IMAGE HERE Immigration Looking back, looking forwards - Motu Economic and Public Policy Research

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

IMAGE HERE

Immigration

Looking back, looking forwards

Motu Public Policy Seminar

Philip Stevens and Ganesh Nana

New Zealand Productivity Commission

Terms of reference

• Review immigration settings for the ‘long-term prosperity and

wellbeing’ of New Zealanders:

– System-wide view, not sector-specific

– ‘Working age’ (ie, not refugees, tourism).

• Think about ‘prosperity and wellbeing’ broadly – four capitals,

productivity, resilience, distribution, Treaty impacts and

implications.

2

Overview: A tale of two reports

Part I: Part II: Inquiry report

Immigration by the numbers Immigration – Fit for the future

PART I

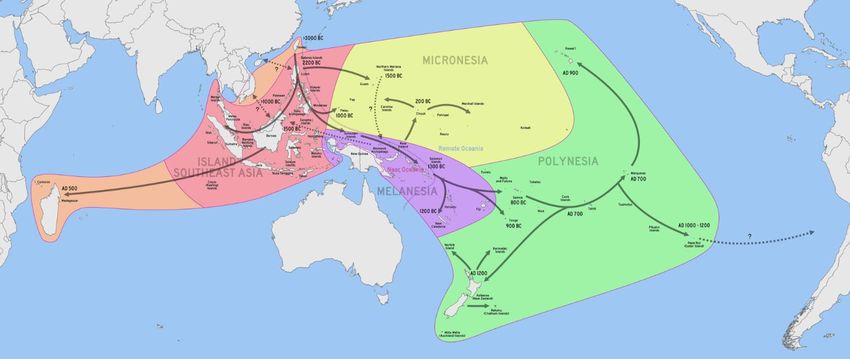

The first migration to Aotearoa New Zealand

Migration, post Tiriti

The arrival of Europeans in Aotearoa New Zealand

Comparison of the Māori and non-Māori populations post-Te Tiriti, 1841–1911

Sources of migrants to New Zealand, 1871–92

6

Migration has re-emerged as a driver

of population growth

100 Covid-19

Australian mining

80 employment

Population change (thousands)

boom peaks

Oil shocks and

stagflation GFC

60

The Long Depression

The Great Depression

40

20

0

-20

The wool shock Asian financial

Economic crisis

-40 restructuring

1860 1880 1900 1920 1940 1960 1980 2000 2020

Natural increase Net migration Population growth 7

Both immigration and emigration

have risen

150

100

Migration (thousands)

50

0

-50

-100

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2018

Arrivals Departures Net migration

Figure | Migration as a share of the New Zealand population

Percentage of population living abroad

0%

10%

15%

20%

25%

5%

Lithuania 30%

Portugal

Latvia

New Zealand

Estonia

Ireland

Luxembourg

Poland

Iceland

Greece

Mexico

Switzerland

Slovakia

United Kingdom

Austria

Figure | Selected countries' diaspora, percentage of the resident population

Netherlands

Finland

Italy

Germany

Denmark

New Zealand has a large diaspora

France

Canada

Sweden

Australia

South Africa

1990

India

United States

2020

China

Japan

Belgium

50

The relative performance of the Australian and New Zealand

Real GDP per capita in 2011 US$ (thousands)

Migration from 45 economies, 1870–2018

Real GDP per capita since 1870, 2011 US$ (thousands)

New Zealand to 40

35

Australia increased

30

when the relative

25

performance of the 20

Australian and NZ 15

economies diverged in 10

the early 1970s. 5

0

1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Australia New Zealand

600

Stock of trans-Tasman migrants, 1881–2018

500

Migrants (thousands)

