INQUIRY INTO FOOD PRICING AND FOOD SECURITY IN REMOTE INDIGENOUS COMMUNITIES

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

This submission has been prepared on behalf

of the Board of Directors of The Arnhem Land

Progress Aboriginal Corporation and in

consultation with ALPA’s directors, staff, &

cultural leadership from the Yolŋu

communities in which we deliver services.

INQUIRY INTO FOOD PRICING

Rev. Doc. Djiniyini Gondarra, OAM

Chairman

AND FOOD SECURITY IN

Alastair King, OAM FAICD

REMOTE INDIGENOUS Chief Executive Officer

COMMUNITIES

Table of Contents

Who We Are ............................................................................................................................................ 1

Introduction ............................................................................................................................................ 3

ALPA respectfully provides the following recommendations to the inquiry Committee: ............................. 3

Response to Terms of Reference .............................................................................................................. 4

1. The environment in which remote community retailers operate ........................................................ 4

2. The licensing and regulation requirements and administration of remote community stores ............ 15

3. The governance arrangements for remote community stores .......................................................... 19

4. Comparative pricing in other non-Indigenous remote communities and regional centres ................. 20

5. Barriers facing residents in remote communities from having reliable access to affordable fresh and

healthy food, groceries and other essential supplies ........................................................................ 21

6. The availability and demand for locally produced food in remote communities ................................ 28

7. The role of Australia's food and grocery manufacturers and suppliers in ensuring adequate supply to

remote communities ...................................................................................................................... 30

8. The effectiveness of federal, state and territory consumer protection laws and regulators ............... 32

Concluding Statement ............................................................................................................................ 33

Image: ALPA Board of Directors

1|Page

Who We Are

The Arnhem Land Progress Aboriginal Corporation (ALPA) was formed in 1972 as a collective of seven

community-controlled stores. ALPA’s initial member communities were Ajurumu, Gapuwiyak, Galiwin’ku,

Milingimbi, Minjilang, Ramingining and Yirrkala. Since that time ALPA has been financially independent, owned

by our Yolŋu members and governed by a Yolŋu Board of Directors.

In the 1970s the ALPA board recognised the importance of accredited training and development for its team,

and with support from the Queensland Retail Training Institute began a program of in-house training. The

training school at Galiwin’ku was built to support this. During this period we also started our benevolent

programs, using the modest surplus funds generated from store operations to benefit the community.

Financial assistance for ceremonies, nutrition, education, medical escorts and community events could be

obtained through these programs.

ALPA became a Registered Training Organisation in 1992 and remains committed to team training. Over 1500

of our remote Indigenous team members have completed apprenticeships or qualifications through ALPA. This

dedication to quality training outcomes saw ALPA recognised as the NT Large Employer of the Year at the NT

Training Awards in both 2015 and 2016 and placing in the top three at the subsequent National Awards in the

same category in both years.

Since 2002, the organisation has expanded through its Retail Consultancy service, running client stores on

behalf of, and in partnership with, other Indigenous community organisations. This model has given those

communities access to ALPA’s systems, processes, financial management, training, nutrition program and

group purchasing. This partnership approach allows these communities to maintain ownership and control of

their business but with the expertise and support of an experienced Indigenous business partner.

In 2013 the ALPA Board of Directors made the decision that it was time for ALPA to diversify from retail and

work with the government and industry partners to increase the economic opportunities for our Yolŋu

members. Our board quickly recognised the ability to support positive change in our communities through

these programs and over the last five years our community services footprint has grown to four CDP regions,

five RSAS teams, business incubators and a self-funded Youth Development program and Community

Engagement Team.

By 2014 our employment services team had filled all of the existing local jobs so ALPA started working in

partnership with local families and traditional landowners to develop new enterprises, create further

employment pathways and to strengthen the economies of our member communities. To date this has seen

the creation of four new Indigenous-owned businesses, delivering services across a variety of sectors including

construction, landscaping, furniture manufacturing, automotive repair, homelands services, hospitality,

tourism, agriculture and cleaning.

In 2020 ALPA operates in 27 remote communities across a 1.2 million km2 footprint. ALPA has over 1000

employees, more than 80% of whom are local Indigenous people, and last financial year the ALPA group

returned over $35 million to our member communities in the form of wages for local Indigenous team

members, community governed benevolent programs, community sponsorships and capital upgrades. A video

sharing the full ALPA story can be found here.

2|Page

Introduction

ALPA welcomes the inquiry into pricing and food security in remote Indigenous communities and we are

grateful for the opportunity to contribute to this important conversation.

Throughout our submission we will seek to describe the remote retail environment and the pricing model for

remote community stores, explain the importance of viable community stores and identify other factors which

impact on food security.

We would welcome the opportunity to address any questions arising from our submission directly with the

Committee through the hearing process and would gladly facilitate visits to our stores to ensure Committee

members are provided the opportunity to experience firsthand the remote retail environment.

We have built a strong business over 50 years, we are successful in our environment and we are the experts,

we have become Australia’s largest Indigenous corporation. We created our own subsidies to make prices

cheaper on healthy food, we don’t get any Government subsidies. We can’t just keep dropping prices, we will

lose half of our Yolngu employment and that isn’t ALPA. If prices are going to come down any further

government need to do consultation and work with us as a partner.

- Mickey Wunungmurra, ALPA Deputy Chairman

ALPA respectfully provides the following recommendations to the inquiry Committee:

1. We recommend an intersectoral taskforce be formed to identify and implement solutions to reduce

costs to the consumer. Improving food affordability in remote communities is a joint responsibility of

the Commonwealth, state and territory governments, in partnership with manufacturers, wholesalers,

major retailers, remote retailers, freight companies, Indigenous organisations and Indigenous

leadership. All of these stakeholders need representation on the working party.

2. We recommend a freight subsidy on essential lines be considered for wet-season affected stores and

barge-dependent stores who experience higher freight costs. Monitoring and controls are required to

ensure subsidies are passed on to customers.

3. We recommend governments prioritise remote road and barge landing maintenance, particularly

after the wet season, to reduce remote store operational costs, and improve safety and food security.

4. We recommend the development of a national price monitoring tool, that is validated, accurate and

prices the most affordable options available. This process should remain anonymous to allow

increased participation. KPIs should be set across each jurisdiction to track government action to

improve food affordability.

