Inflationary Thoughts, and What to Do as Things Unfold

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Inflationary Thoughts, and What to Do as Things Unfold Like many people (perhaps like you, dear reader), I’m a creature of habit. For example, when I buy something in a store I always ask for a receipt. Or I hit the button for a receipt if it’s one of those self-serve dispensers, like with fuel pumps at a gas station. Then I fold the receipt and drop it into the left pocket of my trousers. See? Habit. Later, I empty my pockets, take the receipts, and stuff them into an envelope on my desk. The idea is that I’ll sort them later for taxes. Except I hardly ever do that last part. Staying organized for taxes is not a habit, I guess. At any rate, this short, personal confession is my way of introducing a quick discussion about inflation, currently over 8.5% per no less than the U.S. Government. And it’s likely even more than that number because I believe that government bureaucrats badly misperceive and understate reality. So, here’s what happened. The other day I was cleaning my desk and found a stash of gasoline receipts from about a year ago. Back then it cost about $35 to $40 to fill the fuel tank of my car. Lately, though, it costs me about $70 to $75 to fill my gas tank. That’s about 80% more than a year ago. Same car. Same fuel tank. My driving habits are about the same. Same roads. Same trips to the store, errands, etc. Same everything, except that it costs me much more to fill the tank. There’s a reason for this, of course. A year ago, the price of

oil was nestled in the range of $65 per barrel. Today it’s north of $110. Do the math, right? The price of oil controls the price of motor fuel. Oil up, gasoline up; cause and effect. Meanwhile, rising prices for energy – oil, gasoline, diesel – explain a big whack of why the rate of inflation is high and increasing, not just at the fuel pumps but at the grocery store and pretty much everywhere else. Inflation is up because the global supply of energy is tight, which is certainly the case for oil, and also the scenario for much else in the arena of fuels. And energy demand is up due to a global recovery from Covid. More people want more and more energy. And due to the massive levels of government spending over the past couple years, there’s money out there to chase it. In other words, demand/people/money are chasing – or more precisely, “cornering” – a relatively static supply of oil, hence higher prices to clear the market. All this, while higher costs for energy flow through to everything. Higher energy costs affect what you pay to drive your car, and what it costs farmers and processors to produce food and other goods, and what it costs manufacturers and shippers to create and move everything, and eventually deliver it to stores where people buy it all. In this regard, inflation is now truly structural. That is, inflation is built into the entire economic system. It’s deeply rooted in the fundamentals of energy availability, and how much energy costs its end-users. Now, consider a follow-on point to what we just discussed. That is, absent a lot of additional energy miraculously

showing up and hitting the system (hint: very unlikely) the whole situation will remain bad, if not get worse. However bad you think it is now – high prices at the gas pump or supermarket – it’s about to hurt even more. There’s no relief in sight, unless you’re one of those well-insulated people who want to see a major global recession to, as the saying goes, “destroy demand.” The takeaway here is that inflation is structural. So stand by for more of it. Stand by for higher prices. Stand by for your dollars to buy less and less, while your quality of living declines. And okay, one more takeaway, with an upbeat angle. Looking ahead, hard assets – real things like metals and energy resources – will not only hold their value through the coming storm, but preserve and create wealth for the holders. On that last point, invest accordingly. That’s all for now… Thank you for subscribing and reading. Imperial Mining’s Quebec scandium play is aluminum’s best friend To me scandium sounds like it should be a country between Finland and Sweden in the Baltic Sea, but then again a lot of people have considered some of my thoughts pretty strange. However, scandium is becoming a critical metal of growing importance in aluminum alloys for auto, commercial aircraft, military armor and EV development, significantly reducing

weight and manufacturing costs. It’s used as a hardener and strengthener of common aluminum alloys, which are also heat and corrosion resistant. Its weight reduction applications in the automotive, aerospace, fuel cell and defense sectors in turn help reduce the overall carbon footprint by making aircraft and vehicles lighter and more fuel-efficient with lower emissions. Because of these tremendous applications, demand is expected to grow considerably from the current 35 tonnes per annum of product availability to western markets to as high as 2,000 tonnes by 2040. Source: Imperial Mining Group Corporate Presentation Obviously, I don’t need to comment on the importance of supply chains, “on-shoring”, etc. in light of what the world has seen over the last year or two. We’ll suffice it to say that domestic is better. Which leads us to today’s topic of conversation – Imperial Mining Group Ltd. (TSXV: IPG | OTCQB: IMPNF). Imperial is a Canadian mineral exploration and

development company focused on the advancement of its Crater Lake scandium-Rare Earth property led by an experienced team of mineral exploration and development professionals with a strong track record of mineral deposit discovery in numerous metal commodities. The Company also has a pair of gold prospects, Opawica and La Ronciere all in Quebec. However, what makes Crater Lake so special is that it is the only hardrock scandium deposit in the world and happens to be in the mining friendly jurisdiction of Quebec, close to hydroelectric capacity and Quebec’s aluminum metal production where 90% of Canada’s “Green” aluminum is produced. As well, it is looking like Bécancour in Quebec is becoming Canada’s battery cathode manufacturing hub with recent announcements from BASF regarding a cathode active materials and recycling site to support North American producers in their transition to e-mobility and General Motors and POSCO Chemical’s $400 million facility to produce cathode active materials for vehicle batteries. It would appear that Imperial could borrow a line from the real estate business and say their project is all about location, location, location.