400

300

200

100

0

1954

1981

1881

1891

1901

1911

1921

1933

1947

1961

1966

1971

1976

1986

1991

1996

2001

2006

2013

2018

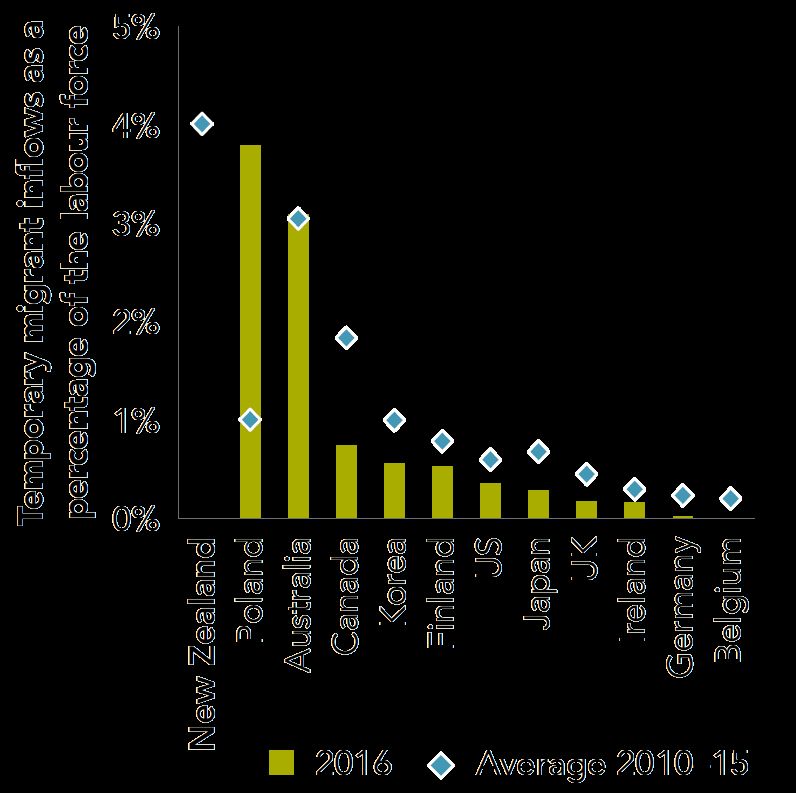

New Zealand-born in Australia Australian-born in New ZealandNew Zealand has high temporary Growth in new arrivals is mostly from

migration by international standards temporary migrants

11Labour shortages and net migration

25% 75

Businesses reporting labour shortages

Net migration (thousands)

20% 60

15% 45

10% 30

5% 15

0% 0

-5% 1990 1995 2000 2005 2010 2015 2020 -15

Labour shortage (left scale) Net migration (right scale)

Source: Quarterly Survey of Business Opinion and Stats NZ.

Figure | What single factor, if any, is most limiting your ability to increase turnover? LabourMigration accompanies job growth

100 25%

Net job creation, net migration (thousands)

Unemployment, economic inactivity (%)

80 20%

60 15%

40 10%

20 5%

0 0%

-20 -5%

-40 -10%

-60 -15%

1995 2000 2005 2010 2015 2020

Net annual jobs creation (left scale) Net migration (left scale)

Unemployment rate (right scale) Economically inactive (right scale)

Source: NZPC calculations based on SNZ Household Labour Force Survey (HLFS)., Linked Employer-Employee Data (LEED) and population data.

Figure | Net job creation and migration, unemployment and inactivity, 1995-2021Who are the migrants?

Migrants are more highly qualified than NZ-born

Migrants come from a wide range of countries Migrants are younger than NZ-born

14Immigration and industry productivity

250%

Finance insurance Chemical, rubber, non-

Figure | Industry intensity of migrant labour, labour productivity and total employment

and superannuation metallic manufacturing

200%

Standardised labour productivity (VA/FTE)

Dairy cattle

farming

Food, beverage, Telecommunication,

Wholesale trade internet, and library

tobacco

150% manufacturing services

Sheep, beef cattle,

and grain farming

Forestry and Professional,

scientific, and

100% logging

tech services

Horticulture and

fruit growing

Building construction

50%

Accommodation

Construction and food services

services

Textile, cloth, footwear Administrative and

manufacturing support services

0%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Percentage of migrant labour

Primary sector Manufacturing, utilities and construction Trade, logistics and hospitalities Other servicesEconometric analysis • Skilled and long-term migrants make contributions to output that exceed moderately-skilled NZ-born workers. • That higher contribution is likely due to a mix of skill differences and/or effort that is largely reflected in higher wages. • Migrants that are not on skilled visas are associated with lower output and lower wages than moderately-skilled NZ-born. • The share of employment for long-term migrants has grown over time (from 2005 to 2019). • Their relative contribution to output appears to be increasing over the same period. • Tentative evidence that high-skilled NZ-born workers make a stronger contribution to output when they work in firms with higher migrant shares, which is suggestive of complementarities between the two groups or, at least, positive mutual sorting of these groups into higher productivity firms.

Immigration and capital

600

Employment, Migrant population, Capital/Labour

500

400

(1960=100)

300

200

100

1960 1970 1980 1990 2000 2010 2019

Total Employment Capital stock Capital/Labour Migrant population

Source: University of Groningen and University of California, Davis.

Figure | Employment, capital and migrants (1960=100), 1960-2019

17House prices were rising long before net migration

rose, and continued to rise after net migration fell

30 600

Natural increase, Net migration (thousands)

25 500

House Price Index

20 400

15 300

10 200

5 100

0 0

-5 -100

1990 1995 2000 2005 2010 2015 2020

Natural increase (left scale) Net migration (left scale)

RBNZ real House Price Index (right scale)

Source: NZPC calculations using SNZ and RBNZ data.