5. We recommend a national funding program be available to remote stores to support improvements

to infrastructure and equipment. This will reduce store operational costs and increase access to quality

goods. The application process should be simplified to allow all stores to apply and should not be

biased towards government-owned operations.

3|Page

6. We recommend the consideration of a national licensing or benchmarking scheme, and/or the

utilisation of lease agreements, to improve food security across all states and territories. The

developed process needs to:

• Learn from the existing NIAA NT Community Stores Licensing Scheme;

• In consultation with community leaders, include strategies from Healthy Stores 2020 to ensure all

stores implement health-enabling retail environments;

• Be adequately resourced to support monitoring visits across all stores in a timely manner;

• Be independently and consistently evaluated to determine its impact on remote food security.

7. We recommend governments invest in increasing the remote nutrition workforce, with priority given

to public health positions that focus on supporting improvements to the remote food supply. Funding

should also be dedicated to the development of targeted training and tools to support this workforce

to achieve population health gains.

8. We recommend governments prioritise investment in job-creating strategies to address the critical

underemployment levels within remote communities.

9. We recommend governments prioritise investment in remote housing construction, repairs and

maintenance. This work should be carried out by local Indigenous business so they can be undertaken

in a quick and cost-effective manner.

10. We recommend consideration be given to an inquiry investigating the impact that major retailers’

market power has on consumer groups in remote and regional areas.

Response to Terms of Reference

1. The environment in which remote community retailers operate

The environment in which ALPA operates remote stores has largely unchanged since the 2009 Parliamentary

Inquiry Everybody’s Business: Remote Aboriginal and Torres Strait Community Stores. But ALPA as a business

has changed greatly. While we continue to operate quality, community-owned, Indigenous-led and financially

independent stores in some of the most remote locations in Australia, we have diversified, increasing our

focus on delivering quality services and creating jobs for local Indigenous people through our Community

Services and Enterprise divisions. This diversity has strengthened the ALPA model. Our stores, like most

remote stores, are much more than a shop.

Our mission remains focused on operating successful and responsible businesses, emphasising local

employment, training, career pathways, customer service and safety. We strive to improve the health, quality

of life, and economic development of our members, giving primacy to their cultural heritage, dignity, and

desire for opportunity and equality with their fellow Australians.

Since 2009, our remote retail footprint has expanded, delivering ALPA’s successful retail model to 27 remote

retail businesses across the Northern Territory and Far North Queensland. We own seven stores in our

member communities, Galiwinku, Gapuwiyak, Milingimbi, Minjilang and Ramingining. In 2014 we acquired the

4|Page

Island & Cape retail business operating under ‘Island & Cape Retail Enterprises Trust’. This business

compromises of six stores across Cape York and the Torres Strait Islands. Additionally, we manage 12 stores

owned by other community organisations or councils – our client stores. Many of these businesses are long-

term clients, happy to be part of a successful group which supports long term financial viability. As a retail

group, we operate viable social enterprises with an emphasis on local employment, training and nutrition.

Surpluses are reinvested back into each store to improve retail services and activities that benefit the

community.

The foundation of ALPA was to ensure reliable access to food and essential goods as a basic human right. ALPA

has done this for almost 50 years with little or no government funding. We are acutely aware of the significant

role we play to support food security in the communities we service. Under the leadership of the ALPA Board

of Directors, our team strives to improve access to sufficient, safe and nutritious foods. Improving affordability,

whist maintaining financial viability, continues to be a key focus for our team.

Images: Fresh produce and takeaway in an ALPA store

Throughout our history, we have implemented many strategies to bring prices down. The following paragraphs

will explain the steps we have taken, and the challenges we continue to face to remove the price disparity that

exist for remote community residents. This story is not new. It has been well documented in government

inquiries, research journals, news articles and personal stories.

Our size is our strength in the remote retail environment. In comparison to independently- or privately-run

remote stores, we turnover a larger volume of stock. Stock volume drives better pricing, rebates, promotional

deals and service levels from suppliers. All these factors improve customer access and affordability. In the

broader Australian retail sector, our business is equivalent to two Coles or Woolworths supermarkets. We are

a very small fish in a big ocean. We do not have the buying power, market concentration and bargaining of the

supermarket giants. We cannot buy products from suppliers at the same cost as Coles and Woolworths, nor

do we benefit from the supplier marketing or resource support that large national supermarkets receive. And,

consequently, we cannot sell products at the same price without impacting the store viability, and ultimately

impacting the food security of a remote community. This unfair market power supermarkets possess has been

documented on a number of occasions, including the 2011 inquiry in the impacts of supermarket price

decisions on the dairy industry:1

1

Parliament of Australia. (2011) The impacts of supermarket price decisions on the dairy industry.

https://www.aph.gov.au/Parliamentary_Business/Committees/Senate/Economics/Completed%20inquiries/2010-

13/dairyindustrysupermarket2011/report/c07

5|Page

Many submissions and witnesses criticised the market share and market power held by Coles and

Woolworths. The two major supermarket chains are able to access products on more favorable terms

and conditions, including at lower prices, than other businesses such as smaller retailers and milk

vendors.

Generally speaking, larger customers will be supplied on more favourable terms (i.e. more generous

rebates and discounts). For example, in its public submission Fonterra stated that it achieves lower unit

costs, predominantly linked to volume, when selling to large customers. Fonterra states that additional

benefits in dealing with larger customers include consistent purchasing patterns which enable

manufacturing efficiencies. Fonterra stated that if a smaller wholesaler or retailer was to purchase the

same volume as a larger customer, in general, they may be able to achieve similar discounts from

Fonterra to the larger customer.

The above references paint the picture of remote stores’ buying power compared to the large supermarket

chains. To change this picture for remote residents we need intersectoral support, from government,

manufacturers and wholesalers. COVID-19 opened this door with the establishment of the National Food

Security Working Group. ALPA were proud members of this group and see benefits for it to continue post the

current pandemic. Governed properly this group has the potential to combine buying power to achieve

improved freight and base cost prices that could be passed on to consumers. In lieu of this, we will continue

to utilise our current methods to address price inequity in remote communities and ensure supply and

sustainability of remote stores.

