Source: Kāinga Ora

16Using scale and innovation to deliver new housing at lower cost

Leveraging the build programme to lower costs

• Scaled-up procurement practices

• Supplier panels

• Standardised designs to speed up consent

process

• Multi-year Construction Partnering Agreements

– providing certainty to innovate and scale up

Innovation and new construction methods

• Offsite manufacturing

• Use of cross-laminated timber

• All new builds now have minimum 6 Homestar

certification (except apartments), apartments

from 1 January 2021

• Bathroom pods with accessibility modifications

• New Building Consent Authority: Consentium

17Urban development

Leading the largest urban

regeneration ever undertaken in

New Zealand, by creating

sustainable, inclusive and thriving

communities that will transform

suburbs by:

Evaluating new land

opportunities to

Reviewing existing deliver large scale

concentrated projects

landholdings for

opportunities

Working in

partnership with

others (Councils,

private developers,

Iwi) to enable quality

urban development

18SECTION 03

Financing

and

financials

Photo: Universal Drive, Henderson,

Auckland

19Our debt programmes

Bonds Bills

Notes offered are: • $1.5 billion programme limit

• Unsecured & unsubordinated • Regular fortnightly tenders of $25 million

• Repo-eligible with the RBNZ (3-month paper)

• Approved Issuer Levy paid by HNZL • Private placements as required

20New debt sourced from the market, legacy Crown loans rolled over

Crown loans

• Legacy loans of around $2.0 billion HNZL bonds on issue

• Annual appropriation allows for refinancing

Market debt

• $7.1 billon of debt can be sourced from the

market under Kāinga Ora’s Borrowing

Protocol – expected to increase over time

• Annual programme around $2.0 billion,

subject to Government decisions

• Total market debt on issue $4.65 billion:

$4,200 million nominal bonds

$300 million inflation-indexed bonds

$150 million bills

21Market conditions

HNZL yield to maturity HNZL spread to NZGB (interpolated)

HNZL Yield to Maturity HNZL spread to NZG

4.00 1.20

2023 2025 2026 2023 2025 2026

2028 2030 2035 2028 2030 2035

3.50

1.00

3.00

0.80

2.50

2.00 0.60

1.50

0.40

1.00

0.20

0.50

0.00 0.00

22Bond tender programme

Overview FY2020/21

• Monthly bond tender operated through Bond tender schedule to 30 June 2021

the Yieldbroker Auction System, to

Announcement Tender Settlement Volume Coverage

complement the use of syndicated issues

30-Nov-20 02-Dec-20 07-Dec-20 100 4.3 x

• Expected to account for around half of

annual issuance on an ongoing basis 18-Jan-21 20-Jan-21 26-Jan-21 100 4.9 x

15-Feb-21 17-Feb-21 22-Feb-21 100 3.0 x

• Volumes up to aggregate $100 million

per tender 29-Mar-21 31-Mar-21 07-Apr-21 100 3.0 x

• Up to three bonds offered, existing 23-Apr-21 28-Apr-21 03-May-21 100

maturities only 17-May-21 19-May-21 24-May-21 100

• No reallocations across maturities if 21-Jun-21 23-Jun-21 28-Jun-21 100

undersubscribed

Tender announcement and results published via Bloomberg landing page

23Diversifying our investor base

• Primary issues supported by both Bank and Fund • Offshore (non-resident) holdings on average

Manager accounts represent ~10% of total bonds outstanding

• Non-bank holdings from 34% (2019) to 54% • Noticeable offshore investor enquiry

Bank / Non-bank holdings of HNZL bonds Domestic / Offshore holdings of HNZL bonds