Figure | Real house prices, population growth 1990-2021

18PART II

Inquiry reports

• Immigration – Fit for the future

• Immigration by the numbers

Supporting work:

• Devine (forthcoming) Migrant selection and outcomes

• Fabling et al. (2022) Migration and productivity

• Fry & Wilson (2022) Planning for prosperity: Transparent and public immigration

settings

• Knopf (2022) Case study: Aged care

• Maré et al (forthcoming) Missing migrants: border closures as a labour supply shock

• NZPC (2021) Supplementary series of six papers

• Schiff (2022) Case study: Construction

• Taylor Fry (2022) Data-led approach to identifying skills shortages

• Whāia Legal (2021) Advice on immigration policy and Te Tiriti o WaitangiIn aggregate immigration has a small positive

effect on productivity and wages in NZ

• Consistent with overseas studies

• GDP growth in NZ has relied on adding more people to the labour force –

both locals and migrants work longer hours compared with OECD

• Productivity is a long game

– Needs sustained investments in physical and community infrastructure, education and

training, workforce development, innovation and supportive regulation.

• Relationship between productivity and immigration

– a balance of trade-offs

– a consideration of short-run and long-run impacts.

• Immigration is not the solution to 21st century productivity challenges, nor

is it the cause of our productivity problemsMigrants make an important

contribution to the economy

• Immigration has more than offset the loss of skilled New Zealanders.

• Immigration has reduced the risk of labour shortages across the

economy – notably in aged care, dairy, IT and hospitality.

• Apart from the GFC, net migration moved in line with net job creation.

90

60

Thousands

30

0

-30

22

-60

2000 2003 2006 2009 2012 2015 2018 2021

Net jobs creation Net migrationNo evidence of systemic labour

displacement from migration

• On average, small positive effects on wages and employment of NZ-born

workers over the last 20 years.

• However, immigration can be negative for certain populations.

– Negative impacts concentrated on people with low levels of skills,

education, and experience, young, including young Māori, Pasifika and

beneficiaries.

– Cost can be very high, felt by individual, whānau and community. It can also

persist (scarring).

• Even these negative impacts are not systematic.

- Occur in particular places at particular times. Same group can experience

positive impacts at different times.

• Pockets of displacement should be targeted with education, training and

empowering active labour market policy.System becomes increasingly unbalanced

• After the GFC, the Government

stimulated economic growth

40

– working holiday visas

– new visa categories

30

– promotion of temporary visas.

Thousands

20

• Led to an unbalanced system

– many temporary workers expecting a

10

pathway to residency

– but no changes to the residency selection

0

criteria 2004 2007 2010 2013 2016 2019 2021

– combined with low rates of emigration to Resident visa Temporary work visa

create…

• High rates of population growth, putting

additional pressure on some aspects of

absorptive capacity 25Migration policy needs to consider

absorptive capacity

• In the short run there are trade-offs.

– The way immigration policy is currently developed risks congestion. Pressure hits if

migration is unbalanced or if not met with investment.

• But in the long run absorptive capacity is not fixed.

– While arriving migrants create demand-side pressure that dominates the supply-side,

over time they become net contributors to the community and the economy’s

productive capacity.

• Rather than limiting migration to manage infrastructure pressures, it

would be better to deal with the root causes.

– Infrastructure Commission research finds that infrastructure is less responsive to

population growth now than in the past.

– Infrastructure is more expensive to build, benchmarking with other countries.Long-term win: Better labour market

information and monitoring

• Improve information around labour shortages

– vacancy indicators of skill shortsage into BOS

– wage pressure information

• Increase informaton and understanding of skills needs and

use of skills

– update ANZSCO/move to ONet

– add citizenship and long term resident informaiton data to IDI

29Long-term win: an immigration

Government Policy Statement (GPS)

• Reflect Te Tiriti o Waitangi in

immigration policy

• Clarify immigration policy objectives

and connections to other government

Investing in absorptive

objectives including capacity to align with

expected population growth

- Education and training policy

- Investments in absorptive capacity GDP growth driven by Clear prospects for

population increases residency to attract

• Set relative priorities balancing the global talent

short- and long-term goals: Uncertainty around

residency prospects Adopting new business

- Explaining how the demand for temporary and models, processes and

residence visas will be managed technologies

Business growth relies

- Supporting infrastructure planning and on more labour

investment, and education, training and labour Investing in capabilities

of New Zealanders

market policies by projecting future migration Filling labour shortages

rates and composition with temporary migrants

• Engage with Māori, communities, and

businesses by compiling data and

performance indicators regularlyThank you

Visit our website to find out more and to subscribe to updates:

www.productivity.govt.nzYou can also read