Source: Imperial Mining Group March 15, 2022 Press Release It also doesn’t hurt that Crater Lake already has 43-101 compliant resource estimate. In September Imperial received the inaugural NI 43-101 Technical Report for the Crater Lake TG Zone Mineral Resource Estimate. Source: Imperial Mining Group Ltd. press release Sep 23, 2021 The results of the Resource Estimate for the Northern Lobe of

the TG Zone far exceeded the minimum threshold resource Imperial internally set for a 20-25-year notional mining operation, or 10 million tonnes. And the good news is mineralization remains open laterally and at depth, demonstrating the potential to increase the mineral resource with additional drilling. The Company has plenty of catalysts over the next several months to keep the news flow coming for investors. Work on a 43-101 Preliminary Economic Assessment (PEA) on the TG Zone scandium-rare earth zone resource is progressing and is expected to be completed in the next few weeks. A diamond drill program on the TG Zone (Northern Lobe and Southern Lobe) will commence in late June with up to 22 diamond drill holes for approximately 2,500 m. In addition, there is excellent potential to expand the mineral resources with further drilling on the Southern Lobe. In late Fall 2022, the new drill hole data from the summer program will be forwarded to a consultant to revise and update the previous 43-101 Resource Estimate of the TG Zone. This revised resource will allow Imperial to move forward with a Pre-Feasibility (PFS) or Feasibility (FS) Study. During Summer 2021, Imperial collected a 50-tonnes bulk sample for use in a pilot plant study. It is expected that the remaining 32-tonnes will be shipped to Sept-Iles, QC by the end of July 2022 to be used in a pilot plant study to further test and optimize Imperial’s patent-pending metallurgical process method. Additionally, Imperial has commissioned a hydrometallurgical flowsheet development program based on its patent pending two-stage hydrometallurgical method for the extraction of scandium and rare earth elements with SGS Canada. The program, which started on January 31, 2022, is partially financed from a $245,355 grant from the Quebec Ministry of Energy and Natural Resources with expected completion at the end of Q3 2022. Results from the work will aid in the engineering design of Imperial’s pilot program for

the Crater Lake project for later in 2022. As you can see, there is plenty on the go at Imperial Mining Group and the good news is they started May with C$2.8 M in working capital and virtually no debt. The Company currently has a market cap of C$14.7 million representing plenty of opportunities for a potential domestic supplier of an up and coming critical material. Jack Lifton, Byron W. King and Ur-Energy’s John Cash explore the future direction of the American uranium industry In this episode of Critical Materials Corner, Jack Lifton and Critical Materials Corner Co-Host & InvestorIntel Columnist Byron W. King speak with John Cash, CEO of Ur-Energy Inc. (NYSE American: URG | TSX: URE). John explains that Ur-Energy is today producing yellowcake, the commercial form of uranium, by the environmentally friendly method of “in-situ” mining, which he explains. Ur- Energy then processes the mine output to commercial yellowcake. John rounds out the discussion by defining the size of the American domestic market for uranium. He tells us where and in what form uranium for domestic American civilian use originates; what parts of the domestic American uranium supply

chain are deficient; and whether or not America can ever have a secure domestic supply of uranium for its largest in the world civilian nuclear electricity generation industry. This is a must-see video for all of those interested in green energy self-sufficiency for America. To access the complete episode of this Critical Materials Corner discussion, click here About Ur-Energy Inc. Ur-Energy is a uranium mining company operating the Lost Creek in-situ recovery uranium facility in south-central Wyoming. We have produced, packaged, and shipped approximately 2.6 million pounds U3O8 from Lost Creek since the commencement of operations. Ur-Energy now has all major permits and authorizations to begin construction at Shirley Basin, the Company’s second in situ recovery uranium facility in Wyoming and is in the process of obtaining remaining amendments to Lost Creek authorizations for expansion of Lost Creek. Ur‑Energy is engaged in uranium mining, recovery and processing activities, including the acquisition, exploration, development, and operation of uranium mineral properties in the United States. The primary trading market for Ur‑Energy’s common shares is on the NYSE American under the symbol “URG.” Ur‑Energy’s common shares also trade on the Toronto Stock Exchange under the symbol “URE.” Ur-Energy’s corporate office is located in Littleton, Colorado and its registered office is located in Ottawa, Ontario. To learn more about Ur-Energy Inc., click here Disclaimer: Ur-Energy Inc. is an advertorial member of InvestorIntel Corp. This interview, which was produced by InvestorIntel Corp., (IIC), does not contain, nor does it purport to contain, a summary of all the material information concerning the

“Company” being interviewed. IIC offers no representations or warranties that any of the information contained in this interview is accurate or complete. This presentation may contain “forward-looking statements” within the meaning of applicable Canadian securities legislation. Forward-looking statements are based on the opinions and assumptions of the management of the Company as of the date made. They are inherently susceptible to uncertainty and other factors that could cause actual events/results to differ materially from these forward-looking statements. Additional risks and uncertainties, including those that the Company does not know about now or that it currently deems immaterial, may also adversely affect the Company’s business or any investment therein. Any projections given are principally intended for use as objectives and are not intended, and should not be taken, as assurances that the projected results will be obtained by the Company. The assumptions used may not prove to be accurate and a potential decline in the Company’s financial condition or results of operations may negatively impact the value of its securities. Prospective investors are urged to review the Company’s profile on Sedar.com and to carry out independent investigations in order to determine their interest in investing in the Company. If you have any questions surrounding the content of this interview, please contact us at +1 416 792 8228 and/or email us direct at info@investorintel.com.

