INCENTIVES FOR ADDITIONAL CREDIT CLAIMS - 18 JUNE 2020 - European ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

INCENTIVES FOR ADDITIONAL CREDIT CLAIMS 18 JUNE 2020

ON TODAY’S CALL

MARCO ANGHEBEN

HEAD OF BUSINESS DEVELOPMENT AND REGULATORY AFFAIRS

+49 160 415 9944

marco.angheben@eurodw.eu

EIRINI KANONI

VICE PRESIDENT, BUSINESS DEVELOPMENT

+49 151 615 67595

eirini.kanoni@eurodw.eu

NICOLA MOSCAN

INTERN, BUSINESS DEVELOPMENT

+49 69 50986 9315

nicola.moscan@eurodw.eu

2

CONTENT

• ADDITIONAL CREDIT CLAIMS (ACC) REGULATORY ASPECTS

• OPERATIONAL ASPECTS FOR ACC

• ACC ELIGIBILITY CRITERIA

• DATA QUALITY VERIFICATION SERVICES FOR ACC

• Q&A

3

ADDITIONAL CREDIT CLAIMS REGULATORY ASPECTS MARCO ANGHEBEN

WHAT IS AN ADDITIONAL CREDIT CLAIM?

Credit claims - more commonly referred to as “bank loans” - represent a large share of the collateral

accepted by the Eurosystem:

• The Eurosystem accepts credit claims as collateral in its credit operations in several forms

• The term “credit claims” is defined in the EU’s Financial Collateral Directive as pecuniary claims arising

out of an agreement whereby a credit institution grants credit in the form of a loan

• The Eurosystem accepts several types of credit claims as collateral

Source: European Central Bank website

5

EUROSYSTEM ADDITIONAL CREDIT CLAIM FRAMEWORK (1)

Eligibility Criteria Non-marketable Assets

Type of asset Credit claims

Credit standards The debtor/guarantor must meet high credit standards. The

creditworthiness is assessed using Eurosystem credit assessment

framework (ECAF) rules for credit claims.

Handling procedures Eurosystem procedures

Type of debtor/guarantors • Public sector

• Non-financial corporations

• International and supranational institutions

Place of establishment of the Euro area

debtor or guarantor

Currency Euro

Minimum size Minimum size threshold at the time of submission of the credit claim

• for domestic use: choice of the NCB;

• for cross-border use: common threshold of € 500,000.

Cross-border use Yes

Source: European Central Bank website

6

EUROSYSTEM ADDITIONAL CREDIT CLAIM (ACC) FRAMEWORK (2)

Source: European Central Bank website

7

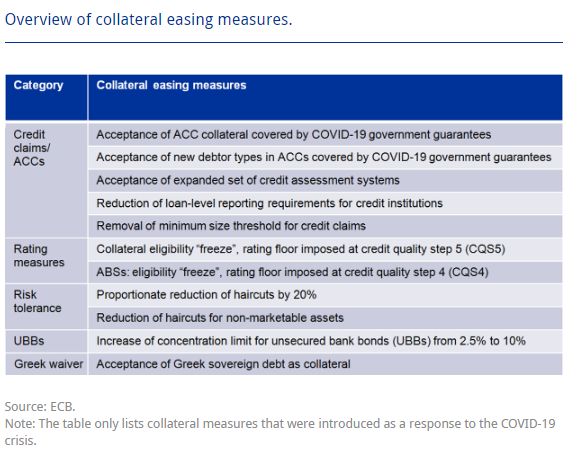

ECB PRESS RELEASE AS OF 7 APRIL 2020

The emergency collateral package contains three main features.

1. Governing Council (GC) decided on a set of collateral measures to

facilitate an increase in bank funding against loans to corporates and

households. GC decided to temporarily extend the additional credit

claims (ACC) frameworks further by:

o Accommodating the requirements on guarantees to include

government and public sector guaranteed loans to corporates,

SMEs and self-employed individuals and households

o Enlarging the scope of acceptable credit assessment systems used

in the ACC frameworks

o Reducing the ACC loan level reporting requirements

2. GC further adopted the following temporary measures:

o A lowering of the level of the non-uniform minimum size threshold

for domestic credit claims to EUR 0 from EUR 25,000 previously to

facilitate the mobilisation as collateral of loans from small

corporate entities;

o An increase in the maximum share of unsecured debt instruments

issued by any single other banking group in a credit institution’s

collateral pool.

o A waiver of the minimum credit quality requirement for marketable

debt instruments issued by the Hellenic Republic for acceptance as

collateral in Eurosystem credit operations.