24Demonstrating strong ability to service financing requirements

90% of

revenue

from Crown

2020 2019 2020 2019

$m % Total $m % Total $m % Total

Repairs and maintenance 359 24% 366 27% Rental revenue - income-related rent

Depreciation and amortisation 301 20% 287 21% subsidy (IRRS) 959 59% 880 61%

Rental revenue - tenants receiving

Personnel 176 12% 152 11%

IRRS 386 24% 368 25%

Rates 171 11% 160 12%

Crown appropriation revenue 103 6% 102 7%

Interest expenses 135 9% 106 8%

Other 166 11% 101 7%

Grants 78 5% 84 6%

Total 1,614 100% 1,451 100%

Third-party rental leases 67 4% 64 5%

Other expenses 206 14% 133 10%

Total 1,493 100% 1,352 100%

25Strong, stable and consistent financial performance

Year ended (NZ$m) Jun-20 Jun-19 Jun-18 As at (NZ$m) Jun-20 Jun-19 Jun-18

Revenue 1,614 1,464 1,338 Total assets 32,934 28,996 27,490

Expenses 1,078 973 854 Total liabilities 8,964 6,072 5,171

Total equity 23,970 22,924 22,319

EBITDA 536 491 484

Total debt 6,439 3,536 2,653

Depreciation and amortisation 301 287 259

EBIT 235 204 225

Net Interest expense 114 92 72

Tax 32 (24) 49

Gains/(losses) (147) (76) (28) As at (NZ$m) Jun-20 Jun-19 Jun-18

Net profit after tax (58) 60 76 Liabilities / Assets 27.2% 20.9% 18.8%

Debt / Assets 19.6% 12.2% 9.7%

Debt / EBITDA 12.0 7.2 5.5

EBITDA / net interest expense 4.7 5.3 6.7

Year ended (NZ$m) Jun-20 Jun-19 Jun-18

Operating cash flow 184 294 360

Investing cash flow (2,968) (1,404) (590) Retain strong

Financing cash flow 2,909 883 697 standalone

credit metrics

on gearing &

serviceability

26Strong and stable credit

Largest Critical Domestic currency credit ratings

residential property owner

and developer in New

To the delivery of Government’s

urban development

AAA / Aaa

Zealand programmes

90% of income received

from the Crown

Conservative

Treasury policies

27Investor relations Direct contacts

News, credit ratings, borrowing programmes,

Matthew Needham

Sustainability Financing Framework, and more Chief Financial Officer

Matthew.Needham@kaingaora.govt.nz

https://kaingaora.govt.nz/investor-centre

Jason Bligh

Treasurer (Acting)

Jason.Bligh@kaingaora.govt.nz

Nicki Reeves

Liquidity and Investor Relations Manager

Nicki.Reeves@kaingaora.govt.nz

28QUESTIONS AND ANSWERS

Photo: Frankmoore Avenue, Johnsonville, Wellington

29DISCLAIMER

This presentation has been prepared by Housing New forward-looking statements and they should not be its contents or otherwise arising in connection with the

Zealand Limited (HNZL). This presentation does not regarded as a representation or warranty by HNZL, the offer of Securities; (b) authorised or caused the issue of,

constitute or form part of, and should not be construed directors of HNZL or any other person that those forward- or made any statement in, any part of this presentation;

as, an offer to sell or issue or the solicitation of an offer to looking statements will be achieved or that the and (c) make any representation, recommendation or

buy or acquire any securities (Securities) of HNZL or any assumptions underlying the forwarding-looking warranty, express or implied regarding the origin, validity,

of its subsidiaries or affiliates in any jurisdiction or an statements will in fact be correct. It is likely that actual accuracy, adequacy, reasonableness or completeness of,

inducement to enter into investment activity. results will vary from those contemplated by these or any errors or omissions in, any information, statement

forward-looking statements and such variations may be or opinion contained in this presentation and accept no

The information in this presentation is in summary form

material. liability (except to the extent such liability is found by a

and must be considered in conjunction with and subject

court to arise under the Financial Markets Conduct Act

to publicly available information of HNZL. It is of a general The information in this document is given in good faith

2013 or cannot be disclaimed as a matter of law).

nature and does not constitute financial product advice, and has been obtained from sources believed to be

investment advice or any recommendation by HNZL or reliable and accurate at the date of preparation, but its A credit rating is not a recommendation to buy, sell or

any other person to subscribe for, or purchase, any accuracy, correctness and completeness cannot be hold any Securities and may be subject to suspension,

Securities. Nothing in this presentation constitutes legal, guaranteed. HNZL makes no representation or warranty change or withdrawal at any time by the assigning rating

financial, tax or other advice. as to the accuracy or completeness of the information in agency.

this presentation and does not undertake to update it.

The information in this presentation does not take into By attending this presentation or otherwise accessing this

account the particular investment objectives, financial HNZL has not prepared or registered an investment document, you agree to be bound by the terms and

situation, taxation position or needs of any person. You statement, prospectus, product disclosure statement or restrictions set out above.

should not rely on this presentation in relation to any other regulated offer document in relation to any offer of

No person may offer or sell Securities, or distribute or

investment assessment. You should conduct your own Securities. No action has been taken or is proposed to be

publish any offering material or advertisement in relation

research on HNZL and analysis of its financial condition, taken by HNZL to register any Securities under the laws

to any offer of Securities, to any person in New Zealand

assets and liabilities, financial position and performance, of any jurisdiction (including New Zealand) for which such

other than to wholesale investors within the meaning of

profits and losses, prospects and business affairs of registration is required or otherwise to enable the

clause 3(2)(a), (c) or (d) of Schedule 1 to the Financial

HNZL, and the contents of this presentation. Securities to be offered to the public or under a regulated

Markets Conduct Act 2013.

offer. This presentation may not be distributed or

This presentation contains certain forward-looking

published in or from any jurisdiction except under

statements with respect to HNZL. All of these forward-

circumstances that will result in compliance with all

looking statements are based on estimates, projections

applicable laws of any such jurisdiction.

and assumptions made by HNZL about circumstances

and events that have not yet occurred. Although HNZL No Arranger or Lead Manager for any offer of Securities

believes these estimates, projections and assumptions to nor any of their respective directors, officers, employees

be reasonable, they are inherently uncertain. Therefore, and agents: (a) accept any responsibility or liability

reliance should not be placed upon these estimates or whatsoever for any loss arising from this presentation or

30You can also read