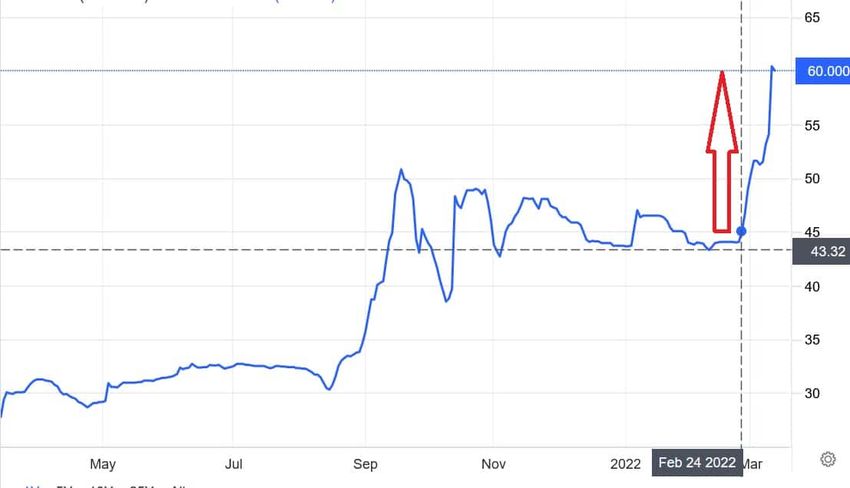

Ur-Energy, Hedging the uranium supply against the chaos of war The big question right now is what will Putin do next? Last week U.S President Biden banned Russian oil and gas imports. Will Russia respond by banning uranium exports to the USA? That would certainly cause a huge drama given that Russia largely controls the uranium market (41% of supply from Kazakhstan, 6% from Russia) and the USA’s dependence on uranium to power 19% of the electricity grid and a significant part of its navy which is nuclear powered. In anticipation of a possible Russian uranium export ban or supply shock, the uranium price has been moving higher since the war began. At the current uranium price of US$60/lb the outlook for uranium producers is looking dramatically improved. Uranium prices have spiked higher since the Russia-Ukraine war began on February 24, 2022

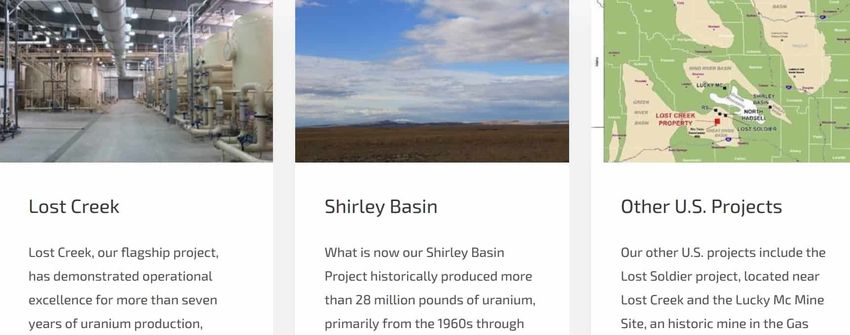

Source: Trading Economics Ur-Energy Inc. (NYSE American: URG | TSX: URE) is among the top two U.S uranium producers (when operational). Ur-Energy operates their flagship Lost Creek ‘in-situ recovery’ uranium mine and facility in south-central Wyoming, USA. The Lost Creek Mine and facility has been on care and maintenance awaiting higher uranium prices. Ur-Energy also owns several other projects including the Shirley Basin Project (construction ready), Lucky Mc Mine, and Last Soldier uranium projects in the USA as well as the Excel Gold Project in Nevada, USA. A summary of U-Energy’s uranium projects in the USA

Source: Ur-Energy website

The recent good news for Ur-Energy investors can be summed up

from the following two key announcements:

1. November 1, 2021 – Ur-Energy announces Lost Creek

development program to advance readiness to ramp up

uranium production. Ur-Energy stated: “We are pleased to

announce the commencement of a development program at

Lost Creek that will advance us from reduced operations

to full production-ready status…… As of October 27,

2021, we had more than $40 million in cash and 285,000

pounds of U.S. produced U 3 O 8 in inventory worth

approximately $13.4 million, stored at the conversion

facility.”

2. March 9, 2022 – “The economic analyses within the Lost

Creek report continue to support the potential viability

of the property. Total future life of mine (LoM)

production (without additional exploration) is modeled

to be 12.3 million pounds from 2022 to 2036 with LoM

operating costs estimated to be $16.34 per pound. All

in, the estimated total costs per pound, including

royalties and extraction taxes, is estimated at $33.61

per pound before income tax of $8.72 per pound. Pricing

used in the analysis ranged from $50.80 to $66.04 per

pound……The Property has a calculated before tax internalrate of return (IRR) of 72.2 percent and a before tax

net present value (NPV) of $210.9 million applying an 8%

discount rate. When income taxes are included in the

calculation, the after-tax IRR is 66.8 percent and the

after tax NPV is $156.8 million.”

Note: Bold emphasis by the author.

Lost Creek update

Minimal controlled production continued at Lost Creek

throughout 2021 in recognition of market conditions. Ur-Energy

has all required permits for operations within the first three

mine units at Lost Creek and expects to have the final permit

to allow operations within the HJ and KM Horizon at LC East

and additional mine units at Lost Creek this year. Ur-Energy

is in the process of obtaining remaining additional amendments

to Lost Creek authorizations for expansion of the Lost Creek

Mine.

Lost Creek recently received an amendment to its license

allowing expansion of mining activities within the existing

Lost Creek Project and the adjacent LC East Project. The

license now allows annual plant production of up to 2.2

million pounds U 3 O 8 , which includes wellfield of up to 1.2

million pounds U 3 O 8 and toll processing of up to 1 million

pounds U 3 O 8 . Additional approvals (as referenced above) for

this expansion are expected in H2 2021.