3. GC decided to temporarily increase its risk tolerance level in credit

operations through a general reduction of collateral valuation haircuts

by a fixed factor of 20%.

Full release is available here.

8

COLLATERAL EASING MEASURES IN RESPONSE TO THE COVID-19 CRISIS

Loan level data reporting

frequency:

• Monthly to quarterly

Haircut levels:

• 20% reduction

As of June 2020

9

EXISTING ACC EUROSYSTEM TEMPLATES ACROSS ASSET CLASSES

ECB Loan Level ECB Loan Level

ECB Loan Level ECB Loan Level

Data - Reporting Data - Reporting

Data - Reporting Data - Reporting

Template Name Template for Template for

Template for Template for

Residential Consumer

SME ACCs Leasing ACCs

mortgage ACCs Finance ACCs

N° fields 118 159 205 71

N° of ND

allowed

18 39 22 20

mandatory

fields

Source: European DataWarehouse

10ASSET CLASSES FOR THE ADDITIONAL CREDIT CLAIMS

So far Bank of Italy has allowed three asset classes of loans to be part of an ACC portfolio, one new asset

class has just been added recently:

1. Residential Mortgages

2. Small and Medium Enterprises

3. Leases

4. Consumer loans [new asset class recently added]

More information can be found in the dedicated section of BI website

11NEW FRAMEWORK FOR GREEK ACC SME/CORPORATE PORTFOLIOS

Source: https://www.bankofgreece.gr/trapeza/nomiko-plaisio/keimena-nomothetikoy-xarakthra?topics=aa49dd6e-2904-4e5f-a59d-b2fdd533adc1

12FRAMEWORK FOR FRENCH ACC PORTFOLIOS

Source: https://www.banque-france.fr/politique-monetaire/cadre-operationnel-de-la-politique-monetaire/remise-dactifs-en-garantie-des-operations-de-refinancement-de-

leurosysteme/la-mobilisation-des-actifs-remis-en-garantie/mobilisation

13FRAMEWORK FOR PORTUGUESE ACC PORTFOLIOS

Source: https://www.bportugal.pt/page/ativos-de-garantia-pol-mon

14BANK OF ITALY PRESS RELEASE AS OF 9 JUNE 2020

The new Eurosystem measures are aimed at supporting the

credit supply to families and companies and create incentives for

Italian banks to access the Eurosystem liquidity.

Banks will be able to pledge the following as collateral for

Eurosystem’s operations:

• Homogeneous loan portfolios consisting of consumer credits

issued for families;

• Resindential mortgage loans within portfolios, regardless of

the debtor’s probability of default (the current 10% threshold

has been eliminated), whereas the current loan-to-value

(80%) has been increased to 100%.

The requirement that only performing loans can be pledged stays

in place.

Two new sources of creditworthiness evaluation have been

introduced:

• The performance component of the Bank of Italy’s internal

credit quality assessment system (ICAS), with evaluations

based exclusively on data from the risk management, to be

used for loans issued to small enterprises and pledged as

collateral within portfolios of corporate loans;

• A unique PD and LGD, calculated according to a conservative

approach, to be used for the evaluation of i) loans issued to

artisans and small family businesses, pledegd as collateral

within corporate loans portfolios; ii) loans pledged as

collateral within consumer credits portfolios.

These measures will be valid from the 17 June 2020 and will apply

until September 2021. The Eurosystem may extend these

temporary measures further in the future.

Source: https://www.bancaditalia.it/media/comunicati/documenti/2020-

01/CS_ulteriori_misure_ACC_202020609.pdf

15BANK OF ITALY ANALYSIS ON THE EUROSYSTEM’S EMERGENCY RESPONSE

TO COVID-19

Source: https://www.bancaditalia.it/media/notizie/2020/Nota-Covid-collaterale-10062020.pdf