This solution can’t just be ALPA dropping our prices, the wholesalers need to drop their prices. We need

to survive, we all need to play this game together. The Government needs to work with stores and

wholesalers to get lower prices if this will work in the longer term.

- Mickey Wunungmurra, Deputy Chairman, ALPA

As stated in the 2009 inquiry, ALPA has strong corporate governance. We are reliable and honest traders,

giving suppliers the confidence to engage and partner with ALPA. This means our preferred suppliers are some

of the largest wholesale food distributors in Australia. They deliver a higher level of service and can negotiate

better prices than smaller wholesalers who some smaller remote stores are known to rely on for stock. It is

worthy to note that despite dealing with large suppliers, our suppliers’ warehouses are still based in the

regional cities of Cairns and Darwin, where the cost of maintaining a business is higher than in major cities.

We continue to operate under the ‘preferred supplier’ model. We source ethical suppliers who provide us

with the best quality, best value for money, highest service levels and favourable payment terms. This allows

our store managers to focus on service and team member training, while our merchandise team focus on

sourcing and negotiating supply. Our store managers are still responsible for placing weekly orders, the

corporation simply decides who they buy from thus ensuring the stores group benefits from the best cost price

available. Any improved cost price is directly passed on to the customer. The purpose of this is to prevent

unscrupulous store managers and suppliers colluding for their own benefit, which is known to exist in the

remote setting. We have other processes in place to ensure integrity and honesty across the whole of our

business.

For some commodity groups we have more than one supplier to ensure quality, value and supply. A smaller

number of suppliers allows us to concentrate stock volume to deliver better prices and reduced administration

costs. Our preferred suppliers know we regularly monitor pricing and service levels; if they are becoming

expensive or their services levels drop, we hold them accountable or source a new preferred supplier. During

COVID-19 we have monitored suppliers’ prices and reported any unsubstantiated increases to the ACCC for

6|Page

consideration, one supplier in particular increased the price on a large number of products without an

acceptable reason in our view, we are exiting our relationship with that supplier.

COVID-19 highlighted the strength in our sourcing model. Panic buying in urban centres put pressure on the

Australian food supply chain resulting in empty shelves in towns and cities across Australia. To address this,

the Prime Minister Scott Morrison allowed a relaxation of ACCC rules which allowed major retailers to combine

efforts and cooperate to improve the logistics of supermarket supply, at the expense of smaller retailers.

Manufacturers prioritised stock for them, and supply became more erratic and difficult for everyone else.

Given remote communities rely on one or two stores for the majority of their food, this decision could, and in

some communities did, severely impact food security. The CEOs of ALPA, Outback Stores (OBS) & Community

Enterprises Queensland (CEQ), worked together to secure stock for all remote stores, including independents,

across NT and Qld through advocacy, direct with manufacturers.

Having preferred suppliers was our first line of defense. During COVID-19 suppliers prioritised delivering stock

to businesses whom they had trading terms with. If you were a store without trading terms, you could not get

stock from them – a challenge for smaller operators who’s supply chain was not formalised and less secure.

As stock became unavailable from our primary supplier, our team moved to our second, then tertiary

suppliers. Eventually, we were forced to find stock everywhere and anywhere, but we were fortunate to have

a merchandise team who could dedicate the time to ensure our supply was maintained. Without our

merchandise resource, which is funded by supplier rebates, all of our stores would have had a significant

disruption to their service levels and would have no doubt encountered cost price rises and product quality

compromises. Moving outside of our preferred suppliers meant we were buying the same products at a higher

price. ALPA decided that where the cost price increased, we would consider the impact to customers’ food

security, and nutrition, and if required we were prepared to absorb this within our own operating margins.

Customers may have noticed that their first choice and preferred brand may not have been available but an

alternative was. This was because manufacturers prioritised the production of Coles and Woolworths high

volume product lines. Our product mix differs greatly, therefore, some of our highest volume lines were not

being produced, impacting affordability with the absence of generic, non-branded products and smaller pack

sizes (e.g. no 1kg rice) in the food supply chain. In some instances we could not stock smaller pack sizes and

cheaper generic-branded product through this period, meaning customers would outlay more money for

larger pack sizes or premium options they would not usually have bought. This was somewhat compensated

by the Government stimulus packages which supported people in remote communities. COVID-19 illustrated

where remote stores sit in the Australian food supply chain – at the end. The National Food Security working

party helped highlight the vulnerabilities of the remote food supply to government and food supply decision

markers.

The next factor in the price gap story is freight. Freight costs are a known contributor to increased food prices

in remote communities.2 Freight costs differ between our stores, based on distance, transport modality (road,

sea, air), volume being transported and product type (dry, chilled, frozen). We have leveraged our volume to

negotiate better freight costs with contracted freight companies. Within our transport contracts, we manage

varying fuel costs and facilitate pallet exchanges which bring our freight costs down. We set KPIs to hold our

transport partners accountable, ensuring stock is delivered within allocated timeframes and in good, safe

condition. We have systems in place to ensure our stores are charged the correct freight per delivery. These

invoicing errors can be a significant expense to stores if they are not identified, but it requires resources to

identify and challenge potential mistakes, which adds additional operating costs.

2House of Representatives Aboriginal and Torres Strait Islander Affairs Committee. (2009) Everybody’s Business Remote Aboriginal and Torres Strait

Community Stores. https://www.aph.gov.au/binaries/house/committee/atsia/communitystores/report/everybody's%20business%20report.pdf

7|Page

As is the case with supply, our size is insignificant to that of the major retailers. Volume drives freight costs as

well. The major supermarkets chains can negotiate cheaper freight rates and, given their size, have been able

to move towards a national freight model – meaning their city supermarkets bear the increased freight costs

of their rural and remote supermarkets. We cannot implement such a model due to our business structure

and business size. Additionally, some manufacturers pay the freight to supermarket distribution centres,

reducing costs, or supermarkets recover freight costs through larger rebates.3

There are a limited number of transport companies delivering to remote communities which means reduced

competition. We do our due diligence to partner with companies who deliver a high level of service – delivering

on time and maintaining quality. We are reimbursed for damaged stock as part of our contract. In some

locations, cheaper transport companies exist, but service is compromised. Smaller transport companies

require adequate volume to warrant a delivery, the delivery is not undertaken until that volume is reached,

reducing delivery frequency. We utilise larger transport companies who have adequate resources to maintain

their fleet, avoiding delivery delays due to breakdowns. These two factors reduce the access and availability

of goods to remote communities. Our stock delivery rate for FY2020 was 98%, with missed deliveries mainly

due to weather events. In those situations, if essential stock levels were critical, stock was flown out – a higher

cost to that store. Often our freight passes over very challenging road conditions, this results in higher repair

and preventative maintenance costs for our freight providers.