At the current uranium price of US$60/lb it looks highly

likely we will very soon hear an announcement of Lost Creek

production restarting.

Shirley Basin update

In addition to Lost Creek, Ur-Energy can bring on their

Shirley Basin Project. It has a before tax IRR of 105.6% and

NPV8% of $129.7 million. Ur-Energy has all major permits and

authorizations to begin construction at Shirley Basin, theCompany’s second in situ recovery uranium facility in Wyoming, USA. 2021 year end results Ur-Energy’s 2021 results are not important given that there was virtually zero (251 pounds of U3O8) uranium production and no sales. Ur-Energy reported: “As of December 31, 2021, we had cash resources consisting of cash and cash equivalents of $46.2 million. No sales of U 3 O 8 were necessary in 2021. The Company had a net loss of $22.9 million or $0.12 per common share.” Ur-Energy, new CEO, John Cash stated: “We are encouraged by the dramatic increase in domestic and global support for nuclear power, as it is increasingly recognized as the only plausible solution to climate change. Ur-Energy is in the enviable position of being able to quickly ramp up and participate in an improving uranium market and, in addition, we could immediately deliver up to 284,000 pounds U3O8 into the Uranium Reserve Program, currently being established by the U.S. Department of Energy. On March 3, 2022, we had $44.7 million in cash, plus our ready to sell U.S. produced inventory, worth approximately $14.4 million at recent spot prices. Additionally, we continue to advance the construction of header house 2‑4 to expedite production when market signals allow us to ramp up at Lost Creek.” Closing remarks Uncertainty of uranium supply from Russia and Russian controlled sources such as Kazakhstan is leading to a surge in uranium prices, up almost 50% in the past 3 weeks since the Russia-Ukraine war commenced. At current prices, Ur-Energy’s two key projects Lost Creek and Shirley Basin would be highly profitable as per recent economic studies done at uranium prices similar to today’s

price. All of this means it is highly likely we will soon see the resumption of uranium production by Ur-Energy at Lost Creek Mine in the near term. It also times well with the U.S.’s intentions to build up a reserve of uranium and the recent White House Fact Sheet aiming to build USA supply chains for key materials. For investors looking at a hedge against the war, then look no further than uranium. And if Putin bans exports of Russian controlled uranium to the USA and others, then expect to see uranium prices closer to US$100/lb, than to today’s price of US$60/lb. Ur-Energy trades on a market cap of US$380 million. Looks appealing. Looking Beyond USD for Gold Note from Peter Clausi: On June 24, 2019 I originally published this piece. Today, it is arguably even more relevant; and as such are re-publishing for your review. Gold is glittering again, having its strongest week since April, 2016. Many reasons are offered for this long-expected global run, including natural economic cycles, industry consolidation, the new-normal of rape talk in The White House, conflicts in the Middle East and trade uncertainties. Whatever the reasons, a higher gold price has a trickle-down impact on the junior exploration companies, the ones in the field doing the high-risk heavy lifting to bring new projects into development and production. It’s a well-known axiom to search for gold in the shadow of a headframe, which is why gold camps develop. You find gold near to where someone else

already found gold. Many of these gold camps were historically in production but became economically non-viable when the gold price fell below all-in sustaining costs. I remember attending the world’s greatest mining show, PDAC in Toronto, in 2001 when gold was under USD$300 an ounce – a very grim time to be in the mining industry! Mines and exploration projects were shuttered because the anticipated revenue from the deposits was less than the cost of running the mine, which left no cash for corporate operations, and that’s not a recipe for success. Those same projects will be back in play, likely in new hands if gold is able to sustain this run. PDAC 2012 was giddy as gold had hit its all-time high of USD$1,900 per ounce the previous August. Projects with iffy economics were being green-lighted to try to exploit that price. We all know how that ended. Gold is almost always quoted in USD. That’s the revenue number, the price at which the producer can sell the gold. What’s very interesting is that the majority of costs on a gold project are incurred in local currencies, not USD, so it’s important to track not only the USD sale price for gold but the movements of gold in the local currency. If the revenue number is up and gold is sold in USD, and the costs are held steady and incurred in local currencies, the opportunity exists for miners in those jurisdictions to increase their margins. What were barely viable projects can be made economically healthy due to exchange rates. This isn’t another trick of accounting from those ivory tower theorists under IFRS. This is the real world of real cash flow. Look at Australia. The Frasier Institute recently pronounced Western Australia to be the world’s second most attractive mining jurisdiction. Gold there is not flirting with a mere $1,400 an ounce. No, gold quoted in AUD hit an all-time high

of $2027 last week, and closed out the week above $2,000. (Thanks to goldbroker.com for the chart below.) This gives the Australian gold projects an advantage in attracting foreign investment capital. If costs are incurred in Australian dollars, and the inflation rate continues to be under 2%, the expanded gross margins will see Australian projects on a fast track. Previously worked mines that had to be shuttered due to the fall in gold will be re-opened. (Note this only speaks to gross margins. Australian mining companies have the stereotype for being lifestyle companies for their directors and management team, killing the net margins. The shareholders must ensure that new investment capital goes into the ground, not the Managing Director’s pocket.) Canada is in a similar position. Gold closed the week at CDN$1,852, and Canada had an inflation rate of 2.4% in April, 2019. Low inflation plus a rising revenue number equals renewed global interest in Canadian gold projects. Saskatchewan finished third globally in that same Frasier Institute report. Quebec, the Yukon, Northwest Territories