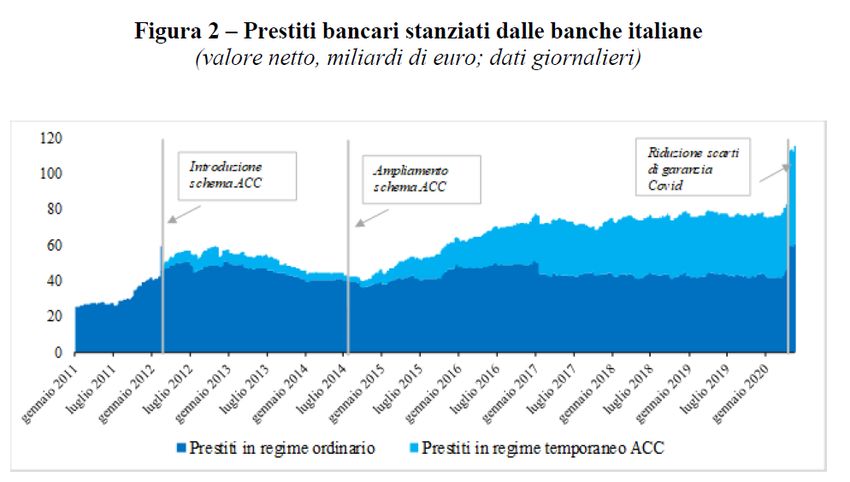

16EVOLUTION OF ACC PLEDGED IN ITALY OVER THE LAST 9 YEARS

17ESTIMATED INCREASE OF THE ECB AND BDI GUARANTEES AS OF JUNE 2020

18OPERATIONAL ASPECTS FOR ACC NICOLA MOSCAN

AVERAGE VALUATION HAIRCUTS APPLICABLE TO ELIGIBLE ASSET CATEGORIES

20BENEFITS OF ACC VERSUS ABS

ACC ABS

Legal requirements Country specific Country specific

Definition of default Common May vary

Rating No Rating required Rating required

Documentation Limited Heavy with offering docs, investor

reports etc.

ECB Templates Auto, RMB, SME, Consumer, Leasing Auto, RMBS, SME, Consumer, Leasing,

Credit Cards, DECC

Reporting Frequency Every three months Monthly, Quarterly

Legal Treatment of loans On-Balance Sheet Off-Balance Sheet

Pool size May vary for each reporting period Static or dynamic

Loan Credit Quality Performing loans only All loans

21ECB ABS & ACC ACCOUNT STATUS REPORTING

Examples of template differences between the ECB ABS and the corresponding ACC fields

ECB ECB Field

Field ECB ABS Field Description Code ECB ACC Field Description

Code

RMBS AR166 Current status of account: AR166 Current status of account:

Performing (1) Performing (1)

Arrears (2) Restructured - no arrears (2)

Default or Foreclosure (3) Arrears (3)

Redeemed (4) Performing but removed from pool by Counterparty (4)

Repurchased by Seller (5) Redeemed or Prepaid (5)

Other (6) Other (6)

No Data (ND)

SME NA NA AS72 Current status of account:

Performing (1)

Restructured - no arrears (2)

Arrears (3)

Performing but removed from pool by Counterparty (4)

Redeemed or Prepaid (5)

Other (6)

May use No Data options

Leasing AL122 Current status of account: AL122 Current status of account:

Performing (1) Performing (1)

Restructured - no arrears (2) Restructured - no arrears (2)

Restructured - arrears (3) Arrears (3)

Default or foreclosure (4) Performing but removed from pool by Counterparty (4)

Arrears (5) Redeemed or Prepaid (5)

Repurchased by Seller – breach of reps and Other (6)

warranties (6) All 'No Data' options ay be used in this field

Repurchased by Seller – restructure (7)

Repurchased by Seller – special servicing (8)

Redeemed (9)

Other (10)

All 'No Data' options may be used in this field

12ELIGIBILITY CRITERIA FOR ACC MARCO ANGHEBEN

CLARIFICATIONS ON THE NEW REPORTING FREQUENCY

Bank of Italy Answers

With the modififcation of the reporting frequency for LLD from monthly to quarterly, will it apply only for the new

ACC portfolios or will it be introduced for the already existing portfolios too?

• The reports’ quarterly frequency will be applied also for the already existing portfolios, whose cut-off dates are

fixed at the end of each quarter and the information duty needs to be fulfilled within a month from the cut-off

date.

Will the quarterly reporting frequency of LLD apply from the first upload for the ACC portfolios created after the

20 of April 2020?

• With regards to portfolios registered with EDW for the first time, the deadline for the quarterly reporting

requirement of LLD depends on the date when the portfolio will be registered at the Bank of Italy, and it

assumes that there would be three months of registration.