Four of the stores we operate are cut off from road transport during the wet season, some for up to 6 months.

While the store is cut off, perishable stock must be flown in at that store’s expense. There are no government

subsidies. Due to the expense, only a small amount of perishable stock is flown in. For one store, it costs

$2000/week to fly 3 planes transporting 600kg worth of perishable goods across a 20 min return journey.

Charter plane operators are used to transport the food. These planes are not built for purpose, so ensuring

the cold chain remains intact is a challenge and can restrict what is flown over. This is in comparison to

transport in the dry season, which costs the store approximately $3000 to transport 20 000kg worth of stock.

The wet season tonnage restriction means affected stores must have sufficient funds to pay for infrastructure

to hold large volumes of stock, and sufficient funds and/or long-term payment terms with suppliers to

purchase large volumes of dry and frozen stock to see them through the cut-off period. It requires experienced

management and merchandise support to get the stock holding right – predicting the weather is impossible.

At times, the stock has run out, leading to increased transport costs to fly dry stock in. Securing this stock and

tailoring payment terms with suppliers is yet another task our merchandising team perform on behalf of our

client stores. Rebate funding is essential to pay for this merchandise support.

Transitioning in and out of wet seasons requires a coordinated effort from our team, our suppliers, transport

companies and the government department managing roads. To reduce freight costs, we aim to switch back

to road transport as quick a possible when the weather is favourable. We have experienced unnecessary

delays in opening roads post wet, due to untrained people making road assessments, and slow movement to

fix the road. Each week this adds a significant cost to the store, and consequently to the customers.

Where possible we will send freight by road as opposed to barge to reduce freight costs. Freight for barge

stores is 3-4 times higher than road stores. Barge-dependent stores have the additional financial burden of

purchasing and maintaining trucks and trailers to transport goods from the barge landing to the store. There

are no freight services in communities to facilitate this. In some cases, it takes 90 minutes to travel the 30km

journey on poorly maintained dirt roads. The road conditions increase vehicle maintenance costs and increase

3Woolworths group (2020, January 24). National Distribution Centre Freight Cost Recovery. Partner Hub – Woolworths Group.

https://partnerhub.woolworthsgroup.com.au/s/article/National-Distribution-Centre-Freight-Cost-Recovery

8|Pagerisk of damaged goods. Longer transit times requires a refrigerated truck to maintain the cold chain, which

comes at an additional expense to the store.

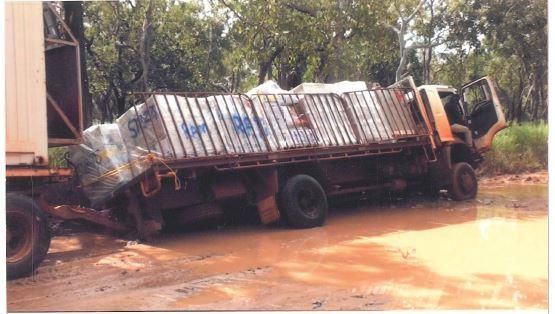

An example of this was in 2011, where the weather conditions were so severe that the communities of

Ramingining and Gapuwiyak were cut off from their barge landings and the airstrips (see images below and

video here). The NT government were forced to bring in half-track vehicles to bring food to the community.

As road conditions have still not improved, we have had to improve storage infrastructure in case of another

similar wet-season event, at considerable cost to our businesses.

Images: Poor road conditions during the wet season in Ramingining, 2011

Due to high freight costs and limited transport options, remote stores are restricted in the delivery frequency.

Where urban supermarkets receive multiple deliveries per day, most of our stores receive one delivery per

week. Store managers must have the experience to order accordingly. If a manager under-orders, the

community would be without that item for weeks. Since the 2009 inquiry we have seen slight improvements

in affordable transport options allowing for increased delivery frequency. At a minimum, all our stores receive

weekly orders. In recent years, we were able to transition two stores from fortnightly to weekly orders, and

we now have four stores who receive two deliveries a week - a rarity in the remote setting. These

improvements increase the quality of foods being sold to customers. Our team work with our suppliers to

sources higher quality produce at the right maturity to hold up throughout the delivery cycle. Most times they

get it right, but if the product arrives unfit for sale the supplier will provide a refund. On many occasions

customers have mentioned our fruit and vegetable quality is comparable to or exceeds the quality sold in

urban supermarkets. Higher quality comes at an increased cost to the customer but is necessary to ensure

availability of products with a reasonable fresh shelf life.

ALPA have implemented a freight subsidy on fresh fruit and vegetables to support consumption. We use two

methods to implement this freight subsidy. In our member stores, based on sales, stores are reimbursed the

proportion of freight for subsidised items, which equated to $250 000 in FY20. Within ALPA, nutrition subsidies

have been in place since the 1980s. Our freight subsidy is completely independent of government funding.

The subsidy now extends to canned and frozen vegetables, and fresh dairy. For client stores, freight is removed

from the price calculation for fresh fruit and vegetables. The cost of the fruit and vegetable freight is spread

across the remainder of the range, particularly targeting less healthy products. Unfortunately, we are unable

to fund a freight subsidy for our Island and Cape stores without impacting the viability of that business. The

previous inquiry acknowledged the high freight costs in the Torres Straits, with Recommendation 23 stating,

the Committee recommended following implementation of supply chain coordination and efficiencies, the

Australian Government consider a freight subsidy for fresh product for the Torres Straits. The Australian

9|PageGovernment currently provides financial assistance for freight to Tasmania, but no such scheme exists for

transport any of the locations of ALPA stores that are only accessible by barge.4

Table 1 outlines how freight as a percentage of total sales, and overall gross profit, has remained stable

between 2008 and 2020. As reported in the 2009 inquiry, our target band for gross profit is between 33-36%,

this target has not changed. We achieve this by controlling shrinkage, good investment buying and having an

appropriate merchandise mix.