also made it into the Top 10 globally. Nunavut came in at 15, Ontario at 20. Of the fifteen provincial or territorial mining jurisdictions in Canada, six finished in the top 20 globally. That’s impressive, and that’s why that same report ranked Canada as the #1 mining jurisdiction on a national level beating out (who else) Australia. There’s more to gold than USD. Christopher Ecclestone analyzes the Impact of the Russian Invasion of Ukraine on the Global Resources Markets In a recent InvestorIntel interview, Tracy Weslosky spoke with Christopher Ecclestone, Principal and Mining Strategist at Hallgarten & Company about the impact of the Russian invasion of Ukraine on the resource market. In this InvestorIntel interview, which may also be viewed on YouTube (click here to subscribe to the InvestorIntel Channel), Christopher Ecclestone pointed out that Russia produces a lot of minerals and metals, but that it is a key producer of critical metals like nickel, cobalt, platinum and palladium. Explaining how Russia is currently being cut off from global markets, he went on to highlight the disruptions in platinum and palladium supply given that Russia is among the largest producers of those metals. Christopher went on to discuss the impact of the European conflict on the rare earths

sector and on the Canadian resource companies with Russian investment. To watch the full interview, click here. About Hallgarten & Company Hallgarten & Company was founded in 2003 by the former partners of a well-known economic think-tank. Their output encompasses top-down and bottom-up research from a Classical Economic (Austrian School) perspective. Over the years, the team has successfully picked trends using macroeconomic underpinnings to guide investors through the treacherous waters of the markets. It was only natural, in light of the focus of Classical Economics upon the “real value” of monetary assets that the firm’s strengths should ultimately have become evident in resources sectors and projections of commodity trends. Hallgarten & Company has advised and managed portfolios of offshore and onshore hedge funds. Hallgarten also provides consultancy services on Latin American economic, politics and corporate matters including the production of bespoke research. Hallgarten research is now available on Bloomberg and FactSet. To learn more about Hallgarten & Company, click here Gold market experts Jack

Lifton, Byron W King, Chris Thompson and John Kontak discuss the present and future gold market In this InvestorIntel Gold Panel discussion, InvestorIntel Editor-in-Chief & Publisher Jack Lifton and Geologist and Newsletter Writer Byron King are joined by Chris Thompson, President of eResearch Corp. and John Kontak, President and Director of West Red Lake Gold Mines Inc. (CSE: RLG | OTCQB: RLGMF) to discuss the present and future gold market. With the theme of the discussion around gold as a secure asset class, the panelists agree that the investment cycle may be setting up for “…a very good day for gold is in the near future.” To hear this InvestorIntel Gold Panel discussion, click here Leading rare earths junior Appia adds a new uranium claim block to their expanding asset portfolio Two of the best-performing commodities in the past year have been the key rare earth magnet material blend, neodymium, praseodymium (NdPr), and the energy metal, uranium. Today’s company has established itself as a leading rare earths junior

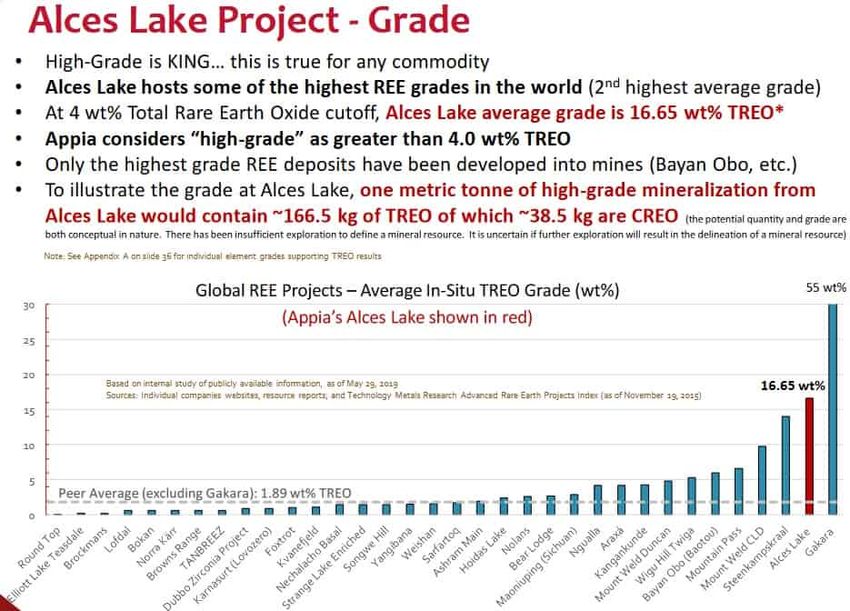

in Canada, but recently changed its name and expanded its uranium portfolio. This means investors get exposure to both the key magnet rare earths and also uranium. Even better, it controls 3 projects/properties. The Company is Appia Rare Earths & Uranium Corp. (CSE: API | OTCQB: APAAF) (Appia) formerly known as Appia Energy, with its Alces Lake rare earths project and its newly acquired uranium mineral claim block (Otherside), as well as other uranium properties located in Northern Saskatchewan, Canada, and its Elliot Lake uranium and rare earths property in Ontario, Canada. Appia’s very high-grade rare earths project at Alces Lake For background on Appia’s rare earths projects you can read some past articles here which focus on Appia’s tremendous asset at Alces Lake, Canada which has the 2nd highest average rare earth’s grade in the world, at 16.65 wt% TREO. High-grade zones are up to 49 wt% TREO. The rare earths are hosted in favorable ‘monazite’ ore at or near surface spread over 27sq km of tenements. There is a 23-25% Critical Rare Earth Oxide (CREO) component, including neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb). Appia’s 100% owned Alces Lake Project has the world’s second highest average grade of TREO

Source: Company presentation

Appia has access to use the Government funded Saskatchewan

Research Council (SRC) processing facility in Saskatoon,

Canada. Existing pilot facilities there(1,000 tpa capacity)

have already optimized a monazite processing flow sheet for

Appia. The SRC production-scale processing facility is

expected to be partially operational in early 2023.