Will the first European DataWarehouse report need to be fulfilled within the end of July 2020 (end of October

2020 for the second report) for a new portflio created on the 23 of April 2020?

• Therefore, with respect to the loans confered for the first time in April, the EDW reporting requirement (with

cut-off date 30 June 2020) needs to be fulfilled within the 31 of July 2020; similarly, for thte loans confered for

the first time in May, the reporting requirement (with cut-off date 31 July 2020) needs to be fulfilled within the

31 of August 2020; after that, the cut-off dates are fixed at the end of each quarter and the reporting

requirement has to be actualized within a month from the cut-off date.

Source: Banca d’Italia

24LLD REPORTING DEADLINES FOR ACC PORTFOLIOS

Example from Bank of Italy ACC reporting frequency requirements

First month Deadline for first Deadline for second Deadline for third

First reporting Second reporting Third reporting

delivering the pool reporting reporting reporting

cut-off date cut-off date cut-off date

to Banca d'Italia submission submission submission

Apr-2020 30 June 2020 31 July 2020 30 September 2020 31 October 2020 31 December 2020 31 January 2021

May-2020 31 July 2020 31 August 2020 30 September 2020 31 October 2020 31 December 2020 31 January 2021

Jun-2020 31 August 2020 30 September 2020 30 September 2020 31 October 2020 31 December 2020 31 January 2021

Jul-2020 30 September 2020 31 October 2020 31 December 2020 31 January 2021 31 March 2021 30 April 2021

Aug-2020 31 October 2020 30 November 2020 31 December 2020 31 January 2021 31 March 2021 30 April 2021

Sep-2020 30 November 2020 31 December 2020 31 December 2020 31 January 2021 31 March 2021 30 April 2021

Oct-2020 31 December 2020 31 January 2021 31 March 2021 30 April 2021 30 June 2021 31 July 2021

Nov-2020 31 January 2021 28 February 2021 31 March 2021 30 April 2021 30 June 2021 31 July 2021

Dec-2020 28 February 2021 31 March 2021 31 March 2021 30 April 2021 30 June 2021 31 July 2021

Jan-2021 31 March 2021 30 April 2021 30 June 2021 31 July 2021 30 September 2021 31 October 2021

Feb-2021 30 April 2021 31 maggio 2021 30 June 2021 31 July 2021 30 September 2021 31 October 2021

Mar-2021 31 maggio 2021 30 June 2021 30 June 2021 31 July 2021 30 September 2021 31 October 2021

Source: Banca d’Italia

25‘COVID-19’ CREDIT ELIGIBILITY

The Bank of Italy accept, as collateral for its financing operations, loans indicated in the Law Decree n.

23/2020 of 8 April 2020 called Decreto Liquidità:

• State-guaranteed loans granted to Families and Corporates

Families

Corporates

Sottogruppo

attivitá economica

SAE 400 and 499

(SAE) 614 and 615

Pool of Credits

26HAIRCUT CALCULATION

The Bank of Italy will apply specific haircuts as a function of the best credit worthiness between the

debtor and the guarantor.

The best rating attributed to Italy will be assigned to the guarantor, hence corresponding to the third

Credit Quality Step (CQS).

Source: Trading Economics as of 2020

• Loan with ‘COVID’ guarantee issued to debtor with PD < Country PD

The haircut is calculated on the basis of the debtor’s rating, regardless of the collateral’s percentage

coverage

• Loan with ‘COVID’ guarantee issued to debtor with PD > Country PD

Loan calculated on the basis of Italy’s rating for the quote covered by the collateral, while the debtor’s

rating is used for the quote not covered by the State guarantee

In case the debtor did not have a rating or had one beyond the regulatory threshold (PD > 10%), the

haircut applied to the non-guaranteed quote would be equal to 100%.