Table 1: Breakdown of sales to gross profit FY08 vs FY20 for ALPA stores

FY2008 (n=5 stores) FY2020 (n=7 stores)

% total sales % total sales

Freight 6.79% 6.5%

Purchases 58.83% 61.90%

Total cost of

65.70% 64.95%

goods

Gross profit 34.30% 35.05%

It is essential we meet this target of GP of 33-36% to cover our operational costs, with the remaining surplus

(table 2) used to maintain financial independence, invest in capital works to maintain store standards and

finance our benevolent programs to support members. Our target band for surpluses remains between 8-12%.

Table 2: Store operation surplus FY08 vs FY20 for ALPA stores

FY2008 (n=5 stores) FY2020 (n=7 stores)

% total sales % total sales

Net surplus

9.52% 11.06%

from stores

All service providers in remote communities – emergency services, schools, councils, and the store –

experience higher operational costs compared to the urban setting. Absolutely everything we do costs more:

employment, insurance, governance, power, rent, repairs and maintenance, yet our stores do not receive

support to cover these expenses like other community services. Table 3 depicts a comparison of our

operational expenses in 2007/08 and 2019/20.

4

Department of Infrastructure, Transport, Regional Development and Communications. (2020 June 20). Tasmanian

Freight Equalisation Scheme. https://www.infrastructure.gov.au/maritime/tasmanian-transport-

schemes/tasmanian/

10 | P a g eTable 3: Breakdown of operational costs FY08 vs FY20 for ALPA stores

FY2008 FY2020

(n=5 (n=7

stores) stores)

% total % total Variance Comments

costs costs

Employment Including on-costs & staff

62% 56% -6%

expenses replacement

Phone, internet, IT, audit, board

Operating

16% 16% 0% meetings, accounting, training,

expenses

admin, HR

Depreciation 8% 7% -1%

Repair and Refrigeration R&M, 48% in FY08

5% 4% -2%

maintenance over and 52% in FY20

Power and water 4% 7% 3%

Paid to Traditional Owners through

Landowners rent 4% 7% 3% NLC in NT; shire councils or private

owners holding the ILUA in Qld

Financial EFTPOS fees, bank charges,

2% 1% -1%

Expenses damaged foods

Vehicle costs 1% 2% 1% Excluding trucks and forklifts

Between 2008 and 2020, there was consistency across most expenses – with the biggest variations being a

decrease in employment costs (covered below) and small increases in power and water, and landowners’ rent.

Note that In Queensland our stores pay very high rents, as high as 6% of sales to local shire councils or private

landlords that hold the Indigenous Land Use Agreement (ILUA). CEQ pay ‘peppercorn’ rents as low as $1500

per year in the Torres Strait, and pay nothing in rent for their Cape York Stores. There is no level playing field

for other store operators including our business.

Employment expenses, including payroll tax, recruitment and superannuation contribute the most to our

operating costs. Higher wages are in place to attract experienced managers to remote locations. If we were to

match the wages offered by government-funded stores groups, it would impact price, or cause a reduction in

benevolent activities. CEQ rarely advertise recruitment. Instead they cherry-pick ALPA personnel, offering

them $20k above market salary. We are constantly investing in recruitment, training and development and

then losing personnel to CEQ (at least 15 former ALPA employees), putting upward pressure on our costs.

There were no advertised positions listed on the CEQ website as of 16/7/2020, yet they cold-called one of our

Queensland store managers the previous week and offered an extra $20k salary. We question how this

behaviour aligns with the CoAG expectations of competitive neutrality by government statutory bodies.

As with other community services, housing, power and increased leave entitlements are also provided to

support team member retention. It is worth noting, as reported in the previous inquiry, government-funded

11 | P a g eservice providers also receive higher wages to account for higher cost of living – yet the majority choose to do

their grocery shopping online, except for the freight subsidised items. This means the money provided to them

as a remote living allowance is going back to major supermarkets, and not benefiting remote communities.

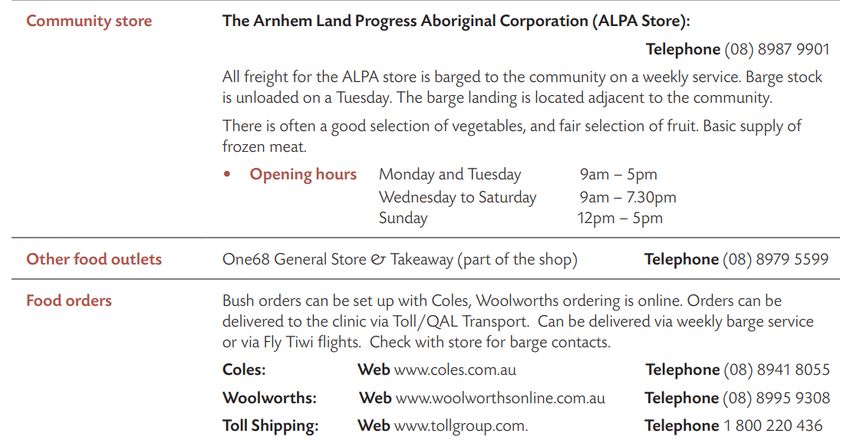

Below is an excerpt from the Remote Area Health Corps (RAHC) profile of Milingimbi, clearly outlining the

process for ordering food from the major retailers instead of the community owned store (and

misrepresenting our food offer which includes minimum 27 varieties of fresh fruit and vegetables and a fresh

meat offer). RAHC is funded by the Australian Government, and provides relief health staff to health centres

across the NT.5

Image: RAHC website with instructions on purchasing from major supermarkets.6

With limited access to trades in remote communities, we fly or drive tradespeople in at a significant expense.