Appia plans a smaller surface and near-surface operation to

start production with an open-pit scenario which is easier to

permit and manage and should have a low CapEx/Opex.

Appia’s latest results include:

Drill results at Wilson North (Alces Lake) with average

17.5 wt% TREO over 9.38 metres with up to 37.9 wt% TREO.

High grade REE mineralization identified over an

estimated 27 square kilometre area. Channel sample of14.71 wt % TREO from Sweet Chili Heat and 11.94 wt %

TREO from Diablo. 10.35 wt % TREO returned from grab

sample at Zesty. 7.86 wt % TREO returned from grab

sample along the Oldman River trend. New discovery of

REEs with 2.27 wt % TREO grab sample from “Train

Domain”. Elevated critical electronics metal, Gallium,

values have also been returned for all samples enriched

in TREO.

Promising Results from Initial Metallurgical Tests on a

Composite Sample from Alces Lake. Laboratory heavy

liquid separation tests recovered 95% of the total rare

earth oxide (TREO). Appia President Frederick Kozak

stated: “TREO recoveries and the percentage of TREO in

concentrate are comparable to other producing global

rare earths projects, supporting the potential for Alces

Lake as a future monazite rare earths supply.”

Appia is waiting on further drilling core and channel sample

assay results from the 2021 program. In terms of major near-

term catalysts, Appia states: “Analysis of 2021 drilling and

assays may lead to NI 43-101 report early 2022.”

Saskatchewan Uranium Properties

Appia recently announced that they significantly increased

their uranium claims by acquiring the Otherside claim block of

27,291 contiguous hectares. Appia states: “The claims were

staked on the basis of similar geological and geophysical

signatures to the Company’s Loranger property as well as other

known high-grade, large-tonnage uranium deposits in the

Athabasca Basin including Fission Uranium Corp’s Triple R

deposit, NexGen Energy’s Arrow deposits and others.”

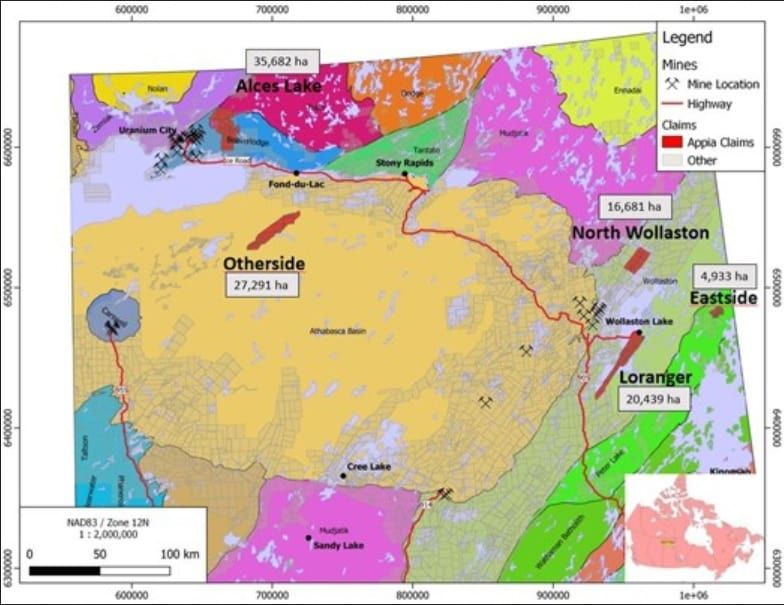

Appia now owns 4 uranium properties/claims over a total of

69,344 hectares – Loranger, North Wollaston, Eastside, and

Otherside. The properties are well located with proximity to

infrastructure such as roads, highway, powerline, an airstrip

as well as two uranium mills. The properties are ready toexplore, with at or near-surface high-grade uranium, no sandstone cover, and negligible overburden. Saskatchewan Uranium Properties – Loranger, North Wollaston, Eastside, and Otherside Source: Company news January 10, 2022 Appia stated on January 10, 2022 that the next steps are: “Appia has commenced the permitting process for a winter drilling program on the Loranger property and anticipates commencement of drilling in approximately one month, depending on weather and permits. The Company is fully funded for this program.” Elliot Lake (Ontario, Canada) Appia also has a 100% interest in 12,545 hectares (31,000

acres), with rare earth element and uranium deposits over five mineralized zones in the Elliot Lake Camp, Ontario. The Resource details are shown in the table below. Source: Company presentation Closing remarks Appia is becoming a significant rare earths and uranium junior. Appia now owns three very promising projects – Alces Lake (very high grade and critical rare earths), Saskatchewan Uranium Properties (Loranger, North Wollaston, Eastside, and Otherside), and Elliot Lake (rare earths & uranium). Appia trades on a market cap of C$54 million. Will Technology Metals’