27PRACTICAL EXAMPLES OF THE HAIRCUT CALCULATIONS

Based on a guaranteed «COVID-19» loan amount of €100.000

Debtor’s PD = 0,05% Debtor’s PD = 4% Debtor’s PD = 11%

Collateral coverage = 80% Collateral coverage = 80% Collateral coverage = 80%

Haircut calculated over Haircut calculated over Corporates

Haircut calculated over

€100.000 as a function of €80.000 as a function of €80.000 as a function of

the debtor’s PD the State’s PD

SAE 400 and the

499State’s PD

Haircut calculated over 100% Haircut on the

€ 20.000 as a function of remaining € 20.000

the debtor’s PD

Source: Pegaso2000 and European DataWarehouse calculations

28DATA QUALITY VERIFICATION SERVICES FOR ACC PORTFOLIOS EIRINI KANONI

DATA QUALITY CONTROLS ON ACC PORTFOLIOS WITH EDITOR

The ED data quality verification services aim at signalling potential inconsistencies and the lack of data (No

Data), within the ACC portfolios, before the data is published and made available to the Eurosystem

The data quality checks available in EDitor for residential and SME/corporate portfolios operates in three

separate steps:

1. Upload of the Loan-Level Data (LLD) file in EDitor

2. Automatic validation checks are run on the data and errors and potential inconsistencies are identified

3. Publication of the LLD file with the Eurosystem

The pre-screening tool verifies the information uploaded in the private area:

• Avoiding subsequent LLD corrections and

• Decreasing the risk of sanctions for lack of data or inconsistencies reported in the LLD file

30EDITOR FUNCTIONALITY FOR ACC (I)

• Data completeness score

based on the ECB matrix

• Data quality checks on ACC

portfolios:

• 300+ validation rules for

ACC residential

• 150+ validation rules for

ACC SME

• Rules for ACC consumer

and leasing portfolios

may be developed in the

future

31EDITOR FUNCTIONALITY FOR ACC (II)

• Data quality checks on the

portfolios and correction

of inconsistencies

• Potential inclusion of

further loans in the ACC

portfolios

32EDITOR FUNCTIONALITY FOR ACC (III)

• The graph shows the

types of checks

available in EDitor

• Data quality checks are

divided in seven

different categories:

• No Data (ND) checks

• inter-submission

inconsistencies

• duplicate entries

• negative values

• interfiled

inconsistency

• unusual entries

• format checks

33IDENTIFICATION OF POTENTIAL INCONSISTENCIES IN THE LLD FILE

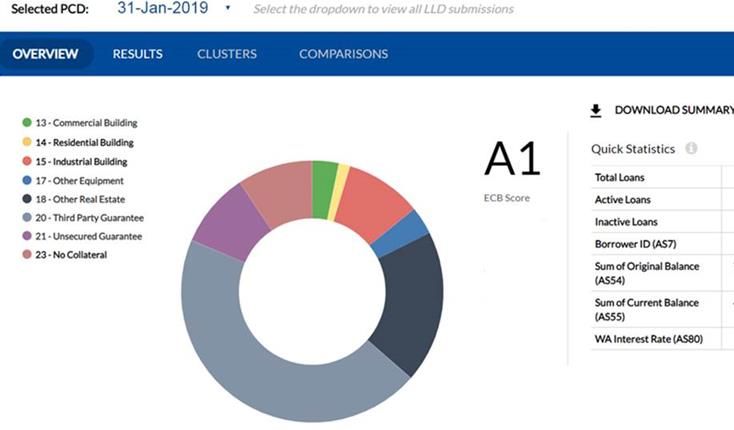

By clicking on “Manage Submissions” and then “Results”, it is possible to view the potential inconsistencies within

the uploaded but not yet published portfolio. If you click on the download symbol , EDITOR shows the details

of the potential inconsistencies that have been indicated.

34DETAILS OF CHECKID AR26/CCR_ND5/A/01

Examples of the details available in EDITOR – CheckID AR26/CCR_ND5/A/01

a) File generated by the EDitor system

b) Loan details

35INCONCISTENCIES RESOLUTION

The details displayed in EDITOR allow for a rapid resolution of the inconsistencies and further inconsistency checks

through an additional upload

36STEPS FOR REGISTERING ACC PORTFOLIOS IN EUROPEAN DATAWAREHOUSE

Signature on the European DataWarehouse Customer Agreement

First Step

Registration of Organisation and Users on My ED Account

Second Step

Creation of ACC portfolio in EDitor with specific ED Code identifier

Third Step

Upload of ECB Loan-Level Data files in EDitor

Fourth Step

Fifth Step

Potential Data Quality Checks on the portfolio/s (RMB & SME)

(optional)

37Q&A

38THANK YOU//CONTACT US

EUROPEAN DATAWAREHOUSE GMBH

Walther-von-Cronberg-Platz 2

60594 Frankfurt am Main

www.eurodw.eu

enquiries@eurodw.eu

+49 (0) 69 50986 9017

39You can also read