Their labour rates start from the time they arrive at the airport and stop when they return. There are many

instances where one repair requires multiple trips, first to diagnose the problem and order the necessary part,

and second to make the repair. ALPA spends $500k on general repair and maintenance annually. On top of

this we spend $1.6m on average for equipment renewal or store refurbishments. In 2019 we invested over

$2m to double the selling space of our community store in Ramingining; this allowed us to expand our fresh

offer and introduce new ranges. We have a cyclical store refresh program that ensures we take preventative

maintenance action in advance of major problems. We also have scheduled quarterly visits to each store for

IT, refrigeration mechanics and pest control to mitigate costly emergency responses. This all comes at a

significant cost when you consider our locations and transport needs.

The Australian Government has a scheme to support improvements to store infrastructure through the

Aboriginals Benefit Account (ABA) grant funding application process, for NT stores only. ALPA retail

applications have been consistently unsuccessful, so we are forced to self-fund these needs. Some of our

smaller client stores have received grants.

5

Remote Area Health Corps. (2020). Remote Area Health Corps. RAHC.

https://www.rahc.com.au/sites/default/files/profiles/Milingimbi_RAHC%20Community%20Profile_2017.pdf

6

Remote Area Health Corps. (2017). Milingimbi – Arnhem Region. RAHC.

https://www.rahc.com.au/sites/default/files/profiles/Milingimbi_RAHC%20Community%20Profile_2017.pdf

12 | P a g eWith limited buying power, increased freight costs and higher operational costs, it is a balancing act to set

affordable prices whilst maintaining store viability. Both are needed to maintain remote food security. The

ALPA Board of Directors and store board members from the client stores oversee the pricing strategy for their

stores. Any changes to product mark-ups (up or down) require store board approval. Store board members

want to ensure long term viability, financial independence and continued contributions to benevolent

activities. These local decision makers have put pricing strategies in place to support healthy food consumption

to reduce the health disparity experienced by remote community residents. These efforts should be

acknowledged and celebrated, as local decision makers are taking responsibility for a serious issue.

As previously mentioned, all ALPA-operated NT stores self-fund a freight subsidy on fresh, canned and frozen

vegetables, fresh fruit, and fresh dairy – reducing the sell price by up to 20%. Long term price discounts are

applied to bottled water ($1 for 600ml across all our stores), artificially sweetened beverages (up to 20% less

than sugar sweetened equivalent), infant formula (an option to sell at equivalent price to urban supermarkets)

and healthy prepared food lines (sandwiches, salads, healthy snacks, and hot meals containing protein and

vegetables). Some of these long-term strategies are supported by manufacturers, while others are ALPA-led

initiatives. In 2020 we received further support from wholesalers to reduce the cost of our generic non-

branded products. These products are high-volume lines across our store, so this reduction will produce

marked improvements to food affordability. Across our essential lines, we ensure a low (generic) and medium

(branded) cost product are available to the customer. Premium priced products are available on request. We

do acknowledge supermarkets have greater access to generic products and are continuing to develop their in-

house brands. We have investigated supply through Coles and Woolworths, but we were able to achieve

cheaper prices and more consistent supply through Metcash, our main supplier. COVID-19 reinforced this

decision. Other remote stores who access stock from the major retailers, rather than setting up a more

sophisticated retail supply chain, were severely affected by the out of stocks due to panic buying. They were

affected in two ways, firstly major retailers shut-down their online shopping facilities, which is the method

most remote stores use to order stock and secondly, many key product lines were out of stock. Some of these

stores are just starting to receive stock from Coles or Woolworths, two months after the peak panic buying

event.

With branded products, we have negotiated consistent promotions to keep the costs down. These discounts

are provided by the manufacturer and passed down the supply chain to the customer. It is clear manufacturers

can reduce the cost price to remote stores, but they may need more support from the major supermarket

chains, to reduce prices further. In the absence of that, we will continue to look for and implement cost saving

measures and continue to be guided by store board members to implement ongoing price strategies. It is

worth noting that when suppliers increase cost prices; these increases, through an automated process, could

be directly passed to stores. Our merchandise team challenge cost increases to ensure that only those with

genuine reasons are accepted. Without rebates funding our merchandising team, these increases are much

less likely to be investigated.

ALPA have collaborated with researchers to trial several price reduction trials. Shop@RIC applied a 20% price

discount on all fresh and frozen fruit and vegetables (excluding frozen potato products), all bottled water, and

all artificially sweetened soft drinks.7 This discount was on top of existing pricing strategies across 20 remote

stores (including 8 ALPA stores). The value of the price discount was reimbursed to the store associations using

Australian National Health and Medical Research Council research funding – highlighting a potential method

7

Brimblecombe, J., Ferguson, M., Chatfield, M. D., Liberato, S. C., Gunther, A., Ball, K., ... & Leach, A. J. (2017). Effect of

a price discount and consumer education strategy on food and beverage purchases in remote Indigenous Australia: a

stepped-wedge randomised controlled trial. The Lancet Public Health, 2(2), e82-e95.

13 | P a g eto implement government-funded price subsidies. Application of price discount alone, and in combination

with a consumer education strategy increased purchases of fruit and vegetables. Despite this, unhealthy food

purchases increased as well, highlighting the need to implement healthy merchandising strategies alongside

price discounts.

Through Island & Cape, we supported Apunipima Cape York Health Council to conduct the ‘Healthy Choice

Reward Scheme’ in Aurukun, a consumer food subsidy scheme utilising a voucher system.8 Customers were

rewarded with a $10-15 fruit and vegetable voucher based on a spend value. Although the trial did not lead

to increase fruit and vegetable purchasing, it was well received by customers. Learnings from this project could

inform direct to consumer subsidies, which is a key call to action by Apunipima.9 ALPA welcomes facilitating

new food affordability projects, such as the newly NHMRC-funded study, led by University of Queensland and

Apunipima.10 This study will investigate how food price subsidies can improve access to healthier food for

mothers and young children as a priority population. Participants will be provided with discount cards that

unlock lower prices on a range of healthy foods at local stores.

Whilst we implement multiple strategies across food procurement, transport, and sale, our efforts have not

closed the price gap that exists between remote community stores and urban supermarkets. Each year we

voluntarily participate in the Northern Territory Government’s (NTG) Market Basket Survey (MBS). This shows

our commitment to price transparency and food security.