Supply Meet the Demand for EVs? Since market economics’ common sense was codified by Adam Smith in the 18th century, people have been aware of the fact that the price for a good or service is what a willing buyer will pay a willing seller. Of course, the seller must be able to get the good or perform the service and the buyer must have or be able to get the money. These last requirements seem to have escaped the notice or understanding of the market manipulators also known as Western politicians. The global OEM transportation vehicle market is really not free. It is being politically manipulated by climate change politics, based on the belief that eliminating the carbon dioxide output from the use of fossil fuels in vehicle powertrains, based on internal combustion engines (ICEs) and replacing them with onboard stored electricity in batteries driving electric motors (BEVs) will have a significant “positive” effect for humans on the earth’s climate. Whether or not this cause-and-effect hypothesis is true the total conversion of the world’s transportation fleet to battery electric power is not possible for the size of the present fleet and its projected growth. This is because the (battery) technology metals necessary to effect this change simply do not exist in sufficient quantities that are accessible to mankind’s engineering abilities, willingness to deploy capital, and the real global energy economy. This supply limit will not become apparent until after 2025, so it is being ignored as a problem easily solved by the “efficient” market, whose actual strictures the political class does not understand. One clue about structural limitations, which politicians either do not understand or do not believe, is that the

current Western commodity price inflation is driven by efficient market supply shortages, which will automatically correct from infinite supply resources, not by free market excess (unsatisfiable) demand. Another, perhaps more insidious, supply limitation is simply the price ceiling, the maximum amount that the consumer can/will pay for a metal, before that metal becomes too expensive for the intended use. This is happening now, for aluminum, as soaring energy costs in Europe, for example, force the shutdown of aluminum electrolytic smelters, the production cost from which has become more than the market price of aluminum. This was caused by an entirely man-made shortage of electricity through sheer political short-sightedness, not by the aluminum marketplace. The politically driven demand pull for BEVs has already skewed the lithium market by driving lithium prices high enough to allow mines and sources, that would have been marginal or worse, to appear to be economical and to develop. But lithium prices are already too high for the continuing decline in battery costs to achieve par with fossil-fueled engines in the near term, if ever. The politicians’ answer to this is to restrict fossil fuel production and make it more costly. Thus a (n inflationary) price spiral has begun that could price BEVs as well as reduced production, thus more expensive, ICEs and their fossil fuels “out of the mass market!” The structural metals and materials used to make vehicles used for the transportation of people and freight can be, and mostly are, recycled. This is driven by the fact that it takes less energy to recycle structural metals than to produce new material from mines. A significantly large proportion of the iron, aluminum, copper, zinc, and lead used to construct new vehicles is recovered each year from the recycling of end-of- life scrapped vehicles. Cars in North America, have average useful lives of 12 -17 years. The North American car “fleet” is over 300 million vehicles and each year about 5% of the fleet is scrapped. This means that enough iron, copper,

aluminum, and lead is recycled each year to build 15 million new vehicles if 100% perfect recycling is assumed. It is noteworthy that the recycling efficiency of the American scrap, iron & steel, aluminum, copper and lead industries is very high and that most American steel for automotive use is made from scrap in, reliable, fossil or nuclear fueled (electrical) baseload requiring, electric arc furnaces. The North American OEM automotive industry considers 17 million vehicles produced and sold to represent a good year, so it does not have a problem sourcing structural metals for components. In fact, enough new vehicles are imported into North America that the need for structural metals for just domestic production by the OEM American automotive industry is met by just the metals produced from recycling. So far, so good. Now comes the not-so-good news about the technology metals required for manufacturing automobiles. Today’s internal combustion engine powered motor vehicles use, on average, about 0.5kg of rare earth permanent magnets (REPMs), so the annual need for such by the domestic OEM industry is between 6,000 and 8,500 tons of REPMs (here I assume that of the 17 million units sold each year up to 5 million are imports from another country (including Mexico and Canada besides China, Japan, Korea, Germany, France and the UK). And, a Tesla Model 3, electric vehicle (EV) with the range required by American buyers uses up to 5kg of REPMs, and 6-8 kg of lithium, measured as the metal, in its lithium-ion rechargeable battery-based powertrain. How many Gigawatt hours of lithium-ion battery storage for use in EVs and stationary storage can be produced with the earth’s known physically and economically accessible deposits of the necessary critical materials? I was going to submit that question as an abstract to a coming battery conference, but I realized that the academics and bureaucrats, and corporate