Since the first MBS survey in 2000 a price gap between remote and supermarkets has existed.11 The cost of a

healthy food basket in remote NT stores is, on average, 33% more than supermarkets. Across the survey

history this price difference has ranged from 18-60% between the two settings. In recent years there has been

a notable difference. The first conclusion drawn by many is remote price gouging. But the reality is, this

difference is the result of increased market power of the major supermarket chains. Over this time period the

country has witnessed price wars between the two main competitors “down, down, prices are down”. And,

with the growing presence of the low-cost supermarket chain Aldi, the pricing pressure has increased. Aldi

have grown from one store in 2001 to over 500 stores across Australia. The consequence of this is cheaper

prices for supermarket shoppers, and increased prices for everyone else, with remote customers affected the

most.

While we are not disputing that a price gap exists between urban supermarkets and remote stores, we are not

confident that reported price gaps are accurate. The MBS is full of inaccuracies. The NTG note some limitations

in their reports, but they fail to acknowledge the major limitations – that the process is not validated, surveyors

are not provided adequate or annual training prior to data collection, and consistent mistakes are not

identified or resolved by NT Department of Health. From the 2019 surveys, we identified a total of 102 pricing

mistakes across the 12 surveys completed in ALPA operated stores. These mistakes increased the healthy

basket cost by an average of 5.4%. The range highlights the inconsistencies in data collection, with the healthy

basket being costed 0.6-14.7% higher than it should have been. It is highly likely these errors existed across

the 58 MBS surveys that were collected in 2019. This finding is totally unacceptable given the MBS is a highly

8

Brown, C., Laws, C., Leonard, D., Campbell, S., Merone, L., Hammond, M., ... & Brimblecombe, J. (2019). Healthy

Choice Rewards: a feasibility trial of incentives to influence consumer food choices in a remote Australian Aboriginal

community. International Journal of Environmental Research and Public Health, 16(1), 112.

9

Apunipima Cape York Health Council. (2017). Position statement – Food security for Cape York. Apunipima.

apunipima.org.au/images/Nutrition_Resources/Apunipima%20Food%20Security%20Position%20Statement.pdf

10

University of Queensland. (2020 January 08). Study to fight food insecurity in Indigenous communities. UQ News.

https://www.uq.edu.au/news/article/2020/01/study-fight-food-insecurity-indigenous-communities

11

Department of Health Strategy Policy and Planning. (2020 July 03). 2019 NT Market Basket Survey (19). Northern

Territory Government. https://hdl.handle.net/10137/8469

14 | P a g ereferenced document and could be used for strategic policy development. We call for a national price

monitoring tool, that is validated, accurate, and remains anonymous to allow increased participation. KPIs

should be set across each jurisdiction to lower the price discrepancy between the urban and remote settings.

At present, relatively no action is taken by NTG when the MBS results are released. Finally, the cheapest

available products should be surveyed to work out the cheapest cost of a healthy basket in all settings. At

present, generic products are excluded from the pricing section of the MBS. This exclusion inflates the

reported portion of household income being spent on food.

As previously mentioned, given the market power held by Coles and Woolworths, expecting comparable

pricing in the remote setting in the current environment is unrealistic. It is fairer to compare remote

community stores to urban corner stores, who possess similar buying powers. Remote community stores are,

on average, 9% more expensive than urban corner stores, with the percent difference ranging from 1-22%

over the MBS history. In the latest survey, the cost of a healthy food basket was 6% more in remote stores

when compared to urban corner stores. Based on these results and the limitations of the MBS, once freight

and operating expenses are considered, remote stores are doing a pretty good job. Despite this, we

acknowledge urban residents have the choice to shop at a cheaper supermarket while remote residents

cannot access this option easily. We will reiterate the need for action across all sectors and governments to

address the structural and systemic problems that have resulted in poor food security for many remote

Indigenous communities.

2. The licensing and regulation requirements and administration of remote community stores

In 2007, as part of the Northern Territory Emergency Response, the Federal Government introduced

Community Stores Licensing. The scheme was renewed in July 2012 under the Stronger Futures in the

Northern Territory Act 2012. ALPA welcomed a set of requirements that would bring all stores up to a

minimum standard to improve food security across remote Northern Territory, a journey ALPA has been on

since 1972. While anecdotally store standards have improved since the licensing scheme has been in place, no

evaluation has quantified or validated this improvement.12 Considering the amount of money being spent of

this scheme, and the amount of data being collected from stores, this is a major weakness. External

evaluations should have been conducted and reported on regularly to assess food security improvements.

Having this evaluation process in place may have saved the resources being dedicated to this current inquiry.

To increase the awareness and understanding of compliance obligations, we engage a member of the NIAA

Community Stores team to deliver an overview of the scheme to new store managers during their induction.

We have facilitated NIAA store monitoring visits across the licensed stores we operate. If we receive a

monitoring report, we work to ensure recommendations are implemented. In our experience however, there

have been times when these reports are not been provided in a timely manner or they are not provided at all.

Monitoring visits have reduced in frequency since the transition of the risk-based model, with only 3 visits

occurring in ALPA-operated stores over the last two years. It is unclear if this is due to our stores being

considered “low risk” or whether the scheme is inadequately resourced to conduct the required number of

monitoring visits. We would suggest the latter given we have competitor stores who are clearly not operating

within the requirements and there has been no major change in their store conditions over the years. The

12

Australian National Audit Office. (2014 September 25). Food Security in Remote Indigenous Communities. Department

of the Prime Minister and Cabinet. https://www.anao.gov.au/work/performance-audit/food-security-remote-

indigenous-communities

15 | P a g e2014 Australian National Audit Office (ANAO) review into the licensing scheme confirmed this, finding stores

received fewer than required visits.13 NIAA have recently implied the lack of visits is due to COVID-19 travel

restrictions14 – this is a convenient excuse for a lack of commitment and resourcing to the scheme that was

present prior to these travel restrictions. Further to this, the lack of visits means store risk ratings are not being

updated. Across the sector, store manager movements are frequent, and store manager skill levels vary,

meaning the food security risk of a store can shift quickly. Given the lack of visits, NIAA are not identifying this

change in a timely manner.