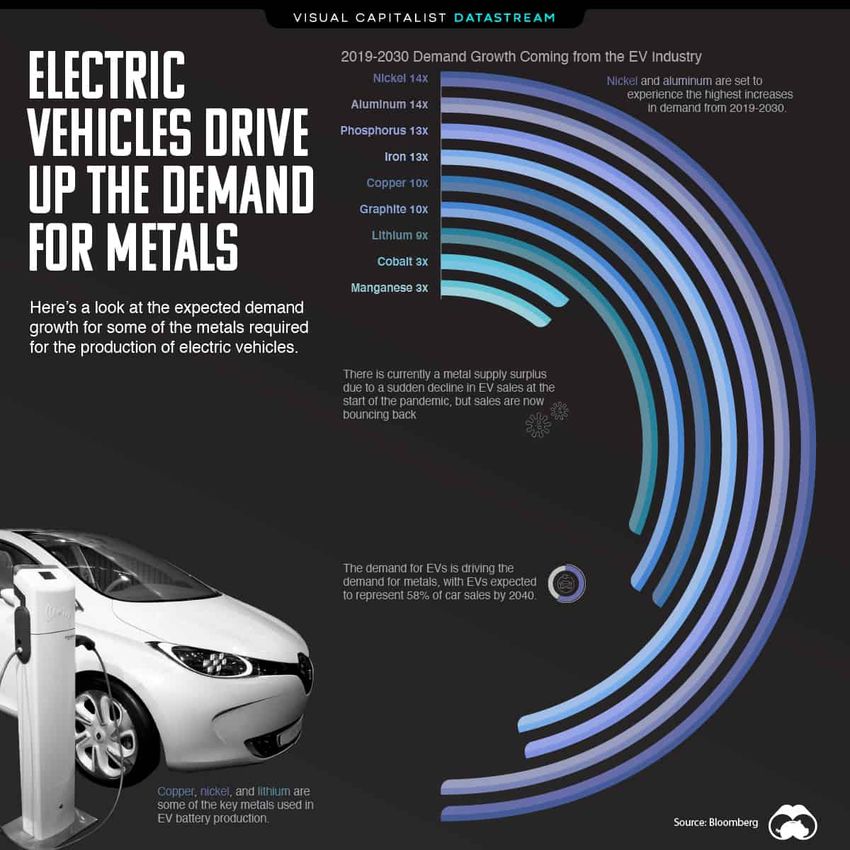

researchers who attend the conference don’t have enough background in industrial mineral economics to understand what I want to say, and, in any case, don’t want to hear it. Below is Bloomberg’s guesstimate of the demand growth for the supply of all of the metals necessary to build (projected levels of) EVs through 2030. It is very important to understand that the only increased demand for metals for building EVs that matters are for those metals that are non- structural, the EV Technology Metals. EVs will use no more of structural metals in the aggregate than ICEs do, so that as the ICEs are replaced by EVs, there will be no increased demand for iron, aluminum, or zinc, and a marked decline in the demand for lead as starter lead-acid batteries are phased out.

Source But those technology metals specifically required for an EV’s powertrain, the battery and the electric motors will see a dramatic increase in demand if and when EVs achieve a significant market penetration. For some reason, which I think is just ignorance, the major news media “predictors” pay no attention to the distinctions between the demand for structural metals, which will simply be the same total, with the exception of that for copper, as is used today unless the annual global total production of motor

vehicles increases dramatically, which is very unlikely. Mature Western (and Japanese and Korean) domestic markets will decline in demand as longer lived vehicles become necessities due to price. This may well have a negative effect on recycling efficiency for all metals as the scrap market re- adjusts to lower supply and lower annual demand for new vehicles. EVs, however, as they replace ICEs will not increase the demand for structural metals per unit, but it is the demand for EV technology metals that could skyrocket, if that much supply were possible. To reiterate: The above chart is wrong with regard to iron and aluminum demand for vehicles; they are a function of the total number of vehicles built in a year, and, since Western markets are mature in transportation vehicles, the demand for new iron and aluminum for that use is unlikely to increase more than 25%, if that, to add new vehicle production, perhaps mostly for the Indian and African home markets. For EV Technology Metals the story is very different. An EV uses about 50 kg of copper for its wiring harness, electric motor windings, and lithium-ion battery internal circuitry. This represents a 50% increase over the demand for copper in an average ICE, so that the demand for copper for EVs could add fifty percent to the overall demand for copper by the OEM automotive industry today if and only if ICEs are completely replaced by EVs. Thus, the factor for copper in the above chart, 10X, should be 1.5X. The potential demand growth for the most critical EV Technology Metal, lithium, is the limiting factor in the projected transformation of power trains from fossil fuels to battery moderated electricity. Today BEV sales are reported to be 3% of the global total vehicle sales. This is projected to reach 10% by 2025, so that by 2025 at least three times as much lithium will be needed to satisfy the demand for

batteries. In 2021 some 86,000 tons of lithium, measured as metal, were produced. 60% of that total was used to manufacture lithium- ion batteries. Let’s call that 50,000 tons for batteries in 2021.The 36,000 tons of lithium used for non-battery uses is unlikely to grow, so the necessary supply increase to satisfy the needs for producing 10% BEVs in 2025 is 3x, for a total demand in 2025 of 150,000 tons of lithium, measured as the metal. Adding the 36,000 tpa of lithium demand for other uses we get a total lithium demand of 186,000 tons for 2025, which is essentially 2X 2021 total demand for lithium. This is most likely do-able by the lithium mining industry, but the downstream supply chain to turn 150,000 tons of lithium into fine chemicals and battery electrodes does not now exist, and although capacity increases may be planned it cannot be determined how much will actually be constructed in time. This is determined by the availability of capital, its proper allocation, the availability of engineering skills, and the availability of construction capacity. Although these can be quantified, government interference, also known as regulation, is the single largest time, and frequently capital, consuming impediment to mining and process engineering in the West. The (mineral) economic illiterates who populate our universities and governmental bureaucracies live in a fantasy world of infinitely available natural resources and their unimpeded economic production. In that world, and only that world, is a green energy transition possible without an unacceptable decline in global standards of living, and the creation of a have and have-not society on a global scale. Let the UK’s current Production and processing of the EV Technology Metals are and will continue to be a good investment until a consensus is reached about a balanced energy economy, in which fossil fuels continue to be used for critical needs for which they are irreplaceable. Continued production of EV Technology Metals

after that will be determined by price. Critical Material Corner experts debate one of the most important minerals for sourcing rare earths In this episode of Critical Materials Corner, InvestorIntel Editor-in-Chief & Publisher Jack Lifton and Geologist and Newsletter Writer Byron King take on monazite — one of the most important and desirable mineral ores for sourcing rare earths. With guest Frederick Kozak, President of Appia Rare Earths & Uranium Corp. (CSE: API | OTCQB: APAAF), Byron King explains that while it is very rare to find a monazite deposit, “it is extremely rare to find a really really good monazite deposit…” “One of the hottest rare earth deposits you will ever see anywhere…” starts King, find out why Saskatchewan, Canada is critical to the production of rare earths in North America. To access the complete episode of Critical Materials Corner, click here

You can also read