The license requirements outline a range of food, drink and grocery items that must be available, reasonably

priced, safe and of sufficient quantity and quality to meet nutritional and related household needs. To assess

if products are reasonably priced, NIAA staff review the price and percentage mark up of certain products

against pricing policies agreed to, set or ratified by store directors. Using this information, NIAA should be able

to report to the Committee incidences and trends of unreasonable prices or price gouging across licensed

stores. There have been reports of independent stores implementing flexible pricing, whereby nothing is

priced in the store, and the price is decided at the checkout. We have been advised of stores who have

competition then the price increases when the other store closes, affecting the reputation of all remote

retailers.

Licensed stores are also required to hold a nutrition policy. NIAA do not stipulate what constitutes a nutrition

policy. And, to our knowledge, holding a “policy” is the only requirement. NIAA do not assess if the policy is

being implemented, or whether the policy is regularly updated with input from nutrition professionals. The

2019 MBS results reported an increase in the percentage of stores with a nutrition policy.15 NIAA have implied

this increase is linked with the licensing scheme,16 however given that 28 of the 33 stores who held a nutrition

policy in the 2019 report were operated by a stores group, the increase is likely due to the nutrition

commitment of stores groups like ALPA, OBS and Mai Wiru, all of whom hold nutrition policies. It should be

noted, some government-funded store groups do not invest in nutrition professionals to support the health

of the communities they service. Recommendation 6 in the 2009 inquiry encouraged the Australian

Government to work collaboratively with all remote Indigenous community store owners, operators and

communities to assist in the development and ongoing management of a healthy store policy. This

recommendation was not implemented. If it was to be implemented it requires a nutrition workforce with

healthy retailing expertise.

We recently collaborated with Monash University to investigate the capacity of the remote nutrition

workforce in NT and Qld to support stores to improve population diet. Preliminary findings reveal multiple

barriers prevent remote nutritionists from working effectively with stores. There is a limited workforce,

particularly in Qld. In both jurisdictions, priority is given to clinical dietetics. The existing workforce has

reported limited knowledge and limited access to training and resources to build capacity in this specialised

field of work. The government should increase the remote nutrition workforce, with priority given to public

health positions to achieve greater health gains.

13

Ibid.

14

National Indigenous Australians Agency. (2020 June). Inquiry into food pricing and food security in remote Indigenous

communities Submission 36. NIAA.

https://www.aph.gov.au/Parliamentary_Business/Committees/House/Indigenous_Affairs/Foodpricing/Submissions

15

Department of Health Strategy Policy and Planning. (2020 July 03). 2019 NT Market Basket Survey (19). Northern

Territory Government. https://hdl.handle.net/10137/8469

16

National Indigenous Australians Agency. (2020 June). Inquiry into food pricing and food security in remote Indigenous

communities Submission 36. NIAA.

https://www.aph.gov.au/Parliamentary_Business/Committees/House/Indigenous_Affairs/Foodpricing/Submissions

16 | P a g eALPA are ideally positioned to train this workforce to work with stores. Since the 1980s, ALPA have

implemented and updated the ALPA Health and Nutrition Policy. Our policy goes above the minimum stocking

requirements outlined by NIAA. Each month our store teams submit monthly nutrition checklists to ensure all

the ALPA nutrition policies, and by default, NIAA stocking requirements are in place. Through our benevolent

fund, we employ two full-time nutritionists to support the implementation of our policy at store level. They

also develop and run in-store initiatives and collaborate with health services and research institutions to

promote good nutrition and support store licensing compliance.

In December 2019 the ALPA Board of Directors passed 29 new nutrition policies that were informed by current

nutrition research and our sales data which highlighted opportunities to curb unhealthy food consumption.

These policies increased the availability of healthy options, with a notable inclusion being that all stores must

stock a fresh meat offer (when weather permits for wet season affected stores). Fresh meat is not commonly

available in other remote stores. Our merchandise team have worked hard with our meat suppliers and

transport companies to provide our customers with a fresh option.

Our new policies also focused on supporting customers to make healthy food and drink purchases and limit

unhealthy purchases through modifications to the store environment, and the way products are promoted.

We tested some of these bold nutrition policies through Healthy Stores 2020 (HS2020), a randomised

controlled trial co-designed by ALPA, Monash University, Menzies School of Health Research and others in

response to community leaders’ requests to curb sugar consumption. This groundbreaking study was

implemented over a 12-week period, across 20 ALPA stores – 10 stores receiving the HS2020 strategies, and

10 stores acting as a control. It resulted in a 2.8% (statistically significant) reduction in total free sugars sold,

which is equivalent to 1.8 tonnes less free sugars being purchased. A massive achievement - over 12 months

that equates to 7.2 tonnes less sugar going into 10 communities. Imagine the impact if it was implemented

across more stores! The biggest reductions came from strategies targeting confectionery (9.5% less sugar from

confectionery) and soft drinks (12.5% less sugar from targeted soft drinks). There were no adverse impacts on

business outcomes as purchases transferred to healthy foods or non-food lines. Customer acceptability was

high as it was driven by each participating store board. The study is currently in the process of being peer

reviewed for publication, please refer to Attachment A: Healthy Stores 2020 for further details.

Since the trial, we have successfully rolled out HS2020 to all ALPA operated stores. The unfortunate exception

to this is one strategy – the relocation of large volume (1.25L) soft drinks. This was unable to be implemented

in communities where we have a competitor store. All stores within the community must implement this

strategy to ensure it has impact and does not financially disadvantage the store wanting to support the health

of the community. An example of this is Galiwinku. We own two stores in Galiwinku, and due to the presence

of two privately owned stores, and one privately owned takeaway, we cannot relocate 1.25L soft drinks, at a

great disappointment to our Galiwinku board representatives. They have seen how successful the strategy is

in the other ALPA member stores and want to achieve the same results for their community.

With our collaborators, we have presented HS2020 to NIAA for consideration if/when changes are made to

the licensing scheme. We are aware changes have been made in the past, with the last one being in 2014 to

our knowledge. There is no structured process to review and update requirements in accordance with new

evidence to support health.17 With the expiry of SFNT in 2022, ALPA welcomes an evaluation of Community

17

Australian National Audit Office. (2014 September 25). Food Security in Remote Indigenous Communities.

Department of the Prime Minister and Cabinet. https://www.anao.gov.au/work/performance-audit/food-security-

remote-indigenous-communities

17 | P a g eYou can also read